china’s innovation hurdle: competition and finances... · property rights (iprs) is poorly...

TRANSCRIPT

China’s Innovation Hurdle: Competition and Finance☆

Junhong Yang

Management School, University of Sheffield,

Conduit Road, Sheffield S10 1FL, United Kingdom

Bo Pan

Management School, University of Sheffield,

Conduit Road, Sheffield S10 1FL, United Kingdom

Abstract

Using a large panel of Chinese industrial firms over the period 1998–2007, this study

investigates the extent to which industry competition affects firms’ innovation activities in

China. We find that firm-level innovation is negatively related to industry competition, and the

negative relation is stronger in industries that are more dependent on external finance. Further

evidence shows that the negative effect in these industries and the R&D-cash flow relationship

are more pronounced for financially constrained firms than for their financially healthier

counterparts. To mitigate endogeneity concerns and identify the causality between innovation

and competition, we exploit the exogenous shift in industrial openness to foreign investment

resulting from China’s WTO accession in 2001 using a difference-in-differences (DID)

approach. Our findings suggest that firms in industries with a reduction in foreign investment

restrictions were less likely to innovate because of increased competition. The results are robust

to the use of various specifications and estimation methods. Our paper provides new insights

into the real causal effects of competition and finance on innovation.

JEL classification: D40; G31; L13; O16; O31; O53

Keywords: Competition; Firm-level innovation; China; External finance dependence; Financial

constraints; Difference-in-differences

☆ We are grateful for valuable help and comments from Alessandra Guariglia, Christopher Baum, Sumon

Bhaumik and the conference participants at the Eastern Finance Association (EFA) 2018 annual meeting

(Philadelphia), the Chinese Economists Society (CES) 2018 North American conference (Athens), the 45th

European Association for Research in Industrial Economics (EARIE) annual conference (Athens), the

International Finance and Banking Society (IFABS) 2017 Asian conference (Ningbo), the 28th Chinese Economic

Association (CEA) UK and 9th Europe 2017 annual conference (Manchester), the 4th Young Finance Scholars

2017 conference (Brighton) and the Development Economics 2017 conference (Lincoln), as well as from seminar

participants at the University of Sheffield, Newcastle University, Durham University and the University of

Manchester. Junhong Yang acknowledges the Research Stimulation Funding of Sheffield University Management

School (SUMS). All errors remain our own. Corresponding author.

E-mail address: [email protected] (J. Yang); [email protected] (B. Pan)

1

1. Introduction

Innovation is a crucial means for business firms to establish competitive advantages and

for a country to ensure long-term economic growth (Solow, 1957; Porter, 1991). However,

information problems and high uncertainty risk tend to discourage firms from innovating

(Holmstrom, 1989; Aboody & Lev, 2000; Harhoff, 2000). Given these difficulties, scholars

have explored ways to effectively promote innovation from various perspectives (Romer, 1990;

Aghion & Howitt, 1992; Brown et al., 2009; Acharya & Xu, 2017; Rong et al., 2017). To shed

light on the understanding of China’s innovation hurdle in competition, in this study we

investigate the extent to which industry competition affects firms’ innovation activities.

Furthermore, we link this with industry-level external finance dependence (EFD) and firm-

level financing constraints challenging firms’ innovation activities.

Following approximately 40 years of reform and opening-up, especially after the

country’s entry into the WTO in 2001, the Chinese economy has transformed in almost every

respect. It has gone from being one of the most closed and isolated economies in the world and

of little relevance to the global economy to being both highly globalized and the world’s

second-largest economy.1 However, China’s fast growth which is mainly driven by huge

investments displays some shortcomings such as low quality, low profits and high pollution. A

large number of firms have grown up by following opportunistic strategies and focusing on the

short term. They have found investment in innovation less attractive than pursuing short-term

profits such as by diversifying into unrelated industries (Rong et al., 2017). There is now

concern about China’s slowing economic growth. 2 In recent years, the importance of

innovation in sustaining high growth in the future has been recognized, and innovation-driven

(rather than investment-driven) growth has been emphasized. The Chinese government has

launched many top-down innovation-related policies (Chen & Naughton, 2016). 3 While

innovation in China has made tremendous strides forwards,4 it still faces various challenges.

1 China’s Gross Domestic Product (GDP) maintained a high growth rate of around 10% per annum from 1978 to

2014. 2 China’s GDP growth has slowed below 7% per annum since 2014. 3 For instance, the State Council of China put forward a ‘National Program for Long- and Medium-Term Scientific

and Technological Development’ in 2006. To fight against the slowing economic growth rate, the Chinese

government adopted a ‘Made in China 2025’ strategy in 2015 to further promote innovation. 4 According to OECD reports (2018), China’s gross spending on research and development (R&D) increased from

0.725% of GDP (1991) to 1.445% (2008) and even to 2.118% (2016). China’s total gross spending on R&D in

2016 is 411,993 million US dollars, which is higher than that of most of the developed economies including the

EU (350,297 million US dollars) but only lower than that of the US (464,324 million US dollars). In addition, the

OECD (2017) shows that China’s business enterprise R&D expenditure dramatically increased from 19,030

million US dollars (2000) to 305,501 million US dollars (2015).

2

For example, statistics show that in 2015 the number of researchers per 1,000 employees in

China was only 2.09. This figure is lower than the average value for all OECD members (8.29)

and that for most developing economies such as Argentina (2.93), Poland (3.61) and Latvia

(4.07). Regarding its number of triadic patent families, in 2015 China had 2,889 and was far

behind most of the developed economies such as the EU (13,599), the US (14,886) and Japan

(17,360). These disadvantages suggest a low return on R&D spending in China and a weak

input-output efficiency of China’s innovation activities. In criticism of its lack of innovation,

China has often been portrayed as a land of copycats where the protection of intellectual

property rights (IPRs) is poorly enforced (Allen et al., 2005; Ang et al., 2014).5 The phrase

‘Made in China’ is often thought to signify cheap, low-quality and counterfeit goods. Overall,

there is a compelling necessity to understand the obstacles to innovation in China.

According to Schumpeter (1943), competition is one of the crucial factors that drive

innovation. In China, there has been a considerable change in the intensity of industrial

competition. Before 1978, Chinese firms faced less market competition due to the domination

of the state-owned capital market, the mandatory planning economy and the seclusion policy.

The policy of ‘reform and opening-up’ after 1978 not only greatly spurred China’s economic

development but also altered the intensity of market competition. A surge in private and foreign

ownership in China dramatically increased the intensity of market competition.6 Therefore, in

this unique Chinese context, it is important to explore the mechanism behind the relationship

between innovation and competition. Although there is a theoretical foundation, i.e. the

‘Schumpeterian effect’ for understanding this relationship (Schumpeter, 1943), there remains

a lack of intellectual consensus. Several scholars assert that there is an inverted-U relationship

between competition and innovation, e.g., Aghion et al. (2005), while a few claim the

relationship is linear and can be either positive (Nickell, 1996; Blundell et al., 1999) or negative

(Romer, 1990; Aghion & Howitt, 1992; Hashmi, 2013). To date, the existing literature on the

relationship between competition and innovation mainly focuses on Western developed

countries, while studies on emerging markets such as China are still sparse. Given the important

5 Until 2018, the US had targeted China with six ‘Section 301 investigations’ and nearly all of them involved

China’s intellectual property protection, as did Trump’s China tariffs in 2018. 6 The increased intensity of China’s market competition is reflected in a rise in the number of corporations. For

instance, in recent years the number of corporate units increased sharply from 6,517,670 (2010) to 12,593,254

(2015) and the number of private corporate units increased from 5,126,438 (2010) to 10,677,612 (2015). (Data

from the National Bureau of Statistics of China,

http://data.stats.gov.cn/easyquery.htm?cn=C01&zb=A010401&sj=2005). Furthermore, since 2004 China has

been the second largest recipient of foreign direct investment (FDI) in the world. This substantive FDI also

contributes to intense competition in China.

3

role of innovation in shaping growth strategies in emerging markets and the dramatic change

in market competition in China, this issue deserves in-depth investigation.

In this paper, we explore a very large dataset covering the period 1998-2007 compiled by

the National Bureau of Statistics (NBS) of China. This large unbalanced panel of 1,957,772

observations covers 555,124 Chinese firms in all manufacturing, mining and public utility

sectors in 31 provinces or province-equivalent municipalities. To measure firms’ innovation

activity, we use the ratio of their new product output values to their total assets. To compute

the intensity of industry competition we use four measures: the Herfindahl-Hirschman Index

(HHI), the Entropy Index (EI), the Lerner Index (LI)/Profit-Cost Margin (PCM) and the natural

logarithm of the number of firms (FI). We find that firm innovation is discouraged in sectors

where competition becomes more intense. Specifically, our main regressions show that a 10%

increase in industry competition reduces the probability that a firm innovates by between 0.12%

and 3.49% and reduces innovation output by between 0.03% and 0.92% for innovative firms,

depending on which measure of competition we use.

Due to the imperfections in China’s capital market and the important role of external

finance in R&D activities (Guariglia & Yang, 2016), we further exploit two important financial

factors: industry-level external finance dependence and firm-level financing constraints. We

find that the negative effect of competition on innovation activities is significantly stronger for

firms in more externally dependent industries. Furthermore, we find that the strengthening of

the negative impact of competition on innovation in industries with higher EFD is more

pronounced for financially constrained firms: private firms, small firms, young firms, firms

without state shares and firms in the central and western regions. Financially constrained firms

rely more on internal finance to fund their innovation activities and exhibit a higher sensitivity

of R&D investment to cash flow.

To overcome endogeneity concerns and identify the causality between innovation and

competition, we exploit an exogenous shock to competition intensity. After China’s WTO

accession in December 2001, the National Development and Reform Commission of China

(NDRC) revised its ‘Catalog for the Guidance of Foreign Investment Industries’ (the Catalog)

in 2002. The Catalog revision had a significant impact on the intensity of competition across

industries since it made changes to restrictions on foreign investment, which can affect industry

competition intensity. In this quasi-experiment, we find that in response to the catalog revision

in 2002, firms in sectors where restrictions on foreign capital were lifted (the treatment group)

4

reduced their innovation output more than firms in sectors with unchanged or more restrictions

on foreign capital (the control group), which confirms our hypothesis according to which more

competition (associated with a lifting of restrictions on foreign capital) decreases firms’

innovation output. The magnitudes of our difference-in-differences (DID) results suggest that

firms in the automobile manufacturing sector (the treatment group) were about 6.64% less

likely to innovate than firms in the metal ship manufacturing sector (the control group) from

the pre- to post-revision periods. In addition, innovation output for the former was about 3.04%

lower than the latter following the exogenous catalog revision in 2002, which was associated

with a shift in industry competition intensity. Further tests show that the impact is enhanced in

industries that are more dependent on external finance. In addition, we use an instrumental

variables approach to address potential endogeneity concerns. Specifically, we use the number

of application procedures that a firm has to go through to enter a particular GB/T four-digit

sector as the instrumental variable for industry competition. We confirm a causal and negative

effect of industry competition on R&D activities.

Our results are also robust to the use of various specifications and estimation methods.

First, to mitigate concerns about omitted factors that may explain corporate innovation

activities, we include contemporaneous terms of independent variables in the main regression

equations that we estimate. Second, to control for potential measurement errors, we use the

ratio of firms’ R&D expenditure to their total assets as an alternative measure of their

innovation activities in estimations. Third, we break down the national market into eight

regional markets classified by the Chinese government in estimations. The results of these

additional tests are consistent with our main empirical findings. Finally, the results are

qualitatively unchanged when we measure different intensities of competition based on GB/T

two-digit or three-digit sector codes, balance our sample data, cluster standard errors by

industries rather than firms, and use time series industry-level EFD and firm-level EFD.

Our study contributes to the literature by providing evidence on a link between the real

economy and the financial sector and by offering insights into the real effects of competition

and finance on innovation. First, it contributes to the literature on competition. Our paper is the

first to use a large number of unlisted firms to explore the impact of competition on innovation.

It is distinct from but also complementary to previous literature, especially by studying an

emerging market. The majority of previous studies focus on Western developed countries, such

as the US (Schumpeter, 1943; Blundell et al., 1999; Hashmi, 2013) and the UK (Nickell, 1996;

Aghion et al., 2005). In addition, nearly all the papers that study the relationship between

5

competition and innovation focus on listed firms (Schumpeter, 1943; Romer, 1990; Nickell,

1996; Blundell et al., 1999; Aghion et al., 2005; Hashmi, 2013). A relatively small number of

listed firms are not representative and are likely to suffer from serious sample selection bias.

We provide new evidence on an emerging market based on a large panel of firms, 95% of

which are unlisted. Second, the paper also enriches the literature on firm innovation in China.

Many scholars have tested various factors related to innovation in China such as institutional

ownership (Rong et al., 2017), R&D subsidies (Boeing, 2016), total factor productivity (Boeing

et al., 2016) and financial constraints (Guariglia & Liu, 2014). Using a large sample of unlisted

firms, our paper explores firm innovation from the perspective of competition in China. Third,

for the first time in the Chinese context, we extend existing research by investigating two

important factors (industry-level external finance dependence and firm-level financing

constraints) that influence the effect of competition on innovation. Fourth, our study provides

clear identification of a causal effect of competition on innovation by setting up a quasi-

experiment based on China’s WTO accession in 2001. Fifth, our analysis provides

microeconomic evidence for the debate on the competition-finance-growth nexus in an

emerging market, as innovation is a key engine of economic transformation. Based on our

empirical findings, we push the causality debate one step further by finding evidence for

channels through which competition and finance influence innovation. We also propose a

number of policies aimed at establishing a policy-related finance system and stimulating firms’

innovation activities in China.

The remainder of the paper is structured as follows. In Section 2 we review relevant

previous literature. In Section 3 we develop testable hypotheses. In Section 4 we construct our

key variables. In Section 5 we describe our dataset and report summary statistics. In Section 6

we illustrate our model specifications. In Section 7 we discuss our main empirical results. In

Section 8 we show further robustness tests and extensions. Finally, we conclude in Section 9.

2. Literature review

2.1. Competition and innovation

Past research has investigated the effect of competition on innovation (Schumpeter, 1911;

Schumpeter, 1943; Scherer, 1967; Nickell, 1996; Blundell et al., 1999; Aghion et al., 2005;

Hashmi, 2013). On the one hand, Schumpeter (1943) proposed the ‘Schumpeterian effect,’ a

6

theory that predicts a typically negative correlation between competition and innovation. To be

specific, the ‘Schumpeterian effect’ is that innovation should drop with increased competition

because more competition decreases the monopoly rents that reward successful innovators.

Aghion et al. (2013) suggest that market competition can impose short-term financial pressure

on managers and exacerbate managerial myopia. Thus, firms in competitive industries have to

innovate less to generate short-term profits. On the other hand, some scholars predict a positive

relationship between competition and innovation, called the ‘escape-competition effect.’ This

can be explained as competition tending to stimulate the incremental profits from innovating,

and so firms may prefer to invest in innovation to escape competition (Nickell, 1996; Blundell

et al., 1999).

Several studies have also tried to reconcile the two effects and develop a nonlinear

relationship between competition and innovation (Scherer, 1967; Levin et al., 1985; Aghion et

al., 2005; Hashmi, 2013). For example, Aghion et al. (2005) find an inverted U-shape

relationship between competition and innovation using an unbalanced panel of 311 UK firms

over the period 1973-1994. Specifically, they show the two effects operating step by step. In

the first step, in ‘neck-and-neck’ sectors when market competition is not severe, the ‘escape-

competition effect’ dominates. Thus innovation rises with more competition. In the second step,

in ‘laggard-and-laggard’ (or ‘less neck-and-neck’) sectors when market competition is intense,

the ‘selection effect’ or ‘Schumpeterian effect’ dominates. At this time, more competition

decreases innovation. Meanwhile, as competition increases, more sectors move from ‘neck-

and-neck’ to ‘laggard-and-laggard.’ In addition, Hashmi (2013) revisits the inverted-U

relationship of Aghion et al. (2005) by controlling for the possible endogeneity of competition

and finds a mildly negative relationship between competition and innovation for US firms,

which is contrary to the inverted-U relationship found for UK firms.

2.2. External finance dependence and innovation

Firms fund their R&D projects either through internal or external finance (Brown et al.,

2009; Mina et al., 2013). Internal finance is favoured over external finance due to a power

imbalance in obtaining information and the adverse selection and moral hazards of the latter

caused by the information asymmetry between internal managers (insiders) and external

investors (outsiders) (Jensen & Meckling, 1976; Myers & Majluf, 1984; Jensen, 1986; Aboody

& Lev, 2000; Brown et al., 2009; Ayyagari et al., 2011). However, reflecting the long-term and

continual nature of R&D investment with sunk costs, firms have to use external finance to fund

7

their innovation investments (Pindyck, 1993; Bernstein & Mohnen, 1998). Since innovative

projects lack collateral value and are difficult to evaluate, the information disadvantage of R&D

investment results in costly external financing premiums (Stiglitz, 1985; Aboody & Lev, 2000;

Harhoff, 2000). R&D investment is sensitive to external finance shocks. In industries that are

highly dependent on external finance, if the external finance premium becomes higher firms

may have to forego innovation activities (even with positive present value) because of the

higher financing pressure. Past research has emphasized the role of external finance

dependence in different economic respects. For example, by studying a large sample of

countries over the 1980s, Rajan & Zingales (1998) find that financial development facilitates

economic growth, especially in industries with more need for external finance, since financial

development can reduce the cost of raising external funds for firms. Almeida & Wolfenzon

(2005) develop an equilibrium model to show that an increase in firms’ external financing

needs improves their capital allocation efficiency. Duygan-Bump et al. (2015) find external

finance dependence tightens the link between financing constraints and unemployment. Many

scholars have tried to link external finance dependence to innovation. Hsu et al. (2014) use a

large dataset covering 32 countries and find that better equity markets increase technological

innovation while the development of credit markets discourages innovation, especially in

industries that are more dependent on external finance. Cornaggia et al. (2015) find that bank

competition increases innovation for private firms that are dependent on external finance and

have limited access to credit from bank loans. Acharya & Xu (2017) find that public firms

spend more on R&D and generate a better portfolio than their private counterparts in external-

finance-dependent industries rather than internal-finance-dependent industries.

2.3. Financing constraints and innovation

Financing constraints have been explored regarding different aspects of firm investment,

including investment in fixed capital (Fazzari & Petersen, 1993), inventory (Blinder & Maccini,

1991; Guariglia & Mateut, 2010), employment (Sharpe, 1994; Nickell & Nicolitsas, 1999) and

acquisitions (Martin, 1996; Erel et al., 2015; Yang et al., 2019). Compared to other types of

investment, R&D is more susceptible to financing constraints as R&D investment is subject to

a high degree of uncertainty and a lack of collateral value (Pindyck, 1993; Bernstein & Mohnen,

1998; Brown et al., 2012). The features of R&D translate into a higher cost premium associated

with the use of external finance, particularly for smaller and younger firms. Such firms

typically face more severe information asymmetry in credit markets, which makes external

8

finance costlier or even impossible. Thus, innovation activities are particularly sensitive to the

degree of financing constraints that firms face. There are papers that explore the presence of

financial constraints on firms’ innovation activities. For developed markets, Brown et al. (2009)

test the presence of financial constraints by using the Euler equation and US data from 1990 to

2004. Hall (1992) and Himmelberg & Petersen (1994) find similar results using US data.

Similarly, Harhoff (2000), Savignac (2008) and Brown et al. (2012) find the existence of

financial constraints on R&D projects in Germany, France, and 16 European countries. For

emerging markets, Guariglia & Liu (2014) find the presence of financial constraints on firms’

innovation activities in China.

3. Developing hypotheses

In this section, we develop four testable hypotheses based on economic theories and

empirical findings. First, we examine whether there is a relationship between industry

competition and firms’ innovation activities in China. As industry competition increases, do

firms’ innovation activities decrease or increase? Second, we test the extent to which industry

external finance dependence affects the relationship between competition and innovation.

Third, we study whether firms’ financing constraints have an influence on the effect of

competition on their innovation activities in China. Fourth, we investigate the extent to which

the degree of financing constraints that firms face affects the R&D-cash flow relationship.

3.1. General industry competition hypothesis

Over 40 years of economic reform and rapid expansion of a market economy, there has

been a tremendous surge in the number of corporations (especially private corporations)

aggressively competing for profits in China. Therefore, the Chinese market has been

characterized by intense competition (Wu, 2012). Firms in competitive industries, e.g., in the

manufacturing sector, have to innovate less because of a lack of internal and external capital

available for their R&D investments. According to the ‘Schumpeterian effect,’ excessive

competition adversely affects firms’ short-term profits, then reduces their value, e.g., their net

asset value, and consequently affects both internal finance and external finance for innovation

projects (Schumpeter, 1943; Aghion et al., 2005). Specifically, first, poor profitability imposes

short-term pressure on managers and negatively affects the internal finance available for

innovation investment. Due to short-termism and myopic investment behavior (Bushee, 1998),

9

firms in competitive industries prefer investments which can generate short-term earnings to

long-term and uncertain investments such as R&D activities (Aghion et al., 2013). Second,

according to Bernanke & Gertler (1989), net asset value is inversely related to the external

finance premium that firms face since net assets are perceived as collateral to guarantee future

loan payments. Thus, when market competition becomes intense firms may have to forego

long-term innovation investment, as managers have to face more financial pressure caused by

the short-term low profitability and higher marginal costs of external financing (Holmstrom,

1989; Brown et al., 2009; Acharya & Lambrecht, 2015). In addition, according to the career

concern hypothesis (Holmström, 1999; Aghion et al., 2013; Rong et al., 2017), R&D

investment tends to be riskier when competition is more intense. The intuition is that innovation

is likely to be imitated by competitors when there is intense competition with more competitors.

This is particularly an issue in an emerging market (e.g., China) where the protection of

intellectual property rights is weak, and it frequently occurs. With a higher likelihood of

imitation, more competition is associated with a higher risk of R&D failure, which can

undermine managerial careers. Based on this career concern view, competition should

discourage firm innovation. We therefore hypothesize as follows:

Hypothesis 1: Industry competition is negatively and significantly related to firms’ innovation

activities. In the Chinese context, the more industry competition there is, the less firms innovate.

3.2. Industry external finance dependence hypothesis

According to our Hypothesis 1, severe competition in China’s market adversely affects

both internal and external finance for firms’ innovation activities. Such an impact could differ

for firms with different needs for external finance. Firms in industries with higher EFD may

become more vulnerable for three reasons. First, these firms do not have sufficient internal

capital for investments including innovation activities. Insufficient internal capital together

with fierce competition tends to increase the possibility of bankruptcy and reduce companies’

tolerance of failure in R&D activities, which impedes corporate innovation. Second, firms in

industries with higher EFD have to rely more on external finance to fund their R&D

investments. These firms tend to have higher gearing ratios. According to the trade-off theory

(Myers, 1984; Campbell & Kelly, 1994), a decline in the value of high-leverage firms resulting

from competition can lead to high potential bankruptcy and monitoring risks (Lopez-Garcia &

Puente, 2012), which in turn negatively impacts their borrowing costs for external funds.

Additionally, banks may impose pressure on firms with higher gearing ratios, which limits

10

corporate innovation. Third, R&D investment opportunities in industries with higher EFD are

accompanied by sparse information (Hsu et al., 2014). It is more difficult for banks to evaluate

innovative projects in more externally dependent industries due to information problems. This

accompanied with insufficient internal capital to service debt (Brown et al. 2012) means that

banks might refuse to finance innovation investment in more externally dependent industries.

Consequently, as industry competition increases, firms in these industries have to reduce

investment in long-term and uncertain R&D projects because of a lack of internal and external

finance for innovation. In contrast, firms in industries with lower EFD suffer less since they

can use more internal capital. The financial advantage of abundant internal capital for firms in

less EFD industries can alleviate the negative effect of higher external finance premiums

caused by increased competition (Byoun & Xu, 2016). Therefore, we put forward our second

hypothesis as follows:

Hypothesis 2: The negative effect of competition on innovation significantly increases with

the degree of dependence on external finance. In the Chinese context, industry competition will

discourage more firm innovation in industries with higher EFD.

3.3. Firm financing constraints hypothesis

Given the capital market imperfections characterizing China, Chinese firms face a high

premium for external finance and rely extensively on internal finance for R&D investment. For

instance, private firms and small and young firms face a high degree of financing constraints

due to the ‘lending bias’ problem in China.7 Oliner & Rudebusch (1996) show that financing

constraints have the effect of discouraging firms’ innovation projects. Financial constraints can

cause information asymmetries that are associated with innovation and impose financial

pressure on managers of firms when it comes to R&D investment, particularly for firms in

industries that rely more on external finance for R&D investment. As competition increases,

short-termism and a cost premium may force financially constrained firms to reduce their R&D

investment. In addition, as Himmelberg & Petersen (1994) and Brown et al. (2012) point out,

R&D investment is associated with high adjustment costs. In order to smooth R&D investment,

7 The most important reason for China’s ‘lending bias’ problem is its unique state-dominated financial system.

The ‘Big-Five’ commercial banks that have always been dominant players in the Chinese financial market are

owned by the state. State-owned enterprises (SOEs) with superior bank finance availability can gain financing

advantages over their private counterparts (Gu et al., 2008). The ‘Big-Five’ commercial banks in China are the

Bank of China Limited, the Agricultural Bank of China Limited, the Industrial and Commercial Bank of China

Limited, the China Construction Bank Corporation and the Bank of Communications.

11

R&D-intensive firms with financing constraints may have to rely more on their limited internal

finance than on external finance, making R&D investment sensitive to cash flow. In contrast,

financially healthier firms have better access to bank loans or other forms of external finance

and this financing advantage can alleviate the negative impact of increased competition in more

highly EFD and so smooth R&D. Consequently, financially healthier firms in more highly EFD

and competitive industries can innovate more than financially constrained firms. Additionally,

since financially healthier firms have better access to external finance, their R&D investments

will be less sensitive to cash flow. Therefore, the negative impact of competition on innovation

in more highly EFD industries and the positive impact of cash flow on innovation should exert

more influence on firms with more financing constraints rather than on their financially

healthier counterparts. Therefore, we propose our third and fourth hypotheses as follows:

Hypothesis 3: The negative effect of industry competition on innovation in more highly EFD

industries is stronger for financially constrained firms than for their financially healthier

counterparts. In the Chinese context, financing constraints will tighten the impact of

competition on innovation in more highly EFD industries.

Hypothesis 4: R&D investment by financially constrained firms will be more sensitive to cash

flow. In the Chinese context, financing constraints will tighten the relationship between R&D

and cash flow.

4. Variable measures

4.1. Measuring Innovation

In this paper, we define firm innovation activity as the ratio of the output value of a firm’s

new products to its total assets. In the China Statistical Yearbook (2006), new products are

defined as “those new to the Chinese market which either adopt completely new significant

principles, technologies or designs, or are substantially improved in comparison with existing

products in terms of performance and functionality, through significant changes in structure,

materials, design or manufacturing process.” New product output value has been widely used

in recent studies to quantify firms’ innovation activities (Henard & Szymanski, 2001; Guariglia

& Liu, 2014). Compared to R&D expenditure, new product output value has three advantages.

First, it is believed to be a better measure of innovation output and the level of efficiency of

12

innovation activities compared to R&D expenditure which is merely a measure of innovation

input (Criscuolo et al., 2010). Second, figures for R&D expenditure in the sample dataset are

only available from 2001 to 2007, while data on new product output value is available from

1998 to 2007.8 Third, according to a survey by Mckinsey & Co (2008), new product output

value is widely adopted to track the performance of firm innovation activities. However, we

also use the ratio of R&D expenditure to total assets as an alternative proxy for innovation in

Section 8.4 and estimate again. All the results are robust.

4.2. Measuring competition

To measure the level of competition, following the previous literature (Horowitz &

Horowitz, 1968; Nickell, 1996; Aghion et al., 2005; Cai & Liu, 2009) we construct four

measures: the Herfindahl-Hirschman Index (HHI), the Entropy Index (EI), the Lerner Index

(LI)/Profit-Cost Margin (PCM) and the natural logarithm of the number of firms (FI). These

four measures are based on GB/T four-digit sector codes.

4.2.1. Herfindahl-Hirschman Index (HHI)

Our first measure of industry competition is based on the Herfindahl-Hirschman Index

(HHI), which is well-grounded in industrial organization theory, competition law and antitrust

and technology management (Tirole, 1988; Brown & Warren-Boulton, 1988; Capozza & Lee,

1996). Specifically, following Nickell (1996) and Cai & Liu (2009), we compute the

competition intensity in industry 𝑗 by using one minus the sum of the squares of all firms’

market shares in the industry. We define the HHI industry competition intensity as follows:

𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡 [𝐻𝐻𝐼] = 1 − ∑ 𝑆𝑖.𝑗,𝑡2𝑁𝑗

𝑖=1,𝑖∈𝑗= 1 − ∑ (

𝑋𝑖,𝑗,𝑡

𝑋𝑗,𝑡)2𝑁𝑗

𝑖=1,𝑖∈𝑗 , (1)

where subscript 𝑖 indexes firms, 𝑗 industries and 𝑡 years (𝑡 = 1998-2007). Thus 𝑆𝑖,𝑗,𝑡 is the

market share of firm 𝑖 in industry 𝑗 in year 𝑡. Market shares are computed based on firms’ main

business product sales (Cornaggia et al., 2015).9 𝑋𝑖,𝑗,𝑡 represents the value of sales of the main

business product of firm 𝑖 in industry 𝑗 in year 𝑡 , and 𝑋𝑗,𝑡 represents all the main business

8 Data on both new product output values and R&D expenditure are missing for 2004. To impute these missing

data, we use the average of the values for 2003 and 2005 and estimate again for robustness tests. The results

remain unchanged. 9 We also use firms’ total assets to calculate their market shares (Giroud & Mueller, 2010) for a robustness test.

The estimation results are not reported for brevity but remain qualitatively unchanged.

13

product sales in industry j in year t. To build a positive indicator of industry competition, we

subtract the industry HHI from one. Thus, the HHI index industry competition

(𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡 [𝐻𝐻𝐼]) takes a value between 1 and 0. 1 indicates perfect competition (no

monopoly) and 0 suggests perfect monopoly (no competition). A higher value of

𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡 [𝐻𝐻𝐼] represents a higher degree of industry competition.

4.2.2. Entropy Index (EI)

Our second measure of industry competition intensity is the Entropy index (EI).10 Like

the HHI, the EI is also computed using firms’ market shares. Compared to the HHI, the EI has

three unique features. First, it gives more weight to small businesses and so it sensitively

reflects the influence of changes in small-scale enterprises in the market. By contrast, the HHI

is more influenced by large firms (Haushalter et al., 2007). Second, the HHI is an inverse

indicator of industry competition intensity, while an industry with a higher value of the EI can

be understood to be more highly competitive. Third, the distribution range of the HHI is from

0 to 1, while the EI has no numerical distribution limit. The EI competition intensity for

industry 𝑗 (𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡 [𝐸𝐼]) is calculated as:

𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡 [𝐸𝐼] = 𝑙𝑜𝑔(1

𝐸)𝑗,𝑡 = ∑ 𝑋𝑖,𝑗,𝑡

𝑁𝑗

𝑖=1,𝑖∈𝑗[𝑙𝑜𝑔(

1

𝑋𝑖,𝑗,𝑡)] , (2)

where 𝑖, 𝑗, 𝑡 and 𝑋𝑖,𝑗,𝑡, are the same as in equation (1).

4.2.3. Lerner Index (LI) or Profit-Cost Margin (PCM)

Our third measure of industry competition is the Lerner Index (LI) or Profit-Cost Margin

(PCM). A firm’s LI is defined as its product’s price minus its marginal costs divided by the

price (Nickell, 1996; Aghion et al., 2005; Leon, 2015). However, we are not able to compute

marginal costs because the data are not available in our dataset.11 Following Peress (2010), we

10 A number of scholars have used the Entropy Index to measure income inequality in Europe (De la Fuente &

Vives, 1995; Duro & Esteban, 1998). Horowitz & Horowitz (1968) suggest that the EI is not only a measure of

industry concentration but also has the valuable property of being truly analogous to industry competition. 11 One difficulty in the specific computation process is that marginal costs are normally hard to observe in most

datasets so scholars have to choose an alternative proxy. For example, Aghion et al. (2005) define the LI as the

difference between operating profits and financial costs over sales. Cai & Liu (2009) use the ratio of total pre-tax

profit to total sales for GB/T four-digit industries to construct a measure of competition.

14

use the ratio of main operation profits to main operation sales (Profit-Cost Margin – PCM) to

construct the firm-level 𝐿𝐼 (𝑃𝐶𝑀)𝑖,𝑗,𝑡:12

𝐿𝐼 (𝑃𝐶𝑀)𝑖,𝑗,𝑡 =𝑀𝑎𝑖𝑛 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛 𝑃𝑟𝑜𝑓𝑖𝑡𝑠

𝑀𝑎𝑖𝑛 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛 𝑠𝑎𝑙𝑒𝑠=

𝑀𝑎𝑖𝑛 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛 𝑆𝑎𝑙𝑒𝑠 − 𝑀𝑎𝑖𝑛 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛 𝐶𝑜𝑠𝑡𝑠

𝑀𝑎𝑖𝑛 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛 𝑆𝑎𝑙𝑒𝑠 . (3)

To account for the impact of firm size, we subsequently compute the industry-level LI

(PCM) from the value-weighted (based on market share) average LI (PCM) across firms in an

industry (Peress, 2010; Leon, 2015). A higher level of an industry’s LI (PCM) indicates that it

has stronger market power or a higher concentration ratio (a weaker degree of competition).

As with the HHI in Section 4.2.1, in order to build a positive indicator of industry competition

intensity we use 1 minus the industry-level LI (PCM) to construct the measure of competition

in industry 𝑗 (𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡 [𝐿𝐼 (𝑃𝐶𝑀)]):13

𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡 [𝐿𝐼 (𝑃𝐶𝑀)] = 1 − ∑ [𝑆𝑖,𝑗,𝑡 𝑁𝑗

𝑖=1,𝑖∈𝑗∗ 𝐿𝐼 (𝑃𝐶𝑀)𝑖,𝑗,𝑡] . (4)

4.2.4. Natural logarithm of the number of firms (FI)

Our fourth measure of industry competition is based on the number of firms in an industry

(Fama & Laffer, 1972; Dixit & Stiglitz, 1977; Bonaccorsi di Patti & Dell'Ariccia, 2004; Cai &

Liu, 2009). Following Cai & Liu (2009), we use the natural logarithm of the number of firms

in industry 𝑗 to measure industry competition intensity:

𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡 [𝐹𝐼] = log (𝑁𝑗,𝑡) . (5)

Like the EI, the FI also has no absolute numerical limit. A higher value of 𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡 [𝐹𝐼]

means more industry competition.

4.3. Measuring industry external finance dependence (EFD)

Firms in an industry with higher external finance dependence rely more on external funds

to finance the tangible and intangible investments they desire. Previous studies show that the

degree of external finance dependence varies across industries (Rajan & Zingales, 1998). For

example, industries such as electrical machinery are more external capital dependent while

12 Main operating profits are profits before depreciation interest, special items and taxes. 13 To assess the robustness of our empirical results, we also divide 1 by the number of firms in an industry and

then multiply the sum of the LI (PCM) of all the firms in the industry to get an equal weighted concentration ratio.

We subsequently subtract this ratio from 1 to obtain the value of industry competition intensity (Aghion et al.,

2005). The results are qualitatively the same as those of value-weighted indexes.

15

industries such as tobacco have fewer needs for external funds. In this study, we construct an

industry-level EFD variable to measure the extent to which industry-level EFD affects the

relation between competition and innovation. Following Rajan & Zingales (1998), Garcia-

Appendini & Montoriol-Garriga (2013), Hsu et al. (2014) and Acharya & Xu (2017), we first

compute a firm’s external finance dependence (EFD) as the fraction of its capital expenditure

that is not financed through its internal cash flow.14 Next, we construct the median value of the

external finance dependence for all the firms in industry 𝑗 in year 𝑡 to create a time series of

industry 𝑗’s external finance dependence. Finally, we measure industry 𝑗’s dependence on

external finance (𝐷𝑒𝑝𝑒𝑛𝑑𝑒𝑛𝑐𝑒𝑗) as the median value of its time series of external finance

dependence over the period 1998-2007. Like industry competition intensity, the industry level

of external finance dependence is also based on GB/T four-digit sector codes. Firms in an

industry with a higher EFD index value tend to rely more on external capital to fund their

tangible and intangible investments including in innovation activities.

4.4. Measuring financing constraints

According to the financial constraints hypothesis proposed by Fazzari et al. (1988), a high

sensitivity of investment to internal funds can be seen as a measure of financing constraints. In

their influential paper, Fazzari et al. (1988) find that cash flow has a stronger impact on

investment by low-dividend firms than that by high-dividend firms. They interpret this fact as

supporting the financing constraints hypothesis since firms that pay low dividends are typically

smaller and younger firms which find it difficult or expensive to obtain external financing.

Therefore, if cash flow declines for these firms, the investment will go down as well. Moyen

(2004) asserts that Fazzari et al.’s (1988) interpretation of cash flow sensitivity holds “when

constrained firms do not have sufficient funds to invest as much as desired.” In addition to

investigating the link between financing constraints and fixed investment (Fazzari et al., 2000;

Love; 2003; Beck et al., 2005), many scholars also extend this method to test for the presence

of financial constraints on firms’ innovation activities (Hall, 1992; Harhoff, 2000; Brown et al.,

2009; Brown et al., 2012; Guariglia & Liu, 2014). According to this view, R&D investment

tends to be constrained by the availability of internal finance, due to limited collateral and the

uncertain risk that can restrict the use of external finance. Therefore, to test our Hypotheses 3

and 4 about financial constraints, in this paper we first use the sensitivity of innovation to cash

14 Following Acharya & Xu (2017), we also include R&D expenditure as part of capital expenditure to compute

an industry’s dependence on external finance for a robustness test. The results (not reported) are qualitatively the

same as our main findings.

16

flow to measure the degree of financial constraints faced by firms. In addition, we separate

firms into different groups based on their a priori likelihood of facing financial constraints in

the Chinese context.

To do this, first, we differentiate firms by ownership types. We compare SOEs and private

firms since in China private firms are normally subject to more financial constraints than their

state-owned counterparts. In China, the government has much control over the allocation of

financial resources so SOEs can enjoy a preferential status when seeking bank loans and other

key inputs (Li et al., 2008). Moreover, guanxi (connections) is a central idea in every aspect of

Chinese society.15 Compared to private firms, SOEs are more likely to benefit from guanxi

such as by obtaining tax incentives for innovation spending and direct grants, which provides

them with sufficient funds to innovate. In addition, banks in China are mainly controlled by

state capital, which causes an ‘institutional bias’ in China’s lending market. Since the late

1990s, the Chinese government has used bank credit as a political instrument to support SOEs,

which absorb three-quarters of bank lending. Therefore, private firms generally face more

financial constraints than SOEs.

Second, we measure financing constraints using firms’ size and age. Size and age have

been commonly used as proxies for financing constraints on R&D investment. First, small and

young firms are typically characterized by high idiosyncratic risk and high bankruptcy costs,

which makes their access to external finance costlier (Carpenter et al., 1994; Chirinko &

Schaller, 1995; Czarnitzki & Hottenrott, 2011; Guariglia & Yang, 2016). Second, compared to

large and mature firms which enjoy the benefits of economies of scale, small and young firms

do not have enough physical assets to use as collateral or a sufficiently long track record.

Therefore, small and young firms are more vulnerable to information asymmetry and

discrimination not only by the state-owned banks but also other types of formal financing

(Ayyagari et al., 2010; Cheng & Degryse, 2010). Titman & Wessels (1988) assert that small

companies lack a high level of diversification, and so have high earnings uncertainty and a high

likelihood of bankruptcy. They face higher premiums in raising external finance. Therefore,

small firms and young firms are more likely to face financing constraints than their large or

mature counterparts.

15 Guanxi means a web of connections in personal or business relations and describes the basic dynamic in

personalized networks of influence. As a crucial informal governance mechanism, guanxi allows firms to make

more profit.

17

Third, we measure financing constraints using firms’ state shares. Firms with more state

shares are more likely to have connections with the government. For this reason, it is easier for

these firms with high political affiliation to obtain credit from state-owned banks (Johnson &

Mitton, 2003; Khwaja & Mian, 2005). Therefore, firms without state shares are more likely to

face financing constraints than firms with state shares.

Last, we investigate this issue using firms’ locations, as China’s regional financial

development level is somewhat unbalanced. Since China’s coastal regions are more financially

developed than China’s central and western regions, firms in coastal regions can benefit by

obtaining bank loans more easily and facing fewer financial constraints than ones in central

and western regions (Bin, 2006).

5. Data and summary statistics

5.1. Data

This study uses firm-level production data drawn from the annual accounting reports

collected and compiled by the China’s National Bureau of Statistics (NBS) covering the period

1998-2007.16 The census dataset provides financial information on medium- and large-sized

Chinese industrial enterprises (all ‘above-scale’ industrial firms) with all types of ownership.

The criterion for inclusion in the dataset is an annual total main business income (i.e., sales) of

more than five million Chinese yuan (CNY), nearly 750,000 US dollars. The NBS dataset

clearly designates each firm with a legal identifier known as the legal person code, which can

be used to construct a panel.17 Approximately 95% of the firms in the dataset are unlisted firms

and public firms only account for about 5%.18 There are four advantages to choosing the

microeconomic-level data provided by this database. First, aggregation problems in estimation

results can be eliminated. Second, accounting of national income from these firms is done by

16 The data up to 2007 are more widely used in research (Cai & Liu, 2009; Guariglia et al., 2011; Brandt et al.,

2012; Guariglia & Liu, 2014; Liu & Qiu, 2016). The reasons why we only use the data until 2007 are as follows.

First, there are some key variables missing after 2007. For example, the current-year depreciation is missing from

2008 to 2010. We need this to calculate the corresponding values for cash flow. Second, the threshold for inclusion

of ‘above-scale’ enterprises was changed by China’s NBS in 2011 from annual sales of more than 5 million to

more than 20 million Chinese yuan. Third, the financial crisis in the period 2008-2010 could also lead to a potential

estimation bias. 17 Following Chang & Wu (2014), we regard firms with different legal person codes as different firms. A change

of the legal person code normally means that the firm’s ownership has changed, which could be caused by

restructuring, joint ventures, mergers and acquisition, etc. 18 The NBS dataset does not allow us to separate listed firms from unlisted ones.

18

the central NBS, which is advantageous as it avoids manipulation by local authorities. Third,

it is possible for us to take firm heterogeneity into account using this very large sample of firms.

Fourth, the dataset covers more than 90% of all Chinese industrial firms’ sales, which can

provide a better measure of the degree of industry competition in China than data only on listed

firms.

The original sample contains 2,222,061 observations. To minimize the potential influence

of outliers, we process the data as follows. First, in 2002 the Chinese central government

revised its industry classification in accordance with late 2001 WTO regulations.19 Following

the new classification, we match the industry codes and exclude those that disappeared or

transferred to other non-manufacturing sectors after 2002.20 The firms in the final sample

operate in 39 GB/T two-digit manufacturing, mining or public utility sectors and across all 31

Chinese provinces or province-equivalent municipal cities.21 Second, following Cai & Liu

(2009), we delete observations of firms whose main business income is below five million

Chinese yuan in order to fit the criterion of ‘above-scale,’ which constitute around 11.0% of

the sample.22 Third, we drop observations with negative values of sales, total assets minus total

fixed assets, total assets minus liquid assets, total sales and accumulated depreciation minus

current depreciation, and also observations without a record of the industry code, ownership

type or location information, which constitute approximately 0.90%. Fourth, we trim

observations in the one percent tails of each of firm-level continuous variables in our main

regressions to mitigate the potential influence of outliers.23 These processes lead to a final

unbalanced panel of 1,957,772 firm-level observations covering 555,124 Chinese firms

19 For example, some industries are broken down into different industries while others are merged. A description

of the 2002 industry classification is available at http://www.stats.gov.cn/tjgz/tjdt/200207/t20020711_16330.html. 20 For example, the ‘logging operation industry’ with two-digit code ‘12’ was moved out of mining industries

after the year 2002. However, the proportion of disappeared or transferred industries is quite low (only

approximately 0.17% of the sample). 21 Our data sample does not include firms in Hong Kong, Macao or Taiwan. 22 After 1998, the dataset records non-SOEs with annual sales of more than five million Chinese yuan (all ‘above-

scale’ non-SOEs) and all SOEs. In other words, SOEs that are not ‘above-scale’ are also included in the dataset. 23 For new product output value and R&D expenditure, we only trim the tail at 99% because these variables are

left-censored at zero.

19

between 1998 and 2007.24 All the variables are deflated using the provincial-level gross

domestic product (GDP) deflators produced by the Chinese NBS.25

Fig. 1 shows time series plots of the mean innovation rates and the average competition

intensity measured with the HHI based on GB/T four-digit sector codes over the period from

1998 to 2007.26 First, we find that the innovation rate for the full sample is relatively low

(average of 8.69%). Specifically, it drops from approximately 8.80% in 1998 to 6.68% in 2003,

increases to 10.0% in 2006 and again decreases to 8.54% in 2007. Guariglia & Liu (2014) argue

that the collapse of the information technology bubble in the late 1990s may explain the initial

decline in innovation and the implementation of government innovation incentive policies in

2003 may explain the short recovery after 2003. The 2007 financial crisis may account for the

decrease in innovation in 2007. Second, we find that there is an increasing trend in industry

competition intensity from 1998 to 2007. Specifically, China’s average competition intensity

slightly declined from 1998 to 2000, which may have been caused by the 1997 Asian economic

crisis, and then started to increase, especially after 2002, which is possibly explained by

China’s accession to the WTO in late 2001. Third, we also find that there is an approximately

negative relationship between the innovation rate and average competition intensity, which is

consistent with our Hypothesis 1.

[Insert Fig. 1 here]

Next, we find that innovation rates vary substantially between SOEs and private firms.

SOEs have higher innovation rates than private firms over the whole sample period. A possible

reason for this is that the former enjoy the privilege of cheap bank loans for innovation input.

However, we find that private firms had an increasing trend in their innovation rates during the

sample period, especially after 2003, which may be explained by the rapid growth of Chinese

private firms with more enthusiasm for innovation. In contrast, SOEs show a downward trend

24 Appendix A shows details of the structure of the unbalanced panel. In addition, because the years 1998 and

1999 are used to construct lagged values of the variables in our regression models (see Section 6.1 for details),

our regression results are estimated based on the sample for the period from 2000 to 2007. To ensure compatibility

with the data estimated in the regression models, we only summarize the data for the years 2000 to 2007 in our

regression estimations in Table 2 (summary statistics). 25 Appendix C shows the complete definitions of all the variables in this paper. Information on the province-level

GDP deflators can be viewed on the NBS website (http://data.stats.gov.cn/). 26 The innovation rate is defined as the percentage of firms which have a positive new product output value. The

rate for 2004 cannot be calculated since there is no record of new product output values for that year.

20

in their innovation rates. Therefore, the difference in mean innovation rates between SOEs and

private firms declined from around 10.93% in 1998 to 3.20% in 2007.

Fig. 2 shows snapshots of the annual innovation rates across different Chinese prefecture-

level administrative cities in 1998 and 2007.27 First, it is evident that cities in the central and

western regions have higher innovation participation rates.28 This finding is contrary to the

conventional view that firms in the eastern regions are more likely to innovate. However, the

finding is consistent with our Hypothesis 1 that more competition discourages firms’

innovation activities since the firms in the coastal regions are exposed to tougher competition

than those located in the central and western regions. Second, we also find that innovation rates

in most cities decreased from 1998 to 2007. As Fig. 2 shows, there are 217 prefecture-level

cities showing decreasing innovation rates during this period and only 114 prefecture-level

cities with increased rates. This finding is also consistent with our Hypothesis 1 that there is a

negative relationship between competition and innovation. The reduction in innovation rates

may be explained by an upward trend in industry competition intensity in China from 1998 to

2007.

[Insert Fig. 2 here]

Fig. 3 presents a plot of annual innovation rates against the four different measures of

industry competition intensity based on GB/T four-digit sector codes. We find that there is a

notable decreasing tendency in innovation rates as competition increases, regardless of the

measure of competition.29 The finding is in line with our Hypothesis 1, according to which

innovation drops with an increase in competition.

27 There are three main administration levels in China. The first is province-level administrative divisions

(provinces or autonomous regions), which are directly governed by the central government. Four municipalities

(Beijing, Tianjin, Shanghai and Chongqing) are also province-level administrations. The second level is

prefecture-level administrative divisions (prefecture-level cities, areas, autonomous prefectures or leagues), which

are directly governed by the provincial governments. Prefectures are ranked below the province level and above

the county level in the administrative structure. The third level is county-level administrative divisions (districts,

county-level cities, counties, autonomous counties, banner or autonomous banner), which are the lowest-ranking

administrative divisions and governed by the prefecture-level city governments. Our maps in Fig. 2 are based on

4 municipalities and prefecture-level administrative divisions. Hong Kong, Macao and 21 cities in Taiwan are

included in this map, but they are not included in our study. 28 According to the Chinese NBS’s region classification for economic development, the two provinces in the

northeast (Jilin and Heilongjiang) are normally regarded as parts of the central regions and Liaoning province is

a part of the coastal regions (Qin & Song, 2009). See Appendix D for details of the region classification and

Appendix E for details of the prefecture-level innovation distribution in 1998 and 2007. 29 We also find a significantly negative relationship between innovation rates and competition intensity based on

GB/T two-digit codes and three-digit codes, which is not reported for brevity.

21

[Insert Fig. 3 here]

5.2. Summary statistics

Table 1 provides descriptive statistics (sample means and medians) of the main variables

for the full sample, firms with/without innovation activities (with/without positive new product

output values), SOEs and private firms. The number of observations of innovative firms

(60,255) is around one-tenth that of non-innovative firms (633,493), which suggests a low level

of innovation in China. In addition, there are 260,919 private firm-year observations compared

to 66,978 SOE firm-year observations.

[Insert Table 1 here]

It is clear that firms with positive new product output values have a high ratio of R&D

expenditure to total assets. Non-innovative firms face stiffer competition than innovative firms

regardless of the measure of industry competition. Specifically, the four measures of industry

competition for firms without innovation output are HHI 98.52%, EI 5.81, LI (PCM) 94.95%

and FI 6.89, which are significantly greater than the levels for firms with innovation output

(HHI 98.05%, EI 5.46, LI (PCM) 94.64% and FI 6.60). This finding is in line with our

Hypothesis 1. The lower values of industry external finance dependence and the cash flow to

total assets ratio for innovative firms (averages of 57.13% and 7.91% respectively) may be

explained by the fact that innovative firms need to spend more internal finance and rely less on

external finance to support their capital expenditure. The negative values of the new long-term

debt to total assets ratio (-0.047%) for the full sample may reflect an average reduction in

Chinese firms’ long-term debts.

For the different measures of financial constraints, we observe that innovative firms

generally are larger (with average total assets of 365.13 million yuan), older (with an average

age of 17.52 years) and have a greater percentage of state shares (16.46%) than non-innovative

firms (the corresponding figures for which are 83.68 million yuan, 11.70 years and 9.08 % of

state shares). These differences can be partly explained by the fact that large firms, mature

firms and firms with more state shares tend to face fewer financial constraints and so have more

resources to invest in innovation. Our findings are consistent with those of Ayyagari et al.

(2011) and Gorodnichenko & Schnitzer (2013) that large and mature firms with sufficient

resources invest more in innovation that is long-term and has high uncertainty.

22

In Table 1, we also show the differences between SOEs and private firms. Generally,

private firms have a higher ratio of new product output value (2.89%) and a lower ratio of R&D

expenditure to total assets (0.09%) compared to SOEs, for which the corresponding values are

2.68% and 0.11% respectively. This finding shows that SOEs have a relatively lower

innovation input-output efficiency compared to private firms. For the different measures of

industry competition, we find that private firms operate in industries with more competition

intensity and SOEs operate in less competitive industries. Regarding industry external finance

dependence, SOEs have higher EFD (65.24%) than private firms (58.46%), which suggests

that SOEs rely more on external funds to finance their investments, possibly due to their

privilege of being able to obtain cheap loans from state-owned banks. Furthermore, private

firms have better operating performance, which is suggested by their higher levels of sales and

cash flow. For new long-term debt, private firms have an increasing trend (0.06%) of using

external capital over the sample period, while SOEs exhibit a downward trend (-0.25%). As

for the other variables related to financial constraints, SOEs are generally larger and more

mature than private firms, suggesting that they face a lower level of financing constraints.

6. Model specifications and estimation methodology

6.1. Baseline model specification

To test the impact of industry competition on firms’ innovation activities, following Bond

& Meghir (1994), Brown et al. (2009) and Brown et al. (2012), we estimate a dynamic Euler

equation model.30 We denote a firm’s new product output values to total assets ratio as 𝑛𝑝𝑖,𝑗,𝑡,

its sales to total assets ratio as 𝑠𝑖,𝑗,𝑡, its cash flow to total assets ratio as 𝑐𝑓𝑖,𝑗,𝑡 and its ratio of

new long-term debt to total assets as 𝑑𝑏𝑡𝑖,𝑗,𝑡.31 𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡 represents industry competition

intensity. The equation regressed is:

30 This Euler equation model is a modified version of the fixed investment specification used by Whited (1992)

and Bond et al. (2003). The specification is extracted from the dynamic optimization ‘Euler condition’ for

imperfectly competitive firms that accumulate productive assets under the condition of symmetric and quadratic

adjustment costs. As a dynamic structural approach, the Euler equation model has the advantage of controlling

for expected future profitability. Therefore, financial variables in the regression do not pick up investment

opportunities (Bond et al., 2003). In addition, to improve the precision of the estimation and to eliminate

simultaneity issues, we use lagged values of all our independent variables (Guariglia & Yang, 2016). 31 New long-term debt is the difference between long-term debt in the current year and the previous year.

Therefore, in the dataset new long-term debt is only recorded from 1999 to 2007.

23

𝑛𝑝𝑖,𝑗,𝑡 = 𝛽1𝑛𝑝𝑖,𝑗,𝑡−1 + 𝛽2𝑛𝑝𝑖,𝑗,𝑡−12 + 𝛽3𝑠𝑖,𝑗,𝑡−1 + 𝛽4𝑐𝑓𝑖,𝑗,𝑡−1 + 𝛽5𝑑𝑏𝑡𝑖,𝑗,𝑡−1 +

𝛽6𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡−1 + 𝑉𝑖 + 𝑉𝑡 + 𝑉𝑜 + 𝑉𝑗 + 𝑉𝑟 + 𝑒𝑖,𝑗,𝑡 , (6)

where the subscript i indexes firms, j industries, o ownership, r region and t time (where

t = 1998-2007). The error terms in Eq. (6) are made up of six components. 𝑉𝑖 is a firm fixed

effect. 𝑉𝑡 is a year fixed effect, which we control for by including year dummies capturing

time-varying movements in the aggregate interest cost and the business cycle. 𝑉𝑜 is a set of five

dummy variables to control for firm ownership status, with a SOE dummy being the benchmark

(Cai & Liu, 2009).32 To capture the industry effect and the location effect, we also construct an

industry-specific component (𝑉𝑗) and a location-specific component (𝑉𝑟).33 Finally, 𝑒𝑖,𝑗,𝑡 is an

idiosyncratic error term.

According to Hypothesis 1, the marginal effect of lagged industry competition intensity

(𝛽6) should be negative. A significantly negative 𝛽6 suggests that industry competition will

discourage innovation. As regards the other variables, the structural model implies that the

marginal effect of 𝛽1 should be positive, and under the assumption of quadratic adjustments

costs in the Euler equation the marginal effect of 𝛽2 should be negative. The structural model

implies that the marginal effect of the lagged sales-to-total assets ratio (𝛽3) should have a

negative sign under imperfect competition. In addition, under the assumption that cash flow

does not pick up investment opportunities, if there is an indicator of the presence of internal

financing constraints 𝛽4 should be positive (Fazzari et al., 1988). Specifically, 𝛽4 should be

greater for firms facing more financial constraints than for firms facing fewer financial

constraints. 𝛽5 should be insignificant, or its magnitude should be lower than that of cash flow

because firms prefer internal finance to external finance.

32 Firm ownership categories are defined according to the majority (at least 50%) of a firm’s total capital paid in

by six different types of agents. Specifically, we partition our firms into stated-owned enterprises (SOEs); foreign

firms; Hong Kong, Macao & Taiwan firms (HMT firms); private firms; collective firms; and mixed-ownership

firms. 33 We use GB/T two-digit sector codes rather than four-digit sector codes as industry dummy variables to control

industry fixed effects. This is because of the limitation of statistical software packages when we estimate a

random-effects Tobit model for such a large sample of approximately 700,000 observations. However, we find

the results are quantitatively similar and qualitatively consistent if we use a pooled Tobit estimator based on the

three-digit and four-digit sector codes. For location dummy variables, we choose the eight economic regions

administered by the State Council of China as the default dummy variables. The eight regions are Northern Coastal

(Shandong, Hebei, Beijing and Tianjin), Southern Coastal (Guangdong, Fujian and Hainan), Eastern Coastal

(Shanghai, Jiangsu and Zhejiang), North Eastern (Liaoning, Heilongjiang and Jilin), Mid-Yangtze Range (Hunan,

Hubei, Jiangxi and Anhui), Mid-Huanghe Range (Shaanxi, Henan, Shanxi and Inner Mongolia), South Western

(Guangxi, Yunnan, Sichuan, Chongqing and Guizhou) and North Western (Gansu, Qinghai, Ningxia, Tibet and

Xinjiang). The eight regions do not include Hong Kong, Macao or Taiwan.

24

6.2. Specification with industry external finance dependence (EFD)

To test our Hypothesis 2, following Hsu et al. (2014) and Acharya & Xu (2017), we

augment Eq. (6) by including the interaction term between the industry EFD variable

(𝐷𝑒𝑝𝑒𝑛𝑑𝑒𝑛𝑐𝑒𝑗) and the competition variable (𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡−1) to get Eq. (7) as follows:34

𝑛𝑝𝑖,𝑗,𝑡 = 𝛽1𝑛𝑝𝑖,𝑗,𝑡−1 + 𝛽2𝑛𝑝𝑖,𝑗,𝑡−12 + 𝛽3𝑠𝑖,𝑗,𝑡−1 + 𝛽4𝑐𝑓𝑖,𝑗,𝑡−1 + 𝛽5𝑑𝑏𝑡𝑖,𝑗,𝑡−1 +

𝛽6𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡−1 + 𝛽7𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡−1 ∗ 𝐷𝑒𝑝𝑒𝑛𝑑𝑒𝑛𝑐𝑒𝑗 +

𝛽8𝐷𝑒𝑝𝑒𝑛𝑑𝑒𝑛𝑐𝑒𝑗 + 𝑉𝑖 + 𝑉𝑡 + 𝑉𝑜 + 𝑉𝑗 + 𝑉𝑟 + 𝑒𝑖,𝑗,𝑡 . (7)

In accordance with our Hypothesis 2, the marginal effect of 𝛽7 should be significantly

negative. A significantly negative 𝛽7 suggests that the negative effect of competition on

innovation increases with the degree of dependence on external finance. We expect that

increased industry competition can discourage firm innovation activities more in industries

with higher EFD because these firms’ large demand for external capital cannot be satisfied.

6.3. Estimation methodology

One significant feature of the data is that a large number of firms do not have a positive

new product output value, thus the dependent variable in our study is censored at zero. To

consider this censored distribution and yield consistent results, we use the Tobit estimator.35

Furthermore, to account for firm heterogeneity, we use the random-effects Tobit estimator in

the regressions to remove any unobserved heterogeneity at the firm level. Standard errors are

also robust to heteroscedasticity, and we cluster them at the firm level.36 To address potential

endogeneity, we also carry out a quasi-experimental approach in Section 8.1 and use the IV

Tobit estimator in Section 8.2.

34 Theoretically, if we control for an industry effect (𝑉𝑗) we should not include the single term of the EFD variable

(𝐷𝑒𝑝𝑒𝑛𝑑𝑒𝑛𝑐𝑒𝑗) in Eq. (7) because otherwise it would cause a collinearity bias. However, since we choose the

GB/T two-digit sector codes as industry dummy variables rather than the GB/T Four-digit sector codes, we can

include the single term (𝐷𝑒𝑝𝑒𝑛𝑑𝑒𝑛𝑐𝑒𝑗) in our regressions. We also re-estimate Eq. (7) without the single term

(𝐷𝑒𝑝𝑒𝑛𝑑𝑒𝑛𝑐𝑒𝑗) and the results remain consistent. 35A random-effects Probit model is applied to test for rubustness in Table A5 in which the results remain consistent.

It should be noted that the OLS estimator ignores the censored nature of the dependent variable and results in an

emergence of inconsistent parameter estimates. 36 We also use the pooled Tobit estimator for a robustness test and the results are consistent with our main

empirical findings. For brevity, we do not report them.

25

Given that our dependent variables are left-censored, in our Tobit result tables we report

marginal effects (percentage change effects) rather than coefficients.37 There are two types of

marginal effects in the Tobit model. One is a probability effect that is the marginal effect of the

explanatory variables on the probability that a firm will have a positive new product output

value. The other is a quantity effect that is the marginal effect of the independent variables on

a firm’s expected new product output value, given that the observations are truncated. Positive

marginal effects suggest an increase in the probability that a firm will innovate and an increase

in the new product output value. Because the sign and significance of both the probability

effects and the quantity effects are consistent, we only report quantity effects to show the effect

of a unit change in industry competition on innovation for firms with a positive new product

output value.

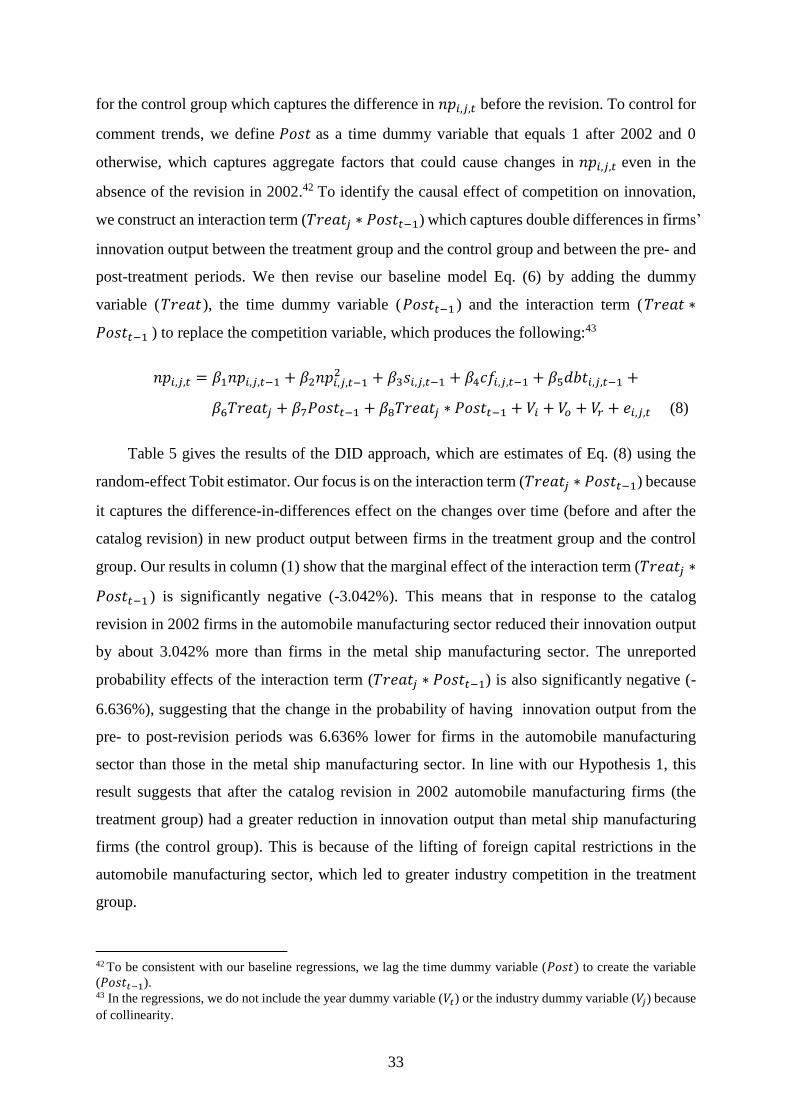

7. Empirical results and analysis

7.1. Competition and innovation

To test our Hypothesis 1, columns (1) to (4) in Table 2 show the estimation results using

the baseline regression of Eq. (6) with the random effects Tobit estimator. The left-censored

observations represent the firms without a positive new product outout value (or without

innovation activities), while the uncensored observations are the firms with a positive new

product output value (or with innovation activities). Columns (1) to (4) correspond to the

different measures of industry competition, i.e., the HHI, the EI, the LI (PCM) and the FI. We

find that the marginal effects (quantity effects) associated with the key variable

(𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡−1) are all negative and significant at the 1% level (HHI -9.157%, EI -0.322%,

LI (PCM) -4.952% and FI -0.266%) regardless of which measure of industry competition is

used, suggesting that an increase in industry competition decreases firms’ new product output.

To be precise, a 1% increase in 𝐶𝑜𝑚𝑝𝑒𝑡𝑖𝑡𝑖𝑜𝑛𝑗,𝑡−1 is associated with a HHI 0.092%, EI 0.003%,

LI (PCM) 0.050% and FI 0.003% decrease in 𝑛𝑝𝑖,𝑗,𝑡 for innovative firms. As regards to

probability effects (not reported), an increase in industry competition significantly decreases

the probability that a firm innovates. To be precise, a 1% increase in industry competition leads

to a HHI 0.349%, EI 0.014%, LI (PCM) 0.319% and FI 0.012% decrease in the probability

37 The estimated coefficients are the marginal effects of a change in the explanatory variable on the unobservable

latent variable in Tobit regressions.

26

that a firm will have a positive new product output value. These results confirm our Hypothesis

1 according to which increased competition in Chinese manufacturing sectors has a

‘Schumpeterian effect’ that leads to a reduction in firms’ innovation activities.

[Insert Table 2 here]

Our results show that the marginal effects associated with 𝑐𝑓𝑖,𝑗,𝑡−1 are significantly

positive at the 1% level. Specifically, the marginal effect of 𝑐𝑓𝑖,𝑗,𝑡−1 is 1.934%, 1.929%, 1.869%

and 1.927% in columns (1) to (4) respectively, suggesting that Chinese firms’ innovation

outputs are constrained by the availability of internal cash flow. This finding reveals that

Chinese firms rely extensively on internal capital to smooth innovation, given the limited

collateral value and the high uncertainty risk characterizing innovation. This finding is also

consistent with Guariglia & Liu (2014) that Chinese firms’ innovation activities are financially

constrained.

For the other control variables, we observe that the marginal effects of 𝑛𝑝𝑖,𝑗,𝑡−1 on 𝑛𝑝𝑖,𝑗,𝑡

are significantly positive at the 1% level. The magnitudes of the marginal effects are close to