coffee economic viability study

TRANSCRIPT

Coffee Economic Viability Study

Authored on Behalf of the Kenya Coffee Platform through research by Coffee Management

Services.

1

ABBREVIATIONS

AFA - Agriculture and Food Authority

AFCA - Africa Fine Coffee Association

BBC - Bacterial Blight of Coffee

CBD - Coffee Berry Disease

CLR - Coffee Leaf Rust

CMS - Coffee Management Services Ltd

COP - Colombian Pesos

CRI - Coffee Research Institute.

ERP - Enterprise Resource Planning

FCS - Farmer Cooperative Society (ies)

GAPs - Good Agricultural Practices

GCP - Global Coffee Platform

GHG - Green House Gas

ILO - International Labour Organization

NCE - Nairobi Coffee Exchange

OT - Outturn

PCRs - Producer Crop Returns

SAI - Social Accountability International

2

Table of Figures

FIGURE 1: NATIONAL PRODUCTION DISTRIBUTION OVERVIEW ................................................................... 7

FIGURE 2: COFFEE GROWERS SAMPLED IN EACH COUNTY ......................................................................... 8

FIGURE 3: STAKE HOLDERS CONSULTATIVE FORUM ................................................................................. 15

FIGURE 4: NATIONAL PRODUCTION DISTRIBUTION OVERVIEW ................................................................. 28

FIGURE 5: COFFEE GROWERS SAMPLED IN EACH COUNTY ....................................................................... 30

FIGURE 6: MAP OF COFFEE GROWING AREAS IN KENYA .......................................................................... 31

FIGURE 7: AGE DISTRIBUTION OF COFFEE GROWERS SURVEYED BY PERCENTAGE ................................. 34

FIGURE 8: AVERAGE AGE BY COUNTY ....................................................................................................... 36

FIGURE 9: GENDER OF COFFEE GROWERS WHO PARTICIPATED IN THE STUDY ........................................ 37

FIGURE 10: GENDER DISTRIBUTION ACROSS DIFFERENT FARMER ARCHETYPES ...................................... 38

FIGURE 11: EDUCATION LEVELS OF THE COFFEE GROWERS INTERVIEWED ............................................. 39

FIGURE 12: ESTATE PRODUCTION WEIGHT PER TREE ................................................................................ 39

FIGURE 13: SMALLHOLDER PRODUCTION WEIGHT PER TREE .................................................................... 41

FIGURE 14: ESTATE FARMERS PRODUCTION COST PER KILO` ................................................................... 41

FIGURE 15: SMALLHOLDER FARMERS PRODUCTION COST PER TREE ........................................................ 43

FIGURE 16: REVENUE DISTRIBUTION IN KENYA SHILLINGS PER KILO OF CHERRY .................................. 44

FIGURE 17: BREAKEVEN POINT FOR ESTATE FARMERS ............................................................................. 46

FIGURE 18: BREAKEVEN POINT FOR SMALLHOLDER FARMERS ................................................................. 46

FIGURE 19: ECONOMIC VIABILITY POINT FOR ESTATE FARMERS .............................................................. 47

FIGURE 20: DISTRIBUTION OF ECONOMIC VIABILITY FOR ESTATE FARMERS BY PRODUCTION LEVELS . 48

FIGURE 21: ECONOMIC VIABILITY POINT FOR SMALLHOLDER FARMERS .................................................. 48

FIGURE 22: DISTRIBUTION OF ECONOMIC VIABILITY FOR SMALLHOLDER FARMERS BY PRODUCTION

LEVELS ........................................................................................................................................................ 49

FIGURE 23: NUMBER OF WET MILLS INTERVIEWED PER COUNTY ............................................................ 49

FIGURE 24: AVERAGE REGISTERED MEMBERS BY COUNTY ...................................................................... 50

FIGURE 25: ACTIVE MEMBER VS. REGISTERED MEMBERS BY COUNTY .................................................... 52

FIGURE 26: GENDER OF WET MILL MEMBERS ........................................................................................... 53

FIGURE 27: DISTRIBUTION OF REVENUE RETENTION RATE ....................................................................... 54

FIGURE 28: PAY-OUT RATE ACROSS WET MILLS ....................................................................................... 55

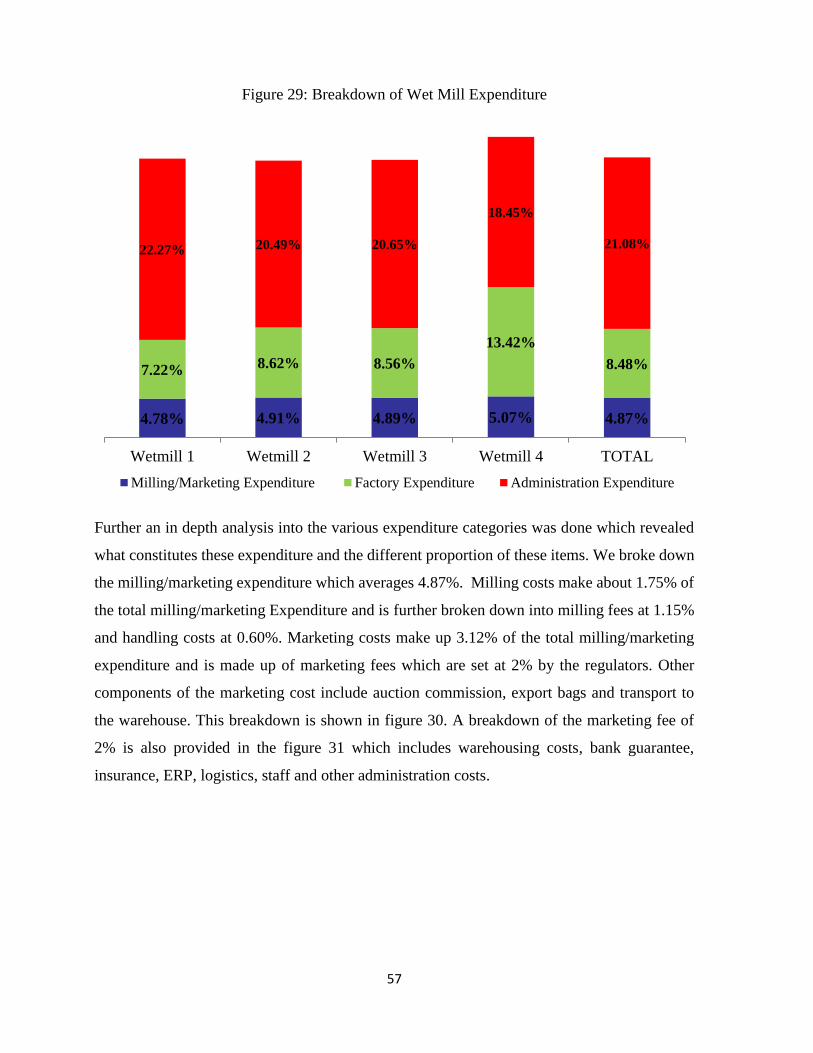

FIGURE 29: BREAKDOWN OF WET MILL EXPENDITURE ............................................................................. 57

FIGURE 30: BREAKDOWN OF MARKETING AND MILLING COSTS .............................................................. 58

FIGURE 31: BREAKDOWN OF THE MARKETING FEE ................................................................................... 58

3

FIGURE 32: BREAKDOWN OF FACTORY AND ADMINISTRATION COSTS .................................................... 59

FIGURE 33: COMPARISON OF AVERAGE PRICES ACROSS DIFFERENT CLEAN COFFEE GRADES ................ 71

FIGURE 34: COMPARISON OF PRICE VARIATION FOR DIFFERENT CLASSES OF SAME GRADE IN SAME

AUCTION ..................................................................................................................................................... 61

FIGURE 35: ESTATE FARMERS SENSITIVITY ANALYSIS WITH REVENUE AND COST GROWTH .................. 61

FIGURE 36: SMALLHOLDER FARMERS SENSITIVITY ANALYSIS WITH REVENUE AND COST GROWTH ...... 62

FIGURE 37: ESTATE FARMERS’ SENSITIVITY ANALYSIS WITH REVENUE GROWTH AND COST DROP ...... 62

FIGURE 38: SMALLHOLDER FARMERS’ SENSITIVITY ANALYSIS WITH REVENUE GROWTH AND COST

DROP ........................................................................................................................................................... 63

4

List of Tables

TABLE 1: COFFEE GROWERS THAT PARTICIPATED IN THE STUDY ................................................... 9

TABLE 2: COFFEE PRODUCTION HISTORY ...................................................................................... 12

TABLE 3: COFFEE GROWERS THAT PARTICIPATED IN THE STUDY ................................................. 31

TABLE 4: ANNUAL AVERAGE PRICE PER KILO OF CLEAN SEASON 2016/17.................................. 43

TABLE 5: PAY OUT COMPARISON ACROSS WET MILLS ................................................................. 56

5

Table of Contents

ABBREVIATIONS ........................................................................................................................ 1

EXECUTIVE SUMMARY ............................................................................................................ 7

1.0 BACKGROUND OF THE STUDY .................................................................................. 10

1.1 Coffee Production in Kenya ........................................................................................... 10

1.2 Sauti ya Kahawa ............................................................................................................. 13

1.3 Coffee Management Services Ltd (CMS) Background ................................................. 14

1.4 Stakeholders’ Consultative Forum Consensus ............................................................... 15

2.0 LITERATURE REVIEW .................................................................................................. 16

2.1 Definitions ...................................................................................................................... 19

2.2 Field Agronomy ............................................................................................................ 22

2.3 Revenue Determination .................................................................................................. 25

2.4 Cost of Production .......................................................................................................... 25

3.0 METHODOLOGY ............................................................................................................ 26

3.1 Coffee Economic Viability Study Background .............................................................. 26

3.2 Stakeholders’ Consultative Forum Consensus ............................................................... 26

4.0 DATA ANALYSIS AND FINDINGS .............................................................................. 27

4.1 Site Selection and Sampling ........................................................................................... 31

4.2 Data Collection and Analysis ......................................................................................... 32

4.3 Results and Findings ...................................................................................................... 33

4.3.1 Age of the Farmers.................................................................................................. 33

4.3.2 Gender of the Coffee Growers ................................................................................ 35

4.3.3 Level of Education .................................................................................................. 37

4.3.4 Household Size ....................................................................................................... 38

4.3.5 Production ............................................................................................................... 38

4.3.6 Cost of Production .................................................................................................. 40

4.3.7 Revenue Distribution .............................................................................................. 43

4.3.8 The Breakeven Points ............................................................................................. 45

6

4.3.9 Economic Viability Point ........................................................................................ 47

4.3.10 The Wet Mill Perspective ........................................................................................... 49

4.3.11 Sensitivity Analysis .................................................................................................... 55

5.0 RECOMMENDATIONS ................................................................................................... 64

6.0 APPENDICES .................................................................................................................... A

APPENDIX 1: ASSUMPTIONS ................................................................................................ B

APPENDIX 2: RESEARCH QUESTIONNAIRES .................................................................... C

7

EXECUTIVE SUMMARY

This report presents the results of the analysis of the data collected for the coffee economic study in all

coffee producing counties across the country in March 2018. This study consisted of in-depth interviews

with a target of 540 coffee farming households. The primary counties in which the sample was targeted are

based on the contribution to the national production as shown in the following graph:

Figure 1: National Production Distribution Overview

Source: Author’s Graphs using NCE data

The sampled estates, smallholders and wet mills were selected randomly in the respective counties. The

following figure shows the county and the respective farmers sampled.

5,636,151

4,325,876

4,286,369

4,066,928

2,466,772

2,200,006

1,755,288

1,372,517

747,363

655,572

557,244

522,362

437,048

320,299

130,945

87,296

48,581

47,717

31,217

20,811

Kiambu

Kirinyaga

Nyeri

Muranga

Kericho

Meru

Machakos

Kisii

Bungoma

Embu

Nakuru

Trans Nzoia

Tharaka Nithi

Kakamega

Nandi

Uasin Gishu

West Pokot

Baringo

Kisumu

Homabay

8

Figure 2: Coffee Growers Sampled in each County

A total of 495 respondents were interviewed from the different counties in coffee growing areas. However,

after cleanup of the data the respondents whose information was used in data analysis is as follows:

56

72 71 72

38

1410

35

5 2

31 32

9

18

512

97

8474 73

38

13 11

35

3 3

32 33

9

18

5

12

Nu

mb

er

of

Re

spo

nd

en

ts

Achieved Response Rate Total Sampled Respondents

9

Table 1: Coffee Growers that participated in the Study

County Number of Smallholder farmers

Number of Estate farmers

Number of Wetmills

Achieved Response Rate

KIAMBU 26 27 3 56

MURANGA 48 21 3 72

NYERI 61 5 5 71

KIRINYAGA 66 2 4 72

MERU 32 2 4 38

EMBU 10 2 2 14

THARAKA NITHI 9 1 10

KERICHO 29 2 4 35

NANDI 2 1 2 5

UASHIN GISHU 1 1 2

MACHAKOS 26 1 4 31

KISII 26 2 4 32

TRANS NZOIA 4 3 2 9

BUNGOMA 13 2 3 18

KAKAMEGA 3 1 1 5

NAKURU 7 2 3 12

363 73 46 482

All participants selected for the study were growing coffee and indeed made a contribution to the

national coffee volumes as per the NCE transaction listing reports in the season 2016/17. Since

quantitative analyses alone could not provide the in-depth understanding of the livelihood systems

employed by the coffee growers, this quantitative study is supplemented by a series of (qualitative)

discussions captured in narrative sections of the report.

Given that this report represents results from the first round of data collection, it presents more of

a profile, or a snapshot at a point in time of the surveyed coffee growers rather than a detailed

analysis of changes over time. A more detailed analysis of change can inform future studies.

Nevertheless, this report captures some interesting findings and results that have emerged from the

data analysis.

10

1.0 BACKGROUND OF THE STUDY

1.1 Coffee Production in Kenya

Agriculture is the backbone of Kenya’s economy with the government of Kenya estimating that

the sector accounts for about 25.4% of annual GDP and another 27% indirectly from agro-based

industries and services with small scale farmers contributing the most. Similarly, smallholder

farmers are responsible for more than three-quarters of Kenya’s coffee production. There are about

570,0001 small-scale farmers who have been most affected by the reducing income from coffee

because of falling productivity and difficulty in meeting international quality standards. For

instance, the production of coffee during Kenya’s independence in 1963 was 43,778 Metric Tons

(MT) and it substantially increased to a high of 128,926 MT in year 1987/1988. However,

following the collapse of International Coffee Agreement in 1989, production of coffee went into

a steady decline and coupled with other key challenges, production today is estimated at 42,000

MT1. This has significantly reduced the income of small scale coffee farmers with majority of

them neglecting the crop.

Smallholder coffee farmers in Kenya own approximately 85,000 hectares out of the approximately

110, 0001 hectares under coffee. It is estimated that six million Kenyans are employed directly or

indirectly in the coffee industry. The major coffee-growing regions in Kenya are the high plateaus

around Mt. Kenya, the Aberdare Ranges, Kisii, Nyanza, Bungoma, Nakuru and Kericho among

others. The high plateaus of Mount Kenya that have acidic soil provide excellent conditions for

growing coffee plants. Coffee from Kenya, which is of the 'mild Arabica' type, is well known for

its intense flavor, full body and pleasant aroma with notes of cocoa. This high grade coffee from

Kenya is one of the most sought-after coffees in the world.

Conditions favoring coffee growing include:

1. Temperature – Coffee does well under temperatures of 14 to 26°C although Arabica

coffee can tolerate temperatures of up to 30°C. In Kenya the coffee growing areas

experience cool to hot climate ideal for coffee growing. The temperatures average 15°—

30°C.

1 Coffee Research Institute

11

2. Rainfall – Arabica coffee requires rainfall ranging between 1000 and 2 000 mm per

annum. Many coffee growing areas in Kenya receive rainfall of about 1000 — 2000 mm

which is well distributed.

3. Soils – Most of the growing areas in Kenya have fertile deep volcanic soils which are

suitable for coffee. The soils are well drained and are acidic with a pH of between 5.3 and

6.0.

4. Topography – The coffee growing areas have undulating landscape with hill slopes as

well as gentle slopes. This has ensured well drained and aerated soils.

5. Altitude – Most of the growing areas have an altitude ranging between 610 m and 1830

m. However in a few areas like Machakos, coffee is grown at slightly lower altitudes.

6. Labour – Coffee growing is labour intensive. A lot of manual labour is required for

planting, pruning and harvesting. The dense human population in the growing areas has

provided a source of labour.

Coffee Varieties

Coffee Plants come in two main varieties: - Arabica and Robusta

Arabica beans are mild in the cup, with comparatively less caffeine, while Robusta is more

aromatic. The Robusta tree appears bushier, the leaves are larger and the berries form in clusters.

Coffee Research Institute (CRI) currently produces five commercial cultivars (varieties) of

Arabica coffee. Different varieties are recommended for various altitudes.

• K7 – low altitude coffee areas with serious Coffee Leaf Rust (CLR).

• SL 28 – medium to high coffee areas without serious CLR.

• SL 34 – high coffee zone with good rainfall.

• Ruiru 11 – all coffee growing areas. Resistant to both Coffee Berry Disease (CBD) and

CLR.

• Batian – all coffee growing areas.

12

Production History

Table 2: Coffee Production History

Season Auction Auction Direct Direct Total

Weight- Kgs Value $ Weight- Kgs Value-$ Weight- Kgs Value – USD

1998/99* 67,406,795 159,633,152 67,406,795 159,633,152

1999/20* 85,862,945 144,043,500 85,862,945 144,043,500

2000/01* 65,163,902 89,165,020 65,163,902 89,165,020

2001/02* 47,427,241 73,683,754 47,427,241 73,683,754

2002/03* 58,612,490 76,827,524 58,612,490 76,827,524

2003/04* 52,873,632 87,992,442 52,873,632 87,992,442

2004/05* 49,753,670 120,403,162 49,753,670 120,403,162

2005/06* 47,495,275 128,290,188 47,495,275 128,290,188

2006/07* 53,368,337 143,006,663 53,368,337 143,006,663

2007/08* 39,448,221 139,823,941 2,045,280 8,106,791 41,493,501 147,930,731

2008/09* 51,881,026 160,459,376 1,195,560 4,385,904 53,076,586 164,845,280

2009/10* 36,197,159 171,347,974 3,784,154 19,492,410 39,981,313 190,840,384

2010/11* 33,633,235 221,468,088 2,231,981 22,211,998 35,865,216 243,680,086

2011/12** 43,366,142 190,810,778 5,701,514 33,580,664 49,067,656 224,391,441

2012/13** 38,140,842 127,164,780 3,723,449 17,991,934 41,864,291 145,156,714

2013/14** 40,927,603 174,151,188 8,282,060 42,988,034 49,209,663 217,139,222

2014/15** 35,194,567 143,669,895 6,018,824 31,666,480 41,213,391 175,336,376

2015/16** 30,801,302 117,114,138 5,276,800 32,277,442 37,117,054 161,274,979

2016/17** 34,092,094 159,211,178 6,755,743 43,738,496 40,847,837 202,949,674

Source: CRI Data*, NCE Data**

13

Though the smallholders have 85,000 hectares out of the 110, 000 hectares under coffee in Kenya,

their productivity is very low. Most of the smallholders produce 300-400Kgs/ha of clean coffee

while the estates can do up to 1600 Kg/ha clean Coffee. This is as a result of the different farming

methods. Large plantations put in a lot of effort on implementation of the good agricultural

practices while smallholders face a number of challenges from lack of information to lack of

capital, poor climate change adaption measures among others. However, challenges like lack of

research capacity and lack of success in developing new resistant high producing varieties is faced

by all producers in Kenya.

1.2 Sauti ya Kahawa

The Kenya coffee stakeholders have found it necessary to create a platform with a view to bringing

the value chain stakeholders together to deliberate on critical issues and develop a common

approach/strategy to address such issues. This idea was actualized with the initial funding and

technical support from Global Coffee Platform (GCP), UTZ, Solidaridad (SECAEC) and Africa

Fine Coffees Association (AFCA). The platform shall make it possible for the stakeholders to

participate in setting the coffee agenda as well as to monitor and track the progress on the agreed

plans and goals. It shall also act as the entry point for the development partners and any other

organizations willing to work with actors along the value chain in country. The Government,

through the Ministry of Agriculture and Livestock and the Department of Cooperatives takes a

crucial role in making the platform a reality. The platform, dubbed Sauti ya Kahawa, borrows from

Global Coffee Platform, Uganda Coffee Platform, Tanzania Coffee Platform (Mkutano wa

Kahawa) and other countries’ coffee platform models and experience. The ultimate goal is to create

an inclusive and participatory County and National level coffee forum that will bring together all

coffee stakeholders to discuss critical issues affecting the sector, resulting in an increase in coffee

production and quality in the Country as well as a conducive business environment. As a basis for

the improvement of Kenyan coffee producers’ profitability, the newly founded Kenyan National

Coffee Platform “Sauti ya Kahawa” and the GCP commissioned a study to identify key areas for

action and to identify agreed criteria to determine the cost of production and living income among

coffee farmers.

14

1.3 Coffee Management Services Ltd (CMS) Background

Coffee Management Services Ltd (CMS) is a private limited company owned by East Africa

Coffee Co LLP. It commenced operations in 2006 and has operated for 12 years emerging the

best coffee marketer in terms of market share. Being an agribusiness firm, CMS provides several

services to its clients. These include farm management, pre-financing coffee production, price risk

management, marketing, bulk competitively priced farm inputs, project management,

environmental audits, sustainability and certification expertise. CMS comprises of 88 employees

out of which 30 are senior agronomists.

Over the years CMS have emerged to be the leading coffee marketer, marketing 23 % of the

Kenyan coffee. Currently CMS is working with 141 wet-mills and this means approximately

250,000 smallholders in Kenya. These farmers are scattered in all the coffee producing counties

in Kenya. The company comprises of highly qualified staff that are equipped with the right skills

for coffee productions, project management, Environmental audits and farm management. CMS

also manages large farms that cover up to 2,800 ha. The company has been training farmers and

has identified most of the challenges facing smallholder farmers: lack of knowledge of soil

nutrition, appropriate inputs, inadequate farmers training, lack of market information,

unfavourable terms while accessing credit, etcetera. CMS has over 30 are field agronomy liaison

officers who do farmers’ trainings. CMS has been guiding farmers towards sustainability and more

so advising them on how the crop is likely to behave. One of the major activities has been to

encourage farmers take their soils for expert analysis so that they may be sure of the nutrients that

the soils need to support the coffee tree. This is meant to avoid deficiency or over dose of some

nutrients. This has given a wide range of experiences in terms of identifying the factors affecting

coffee production , cost of production for coffee, coffee industry policies , production trends ,

market trends and price trends . The combination of the said factors determines the amount of

income realized by the producers.

Previously CMS has partnered with several other partners ranging from local institutions to

international institutions. Some of the partners have been other private companies, NGOs, public

institutions, government institutions and The Dutch government. These partnerships include;

Nescafe plan – Creating Shared Value with Nestle, CSR projects with Tchibo in Germany, Dutch

15

government in food security, Bill and Melinda Gates, DEG and IDH. CMS is also in Tanzania and

Rwanda. It is also offering consultancy services in Ethiopia.

1.4 Stakeholders’ Consultative Forum Consensus

A consultative meeting was held at the beginning of the study to get stakeholder input which

involved methodology and data collection. See picture below:

Figure 3: Stake Holders Consultative Forum

16

2.0 LITERATURE REVIEW

Economic viability for farmers has been an area of interest over the years. Numerous studies on

crops viability have been done around the whole world. A study conducted by Joni Valkila of

Institute of Development Studies was to evaluate the viability and advantages of Fairtrade organic

coffee production and trade in the case of the Nicaraguan small-scale farmers. This study indicated

the economic advantages of growing coffee are not always clear though Fairtrade organic coffee

production can increase farmer income in the case of low-intensity coffee production. It was

however noted that more intensive Fairtrade organic Coffee production can yield benefits through

premium but still yields tend to be lower compared to conventional methods. The study further

noted that when the conventional prices are low, Fairtrade prices will be a bit high. The conclusion

was that it’s hard to determine the viability of Fairtrade organic Coffee in Nicaragua since the

prices are not stable.

A study conducted in Colombia (2007) by the Global Coffee Platform (GCP) on Coffee Economic

viability indicated that farmers were not producing optimally. It was noted that the farmers were

producing 300 kg green / ha and could be increased by 65% on average. 70 % of the coffee growing

population was producing below the average. This meant that they were not viable. The study

noted that among the factors affecting coffee viability include poor agronomic practices, cash flow

issues, lack of training, very old trees among others. If the above issues could be solved, the study

indicates that it would be possible to increase productivity by 25%.

Another study conducted in Colombia by International Coffee Organization in 2016 indicated that

the coffee revenue could only cover variable costs and thus the operating profit was positive.

However the long-term viability of Coffee was uncertain since the revenues would not cover full

costs of production i.e. variable and fixed costs. The study also mentioned that if the established

cost of 10 million COP/ha was brought into the picture and spread over 8 year’s lifetime, the

situation worsens. There were only four crop years out of the 10 years that were studied that had

the total profits greater than or equal to zero.

The same study noted that the scenario in Costa Rica is more or less the same with Colombia in

terms of cost of production. Costa Rica had very high prices and thus the revenues would cover

17

the costs comfortably in the case of 2005-2011. However, in 2012 the prices dropped drastically

and farmer incurred losses. This is a clear indication that coffee viability depends to some extent

on the prices though it’s a combination of cost management and optimal production.

In El Salvador , the same study indicated that the costs were taking an upward trend up to 2012

but in 2013 there was a leaf rust outbreak that affected the crop adversely and this resulted to

reduced labour cost and eventually a drop in the cost of production from 1400 USD/ha to 1300

USD/ha. On the other hand, the prices decreased and this led to 50% decrease in revenue again

threatening the viability of Coffee. As result, it was expected that most of the farmers would move

from Coffee to cocoa production. In Brazil, contrary to other countries, the study showed positive

profits both in Arabica and Robusta cases. Even when the establishment costs were brought into

account, the profits were still positive, an indication that Coffee farming was viable in Brazil then.

In Africa, a case study of coffee growing association conducted in Rwanda indicated that coffee

growing would only be profitable if the specialty market buys that coffee. However, this study had

limitations since it studied only on farmers’ association.

A study conducted by TechnoServe for GCP (2017) indicated that production for smallholders was

as low as 300 kg green/ ha with potential for a 65% increase in average yield. However the potential

may be lower for regions with poorer soil and older trees. The study mentioned some of the key

levers for yield improvement as farm rejuvenation, training in GAPs and targeted fertilizer and

pesticide application. The study also foresaw an opportunity for a 144% increase in profitability

for farmers, which translates into an estimated $55m annual potential value across the 571,000

smallholder farmers.

Sector study conducted by Agri-Logic for GCP (2016) on sector reviews of Angola, Burundi,

Cameroon, Côte d’Ivoire, Ethiopia, Kenya, Rwanda, Tanzania and Uganda indicated that in most

African origins, yields are low, quality is inconsistent and supply chains are inefficient. The study

indicated that coffee production has really reduced in Côte d’Ivoire, Zimbabwe, Congo

(Brazzaville), Gabon Zambia and the Central African Republic. However, a positive trend in

growth was noted in Kenya, Tanzania and Rwanda since supply over the past 5 years is positive.

This study noted that farming household income was below poverty line in all of the African coffee

origins. This would mean coffee farming is not viable but with proper investment, farmer training,

18

rejuvenation/replanting, input supply, improvement of processing capacity, access to credit and

farmer organization capacity building, the study noted that productivity can improve making

coffee viable in these countries. This study further suggested that the bulk of the investment should

be on farmers’ training and input supply.

Strategic Literature Review study on coffee production costs and farm profitability conducted by

Specialty Coffee Association (2016) indicated that there was a highly significant correlation

between profitability and production cost per kilogram. This was based on the understanding that

profitability is the value of guaranteed price against production costs. The study also showed that

production costs per kilogram and yield are not correlated and neither are production costs per

kilogram versus costs per hectare correlated. This means that the extra cost invested per hectare

would not automatically be compensated by achieving extra yield.

A study by True Price, commissioned by Fairtrade International (2017), “Assessing Coffee Farmer

Household Income” indicated that farmers in Indonesia relied highly on income from coffee

production whereas farmers in Kenya relied mainly on other sources of income. On average about

50% of farmer household income resulted from coffee production. The other large contributors

were income from other farm goods and off-farm wage income. Indonesian and Vietnamese

farmers had the highest farmer household incomes, which was mainly due to relatively high

incomes from coffee. Indonesian farmers had the highest coffee profitability, which resulted from

relatively low costs of production. Tanzanian farmers also had a high profitability per kilo of

coffee, but this did not translate into high farmer household incomes due to relatively low coffee

production volumes. Moreover, Tanzanian farmers had almost negligible in-kind farm income and

income from off-farm activities. While some Kenyan farmers were making a profit on their farms,

the overall picture is very mixed, so that on average, Kenyan farmers were making losses on coffee

production. The results of this study were placed on the living wage concept and it was found that

on average Indian, Indonesian and Vietnamese farmers earned a household income, but only

Indonesia farmers earned a living household income from coffee production alone. Twenty-five

percent of Indian farmers, almost 50% of Indonesian and Vietnamese farmers and 100% of Kenyan

farmers could not earn a living income. An additional ‘value added analysis’, showed that farmers

were able to provide their households and their hired workers with a living income from coffee

19

production in India and Indonesia. In Kenya – where farmers made losses on coffee production –

and Vietnam, that was not the case then.

2.1 Definitions

Economic Viability

Economic viability means that the real returns from farming operations relative to the farm’s asset

value and labour inputs are competitive compared to other alternatives. Farming is the defining

characteristic of a farm; it must succeed on that basis in order to be viable.

Estate Farmer Economic Viability

Economic viability in the case of an Estate farmer refers 11.16% risk free rate (one Year Treasury

Bill) plus annual average inflation rate of 5% plus a return on tax of 30%, all this summing up to

around 22%. This means that economic viability of this farmer shall be a Return on Investment of

above 22%.

Smallholder Farmer Economic Viability

Economic viability in the case of a smallholder farmer refers to the ability and capacity of a farm

to 'make a living'. This shall be influenced by ability over time of the farmer to apply good

agriculture practices that enable them to continually produce above their cost of production and

earn at least the living wages as given by Anker and Anker (2015).

Profitability

Profitability is defined as the ability of the farmer to produce a return on an investment based on

their resources in comparison with alternative investments.

Profit

Profit is a measure of the financial performance of the farm. It is computed as total revenue less

total expenses incurred by the farmer. Although the farmer may realize a profit, this does not

necessarily mean that their coffee growing is viable.

20

Living Income may be defined as:

• The level of wages sufficient to meet the basic living needs of an average-sized family in

a particular economy, (ILO).

• The remuneration received for a standard work week by a worker in a particular place

sufficient to afford a decent standard of living for the worker and her or his family, Social

Accountability International, (SAI).

• Income sufficient to pay the bills, buy enough food, handle emergencies and stay off

welfare, (Black's Law Dictionary)

Elements of a decent standard of living include; food, water, housing, education, health care,

transport, clothing and other essential needs including provision for unexpected events.

A study conducted by Anker and Anker (2016) on Living Wage Report in Kenya with a focus on

rural Mount Kenya Area has placed the living wage at KShs.13, 193 gross per month. The same

author had in 2014 done a study on living wage for Lake Naivasha flower growing area and

currently tags it at KShs. 22,104 gross per month after adjusting for inflation and taxes for the

period from 2014 to 2016.

Costs of production include:

• What the farmer has to give up as they venture into the coffee farming. It is the necessary

investment needed to initiate the production process and keep it going.

• All the farm level cash outflow costs, selling costs, implicit costs for activities done by the

farmer himself, the farmer’s time spent in the farm and the interest income forgone by

committing the capital resources into the farm, transport, administrative, financing and

security costs.

• Cost of production goes with the scale of production derived from economies of size.

Bigger farms have advantages over smaller farms. However, due to scale drawbacks, it is

not easy to determine the optimal size especially with the concept of diminishing returns

that often affect large scale farms.

21

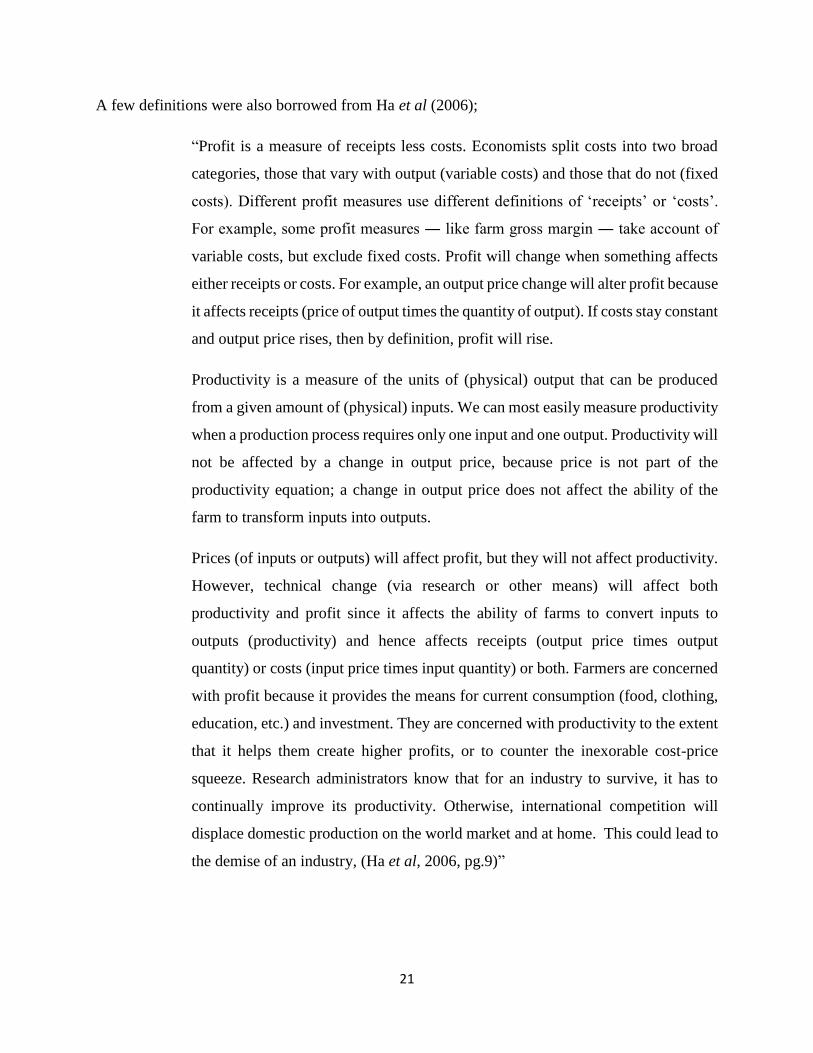

A few definitions were also borrowed from Ha et al (2006);

“Profit is a measure of receipts less costs. Economists split costs into two broad

categories, those that vary with output (variable costs) and those that do not (fixed

costs). Different profit measures use different definitions of ‘receipts’ or ‘costs’.

For example, some profit measures ― like farm gross margin ― take account of

variable costs, but exclude fixed costs. Profit will change when something affects

either receipts or costs. For example, an output price change will alter profit because

it affects receipts (price of output times the quantity of output). If costs stay constant

and output price rises, then by definition, profit will rise.

Productivity is a measure of the units of (physical) output that can be produced

from a given amount of (physical) inputs. We can most easily measure productivity

when a production process requires only one input and one output. Productivity will

not be affected by a change in output price, because price is not part of the

productivity equation; a change in output price does not affect the ability of the

farm to transform inputs into outputs.

Prices (of inputs or outputs) will affect profit, but they will not affect productivity.

However, technical change (via research or other means) will affect both

productivity and profit since it affects the ability of farms to convert inputs to

outputs (productivity) and hence affects receipts (output price times output

quantity) or costs (input price times input quantity) or both. Farmers are concerned

with profit because it provides the means for current consumption (food, clothing,

education, etc.) and investment. They are concerned with productivity to the extent

that it helps them create higher profits, or to counter the inexorable cost-price

squeeze. Research administrators know that for an industry to survive, it has to

continually improve its productivity. Otherwise, international competition will

displace domestic production on the world market and at home. This could lead to

the demise of an industry, (Ha et al, 2006, pg.9)”

22

2.2 Field Agronomy

The stakeholders agreed that the study would assume that the farmers have mature coffee trees.

The cost areas were to comprise the below areas;

Pruning

Pruning literally means removing superfluous parts of a tree. It is therefore a very large field of

operation. To be more precise, it is necessary to refer to pruning in its separate operations:

Conversion and first pruning, main pruning, handling, de-suckering and chimney opening.

Weed Management

Weeds are plants growing in a farm where they are not wanted. They pose a threat to the crop as

they compete for nutrients and water as well as harbor pests that may pose harm to the crop. Weeds

are characterized by very fast proliferation and can be a nuisance to control as they can interfere

with coffee management practices like fertilizer application.

Weed Control methods are the methods applied to suppress growth of the weeds or to eradicate

the weeds from the coffee field. They are both preventative and eliminative in nature. Weeds

control should be carried out whenever weeds are spotted especially during the wet weather and

should be a continuous activity to suppress their growth. The methods are classified into:

• Mechanical

• Chemical

• Cultural

Major Pest and Diseases

Diseases

The major coffee diseases are fungal and bacterial. They include:

• Coffee Berry Disease(CBD)

• Coffee Leaf Rust(CLR)

• Bacterial Blight of Coffee (BBC) being the only major disease caused by bacteria.

23

Other diseases include:

• Fusarium root disease

• Fusarium bark disease

• Brown eye spot disease

• Botrytis warty disease.

Pests

The major pests in coffee include:

Pest Type Economic Injury .Level

• Antestia 2 per tree

• capsid bug 4 tree

• Berry borer 10 adults

• Leaf skeletonizers 20 per tree

• Giant loopers 10 on suckers,20 on adults

• Thrips 2 per leaf

• Leaf miner 35 moths per tree

• Scales 10% in inspected area

Economic injury level refers to the smallest number of insects (amount of injury) that will cause

yield losses equal to the insect management costs

Coffee Nutrition

Nutrients are classified into Micronutrients and Macronutrients.

Macronutrients are those nutrients required in large and sufficient amounts and as such their

availability in less quantities result in nutrient deficiency disorders.

Foliar Feeds

They supplement ground applied fertilizers as well as supply micronutrients especially Zinc, Boron

and magnesium.

24

They are beneficial especially to plants carrying a heavy crop and in situations where the plant is

unable to absorb nutrients especially in dry seasons. The foliar should be applied when the

temperatures are low to prevent berry and leaf scorching.

Manures in Coffee

Application of organic manure to coffee is of utmost importance because manure contains the

major nutrients required for plant growth.

Manure as well, increases microorganism activities in the soil thus promoting nutrient availability.

They suppress weeds and moderate soil temperatures. They also improve soil structure and

improve water percolation.

Manure should be applied at a rate of 1-2 debes2 per hole during planting and yearly on mature

trees. This will greatly improve the soil nutrient profile and increase coffee production immensely.

Coffee Harvesting

Coffee quality is made in the field through the various agronomic activities carried throughout the

growth stages till maturity. To maintain the quality of coffee, it is essential that all stages are

followed and carried out as per the recommended procedures. Coffee harvesting begins when the

berries begin to ripen by turning red over at least 75 % of the surface.

This is achieved approximately 8 months after first flowering. Picking is the first operation towards

processing as it entails the removal of the ripe cherries from the coffee trees for processing. It is

during picking that the initial standard for quality is maintained through selective picking and

sorting

2 Debe is a 20 litre can.

25

Coffee Processing

Coffee processing is a critical stage from a quality maintenance point of view. It involves a series

of stages each of which has a distinct purpose. Good cherries from the farm may be spoilt if

processing conditions are not properly managed. There are three methods of processing namely:

wet processing, dry processing and honey processing.

Wet processing method involves pulping of cherries, fermentation then drying. This method gives

better quality coffee and as such is the main method used in Kenya. It is so called because most

stages require use of water.

Dry processing is also known as “mbuni”3 drying. It involves harvesting and drying the cherries

without pulping.

The third method of processing is a new method that is being adopted in Kenya. Honey processing

involves only picking the perfectly ripe cherries which are pulped without water. The parchment

is then dried with the mucilage still fully attached.

2.3 Revenue Determination

Revenue was calculated as per the below:

Total yield per tree (kg of cherry) multiplied by Price per Kg of cherry

2.4 Cost of Production

In our case, the costs of production included all the farm level cash outflow costs, selling costs,

implicit costs for activities done by the farmer himself, the farmer’s time spent in the farm and the

interest income forgone by committing the capital resources into the farm, transport,

administrative, financing and security costs.

Cost of production goes with the scale of production derived from economies of size. Bigger farms

have advantages over smaller farms. However, due to scale drawbacks, it’s not easy to determine

the optimal size especially with the concept of diminishing returns that often affect large scale

farms.

3 Mbuni refers to the Cherries that are dried without the removal of the pulp

26

3.0 METHODOLOGY

3.1 Coffee Economic Viability Study Background

In order to be able to understand the question of coffee economic viability in Kenya, the Kenya

National Coffee Platform “Sauti ya Kahawa” commissioned a study to identify key areas for action

and identify agreed criteria to determine the cost of production and living income among coffee

farmers. The objective of the study was to identify and pilot key criteria to determine the cost of

production, profitability and living income among coffee farmers, which would be agreed among

Kenyan coffee stakeholders and endorsed by the Kenya National Coffee Platform, to be used as a

national standard for farm economy assessments and to inform further areas of action. This study

focused on coffee growers across the country.

3.2 Stakeholders’ Consultative Forum Consensus

According to Agriculture and Food Authority (AFA), the smallholders are about 570,000 farmers

(grouped into about 600 Farmer Co-operatives). An estimated 3,850 farmers are in coffee estates.

These smallholder farmers produced 27,230 metric tons of coffee out of 40,848. This was 65% of

the total Kenya coffee production in the year 2017.

It was agreed that the sample size would thus be composed of 65% farmer co-operatives and 35%

from estate farmers. The sample on farmer co-operatives would be further broken down into wet

mills from where the smallholder farmers to be sampled would be drawn. The sample used 3

criteria, sampling error being at 5% significant level and 95% confidence level meaning that 95

out of 100 samples would have the true population value within the range of our precision.

The following explains how the sample size was obtained.

The assumptions made were as follows:

• We do not know the variability in the proportion that will adopt the generic coffee farming

Good Agricultural Practices; therefore, assumed p=.5. (the maximum variability in a

population)

• The coffee growing farmers is a large population by the definition of Cochran (1963:75)

and hence uses his equation as below to determine a representative sample for proportions.

27

Where:

Equation 1: no = Z2pq

e2

n0 is the sample size

Z2is the abscissa of the normal curve that cuts off an area at the tails (1 - equals the desired

confidence level, e.g., 95%). The value for Z is found in statistical tables which contain the

area under the normal curve, e.g. Z = 1.96 for 95 % level of confidence

e is the desired level of precision implying the acceptable sampling error

p is the estimated proportion of an attribute that is present in the population

q is 1-p

A total of 540 farmers were sampled on stratified sampling method on the basis of 65 % for

smallholder and 35 % for estates. Each county was allocated a sample size based on the average

volumes produced and sold in the NCE for the previous 3 years. Each county sample size was

further grouped into estates and farmer co-operatives following the established ratio. Interviews

conducted randomly for each of the groups. This is to say that counties that had below 1% of the

three year average national production were not viable for the study. This formed part of the study

limitations.

The average national market price was based on clean coffee data obtained from the NCE market

reports for the season 2016/17. Cost of production for the wet mills was obtained from Producer

Crop Returns (PCRs) that are maintained by the wet mills and filed with the Ministry in charge of

Cooperatives.

It was also agreed that data collection would be done through face to face interviews, observations,

documents and records review.

4.0 DATA ANALYSIS AND FINDINGS

28

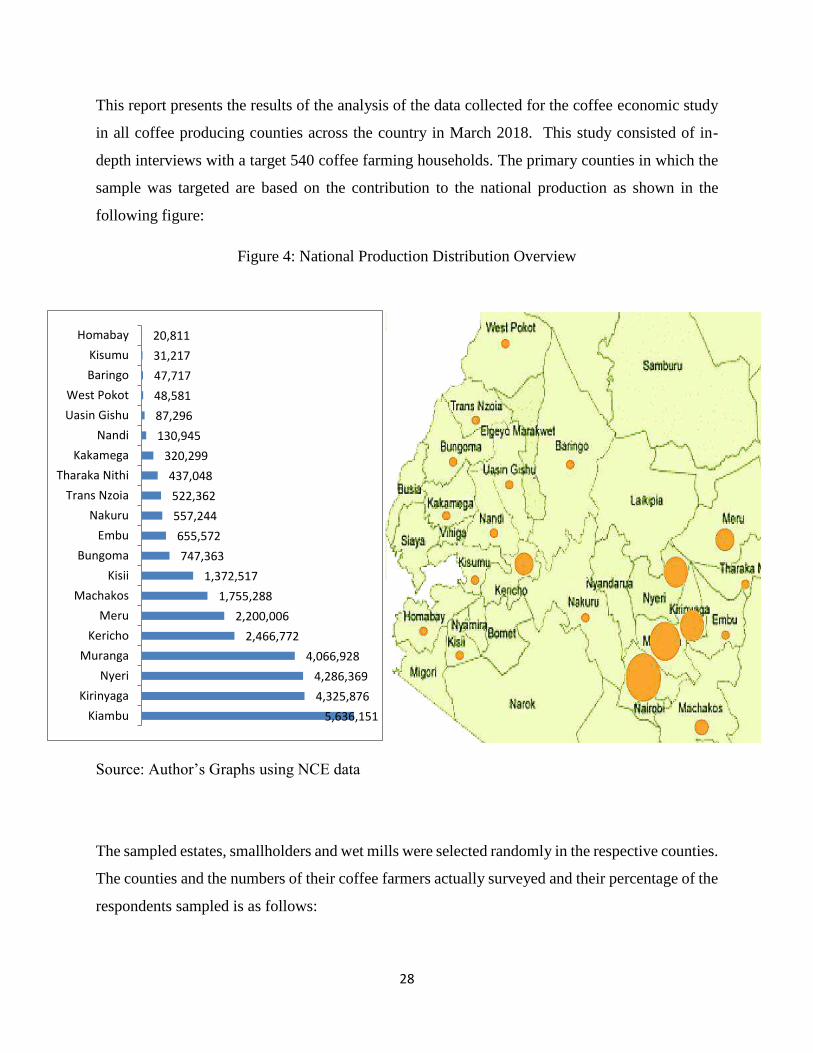

This report presents the results of the analysis of the data collected for the coffee economic study

in all coffee producing counties across the country in March 2018. This study consisted of in-

depth interviews with a target 540 coffee farming households. The primary counties in which the

sample was targeted are based on the contribution to the national production as shown in the

following figure:

Figure 4: National Production Distribution Overview

Source: Author’s Graphs using NCE data

The sampled estates, smallholders and wet mills were selected randomly in the respective counties.

The counties and the numbers of their coffee farmers actually surveyed and their percentage of the

respondents sampled is as follows:

5,636,151

4,325,876

4,286,369

4,066,928

2,466,772

2,200,006

1,755,288

1,372,517

747,363

655,572

557,244

522,362

437,048

320,299

130,945

87,296

48,581

47,717

31,217

20,811

Kiambu

Kirinyaga

Nyeri

Muranga

Kericho

Meru

Machakos

Kisii

Bungoma

Embu

Nakuru

Trans Nzoia

Tharaka Nithi

Kakamega

Nandi

Uasin Gishu

West Pokot

Baringo

Kisumu

Homabay

29

Figure 5: Coffee Growers Sampled in each County

A total of 495 respondents were interviewed in different counties in coffee growing areas.

However, after cleanup of the data the respondents whose information is used in data analysis is

as shown below:

56

72 71 72

38

1410

35

52

31 32

9

18

5

12

97

8474 73

38

1311

35

3 3

32 33

9

18

5

12

Nu

mb

er

of

Re

spo

nd

ed

nts

Achieved Response Rate Total Sampled Respondents

30

Table 3: Coffee Growers that participated in the Study

County Number of Smallholder farmers

Number of Estate farmers

Number of Wetmills

Achieved Response Rate

KIAMBU 26 27 3 56

MURANGA 48 21 3 72

NYERI 61 5 5 71

KIRINYAGA 66 2 4 72

MERU 32 2 4 38

EMBU 10 2 2 14

THARAKA NITHI 9 1 10

KERICHO 29 2 4 35

NANDI 2 1 2 5

UASHIN GISHU 1 1 2

MACHAKOS 26 1 4 31

KISII 26 2 4 32

TRANS NZOIA 4 3 2 9

BUNGOMA 13 2 3 18

KAKAMEGA 3 1 1 5

NAKURU 7 2 3 12

363 73 46 482

All participants selected for the study were growing coffee and indeed made a contribution to the

national coffee volumes as per the NCE transaction listing reports in the season 2016/17. Because

quantitative analyses alone cannot provide the in-depth understanding of the livelihood systems

employed by the coffee grower, this quantitative study is supplemented by a series of (qualitative)

discussions captured in the narrative sections of the report.

Given that this report represents results from the first round of data collection, it presents more of

a profile, or a snapshot at a point in time of the surveyed coffee growers rather than a detailed

analysis of changes over time. A more detailed analysis of change can inform future studies.

Nevertheless, this report captures some interesting findings and results have emerged from the data

analysis.

The interviews were conducted in a large number of randomly selected coffee growers in the

participating counties. Typically, farmers from various zones in the different counties were

31

interviewed. The data presented here represents a profile or a snapshot at a point in time of the

interviewed coffee growers rather than an analysis of changes that have taken place.

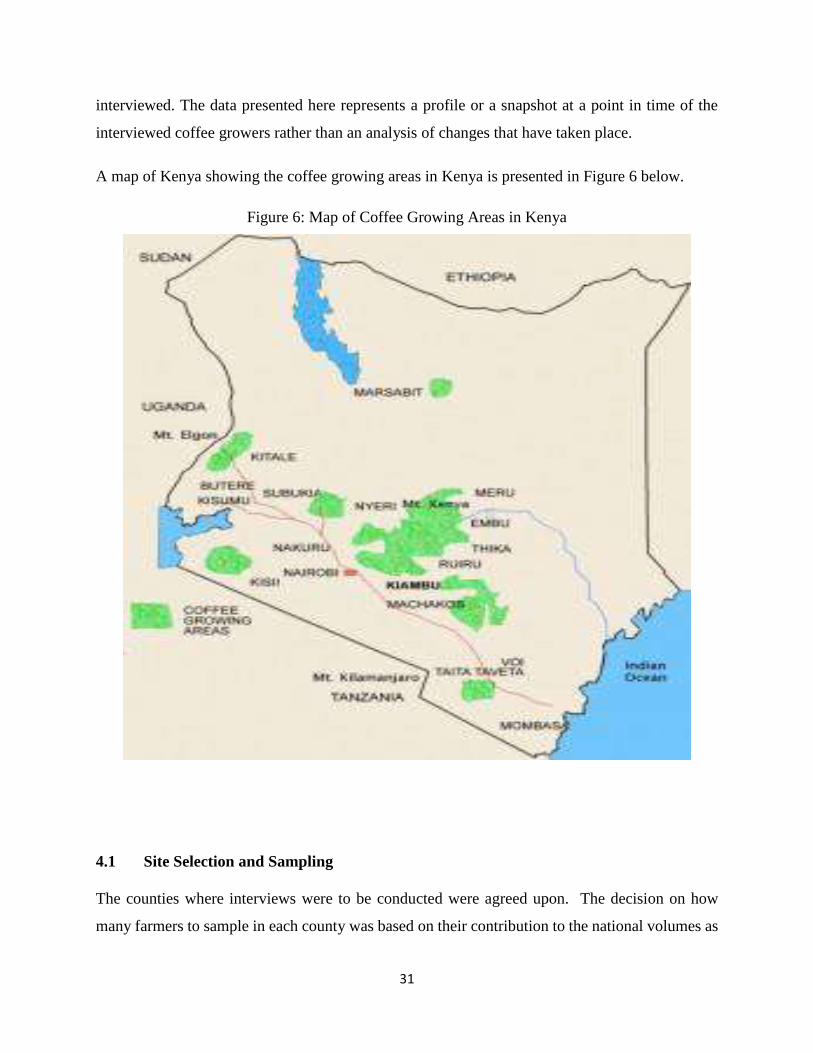

A map of Kenya showing the coffee growing areas in Kenya is presented in Figure 6 below.

Figure 6: Map of Coffee Growing Areas in Kenya

4.1 Site Selection and Sampling

The counties where interviews were to be conducted were agreed upon. The decision on how

many farmers to sample in each county was based on their contribution to the national volumes as

32

available in the Nairobi Coffee Exchange (NCE) 2016/17 Report. In each of the counties, the

coffee growers to be interviewed were randomly selected.

The farmers selected in the sample met the following criteria:

a. Must be a coffee producer.

b. Must be active i.e. have contributed to the national volume in season 2016/17.

c. Must be a member of the society for smallholders.

d. Must have delivered coffee to the respective FCS.

4.2 Data Collection and Analysis

After the respondents were identified, questionnaires were administered by the enumerators

capturing various areas of interest. The data collection was carried out between 26th February 2018

and 16th March 2018 on the targeted 540 coffee growers across all coffee growing counties of

Kenya. The data was entered, edited and analyzed using Microsoft Excel and is presented in

various forms such as graphs, tables, pie charts and others in this report.

Some of the conventions used throughout this report include the following:

• For ease of reviewing some of the results, percentages in figures and tables of results are usually

rounded off to the nearest whole percent. This means that occasionally the sum of percentages

in a table row or column or discussion in the text will not add up to exactly 100%

• Unless otherwise explicitly stated, missing cases and clearly erroneous outliers have been

excluded from the tables and figures. There are two reasons for this: (1) to avoid statistical

distortion of the results due to unrealistically large and/or small values and; (2) to improve the

clarity and details in some figures by reducing the ranges of the data considered. The

accompanying narrative indicates the ranges of the variables considered as being valid as well

as the number and/or percentage of the total number of surveyed coffee growers (540) that are

represented in these tables and figures.

• Some other numbers presented in the various tables throughout this report that have smaller

magnitudes may also be rounded off to either the nearest whole number or nearest one-tenth

percent unless otherwise stated.

• In order to protect the proprietary and confidential data of the Farmers, the vast majority of the

data presented in this report have not been disaggregated by farmer units.

33

4.3 Results and Findings

The respondents (coffee growers) were sampled from various counties across all the coffee

growing counties of Kenya where the survey was conducted.

The remainder of this report is organized into sections, where each section presents the analysis of

the baseline data relating to various aspects of interest. These sections and their subjects are as

follows:

▪ Section 4.3.1 - 4.3.4: Social Economic and Demographic Characteristics

▪ Section 4.3.5 - 4.3.8: Production revenues and costs

▪ Section 4.3.9: Sensitivity Analysis

4.3.1 Age of the Farmers

Figure 7: Age Distribution of Coffee Growers Surveyed by Percentage

Out of the 363 smallholder farmers surveyed, 177 farmers were above 60 years (the government

retirement age) which represents about 49%. This is not a surprising trend as coffee is popularly

known as “an old man’s crop”. It is also in line with earlier project literature review that indicated

that very few youth are involved in coffee growing. However, this data reaffirms the great need

for youth engagement and integration interventions to generate interest in coffee and more

5%

46%49%

18-35 35-60 >61

34

importantly to get them engaged in active coffee growing. Only 19 farmers were under the

stipulated youth age bracket of 35 years representing only about 5%. The low involvement of youth

in coffee farming could be explained by different reasons including the fact that some of the

counties like Kiambu are closer to the capital city of Nairobi and so most of their youth have

migrated there in search of jobs hence not involved in coffee growing. It could also be that there

is a general trend by the older folk not to pass along the coffee farming activities to the younger

generation. Competing enterprises including horticulture, dairy, and business could also be more

attractive for the youth compared to coffee farming.

When we drill down to the counties, we observe that the trend of old farmers is a common

occurrence across all the coffee growing counties regardless of the contribution towards the

national production which informed the number of growers to be sampled in each county as shown

in Figure 1.4 below. This further builds the case that the issue of youth integration in coffee

growing is a national issue rather than a regional one.

The average age of the coffee growers who participated in the study is 62 years across all the

counties surveyed. We put an upper age limit of 100 years and a lower age limit of 18 years to

eliminate outliers in analyzing the data.

35

Figure 8: Average Age by County

4.3.2 Gender and Coffee Growers

Coffee is pre-dominantly considered a male crop and the results of the baseline survey seem to

support this hypothesis as shown in Figure 9. Although women and youth provide most of the

labour on the coffee farms, ownership and decision making remain with the male in the household.

As highlighted in the literature review, women have been excluded in areas of training, leadership

positions and decision making. This has resulted in a big gap between training and implementation

resulting in low rates of adoption of Good Agricultural Practices. Most of the studies also noted

that there is a positive correlation between women and productivity and therefore recommends

women inclusion in coffee farming or employment of the household approach.

63

64

59

68

56

66

68

64

57

60

51

59

56

53

51

58

Kiambu

Kirinyaga

Nyeri

Muranga

Kericho

Meru

Machakos

Kisii

Bungoma

Embu

Nakuru

Trans Nzoia

Tharaka Nithi

Kakamega

Nandi

Uasin Gishu

Average Age ( Years )

Co

un

ty

36

Figure 9: Gender of Coffee Growers who participated in the Study

Only about 17 percent of all respondents interviewed across the coffee growing counties and across

estates and smallholders are female. This is in line with the literature review on gender in the coffee

sector that shows low women involvement. There were only 2 female estate owners from the total

73 estates interviewed which is only about 3% as shown in Fig 10. This could be explained by the

fact that most estates are passed on to the next generation and with a patrilineal inheritance system

then the estates tend to be passed onto the sons. Among the smallholder coffee growers

interviewed, 20% were female. This could be explained by the fact that for the smallholders, we

used the member registration documents at the cooperatives level. In some household the male

work away from home so the women are the ones who have a member number in the cooperative.

Also, there are a number of widows who have taken up the numbers of their spouses at the

cooperatives. Based on these observations, the higher number among smallholders should be

understood as growing and delivering coffee at the cooperative and not necessary an indicator to

coffee farm ownership.

83%

17%

Male

Female

37

Figure 10: Gender Distribution across different Farmer Archetypes

4.3.3 Level of Education

The education level of the head of the household could have a significant impact on their ability

to profitably run a coffee farming business .This may be due to their literacy level (their ability to

assimilate written manuals and other materials). Other factors may explain the strong correlation

seen between their education level and the impacts of a project on their specific household. The

coffee viability study interview asked about the highest educational achievement by respondent.

These results are presented in Figure 11 and show that, most of the farmers interviewed (66%)

have attained basic education which is the secondary school level as currently set by the

government of Kenya.

97%

3%Estates

80%

20%

Smallholders

Male

Female

38

Figure 11: Education Levels of the Coffee Growers Interviewed

4.3.4 Household Size

The average size of the household of the coffee growers interviewed is 6 people with average of 3

males and 3 females. The households have an average of 2 children and the other 4 being adults

including children above the age of 18 years. Although the primary activity from most of the coffee

growers interviewed is coffee, they also engage in other major activities including other cash and

food crops and dairy farming.

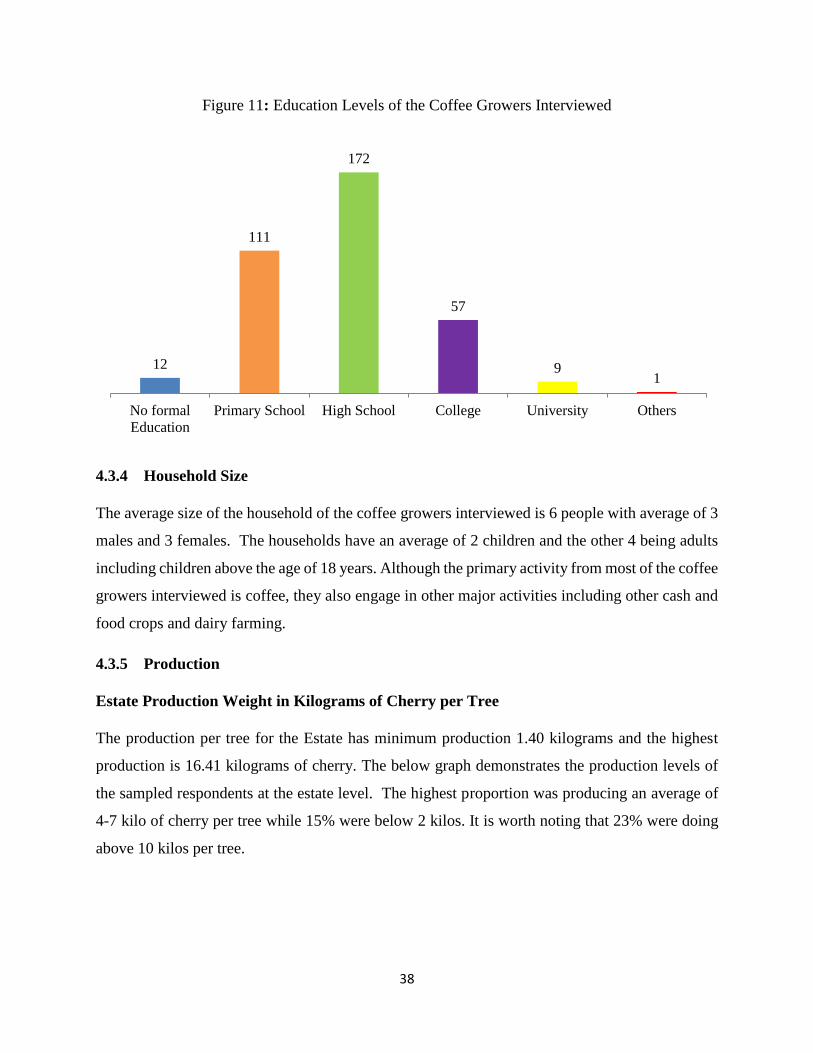

4.3.5 Production

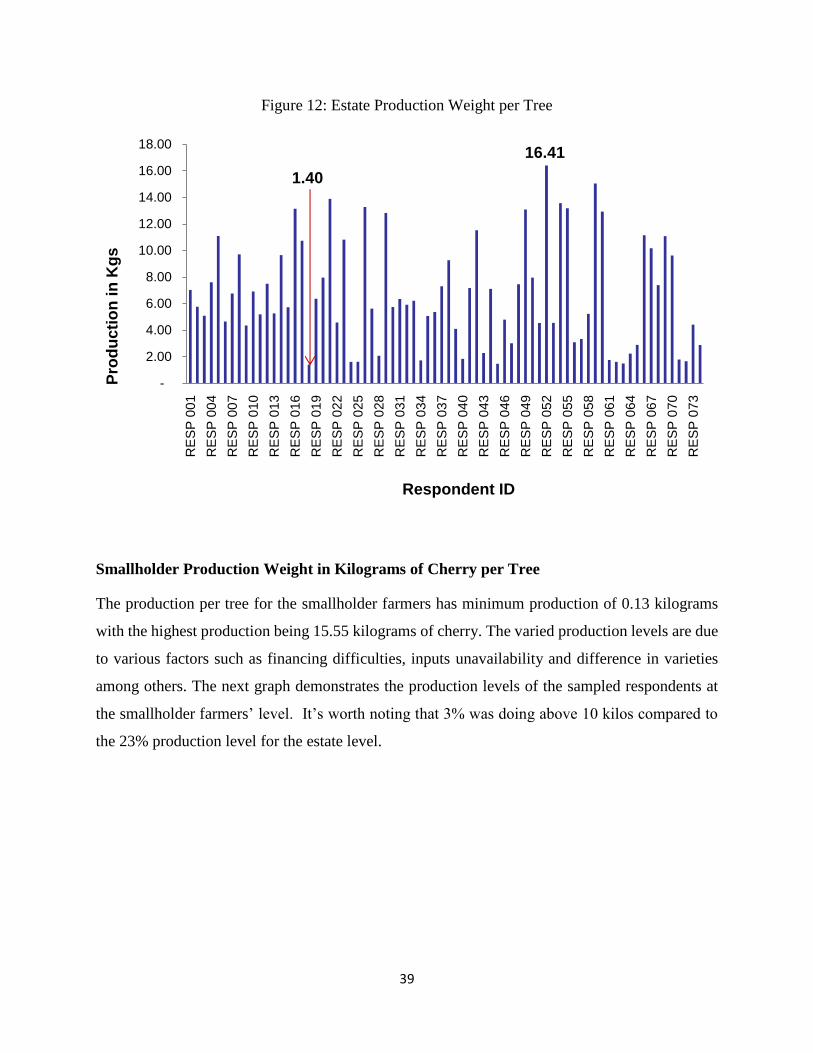

Estate Production Weight in Kilograms of Cherry per Tree

The production per tree for the Estate has minimum production 1.40 kilograms and the highest

production is 16.41 kilograms of cherry. The below graph demonstrates the production levels of

the sampled respondents at the estate level. The highest proportion was producing an average of

4-7 kilo of cherry per tree while 15% were below 2 kilos. It is worth noting that 23% were doing

above 10 kilos per tree.

12

111

172

57

91

No formal

Education

Primary School High School College University Others

39

Figure 12: Estate Production Weight per Tree

Smallholder Production Weight in Kilograms of Cherry per Tree

The production per tree for the smallholder farmers has minimum production of 0.13 kilograms

with the highest production being 15.55 kilograms of cherry. The varied production levels are due

to various factors such as financing difficulties, inputs unavailability and difference in varieties

among others. The next graph demonstrates the production levels of the sampled respondents at

the smallholder farmers’ level. It’s worth noting that 3% was doing above 10 kilos compared to

the 23% production level for the estate level.

1.40

16.41

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

RE

SP

001

RE

SP

004

RE

SP

007

RE

SP

010

RE

SP

013

RE

SP

016

RE

SP

019

RE

SP

022

RE

SP

025

RE

SP

028

RE

SP

031

RE

SP

034

RE

SP

037

RE

SP

040

RE

SP

043

RE

SP

046

RE

SP

049

RE

SP

052

RE

SP

055

RE

SP

058

RE

SP

061

RE

SP

064

RE

SP

067

RE

SP

070

RE

SP

073

Pro

du

cti

on

in

Kg

s

Respondent ID

40

Figure 13: Smallholder Production Weight per Tree

4.3.6 Cost of Production

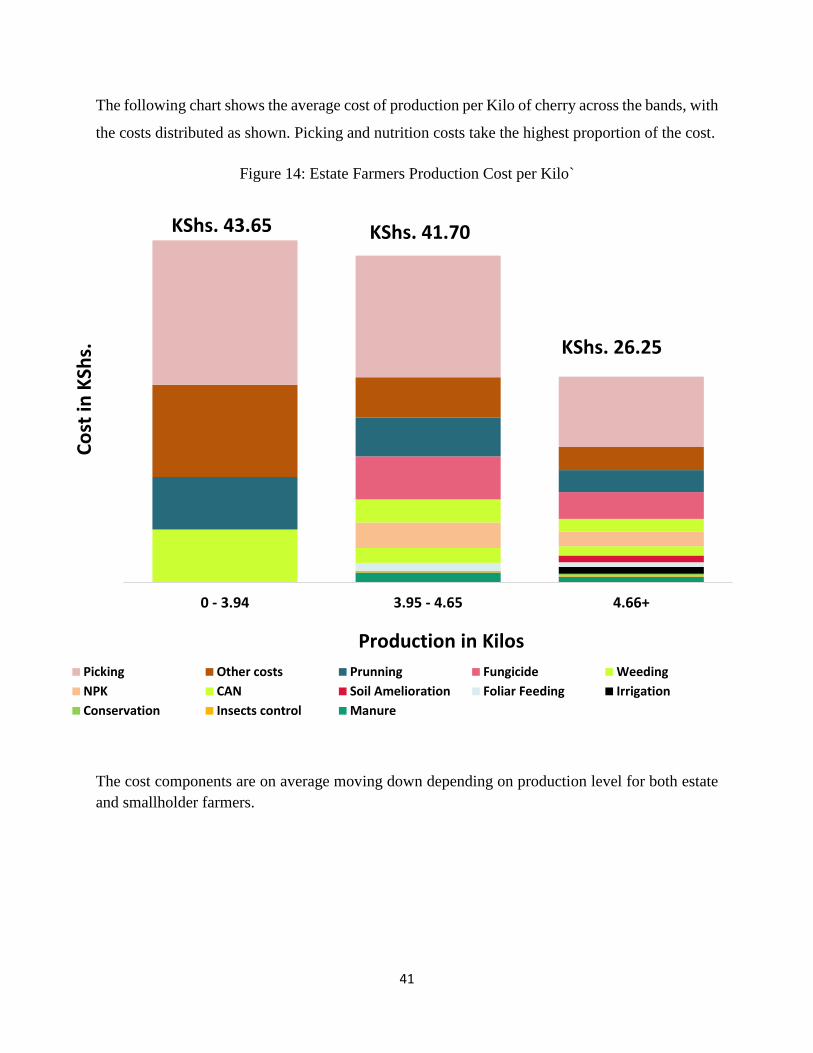

Average Production Cost for Estate Farmers

The production costs have labour cost components (pruning, weed control and picking) as the main

cost components for both estates and smallholder farmers. The estates have additional costs being

administration and processing costs forming part of major costs for the estates but not found in the

smallholder farms. The cost components are on average moving down depending on production

level for both estate and smallholder farmers.

From the raw data, the cost of production per kilogram of cherry had a high of KShs. 96.52 and a

low of KShs. 30.48 for the estate farmers. The variations in the costs are due to different farming

scales. Estate farmers are categorized in small, medium and large estates. They thus have varied

levels of adoption of Good Agricultural Practices. Other factors include labour, input costs, coffee

varieties among others.

0.13

15.55

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

RE

SP

00

1

RE

SP

01

0

RE

SP

01

9

RE

SP

02

8

RE

SP

03

7

RE

SP

04

6

RE

SP

05

5

RE

SP

06

4

RE

SP

07

3

RE

SP

08

2

RE

SP

09

1

RE

SP

10

0

RE

SP

10

9

RE

SP

11

8

RE

SP

12

7

RE

SP

13

6

RE

SP

14

5

RE

SP

15

4

RE

SP

16

3

RE

SP

17

2

RE

SP

18

1

RE

SP

19

0

RE

SP

19

9

RE

SP

20

8

RE

SP

21

7

RE

SP

22

6

RE

SP

23

5

RE

SP

24

4

RE

SP

25

3

RE

SP

26

2

RE

SP

27

1

RE

SP

28

0

RE

SP

28

9

RE

SP

29

8

RE

SP

30

7

RE

SP

31

6

RE

SP

32

5

RE

SP

33

4

RE

SP

34

3

RE

SP

35

2

RE

SP

36

1

Pro

du

cti

on

in

Kg

s

Respondent ID

41

The following chart shows the average cost of production per Kilo of cherry across the bands, with

the costs distributed as shown. Picking and nutrition costs take the highest proportion of the cost.

Figure 14: Estate Farmers Production Cost per Kilo`

The cost components are on average moving down depending on production level for both estate

and smallholder farmers.

0 - 3.94 3.95 - 4.65 4.66+

Picking Other costs Prunning Fungicide Weeding

NPK CAN Soil Amelioration Foliar Feeding Irrigation

Conservation Insects control Manure

Co

st in

KSh

s.

Production in Kilos

KShs. 43.65 KShs. 41.70

KShs. 26.25

42

Average Production Cost for Smallholder Farmers

Cost factors include labour, input costs, coffee varieties among others. The below chart shows the

average cost of production per kilo of cherry across the bands, with the costs distributed as shown.

However, the bulk of the costs are in picking. From the below, the smallholder farmers seem not

to invest much in pest and disease control and nutrition.

Figure 15: Smallholder Farmers Production Cost per Tree

The cost components are on average moving down depending on production level for both estate

and smallholder farmers.

0 - 1.28 1.29 - 2.53 2.54+

Picking Weeding Prunning Fungicide CAN

NPK Manure Foliar Feeding Insect Control Financing Costs

Production in Kilos

KShs. 91.16

KShs. 29.46

KShs. 42.09

43

In general, the cost of production for both categories will vary based on various factors among

them:

• Levels of adoption of Good Agricultural Practices

• Cost of labour

• Cost of input

• Coffee varieties

• Level of productivity ( Higher production = lower cost per unit )

• Level of farm management efficiency among others

4.3.7 Revenue Distribution

This study looked at revenue on various fronts as shown:

✓ Estate revenue as distributed through the value chain

✓ Smallholder revenue as distributed throughout the value chain.

✓ Smallholder revenue as distrusted with the cooperative society.

The average ex- auction rate was determined as KShs. 71 per kilo of cherry, which was based on

the national average price of USD 4.97 per kilo of clean for year 2016/17. The USD 4.97 was then

multiplies with 7 as per the conversion ratio. To explain how this is arrived at, see the following

table.

Table 4: Annual Average Price per Kilo of Clean season 2016/174

Green Coffee

Weight(Kgs)

No. of

bags(50Kg)

Value in USD Average Price

Per 50kg bag

Average Price

Per Kg

40,847,837 816,957 202,949,674 248.42 4.97

4 Nairobi Coffee Exchange Season 2016/17 Market Report

44

This amount was distributed throughout the value chain to determine what the different farmer

archetypes take home.

Figure 16: Revenue Distribution in Kenya Shillings per Kilo of Cherry

The total revenue of KShs. 71 was distributed throughout the value chain with the farmer being

left with KShs. 53.75 after taking care of processing and administrative costs at the society and

wet mill level.

As explained in the literature review, all smallholder farmers aggregate their coffee at the wet mill

thus the smallholder revenue may be looked at from two perspectives; value chain perspective and

the society level perspective as shown in the graph above.

Value Chain Wet Mill Estates1.25

1.25

2.56 2.56

67.19 67.19

67.19

9.10 9.10 3.53

4.33 4.33

21.2

53.75 53.75

42.46

Net paid to Farmers

Total Administration

cost

Total Factory

Processing cost

Net paid to FCS

Marketing Costs

Total Milling costs

45

From the value chain perspective, it was observed that the marketing revenue (this included milling

component) was only KShs3.86. This left a total of KShs. 67.19 that was transferred to the society

level. However, the farmer received KShs. 53.75, with a difference of KShs. 13.43 being retained

in the society/wet mill level.

From the society perspective, it was observed that the society received KShs. 67.19 which it shared

to administration and factory expenses before distributing the rest (KShs. 53.75) to the farmer. The

retained amount KShs. 13.43 was shared between the two functional costs such that administration

cost received KShs. 4.33 while factory expenses shared KShs. 9.10.

For estate farmers they still have to pay the marketing and milling costs thus after the amount

was distributed throughout the value chain with the estate farmer being left with KShs. 42.46 after

taking care of processing and administrative costs that include cost of security and financing.

Although the processing costs are much lower for estates, their administration costs seem to offset

this gain so they earn less per kilo of cherry compared to the smallholder farmers. However, due

their huge volumes, their total income is much higher for the individual farmer.

4.3.8 The Breakeven Points

The Breakeven Point for Estate Farmers

The breakeven per tree for the estate farmer is 3.94 kilo grams. Farmers will make losses while

producing anything below 3.94 Kgs of cherry per tree. Above this production, on average, the

farmers shall be making profits.

46

Figure 17: Breakeven Point for Estate Farmers

The Breakeven Point for Smallholder Farmers

The Breakeven per tree for the smallholder farmer is 1.28 kilo grams. Farmers will make losses

while producing anything below 1.28 Kgs of Cherry per tree. Above this production, on average,

the farmers shall be making profits.

Figure 18: Breakeven Point for Smallholder Farmers

y = 0.2532x - 0.3235

-150%

-75%

0%

75%

150%

225%

300%

375%

450%

- 2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00 18.00

Small Holder Farmers Break Even Point Margin %

Production per tree in

BEP:

1.28 Kgs per tree

47

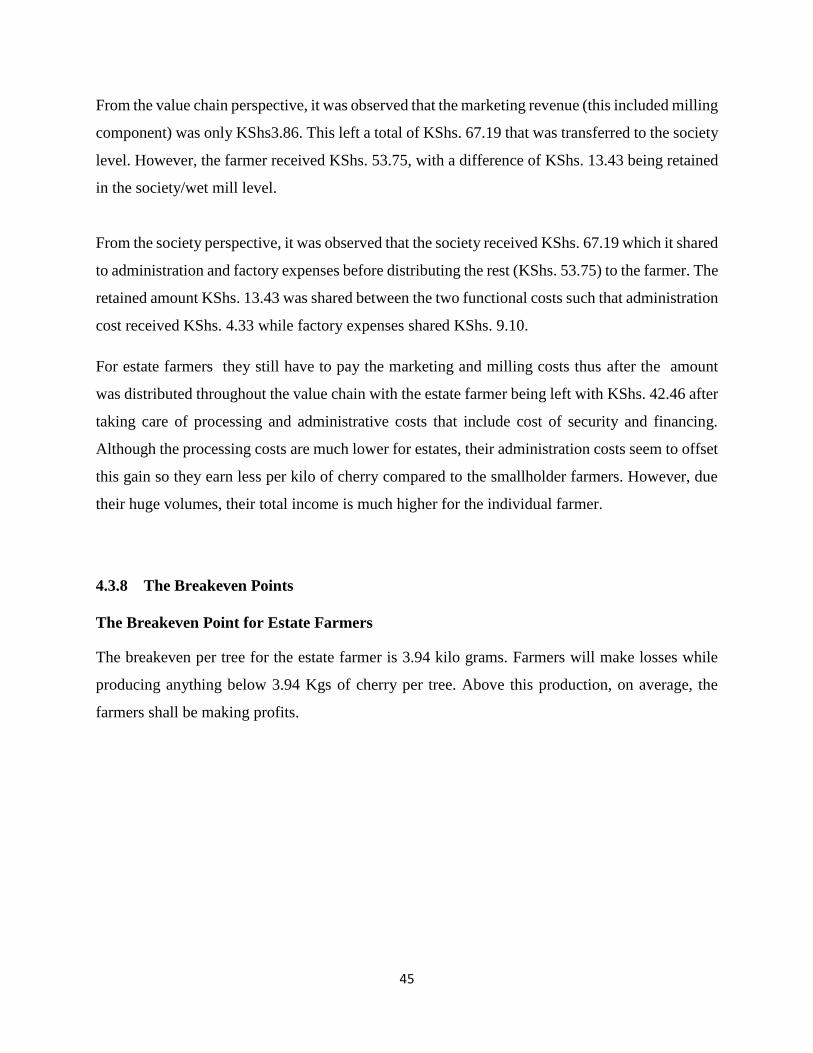

4.3.9 Economic Viability Point

The Economic Viability Point for Estate Farmers

The Economic Viability for the estate farmer is 4.65 kilo grams per tree. The farmers shall not be

economically viable while producing anything below 4.65 Kgs of Cherry per tree.

Figure 19: Economic Viability Point for Estate Farmers

Figure 20: Distribution of Economic Viability for Estate Farmers by production levels

-100%

-50%

0%

50%

100%

150%

200%

- 5.00 10.00 15.00 20.00

Ma

rgin

(%

)

Cherry Production per Tree (Kgs)

4.65

27

0 - 3.9426%

3.95 - 4.659%

4.66+65%

65% are above the economically viable production level

48

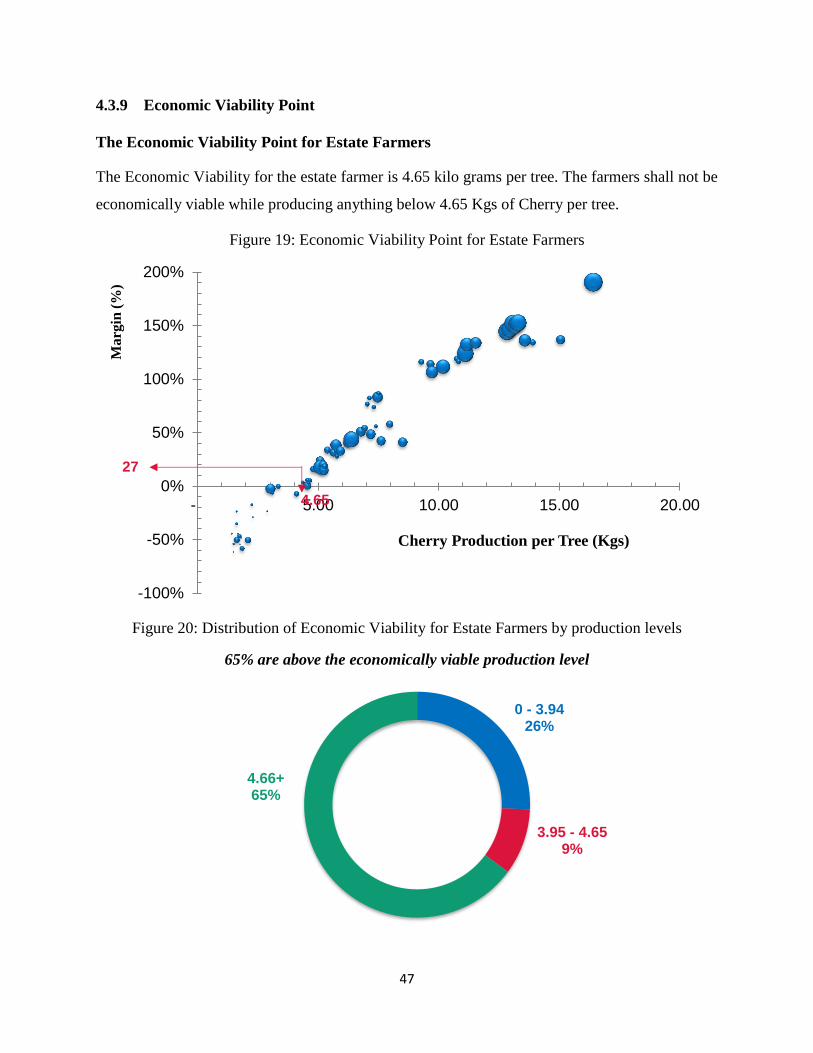

The Economic Viability Point for Smallholder Farmers

The Economic Viability for the smallholder farmer is 2.53 kilo grams per tree. At this production

rate, the farmer shall earn living wage, which is our measure of economic viability. The farmers

shall not be economically viable while producing anything below 2.53 Kgs of Cherry per tree as

they shall not be earning a living wage as calculated by Anker and Anker 2015.

Figure 21: Economic Viability Point for Smallholder Farmers

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

(2.00) - 2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00

Ma

rgin

( %

)

Cherry Production per Tree (Kgs)

2.5

88

49

Figure 22: Distribution of Economic Viability for Smallholder Farmers by production levels

4.3.10 The Wet Mill Perspective

There were a total of 46 wet mills that participated in the study from all the coffee growing regions

in the country as shown below:

Figure 23: Number of Wet mills Interviewed per County

0 - 1.2822%

1.29 - 2.5328%

2.54+49%

Close to 50% are above economically viable production level

3 3

5

4 4

2

1

4

2

1

4 4

2

3

1

3

50

Information was collected and analyzed from the participating wet mills through a questionnaire

administered by the field team. The data was then analyzed and used to corroborate data gathered

from the smallholder farmers. The wet mill data was also used to identify other factors that affect

the handling of the coffee once it leaves the farms and that affect the final payment that the farmer

receives.

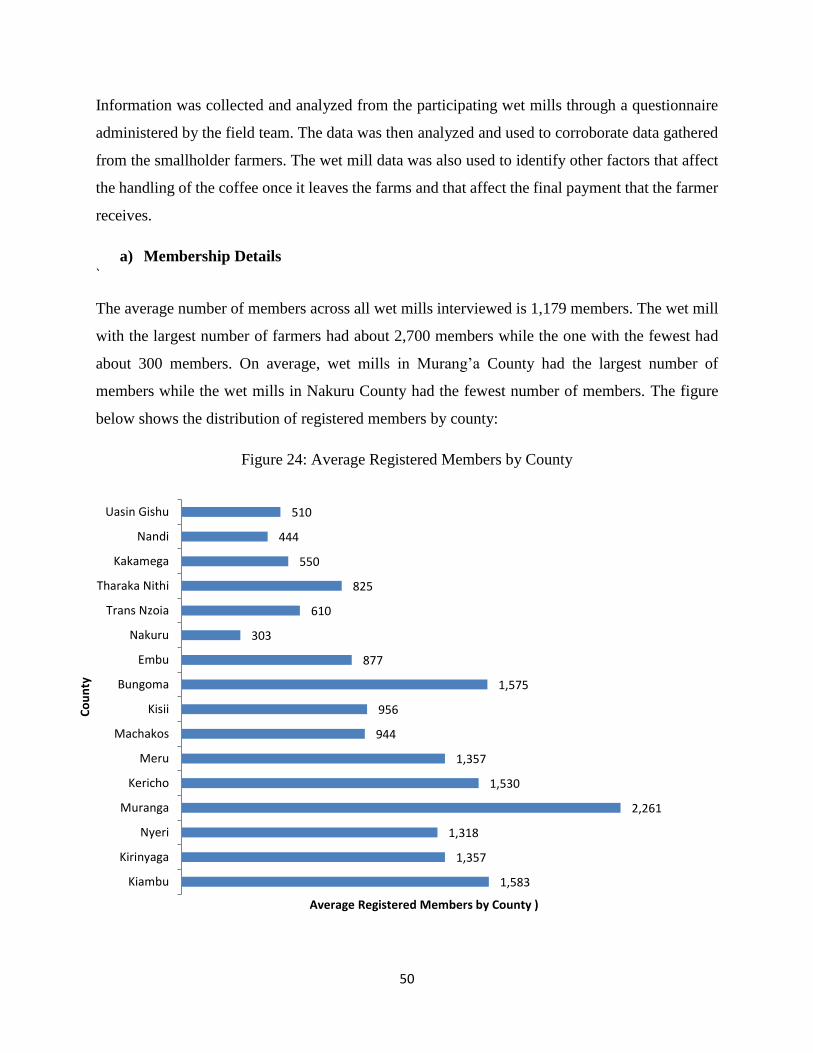

a) Membership Details `

The average number of members across all wet mills interviewed is 1,179 members. The wet mill

with the largest number of farmers had about 2,700 members while the one with the fewest had

about 300 members. On average, wet mills in Murang’a County had the largest number of

members while the wet mills in Nakuru County had the fewest number of members. The figure

below shows the distribution of registered members by county:

Figure 24: Average Registered Members by County

1,583

1,357

1,318

2,261

1,530

1,357

944

956

1,575

877

303

610

825

550

444

510

Kiambu

Kirinyaga

Nyeri

Muranga

Kericho

Meru

Machakos

Kisii

Bungoma

Embu

Nakuru

Trans Nzoia

Tharaka Nithi

Kakamega

Nandi

Uasin Gishu

Average Registered Members by County )

Co