clsa asean forum 2011 deepak sarup, cfo - siam ... trade finance, corporate finance and corporate...

TRANSCRIPT

INVESTOR PRESENTATION

CLSA ASEAN FORUM 2011

Deepak Sarup, CFO10th February 2011

Investor Relations | CLSA ASEAN Forum | February 2011

I. Review of Results – 2010

II. Future Positioning

III. 2011 Targets

2

AGENDA

IMPORTANT DISCLAIMER:

Information contained in this document has been prepared from several sources and the Bank cannot confirm, in all cases, the accuracy and completeness of such data, particularly where sourced from outside the Bank. In addition, any forward looking statements are subject to change as a result of market conditions and the final result may be different to that indicated. The Bank makes no representation or warranty of any type whatsoever on the accuracy or completion of the information contained herein.

Pages

3-15

17-27

29

Investor Relations | CLSA ASEAN Forum | February 2011

Profitability

ROE

ROA

NIMs

Loan Growth

Total Loans (yoy)

Wholesale

SME

Retail

Cost and Income

Non-NII Growth (yoy)

Fee income Growth (yoy)

Cost to Income

NPLs (gross)

Branches/ATMs

Capital Adequacy Ratio

1/ Depends on the interest rate environment2/ Stripping out non-recurring. If non-recurring items are included, non-NII growth would be 7.7% in 2009 and 20.6% in 2010, while cost to income ratio would be 51.5% in 2009 and 50.0% in 2010.

1/

2/

2/

ND = Not disclosed

2009 Actual 2010 Target 2010 Actual

2010 Results (Highlights):

• High loan growth of 12.6% yoy was the tangible outcome of the Bank’s market-share growth strategies adopted in early 2010

• Non-NII growth exceeded target driven by solid fee income growth of 19.4% yoy

• Cost to Income ratio lower than target, at 50%

• NPL ratio substantially lower than last year’s and the 2010 target

2010 PERFORMANCE VS. TARGETS Targets and Results

3

On track to target or higher

16.4%

1.7%

3.63%

12.6%

11.0%

14.4%

15.6%

17.7%

19.4%

50.5%

3.25%

1,019/8,006

15.5%

16%+

1.8%

3.5-3.8%

7-10%

8-11%

10-13%

6-10%

17%

15%+

51%

3.90%

1,040/7,700

ND

15.5%

1.6%

3.4%

2.5%

9.4%

-7.0%

3.7%

10.4%

10.9%

50.6%

4.41%

987/7,129

16.5%

2/

2/

Investor Relations | CLSA ASEAN Forum | February 20114

Solid 2010 results with ROE of 16.4% and ROA of 1.7%

High loan growth of 12.6% yoy and improving asset quality

Robust fee income growth of 19.4% yoy

World class level of customer and employee engagement

Market leading positions in key product areas

Improved productivity

Solid capital base

1

KEY ACHIEVEMENTS IN 2010 Achievements

Page

5

6-9

10

11

12

13

14

2

3

4

5

6

7

Investor Relations | CLSA ASEAN Forum | February 20115

Solid ResultsTHE SOLID INCREASE IN NET PROFIT WAS DRIVEN BY MARKET SHARE GROWTH IN ALL SEGMENTS

Net profit increased 16.6% yoy in 2010 and 26.3% yoy in 4Q10

+16.6% yoyNet Profit(Baht Billion)

Core Operating Profit(Baht Billion)

ROE (%)

ROA (%)

Robust profitability with highest ROE and ROA among the big Thai banks

+21.4% yoy

Investor Relations | CLSA ASEAN Forum | February 2011

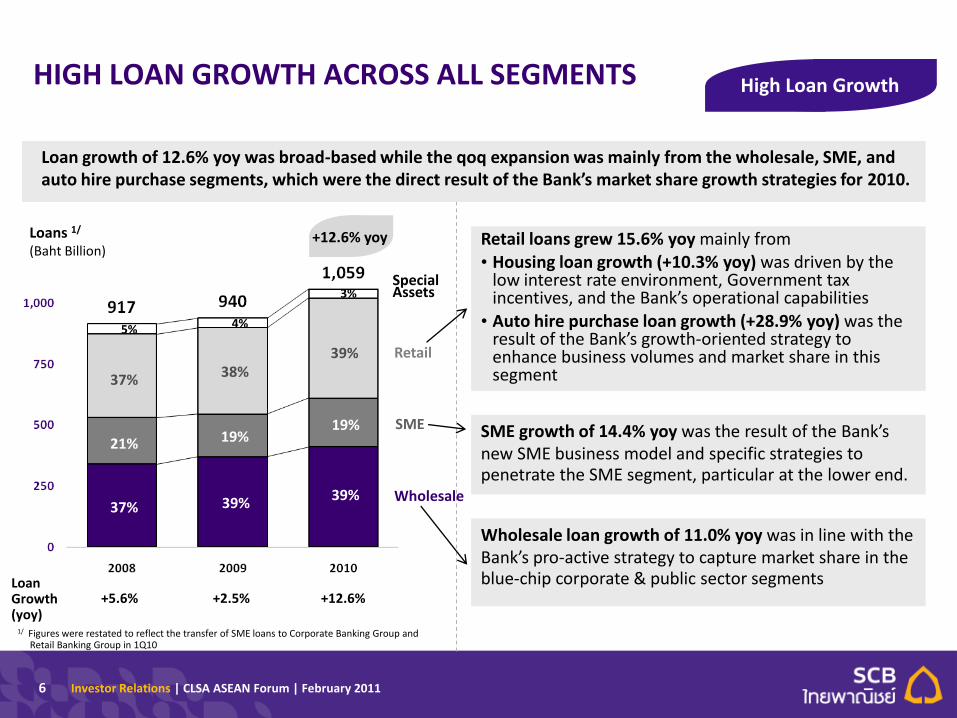

HIGH LOAN GROWTH ACROSS ALL SEGMENTS

6

1/ Figures were restated to reflect the transfer of SME loans to Corporate Banking Group and Retail Banking Group in 1Q10

5% 4%

3%

37%

21%

38%

19%

39%

19%

Loan Growth (yoy)

Loan growth of 12.6% yoy was broad-based while the qoq expansion was mainly from the wholesale, SME, and auto hire purchase segments, which were the direct result of the Bank’s market share growth strategies for 2010.

High Loan Growth

Retail loans grew 15.6% yoy mainly from• Housing loan growth (+10.3% yoy) was driven by the

low interest rate environment, Government tax incentives, and the Bank’s operational capabilities

• Auto hire purchase loan growth (+28.9% yoy) was the result of the Bank’s growth-oriented strategy to enhance business volumes and market share in this segment

Wholesale loan growth of 11.0% yoy was in line with the Bank’s pro-active strategy to capture market share in the blue-chip corporate & public sector segments

SME growth of 14.4% yoy was the result of the Bank’s new SME business model and specific strategies to penetrate the SME segment, particular at the lower end.

Loans 1/

(Baht Billion)

Wholesale

SME

Retail

Special Assets

+12.6% yoy

37% 39% 39%

+5.6% +2.5% +12.6%

Investor Relations | CLSA ASEAN Forum | February 20117

96.9%

93.3%

Loan to Deposit

* BE is included in deposits as they are essentially akin to uninsured deposits

Loan to Deposit + BE *

Loan to Deposit

As the Bank was successful in growing its deposit base through both special deposit campaigns and effective leverage of its strong retail franchise, the LDR was reduced to a comfortable level.

LOAN-TO-DEPOSIT RATIO NOW AT A COMFORTABLE LEVEL

Investor Relations | CLSA ASEAN Forum | February 2011

IMPROVING NII FROM LOAN GROWTH AND BETTER SPREAD

8

Higher NIM

NII Growth (yoy)

The growth in NII yoy was the result of strong loan growth and higher yield compared to 2009.

Net Interest Income(Baht Billion)

Cost of Funds

NIMYield on Earning Assets

NIM excluding Dividend from Vayupak

Yield on Earning Assets, Cost, and NIM

Yield on Loan

Wholesale 4.1% 4.0% 3.9% 4.1% 3.9%

SME 5.2% 5.2% 5.1% 5.1% 5.1%

Retail 6.1% 6.0% 5.8% 5.8% 5.8%

+6.0% yoy

+13.2% -5.2% +6.0%

Investor Relations | CLSA ASEAN Forum | February 2011

IMPROVED ASSET QUALITY HAS LED TO HIGHER RESERVE COVERAGE AND LOWER CREDIT COSTS

NPLs fell to 3.25%, the lowest level in over a decade, due to debt restructuring, NPL sales, and the Bank’s pre-emptive strategies to prevent new NPL formation. The improvement in asset quality was broad-based.

Reserve coverage exceeded 100% for the second quarter in a row, partly as a result of the economic recovery and partly from the strength of the Bank’s credit underwriting practices and risk management framework.

Gross NPLs(Baht Billion)

% NPL

% NPL by Segment

Loan Loss Reserve(Baht Billion)

% LLR/NPL

Improving Asset Quality

1/ Annualized provisions as a % of average loans

Credit Cost 1/

(bps)

9

56 60 47Wholesale 5.5% 3.6% 3.1%

SME 7.3% 8.7% 7.0%

Retail 4.3% 3.9% 2.4%

Investor Relations | CLSA ASEAN Forum | February 2011

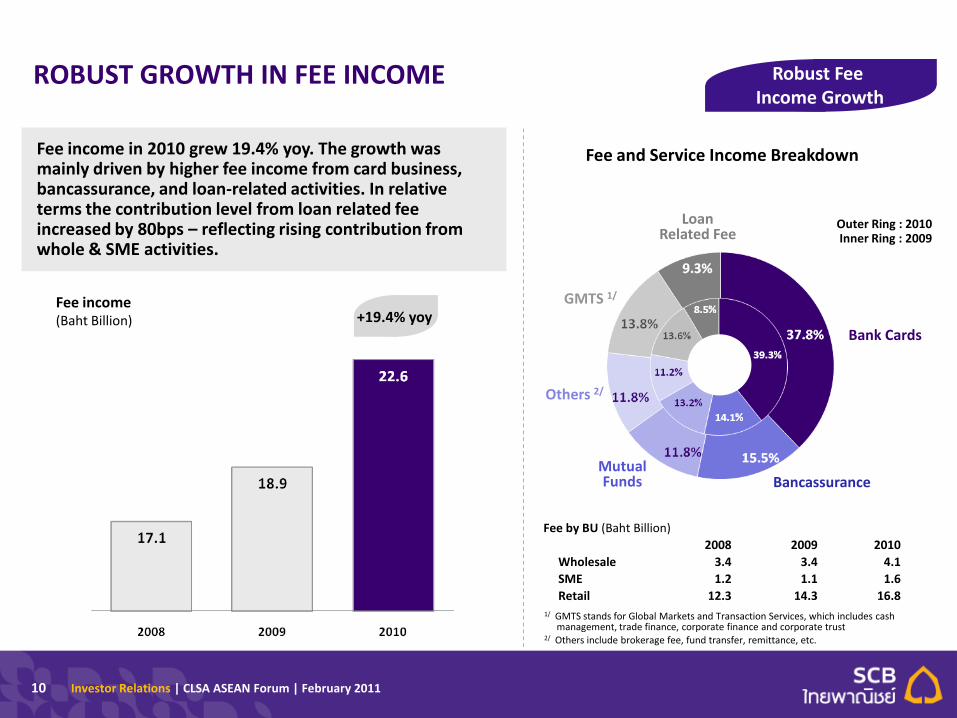

ROBUST GROWTH IN FEE INCOME

10

Fee and Service Income Breakdown

Outer Ring : 2010Inner Ring : 2009

Bank Cards

Loan Related Fee

GMTS 1/

Others 2/

Mutual Funds Bancassurance

Fee income in 2010 grew 19.4% yoy. The growth was mainly driven by higher fee income from card business, bancassurance, and loan-related activities. In relative terms the contribution level from loan related fee increased by 80bps – reflecting rising contribution from whole & SME activities.

1/ GMTS stands for Global Markets and Transaction Services, which includes cash management, trade finance, corporate finance and corporate trust

2/ Others include brokerage fee, fund transfer, remittance, etc.

Robust Fee Income Growth

Fee income(Baht Billion) +19.4% yoy

Fee by BU (Baht Billion)

2008 2009 2010

Wholesale 3.4 3.4 4.1

SME 1.2 1.1 1.6

Retail 12.3 14.3 16.8

Investor Relations | CLSA ASEAN Forum | February 2011

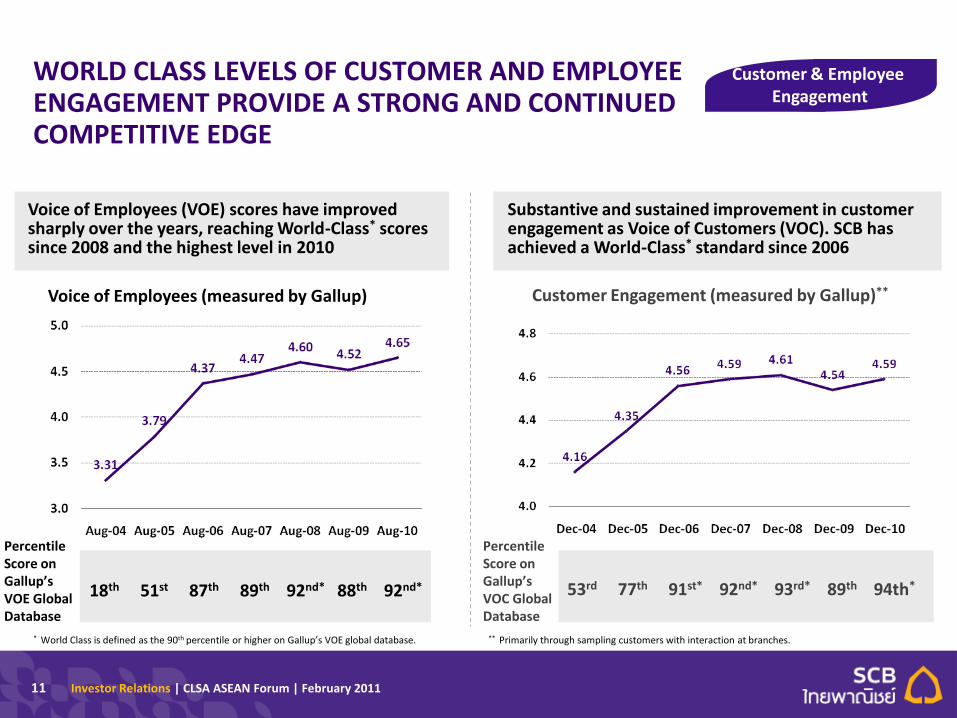

WORLD CLASS LEVELS OF CUSTOMER AND EMPLOYEE ENGAGEMENT PROVIDE A STRONG AND CONTINUED COMPETITIVE EDGE

11

Voice of Employees (VOE) scores have improved sharply over the years, reaching World-Class* scores since 2008 and the highest level in 2010

Customer & Employee Engagement

Voice of Employees (measured by Gallup)

18th 51st 87th 89th 92nd* 88th 92nd*

Customer Engagement (measured by Gallup)**

53rd 77th 91st* 92nd* 93rd* 89th 94th*

* World Class is defined as the 90th percentile or higher on Gallup’s VOE global database.

Substantive and sustained improvement in customer engagement as Voice of Customers (VOC). SCB has achieved a World-Class* standard since 2006

Percentile Score on Gallup’s VOE Global Database

Percentile Score on Gallup’s VOC Global Database

** Primarily through sampling customers with interaction at branches.

Investor Relations | CLSA ASEAN Forum | February 2011

4/ As of Nov-105/ Total life premiums which include individual life & credit life (new premium & renewals)

RETAIL BANKING - KEY PRODUCTS

12

Housing Loans 2/

(Baht Billion)

1/ Market share for mortgage portfolio comprised of housing loans and consumer loans2/ Classified by product, including NPLs

Total Bancassurance Premiums 5/

(Baht Billion)

Mortgage Lending: Maintained dominance with approximately 29% market share 1/ among commercial banks

Bancassurance: #1 with 25% market share 4/

Credit Card Spending(Baht Billion)

Mutual Fund Assets under Management (AUM)(Baht Billion)

Credit Card: #1 in terms of total card spending with 16.5% market share 3/

Mutual Funds: #2 with 25% market share

3/ As of Nov-10

Leading Positions in Retail Products

+11.4% yoy +12.3% yoy

+27.4% yoy +13.5% yoy

Investor Relations | CLSA ASEAN Forum | February 2011

2010 COST-TO-INCOME REMAINED BELOW FULL-YEAR TARGET

13

Operating Expense(Baht Billion)

1/ Including non-recurring items, if non-recurring items are excluded, cost-to-income ratio would be 50.6% in 2009 and 50.5% in 2010.

% Cost-to-Income Ratio 1/

Operating expenses rose 8.6% yoy reflecting seasonal costs in the last quarter. Nevertheless, given strong total income, cost to income ratio fell to 50.0% from the 51.5% in 2009.

Improved Productivity

+8.6% yoy

Investor Relations | CLSA ASEAN Forum | February 201114

STRONG CAPITAL BASE TO SUPPORT GROWTH AND EMERGING REGULATORY REQUIREMENTS

Capital Adequacy RatioBasel II - Standardized Approach

Tier I

Tier II

Solid Capital Base

15.5%15.2%16.5%

Should the 2H10 net profit be taken into consideration, CAR would have been 16.7%, while Tier I would have been 12.8%.

Investor Relations | CLSA ASEAN Forum | February 2011

SCB RETAINS A STRONG MARKET POSITION AMONGST THE BIG THAI BANKS

2010 ROE 2010 ROA

Strongest Profitability with Highest ROE and ROA

Capital Adequacy Ratio

Solid CAR (as at Dec 31, 2010)

# of Branches # of ATMs

Largest Branch & ATM Networks (as at Dec 31 ,2010)

Market Capitalization(Baht Billion)

Highest Market Cap (as at Dec 31, 2010)

15

Competitive Positioning

Investor Relations | CLSA ASEAN Forum | February 2011

I. Review of Results – 2010

II. Future Positioning

III. 2011 Targets

16

AGENDA

Pages

3-15

17-27

29

Investor Relations | CLSA ASEAN Forum | February 2011

Comment and outlookKey drivers

* %YOY except for policy rate (% per annum) and exchange rate (THB/USD).** Based on information from commercial banks financial reports, as of December 2010

Source: SCB EIC analysis

Expect Thai GDP growth of 4.0-5.0% in 2011 on back of global economic slowdownGDP growth

Expect hikes to be front-loaded and paused by THB appreciation

Policy rate(end period)

Expect average crude oil price (WTI) of around USD 93 /bbl in 2011, rising 18%YOY, compared to 27%YOY in 2010. Inflation to accelerate on back of rising prices of palm oil and food

Headline inflation

2010

7.5-8.0

Estimates (%)*

3.3

2.00

THB/USD(end period)30.1

Expect THB to appreciate around 5% on back of USD weakening, especially against major Asian currencies

17

4.0-5.0

3.5

3.25

28.5

2011

MacroMACRO TRENDS FORECAST FOR 2011

Expect growth of 5-6% in 2011 due to policy rate hike

Deposit growth (sector-wide)

11.5**

5**Expect milder growth as compared to loan growth mainly on back of decreasing current account surplus

5.0 - 6.0

2.0 - 3.0

Loan growth(sector-wide)

Investor Relations | CLSA ASEAN Forum | February 2011

LONG-TERM POSITIONING

SUPPORTED BY:

A dominant brand - 1st Thai Bank (established in 1906) Large and growing customer base (11 million customers) Largest distribution network (1,019 branches & 8,006

ATMs*) Commitment of major shareholders Full franchise licenses (Securities, Asset Management,

Life and Non-Life Insurance)

STRATEGIC THRUST: To be the PREMIER UNIVERSAL BANK in Thailand through adopting a strong focus on key markets or segments and by rapidly responding to evolving customer needs, better leveraging SCB franchise strengths, and utilizing the implemented market leading infrastructure and systems.

The Bank of Choice

To be the Premier

Universal Bank in Thailand

Vision

Mission

* As at 30 December 2010

Positioning

18

Investor Relations | CLSA ASEAN Forum | February 2011

Banking Sector Loan Growth

Market-share growth strategy in three areas (i.e. Wholesale, Auto Loans, and SME) will be key drivers of the bank’s growth in the near future

Lending Outlook

19

Loan Growth (% yoy)

SCB Loan Growth

The Bank adopted a cautious stance in lending since early 2008, beginning with the U.S. subprime crisis and the financial turmoil in late 2008

10-12%

5-6%

SCB LOAN GROWTH HAS TENDED TO BE WELL AHEAD OF THE MARKET, EXCEPT DURING THE RECENT GLOBAL CRISIS WHEN THE BANK ADOPTED A MORE CAUTIOUS STANCE

Investor Relations | CLSA ASEAN Forum | February 2011

% Non-NII to Total Revenue

24%25%

30%

10%

20%

30%

2009 2010 Medium to Long Term

% Fee income contribution from Wholesale and SME as a % of total fee income

Given the Bank’s strong focus to increase its fee income, the Bank has a medium-to-long term objective of non-interest income accounting for more than 40% of total income and the aggregate fee income contribution from Wholesale Banking and Business Banking (SME) to increase from the current level to above 30% of fee income

Fee OutlookSTRONG FOCUS ON NON-NII SHOULD YIELD BETTER RESULTS

20

Investor Relations | CLSA ASEAN Forum | February 2011

KEY ‘DELTA GROWTH’ DRIVERS OVER THE NEXT 3 YEARS

Major current initiatives to obtain market share growth, over and above business as usual:

1) WHOLESALE - Expansion of market share, particularly in terms of fee income from the blue-chip and the public sector enterprises segment

2) SME - Gain momentum from new SME business model, centered around gaining market share in small and medium scale businesses

3) AUTO LOANS - Expansion of market share in the auto hire-purchase segment and aim to be the #1 originator within 2-3 years

Key Growth Segments

21

Investor Relations | CLSA ASEAN Forum | February 2011

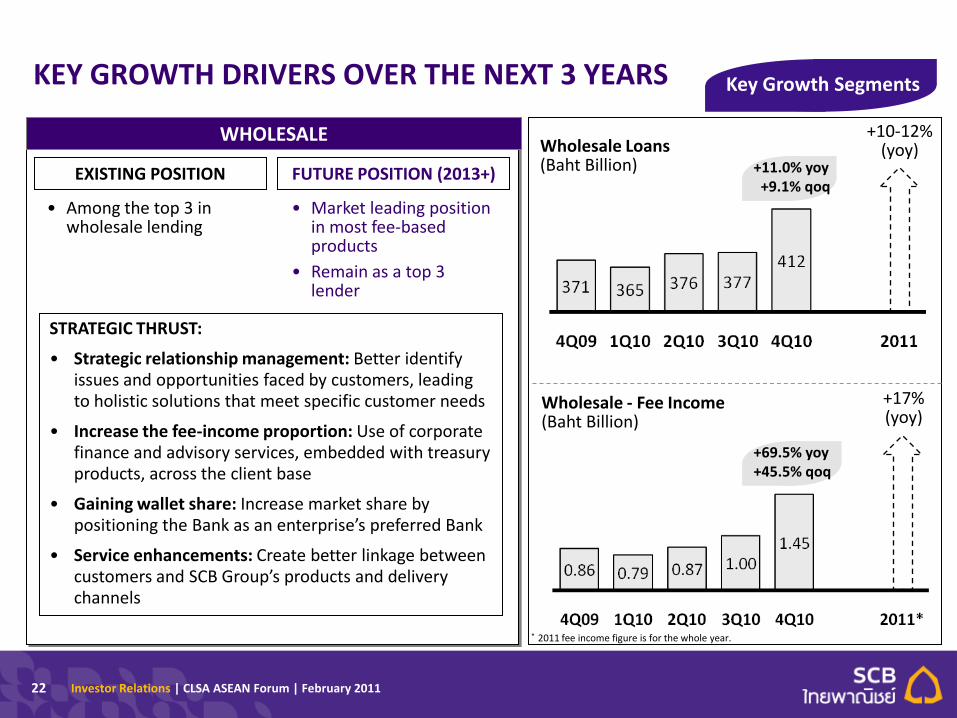

KEY GROWTH DRIVERS OVER THE NEXT 3 YEARS

STRATEGIC THRUST:

• Strategic relationship management: Better identify issues and opportunities faced by customers, leading to holistic solutions that meet specific customer needs

• Increase the fee-income proportion: Use of corporate finance and advisory services, embedded with treasury products, across the client base

• Gaining wallet share: Increase market share by positioning the Bank as an enterprise’s preferred Bank

• Service enhancements: Create better linkage between customers and SCB Group’s products and delivery channels

WHOLESALE

EXISTING POSITION FUTURE POSITION (2013+)

• Among the top 3 in wholesale lending

• Market leading position in most fee-based products

• Remain as a top 3 lender

Wholesale Loans(Baht Billion)

Wholesale - Fee Income(Baht Billion)

+10-12%(yoy)

+17%(yoy)

Key Growth Segments

+11.0% yoy+9.1% qoq

+69.5% yoy+45.5% qoq

* 2011 fee income figure is for the whole year.

22

Investor Relations | CLSA ASEAN Forum | February 2011

KEY GROWTH DRIVERS OVER THE NEXT 3 YEARS

STRATEGIC THRUST:

• SCB’s SME Brand: Strengthen the “SCB SME” brand by anchoring marketing activities around core SME products

• Footprint: Expand nationwide footprint through establishing Business Relationship Centers in new areas

• Products: Introduce new products to expand the customer base and generate higher margins. Grow fee-based income, by offering product packages and solutions

SME

EXISTING POSITION FUTURE POSITION (2013+)

• Ranked #6 in the market with Bt 183bn loans1/

• Ranked #3 in the market

• Increase the SME loan volume by about Bt 150 bn over the next three years, with substantial uplift in fee income

SME Loans(Baht Billion)

SME - Fee Income(Baht Billion)

+20%(yoy)

+30%(yoy)

1/ Outstanding at end 2010 will be around Baht 150 billion after the last tranche of commercial loans (Bt 40bn) is transferred to commercial (wholesale bank)

+14.4% yoy+9.0% qoq

+70.2% yoy+19.0% qoq

* 2011 fee income figure is for the whole year.

23

Key Growth Segments

Investor Relations | CLSA ASEAN Forum | February 2011

KEY GROWTH DRIVERS OVER THE NEXT 3 YEARS

STRATEGIC THRUST:

• Strengthen relationships with existing dealers: Using key account management programs

• Footprint: Develop relationships with new dealers

• Distribution network: Leverage the Bank’s comprehensive retail banking platform to introduce new products such as “My Car, My Cash”

AUTO LOANS

EXISTING POSITION FUTURE POSITION (2013+)

• Ranked #1 in Mortgage, Credit Cards, Bancassurance

• Maintain existing #1 position in key products

• #1 in terms of loan origination for Auto loans

SCB-Auto Loans (Baht Billion)

SCB-Monthly Booking of New Auto Loan Contracts(Units x 1,000)

+25%(yoy)

2010

+50%(yoy)

+28.9% yoy+8.8% qoq

24

Key Growth Segments

Investor Relations | CLSA ASEAN Forum | February 2011

SHARPER, MORE AGILE WHOLESALE BANKING GROUP TO RESPOND TO SCALE AND COMPLEXITY CHALLENGES

WHOLESALE BANKING GROUP

Corporate Banking(60+ groups, 7 industries)

Commercial Banking(2,000+ groups, 8 industries)

Corporate Finance

Capital Markets

Market Sales & Trading

Global Transaction

ServicesLoans

Co

vera

ge

Pro

du

cts

Reorganization

25

Investor Relations | CLSA ASEAN Forum | February 2011

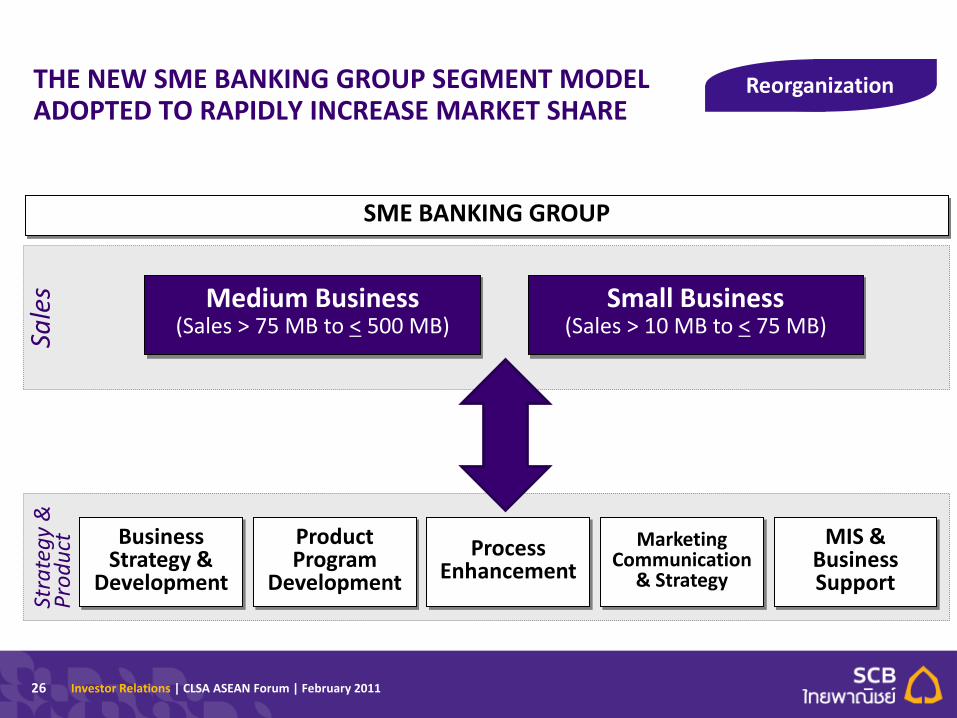

THE NEW SME BANKING GROUP SEGMENT MODEL ADOPTED TO RAPIDLY INCREASE MARKET SHARE

SME BANKING GROUP

Medium Business(Sales > 75 MB to < 500 MB)

Small Business(Sales > 10 MB to < 75 MB)

Business Strategy &

Development

Product Program

Development

Process Enhancement

Marketing Communication

& Strategy

MIS & Business Support

Sale

sSt

rate

gy

&

Pro

du

ct

26

Reorganization

Investor Relations | CLSA ASEAN Forum | February 2011

Wealth Management

Lines of Business

Lending Lines of Business

Shared Channelsfor Origination

& Servicing

• Deposit

• Asset Management

• Bancassurance

• Private Banking

• Mortgage

• Auto Finance

• Credit Card

• S/SME

Branch

E-Channels

AN INVIGORATED RETAIL BANKING GROUP POSITIONED TO GROW OUT FROM ITS CORE AND CAPITALIZE ON EMERGING OPPORTUNITIES

Direct Sales

Customer Segment

Management

& Retail Marketing

IndependentCredit

Risk Function

27

Reorganization

Investor Relations | CLSA ASEAN Forum | February 2011

I. Review of Results – 2010

II. Future Positioning

III. 2011 Targets

28

AGENDA

Pages

3-15

17-27

29

Investor Relations | CLSA ASEAN Forum | February 2011

2011 ASPIRATIONS

29

Targets and Results

2009 Actual 2010 Target 2010 Actual

Profitability

ROE

ROA

NIMs

Loan Growth

Total Loans (yoy)

Cost and Income

Non-NII Growth (yoy)

Fee income Growth (yoy)

Cost to Income

NPLs (gross)

Branches/ATMs

Capital Adequacy Ratio

15.5%

1.6%

3.4%

2.5%

10.4%

10.9%

50.6%

4.41%

987/7,129

16.5%

16%+

1.8%

3.5-3.8%

7-10%

17%

15%+

51%

3.90%

1,040/7,700

ND

16.4%

1.7%

3.63%

12.6%

17.7%

19.4%

50.5%

3.25%

1,019/8,006

15.5%

1/

2/

2/

2011 Target

16-18%

1.8-2.0%

3.6%+

10-12%

ND

15%+

50%

2.9%

1,050+/9,250+

ND

1/

On track to target or higher ND = Not disclosed

1/ Depends on the interest rate environment2/ Stripping out non-recurring. If non-recurring items are included, non-NII growth would be 7.7% in 2009 and 20.6% in 2010, while cost to income ratio would be 51.5% in 2009 and 50.0% in 2010.

2/

2/