chapter 40 - understanding reinsurance

TRANSCRIPT

Chapter 40UNDERSTANDING REINSURANCE

by David M. Raim and Joy L. Langford*

I. OVERVIEW

40.01 Scope40.02 Key Practice Insights40.03 Master Checklist

II. APPRECIATING PURPOSE OF REINSURANCE

40.04 Types of Reinsurance40.04[1] Facultative vs. Treaty40.04[2] Proportional vs. Non-proportional40.04[3] Catastrophe Reinsurance40.04[4] Finite Reinsurance40.04[5] Fronting Arrangements

40.05 Lack of Privity of Contracts40.05[1] Know General Rule40.05[2] Consider Cut-Throughs

III. CONSIDERING REINSURANCE REGULATION

40.06 Credit for Reinsurance40.07 Letters of Credit40.08 Insolvency Clause

IV. CONSIDERING INSURER’S OBLIGATIONS TO REINSURERS IN CASEOF CLAIM

40.09 Consider Insurer’s Notice Obligations40.09[1] Know What Notice Clause Requires

40.09[2] Reinsurer’s Assertion of Late Notice As Defense to Paymentof Its Reinsurance Obligations

40.09[2][a] Jurisdictions Requiring Proof of Prejudice40.09[2][b] Jurisdictions Recognizing Late Notice As Defense

Regardless of Ability to Prove Prejudice40.10 Consider Reinsurer’s Right to Access Insurer’s Records

40.10[1] Consider What Access to Records Clause Requires to BeMade Available to Reinsurer

40.10[2] Consider Whether Insurer’s Disclosure of PrivilegedDocuments to Its Reinsurer Constitutes Waiver As to ThirdParties, Including Its Insureds

40.10[2][a] Common Interest Doctrine40.10[2][b] Disclosure Made Prior To Insurance Coverage

Litigation40.10[2][c] Disclosure Made During Course of Insurance

Coverage Litigation40.10[2][d] Disclosure Made After Resolution of Insurance

Coverage Litigation But Prior to Institution ofArbitration or Litigation Between Cedent And Reinsurer

40.10[2][e] Disclosure Made During Course of ReinsuranceLitigation

40.10[2][f] Use of Confidentiality and Common InterestAgreements

40.10[3] Consider Reinsurer’s Ability to Compel Production ofCedent’s Privileged Documents

40.10[3][a] Consider Whether Inclusion of Access to RecordsClause Constitutes Waiver

40.10[3][b] Know When Privileged Documents Are “In Issue”Therefore Requiring Production by Cedent

40.10[3][c] Consider Application of Common Interest Doctrine toCompel Production of Cedent’s Privileged Documents

40.10[3][c][i] Prior to Dispute Between Cedent and Reinsurer40.10[3][c][ii] During Reinsurance Dispute Between Cedent and

Reinsurer40.10[4] Understand When Insured Is Entitled to Discover Its Insurer’s

Reinsurance Information40.11 Consider Reinsurer’s Rights Under Right to Associate Clause

or Claims Control Clause

New Appleman Insurance Practice Guide

40-2

V. CONSIDERING REINSURER’S OBLIGATIONS

40.12 Determine Extent of Coverage40.13 Consider Obligation to Reimburse Insurer for Declaratory

Judgment Expense40.14 Consider Obligation to Reimburse Insurer for Extra-

Contractual Obligations and Excess of Policy Limits (“ECO/XPL”) Damages

VI. CONSIDERING DUTY OF UTMOST GOOD FAITH OR UBERRIMAEFIDEI

40.15 Consider Insurer’s Duty to Disclose to Reinsurer All MaterialFacts About Risk Being Reinsured

40.16 Consider Application of Duty of Utmost Good Faith BeyondDisclosure at Inception of Reinsurance Relationship

40.16[1] Application of Duty of Utmost Good Faith to Parties’Conduct During Life of Reinsurance Contract

40.16[2] Application of Duty of Utmost Good Faith to Underwritingand Administration of Ongoing Business

40.16[3] Application of Duty of Utmost Good Faith to Obligation toGive Notice of Claim

40.16[4] Application of Duty of Utmost Good Faith to Reinsurer toPay Under Reinsurance Agreement

VII. CONSIDERING FOLLOW THE FORTUNES/FOLLOW THESETTLEMENTS

40.17 Understand Distinction Between Follow the Fortunes andFollow the Settlements

40.18 Consider Reinsurer’s Preclusion from Second-GuessingReinsured’s Good Faith Claims Decisions

40.19 Consider Application of Follow the Fortunes/Follow theSettlements to Allocation Decisions

VIII. CONSIDERING BROKERED MARKET

40.20 Brokered vs. Direct Market40.21 Understand Which Entity Broker Represents

Understanding Reinsurance

40-3

IX. CONSIDERING REINSURANCE ARBITRATION

40.22 Consider Obligation to Arbitrate40.23 Neutral Panel or Party Advocate System40.24 Strict Rule of Law vs. Obligations Pursuant to Honorable

Engagement40.25 Discovery in Arbitration40.26 Summary Disposition in Arbitration40.27 Reasoned Awards40.28 Know When to Move to Vacate or Affirm Arbitration Award40.29 ARIAS Forms

X. FORMS

40.30 BRMA Reinsuring Clause Form 44 C (Quota ShareAgreement)

40.31 BRMA Reinsuring Clause Form 44 B (Surplus ShareAgreement)

40.32 BRMA Reinsuring Clause Form 61 C (Excess of LossAgreement)

40.33 BRMA Unauthorized Reinsurance Clause Form 55 A40.34 BRMA Insolvency Clause Form 19 M40.35 BRMA Offset Clause Form 36 A40.36 BRMA Loss Notice Clause Form 26 B40.37 Notice of Loss Clause Incorporating Right to Associate40.38 BRMA Loss Notice Clause Form 26 A40.39 BRMA Access to Records Clause Form 1 B40.40 BRMA Confidentiality Clause Form 69 D40.41 BRMA Claims Cooperation Clause Form 8 A40.42 BRMA Excess of Original Policy Limits Clause Form 15 A40.43 BRMA Extra Contractual Obligations Clause Form 16 D40.44 BRMA Intermediary Clause Form 23 A40.45 BRMA Arbitration Clause Form 6 A40.46 BRMA Arbitration Clause Form 6 E40.47 ARIAS-U.S. Umpire Questionnaire Sample Form 2.1

New Appleman Insurance Practice Guide

40-4

I. OVERVIEW.

40.01 Scope. In essence, reinsurance is insurance for insurance compa-nies. It is a contractual arrangement under which an insurer securescoverage from a reinsurer for a potential loss to which it is exposed underinsurance policies issued to original insureds. The risk indemnifiedagainst is the risk that the insurer will have to pay on the underlyinginsured risk. Because reinsurance is a contract of indemnity, absent specificcash-call provisions, the reinsurer is not required to pay under the contractuntil after the original insurer has paid a loss to its original insured.Reinsurance enhances the fundamental financial risk-spreading functionof insurance and serves at least four basic functions for the directinsurance company: increasing the capacity to write insurance (underprevailing insurance-regulatory law); stabilizing financial results in thesame manner that insurance protects any other purchaser against spikesfrom realized financial losses; protecting against catastrophic losses; andfinancing growth.The reinsurance relationship is structured in the following manner:original insured > insurer > reinsurer. The insurer is called, for reinsurancepurposes, the cedent (or cedant). There is typically no contractual rela-tionship between the reinsurer and the original insured. Reinsurance may,but need not, dovetail with the scope of the original insurance. Basically,all of the risks that are insured can be reinsured, unless contrary to publicpolicy under the relevant governing law for the reinsurance contract.This chapter principally discusses how insurance claims and coveragelitigation can evolve into reinsurance claims and in that context presentsthe most common legal issues that arise from reinsurance relationships.The coverage afforded insurers through the most commonly purchasedtypes of reinsurance is explained to provide a context for most reinsuranceclaims. Certain aspects of reinsurance regulation are set forth to illustratethe role of reinsurance in the entire insurance scheme and the payment ofpolicyholder claims. Also described are the special rights and obligationsof cedents and reinsurers as between them and important aspects ofreinsurance arbitration (the common form of dispute resolution), both ofwhich strongly influence reinsurance recoveries. This chapter provides abackground in reinsurance and explains how an insured’s relationshipwith its insurer fits within the context of the entire reinsurance scheme.Reinsurance, like many areas of business law, has a language of its own.The insurance company purchasing reinsurance is called the “cedingcompany” (or the “cedent” (or “cedant”), “reinsured” or “ceding insurer”)because it “cedes” or transfers part of the risk. The company selling

40-5

reinsurance is called the “reinsurer”. Typically, these are the only parties tothe reinsurance agreement; all rights and obligations run only betweenthem. The reinsurance contract does not change the direct, or original,insurer’s responsibility to its policyholder (the “original insured” or“policyholder”), and the insurer must fulfill the terms of its policy whetheror not it has reinsurance or whether or not the reinsurer is rightly orwrongly refusing to perform. The liability or risk ceded is called a“cession,” and the original policy that the cedent issues to a policyholderis referred to as “direct” insurance. A reinsurer also can purchase its ownreinsurance protection, and such reinsurance of reinsurance is called a“retrocession.” A reinsurer that transfers all or part of its assumedreinsurance is called a “retrocedent,” and the company reinsuring this riskis called the “retrocessionaire.” Retrocessions need not incorporate theoriginal reinsurance and often do not. (Retrocessionaires in turn canpurchase reinsurance again, ad infinitum.)

Reinsurance relationships can be simple or complex. A cedent can cedecertain loss exposures under one contract or purchase several contractscovering different aspects or portions of the same policy to achieve thedesired degree of coverage. A layering process involving two or morereinsurance agreements is commonly employed to obtain sufficient mon-etary limits of reinsurance protection. When a claim is presented, thereinsurers respond in a predetermined order to cover the loss.

The reinsurance relationship is evidenced by a written contract reflectingthe negotiated terms. Although reinsurance contracts between differentcedents and reinsurers can include clauses with similar purposes, thewording of particular provisions varies significantly, depending on theparties’ specific needs, customs and practices. Sample clauses are pro-vided where instructive.

Payments that are due pursuant to a reinsurance agreement are consid-ered an asset of the cedent; in contrast to other types of contingentpayments, the applicable regulatory regime may permit the cedent tocount a reinsurance recoverable as a present asset on its own balancesheet. Reinsurance is payable only after the cedent has paid losses dueunder its own insurance agreements. However, most U.S. reinsurancecontracts include an insolvency clause, which allows the receiver of aninsolvent insurer to collect on reinsurance contracts as if the insolventinsurer had paid the claim in full even if it did not [see § 40.08 belowdiscussing the insolvency clause].

Reinsurance should not be confused with other commercial arrangements.It is not co-insurance, where separate insurers assume shares of the sameinsurance risk. Nor is it a novation as between the original insured and its

40.01 New Appleman Insurance Practice Guide

40-6

insurer or substitution of one insurer for another. A reinsurance agreementdoes not establish a partnership between the insurer and the reinsurer ora separate joint venture as between them, although some pro rata contractsprovide that the parties share proportionally in the premiums collected bythe cedent and in losses paid by it. Reinsurance ordinarily does not conferthird-party beneficiary status on the original insured. Absent a “cut-through” clause or similar modification [see § 40.05 below for discussion ofthese exceptions], there is no privity of contract between the insurancepolicyholder and the reinsurer. In the absence of language in the reinsur-ance agreement granting the original insured rights against the reinsureror unusual factual circumstances, attempts by original insureds to suereinsurers directly generally fail; claimants against the original insuredssimilarly are unsuccessful in bringing suit directly against reinsurers, evenwhere, in direct-action states or in other circumstances, the claimant mightbe able to sustain an action against the original insurer (cedent).

Underlying claims and coverage litigation can trigger reporting and noticeobligations of cedents to reinsurers. Reinsurers that potentially oweindemnity may commence investigations, monitor claims, and establishclaim reserves. Counsel for original insureds in coverage litigation some-times seek production of communications generated between the cedentand reinsurer on the grounds that insurance covering a defendant isgenerally discoverable (even though in the circumstance the “insurance”is reinsurance), or for more narrowly tailored purposes such as to collectevidence that the original insurance policy existed at one time even if it isno longer is available. In some instances, the disclosure of cedent/reinsurer communications can potentially be detrimental to the cedent’scoverage position vis-a-vis its insured.

Typical reinsurance claim issues that are discussed here include: reportingand notice obligations; defenses stemming from interpretation of thereinsurance wording to the indemnity sought; cooperation and claim-handling obligations; and defenses seeking rescission of the reinsurancecontract including nondisclosure and misrepresentation with respect tothe details of risk. The nature of the reinsurance relationship — especiallythe notion of “utmost good faith” or uberimae fidei — may provide a glosson how certain issues get resolved in the reinsurance context that maydiffer from how similar issues are resolved in the ordinary insured-insurercontext. Other common issues addressed here include the reinsurer’sobligations to indemnify the insurer for declaratory judgment expensesincurred in defending or prosecuting coverage litigation against theoriginal insured, and payments by insurers in excess of policy limits orpayments of extracontractual damages.

Understanding Reinsurance 40.01

40-7

Reinsurance claims generate certain legal issues distinct from issues thattypically arise in the context of direct insurance. Rules found in insurancelaw in different arenas may not apply or may apply with different nuancesin the context of reinsurance disputes, and the duties and obligationsbetween a cedent and reinsurer may differ from those between an originalinsurer and policyholder, considering some of the differences in therelative sophistication and bargaining power, custom and practice, ordifferent aspects in which one party is largely dependent upon another.Several important distinctions between the resolution of insurance andreinsurance disputes are examined in this chapter, including the effect ofthe bilateral duty of utmost good faith, which is perhaps unique toreinsurance agreements. Reinsurance disputes also are distinguished bytheir typical resolution through arbitration, rather than courtroom litiga-tion. Among other differences, in typical U.S. arbitrations, the availabilityand weight of legal precedent is less predictable and meaningful than inlitigation in the courts. Arbitrators may not be bound by strict legal rulesand do not always strictly apply contract law and other legal principles toreinsurance agreements; indeed, some reinsurance contracts eschew reli-ance upon legal rules in favor of construing the reinsurance relationshipmemorialized by the reinsurance contract as principally an honorableengagement pursuant to industry custom and practice.

Lexis.com Searches: To find statistics on reinsurance premiums, trythis source: RDS TableBase. Enter this search: PUB(Reinsurance).

To find articles on specific cases involving reinsurance, try this source:Reinsurance: Mealey’s Litigation Report. Enter specific search terms ordate ranges.

40.02 Key Practice Insights. The parties to reinsurance contracts aretypically sophisticated insurers transferring the financial risk assumed ininsuring businesses, homes, cars and individuals. Note that sometimesreinsurers create the instrument that is to be sold to an insured and thenlook for a middleman (cedent) to (i) issue the policy to the insured and (ii)purchase the corresponding reinsurance. Indeed, in such transactions,sometimes the cedent will 100 percent reinsure the risk undertaken to thepolicyholder, in exchange for a ceding commission deducted from thepremium collected from the direct insured, which is ultimately passed onto the reinsurer.

There are no standard reinsurance contracts, although many includecommonly used provisions and clauses sometimes required by state law.Each reinsurance treaty or facultative certificate reflects the special needsof the parties with respect to the type and amount of risk covered, the

40.02 New Appleman Insurance Practice Guide

40-8

calculation of the premium, the role of the reinsurance intermediary, themethod and timing of notice and submission of claims, various reportingobligations, and resolution mechanisms for potential disputes. Reinsur-ance contracts therefore are often complex and unique and must becarefully drafted and, in the event of dispute, carefully interpreted.Lawyers practicing in the reinsurance field must become familiar with thespecialized business of reinsurance, including the purposes and types ofreinsurance and the financial goals and consequences typically involved.Practitioners also must be knowledgeable about the meaning, use andlegal effect of commonly employed reinsurance contract provisions,including insolvency, access to records, claims control, notice, extra-contractual obligations (“ECO”), excess of policy limits (“XPL”), followthe fortunes/settlements, intermediary and arbitration provisions. Attor-neys also should carefully review complete versions of reinsurancewordings, including endorsements and amendments. (Indeed, sorting outwhich is the governing wording particularly when insurers operating indifferent markets or in different countries are involved can prove tediousand time consuming.)

Although regulation of the reinsurance industry in the United States ismore limited than that of the insurance industry in general, lawyersshould be mindful of the insurer’s statutory licensing, solvency andaccounting requirements. Attorneys should understand how insurersmust account for finite risk reinsurance, as this subject recently hasattracted significant regulatory attention. Also of particular concern are“fronting” arrangements and cut-through endorsements, which may notbe allowed or may be subject to special regulations in certain jurisdictions.

Reinsurance disputes are typically resolved through arbitration, andpractitioners should be familiar with arbitration law, particularly theFederal Arbitration Act (“FAA”) and statutory law applicable to non-admitted reinsurers and the availability of pre-answer or pre-judgmentsecurity. Of course, counsel handling a dispute should be familiar withhow reinsurance arbitrations are generally handled. A thorough knowl-edge of the reinsurance industry is needed as many issues are decidedbased upon the custom and practice in the industry (especially where thearbitration panel is comprised of non-lawyers, as is often the case).Lawyers also should know that leading industry and professional orga-nizations offer practice guides, forms, and other resources useful forreinsurance arbitrations (such as lists of professional trained reinsurancearbitrators).

Understanding Reinsurance 40.02

40-9

40.03 Master Checklist.

□ Understand whether the reinsurance contract at issue is a faculta-tive certificate or a treaty.

Discussion: § 40.04[1]

□ Understand whether the reinsurance at issue is proportional ornon-proportional.

Discussion: § 40.04[2]

Forms: §§ 40.30-40.32

□ Become familiar with specific types of reinsurance such as catas-trophe reinsurance, clash cover and finite reinsurance.

Discussion: §§ 40.04[3]-40.04[4]

□ Understand how insurers must account for finite risk reinsuranceunder applicable regulations.

Discussion: § 40.04[4]

□ Determine all of the parties’ responsibilities and liabilities in afronting arrangement, including any obligation to monitor a man-aging general agency.

Discussion: § 40.04[5]

□ Confirm that fronting is permissible in the jurisdiction where thearrangement is executed.

Discussion: § 40.04[5]

□ Determine if special circumstances exist which may providegrounds for a policyholder of the ceding insurer to assert a directaction against the reinsurer.

Discussion: § 40.05[1]

□ Research the legality and enforceability of cut-through clauses (orassumption of liability endorsements) contained in insurance con-tracts covered by reinsurance.

Discussion: § 40.05[2]

□ Understand the credit for reinsurance laws governing your rein-surance transaction.

40.03 New Appleman Insurance Practice Guide

40-10

Discussion: § 40.06

□ Confirm that a letter of credit obtained by a ceding company thatintends to take financial statement credit for reinsurance placedwith a non-admitted reinsurer complies with statutory require-ments.

Discussion: § 40.07

□ Ensure that an adequate insolvency clause is included in thereinsurance contract if required in your jurisdiction. Most statesrequire that the reinsurance contract include an insolvency clausefor the ceding insurer to take credit for reinsurance on its financialstatement.

Discussion: § 40.08

Form: § 40.34

□ Understand the effect of an offset clause, or any applicable commonlaw or statutory set-off rights, on the rights and obligations underthe reinsurance agreement.

Discussion: § 40.08

Form: § 40.35

□ Understand the requirements of the reinsurance contract’s noticeprovision.

Discussion: § 40.09[1]

Forms: §§ 40.36-40.38

□ Determine whether, in your jurisdiction, the reinsurer must dem-onstrate prejudice in order to successfully assert a late noticedefense.

Discussion: § 40.09[2]

□ Understand the effect of an access to records clause in the reinsur-ance agreement.

Discussion: § 40.10[1]

Form: § 40.39

□ If your client is the ceding insurer, beware the consequences of

Understanding Reinsurance 40.03

40-11

disclosing privileged information to reinsurers pursuant to anaccess to records clause.

Discussion: § 40.10[2]

□ Research the applicability in your jurisdiction of the commoninterest doctrine to a cedent’s disclosure of privileged communi-cations to its reinsurer.

Discussion § 40.10[2]

□ Determine whether the parties to a reinsurance contract shouldexecute a confidentiality or common interest agreement to try topreserve applicable privileges or immunities against disclosure tothird parties.

Discussion: § 40.10[2][f]

□ Understand the circumstances under which a reinsurer can compeldisclosure of its cedent’s privileged communications.

Discussion: § 40.10[3]

□ Understand the circumstances under which an insured will beentitled to discover its insurer’s reinsurance information.

Discussion: § 40.10[4]

□ Become familiar with the rights and obligations presented by rightto associate and claims control clauses in reinsurance contracts.

Discussion: § 40.11

Forms: § 40.41

□ Draft the reinsuring or business covered clause of the reinsuranceagreement carefully to avoid disputes concerning the scope ofcoverage.

Discussion: § 40.12

□ Understand whether the reinsurance contract wording (in manycases the definition of “allocated loss expenses”) obligates thereinsurer to reimburse its cedent for declaratory judgment ex-penses.

Discussion: § 40.13

□ Understand the coverage provided by excess of policy limits

40.03 New Appleman Insurance Practice Guide

40-12

(“XPL”) and/or extra-contractual obligations (“ECO”) clauses inthe reinsurance contract.

Discussion: § 40.14

Forms: §§ 40.42-40.43

□ Understand the duty of utmost good faith that is central to therelationship between cedent and reinsurer.

Discussion: § 40.15

□ If your client is the cedent, determine the facts that must bedisclosed during the underwriting process.

Discussion: § 40.15

□ If your client is the cedent, ensure that all proper and businesslikesteps are taken in underwriting the underlying business and insettling claims.

Discussion: § 40.16[2]

□ Understand the effect of follow the fortunes or follow the settle-ments wording in the reinsurance contract.

Discussion: § 40.17

� Cross References: §§ 40.18-40.19

□ Determine the extent to which follow the fortunes or follow thesettlements language in the reinsurance contract requires a rein-surer to follow its cedent’s allocation and aggregation decisions asrespects it direct insurance obligations.

Discussion: § 40.19

□ Understand the obligations of the reinsurance intermediary.

Discussion: § 40.20

□ Determine whether, and for what purposes, the reinsurance brokeror intermediary is the agent of the ceding company, the reinsurer,or both parties.

Discussion: § 40.21

Form: § 40.44

Understanding Reinsurance 40.03

40-13

□ Understand what disputes are arbitrable under the reinsurancecontract’s arbitration clause.

Discussion: § 40.22

Forms: §§ 40.45-40.46

□ In drafting reinsurance agreements, counsel should determinewhether the scope of the arbitration clause in the reinsurancecontract is intended to be broad or narrow.

Discussion: § 40.22

Forms: §§ 40.45-40.46

□ Arbitration counsel should consider whether non-signatories to thearbitration agreement may be forced to arbitrate.

Discussion: § 40.22

□ Consider whether or not to include consolidation and joinderprovisions in an arbitration agreement, or whether to requestconsolidation once arbitration has commenced.

Discussion: § 40.22

Form: § 40.45

□ Consider what procedures should be included in the arbitrationprovision concerning the selection of arbitrators and/or umpires,what qualifications the arbiters should have, and whether thearbiters should be neutral or non-neutral.

Discussion: § 40.23

□ Make certain that your client appoints its arbiter on a timely basis.

Discussion: § 40.23

□ Become familiar with the standards and procedures for selectingarbitrators and the lists of qualified individuals published byarbitration and reinsurance organizations.

Discussion: § 40.23

Form: § 40.47

□ Understand the effect of any honorable engagement wording in the

40.03 New Appleman Insurance Practice Guide

40-14

reinsurance agreement.

Discussion: § 40.24

Form: § 40.46

□ Counsel drafting a reinsurance contract should determine whetherspecific discovery procedures should be included in the reinsur-ance contract’s arbitration provision and, if so, whether theyshould incorporate any procedures published by reinsurance orarbitration organizations.

Discussion: § 40.25

□ Counsel should determine how and whether a reinsurance inter-mediary can be required to participate in the discovery process inthe event of a reinsurance arbitration.

Discussion: § 40.25

□ Arbitration counsel should consider whether to submit a motionfor summary disposition of a reinsurance claim or dispute.

Discussion: § 40.26

□ Arbitration counsel should consider whether to move to confirm afavorable arbitration award in court.

Discussion: § 40.28

□ Arbitration counsel should consider whether grounds exist tomove to vacate an arbitration award in court.

Discussion: § 40.28

□ Arbitration counsel should consider whether there are grounds torequest a court to modify or correct an arbitral award.

Discussion: § 40.28

□ Become familiar with the forms provided by ARIAS.

Discussion: § 40.29

Form: § 40.47

Understanding Reinsurance 40.03

40-15

II. APPRECIATING PURPOSE OF REINSURANCE.

40.04 Types of Reinsurance.

40.04[1] Facultative vs. Treaty. There are two basic types of reinsur-ance: “treaty” and “facultative.” Facultative reinsurance is a contractonly covering all or part of a single specific policy of insurance. Foreach transaction sought to be reinsured, the reinsurer reserves the“faculty” to accept or decline all or part of any insurance policypresented, and the cedent chooses whether to secure reinsurance fora particular policy. The reinsurer and cedent negotiate the terms foreach facultative certificate. Facultative reinsurance is commonlypurchased for large, unusual or catastrophic risks. Reinsurers thusmust have the necessary resources to underwrite individual riskscarefully. (“Treaty” reinsurance, discussed further below, involves apreexisting commitment by the reinsurer to cover a predeterminedclass and amount of coverage that will be sold by the insurer-cedent.)

Other uses of facultative reinsurance include:

1. When an insurer is offered a risk that exceeds its standardunderwriting or reinsurance limits for that class, facultativereinsurance can permit the ceding company to accept the risk.

2. Insurers can fill gaps in coverage caused by reinsurance treatyexclusions by seeking separate facultative coverage for aspecific policy or group of policies.

3. A reinsurer can issue facultative reinsurance to participate in amarket in the short term to minimize risk and take advantageof favorable rates.

4. A treaty reinsurer may purchase facultative reinsurance toprotect itself and its treaty reinsurers.

Insurers sometimes purchase both facultative and treaty reinsuranceto cover the same risk. Unless there are contract terms to the contrary,the facultative reinsurance will perform first and completely beforeany of the treaty reinsurance performs. Sometimes the facultativereinsurance only applies to the ceding company’s net retention; othertimes facultative coverage also inures to the benefit of the treatyreinsurers. Ideally, the wording of the facultative certificate will makethis clear. As a general matter, whether the facultative reinsuranceinures to the benefit of the treaty reinsurers will depend on whetherthe treaty reinsurers paid a portion of the premium for the facultative

40-16

XPP 7.3C.1 Patch #3 SC_01347 nllp 60099 [PW=500pt PD=684pt TW=360pt TD=548pt]

coverage. If not, the facultative reinsurance likely will not inure to thetreaty reinsurers’ benefit.

Facultative certificates are often one or two page documents. Thefront of a typical contract identifies the parties, the underlyingpolicyholder and policy number reinsured, amounts of the policyceded and retained, the type of reinsurance (proportional or non-proportional) and the premium. The back of each certificate usuallycontains the following provisions: notice of loss; net retention;coverage for loss adjustment expenses; claims handling; cancellation;insolvency; tax; offset and intermediaries. Many facultative certifi-cates do not include an arbitration provision [see § 40.22 below for adiscussion of arbitration clauses in reinsurance agreements].

Treaty reinsurance, the most common form of reinsurance, coverssome portion of a defined class of an insurance company’s business(e.g., an insurer’s products liability or property book of business).Reinsurance treaties cover all of the risks written by the cedinginsurer that fall within their terms unless exposures are specificallyexcluded. Thus, in most cases, neither the cedent nor the reinsurerhas the “faculty” to exclude from a treaty a risk that fits within thetreaty terms. Therefore, treaty reinsurers rely heavily on the cedent’sunderwriting. Treaty relationships are often long-term; treaties some-times are renewed automatically unless a change in terms is re-quested. A typical treaty can include thirty or forty articles or clauseswhich describe the class or classes of business covered, the type oftreaty (proportional or non-proportional), the amount of reinsuranceprovided and details about the parties’ obligations with respect totreaty operation.

� Cross Reference: For a thorough discussion of the distinctionbetween facultative and treaty reinsurance, see Compagnie deReassurance D’Ile de France v. New England Reinsurance Corp.,825 F. Supp. 370 (D. Mass. 1993), aff’d in part and rev’d in part, 57F.3d 56 (1st Cir. 1995).

z Strategic Point: Reinsurance treaties that run consecutively formany years can present certain difficulties in terms of claimsprocessing. Contracts are often amended by endorsements whichcan add or delete reinsurers, change premium or ceding commis-sion rates or add, delete or alter important contract terms. Thesechanges may be retroactive to contract inception or have adifferent effective date. Practitioners evaluating indemnity underreinsurance treaties must take care to review complete versions of

Understanding Reinsurance 40.04[1]

40-17

the wordings, including endorsements and amendments.

40.04[2] Proportional vs. Non-proportional. Proportional or pro-ratareinsurance is characterized by a proportional division of liabilityand premium between the ceding company and the reinsurer. Thecedent pays the reinsurer a predetermined share of the premium, andthe reinsurer indemnifies the cedent for a like share of the loss andthe expense incurred by the cedent in its defense and settlement ofclaims (the “allocated loss adjustment expense” or “LAE”). Accord-ing to the percentage agreed, the cedent and reinsurer share thepremium and losses from the business reinsured. Proportional rein-surance spreads the risk of loss and creates a broad identity ofinterests between the cedent and the reinsurer, which effectivelyco-venture in relationship to their relative shares of the risk, eventhough only the cedent has contractual privity with the directinsured.

The two most common types of proportional reinsurance are “quotashare” and “surplus share” reinsurance. Under quota share reinsur-ance, the reinsurer assumes an agreed percentage of each risk fromthe first dollar, up to any limit assigned. For example, if there is a $100loss under a 40 percent quota share reinsurance contract, the cedentwould bear $60 of that loss and the reinsurer concurrently would bear$40 of that loss. The percentage always reflects the percentage of lossborne by the reinsurer. The portion of the risk that the reinsurerassumes is called the “ceded risk,” and the portion that the cedentkeeps is referred to as the reinsurance “retention.” Although it is nota partnership, quota share reinsurance presents a greater identity ofinterests between the ceding insurer and the reinsurer than doesexcess of loss reinsurance (discussed below).

Surplus share is similar to quota share reinsurance in that premiumsand losses are shared on a proportional basis, but differs in that theportion of the reinsured policy the direct insurer retains is expressedas a fixed monetary amount, and the reinsurance may or may notapply from the first dollar (i.e., the reinsurance may apply only inexcess of the fixed dollar amount or the cedent and reinsurer maytogether share losses as they are incurred until the cedent incurs anamount equal to its overall retention). Premium is shared based onthe ratio of retained liability, and the reinsurer agrees to pay the samepro rata portion of any loss and expense incurred by the cedent.

Examples: Where the policy limit is $150,000, and the cedent’sretention is $25,000, the amount ceded to the reinsurer is $125,000

40.04[2] New Appleman Insurance Practice Guide

40-18

and the ratio of what is ceded to what is retained is 5:1. Lossestherefore will be shared in that proportion. For a loss of $100,000,the cedent is responsible for $16,667 and the reinsurer pays fivetimes more, or $83,333.

In addition, in surplus share reinsurance contracts, the proportion ofpremium and liability ceded can vary, at the cedent’s option, fromrisk to risk. Although it can be advantageous for the direct insurer tovary the percentage of premium and liability ceded for each risk,these variations make a surplus share contract more difficult toadminister than a simple quota share.Under non-proportional or excess of loss reinsurance (sometimesreferred to as “XL” or “XOL”), the reinsurer’s liability is not triggereduntil the cedent’s losses exceed a specified monetary amount, calledthe “retention.” If losses to the ceding company are less than theretention, the reinsurer owes nothing. The reinsurance agreementwill include a limit of liability for each claim above which thereinsurer is not obligated to pay. Excess of loss reinsurance can beprovided on an individual risk, an occurrence or an aggregate basis,and is typically placed in layers. Non-proportional reinsurance tendsto cost less than does quota share reinsurance because the reinsurerdoes not participate in every loss. However, because the level of riskunder non-proportional reinsurance depends on the nature of thereinsurance undertaking, there is a great deal of uncertainty with thiscoverage. In addition to the underlying risk, reinsurers must considerthe layer of coverage on which it will participate.Whether a potential cedent seeks to obtain or place coverage on a firstdollar basis versus excess of loss reinsurance depends on severalfactors, including the cedent’s anticipated loss profile. For example, ifthe cedent expects to incur frequent losses at low levels, it may makeeconomic sense for the cedent to secure quota share reinsurance, so ithas some protection for even the smallest losses. In contrast, if thecedent expects to have infrequent losses at significant levels or wishesto guard against risk of a significant loss, it may choose to purchaseexcess of loss coverage.

z Strategic Point — Reinsurer: Because non-proportional reinsur-ance is characterized by unpredictability and potentially highlosses, XOL reinsurers may incur a disproportionate share of totallosses. This is especially problematic with respect to “long tail”lines of insurance where the incidence of loss and determinationof damages can extend well beyond the period in which theinsurance or reinsurance is in force. In such cases, premiums may

Understanding Reinsurance 40.04[2]

40-19

be received long before liability is manifested or developed, andliability may be difficult to estimate because it is determined bythe prevailing legal or economic environment in the future. (Onthe other hand, the reinsurer is able to hold on to the premiumpaid by the cedent for a longer period, offering it the opportunityto “earn out” losses through investment return.) Examples oflong-tail lines of insurance include malpractice, products liability,and errors and omissions.

� Cross Reference: For discussion of the advantages and disad-vantages of proportional and non-proportional reinsurance con-tracts, see Eric Mills Holmes, Appleman on Insurance 2d § 102.3.

� Cross References: For an example of a reinsuring clause for aquota share reinsurance agreement, see § 40.30 below. For anexample of a reinsuring clause for a surplus share reinsuranceagreement, see § 40.31 below. For an example of a reinsuringclause for an XOL reinsurance agreement, see § 40.32 below.

40.04[3] Catastrophe Reinsurance. Catastrophe reinsurance is a formof excess of loss reinsurance which, subject to a specific limit,indemnifies the cedent for the amount of loss in excess of its retentionwith respect to an accumulation of individual losses affecting mul-tiple policies resulting from a catastrophic event. Rather than singlelarge losses, even an unexpected number of such losses within thereinsurance policy term, catastrophe coverage principally providesprotection for the cedent against the concentration of several losses,each of which may stem from different direct insureds but whichaltogether arise from a common event (or closely related series ofevents). The reinsurance contract is typically called a “catastrophecover.” Catastrophe reinsurance can be provided on an aggregatebasis with coverage for losses over a certain amount for each loss inexcess of a second amount in the aggregate for all losses in allcatastrophes occurring during a certain time period (often one year).Catastrophe cover is typically secured to protect the cedent against anintolerable accumulation of actual loss and to stabilize its underwrit-ing experience.

Another variant of reinsurance purchased by insurers is “clashcover,” which requires two or more coverages or policies issued bythe reinsured to be involved in a loss, for coverage to apply. Thisreinsurance typically attaches above the limits of any one policy.Clash covers are often catastrophe covers.

40.04[3] New Appleman Insurance Practice Guide

40-20

� Cross Reference: For discussion of the typical terms of catastro-phe cover, see Eric Mills Holmes, Appleman on Insurance 2d§ 102.3[B][2].

40.04[4] Finite Reinsurance. There is no generally accepted definitionof finite risk (sometimes called “financial”) reinsurance. Broadlyspeaking, it is a form of reinsurance that carefully controls and limitsthe amount and type of risk transferred to the reinsurer, but ofteninvolves the transfer of money, a return premium from the reinsurer,to the cedent as a result of how losses developed under thereinsurance contract. Finite reinsurance can be distinguished fromother non-finite or “traditional” types of reinsurance based on theextent to which there are limitations on the “underwriting risk,” therisk that the amount of losses will exceed premiums. Participants infinite risk reinsurance transactions tend to focus primarily on finan-cial risks, such as timing risk (the risk that losses will need to be paidsooner than expected), investment risk (the risk that the reinsurer willearn less investment income than expected on the reinsurancepremium) and credit risk (the risk that the cedent will not make therequired premium payments).

Finite risk reinsurance contracts are typically treaties that are closelytailored to meet the particular needs of a cedent. They can be quotashare or excess of loss treaties and may cover losses that have yet tobe quantified or to have occurred at all or losses that have alreadyoccurred in part but where the amount and timing of the loss is stilluncertain. Finite risk reinsurance contracts often include some or allof the following:

1. A ceiling on the amount of underwriting risk assumed by thereinsurer;

2. An explicit recognition of the time value of money through theuse of experience accounts funded by large reinsurance pre-miums, which accumulate investment income over time andfund the loss payments;

3. Inclusion of a commutation clause that allows for profitsharing between the cedent and reinsurer based on the finan-cial results of the reinsurance contract;

4. Multi-year contracts that allow the cedent to mitigate volatilityby recognizing a loss gradually, rather than all at once.

Finite risk transactions are legitimate and widespread, though someforms of transactions have been criticized as being in substance

Understanding Reinsurance 40.04[4]

40-21

distinguished loans but which as something other than a loan obtainsmore favorable tax or accounting treatment (until challenged). Thekey issue is how to account for the transaction. If there has beensufficient risk transfer, the contract can be accounted for as reinsur-ance. If not, then contract deposit accounting is appropriate.

t Warning: Significant regulatory attention has recently beendirected at how insurers account for finite risk reinsurance andwhether the principal objective of these transactions is untetheredfrom an underlying business rationale but instead is designed toimprove the appearance of the balance sheet of the cedent (andthus implicitly, or so the argument goes, to mislead investors andregulators as to the true financial condition of the cedent).Insurers and reinsurers in the United States and elsewhere havebeen investigated by the SEC, state Attorneys General, stateInsurance Departments, and other law-enforcement officials withjurisdiction. A common element in many of the finite riskreinsurance transactions under attack by regulators is an allega-tion that the transactions were presented and accounted for as ifthey genuinely transferred material risk, when in fact the trans-actions did not do so and thus were more in the nature of loansor deposits on account. They were instead allegedly intendedonly to achieve a particular result on a company’s balance sheet— what is sometimes referred to as “financial engineering” ormore commonly “smoothing” of earnings.

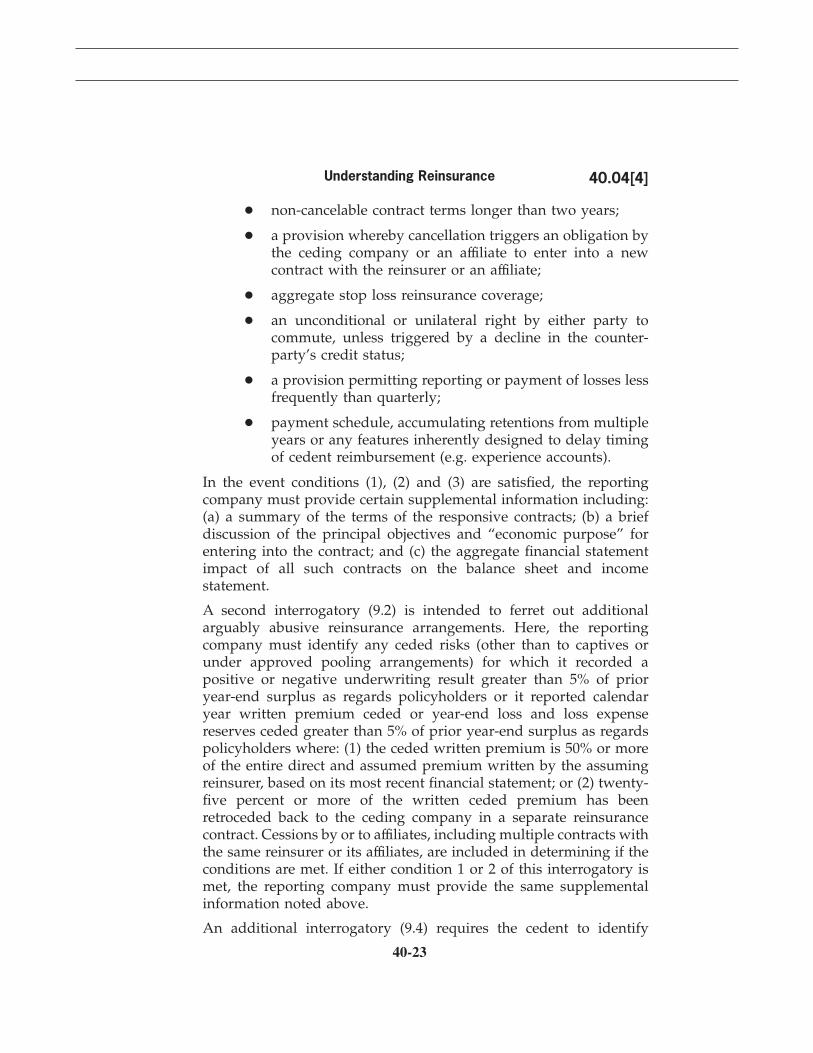

Example: Effective in 2006 and 2007, the National Association ofInsurance Commissioners (“NAIC”) amended the disclosure re-quirements for companies that purchase finite risk reinsurance,and the new requirements demand substantial and ongoingmanagement attention. The new requirements include severalnew interrogatories (which are part of the “General Interrogato-ries” section of the Annual Statement) that apply to “ceded”reinsurance and are intended to identify reinsurance agreementsthat have characteristics of contracts which the regulators haveidentified as prone to abuse and which warrant closer review. Forexample, under Interrogatory 9.1, the reporting company is askedto identify any ceded reinsurance which meets three conditions:(1) the agreement alters surplus by more than 3% (positive ornegative) or represents more than 5% of premiums or losses; (2)the contract was accounted for as reinsurance and not as adeposit; and (3) the contract has one or more of the followingfeatures “or other features that would have similar results”:

40.04[4] New Appleman Insurance Practice Guide

40-22

• non-cancelable contract terms longer than two years;

• a provision whereby cancellation triggers an obligation bythe ceding company or an affiliate to enter into a newcontract with the reinsurer or an affiliate;

• aggregate stop loss reinsurance coverage;

• an unconditional or unilateral right by either party tocommute, unless triggered by a decline in the counter-party’s credit status;

• a provision permitting reporting or payment of losses lessfrequently than quarterly;

• payment schedule, accumulating retentions from multipleyears or any features inherently designed to delay timingof cedent reimbursement (e.g. experience accounts).

In the event conditions (1), (2) and (3) are satisfied, the reportingcompany must provide certain supplemental information including:(a) a summary of the terms of the responsive contracts; (b) a briefdiscussion of the principal objectives and “economic purpose” forentering into the contract; and (c) the aggregate financial statementimpact of all such contracts on the balance sheet and incomestatement.

A second interrogatory (9.2) is intended to ferret out additionalarguably abusive reinsurance arrangements. Here, the reportingcompany must identify any ceded risks (other than to captives orunder approved pooling arrangements) for which it recorded apositive or negative underwriting result greater than 5% of prioryear-end surplus as regards policyholders or it reported calendaryear written premium ceded or year-end loss and loss expensereserves ceded greater than 5% of prior year-end surplus as regardspolicyholders where: (1) the ceded written premium is 50% or moreof the entire direct and assumed premium written by the assumingreinsurer, based on its most recent financial statement; or (2) twenty-five percent or more of the written ceded premium has beenretroceded back to the ceding company in a separate reinsurancecontract. Cessions by or to affiliates, including multiple contracts withthe same reinsurer or its affiliates, are included in determining if theconditions are met. If either condition 1 or 2 of this interrogatory ismet, the reporting company must provide the same supplementalinformation noted above.

An additional interrogatory (9.4) requires the cedent to identify

Understanding Reinsurance 40.04[4]

40-23

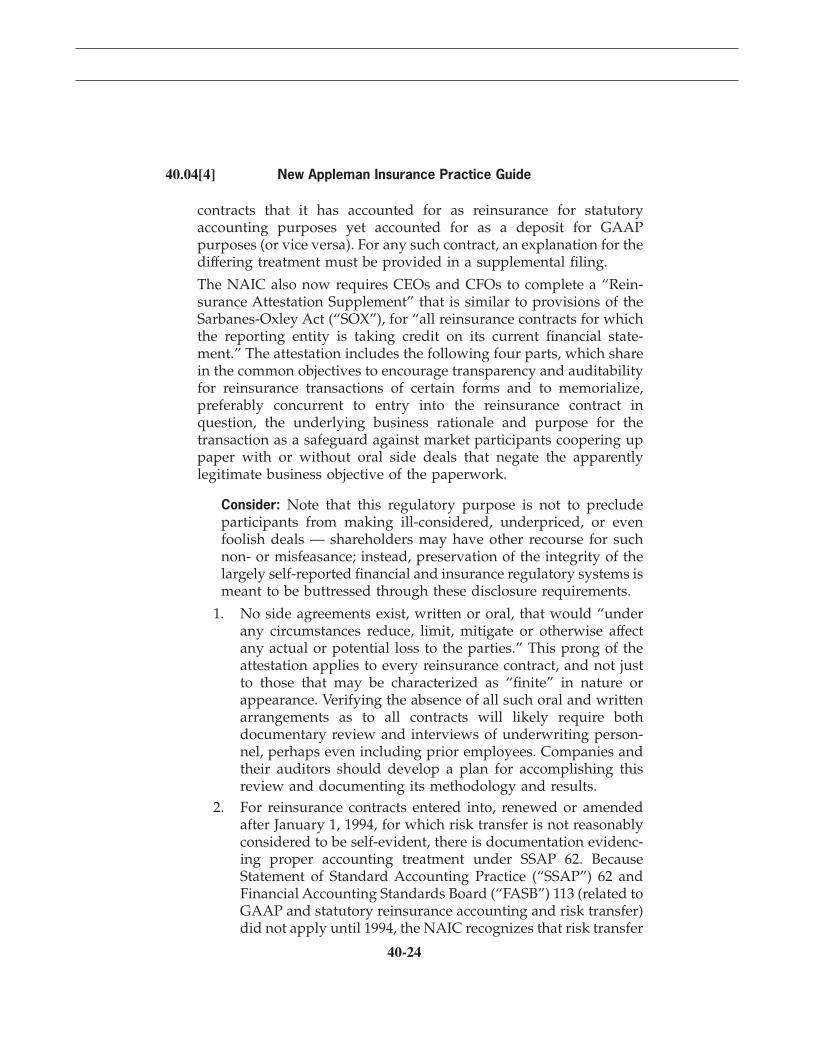

contracts that it has accounted for as reinsurance for statutoryaccounting purposes yet accounted for as a deposit for GAAPpurposes (or vice versa). For any such contract, an explanation for thediffering treatment must be provided in a supplemental filing.

The NAIC also now requires CEOs and CFOs to complete a “Rein-surance Attestation Supplement” that is similar to provisions of theSarbanes-Oxley Act (“SOX”), for “all reinsurance contracts for whichthe reporting entity is taking credit on its current financial state-ment.” The attestation includes the following four parts, which sharein the common objectives to encourage transparency and auditabilityfor reinsurance transactions of certain forms and to memorialize,preferably concurrent to entry into the reinsurance contract inquestion, the underlying business rationale and purpose for thetransaction as a safeguard against market participants coopering uppaper with or without oral side deals that negate the apparentlylegitimate business objective of the paperwork.

Consider: Note that this regulatory purpose is not to precludeparticipants from making ill-considered, underpriced, or evenfoolish deals — shareholders may have other recourse for suchnon- or misfeasance; instead, preservation of the integrity of thelargely self-reported financial and insurance regulatory systems ismeant to be buttressed through these disclosure requirements.

1. No side agreements exist, written or oral, that would “underany circumstances reduce, limit, mitigate or otherwise affectany actual or potential loss to the parties.” This prong of theattestation applies to every reinsurance contract, and not justto those that may be characterized as “finite” in nature orappearance. Verifying the absence of all such oral and writtenarrangements as to all contracts will likely require bothdocumentary review and interviews of underwriting person-nel, perhaps even including prior employees. Companies andtheir auditors should develop a plan for accomplishing thisreview and documenting its methodology and results.

2. For reinsurance contracts entered into, renewed or amendedafter January 1, 1994, for which risk transfer is not reasonablyconsidered to be self-evident, there is documentation evidenc-ing proper accounting treatment under SSAP 62. BecauseStatement of Standard Accounting Practice (“SSAP”) 62 andFinancial Accounting Standards Board (“FASB”) 113 (related toGAAP and statutory reinsurance accounting and risk transfer)did not apply until 1994, the NAIC recognizes that risk transfer

40.04[4] New Appleman Insurance Practice Guide

40-24

analysis may not have been memorialized contemporaneously.In terms of which contracts have reasonably self-evident risktransfer, the ceding company may want to look back to theInterrogatories. Certainly, any contract reportable under theconditions delineated will be subject to this prong of theattestation. Companies will want to obtain guidance fromcounsel and auditors as to what constitutes sufficient “risktransfer analysis” in today’s environment.

3. The reporting entity complies with all requirements of SSAP62. This deceptively simple sounding prong will require thecareful exercise of “due diligence.” Each company will deter-mine, perhaps based on consultation with accountants, law-yers and independent auditors, what constitutes sufficient duediligence to establish compliance with all of the risk transferand accounting requirements of SSAP 62.

4. The reporting entity has appropriate controls in place tomonitor the use of reinsurance and adhere to the provisions ofSSAP 62. This prong is the key to the ability to make theCEO/CFO attestations on an ongoing basis. Some companieswill have sufficient controls already in place; others will needto develop such controls and put them in place as soon aspossible.

40.04[5] Fronting Arrangements. There is not a general agreement inthe reinsurance industry as to how fronting is defined, and there arevarying perceptions of whether the general duties and relationshipsbetween cedent and reinsurer change in the context of a “fronting”arrangement. At a minimum, fronting involves the reinsurance of allor substantially all of a book of business. The ceding company retainslittle or no net liability on the ceded business and receives a fee(through the ceding commission and perhaps other forms of com-pensation such as service fees) in exchange for allowing the businessto be written on its paper. Sometimes, the goal of a fronted arrange-ment is to have the insurance that is sought to be brought to themarketplace sold through the auspices of an “admitted” carrier, eventhough the real party in interest — with underwriting expertise andper the reinsurance contract financial exposure vis-a-vis the cedent/front — is the reinsurer. In many fronting arrangements, a managinggeneral agency (“MGA”) underwrites the business and handlesclaims on the reinsured policies. There is disagreement as to whatextent responsibility for monitoring the MGA and responsibility forthe MGA’s misdeeds lies with cedent or reinsurer. It is clear, however,

Understanding Reinsurance 40.04[5]

40-25

that a fronting insurer remains contractually liable to perform withrespect to its insureds under the direct policies, whether or not it isindemnified by its reinsurer [Am. Special Risk Ins. Co. v. Delta Am.Re-Insurance Co., 836 F. Supp. 183, 185 (S.D.N.Y. 1993)]. The rein-surer, lacking privity with the direct insured, may be exposed toclaims of tortious interference with contract or for prospectiveeconomic advantage if it directs the cedent/front not to pay a validclaim. At the same time, the cedent faces the risk that if it pays thedirect claim without the support of its reinsurer a risk that it thoughtit may be only fronting may remain on its doorstep, for the reinsurermay assert that the payment to the direct insured was never owed inthe first place under the direct insurance policy and thus representsan uncovered, ex gratia or gratuitous payment for which indemnifi-cation under the reinsurance arrangement is not owed.

z Strategic Point: The reinsurance contract in a fronting arrange-ment should optimally specify who is responsible for oversight ofthe MGA and who is responsible if the MGA breaches its duties.

Consider: Parties should confirm that fronting is allowed in theirjurisdiction, and that there are no specific regulations that arerelevant to their arrangements.

z Strategic Point: Fronting arrangements enable reinsurers toaccept 100 percent of the liability in states where they are notlicensed to write such business on a direct basis [Reliance Ins. Co.v. Shriver, 224 F.3d 641, 642 (7th Cir. 2000); Union Sav. Am. LifeIns. Co. v. N. Central Life Ins. Co., 813 F. Supp. 481, 484 (S.D. Miss.1993); Equity Diamond Brokers, Inc. v. Transnational Ins. Co., 785N.E.2d 816, 818 (Ohio Ct. App. 2003)]. In some instances, frontingallows alien insurers to accept 100 percent of the exposure onrisks it is prohibited by regulatory restrictions to write directly[Gallinger v. Vaaler Ins., 12 F.3d 127, 128 n.1 (8th Cir. 1994)(applying North Dakota law)]. It should be noted that frontingcan be done as a retrocession also. Fronting allows cedinginsurers to receive reinsurance credit that would not be available,at least without security, if the reinsurance was issued directly byan unauthorized reinsurer [see § 40.06 below for a discussion ofcredit for reinsurance]. A licensed reinsurer can front for anunauthorized reinsurer or a reinsurance syndicate, to permit theceding insurer to take credit for the reinsurance without need forsecurity [Am. Special Risk Ins. Co. v. Delta Am. Re-Insurance Co.,836 F. Supp. 183, 185 (S.D.N.Y. 1993)].

40.04[5] New Appleman Insurance Practice Guide

40-26

40.05 Lack of Privity of Contracts.

40.05[1] Know General Rule. A fundamental principle of reinsuranceis that the reinsurer ordinarily is not liable to the original policy-holder of the ceding insurer; it is not a co-signer of the policy issuedto the original policyholder, and it is not jointly and severallyobligated to make good on the benefits the policyholder sought toobtain under the insurance contract sold by the insurer/cedent.Many court decisions have recognized that the reinsurer is incontractual privity only with the ceding company and has nocontractual obligation to the original insured, underlying claimants,or any third parties [Barhan v. Ry-Ron, Inc., 121 F.3d 198 (5th Cir.1997) (applying Texas law); Travelers Cas. & Sur. Co. v. PrudentialReinsurance Corp., 2001 U.S. Dist. LEXIS 10913 (N.D. Ohio 2001),citing Stickel v. Excess Ins. Co. of Am., 23 N.E.2d 839 (Ohio 1939);Prudential Reinsurance Co. v. Superior Court (Garamendi), 842 P.2d48 (Cal. 1992)]. Moreover, most courts have rejected claims broughtby original policyholders against reinsurers based on agency andthird-party beneficiary theories [Aetna Ins. Co. v. Glens Falls Ins. Co.,453 F.2d 687, 690 (5th Cir. 1972) (applying Georgia law); Reid v.Ruffin, 469 A.2d 1030 (Pa. 1983)].

Exception: While the rule of lack of privity is generally respsectedby the courts, there have been some cases, particularly arising outof the insolvency of the direct insurer/cedent, where a court hascharacterized the original policyholder as a third-party benefi-ciary of the reinsurance arrangement, thus possessing the rightsto enforce a contract to which it is not a party in accordance withthe ordinary contract-law rules governing third-party beneficia-ries. Policyholders may seek to skip over the insurer with whichit has privity by arguing that the reinsurer is the alter ego of theinsurer, at least insofar as the particular policy or particularinsurance program is concerned. For example, in the bankruptcycontext, reinsurers were considered to be the true risk bearerswhere the ceding insurer merely acted as the fronting company,bore no underwriting risk, and left responsibility for claimshandling and funding to the reinsurers [Koken v. Legion Ins. Co.,831 A.2d 1196, 1237-38 (Pa. Commw. Ct. 2003)]. In another case,the court found that an insured had third-party beneficiary statuswhere the insurer acted as a fronting company and the reinsurersbore all responsibility for underwriting and claims handling andmanaged the defense of coverage claims [Venetsanos v. Zucker,Facher & Zucker, 638 A.2d 1333, 1339-40 (N.J. Super. Ct. App. Div.

Understanding Reinsurance 40.05[1]

40-27

1994)]. [See § 40.04[5] above for a discussion of fronting arrange-ments]. However a federal district court in Missouri rejected thetheory that a reinsurer’s conduct in paying claims alone can makethe reinsurer liable directly to the original insured [AllendaleMut. Ins. Co. v. Crist, 731 F. Supp. 928, 932-33 (W.D. Mo. 1989)].Similarly, a federal district court in New Jersey rejected thepolicyholders’ assertion that a reinsurer’s involvement in the“adjustment and settlement of claims” (as is common where thereis a claims-control clause) allowed the court to “pierce the allegedreinsurance veil” [G-I Holdings v. Hartford Fire Ins. Co., 2007 U.S.Dist. LEXIS 19060, at *40-41 (D.N.J. 2007)].

Exception: It may be possible for an insured to bring a directaction against a reinsurer if the reinsurer allegedly induced thedirect insurer to breach the underlying policy by denying theclaims in question. For example, a tort claim based on this theoryasserted by policyholders against a reinsurer recently survived amotion to dismiss in a federal district court in Florida [LawOffices of David J. Stern v. SCOR Reinsurance Corp., 354 F. Supp.2d 1338, 1341-42 (S.D. Fla. 2005)].

� Cross Reference: For a general discussion of a reinsurer’spotential liability to the policyholder of the ceding insurer, see EricMills Holmes, Appleman on Insurance 2d § 106.7.

40.05[2] Consider Cut-Throughs. A significant exception to the gen-eral rule that an insured may not seek payment directly from areinsurer is present where a cut-through endorsement is contained inthe original underlying policy. A cut-through provision gives aninsured a contractual right to pursue a direct action against thereinsurer; it can be conceived of as an express grant of third-partybeneficiary status of the putative non-party direct insured. Cut-throughs most often apply only when the direct insurer is insolventand provide that the loss which the reinsurer would have paid to theestate of the insolvent insurer is instead paid directly to the originalpolicyholder [compare Wilcox v. Anchor Wate, 2006 UT 6]. A cut-through is similar to an “assumption reinsurance” arrangement,which effectively is the consensual substitution of the reinsurer forthe cedent as the agent for performance, which in turn typically vestsin the direct insured the right to pursue either the original directinsurer (with which it has contract privity) or the assumer of thedirect insurer’s liability, at the insured’s election. One differencebetween a cut through and an assumption arrangement, is that cut

40.05[2] New Appleman Insurance Practice Guide

40-28

throughs more often are agreed ex ante, that is, when the policy isplaced, and assumptions occur when the cedent effects a loss-portfolio transfer to a reinsurer by which the reinsurer steps into itsshoes inter sese. The assumption must be an explicit written assump-tion of liability to the original policyholder who acquires a directright of action against the reinsurer; note that since the assumptiontakes place on only one side of the transaction, it is not a “novation,”freeing the original contracting party from its contractual duties; it isnot fictive, however, which is why the direct insured often will bepermitted to elect to pursue either the original party in privity or theassumption reinsurer. Many state statutes permit reinsurers to enterinto cut-through endorsements. [Cal. Ins. Code § 922.2; N.Y. Ins.Code § 1308(a)(2)(B); Tex. Ins. Code § 493.055]. This right has beenrecognized by many courts as well [Martin Ins. Agency, Inc. v.Prudential Reinsurance Co., 910 F.2d 252-53 (5th Cir. 1990) (interpret-ing Louisiana law); Bruckner-Mitchell, Inc. v. Sun Indem. Co., 82 F.2d434, 444 (D.C. Cir. 1936); Klockner Stadler Hurter, Ltd. v. Ins. Co. ofPennsylvania, 785 F. Supp. 1130, 1134 (S.D.N.Y. 1990)].

Exception: Cut-through endorsements that interfered with admin-istration of an insolvent insurer’s estate were found to beunenforceable [Colonial Penn Ins. Co. v. Am. Centennial Ins. Co.,1992 U.S. Dist. LEXIS 17552, at *15-18 (S.D.N.Y. 1992), discussingFoster v. Mutual Fire, Marine & Inland Ins. Co., 531 Pa. 598, 614(1992)].

t Warning: Cut-through endorsements are unenforceable underBermuda law [Dunlop Pneumatic Tire Company Ltd. v. Selfridge& Co. Ltd. [1915] A.C. 847]. Insurers and reinsurers shouldcarefully research the legality and enforceability of cut-throughclauses before using them.

� Cross Reference: For a discussion of cut-through endorsementsand related contract provisions, see Eric Mills Holmes, Applemanon Insurance 2d § 167.2[B][1].

Understanding Reinsurance 40.05[2]

40-29

III. CONSIDERING REINSURANCE REGULATION.

40.06 Credit for Reinsurance. Credit for reinsurance laws constitute a keycomponent of the regulation of reinsurance in the United States. Theselaws determine the circumstances in which a ceding insurer can takefinancial statement credit for reinsurance recoverables as an asset and as areduction of its unearned premium and loss reserves on account ofreinsurance ceded. Where an insurer can take credit for reinsurance, it canincrease its “surplus” and thus expand its allowed capacity to write newinsurance business. In order to qualify for financial statement credit, moststates require that the reinsurer be licensed or accredited in the same statewhere the direct insurer does business, or that the reinsurer be domiciledand licensed in a state that employs substantially similar credit forreinsurance standards to those imposed by the direct insurer’s state ofdomicile. Most states also allow credit for reinsurance ceded to a non-United States reinsurer that maintains a trust fund in the U.S. for theprotection of its U.S. ceding insurers. In addition, the reinsurance contractmust actually materially transfer risk from the cedent to the reinsurer andinclude an insolvency clause [see § 40.08 below for a discussion of theinsolvency clause]. Some states also require that the reinsurer assume allcredit risks of any intermediary receiving payments [N.Y. Comp. Codes R.& Regs. tit. 11, § 125.6].

Exception: A significant portion of the reinsurance in the U.S. is cededto unlicensed alien reinsurers that are not regulated for solvency in anystate. A ceding insurer can still take credit for reinsurance ceded tounlicensed or unaccredited reinsurers if the recoverables are ad-equately collateralized. This requirement is satisfied if the reinsurermaintains certain trust deposits for the protection of all of its U.S.cedents. Alternatively, the reinsurer can provide individual cedentswith collateral. The ceding company can reduce its balance sheetliabilities by an amount equal to the collateralization. Ceding insurerstypically secure the payment of reserves on reinsured liabilities (i.e.,case reserves, incurred but not reported reserves (“IBNR”), unearnedpremium reserve and reserve for allocated loss adjustment expenses(“LAE”)) by means of a clean letter of credit issued or confirmed by afinancial institution approved by the state insurance commissioner [see§ 40.06 below for a discussion of letters of credit]. In these circum-stances, the reinsurer is the applicant requesting the bank to issue theletter of credit in favor of the beneficiary, the ceding insurer. Trustfunds, reinsurer funds held by the cedent as security (“fundswithheld”) or other approved mechanisms also may be viewed as

40-30

collateral sufficient to permit credit for reinsurance [N.Y. Comp. CodesR. & Regs. tit. 11, § 126.3]. Many of these rules, however, are currentlyunder review by the National Association of Insurance Commissioners(“NAIC”) and the federal government.

Example: The NAIC develops model laws, regulations and financialstatements in order to achieve substantial similarity of state laws andprocedures in key areas of solvency, including credit for reinsurance.The NAIC has issued a recommended credit for reinsurance modellaw and regulation, some variation of which has been promulgated byevery state [Model Law on Credit for Reinsurance (2003) and ModelRegulation on Credit for Reinsurance reprinted in Eric Mills Holmes,Appleman on Insurance 2d].

Example: The State of California recently adopted a comprehensive setof regulations, referred to as the “Reinsurance Oversight Regulations,”which cover the following three general topics: (1) the ceding compa-ny’s accounting for reinsurance on its financial statements; (2) require-ments applicable to the form and content of reinsurance agreements;and (3) oversight of reinsurance transactions and related sanctions.The requirements are intended “to elicit from insurers a true exhibit oftheir financial condition and to safeguard the solvency of licensees”and apply to all insurers licensed or accredited in California, allapproved U.S. trusts of otherwise unauthorized reinsurers and li-censed reinsurance intermediaries. In addition, reinsurers that are notlicensed in California but assume risks from California domestic andforeign insurers may also be affected by changes in the regulationswith respect to approved forms of security securing reinsuranceobligations. The regulations contain detailed requirements for licensedinsurers intending to receive credit for reinsurance on their financialstatements, requirements for risk transfer and requisites for reinsur-ance arrangements, including, specifically:

• Credit for reinsurance ceded to admitted insurers and accred-ited reinsurers;

• Credit for reinsurance secured by an approved U.S. trust;

• Credit for reinsurance required by law;

• Credit for reinsurance secured by a single beneficiary trust, aletter of credit, or funds withheld;

• Credit for reinsurance of foreign insurers;

• Transfer of risk for both life and disability and property andcasualty business;

Understanding Reinsurance 40.06

40-31

• Contract requirements for statement credit; and

• Requirements regarding the form of reinsurance arrangements[Cal. Code Regs. tit. 10, §§ 2303-2303.25].

Example: New York similarly provides credit for reinsurance asfollows:

Ҥ 1301. Admitted assets

(a) In determining the financial condition of a domestic or foreigninsurer or the United States branch of an alien insurer for the purposesof this chapter, there may be allowed as admitted assets of such insurer,unless otherwise specifically provided in this chapter, only the follow-ing assets owned by such insurer:

* * *

(14) Reinsurance recoverable by a ceding insurer: (i) from an insurerauthorized to transact such business in this state, except from a captiveinsurance company licensed pursuant to the provisions of article seventy ofthis chapter, in the full amount thereof; (ii) from an accredited reinsurer . . .to the extent allowed by the superintendent on the basis of the insurer’scompliance with the conditions of any applicable regulation; or (iii) from aninsurer not so authorized or accredited or from a captive insurance companylicensed pursuant to the provisions of article seventy of this chapter, in anamount not exceeding the liabilities carried by the ceding insurer foramounts withheld under a reinsurance treaty with such unauthorized insureror captive insurance company licensed pursuant to the provisions of articleseventy of this chapter as security for the payment of obligations thereunderif such funds are held subject to withdrawal by, and under the control of, theceding insurer” [N.Y. Ins. Law § 1301].

� Cross Reference: For an example of an unauthorized reinsuranceclause applying to reinsurance ceded to an unauthorized reinsurer, see§ 40.33 below.

40.07 Letters of Credit. Sometimes, reinsurance contracts require licensedreinsurers to post letters of credit. However, letters of credit are morecommonly obtained by ceding companies which place reinsurance withnon-admitted reinsurers and wish to take credit for reinsurance on theirfinancial statements [see § 40.06 above for a discussion of letters of creditas security under credit for reinsurance laws]. The “Asset or Reductionfrom Liability” section of the NAIC’s Model Law on Credit for Reinsur-ance, adopted in the same or an equivalent form by most states, sets forththe requirements for collateralization of recoverables from non-admittedreinsurers. The NAIC provision stipulates that letters of credit securing the

40.07 New Appleman Insurance Practice Guide

40-32

payment of reinsurance obligations must be issued or confirmed by aqualified U.S. financial institution and be clean, irrevocable, unconditionaland “evergreen,” requiring the financial institution to provide notice priorto expiration [Model Law on Credit for Reinsurance, Section 23 (2003)].The NAIC Model Letter of Credit regulations further provide that lettersof credit must not be subject to side agreements and must stipulate that thebeneficiary need only draw a sight draft under the letter of credit andpresent it to obtain funds and need not present any other document[Credit for Reinsurance Model Regulation, Section 11A (July 2003)].

z Strategic Point — Cedent: Ceding insurers should make sure thatletters of credit comply with statutory requirements so they canproperly take credit for reinsurance.

Example: Regulation 133 issued by the New York State InsuranceDepartment sets forth conditions for letters of credit which may betreated as an asset by a ceding insurer. Among other things, anacceptable letter of credit must: be irrevocable; be clean and uncondi-tional; be issued, presentable and payable at an office of the qualifiedbank in the U.S.; contain a statement that identifies the beneficiary;contain a statement that it is not subject to any agreement, condition orqualification outside of the letter of credit; contain a statement to theeffect that the obligation of the issuing bank under the letter of creditis an individual obligation of such bank and is in no way contingentupon reimbursement with respect thereto; contain an issue date and adate of expiration; have a term of at least one year and contain anevergreen clause which provides at least 30 days’ written notice to thebeneficiary prior to expiry date for nonrenewal; and state that it issubject to and governed by New York law [N.Y. Comp. Codes R. &Regs. tit. 11, § 79.2].

40.08 Insolvency Clause. In most states, a rehabilitator or liquidator underthe direction of the domiciliary state’s insurance department takes controlof an insurance company that is determined to be insolvent. Althoughreinsurance agreements are indemnity contracts, they usually include aninsolvency clause which alters the indemnity nature of the contract whenthe ceding insurer becomes insolvent. The insolvency clause permits aliquidator to collect from the reinsurer the amount of reinsurance proceedsthat would have become due if the ceding insurer had not becomeinsolvent, even if the cedent has not paid its original policyholders. Theliquidator of the estate assumes the insurer’s rights and obligations underthe reinsurance agreement, including the reporting, settlement and de-

Understanding Reinsurance 40.08

40-33

fense of claims, and can promptly discharge the insolvent insurer’sobligations to claimants.

Most states have encouraged the inclusion of insolvency clauses byenacting legislation providing that the original insurer may not take creditfor reinsurance on its financial statement unless the reinsurance contractcontains an insolvency provision [Cal. Ins. Code § 922.2; N.Y. Ins. Law§ 1308[a][2]; Mass. Ann. Laws ch. 175, § 20A]. This is a significantincentive, as one of the primary reasons for obtaining reinsurance isdefeated if the cedent is forced to maintain reserves for the full amount ofreinsurance ceded [see § 40.06 above which discusses the advantages ofobtaining credit for reinsurance]. As a result, these statutes have had theeffect of ensuring that virtually all reinsurance agreements issued to U.S.cedents include an insolvency clause.

z Strategic Point — Cedents: Cedents should ensure that the insol-vency clause meets the requirements of the insurance department oftheir domiciliary state. There are generally five key provisions in-cluded in the insolvency clause: (1) there is no diminution of the claimspaid by virtue of the cedent’s insolvency; (2) the liquidator mustprovide notice of the pendency of a claim; (3) the reinsurer has theright to investigate and defend claims; (4) the expenses incurred by thereinsurer in defense of claims may be reimbursable; and (5) thereinsurance proceeds are payable to the liquidator with statutoryexceptions (i.e. cut-throughs) [Robert C. Reinarz, et al., ReinsurancePractices, Vol. I, 67-68 (1st ed. 1990)].

� Cross Reference: For an example of a standard insolvency clause, seeBusiness Insurance Law and Practice Guide § 14.08[3]; see also § 40.34below.

z Strategic Point — Reinsurer: There can be a tension between theliquidator’s interests and those of the insolvent company’s reinsurers;if the liquidator agrees to pay a direct insurance claim, it can collectreinsurance on the claim even if the estate does not have sufficientassets to pay the claim, in whole or in part [see Robert W. Hammesfahrand Scott W. Wright, The Law of Reinsurance Claims 254 (1992)].Therefore, reinsurers often monitor liquidators to ensure that theyhandle claims properly until a full settlement is concluded. Many statestatutes provide that the insolvency clause may permit the reinsurer toinvestigate claims against the insolvent ceding company and interposeany defense or defenses which it may deem to be available to theceding company or its liquidator, receiver or statutory successor in theproceeding where the claim is adjudicated [N.Y. Ins. Law § 1308(a)(3);

40.08 New Appleman Insurance Practice Guide

40-34

Cal. Ins. Code § 922.2(a)(2)]. Reinsurers should ensure that theirinsolvency clauses include this wording.

z Strategic Point — Reinsurer: Many reinsurance contracts include anoffset clause providing for net accounting between the parties [see§ 40.35 for an example of a typical offset clause]. In addition, areinsurer may have a statutory or common law right of set-off (oroffset) against amounts owed to an insolvent insurer’s estate for anyamounts that the insolvent insurer owed to the reinsurer. In the eventof the cedent’s insolvency, an offset clause protects the reinsurer byallowing it to reduce the sum that would otherwise be payable to theinsolvent estate by the amount it is owed. In the absence of a right ofoffset, the reinsurer would be forced to pay claims in full, and it wouldpossess an independent claim for any premiums or other sums owedby the cedent (which might be paid at only a fraction of the amountdue given that the cedent is insolvent). Several state insurance statutesexpressly permit set-offs when the insolvent insurer owed the debtbefore the date of liquidation and the debts and credits are consideredmutual [Cal. Ins. Code § 1031; Fla. Stat. Ann. § 631.281; N.Y. Ins. Law§ 7427]. Several courts have held that inclusion of a statutory insol-vency clause in the reinsurance contract does not destroy the reinsur-er’s right to set-off [Comm’r of Ins. v. Munich Am. Reinsurance Co.,706 N.E.2d 694, 697 (Mass. 1999); Prudential Reinsurance Co. v.Superior Court, 842 P.2d 48, 63-64 (Cal. 1992); In re Midland InsuranceCo., 590 N.E.2d 1186, 1192 (N.Y. 1992)]. However, at least one court hasfound that the insolvency clause’s directive that reinsurance bepayable without “diminution due to the insolvency of the cedinginsurer” abrogates the reinsurer’s right to offset unpaid premiumsfrom sums due under the insurer’s policies [Bluewater Ins., Ltd. v.Balzano, 823 P.2d 1365, 1371-74 (Colo. 1992)]. Another court hasdetermined that allowing a reinsurer to set-off unpaid premiumsagainst sums owed the insolvent insurer under the reinsuranceagreement would conflict with the priority of claims established bystate statute and thus, in effect, is a disguished preference in favor ofone creditor (the reinsurer) [Allendale Mut. Ins. Co. v. Melahn, 773 F.Supp. 1283, 1287-88 (W.D. Mo. 1991) (applying Missouri law)].

t Warning: Reinsurers of insolvent companies must take care to payclaims to the appropriate party; they are generally obligated to pay theliquidator administering the insolvent company’s estate, who isdeemed the “statutory successor” to the insolvent insurer [Martin Ins.Agency, Inc. v. Prudential Reinsurance Co., 910 F.2d 249 (5th Cir. 1990)(applying Missouri law); Excess & Cas. Reinsurance Ass’n v. Ins.