china’s ofdi in the eu as a latecomer - · pdf file1. introduction and literature review...

TRANSCRIPT

China’s OFDI in the EU as a Latecomer

LI Jinshan, Professor, Director, Centre for European Studies, ZhejiangUniversity (China)ZHANG Mohan, PH.D Student, Centre for European Studies, ZhejiangUniversity (China)

1. Introduction and literature review

● Coupled with its attracting inward foreigndirect investment (IFDI) since 1980s, Chinahas become a potential power of outwardforeign direct investment (OFDI) in recentyears.● Since FDI is probably one of the increasing

driving forces contributing to the EU-Chinarelations, with the growth of China’s OFDI,Chinese economy has getting closer link withEuropean economy.

2. China’s OFDI policy evolution

● China’s OFDI policy has experienced three decades of reform, which hasbeen aimed at changing and increasing the degree of integration of itseconomy into the global economy. As a result,China has evolved from aposition of marginal relevance in terms of its OFDI to becoming anemerging sourcing country among developing economies; however, itsOFDI flow and stock are both at very low levels compared with developedecpnomies (See graph 1 and graph 2).

Graph 1 China’s OFDI Flow (Millions of US $)

Notes: The left axis represents OFDI flow of the world total and the developed economies; the right axis represents OFDI flow of China and the developing economiesSources: UNCTAD, World Investment Reports

Graph 2 China’s OFDI Stock (Millions of US $)

Notes: The left axis represents OFDI stock of the world total and the developed economies; the right axis represents OFDI stock of China and the developing economiesSources: UNCTAD, World Investment Reports

-

500 000

1 000 000

1 500 000

2 000 000

2 500 000

!"#$

!"#!

!"#%

!"#&

!"#'

!"#(

!"#)

!"#*

!"##

!"#"

!""$

!""!

!""%

!""&

!""'

!""(

!"")

!""*

!""#

!"""

%$$$

%$$!

%$$%

%$$&

%$$'

%$$(

%$$)

%$$*

Years

Milli

ons

of U

S $

-

50 000

100 000

150 000

200 000

250 000

300 000

+,-./ 0121.,31/415,6,7819 0121.,386:415,6,7819 ;<86=

-

2 000 000

4 000 000

6 000 000

8 000 000

10 000 000

12 000 000

14 000 000

16 000 000

18 000 000

!"#$!"#%!"#&!"#'!"##!""$!""%!""&!""'!""#%$$$%$$%%$$&%$$'

Years

Milli

ons

of U

S $

-

500 000

1 000 000

1 500 000

2 000 000

2 500 000

()*+, -./.+)0.,1.2)3)45.6 -./.+)05371.2)3)45.6 8953:

2.1 Rigid control and policy skepticism phase: 1980s

● Following the “Open Door” strategy applied in 1978, thestrong ideological antipathy and prejudice against Chineseenterprises operating overseas was gradually eased, butChinese government’s attitude towards overseas investmentwas still skeptical and cautious, mainly due to the lack ofadequate overseas operating experiences of domesticenterprises.

● Regarding to policy field, OFDI was almost ignored in theagenda of government in the 1980s.

● only one is worthy mentioning released by MOFERT in1985, “Procedures of Control and Approval for Non-TradeEnterprises Overseas” (see Box 1)

Box 1 Policy Motivations and Project Categories of China’s OFDI during 1980s

• secure access to domestically scarcenatural resources

• access and transfer technology to China• enhance export possibilities for Chinese

companies• promote managerial skills through ‘on-the-

job training’

• import advanced technology andequipment

• provide a long-term reliable supply of rawmaterials

• export China’s machinery, materials,engineering and labour service

• help serve China’s domestic market andearn foreign currency

OFDI Project CategoriesOFDI Policy Motivations

Source: Guo, 1984; Cheng and Stough, 2007; Provisions Governing Control and Approval Procedures for OpeningNon-Trade Enterprises Overseas, 1985, MOFERT

● According to UNCTAD FDI Statistic Database, by the end of 1989, China'scumulative OFDI stock had reached 3.625 billion U.S. dollars, accounting for0.25% of the world's total stock and 2.8% of developing countries’ total stock.In 1989, China's OFDI flow was 780 million U.S. dollars, accounting for0.34% of the world's total flow and 3.95% of developing countries’ total flow,which was at very low level compared with the other developing economies.

2.2 Flexible adjustment and policy acceptance phase: 1990s

● Deng Xiaoping’s landmarkjourney in 1992 strengthenedthe liberal politicians in ChineseCommunist Party (CCP) alongwith bureaucrats in governmentagencies.

● Policy-making circumstances towards China’s OFDI have been changed

• At the national level, former President Jiang Zemin stated that “weshould encourage enterprises to investment and to expand theirtransactional operation abroad in 1992; and restated that “China willestablish highly competitive large enterprise-groups withtransnational operations, but the state-owned sectors must be in adominant position in major industries” at the 15th National Congressof the Chinese Communist Party in 1997.

• At the sub-national level, some provincial and municipal governments wereencouraged to promote overseas business operations, which led to a huge surgein local level enterprises investing outside due to the relaxed requirements,especially in Hong Kong.

• Two of the most important policy documents were released by the State PlanningCommission in 1991, and they set OFDI approval procedures and fundlimitations (See box 2).

Box 2 Approval Procedure and Authorization of China’s ODFI Projects during 1990s

• ODFI Projects < US$ 1 million: verification and approval by sub-national level departments• 1 million ≤ ODFI Projects < 30 million : verification and approval by the SPC• ODFI Projects ≥ US$ 30 million: verification and approval by the SPC; report to the State Council

• Before the project proposal application: ask for advices from the embassies and consulates in thetarget countries

• submitting the project proposal and feasibility reports

Source: “Opinion of the State Planning Commission on the strengthening of the administration of overseas investment projects”;“Regulations on examination and approval of project proposal and feasibility report on FDI projects”, the State Planning Commission

● According to UNCTAD FDI Statistic Database, by the end of 1999, China'scumulative OFDI stock had reached 26.853 billion U.S. dollars, accountingfor 0.52% of the world's total stock and 3.7% of developing countries totalstock; in 1999, China's OFDI flow was 1.774 billion U.S. dollars, accountingfor 0.16% of the world's total flow and 2.59% of developing countries totalflow, which was still at very low level compared with the other countries.

2.3 Going global and policy enthusiasm phase: 2000s

● since the entry to WTO in 2001, the businessenvironment for Chinese enterprises has changed

● The concept of “Going Global” was first officiallyinitiated by former Premier Minister Zhu Rongji in his2000 report to the National People’s Congress. It thusbecame an important part of the 10th National Economicand Social Development Five Year Plan (2001-2005).The “Going Global” strategy was stressed again in thecurrent 11th Five-Year Plan in 2006 by Premier MinisterWen Jiabao.

● In this period, there started to have OFDI Policy framework and guideline(See box 3).

Box 3(a) China’s OFDI Guidelines in the 10th Five Year Plan (2001-2005)

• achieving stage of using domestic and foreign resources and markets• Encouraging outward investment that can benefit China’s comparative

advantage, widen the areas, channels and methods of economic and technicalcooperation

• Supporting the transnational operations of competitive enterprises• Providing help in the areas of loans, insurance, etc.• Monitoring the formulation and regulation of the system of supervision for

domestic enterprises going abroad to invest• Improving the administration and investment services of Chinese companies

abroad

Box 3 (b) China ’s OFDI G uidelines in the 11th Five Year Plan (200 6-2010)

The encourag ed OFDI include:

! those can obtain scary resources or raw materials that national

economy urgently requires

! those can stimulate the export of pr oducts, equipment or

technology, and labour service that China has a comparative

advantage

! those can raise China’s technological R&D capability, and which

can make use of internationally advanced technology, advanced

management exper tise and speciali sed human resources

The pr ohibiting OFDI include:

! those threaten China’s national security or damage the public

interest of society

! those use proprietary techniques or technology the export of

which has been prohibited

! those the law of the recipient country prohibits and tho se

prohibited by the provisions of international treaties which China

has signed

Apart from the encouraged and prohibited sectors all others are

“permitted”

Source: Freeman, 2008

● Lots of policy documents toward China’s OFDI were released during the 2000s.

• One of the core policy documents was released by National Development andReform Commission (NDRC) in October 2004, “The Procedure of Verificationand Approval of Overseas Investment Projects”. The official thresholds forverification and approval of investments were stipulated (See box 4).

Box 4 Thresholds for Verification and Approval of China’s OFDI during 2000s

Source: The Verification and Approval of Overseas Investment Projects Tentative Administrative Procedures , NDRC

Overseas investment in natural resources:

! US$ 30 million: verification and approval by the NDRC

! US $ 200 million: verification and approval by t he NDRC; report to the

State Council

< US$ 30 million: verification and approval by Development and Reform Dept.

on provincial level

Overseas investment non -resources sector:

! US $ 10 million: verification and approval by the NDRC

! US $ 50 million: verification and approval by the NDRC; report to the State

Council < US$ 10 million: verification and approval by Development and Reform Dept.

on provincial level

Regulation for overseas investment for SOEs

< US$ 30 million, resource de velopment: independent decision by enterprises

< US$ 10 million, other investment: independent decision by enterprises

• Another core policy document we should pay attentions to wasreleased by the Ministry of Commerce (MOFCOM) in 2009“The Administration on Outbound Investment”, which pointedout the national and provincial level MOFCOM approvalrequirements towards China’s OFDI.

Box 5 National and Provincial level MOFCOM Approval Requirements during 2000s

National level MOFCOM approval requirement:

! in countries with no diplomatic relations with China.

! in certain countries or regions (MOFCOM guidance on which

particular countri es or regions come within this category is due to be issued in the future).

! any investments of over US$100 million.

! investments spread over multiple countries.

! investments involving the establishment of offshore special purposes

vehicles. Provincial level MOFCOM approval requirement:

! amounts of more than US$10 million but below US$100 million.

! investments in the energy or mineral sector.

! investments that also need to attract other domestic investors. Source: The Administration Measures on Outb ound Investment , MOFCOM

● According to 2008 Statistical Bulletin of China’s OFDI, by the end of2008, nearly 8,500 domestic investing entities had established about 12,000overseas enterprises, spreading in 174 countries (regions) globally. China'scumulative OFDI stock had reached 183.97 billion U.S. dollars; China'sOFDI flow in 2008 was 55.91 billion U.S. dollar, which has been at veryhigh speed level compared with the other developing countries. At the endof 2009, the accumulation ODFI has reached to 220 billion US dollars.

3. China’s OFDI in the EU● China’s OFDI in the Europe is still relatively insignificant; there is only

5.13 billion US dollars OFDI stock to Europe countries at the end of 2008(See Graph 3).

Graph 3 Chinese OFDI Flow and Stock by Regions in 2008

0

20000

40000

60000

80000

100000

120000

140000

!"#$ !%&#'$ ()&*+, -$.#/

!0,&#'$

1*&.2

!0,&'$

3',$/#$

Regions

Milli

ons

of U

S$

4.*'5 67*8

Source: Statistic Bulletin of China’s OFDI (2008)

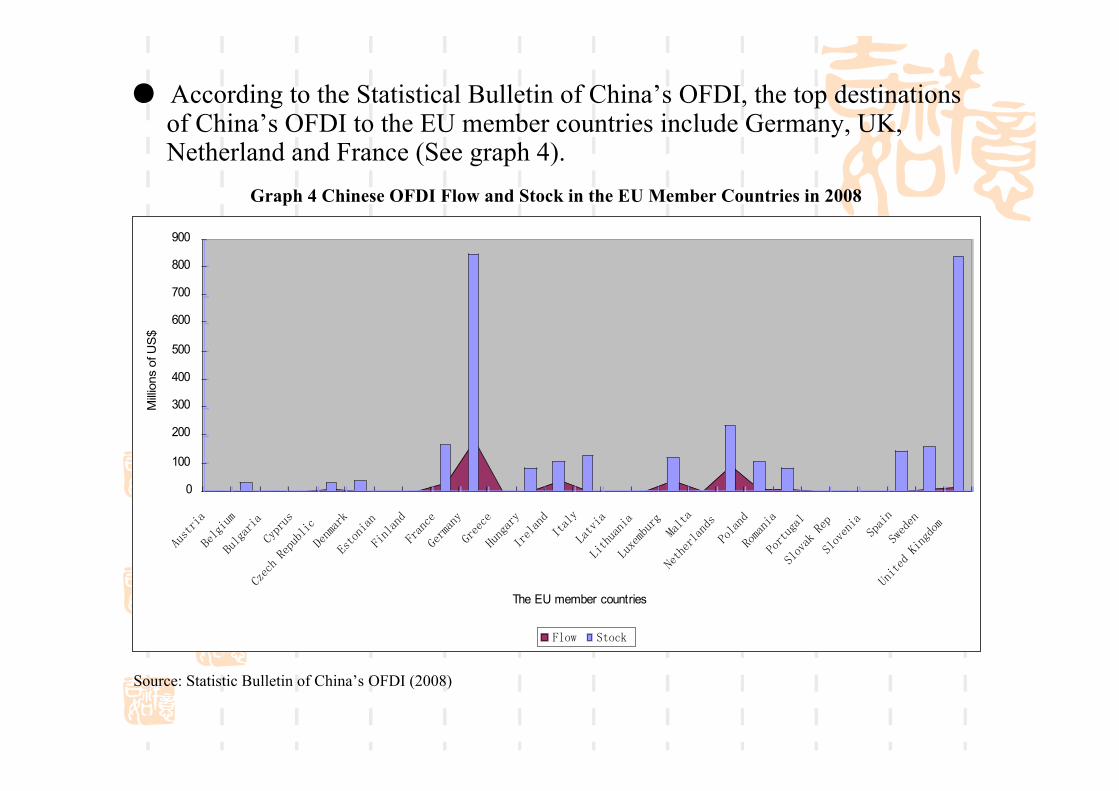

● According to the Statistical Bulletin of China’s OFDI, the top destinationsof China’s OFDI to the EU member countries include Germany, UK,Netherland and France (See graph 4).

Graph 4 Chinese OFDI Flow and Stock in the EU Member Countries in 2008

0

100

200

300

400

500

600

700

800

900

!"#$%&'

()*+&",

("*+'%&'

-./%"#

-0)1234)/"5*&1

6)7,'%8

9#$:7&'7

;&7*'7<

;%'71)

=)%,'7.

=%))1)

>"7+'%.

?%)*'7<

?$'*.

@'$A&'

@&$2"'7&'

@"B),5"%+

C'*$'

D)$2)%*'7<#

E:*'7<

4:,'7&'

E:%$"+'*

F*:A'834)/

F*:A)7&'

F/'&7

FG)<)7

H7&$)<3I&7+<:,

The EU member countries

Mill

ions o

f U

S$

;*:G F$:18

Source: Statistic Bulletin of China’s OFDI (2008)

● In term of industry distributions, China’s OFDI in the EU mainly focus onthe area of business service, manufacturing, finance, retailing andwholesaling (See graph 5, graph 6).

Graph 5 Industrial Distributions of China’s OFDI Flow in the EU (2008)

!"#$%&

'(#!%&

)*#!%&

)+#!%&

,-./01..2.134/51 670-8759-3/0: ;/07051 <9=13.

Source: Statistic Bulletin of China’s OFDI (2008)

Graph 6 Industrial Distributions of China’s OFDI Stock in the EU (2008)

!"#$"%

&$#'"%

&(#("%

!(#""%

&$#$"%

)*+,-.++/+.01,2. 34-*5426*0,-7

8,-4-2. 9.64,:,-7/4-;/<=>:.+4:,-7

?6=.0+

Source: Statistic Bulletin of China’s OFDI (2008)

3.1 Administration actors taking effect to China’s OFDI in the EU

● The main administrative actors include the State Council, the People’s Bankof China, the Ministry of Commerce, the National Development and ReformCommission, the State Asset Supervision and Administration Commission,the State Administration for Foreign Exchange. The basic mechanism ofinvolvement can be depicted as follows (See figure 1).

Figure 1 Basic Mechanism of Administration Actors and Main Players

State Council

PBC

SAFE

MOFCOM NDRC SASAC

State Level

Ministry Level

Vice Ministry Level

Administration

Actors

Main Players

Special Commission

CIC

State Owned Enterprises

Private Owned Enterprises

Policy Stimulations

Information Feedbacks

● The State level actor: the State Council

• The State Council has played a central leadership role in encouraging OFDIand liberalizing various measures that in turn stimulate overseasinvestments. It pays more attention to the blueprinting of China’s overallOFDI trend in the long term, drafting China’s OFDI guidelines and policiesin the macroeconomic way.

• With the purpose of strengthening EU-China cooperation, in 2009, PrimeMinister Wen Jiabao met with European Commission President JoseManuel Barroso in Brussels and Nanjing, respectively.

● The ministry level actors:• The People's Bank of China (PBC)

• The Ministry of Commerce (MOFCOM)

• The National Development andReform Commission (NDRC)

• The State Asset Supervision andAdministration Commission (SASAC)

● The vice ministry level actor:• The State Administration of Foreign Exchange (SAFE)

3.2 Main players of China’s OFDI in the EU● Foundation stones: state owned enterprises (SOEs)• Central enterprises are actively implementing the "Going Global" strategy.

According to statistics,to the end of 2008, 104 central SOE had set up 969overseas branches, including 4,141 subsidiaries and 828 organizations.

• Case Analysis: Nanjing Automobile (Group) Corporation taking overRover.

NAC bought the failed British carmaker MG Rover in July 2005 for 97million U.S. dollars.

● Active ingredients: private owned enterprises (POEs) • On one hand, POEs often have more limited financial resources, fewer

capabilities and know-how, less formal business education, fewereconomies of scale and scope, and less access to cutting-edge technology.They may also experience difficulties in obtaining access to investment andcredit facilities. On the other hand, POEs’ flexibility and creativity are theircompetitive advantages.

• Case Analysis: SANY Heavy Industry’s Greenfield investment inGermany. According to the agreement, SANY would invest 100 millionEuros to build a research and development center and mechanicalmanufacturing foundation in Koln, Nordrhein-Westfalen of Germany.

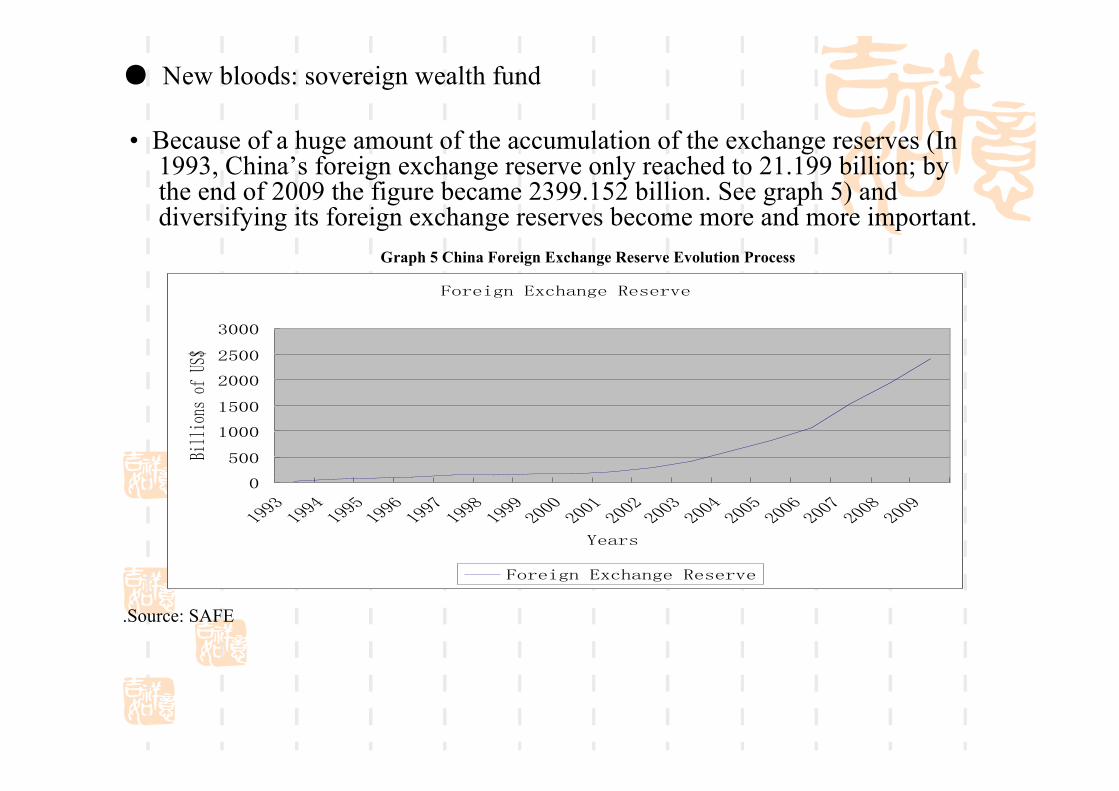

● New bloods: sovereign wealth fund

• Because of a huge amount of the accumulation of the exchange reserves (In1993, China’s foreign exchange reserve only reached to 21.199 billion; bythe end of 2009 the figure became 2399.152 billion. See graph 5) anddiversifying its foreign exchange reserves become more and more important.

Graph 5 China Foreign Exchange Reserve Evolution Process

.Source: SAFE

!"#$%&'()*+,-'&$(.$/$#0$

1

211

3111

3211

4111

4211

5111

36653667366236683669366:366641114113411441154117411241184119411:4116

;$-#/

<%==%"'/(">(?@A

!"#$%&'()*+,-'&$(.$/$#0$

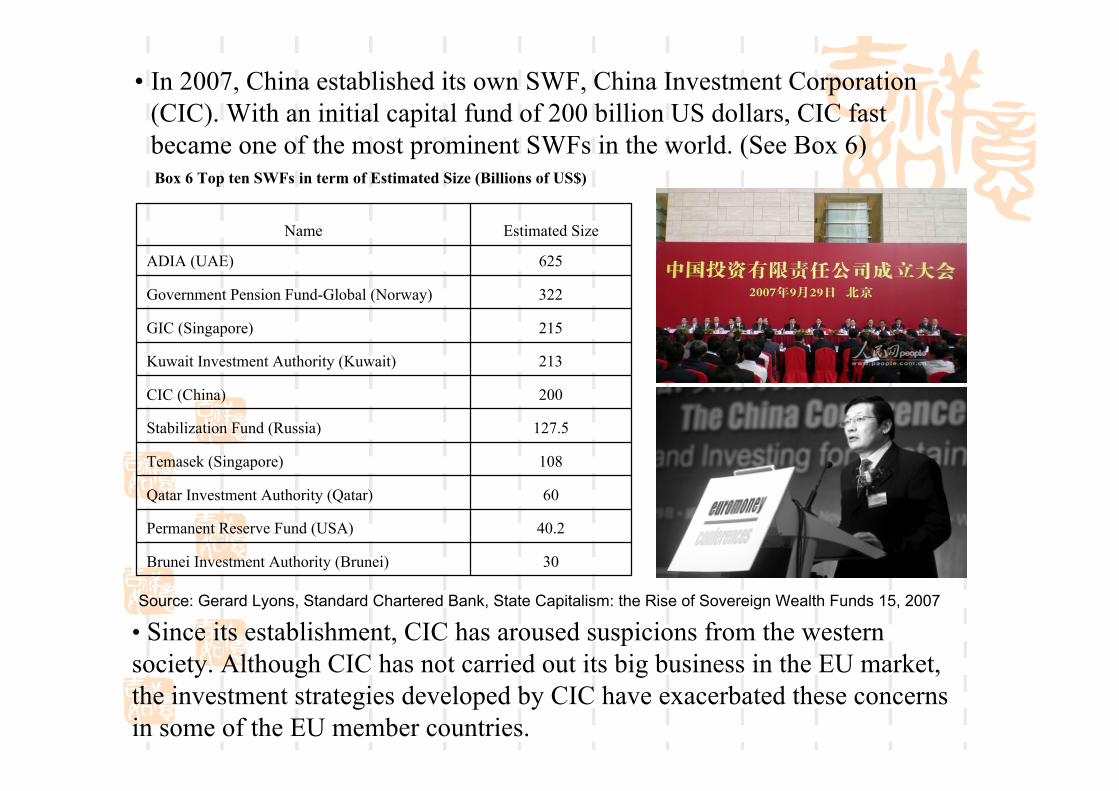

• In 2007, China established its own SWF, China Investment Corporation(CIC). With an initial capital fund of 200 billion US dollars, CIC fastbecame one of the most prominent SWFs in the world. (See Box 6)Box 6 Top ten SWFs in term of Estimated Size (Billions of US$)

30Brunei Investment Authority (Brunei)

40.2Permanent Reserve Fund (USA)

60Qatar Investment Authority (Qatar)

108Temasek (Singapore)

127.5Stabilization Fund (Russia)

200CIC (China)

213Kuwait Investment Authority (Kuwait)

215GIC (Singapore)

322Government Pension Fund-Global (Norway)

625ADIA (UAE)

Estimated SizeName

• Since its establishment, CIC has aroused suspicions from the westernsociety. Although CIC has not carried out its big business in the EU market,the investment strategies developed by CIC have exacerbated these concernsin some of the EU member countries.

Source: Gerard Lyons, Standard Chartered Bank, State Capitalism: the Rise of Sovereign Wealth Funds 15, 2007

3.3 Motivations and obstacles

3.3.1 Motivations analysis

(1) The forerunner standpoint versus the latecomer standpoint

● The forerunner standpoint in transnational business assumes thatmultinational enterprises will internationalize on the basis of strongcompetitive advantages that allow them to secure enough return to coverthe additional costs and risks associated with operating abroad.

● The latecomer standpoint lies in the way it directs attention to internationalinvestment as a means of addressing competitive disadvantages.

● It is significant that latecomer enterprises from China did not start frompositions of strength, but rather ‘from the resource-meager position of anisolated firm seeking some connection with the technological and businessmainstream’.

(2) The internal pressures and the external attractions

● The first perspective: the deteriorating of the domestic investmentenvironment.

• MNEs from developed countries have seized more of China’s domesticmarket share by using their monopoly advantages. The survival anddevelopment spaces of domestic enterprises have been squeezed by theseglobal competitors

• Some China’s enterprises take advantage of the outbound leg of round-tripping.

● The second perspective: the attractions from the EU market environment.

• Good market environments in the EU

• High quality strategic-assets of the companies in the EU

3.3.2 Obstacles analysis

(1) At the EU level, policy discriminations and protection behaviors can be themost serious obstacles toward China’s MNEs.

(2) At the firm level, we can use Dunning’s eclectic paradigm to explain whatkinds of obstacles Chinese MNEs will meet when they pursuit theiroverseas operations in the EU market. (See figure 2)

Figure 2 Basic Mechanisms of Motivations and Obstacles in the EU Member Countries

Parent Enterprises

Psychical Distance

Weak Public Relations Abilities

Policy Discriminations

Self -interest Seeking

EU Market s EU Enterpr ises Overseas Subsidiaries

The European Commission

Market -Seeking Strategic -Asset Seeking

Internalization -specific Disadvantages

Ownership -specific Disadvantages

Reverse Transfer Obstacles

Liability of Foreignness

Market Protection Behaviors Enterprises Protection Behaviors

EU Enterprises Unfamiliarity

Chinese Government Domestic Market Policy Stimulations Saturation Pressures

Internal Environment s

Ex ternal Environment s

EU Market s Unfamiliarity

Cognitive Gap Location -specific Disadvantag es

Poor After -acquisition Management

● Ownership-specific disadvantages: the cognitive gap and the poor after-acquisition management

• Ownership-specific advantages mainly contain property rights orintangible assets, such as patents, trademarks, organizational and marketingexpertise, production technology, and management and generalorganizational abilities, which form the basis for a company's advantageover other firms.

• Compared with the local European competitors, China’s MNEs lack ofOwnership-specific advantages when they carry out their business in theEU markets.

• Ownership-specific disadvantages can lead to a cognitive gap betweenlocal consumers and the Chinese products.

• Case Analysis: Zhejiang YANKON Greenfield investment in Belgium • Ownership-specific disadvantages can cause the poor after-acquisition

management. • Case Analysis: TCL takeover of Thomson

● Location-specific disadvantages: the liability of foreignness (the spatialdistance and the psychical distance)

• Location-specific advantages mean that the more the immobile, natural orcreated endowments-which firms need to use jointly with their owncompetitive advantages, favor a presence in a foreign, rather than adomestic, location-the more firms will choose to augment or exploit theirownership-specific advantages by engaging in OFDI.

• China’s MNEs should deal with the liability of foreignness, especially toovercome the psychical distance.

• Case Analysis: SANY Belgium Holdings SA

● Internalization-specific disadvantages: the reverse transfer obstacle and theself-interest behavior

• Internalization-specific advantages avows that the greater the net benefitsof internalizing cross-border intermediate product markets, the more likelya firm will prefer to engage in foreign production itself, rather than licensethe right to a foreign firm.

• From the parent enterprises point of view, since the absence themselves ofthe EU markets; they cannot optimize their resources and powers betweenthe parent companies and the overseas subsidiaries.

• From the overseas subsidiaries point of view, the self-interestconsideration may lead to the obstacles of communications, and the usefulmarket information cannot feed back to the parent enterprises, bringingabout the reverse transfer obstacles.

• Case Analysis: Hainan Airline Belgium

4. Conclusion

● China’s OFDI in the EU is still relatively insignificant.

● Compared to the global competitors, most China’s MNEs develop OFDI inthe EU member countries to address a relative disadvantage rather thanusing their competitive advantages.

● China’s MNEs are facing increased competition and declining profitmargins in the home market.

● When investing in the EU, China’s MNEs mainly play as market seekersand strategic asset seekers, and their investment business faces someinternal and external obstacles and pressures, it takes time for them toreally integrate into the EU market.

● Mutual understandings between the EU and China to foster a bilateralreciprocity environment for investment are imperative.

•

Thank you!