cit group inc. - iis windows serverlibrary.corporate-ir.net/.../091505lehmanfsccitgroup.pdfcit group...

TRANSCRIPT

1

CIT Group Inc.

Lehman Financial Services ConferenceSeptember 15, 2005

2

NoticesForward Looking StatementsCertain statements made in these presentations that are not historical facts may constitute "forward-looking" statements under the Private Securities Litigation Reform Act of 1995, including those that are signified by words such as "anticipate", "believe", "expect", "estimate", “target”, and similar expressions. These forward-looking statements reflect the current views of CIT and its management and are subject to risks, uncertainties, and changes in circumstances. CIT's actual results or performance may differ materially from those expressed in, or implied by, such forward-looking statements. Factors that could affect actual results and performance include, but are not limited to, potential changes in interest rates, competitive factors and general economic conditions, changes in funding markets, industry cycles and trends, uncertainties associated with risk management, risks associated with residual value of leased equipment, and other factors described in our Form 10-K for the year ended December 31, 2004 and our Form 10-Q for the quarter ended June 30, 2005. CIT does not undertake to update any forward-looking statements.

Non-GAAP Financial MeasuresThese presentations include certain non-GAAP financial measures, as defined in Regulation G promulgated by the Securities and Exchange Commission. Any references to non-GAAP financial measures are intended to provide additional information and insight into CIT's financial condition and operating results. These measures are not in accordance with, or a substitute for, GAAP and may be different from or inconsistent with non-GAAP financial measures used by other companies. For a reconciliation of these non-GAAP measures to GAAP, please refer to the appendix within this presentation or access the reconciliations through CIT's Investor Relations website at [email protected].

Data as of June 30, 2005 unless otherwise noted.

3

Corporate Profile

$9 BillionMarket

Capitalization

Global Servicing Capabilities

Predominately a Secured Lender

97 YearOperating History

Managed Assets$58 Billion

Premium Brand

Diverse Portfolio

3

4

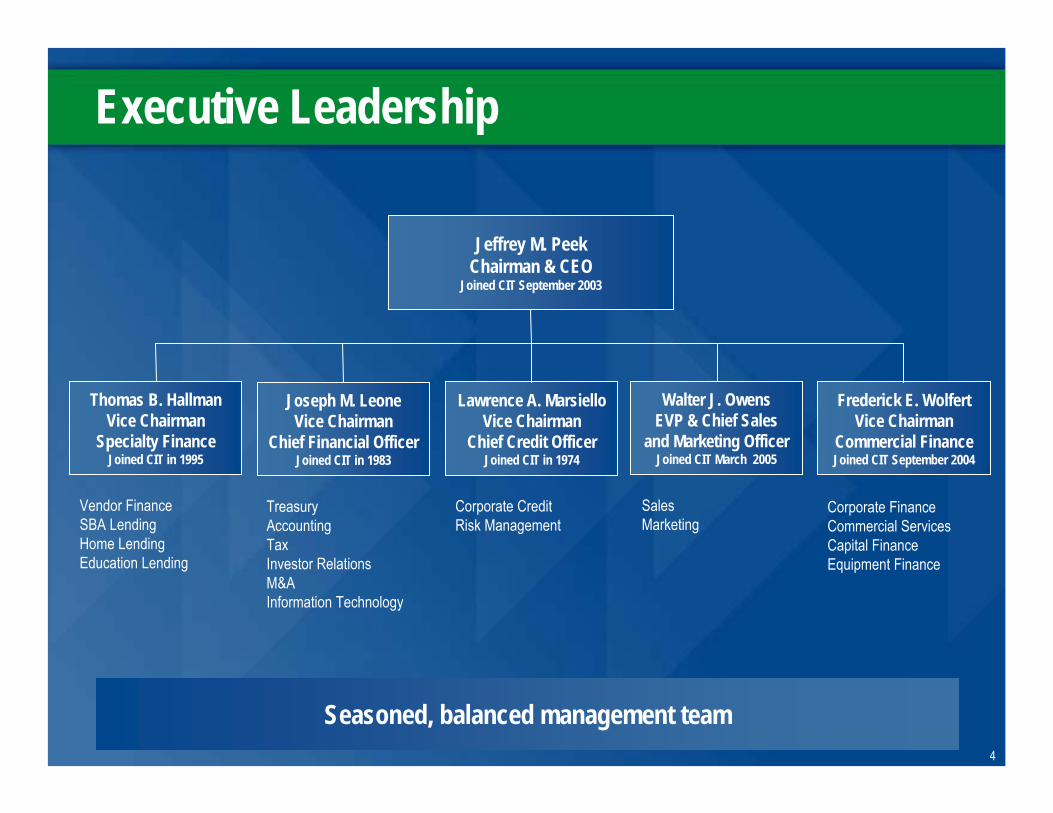

Executive Leadership

Lawrence A. MarsielloVice Chairman

Chief Credit OfficerJoined CIT in 1974

Corporate CreditRisk Management

Joseph M. LeoneVice Chairman

Chief Financial OfficerJoined CIT in 1983

TreasuryAccountingTaxInvestor RelationsM&AInformation Technology

Thomas B. HallmanVice Chairman

Specialty FinanceJoined CIT in 1995

Vendor FinanceSBA LendingHome LendingEducation Lending

Frederick E. WolfertVice Chairman

Commercial FinanceJoined CIT September 2004

Corporate FinanceCommercial ServicesCapital FinanceEquipment Finance

Walter J. OwensEVP & Chief Sales

and Marketing OfficerJoined CIT March 2005

SalesMarketing

Seasoned, balanced management team

Jeffrey M. PeekChairman & CEO

Joined CIT September 2003

5

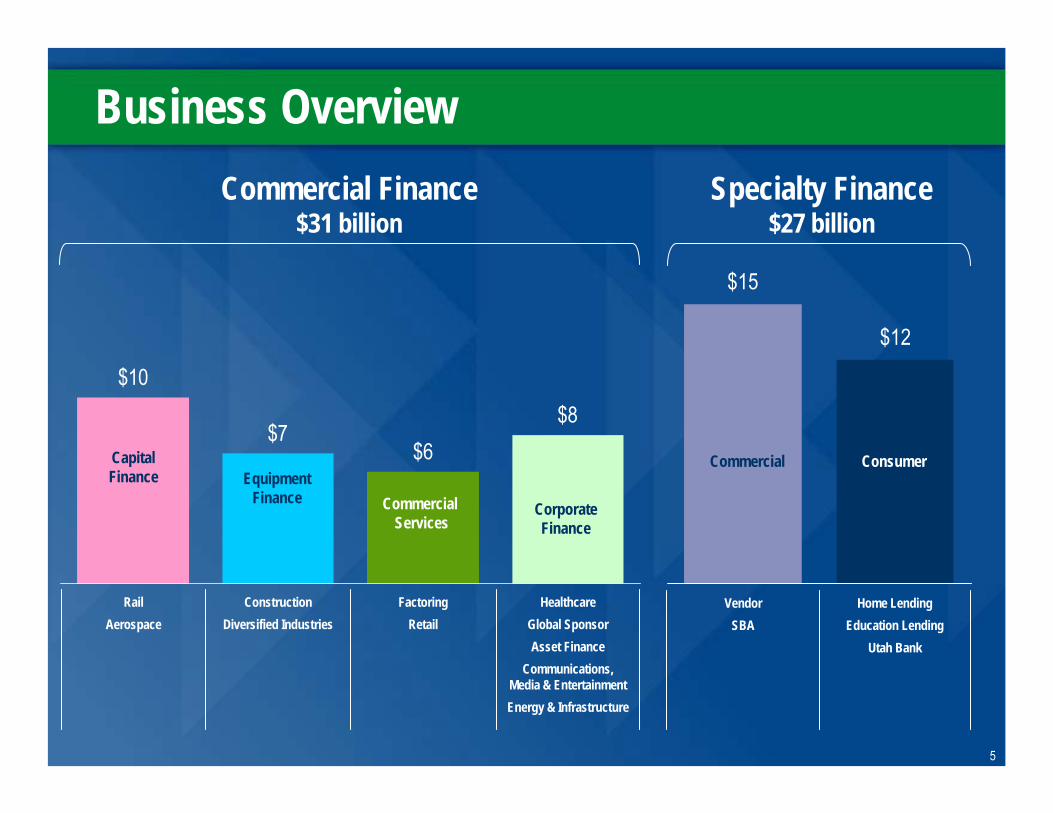

HealthcareGlobal Sponsor Asset Finance

Communications, Media & EntertainmentEnergy & Infrastructure

FactoringRetail

ConstructionDiversified Industries

RailAerospace

Business Overview

$10

$7$6

$8

$15

$12

Home LendingEducation Lending

Utah Bank

VendorSBA

Commercial Services

Corporate Finance

Capital Finance Equipment

Finance

Commercial Consumer

Commercial Finance $31 billion

Specialty Finance $27 billion

6

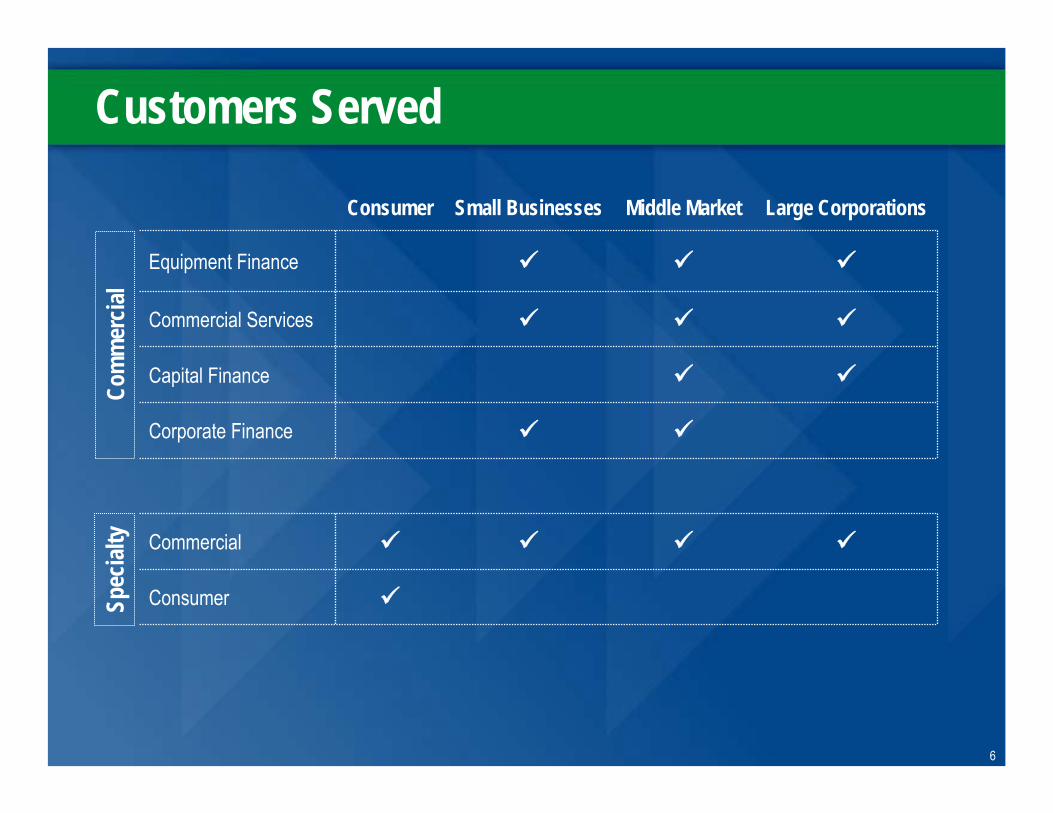

Customers Served

Capital Finance

Commercial

Consumer

Corporate Finance

Commercial Services

Equipment Finance

Large CorporationsMiddle MarketSmall BusinessesConsumer

Com

mer

cial

Spec

ialty

7

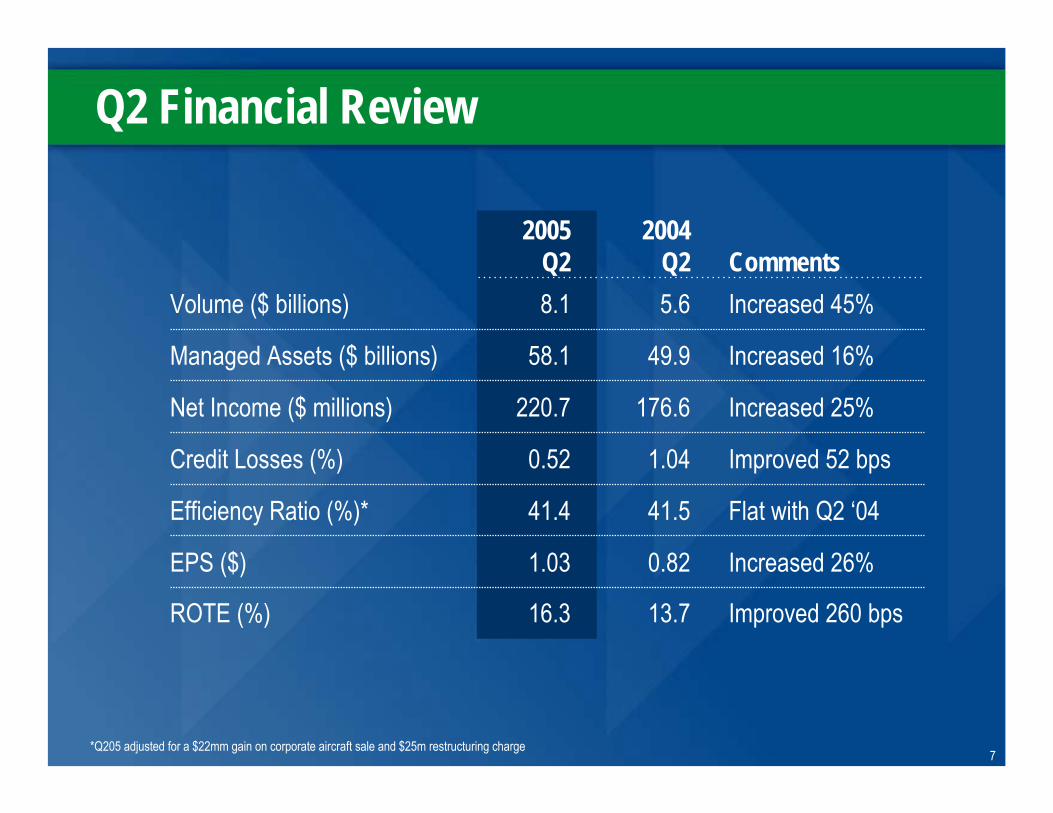

Increased 45%5.68.1Volume ($ billions)

Improved 260 bps

Increased 26%

Flat with Q2 ‘04

Improved 52 bps

Increased 25%

Increased 16%

Comments

41.541.4Efficiency Ratio (%)*

1.040.52Credit Losses (%)

49.958.1Managed Assets ($ billions)

20042005

13.7

0.82

176.6

Q2

16.3

1.03

220.7

Q2

ROTE (%)

EPS ($)

Net Income ($ millions)

Q2 Financial Review

*Q205 adjusted for a $22mm gain on corporate aircraft sale and $25m restructuring charge

8

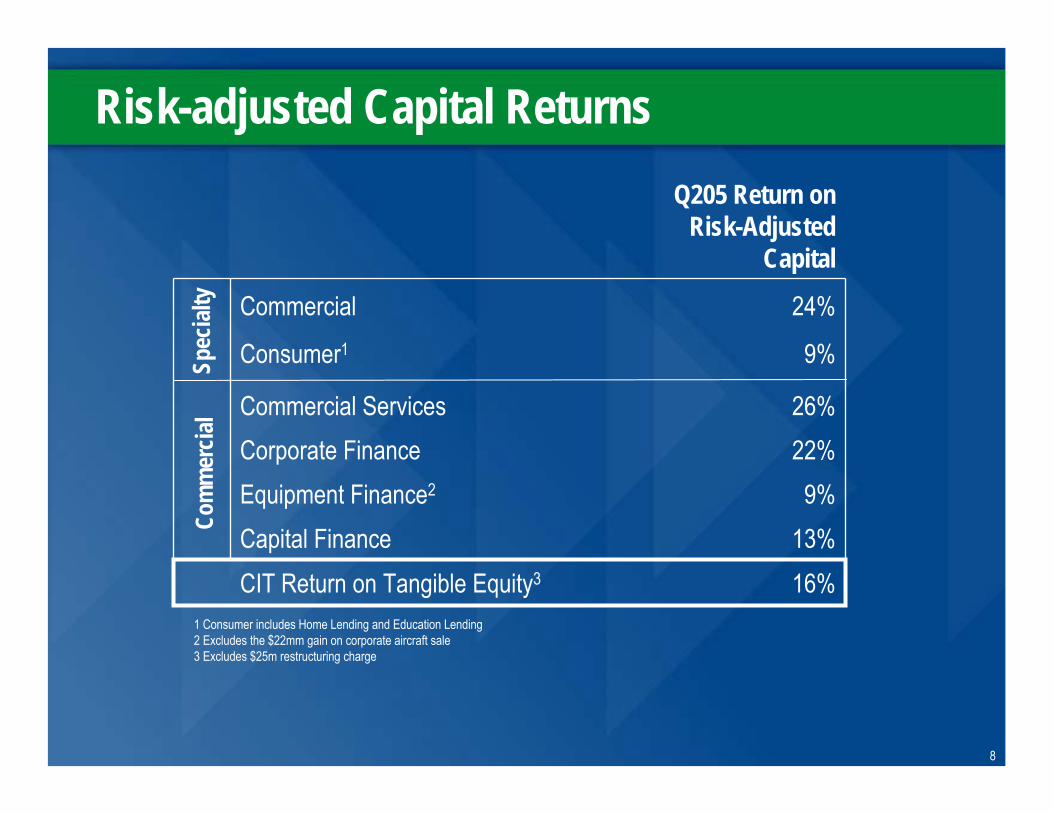

16%CIT Return on Tangible Equity3

13%9%

22%26%

9%

24%

Q205 Return on Risk-Adjusted

Capital

Equipment Finance2

Corporate Finance

Consumer1

Commercial

Capital Finance

Commercial Services

Com

mer

cial

Spec

ialty

Risk-adjusted Capital Returns

1 Consumer includes Home Lending and Education Lending2 Excludes the $22mm gain on corporate aircraft sale3 Excludes $25m restructuring charge

9

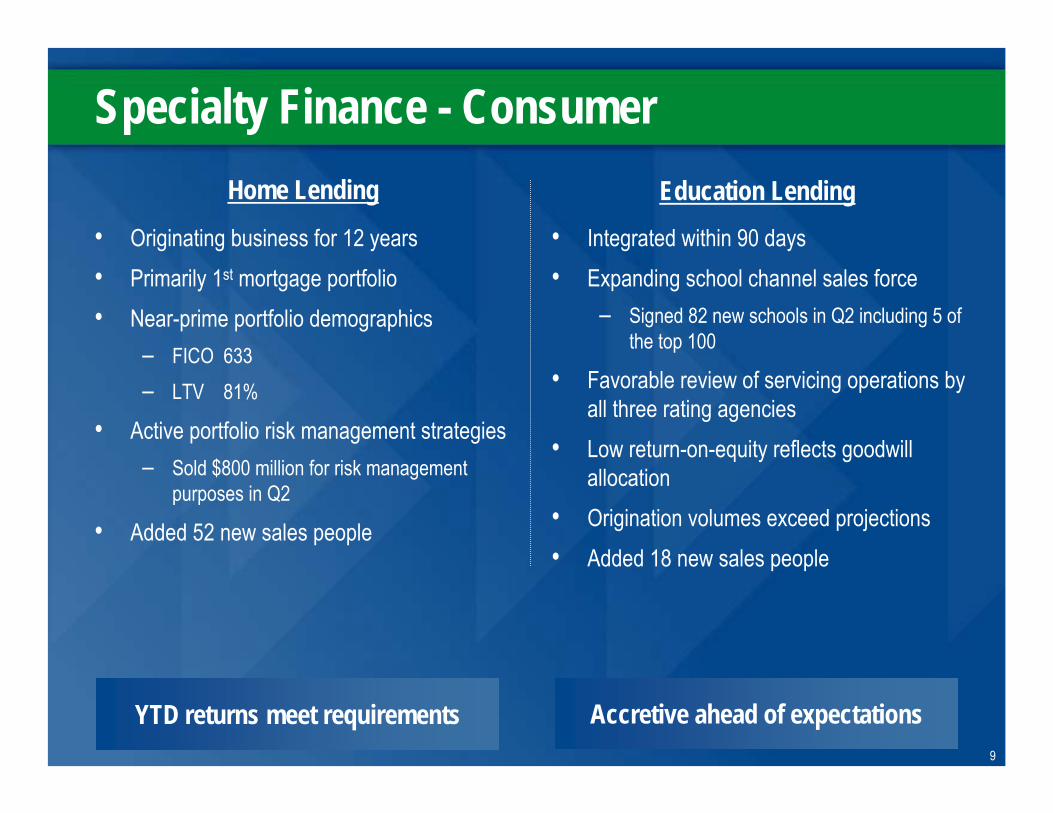

Specialty Finance - Consumer

• Originating business for 12 years• Primarily 1st mortgage portfolio• Near-prime portfolio demographics

– FICO 633– LTV 81%

• Active portfolio risk management strategies– Sold $800 million for risk management

purposes in Q2

• Added 52 new sales people

• Integrated within 90 days• Expanding school channel sales force

– Signed 82 new schools in Q2 including 5 of the top 100

• Favorable review of servicing operations by all three rating agencies

• Low return-on-equity reflects goodwill allocation

• Origination volumes exceed projections• Added 18 new sales people

Home Lending Education Lending

YTD returns meet requirements Accretive ahead of expectations

10

Equipment Finance• Refocus the marketing strategy on the core Construction and Industrial businesses

– Exited Technology Rental Service and Business Aircraft– Transferred Healthcare and Sports & Gaming to Corporate Finance

• Improved credit process– Further automated underwriting process– Reduced reliance on collateral values

• Rationalized expenses– Reduced headcount– Consolidated operation centers

Returns are still below hurdle but up over 200 basis points from a year ago

11

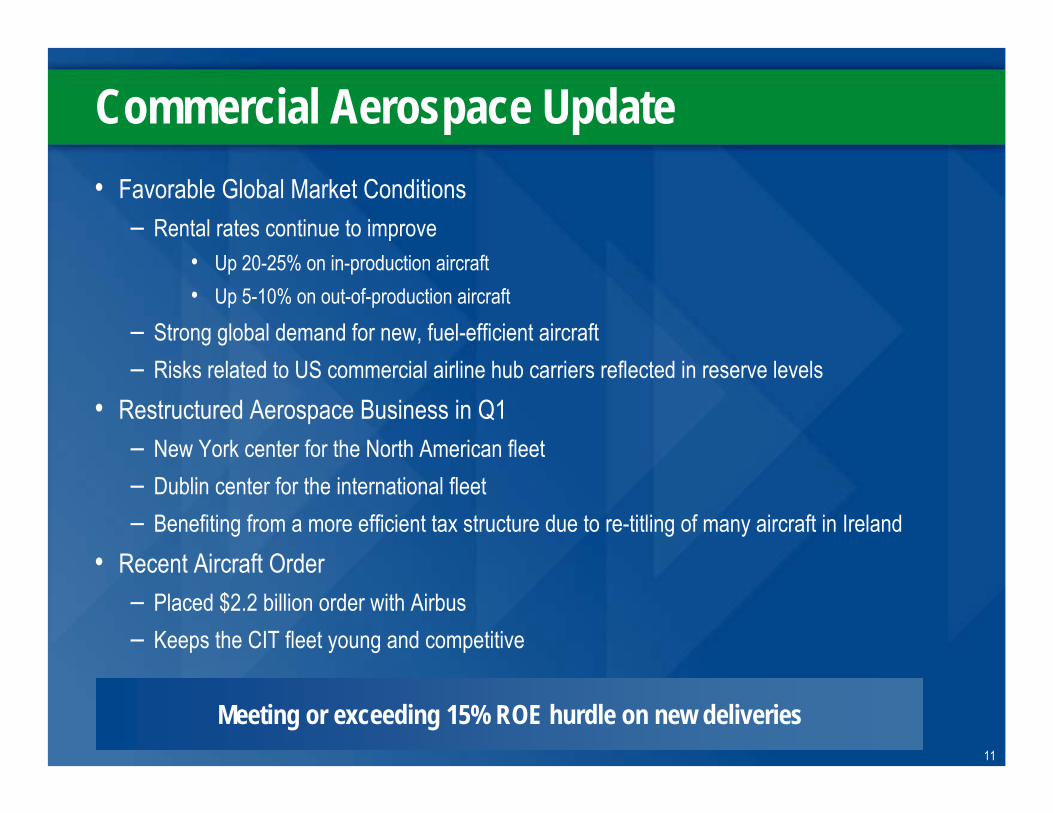

Commercial Aerospace Update• Favorable Global Market Conditions

– Rental rates continue to improve• Up 20-25% on in-production aircraft• Up 5-10% on out-of-production aircraft

– Strong global demand for new, fuel-efficient aircraft– Risks related to US commercial airline hub carriers reflected in reserve levels

• Restructured Aerospace Business in Q1– New York center for the North American fleet– Dublin center for the international fleet– Benefiting from a more efficient tax structure due to re-titling of many aircraft in Ireland

• Recent Aircraft Order– Placed $2.2 billion order with Airbus– Keeps the CIT fleet young and competitive

Meeting or exceeding 15% ROE hurdle on new deliveries

12

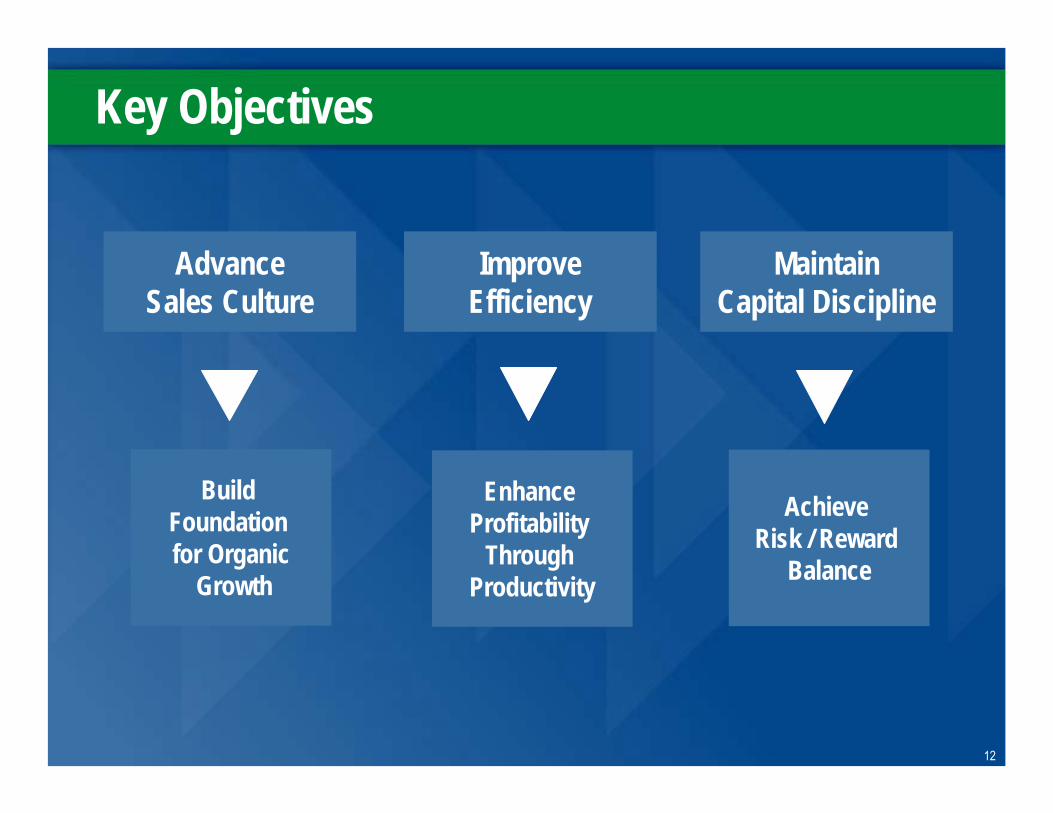

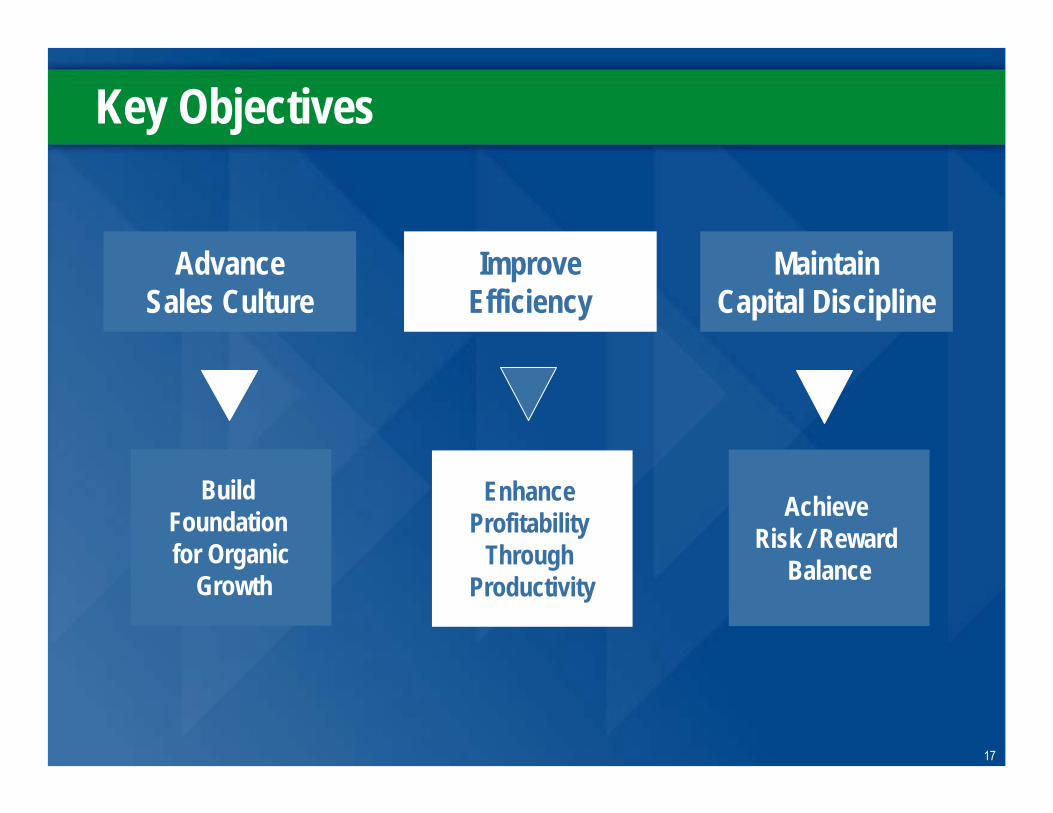

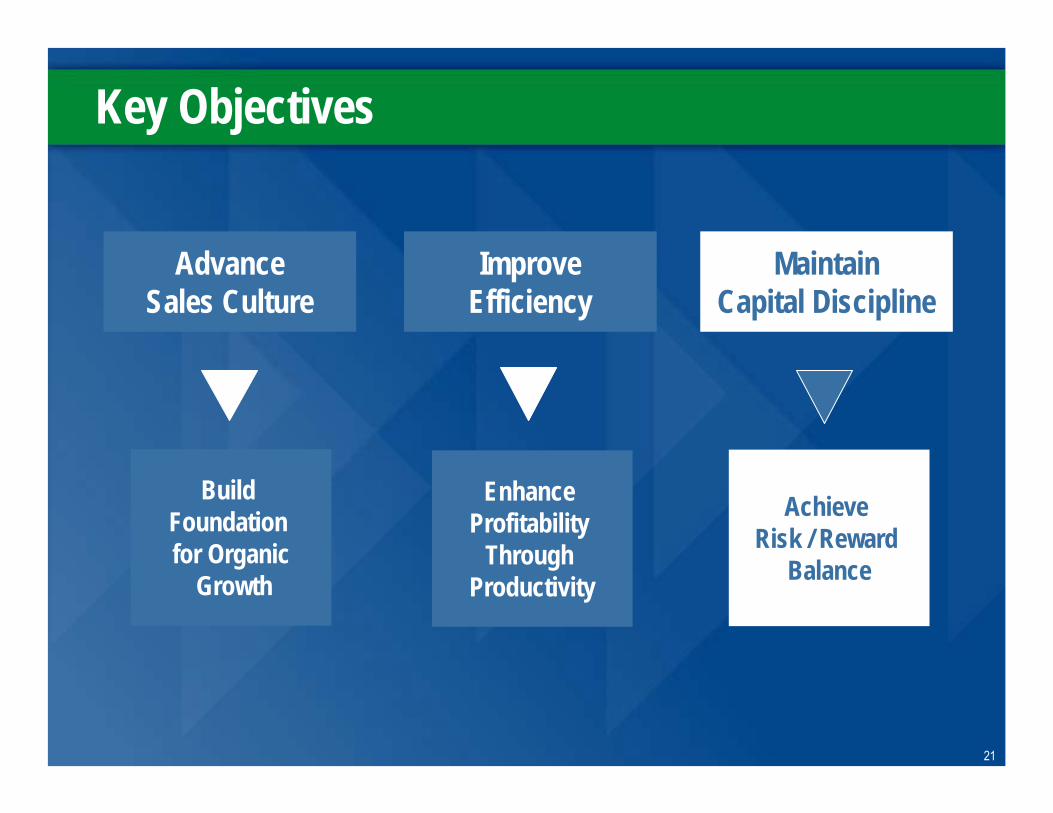

Key Objectives

ImproveEfficiency

MaintainCapital Discipline

Enhance Profitability

Through Productivity

Achieve Risk / Reward

Balance

AdvanceSales Culture

Build Foundation for Organic

Growth

13

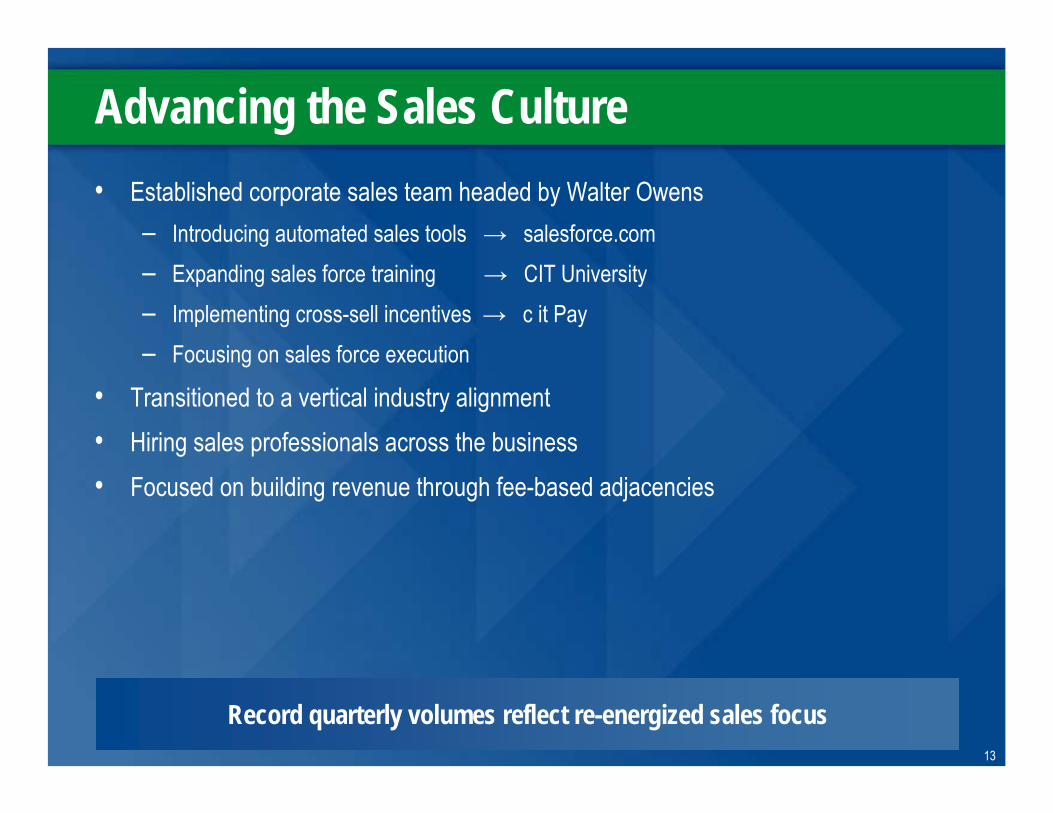

Advancing the Sales Culture• Established corporate sales team headed by Walter Owens

– Introducing automated sales tools → salesforce.com– Expanding sales force training → CIT University– Implementing cross-sell incentives → c it Pay– Focusing on sales force execution

• Transitioned to a vertical industry alignment • Hiring sales professionals across the business• Focused on building revenue through fee-based adjacencies

Record quarterly volumes reflect re-energized sales focus

14

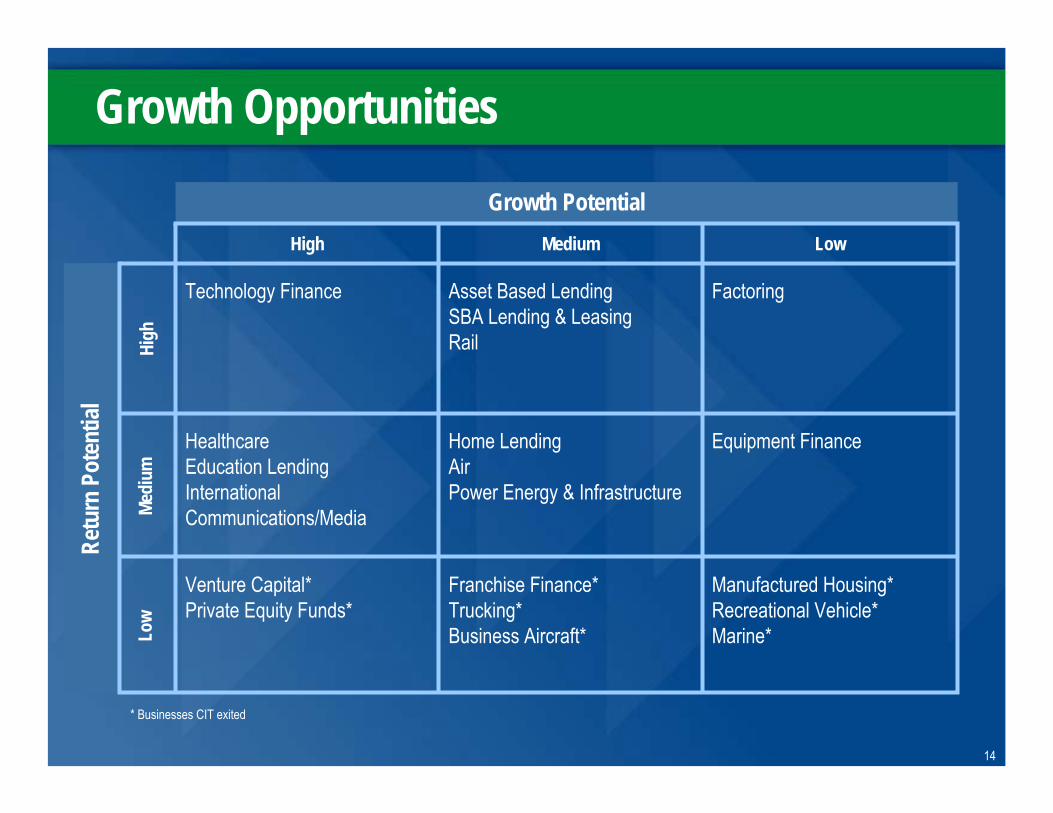

Growth Opportunities

Manufactured Housing*Recreational Vehicle*Marine*

Franchise Finance*Trucking*Business Aircraft*

Venture Capital*Private Equity Funds*

Equipment FinanceHome LendingAirPower Energy & Infrastructure

Healthcare Education LendingInternational Communications/Media

FactoringAsset Based LendingSBA Lending & LeasingRail

Technology Finance

LowMediumHigh

Growth Potential

High

Medi

umLo

w

Retu

rn P

oten

tial

* Businesses CIT exited

15

Healthcare Vertical

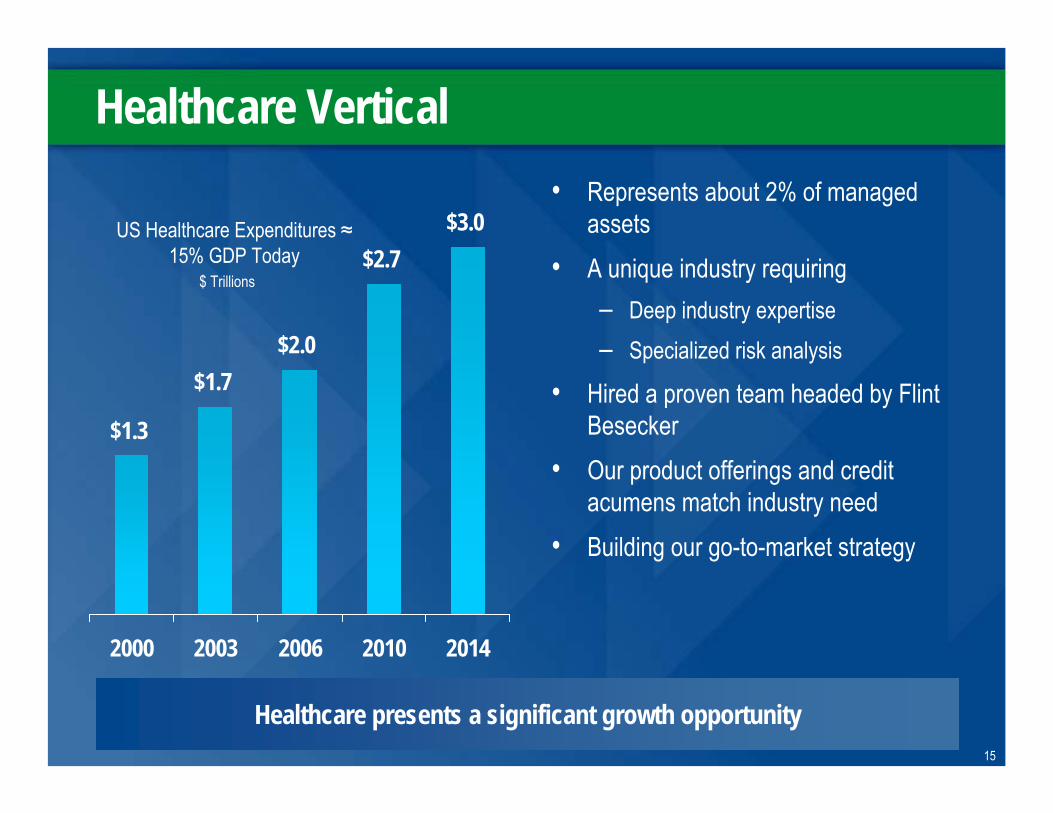

$1.3

$1.7$2.0

$2.7$3.0

2000 2003 2006 2010 2014

• Represents about 2% of managed assets

• A unique industry requiring – Deep industry expertise– Specialized risk analysis

• Hired a proven team headed by Flint Besecker

• Our product offerings and credit acumens match industry need

• Building our go-to-market strategy

Healthcare presents a significant growth opportunity

US Healthcare Expenditures ≈15% GDP Today

$ Trillions

16

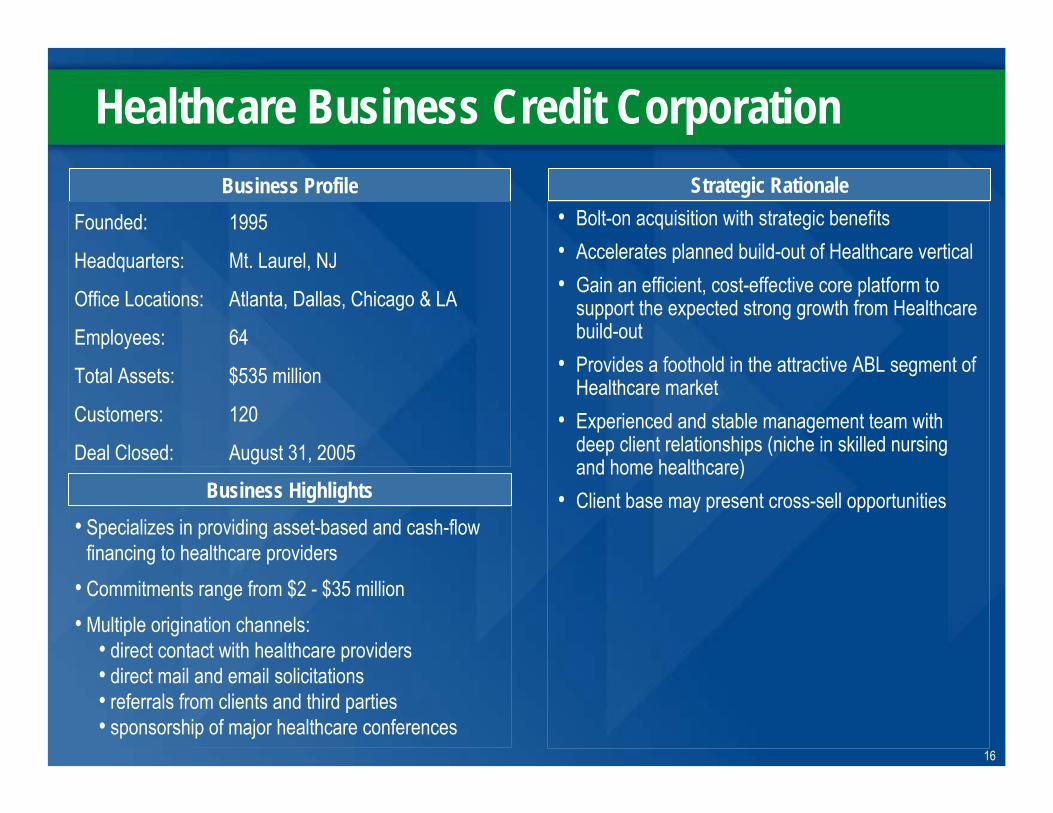

Healthcare Business Credit CorporationBusiness Profile

Founded: 1995

Headquarters: Mt. Laurel, NJ

Office Locations: Atlanta, Dallas, Chicago & LA

Employees: 64

Total Assets: $535 million

Customers: 120

Deal Closed: August 31, 2005

• Specializes in providing asset-based and cash-flow financing to healthcare providers

• Commitments range from $2 - $35 million • Multiple origination channels:

• direct contact with healthcare providers• direct mail and email solicitations• referrals from clients and third parties• sponsorship of major healthcare conferences

• Bolt-on acquisition with strategic benefits• Accelerates planned build-out of Healthcare vertical• Gain an efficient, cost-effective core platform to

support the expected strong growth from Healthcare build-out

• Provides a foothold in the attractive ABL segment of Healthcare market

• Experienced and stable management team with deep client relationships (niche in skilled nursing and home healthcare)

• Client base may present cross-sell opportunities

Strategic Rationale

Business Highlights

17

Key Objectives

ImproveEfficiency

MaintainCapital Discipline

Enhance Profitability

Through Productivity

Achieve Risk / Reward

Balance

AdvanceSales Culture

Build Foundation for Organic

Growth

18

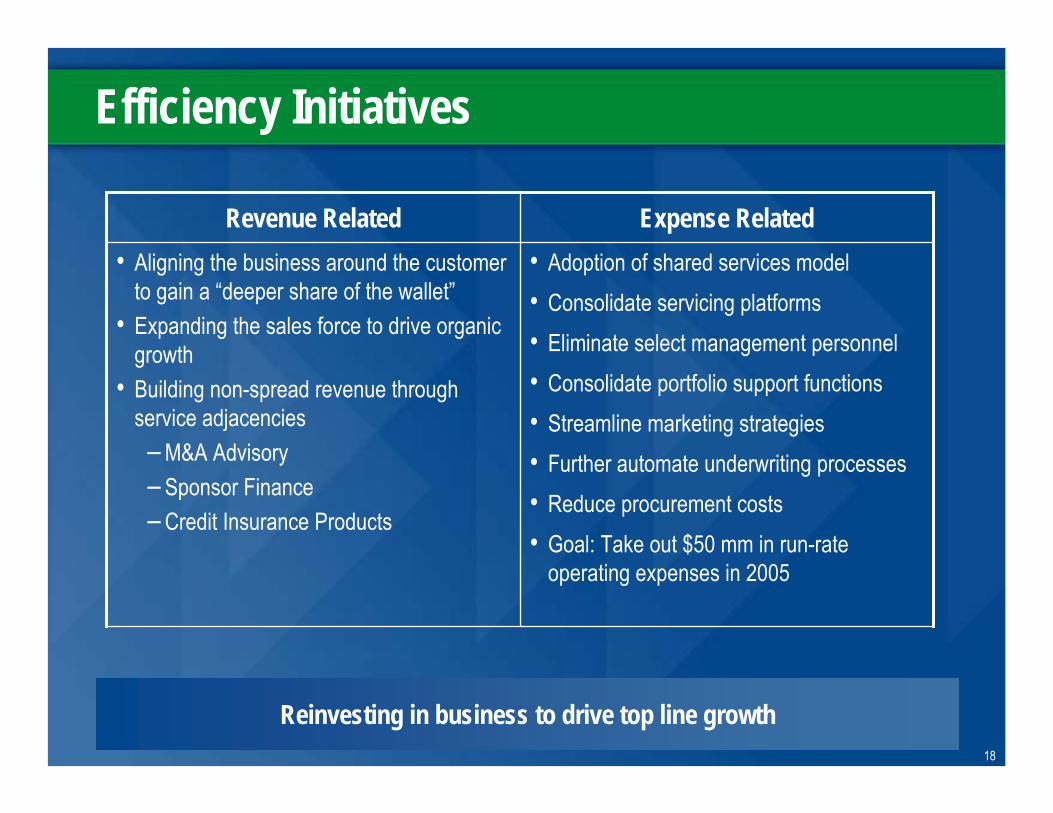

Efficiency Initiatives

• Adoption of shared services model• Consolidate servicing platforms• Eliminate select management personnel• Consolidate portfolio support functions• Streamline marketing strategies• Further automate underwriting processes• Reduce procurement costs• Goal: Take out $50 mm in run-rate

operating expenses in 2005

• Aligning the business around the customer to gain a “deeper share of the wallet”

• Expanding the sales force to drive organic growth

• Building non-spread revenue through service adjacencies– M&A Advisory– Sponsor Finance– Credit Insurance Products

Expense RelatedRevenue Related

Reinvesting in business to drive top line growth

19

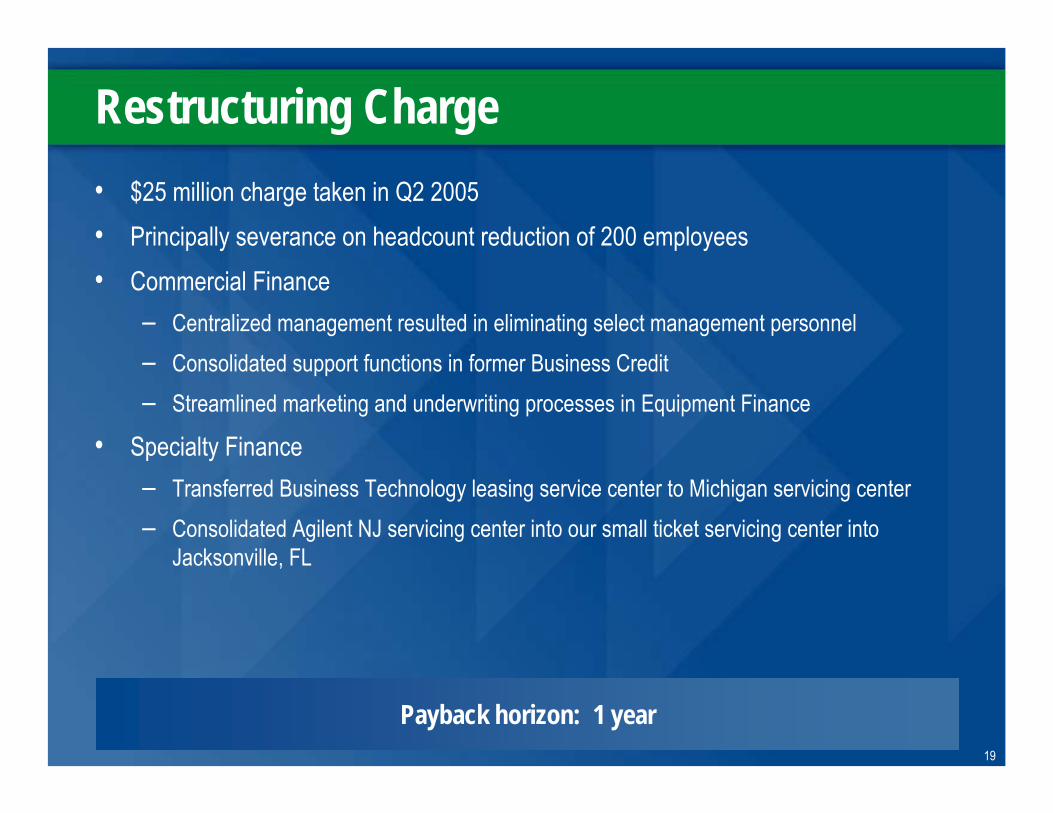

Payback horizon: 1 year

Restructuring Charge• $25 million charge taken in Q2 2005• Principally severance on headcount reduction of 200 employees• Commercial Finance

– Centralized management resulted in eliminating select management personnel– Consolidated support functions in former Business Credit– Streamlined marketing and underwriting processes in Equipment Finance

• Specialty Finance– Transferred Business Technology leasing service center to Michigan servicing center – Consolidated Agilent NJ servicing center into our small ticket servicing center into

Jacksonville, FL

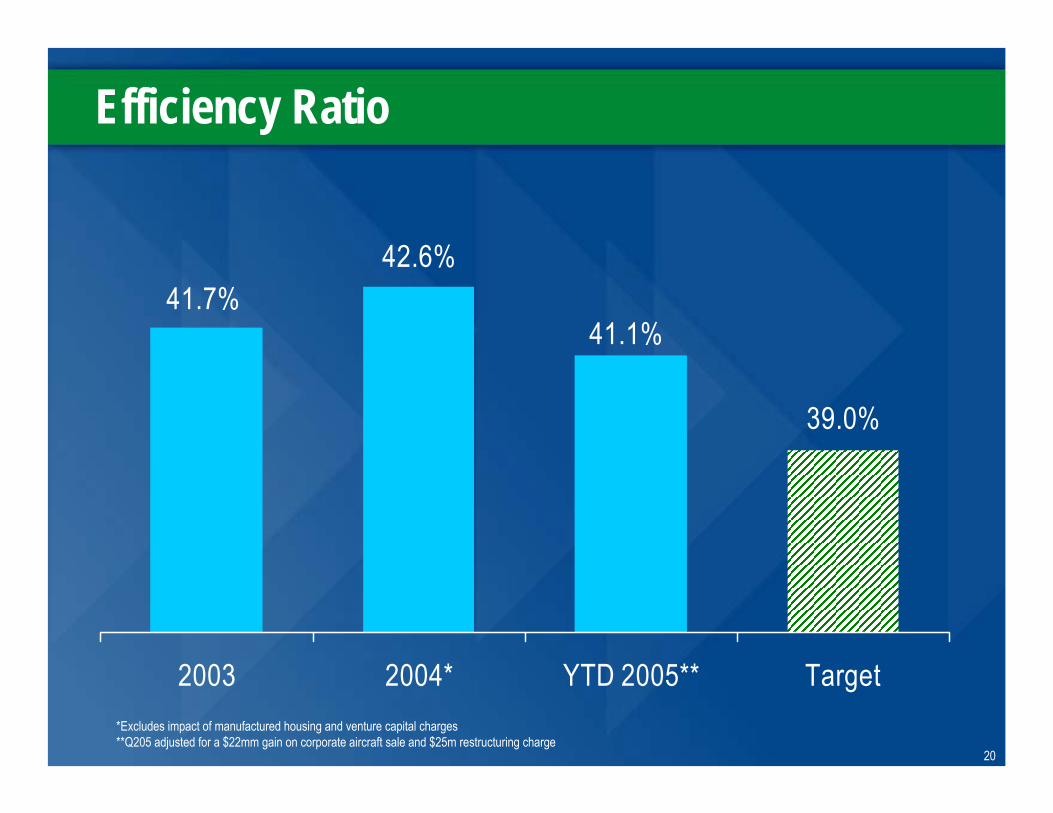

20

39.0%

41.1%

42.6%41.7%

2003 2004* YTD 2005** Target

Efficiency Ratio

*Excludes impact of manufactured housing and venture capital charges**Q205 adjusted for a $22mm gain on corporate aircraft sale and $25m restructuring charge

21

Key Objectives

ImproveEfficiency

MaintainCapital Discipline

Enhance Profitability

Through Productivity

Achieve Risk / Reward

Balance

AdvanceSales Culture

Build Foundation for Organic

Growth

22

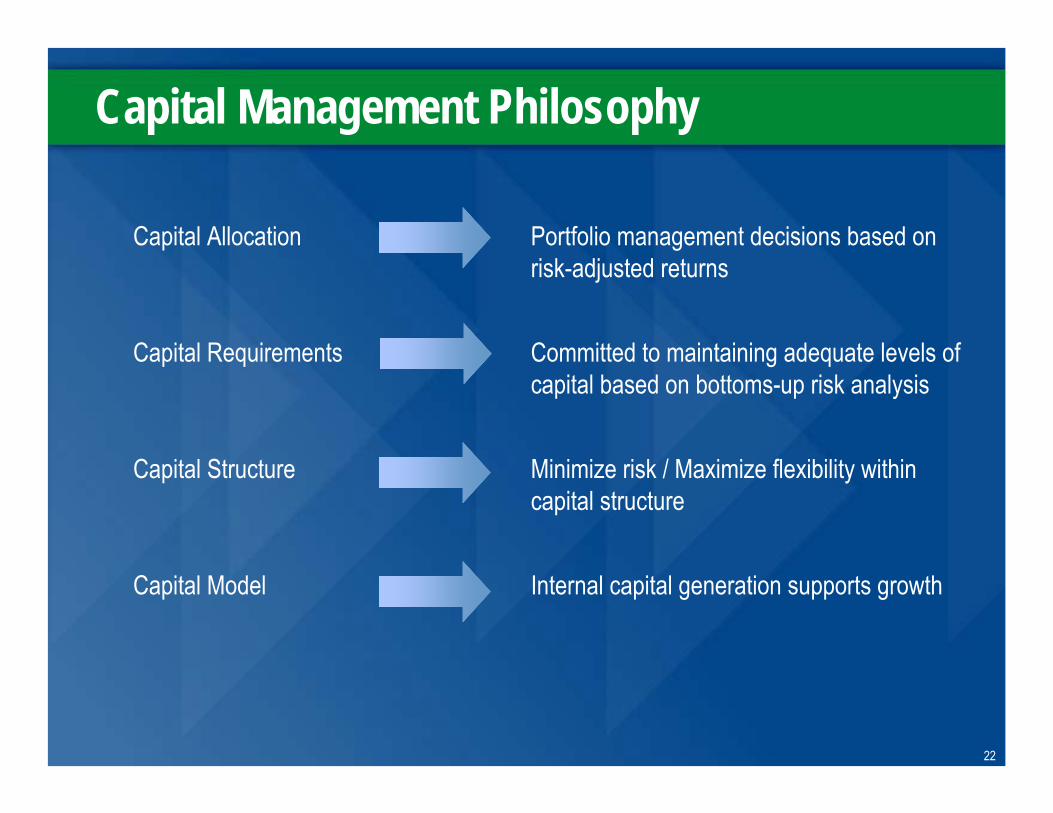

Portfolio management decisions based on risk-adjusted returns

Capital Allocation

Minimize risk / Maximize flexibility within capital structure

Capital Structure

Committed to maintaining adequate levels of capital based on bottoms-up risk analysis

Capital Requirements

Internal capital generation supports growthCapital Model

Capital Management Philosophy

23

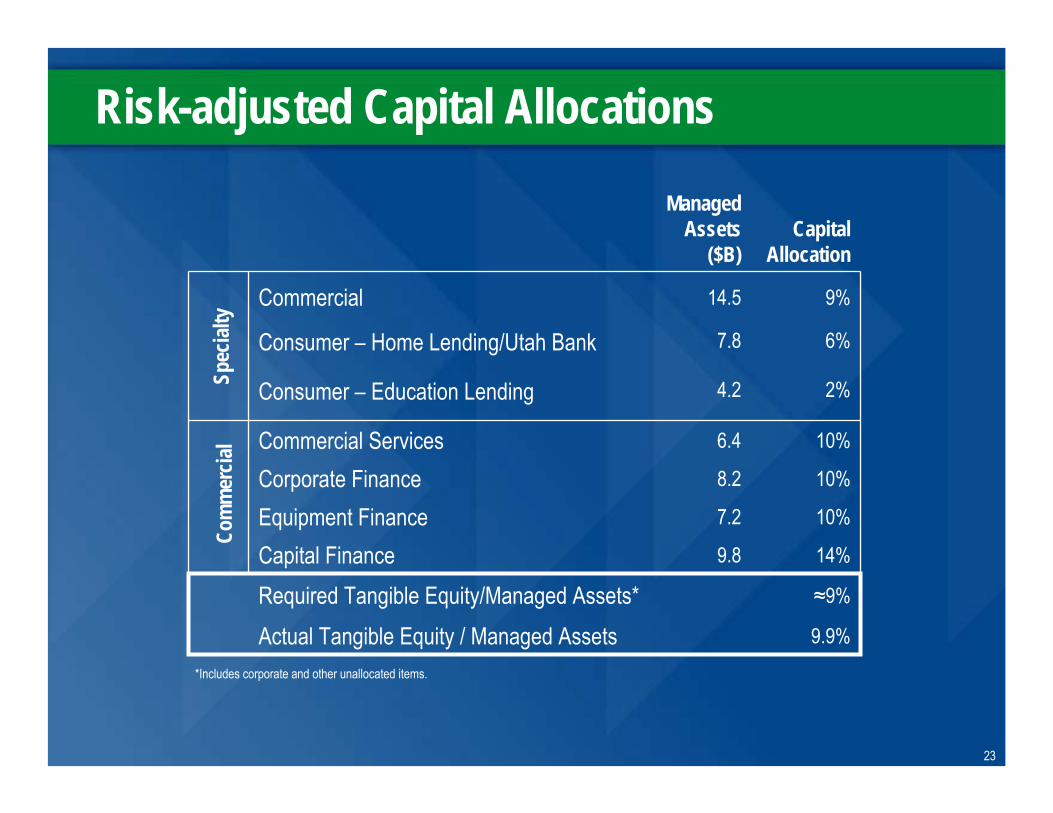

2%4.2Consumer – Education Lending

9.8

7.2

8.2

6.4

7.8

14.5

Managed Assets

($B)

≈9%Required Tangible Equity/Managed Assets* 9.9%Actual Tangible Equity / Managed Assets

14%

10%

10%

10%

6%

9%

Capital Allocation

Equipment FinanceCorporate Finance

Consumer – Home Lending/Utah Bank

Commercial

Capital Finance

Commercial Services

Com

mer

cial

Spec

ialty

Risk-adjusted Capital Allocations

*Includes corporate and other unallocated items.

24

Portfolio Optimization Initiatives• Accelerated liquidation of approximately $600 million in assets

– Manufactured Housing– Recreation Vehicle– Marine

• Sold Technology Rental Services portfolio ($100 million)• Sold majority of Venture Capital portfolio ($68 million)• Sold majority of Private Equity Funds ($140 million)

• Sold $900 million in business aircraft assets• Examining:

– Manufactured Housing

2004

YTD

2005

− Trucking− Franchise Finance

− Under-performing business lines

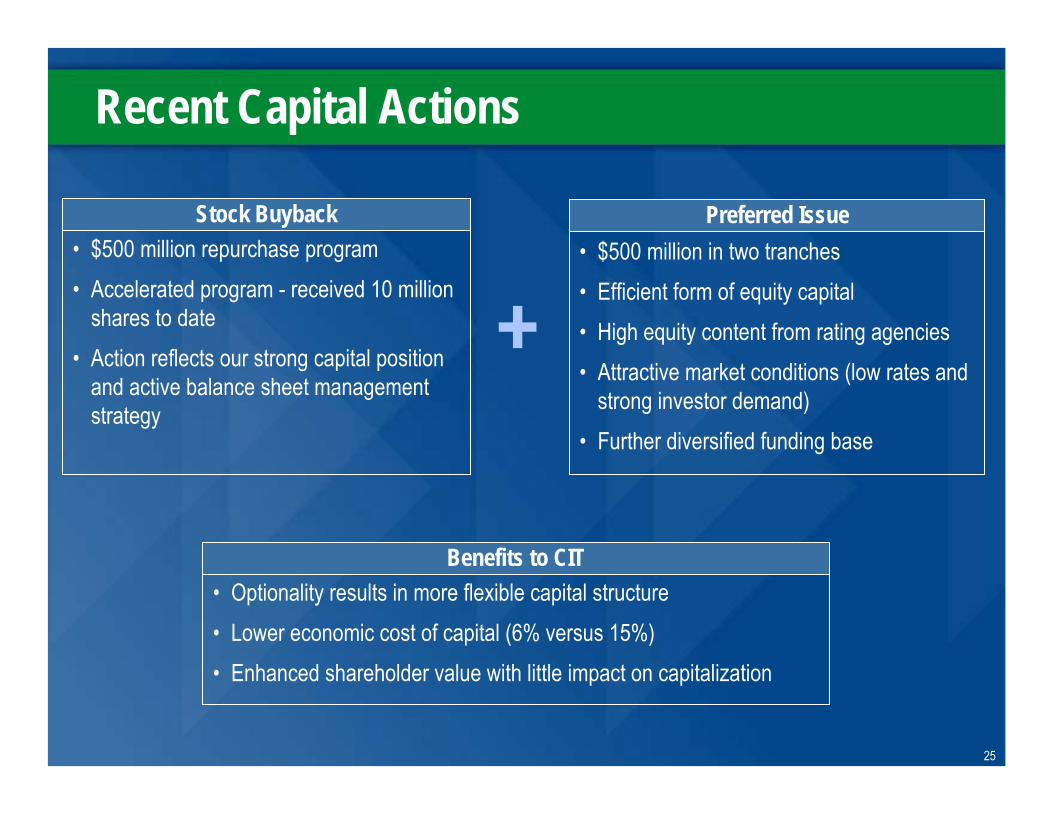

25

Recent Capital Actions

• $500 million repurchase program• Accelerated program - received 10 million

shares to date• Action reflects our strong capital position

and active balance sheet management strategy

• $500 million in two tranches• Efficient form of equity capital• High equity content from rating agencies• Attractive market conditions (low rates and

strong investor demand)• Further diversified funding base

Stock Buyback Preferred Issue

+

• Optionality results in more flexible capital structure• Lower economic cost of capital (6% versus 15%)• Enhanced shareholder value with little impact on capitalization

Benefits to CIT

26

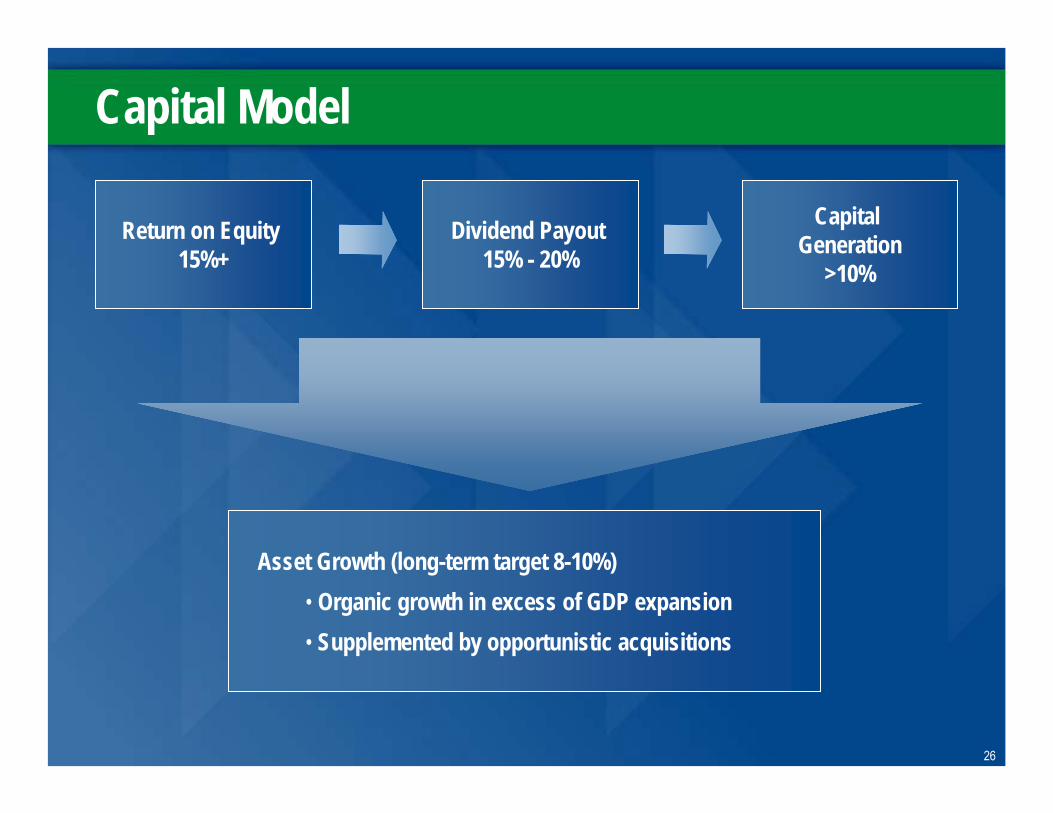

Capital Model

Return on Equity 15%+

Dividend Payout 15% - 20%

Capital Generation

>10%

Asset Growth (long-term target 8-10%)• Organic growth in excess of GDP expansion• Supplemented by opportunistic acquisitions

27

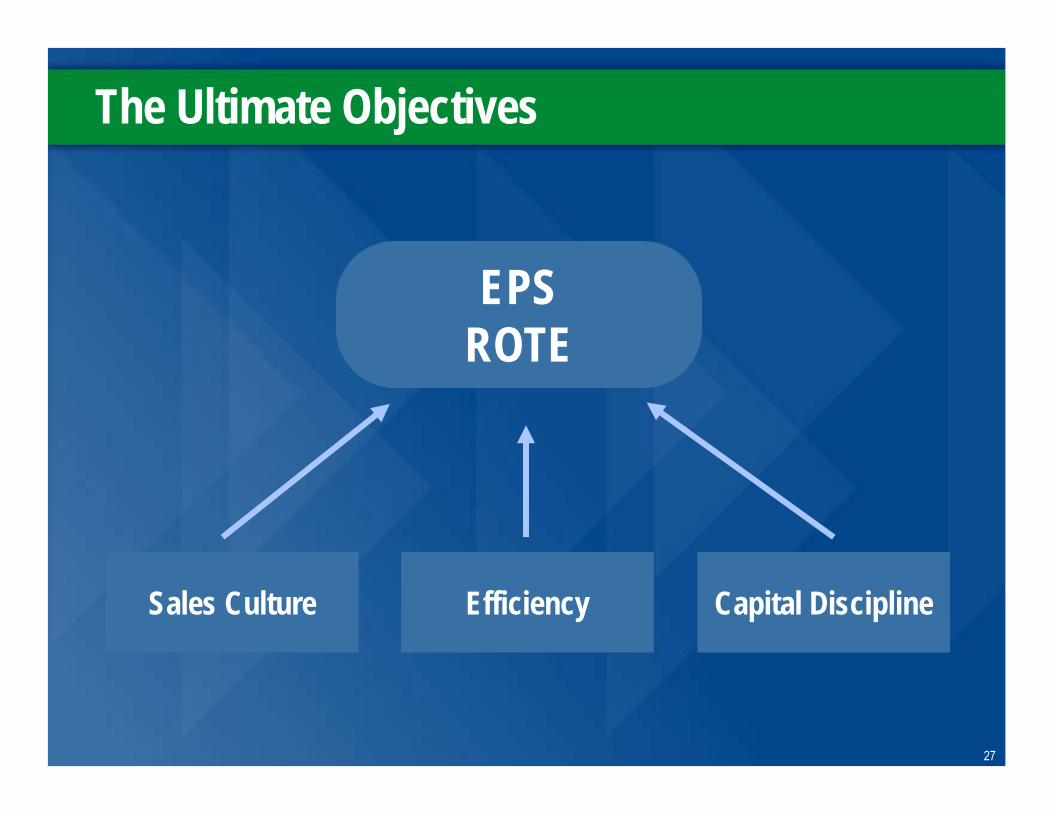

The Ultimate Objectives

EPSROTE

Efficiency Capital DisciplineSales Culture

28

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

16.0%

17.0%

Perce

nt RO

TE

Mar-03 Jun-03 Sep-03 Dec-03* Mar-04* Jun-04 Sep-04* Dec-04* Mar-05* Jun-05$0.50

$0.60

$0.70

$0.80

$0.90

$1.00

$1.10

$1.20

Earni

ngs P

er Sh

are

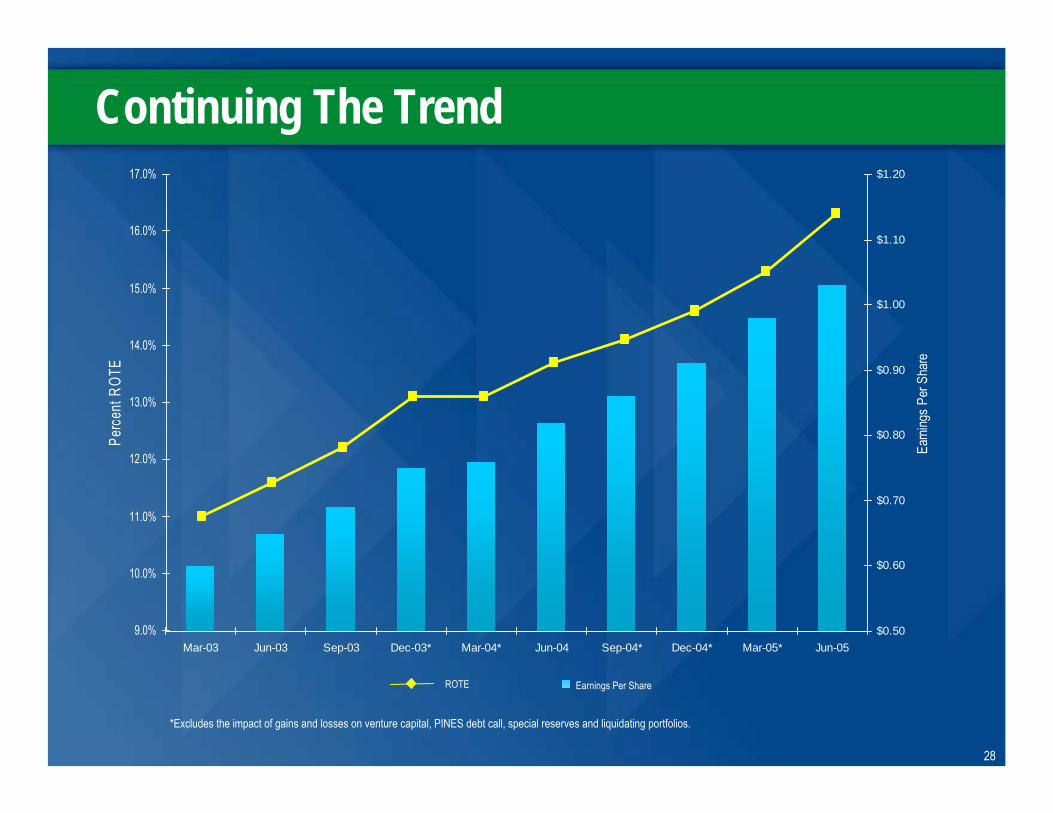

Continuing The Trend

*Excludes the impact of gains and losses on venture capital, PINES debt call, special reserves and liquidating portfolios.

ROTE Earnings Per Share

29

Appendix

30

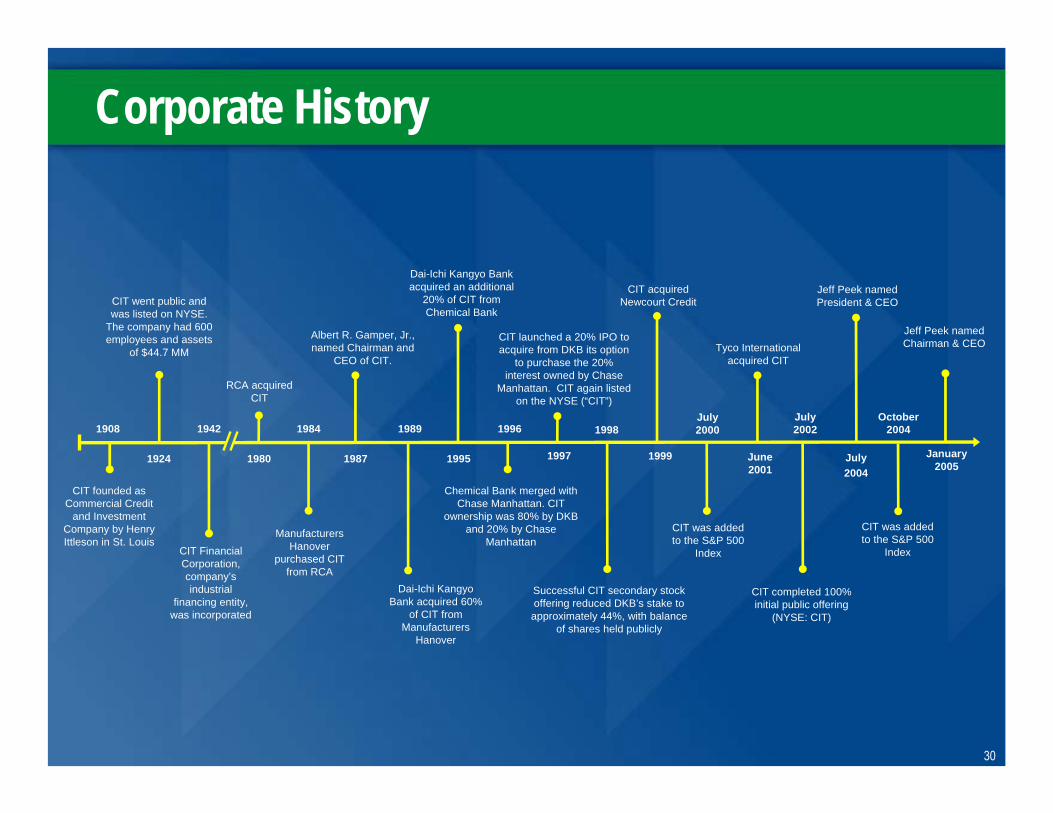

Corporate History

Dai-Ichi Kangyo Bank acquired 60%

of CIT from Manufacturers

Hanover

CIT Financial Corporation, company’s industrial

financing entity, was incorporated

CIT founded as Commercial Credit

and Investment Company by Henry Ittleson in St. Louis

CIT launched a 20% IPO to acquire from DKB its option

to purchase the 20% interest owned by Chase

Manhattan. CIT again listed on the NYSE (“CIT”)

Albert R. Gamper, Jr., named Chairman and

CEO of CIT.

CIT completed 100% initial public offering

(NYSE: CIT)

Tyco International acquired CIT

CIT acquired Newcourt Credit

Successful CIT secondary stock offering reduced DKB’s stake to approximately 44%, with balance

of shares held publicly

1997

Chemical Bank merged with Chase Manhattan. CIT

ownership was 80% by DKB and 20% by Chase

Manhattan

Dai-Ichi Kangyo Bank acquired an additional

20% of CIT from Chemical Bank

Manufacturers Hanover

purchased CIT from RCA

CIT went public and was listed on NYSE.

The company had 600 employees and assets

of $44.7 MM

July 2002

June 2001

July 2000

CIT was added to the S&P 500

Index

1999

19981996

1995

1989

1987

1984

1980

RCA acquired CIT

1942

1924

1908

July2004

Jeff Peek named President & CEO

CIT was added to the S&P 500

Index

October 2004

January 2005

Jeff Peek named Chairman & CEO

31

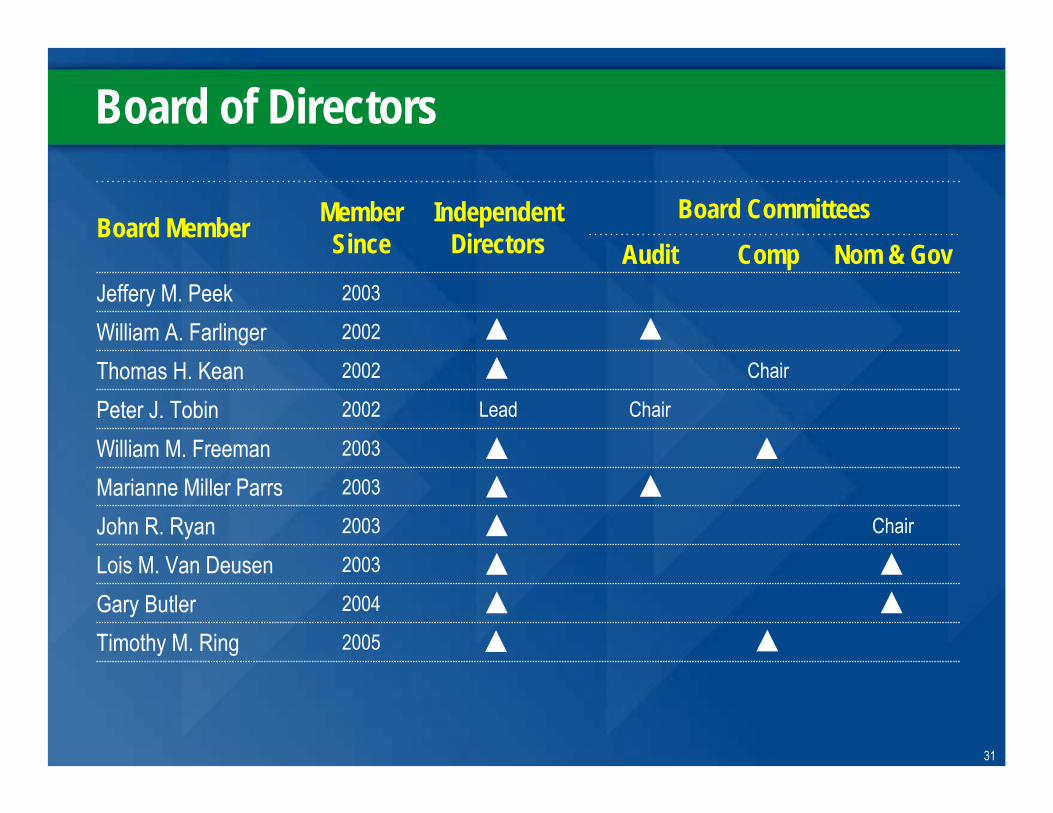

Board of Directors

2005Timothy M. Ring2004Gary Butler2003Lois M. Van Deusen

Chair2003John R. Ryan2003Marianne Miller Parrs2003William M. Freeman

ChairLead2002Peter J. TobinChair2002Thomas H. Kean

2002William A. Farlinger2003Jeffery M. Peek

Nom & GovCompAuditBoard Member

Board CommitteesIndependent Directors

Member Since

32

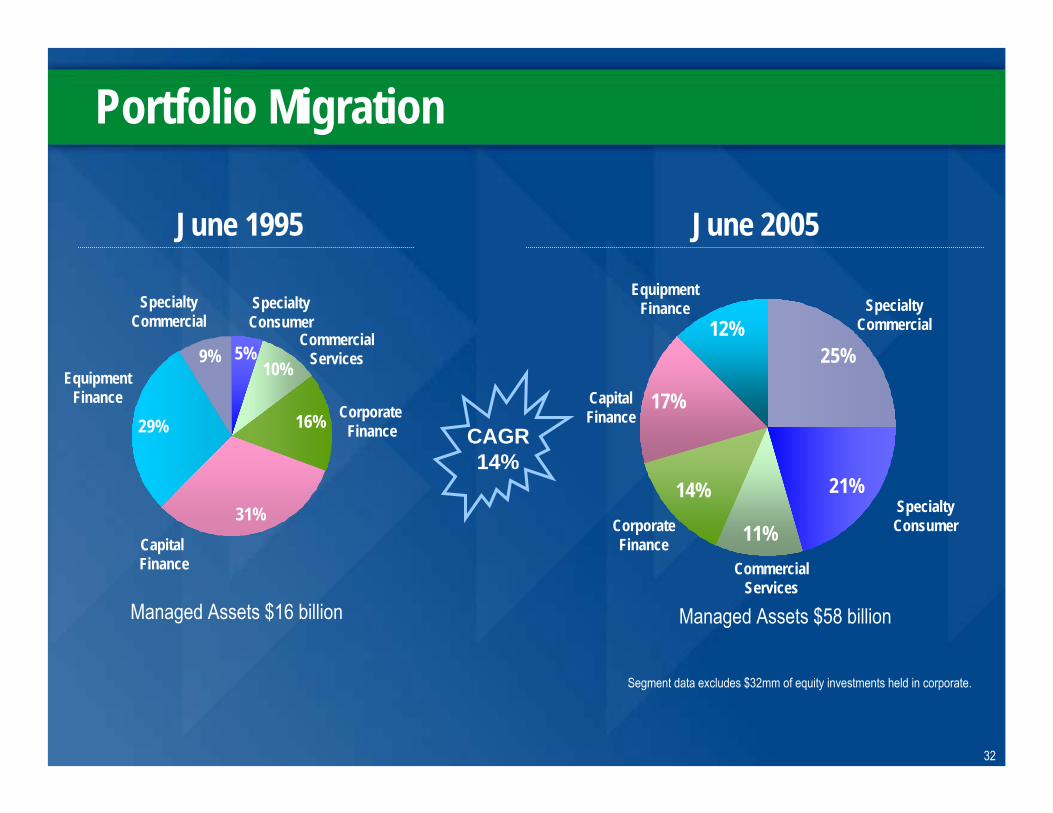

Portfolio Migration

Managed Assets $16 billion Managed Assets $58 billion

5%10%

16%

31%

29%

9%Commercial

Services

Capital Finance

SpecialtyConsumer

Corporate Finance

25%

21%

11%

14%

17%

12%

EquipmentFinance

CommercialServices

CapitalFinance

SpecialtyCommercial

SpecialtyConsumer Corporate

Finance

Segment data excludes $32mm of equity investments held in corporate.

June 1995 June 2005

CAGR14%

Equipment Finance

SpecialtyCommercial

33

19.6%

11.0%

11.1%2.7%2.1%

13.1%

8.9%

13.5%

4.5%2.2%13%

19.8%15.7%

5.1%

10.1%

14.4%

16.4%

18.5%

14.1%

12.0%

12.4%

11.8%8.5%

5.7%

4.8%

4.6%

3.8%3.2%

2.5%2.2%

14.4%

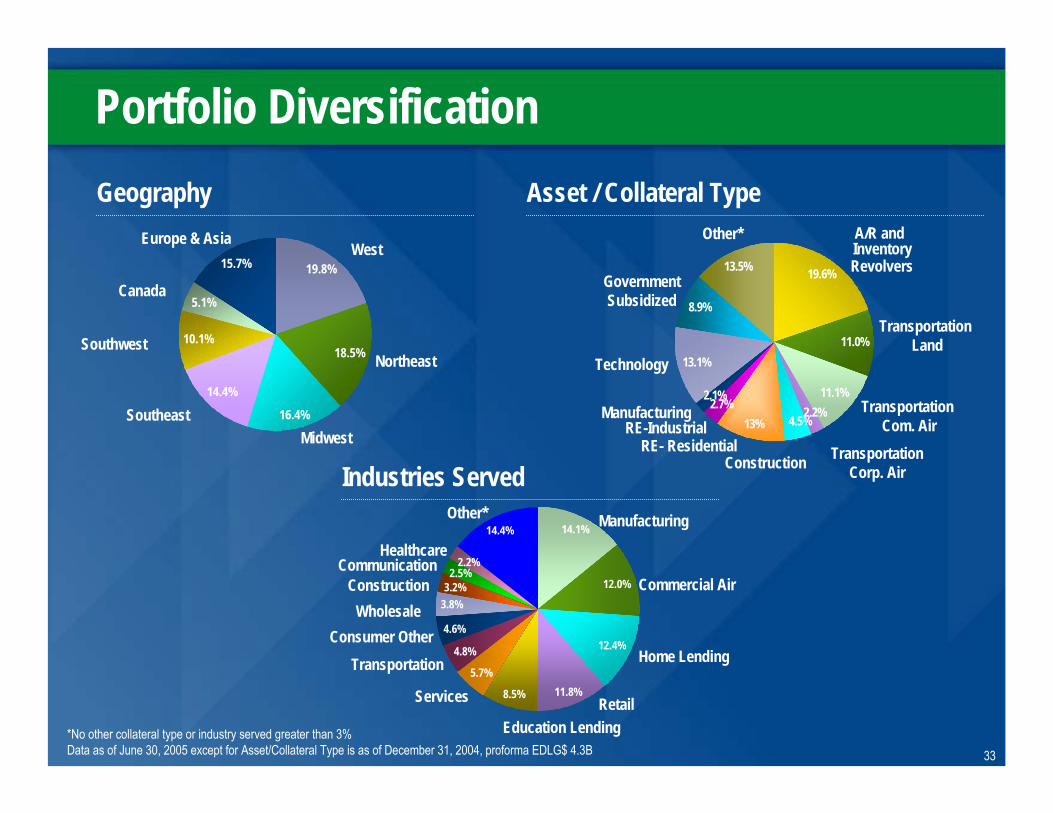

Portfolio DiversificationGeography Asset / Collateral Type

Industries Served

Northeast

Europe & Asia

Canada

Southwest

SoutheastMidwest

WestA/R and Inventory Revolvers

Technology

Manufacturing

Construction

Transportation Land

Other*

RE- Residential

Manufacturing

Commercial Air

Home LendingTransportation

Services

Consumer Other

Construction Wholesale

CommunicationHealthcare

Other*

Retail

Transportation Com. Air

TransportationCorp. Air

RE-Industrial

*No other collateral type or industry served greater than 3%Data as of June 30, 2005 except for Asset/Collateral Type is as of December 31, 2004, proforma EDLG$ 4.3B

Education Lending

GovernmentSubsidized

34

Growth Indicators

Industrial ProductionCar Loadings

Oil Prices

Capacity UtilizationCapital Spending

C & I Loan GrowthBankruptcy Filings

Consumer ConfidenceGovernment Sponsorship7(a) Funding Levels Switch

Home PricesMortgage Applications

PC SalesIP – Telephony Sales

C & I Loan GrowthConstruction Spending

Equipment Finance

Consumer ConfidenceSmall Business AdministrationCost of EducationEducation Lending

Restructuring ActivityLBO Activity

Asset Based Lending

Coal ProductionGrain Yield

Rail

Revenue Passenger MilesGlobal Economic Growth

Air

Retail SalesConsumer Credit Growth

Factoring

Interest RatesConsumer Confidence

Home Lending

Capital SpendingGDP

Vendor and Small to Mid-TicketKey Data Points

35

Growth: Acquisition Summary

Accelerated Build outQ3535HealthcareHBCC

Integration completeQ1864FactoringSunTrust

Expanding sales force

Realizing synergies

Strong volume

Strong client retention achieved

Lease rates improved

Comments

4,400

800

520

1,000

450

400

Assets ($mm)

Q1Education LoansEDLG

Q3Vendor FinanceCitiCapital

Q2Tech. LeasingGATX

Q4FactoringHSBC

Q3FactoringGECC

Q2RailcarsFlex Leasing

ClosedAsset TypeSeller

2003

2004

2005

36

Home Lending - Highlights• Originating business for 12 years• Predominately a first mortgage lender• 31 national sales offices located in major MSAs• Centralized servicing operation located in Oklahoma City• State-of-the-art systems offer a competitive advantage – “BrokerEdge”• Commercially sourced origination platform: over 4,000 mortgage brokers• Service and monitor portfolio through advanced technologies• Full control of credit adjudication process with 100% appraisal review

36

37

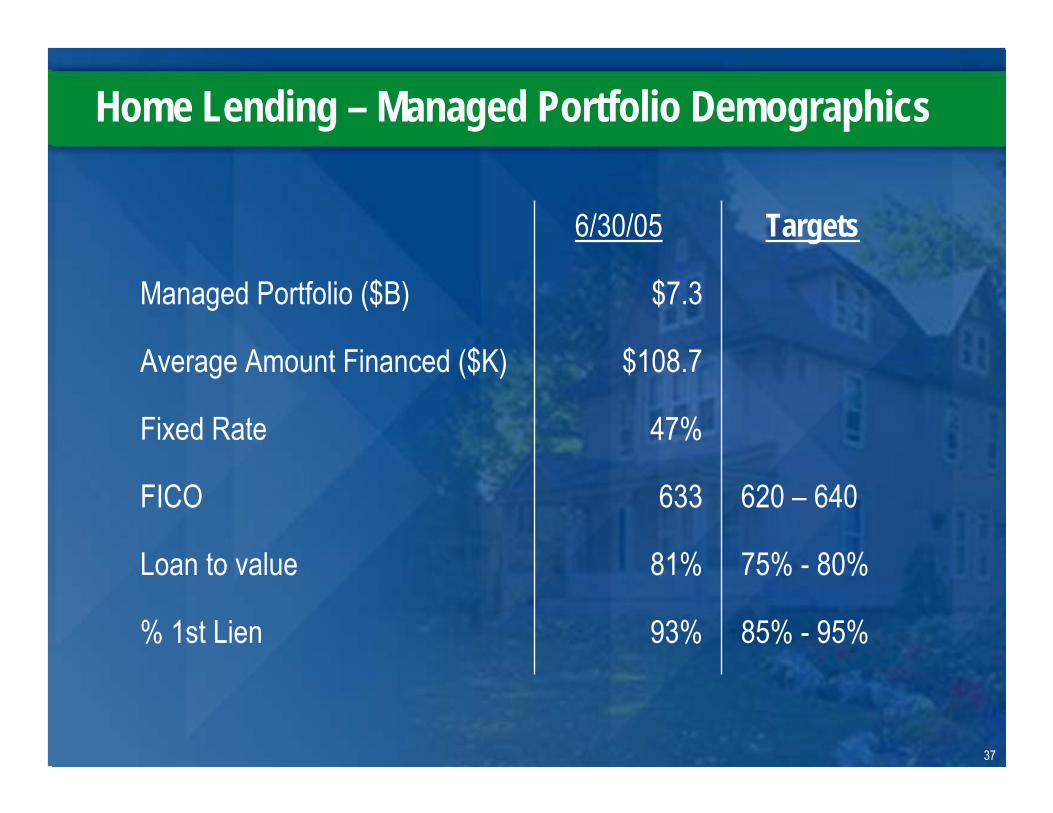

Home Lending – Managed Portfolio Demographics

37

Targets6/30/05

85% - 95%93%% 1st Lien

75% - 80%81%Loan to value

620 – 640633FICO

47%Fixed Rate

$108.7Average Amount Financed ($K)

$7.3Managed Portfolio ($B)

38

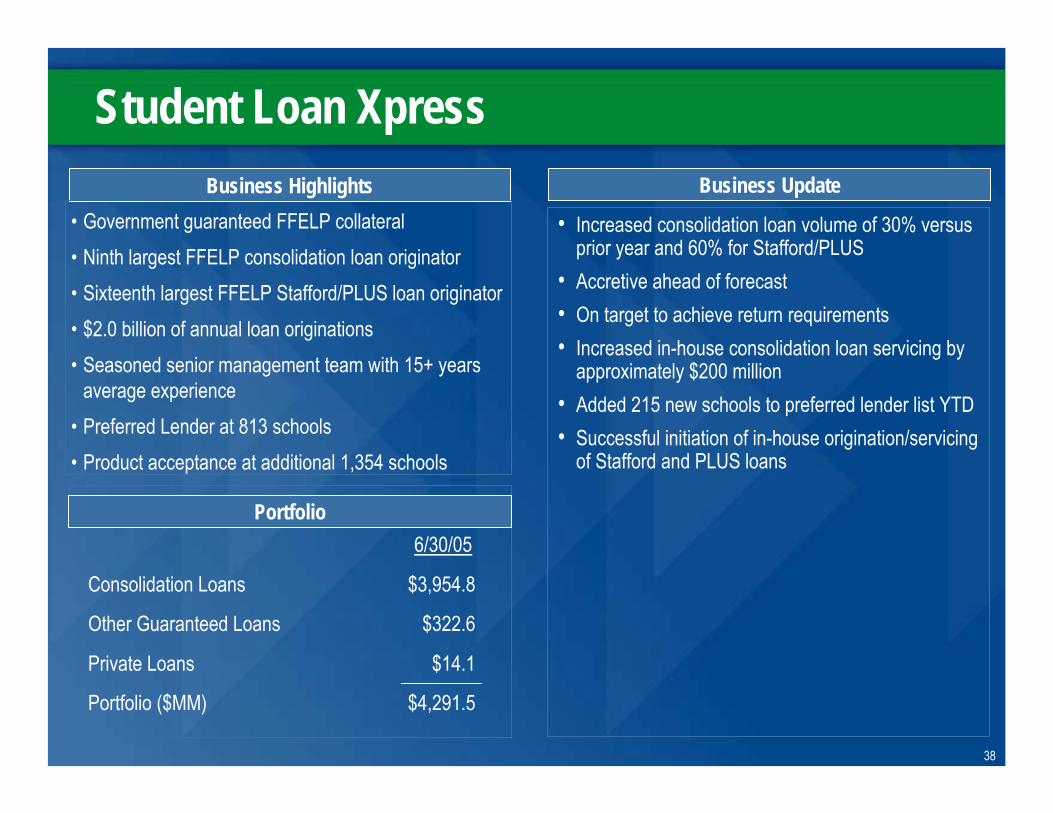

Student Loan XpressBusiness Highlights

• Government guaranteed FFELP collateral• Ninth largest FFELP consolidation loan originator• Sixteenth largest FFELP Stafford/PLUS loan originator • $2.0 billion of annual loan originations • Seasoned senior management team with 15+ years

average experience• Preferred Lender at 813 schools• Product acceptance at additional 1,354 schools

Portfolio

• Increased consolidation loan volume of 30% versus prior year and 60% for Stafford/PLUS

• Accretive ahead of forecast• On target to achieve return requirements• Increased in-house consolidation loan servicing by

approximately $200 million• Added 215 new schools to preferred lender list YTD• Successful initiation of in-house origination/servicing

of Stafford and PLUS loans

Business Update

$4,291.5Portfolio ($MM)

$14.1Private Loans

$322.6Other Guaranteed Loans

$3,954.8Consolidation Loans

6/30/05

39

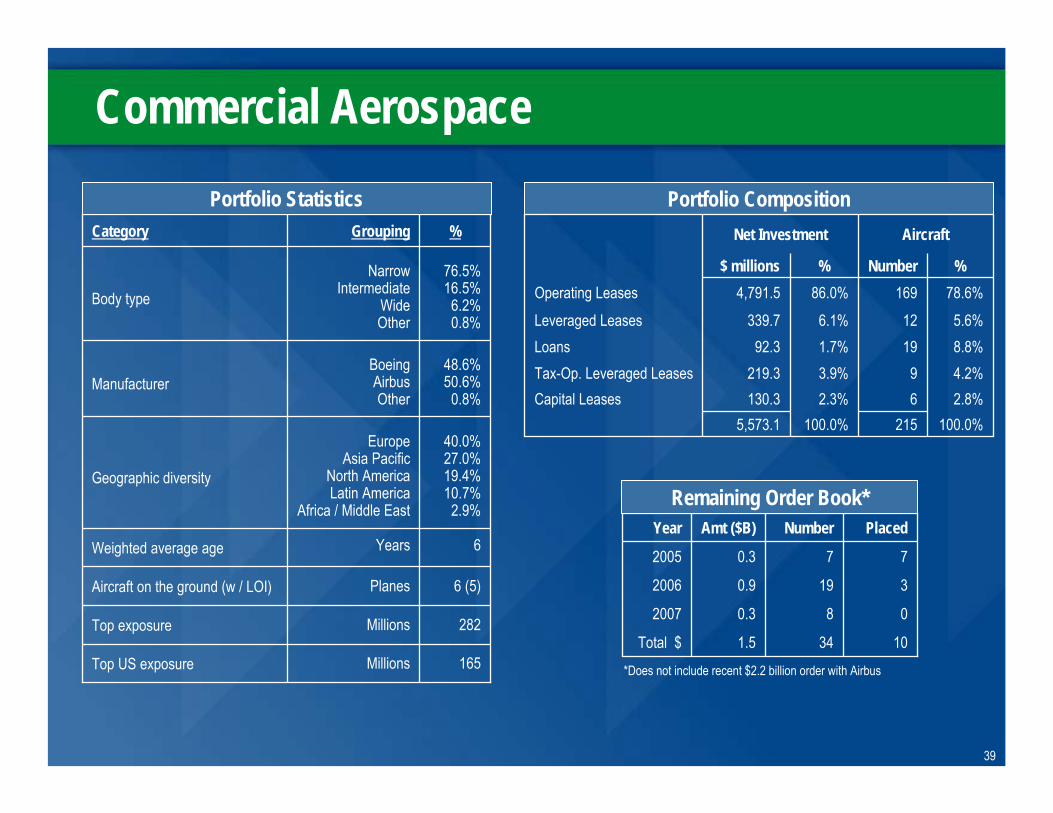

Portfolio Composition

Commercial Aerospace

AircraftNet Investment

100.0%215100.0%5,573.12.8%62.3%130.3Capital Leases4.2%93.9%219.3Tax-Op. Leveraged Leases8.8%191.7%92.3Loans5.6%126.1%339.7Leveraged Leases

78.6%16986.0%4,791.5Operating Leases%Number%$ millions

165MillionsTop US exposure

282MillionsTop exposure

Planes

Years

EuropeAsia Pacific

North AmericaLatin America

Africa / Middle East

BoeingAirbusOther

NarrowIntermediate

WideOther

Grouping

48.6%50.6%

0.8%Manufacturer

6 (5) Aircraft on the ground (w / LOI)

6Weighted average age

40.0% 27.0%19.4%10.7% 2.9%

Geographic diversity

76.5%16.5%

6.2% 0.8%

Body type

%Category

10341.5Total $

0 8 0.3 2007

3 19 0.9 2006

7 7 0.3 2005

PlacedNumberAmt ($B)Year

Portfolio Statistics

Remaining Order Book*

*Does not include recent $2.2 billion order with Airbus

40

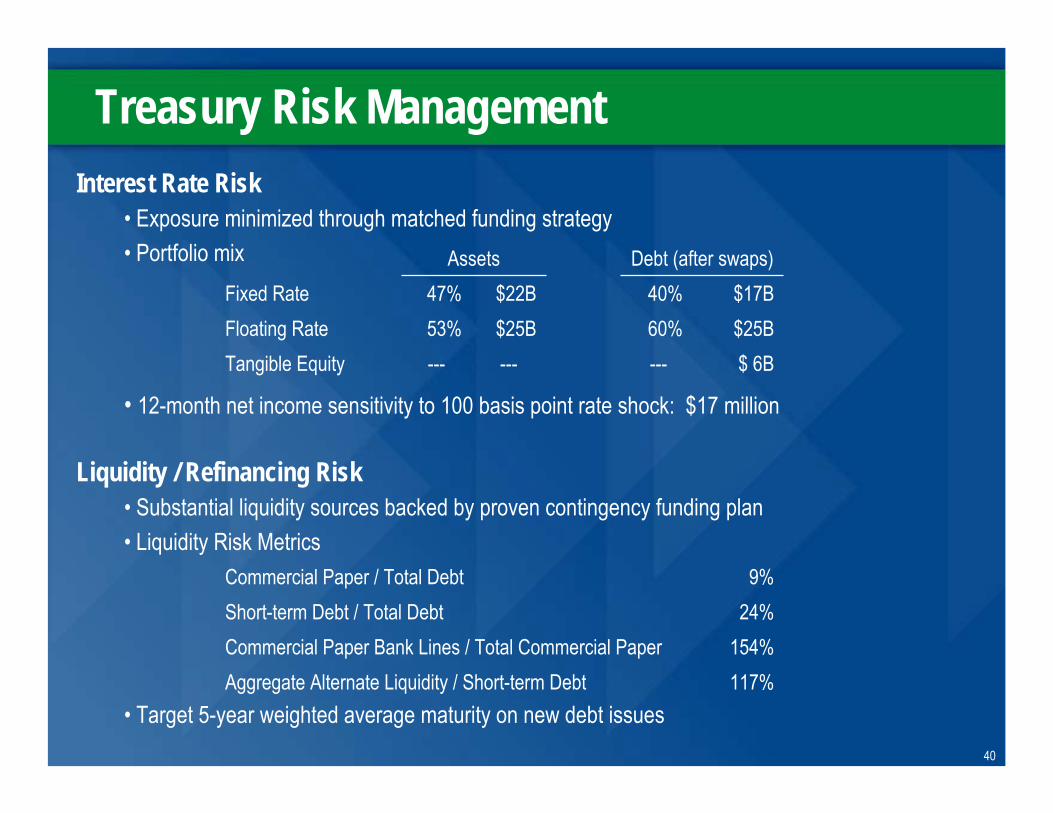

Treasury Risk ManagementInterest Rate Risk

• Exposure minimized through matched funding strategy• Portfolio mix

• 12-month net income sensitivity to 100 basis point rate shock: $17 million

Liquidity / Refinancing Risk• Substantial liquidity sources backed by proven contingency funding plan• Liquidity Risk Metrics

• Target 5-year weighted average maturity on new debt issues

$ 6B---------Tangible Equity$25B60%$25B53%Floating Rate$17B40%$22B47%Fixed Rate

Debt (after swaps)Assets

117%Aggregate Alternate Liquidity / Short-term Debt154%Commercial Paper Bank Lines / Total Commercial Paper24%Short-term Debt / Total Debt9%Commercial Paper / Total Debt

41

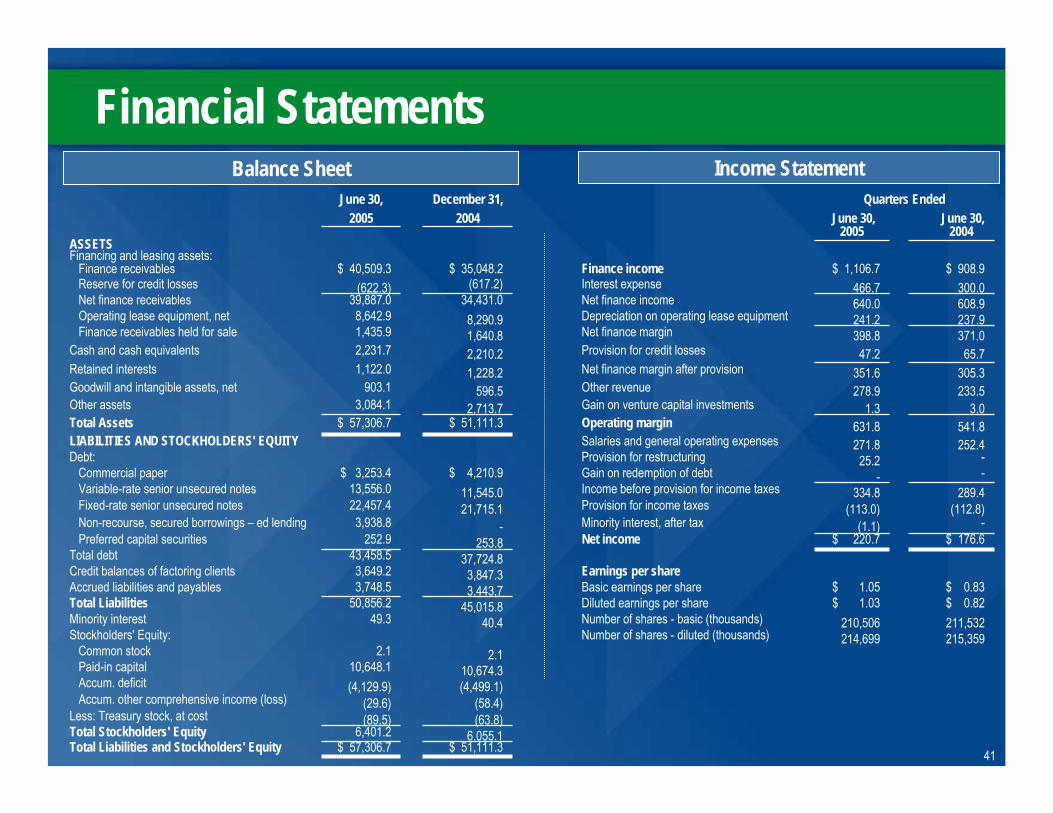

Financial Statements

$ 51,111.3 $ 57,306.7 Total Liabilities and Stockholders' Equity6,055.1 6,401.2 Total Stockholders' Equity

(63.8)(89.5)Less: Treasury stock, at cost(58.4)(29.6)Accum. other comprehensive income (loss)

(4,499.1)(4,129.9)Accum. deficit10,674.3 10,648.1 Paid-in capital

2.1 2.1 Common stock215,359 214,699 Number of shares - diluted (thousands)Stockholders' Equity:211,532 210,506 Number of shares - basic (thousands)40.4 49.3 Minority interest$ 0.82 $ 1.03 Diluted earnings per share45,015.8 50,856.2 Total Liabilities$ 0.83 $ 1.05 Basic earnings per share3,443.7 3,748.5 Accrued liabilities and payables

Earnings per share3,847.3 3,649.2 Credit balances of factoring clients37,724.8 43,458.5 Total debt

$ 176.6 $ 220.7 Net income253.8 252.9 Preferred capital securities-(1.1)Minority interest, after tax-3,938.8 Non-recourse, secured borrowings – ed lending

(112.8)(113.0)Provision for income taxes21,715.1 22,457.4 Fixed-rate senior unsecured notes289.4 334.8 Income before provision for income taxes11,545.0 13,556.0 Variable-rate senior unsecured notes

--Gain on redemption of debt$ 4,210.9 $ 3,253.4 Commercial paper-25.2 Provision for restructuringDebt:

252.4 271.8 Salaries and general operating expensesLIABILITIES AND STOCKHOLDERS' EQUITY541.8 631.8 Operating margin$ 51,111.3 $ 57,306.7 Total Assets

3.0 1.3 Gain on venture capital investments2,713.7 3,084.1 Other assets233.5 278.9 Other revenue596.5 903.1 Goodwill and intangible assets, net305.3 351.6 Net finance margin after provision1,228.2 1,122.0 Retained interests65.7 47.2 Provision for credit losses2,210.2 2,231.7 Cash and cash equivalents

371.0 398.8 Net finance margin1,640.8 1,435.9 Finance receivables held for sale237.9 241.2 Depreciation on operating lease equipment8,290.9 8,642.9 Operating lease equipment, net608.9 640.0 Net finance income34,431.0 39,887.0 Net finance receivables300.0 466.7 Interest expense(617.2)(622.3)Reserve for credit losses

$ 908.9 $ 1,106.7 Finance income$ 35,048.2 $ 40,509.3Finance receivablesFinancing and leasing assets:ASSETS

20042005June 30, June 30, 20042005

Quarters EndedDecember 31,June 30,

Balance Sheet Income Statement

42

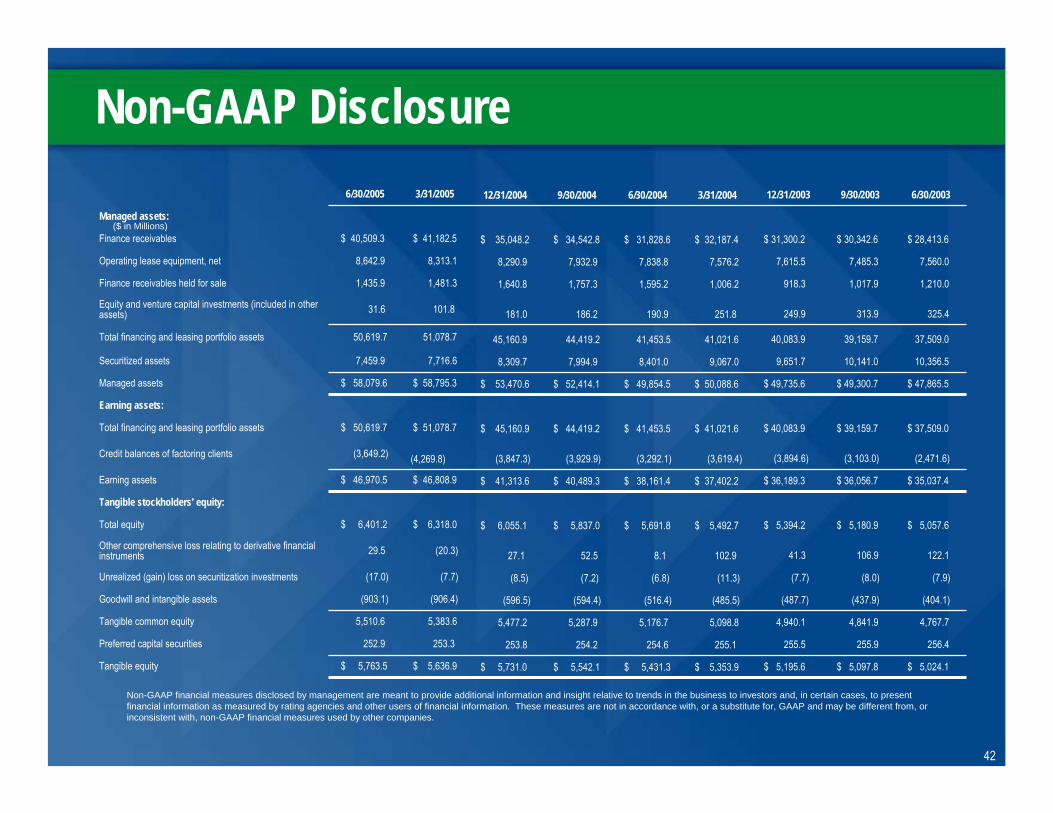

Non-GAAP Disclosure

Non-GAAP financial measures disclosed by management are meant to provide additional information and insight relative to trends in the business to investors and, in certain cases, to present financial information as measured by rating agencies and other users of financial information. These measures are not in accordance with, or a substitute for, GAAP and may be different from, or inconsistent with, non-GAAP financial measures used by other companies.

($ in Millions)

$ 5,024.1 $ 5,097.8 $ 5,195.6 $ 5,353.9 $ 5,431.3 $ 5,542.1 $ 5,731.0 $ 5,636.9 $ 5,763.5 Tangible equity

256.4 255.9 255.5 255.1 254.6 254.2 253.8 253.3 252.9 Preferred capital securities

4,767.7 4,841.9 4,940.1 5,098.8 5,176.7 5,287.9 5,477.2 5,383.6 5,510.6 Tangible common equity

(404.1)(437.9)(487.7)(485.5)(516.4)(594.4)(596.5)(906.4)(903.1)Goodwill and intangible assets

(7.9)(8.0)(7.7)(11.3)(6.8)(7.2)(8.5)(7.7)(17.0)Unrealized (gain) loss on securitization investments

122.1 106.9 41.3 102.9 8.1 52.5 27.1 (20.3)29.5 Other comprehensive loss relating to derivative financial instruments

$ 5,057.6 $ 5,180.9 $ 5,394.2 $ 5,492.7 $ 5,691.8 $ 5,837.0 $ 6,055.1 $ 6,318.0 $ 6,401.2 Total equity

Tangible stockholders' equity:

$ 35,037.4 $ 36,056.7 $ 36,189.3 $ 37,402.2 $ 38,161.4 $ 40,489.3 $ 41,313.6 $ 46,808.9 $ 46,970.5Earning assets

(2,471.6)(3,103.0)(3,894.6)(3,619.4)(3,292.1)(3,929.9)(3,847.3)(4,269.8)(3,649.2)Credit balances of factoring clients

$ 37,509.0 $ 39,159.7 $ 40,083.9 $ 41,021.6 $ 41,453.5 $ 44,419.2 $ 45,160.9 $ 51,078.7 $ 50,619.7Total financing and leasing portfolio assets

Earning assets:

$ 47,865.5 $ 49,300.7 $ 49,735.6 $ 50,088.6 $ 49,854.5 $ 52,414.1 $ 53,470.6 $ 58,795.3 $ 58,079.6 Managed assets

10,356.5 10,141.0 9,651.7 9,067.0 8,401.0 7,994.9 8,309.7 7,716.6 7,459.9Securitized assets

37,509.0 39,159.7 40,083.9 41,021.6 41,453.5 44,419.2 45,160.9 51,078.7 50,619.7 Total financing and leasing portfolio assets

325.4 313.9 249.9 251.8 190.9 186.2 181.0 101.8 31.6 Equity and venture capital investments (included in other assets)

1,210.0 1,017.9 918.3 1,006.2 1,595.2 1,757.3 1,640.8 1,481.3 1,435.9 Finance receivables held for sale

7,560.0 7,485.3 7,615.5 7,576.2 7,838.8 7,932.9 8,290.9 8,313.1 8,642.9Operating lease equipment, net

$ 28,413.6 $ 30,342.6 $ 31,300.2 $ 32,187.4 $ 31,828.6 $ 34,542.8 $ 35,048.2 $ 41,182.5 $ 40,509.3 Finance receivables

Managed assets:

6/30/20039/30/200312/31/20033/31/20046/30/20049/30/200412/31/20043/31/20056/30/2005