coal demand and supply

TRANSCRIPT

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 1/23

1

OUTLOOK OF COAL DEMAND/SUPPLY AND POLICY IN INDIA

2009 APEC CLEAN FOSSIL ENERGY TECHNICAL AND POLICY SEMINAR

12TH - 14TH OCTOBER 2009INCHEON, KOREA

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 2/23

Presentation Sturcture

nCoal Sector Overview

nDemand profile

n Production Profile

n Strategic Initiatives

n Policy Challenges

22

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 3/23

Coal Sector Overview

33

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 4/23

Coal: World’s Fastest Growing Fuel

4

n Coal has been the world’s fastest growing fuel and coal use is expected

to grow faster than any other fuel far into the future

n Steep demand growth in China and India

4

7 Year Change in

Global Energy Consumption

Source: International Energy Outlook 2009, BP World Energy Report 2009

3%

10%

22%

23%

41%

0% 10% 20% 30% 40% 50%

Nuclear

Oil

Hydro

Natural Gas

Coal

2 0 0 1 - 2 0 0 8 C h a n g

CAGR

5.0%

3.0%

2.9%

1.4%

0.4%

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 5/23

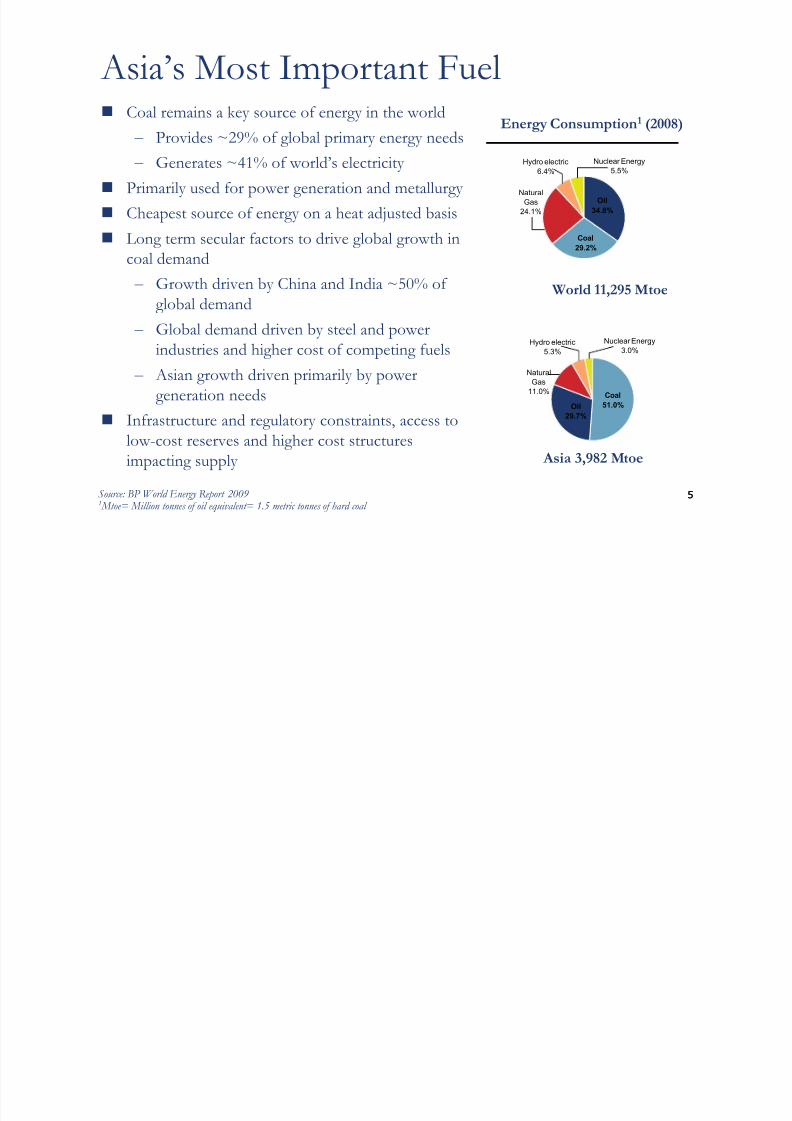

Asia’s Most Important Fueln Coal remains a key source of energy in the world

– Provides ~29% of global primary energy needs – Generates ~41% of world’s electricity

n Primarily used for power generation and metallurgy

n Cheapest source of energy on a heat adjusted basis

n Long term secular factors to drive global growth incoal demand

– Growth driven by China and India ~50% of global demand

– Global demand driven by steel and powerindustries and higher cost of competing fuels

– Asian growth driven primarily by powergeneration needs

n Infrastructure and regulatory constraints, access tolow-cost reserves and higher cost structuresimpacting supply

5

Energy Consumption1 (2008)

5

Oil

34.8%

Coal

29.2%

Natural

Gas

24.1%

Hydro electric

6.4%

Nuclear Energy

5.5%

World 11,295 Mtoe

Asia 3,982 Mtoe

Coal

51.0%Oil

29.7%

Natural

Gas

11.0%

Hydro electric

5.3%

Nuclear Energy

3.0%

Source: BP World Energy Report 2009 1 Mtoe= Million tonnes of oil equivalent= 1.5 metric tonnes of hard coal

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 6/23

6

Coal Industry in Indian Total resources

– ~267bn tonnes: 106bn proved,124bn indicated and 37bn inferred

n 81% of production from opencastmines; 19% from underground mines

n Coal present in 14 out of 28 states

n [Indian coal is generally high ash,

~4500 GCV, low Sulfur]

6

Coal Production and Imports

Source: Ministry of Coal, India; Coal India Management

Types of Coal Produced in India

Coking

12.6%

Non Coking

87.1%

Tertiary Coking

0.4%

Coal Reserves in India

India

China

Pakistan

Myanmar

Nepal Bhutan

Sri Lanka

Coalfields

India

China

Pakistan

Myanmar

Nepal Bhutan

Sri Lanka

Coalfields

323.5 343.4 360.9 379.5 403.7

59.163.6 69.9

77.689.3

29.038.6

43.149.8

59.0

411.6445.6

473.9506.9

552.0

0.0

100.0

200.0

300.0

400.0

500.0

600.0

2004-05 2005-06 2006-07 2007-08 2008-09

Coal Others Imports

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 7/23

Unparalleled Strategic Relevance

n The Indian economy expected to grow at 7.5% p.a. over the next 5 years

– Access to electricity a core element to achieving this growth

n Energy demand growing at 7% per year

– Additional generation capacity of 79 GW 1 by 2011-12 – of which 72%

coal-fired

– Over 50% of Indians currently do not have access to electricity

n Coal contributes ~54% of commercial energy in India

77

Growth in GW in India

Coal Consumption as % of Energy

Consumption in India2

Coal

53%Oil

31%

Natural Gas

9%

Hydro Electric

6%Nuclear Energy

1%

Total = 433.3 Mtoe

Source: External Research, Ministry of Coal, Planning Commission of India 1 Excludes Wind and Renewable Energy 2 Mtoe= Million tonnes of oil equivalent= 1.5 metric tonnes of hard coal

6985

105132

211

0

50

100

150

200

250

1992 1997 2002 2007 2012E I n s t a l l e d C a p a c i t y ( G W )

CA G R : 6 %

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 8/23

8

Indian Coal Industry in Context

8

Electricity Consumption per Capita

Source: International Energy Outlook

Per Capita Electricity Consumption Growthin India (units per capita)

Global Coal Reserves by Country

Global Coal Production by Country

238

157

115 106

76

34 31 30

4

0

50

100

150

200

250

300

U S A

R u s s i a

C h i n a

I n d i a

A u s t r a l i a

U k r a i n e

K a z a k h s t a n

S o u t h

A f r i c a

S o u t h

A f r i c a

B i l l i o n T o n n e s

1

504

631

2,024

2,444

7,493

10,347

13,515

Indonesia

India

Brazil

China

France

Australia

US (2007)

(2007)

(2007)

(2007)

(2007)

(2006)

(2007)

18

35

84

131

238

408

582

631

1,000

1950

1960

1970

1980

1990

2001

2004

2006

2012

58% Growth in

XIth Plan

993

256 327

1,455

2,782

358512

342 402

1,063

0

500

1,000

1,500

2,000

2,500

3,000

2002 2008

M i l l i o n T o n n e s

1

USA Russia China India Australia

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 9/23

Coal Reserves (as on 01.04.2009)

ØEstimated Coal Resources - 267.2 Bt Coking - 33.4 Bt; Non-coking - 233.8 Bt

ØProved Reserves – 105.8 Bt or 39.6%

Coking - 17.5 Bt; Non-coking coal- 88.3 Bt

ØRemaining 161.4 Bt or 60.4% of resources to be brought in

to proved category

ØExtractable reserves of about 55 Bt – may last for 50 years

with projected level of production.

ØEstimated Lignite resources - 38.93 Bt

– Proved Reserves - 4.82 Bt (12%)

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 10/23

IMPORTANCE OF COAL RESOURCES

IN INDIA

Ø In power generation coal contributes 75%.

Ø Power sector consumes 78% of total country’s

coal production.

Ø Industries such as steel, cement, fertilizer,

chemical, paper and a host of other industries

also dependent on coal.

10

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 11/23

Actual and Projected Coal Demand during XI Plan

731.00604.44555.00467.38463.87351.49Total

61.5858.9352.0060.29355.5237.76BRK & Others

28.9644.3318.0020.9217.474.40Sponge Iron

31.9125.6925.0019.3219.7415.25Cement

68.5020.2944.0040.0117.3017.37Steel & Coke

Oven

57.0657.6638.0033.1347.6629.42Power (Captive)

483.00397.54378.00333.44309.38250.38Power (Utility)

11-12(XI Plan)

09-10(BE)

08-09(RE)

07-08(Actual)

06-07(X Plan)

01-02(IX Plan)

Sectors

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 12/23

Actual & Projected Coal production targets for XI Plan

12680.00532.33492.95457.00430.84327.65Total

118.7052.8344.6736.94430.84327.65Others

40.8044.5044.5440.6037.7130.81SCCL

520.50435.00403.74379.46360.92279.65CIL-Total

46.00

30.00

78.00

70.0045.00

111.00

137.00

3.50

31.00

28.00

48.00

66.5045.00

106.00

109.30

1.20

28.14

25.51

43.24

63.6544.70

101.15

96.34

1.01

24.06

25.22

44.15

59.6243.51

93.79

88.01

1.10

30.47

24.21

41.32

52.1643.21

88.50

80.00

01.05

28.55

25.25

33.81

42.4637.01

64.12

47.81

0.64

ECL

BCCL

CCL

NCLWCL

SECL

MCL

NEC

11-12

(XI Plan)

09-10

(BE)

08-09

Actual

07-08

Actual

06-07

(X Plan )

01-02 (IX

Plan )

Company

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 13/23

Emerging Demand – Supply Gap in XI Plan

n Actual production from domestic sources - not likely toreach the envisaged level by the terminal year of XIPlan.

n Estimated demand based on existing linkages/ FSAs

and LOAs - outstrips estimated supply projections.nGgap likely to be wider than the gap projected by

Working Group.

13

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 14/23

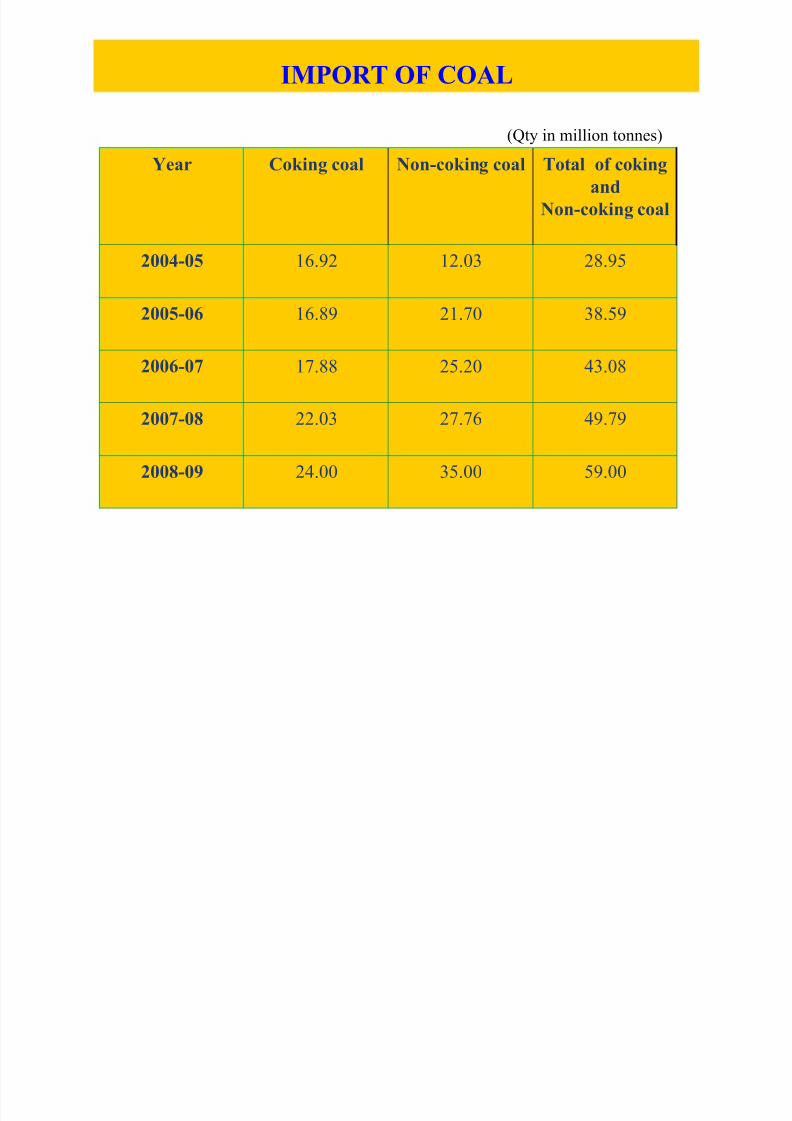

IMPORT OF COAL

59.0035.0024.002008-09

49.7927.7622.032007-08

43.0825.2017.882006-07

38.5921.7016.892005-06

28.9512.0316.922004-05

Total of coking

and

Non-coking coal

Non-coking coalCoking coalYear(Qty in million tonnes)

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 15/23

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 16/23

Key Strategic Initiatives

1616

Ø Enhancing Availability of

Resources

Ø Ensuring Accessibility of

Resources

Ø Increasing Acceptability

of Mining Practices

Ø Improving Profitability

and Efficiency

Targeting:

Ø Sustainable

Development

Ø Growth

Ø Profitability

Ø Efficiency

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 17/23

17

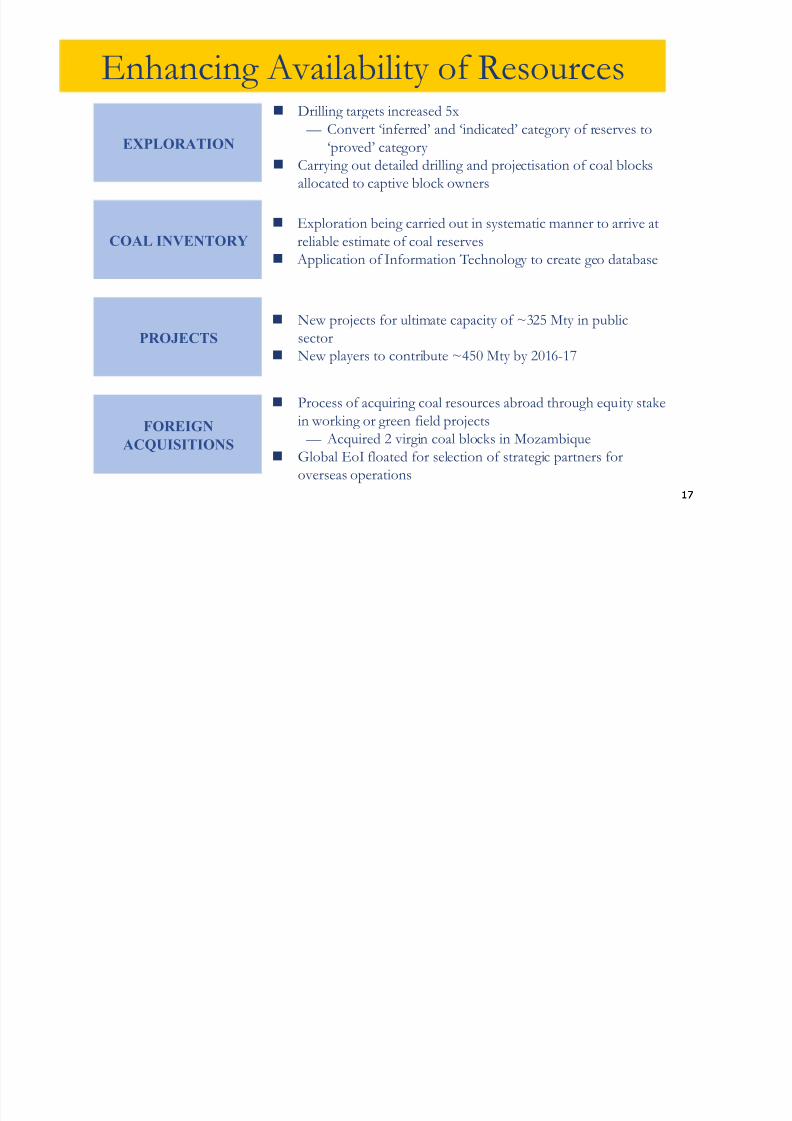

Enhancing Availability of Resources

17

EXPLORATION

COAL INVENTORY

n Drilling targets increased 5x

— Convert ‘inferred’ and ‘indicated’ category of reserves to‘proved’ category

n Carrying out detailed drilling and projectisation of coal blocksallocated to captive block owners

n Exploration being carried out in systematic manner to arrive at

reliable estimate of coal reservesn Application of Information Technology to create geo database

PROJECTS

n New projects for ultimate capacity of ~325 Mty in publicsector

n New players to contribute ~450 Mty by 2016-17

FOREIGN

ACQUISITIONS

n Process of acquiring coal resources abroad through equity stake

in working or green field projects — Acquired 2 virgin coal blocks in Mozambique

n Global EoI floated for selection of strategic partners foroverseas operations

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 18/23

P r

1818

EXPLORATION

COAL MINING

BENEFICIATION

n CIL owns 473 mines

– 279 UG – 163 OC

– 31 Mixedn SCCL and TISCO are the other main players in coal mining

n 201 blocks are allotted to public/private companies.

n CIL operates 17 washeries ( 11 coking and 6 non –coking)

n CIL has taken a decision to supply beneficiated coal to allconsumers, other than those located at pitheads

n19 new washeries are being taken up for construction underBOM with a total washing capacity of 105.6 Mty

n Carried out in two stages: Regional and Detailed

n In 2008-09, 0.272mn meters of drilling has been achieved

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 19/23

19

Ensuring Accessibility of Resources

19

OPENCAST MINING

UNDERGROUND

MINING

n Computer-aided mine planning for deeper OC mines

n Deploying high capacity equipment to achieve economies of scale

n OITDS for efficient fleet managementn State-of-the-Art mass production technology being used

n Tapping large reserves below 300m depth

n 7 UG Greenfield properties being developed

n 18 abandoned mines with estimated reserves over 1600 MTidentified for development

HIGHWALL MINING

n Mining of good quality thin seams

n Recovery of good quality coal in OC mines beyond economicstripping ratio limit

CBM/UCG

n Recovery and commercial utilization of CBM from deep seated

seamsn Underground coal gasification of deep seated seams

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 20/23

20

Increasing Sustainability of Mining Practices

20

SOCIAL

n Liberalized R&R policy for the Project Affected People (PAP)

n Supports 665 educational institutes in coalfield areas

n Provides medical assistance through 85 fully-equipped hospitals andnumerous dispensaries

n Setting up 19 washeries with a capacity of 105.6 Mty

n Started satellite surveillance for land reclamation and

restoration of OC minesn 29 OCPs secured ISO 14001 (Environmental Certification)

n Planted ~70 million trees with survival rate of over 75%

ENVIRONMENTAL

Plantations and Greeneries over OB Dumps1

1 Left Picture: Plantation over OB Dump, MCL. Right Picture: Greeneries over OB Dump, Umrer, WCL Source: Coal India Management

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 21/23

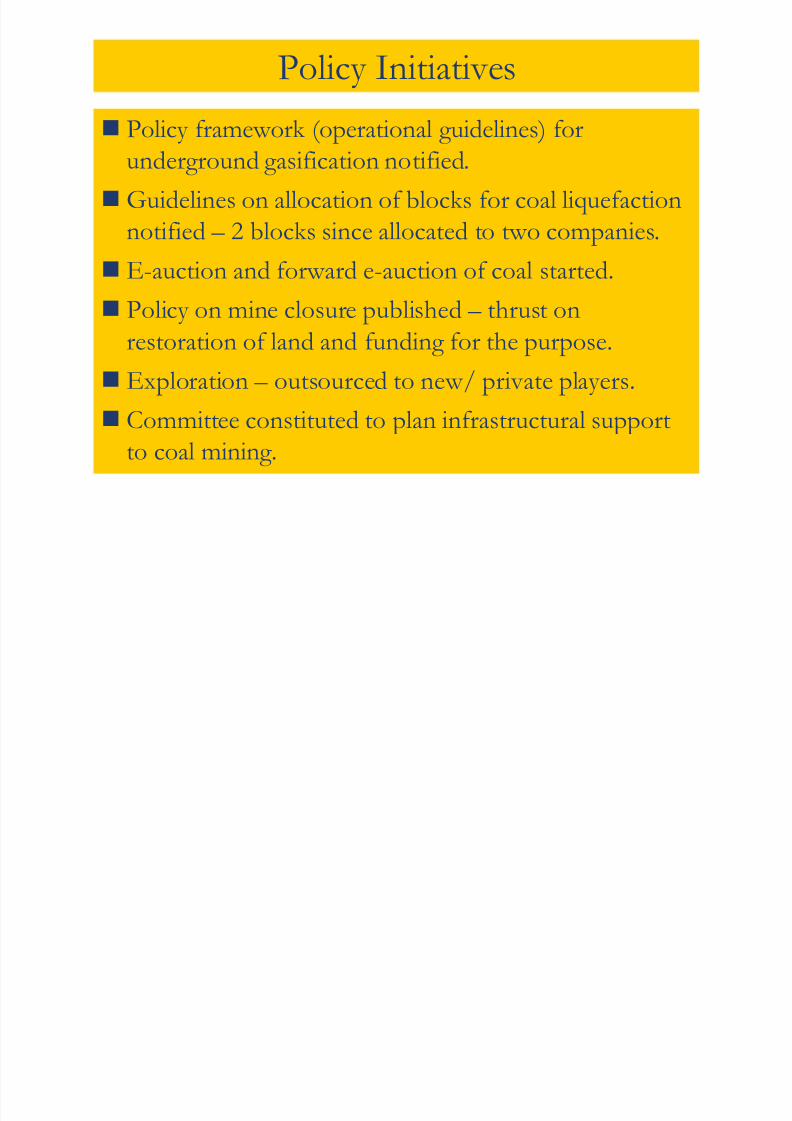

Policy Initiatives

nPolicy framework (operational guidelines) forunderground gasification notified.

nGuidelines on allocation of blocks for coal liquefactionnotified – 2 blocks since allocated to two companies.

nE-auction and forward e-auction of coal started.

n Policy on mine closure published – thrust on

restoration of land and funding for the purpose.

n Exploration – outsourced to new/ private players.

n Committee constituted to plan infrastructural supportto coal mining.

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 22/23

Policy Challenges

n

Opening up of sector – removal of entry barriers :Group of Ministers constituted.

n Independent Regulator – draft Bill (legislation) circula-ted for inter-Ministerial consultation.

n Competitive bidding for grant of concessions – a Bill

(legislation) introduced in the Parliament.n Listing of coal PSEs/ SOEs – for better corporate

governance and market discipline.

n Land use regulation – entire coal bearing area to be

mapped, regulation of use for other purposes.nNew statute on land acquisition, resettlement & rehab.

7/31/2019 Coal Demand and Supply

http://slidepdf.com/reader/full/coal-demand-and-supply 23/23

Thank You!

23