co-operatives in modern times

TRANSCRIPT

Wiebe Draijer 5 July 2018

Co-operatives in Modern Times Some contemplations

Content

1. Global snapshot and prospects

2. European co-operative banks

3. Rabobank

2

Some astonishing facts and figures……

• Over 1.2 billion people are members of a co-operative

• Co-operatives provide employment for or supports the

livelihood of 280 million people globally

• UN estimates that there are 2.5 million co-operatives around

the world

• About 10% of working population works in or through co-

operatives

• There are three times as many member owners of co-

operatives as individual shareholders worldwide

• In 2016 the largest 300 coops had a combined annual turnover

of over US$ 2.2 trillion (equals GDP of France)

• Over 1,400 coops have a turnover of US$ 100m+

3

0%

10%

20%

30%

40%

50%

60%

70%

80%

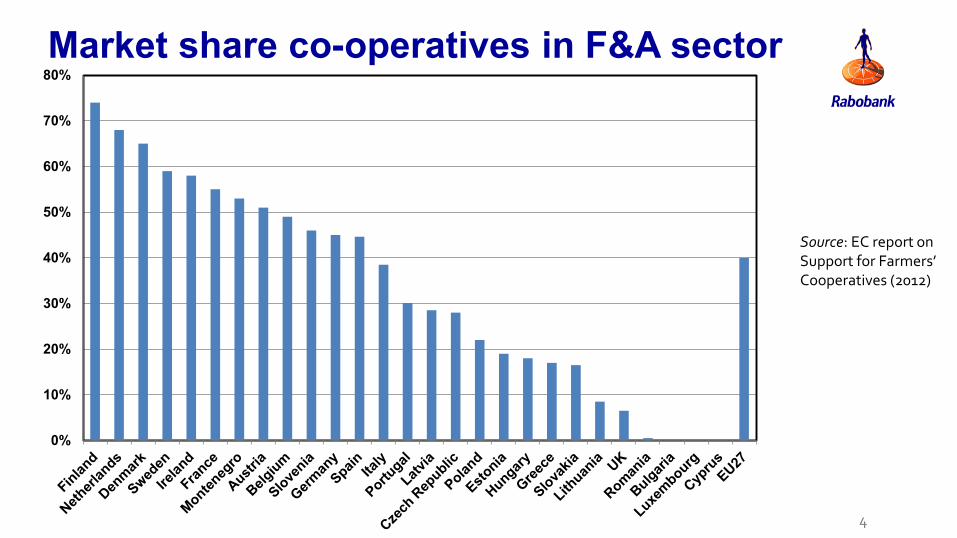

Market share co-operatives in F&A sector

4

Source: EC report on Support for Farmers’ Cooperatives (2012)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1949 1953 1957 1961 1965 1969 1973 1977 1981 1985 1989 1993 1997 2001 2005 2009 2013

Total Agriculture Local Rabobanks and mutual insurers Energy

Evolution of active co-operatives in the Netherlands

Source: own calculations based on

data of Statistics Bureau and

National Co-operative Council

5

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

1949 1953 1957 1961 1965 1969 1973 1977 1981 1985 1989 1993 1997 2001 2005 2009 2013

Total Agriculture Local Rabobanks and mutual insurers Energy

Evolution of active co-operatives in the Netherlands

Source: own calculations based on

data of Statistics Bureau and

National Co-operative Council

6

Important reasons for increasing global popularity of co-operative organisational form

• Observed resilience of coops during and after Great

Financial Crisis

• High (youth) unemployment and new forms of flexible

employment (e.g. self-employed workers)

• Withdrawing government (in combination with ageing

population in EU)

• Policy support (e.g. ‘Social Economy’ in EU)

• Betrayed trust in institutions, professionals, market

forces, scale increase, Europe,…..

• People’s initiatives are taken away by the market,

government and professionals (i.e. ‘democratic deficit’)

• Imminent or existing exclusion or ‘unmet’ needs in the

broadest sense of the word

7

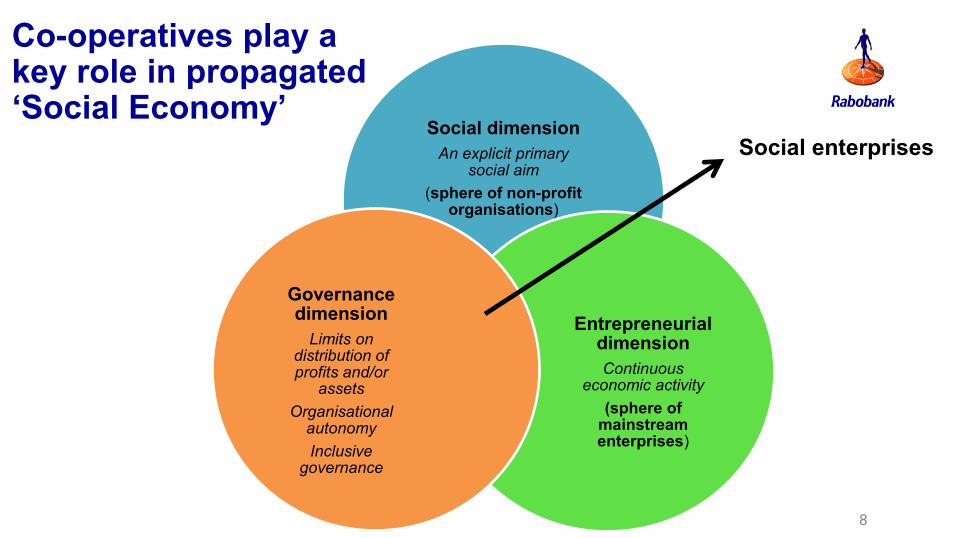

Social dimension

An explicit primary social aim

(sphere of non-profit organisations)

Entrepreneurial dimension

Continuous economic activity

(sphere of mainstream enterprises)

Governance dimension

Limits on distribution of profits and/or

assets

Organisational autonomy

Inclusive governance

Co-operatives play a key role in propagated ‘Social Economy’

Social enterprises

8

Hugh potential for all types of co-operatives

Source: Global Findex database (2014)

9

Part II: European co-operative banking groups

10 10

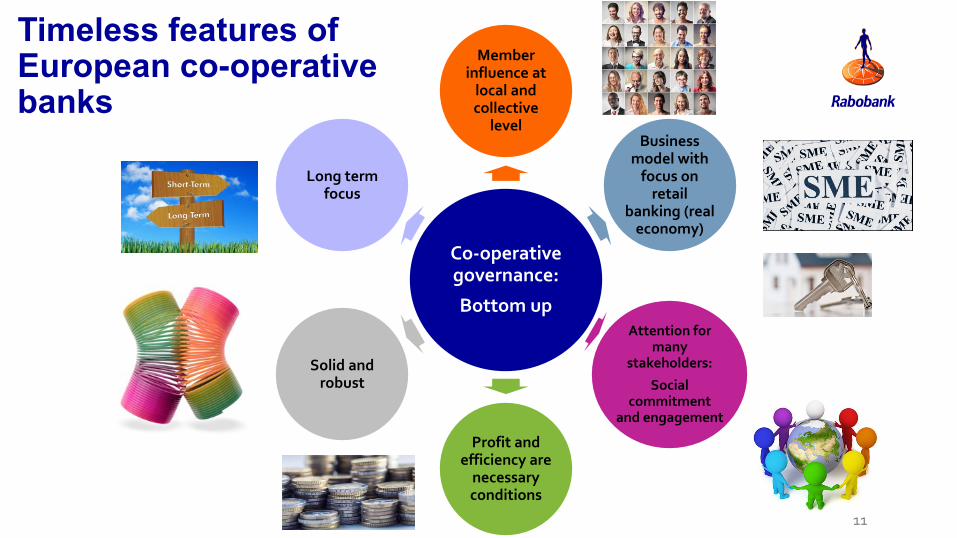

Timeless features of European co-operative banks

Co-operative governance:

Bottom up

Member influence at

local and collective

level Business

model with focus on

retail banking (real

economy)

Attention for many

stakeholders:

Social commitment

and engagement

Profit and efficiency are

necessary conditions

Solid and robust

Long term focus

11

12 12

Communalities and differences between co-operative banks

Members and member-population ratio

0

3

6

9

12

15

18

21

24

27

0

10,000,000

20,000,000

30,000,000

40,000,000

50,000,000

60,000,000

70,000,000

80,000,000

90,000,000

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Ra

tio

Nu

mb

er

Members (left scale) Member to population ratio 13

Loan and deposit growth (2011 = 100)

14

90.0

95.0

100.0

105.0

110.0

115.0

120.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

2011 2012 2013 2014 2015 2016

Ind

ex

Ind

ex

Loans co-operative banks Loans entire banking sector

Deposits co-operative banks Deposits entire banking sector

Co-operative banks: at the service of their members and society

• Long and rich history

• Long-term orientation as opposed to short-termism

• Frequent adaptations of governance and strategy in response to or

in anticipation of many changes in society, technology, etcetera.

• Opportunities

– Social goals and agenda (sustainable development of local territories)

– Participation in local networks and communities

– Commitment and dedication to serve the real economy (with focus on

private households, SMEs and agricultural sector)

• Challenges

– Digitalisation and virtualisation

– Constant adjustments in regulatory and supervisory framework

– A new risk: compliance cost risk

• Contribute to diversity – and hence systemic stability – in banking

15

Part III: Strategic developments at Rabobank

Profile of Rabobank

• Simplified, focused top structure

• Dedicated Fintech & Development team

• Centralised Portfolio Management unit

• Shared back-offices

• Integration of FGH Bank into Rabobank; non-core CRE portfolio managed separately

Organisational changes support our strategy

A+/Stable/A-1

Aa2/Negative/P-1

AA-/Stable/F1+

AA/Stable/R-1(high)

Ratings unchanged and at a high level in 2017

One Rabobank as the basis

Market shares 2017 2016

Mortgages 22% 21%

Savings 34% 34%

Trade, Industry & Services (TIS) 39% 41%

Food & Agri 86% 84%

Commanding domestic market shares

New governance: • One legal entity: local Rabobanks + central organisation • One banking license • One balance sheet

New governance: • One legal entity: local Rabobanks + central organisation • One banking license • One balance sheet

Active in 40 countries 8.5 million customers worldwide

7.3 million local Rabobank customers 1.9 million members

Specialised Rabobank subsidiaries

17

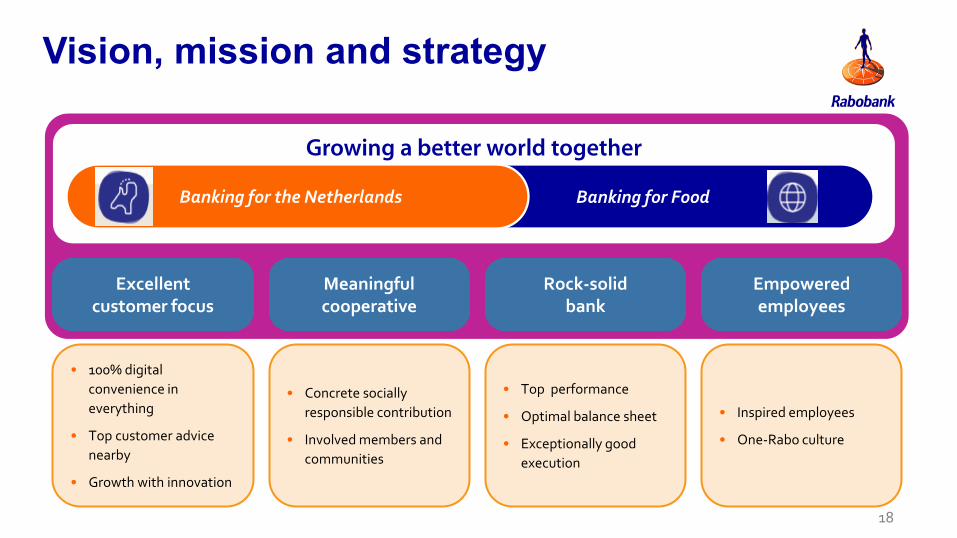

Vision, mission and strategy

Growing a better world together

Excellent customer focus

Excellent customer focus

• Top performance

• Optimal balance sheet

• Exceptionally good

execution

• Concrete socially

responsible contribution

• Involved members and

communities

• Inspired employees

• One-Rabo culture

• 100% digital

convenience in

everything

• Top customer advice

nearby

• Growth with innovation

Banking for Food Banking for the Netherlands

Meaningful cooperative Meaningful cooperative

Rock-solid bank

Rock-solid bank

Empowered employees

Empowered employees

18

Main outcomes of governance revision

Better cooperative

Enhanced member influence on Rabobank's strategic course and identity

Increased transparency in roles and responsibilities in organisation

Increased distinctiveness, enhanced visibility and participation in local communities

Streamlined consultation structure

Better bank

Annual accounts and P&L reflect solidity of Rabobank Group

Full and prompt compliance with new regulatory, supervisory, and resolution requirements in the future

More efficient and effective internal processes due to abolition of delegated supervision

Improved cost efficiency

19

± 100

Elect

Supervise local bank

Employer’s role

Chairman is member

of GMC • Approval of

decisions by MB

• Amendment of

statutes Local

authorisations and

responsibilities

Appoint

Bank Managing Board ultimately responsible for local banks and all subsidiaries

Members’

Department A

Members’

Council A

Local

Supervisory

Body A

1.9 million members

Members’

Department B

Members’

Council B

Local

Supervisory

Body B

Members’

Department C

Members’

Council C

Local

Supervisory

Body C

Members’

Department D

Members’

Council D

Local

Supervisory

Body D

Accountable

Local bank A Local bank B Local bank C Local bank D

Appoint and

supervise

MB

Supervisory

Board

Ac

co

un

tab

le

Ap

po

int

General

Members’

Council

Main internal governance relationships

20

Banking for Food Today, Rabobank has large food & agriculture portfolios all over the world

US & Can

€ 20,1 bln.

S. Am

€ 7,8 bln.

Europe

€ 11,2 bln.

NL & Afr.

€ 35,6 bln.

Asia

€ 5,1 bln.

Aus & NZ

€ 18,2 bln.

North

Americas

36%

11%

Netherlands

21%

8%

5%

19% Asia

Europe

South

Americas

Aus. & NZ

21

Thank you for your attention