the reinsurance section presents advanced reinsurance seminar - soa · the reinsurance section...

TRANSCRIPT

The Reinsurance Section Presents

Advanced Reinsurance Seminar August 15‐16, 2016 | Hyatt Rosemont Hotel | Rosemont, IL

Off‐shore Reinsurance, Certified Reinsurers and Counterparty Credit Risk

Presenters: Donald D. Solow, FSA, MAAA

Advanced Reinsurance Seminar 2016Offshore Reinsurance and Counterparty Credit RiskDonald D Solow, FSA, MAAA

I. Offshore Reinsurance

• Definition• Reinsurance ceded to a non-North American

reinsurer, generally one domiciled in a jurisdiction having a different regulatory and/or tax regime

• Examples include Bermuda, Cayman Islands, Barbados, Ireland

• Not to be confused with “captives”

Advantages for the Reinsurer

• Ease of setting up• Flexible capital requirements based on

business plan rather than rigid rules• Accounting under GAAP or IAS• Potential for lower overall tax burden

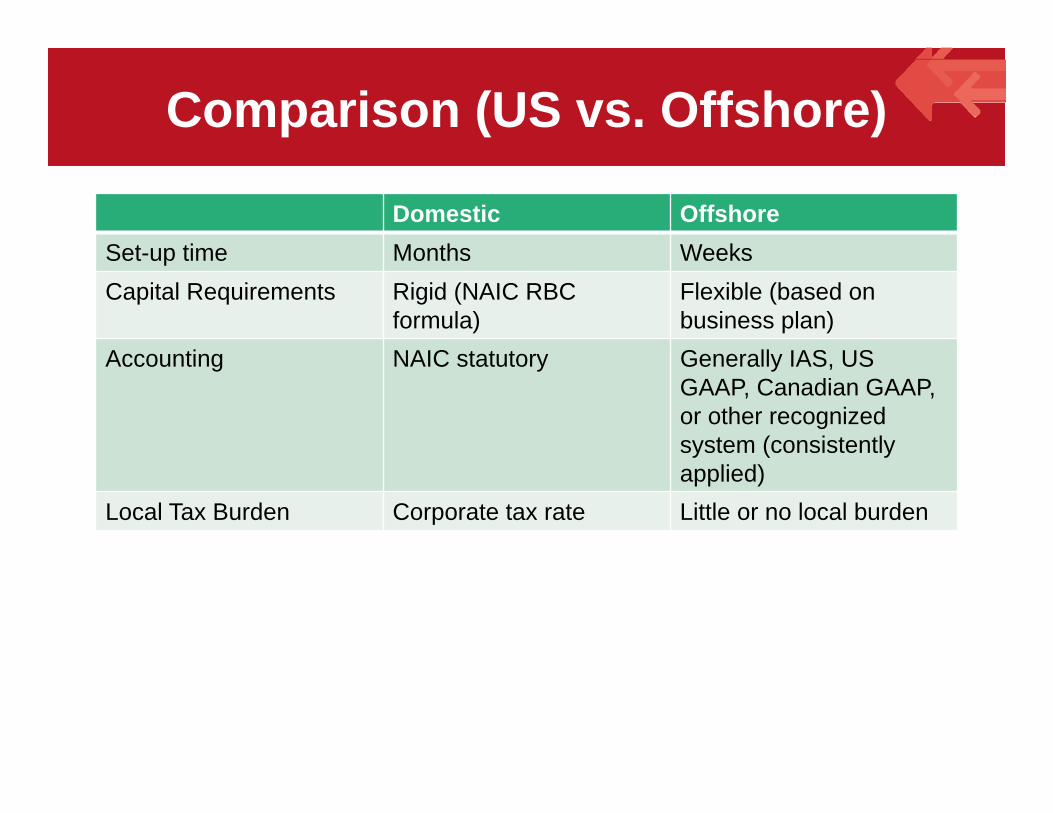

Comparison (US vs. Offshore)

Domestic OffshoreSet-up time Months WeeksCapital Requirements Rigid (NAIC RBC

formula)Flexible (based on business plan)

Accounting NAIC statutory Generally IAS, US GAAP, Canadian GAAP, or other recognized system (consistently applied)

Local Tax Burden Corporate tax rate Little or no local burden

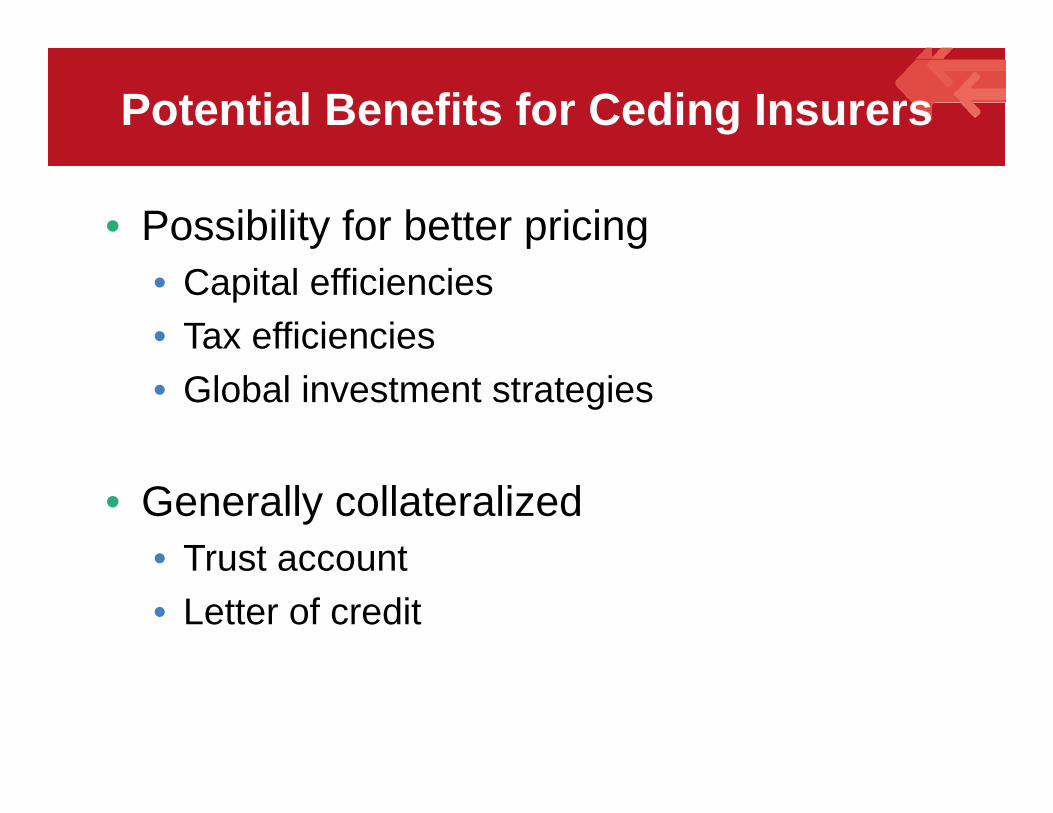

Potential Benefits for Ceding Insurers

• Possibility for better pricing• Capital efficiencies• Tax efficiencies• Global investment strategies

• Generally collateralized• Trust account• Letter of credit

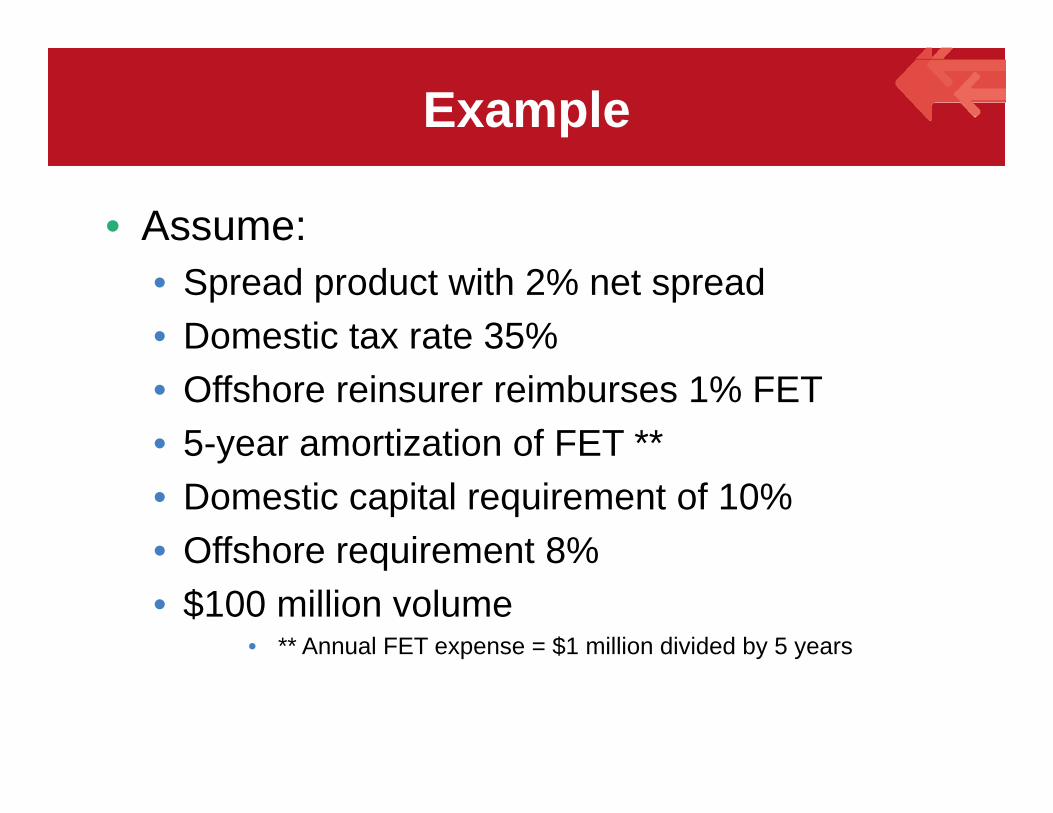

Example

• Assume:• Spread product with 2% net spread• Domestic tax rate 35%• Offshore reinsurer reimburses 1% FET• 5-year amortization of FET **• Domestic capital requirement of 10%• Offshore requirement 8%• $100 million volume

• ** Annual FET expense = $1 million divided by 5 years

Example (cont’d)

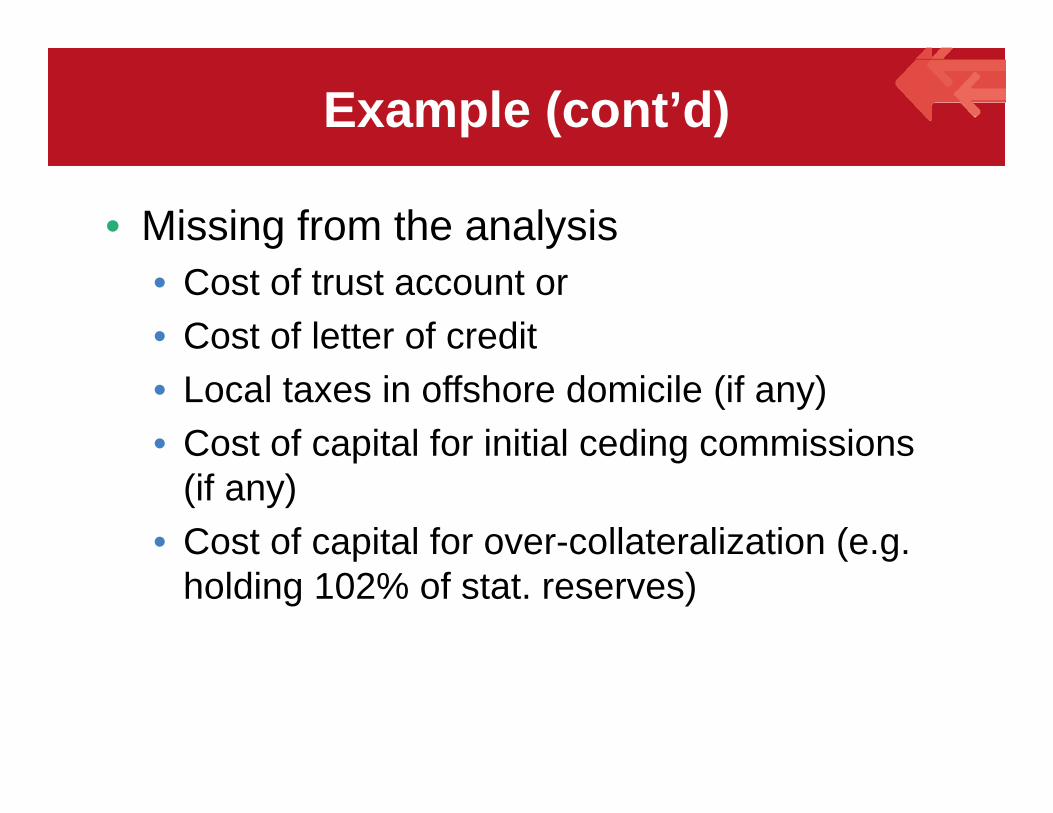

• Missing from the analysis• Cost of trust account or• Cost of letter of credit• Local taxes in offshore domicile (if any)• Cost of capital for initial ceding commissions

(if any)• Cost of capital for over-collateralization (e.g.

holding 102% of stat. reserves)

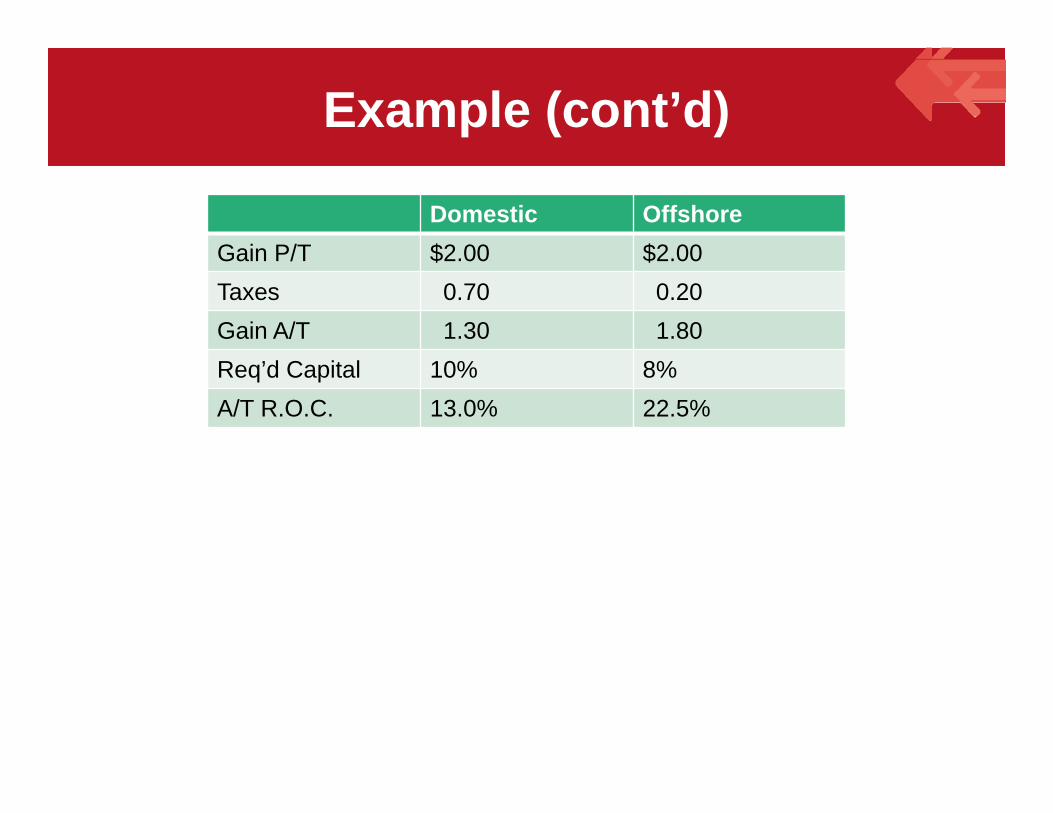

Example (cont’d)

Domestic OffshoreGain P/T $2.00 $2.00Taxes 0.70 0.20Gain A/T 1.30 1.80Req’d Capital 10% 8%A/T R.O.C. 13.0% 22.5%

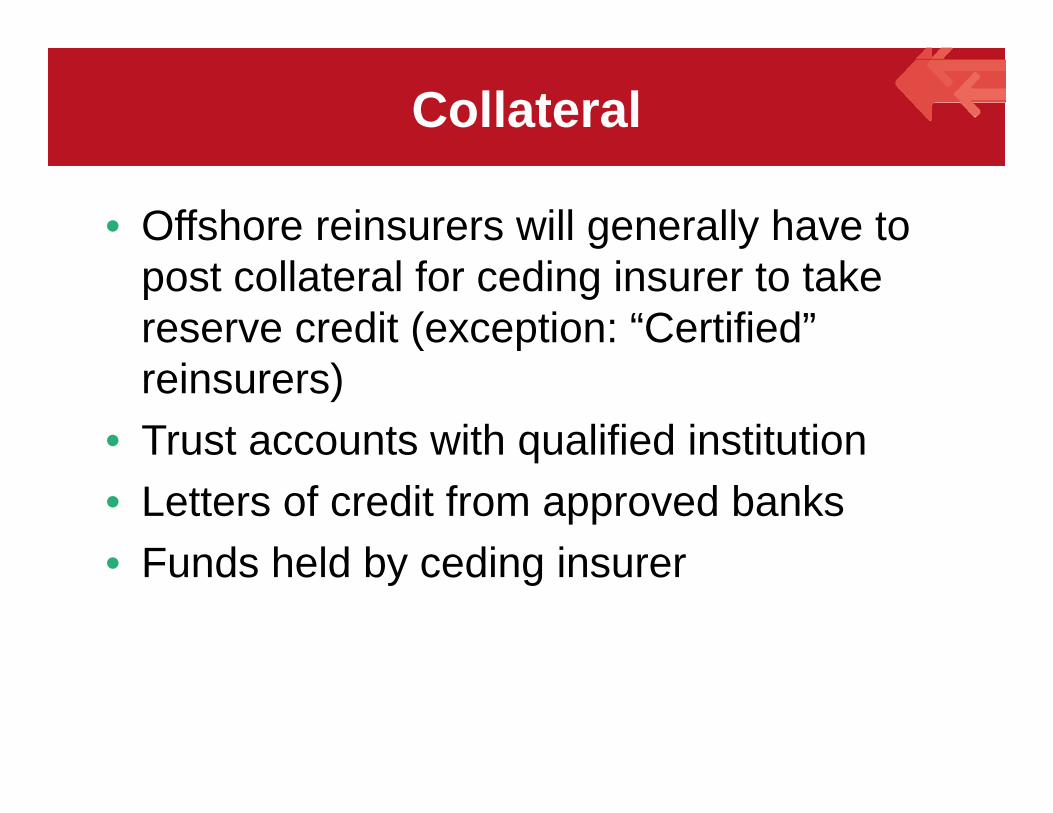

Collateral

• Offshore reinsurers will generally have to post collateral for ceding insurer to take reserve credit (exception: “Certified” reinsurers)

• Trust accounts with qualified institution• Letters of credit from approved banks• Funds held by ceding insurer

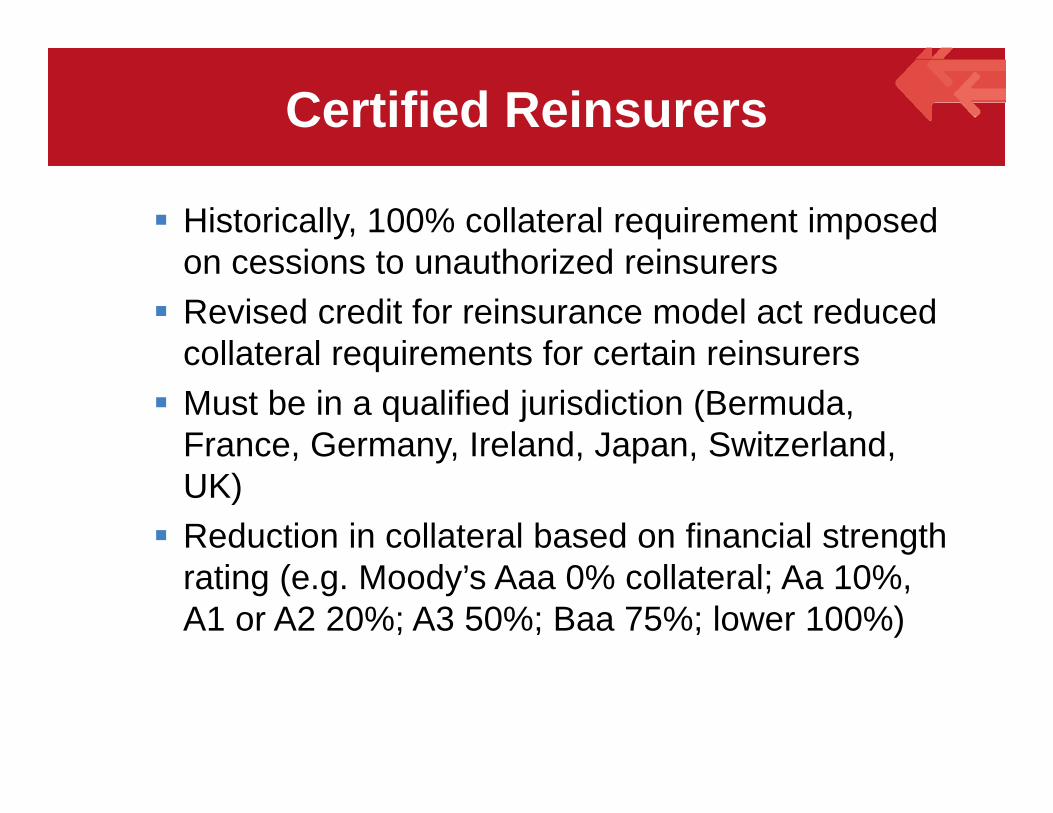

Certified Reinsurers

Historically, 100% collateral requirement imposed on cessions to unauthorized reinsurers Revised credit for reinsurance model act reduced

collateral requirements for certain reinsurers Must be in a qualified jurisdiction (Bermuda,

France, Germany, Ireland, Japan, Switzerland, UK) Reduction in collateral based on financial strength

rating (e.g. Moody’s Aaa 0% collateral; Aa 10%, A1 or A2 20%; A3 50%; Baa 75%; lower 100%)

Additional Considerations

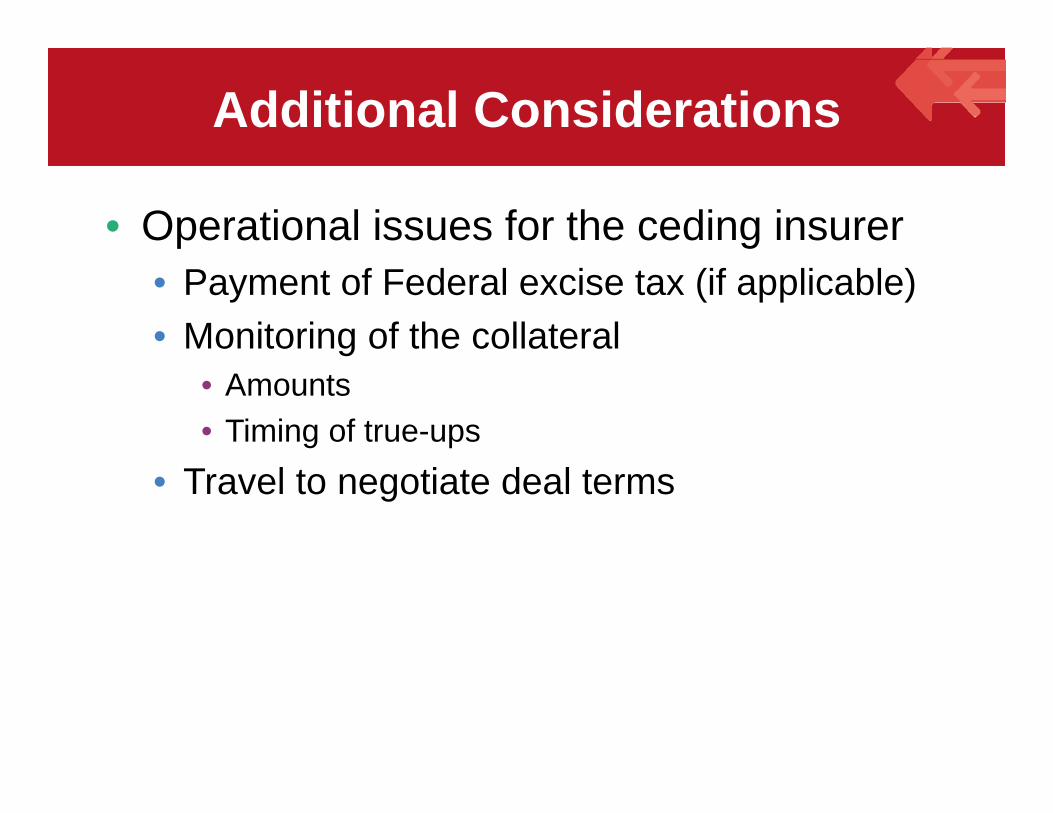

• Operational issues for the ceding insurer• Payment of Federal excise tax (if applicable)• Monitoring of the collateral

• Amounts• Timing of true-ups

• Travel to negotiate deal terms

II. Reinsurer Concentration Risk

Defined:• Too much credit risk exposure to one or

more reinsurers• But we need to clarify: What is “credit risk”? How much is “too much”?

Credit Risk in Reinsurance

Risk of default has two prongs:• Ability to perform all contractual

obligations• Willingness to do so

As a ceding insurer, have you clarified what you are worried about?

Reinsurer Events of Default

Consider:• Failure to pay an amount due• Failure to post proper level of collateral (if

so required)• Declaration of insolvency or bankruptcy• Winding up (running off) and its

implications

Events of Default (cont’d)

Consider:• Material breach of the reinsurance

agreement (other than failure to pay or post proper level of collateral)

• Cross default• Change in control• Loss of license or authority to do business

Failure to Pay / Failure to Post

Inability to pay – lack of adequate cash on hand to pay an amount due or true up collateral balance Company may be solvent but unable to generate

cash (e.g. too many illiquid assets) No easy remedy

Unwillingness to pay – amount may be in dispute, or lack of agreement on coverage May lead to arbitration or litigation

In case of failure to pay, having access to collateral may help

Declaration of Insolvency or Bankruptcy

Insolvency: liabilities > assets Bankruptcy: legal inability to pay debts Company may have ability to pay, but likely

subject to regulatory actions Payments may be limited, with some amounts

held back for potential payment later Having access to collateral should help

Winding Up (Running Off)

Implications may be problematic since reinsurer does not intend to write new business: Increases in non-guaranteed contract elements

(e.g. YRT rate increases) Scrutiny of contracts to look for ways out or for

ways to minimize payouts Coverage and/or claim disputes Management team replaced with run-off specialists

Material Breach

Failure to honor the contract (other than failure to pay and failure to post) Examples: failure to maintain pre-agreed

financial ratios, ratings, or asset mix Remedy may be arbitration/litigation or

recapture

Cross Default

Definition: company is considered in default on its obligation to you if it is in default on any other obligation to any party Example: reinsurer defaults on an interest

rate swap, or a bank line of credit Cross default provision not used in

reinsurance agreements

Change in Control

Company is sold to another group Possible implications: New team to deal with Different philosophy New owner may wish to wind up the company or

take substantial equity out You may already have exposure to the new owner

Recapture could be a possible remedy but reinsurer unlikely to agree

Loss of License or Authority

May be a breach of a contractual covenant to maintain license or authority to do business May be inadvertent (e.g. failure to pay a fee) If not accidental, then often a sign of severe

problems Remedy might be recapture

Measuring the Exposure

Once you have defined credit risk, how do you measure the exposure?• Maximum possible loss (“MPL”)• Probable maximum loss (“PML”)• Current level of reserve credit• Maximum level of reserve credit (if

reserves will increase)

Measuring the Exposure (cont’d)

• Maximum possible loss (“MPL”): for life insurance, this might be sums reinsured, or net amount at risk reinsured; may not be applicable to, for example, deferred annuities

• Probable maximum loss (“PML”): present value of loss under probable worst case; difficulty is in establishing this case

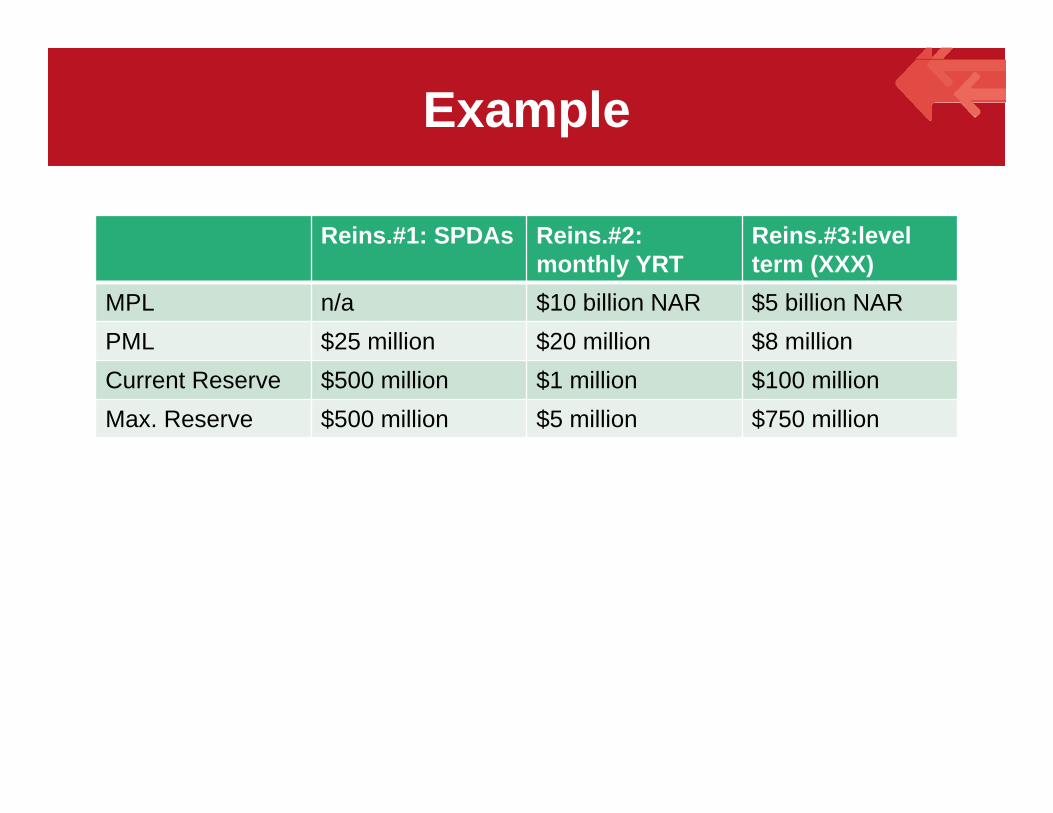

Example

Reins.#1: SPDAs Reins.#2: monthly YRT

Reins.#3:levelterm (XXX)

MPL n/a $10 billion NAR $5 billion NARPML $25 million $20 million $8 millionCurrent Reserve $500 million $1 million $100 millionMax. Reserve $500 million $5 million $750 million

Handling the Exposure

What might a risk committee think about?• Financial strength (claims-paying) ratings• Collateral• Type of reinsurance• Treaty provisions• Reinsurers’ own diversification by line of

business

Ratings

• An opinion of a (re)insurer’s claims-paying ability

• Generally based on a capital adequacy model adjusted for many factors, including liquidity and profitability

• Not durable – opinion must change as circumstances change

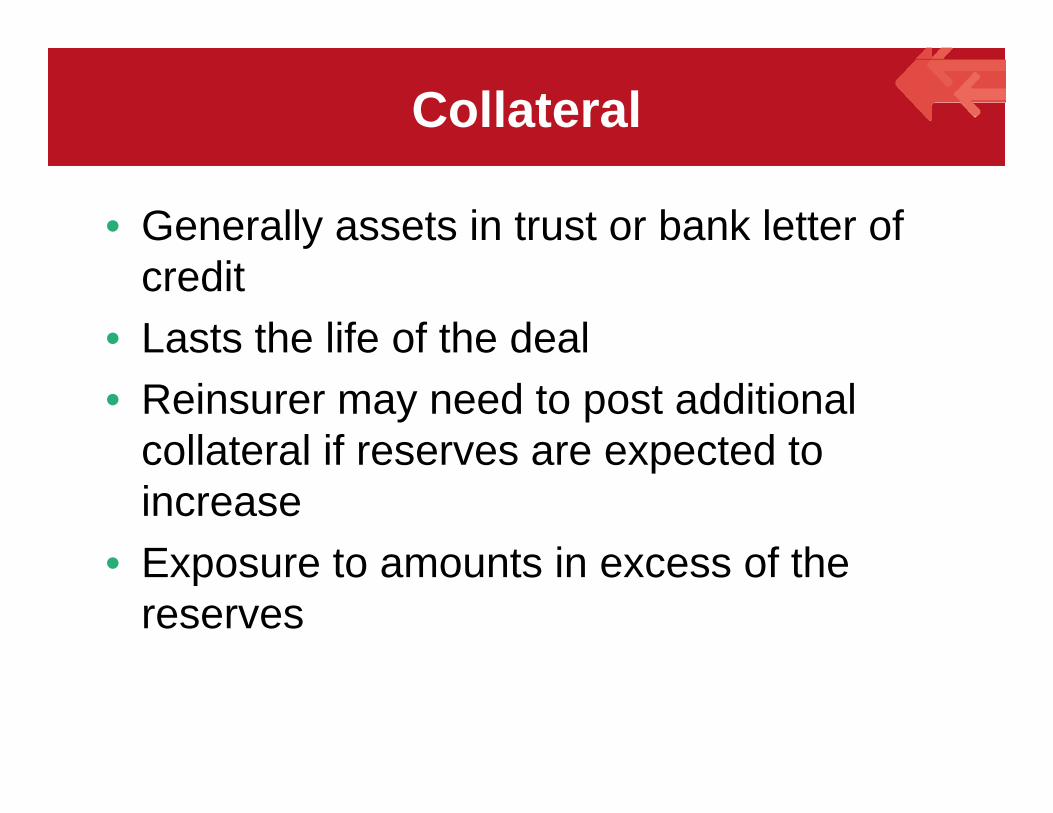

Collateral

• Generally assets in trust or bank letter of credit

• Lasts the life of the deal• Reinsurer may need to post additional

collateral if reserves are expected to increase

• Exposure to amounts in excess of the reserves

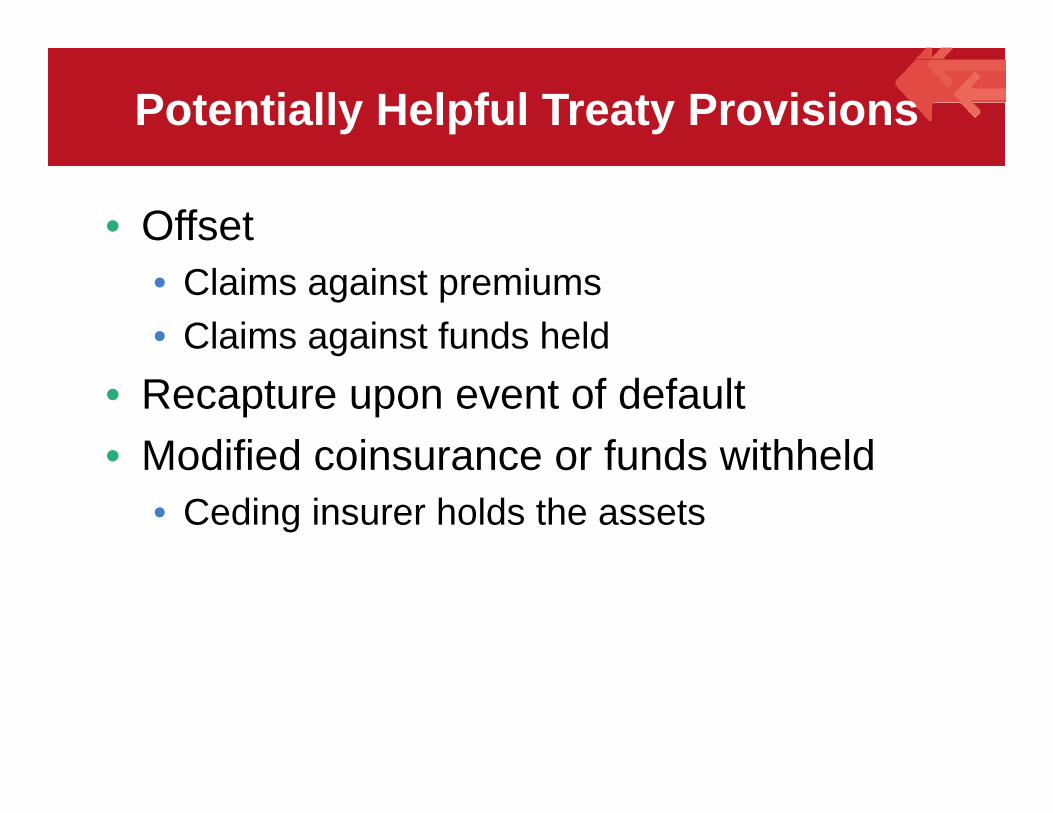

Potentially Helpful Treaty Provisions

• Offset• Claims against premiums• Claims against funds held

• Recapture upon event of default• Modified coinsurance or funds withheld

• Ceding insurer holds the assets

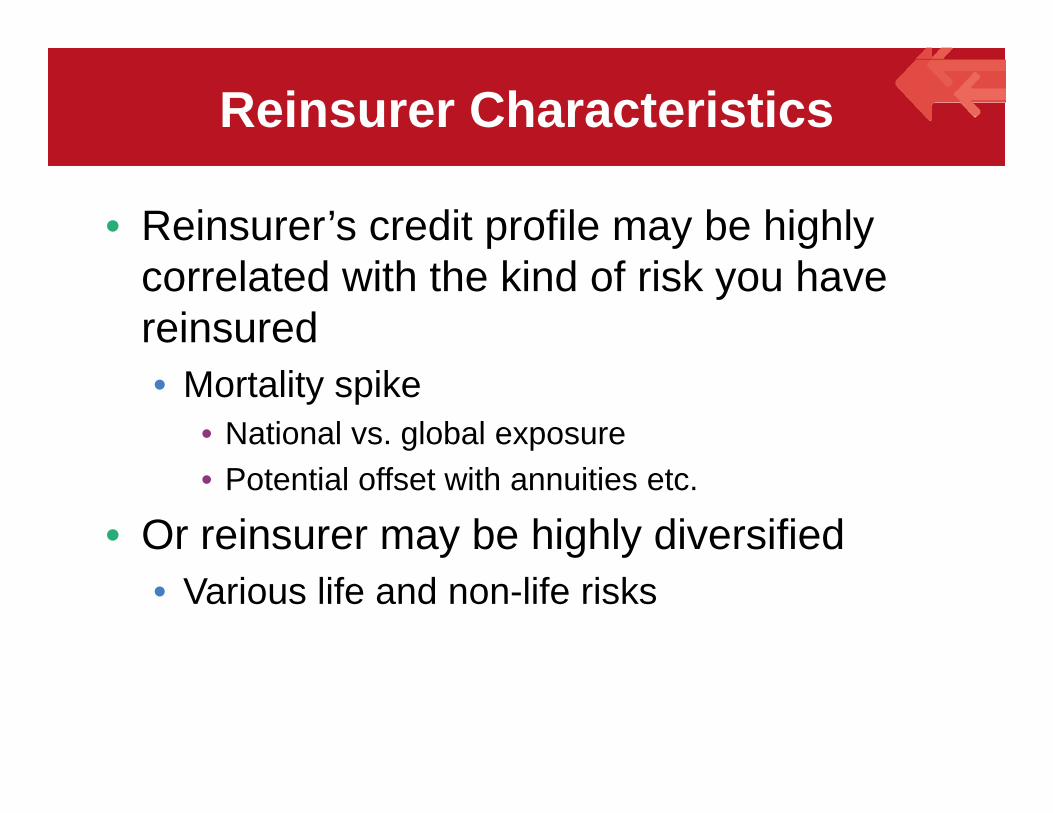

Reinsurer Characteristics

• Reinsurer’s credit profile may be highly correlated with the kind of risk you have reinsured• Mortality spike

• National vs. global exposure• Potential offset with annuities etc.

• Or reinsurer may be highly diversified• Various life and non-life risks