chapter 23 international asset pricing

DESCRIPTION

Chapter 23 International Asset Pricing. 23.1The Traditional Capital Asset Pricing Model (CAPM) 23.2The International Asset Pricing Model (IAPM) 23.3Roll’s Critique 23.4Factor Models and Arbitrage Pricing Theory (APT) 23.5Applications of Arbitrage Pricing Theory - PowerPoint PPT PresentationTRANSCRIPT

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-1

Chapter 23Chapter 23International Asset PricingInternational Asset Pricing

23.1 The Traditional Capital Asset Pricing Model (CAPM)

23.2 The International Asset Pricing Model (IAPM)

23.3 Roll’s Critique

23.4 Factor Models and Arbitrage Pricing Theory (APT)

23.5 Applications of Arbitrage Pricing Theory

23.6 The Currency Risk Factor in Stock Returns

23.7 Currency Risk Exposure

and MNC Hedging Activities

23.8 Summary

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-2

On asset pricing and market efficiency...On asset pricing and market efficiency...

It is the theory that decides

what can be observed.

Albert Einstein

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-3

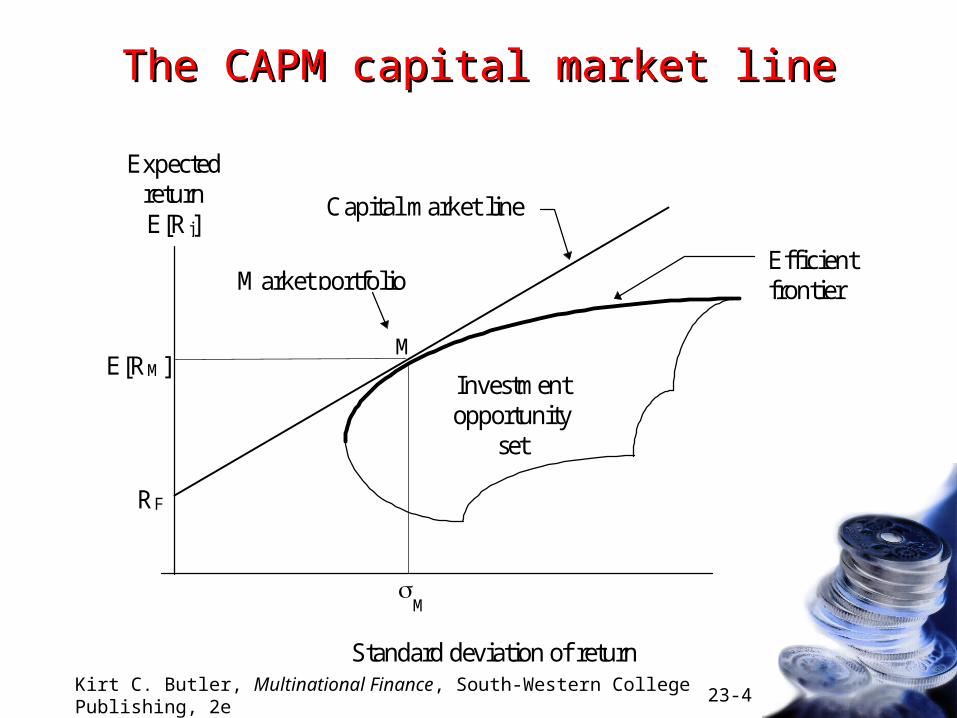

The traditional capital asset pricing model The traditional capital asset pricing model (CAPM)(CAPM)

Perfect financial markets

» Frictionless markets

» Rational investors have equal access to costless information and market prices

Homogeneous expectations Everyone can borrow and lend at the riskless

rate of interest RF

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-4

The CAPM capital market lineThe CAPM capital market line

Capital market line

Investmentopportunity

set

Efficientfrontier

ExpectedreturnE[Rj]

Standard deviation of return

RF

E[RM]

M

M

Market portfolio

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-5

The CAPM security market lineThe CAPM security market line

RF

M

1.0

Ri = RF + i (E[RM] - RF)

Security market line

E[RM]

0

ExpectedreturnE[Ri]

Systematic risk (beta i)

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-6

The International Asset Pricing Model (IAPM)The International Asset Pricing Model (IAPM)

In addition to the CAPM assumptions, suppose– Investors in each country have the same consumption

basket

– Purchasing power parity holds

This leads to an international version of the CAPM

The market portfolio includes all assets in the world weighted according to their market values

Investors also hold a hedge portfolio of domestic and foreign bonds» as a store of value (that is, as a riskfree asset)

» to hedge the currency risk of the market portfolio

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-7

Integrated vs segmented capital marketsIntegrated vs segmented capital markets

Integrated financial marketsThere are no barriers to financial flows and purchasing power parity holds across equivalent assets wherever they are traded.

Segmented financial marketsPrices are set independently in each national market.

Real-world financial markets fall somewhere between these two extremes.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-8

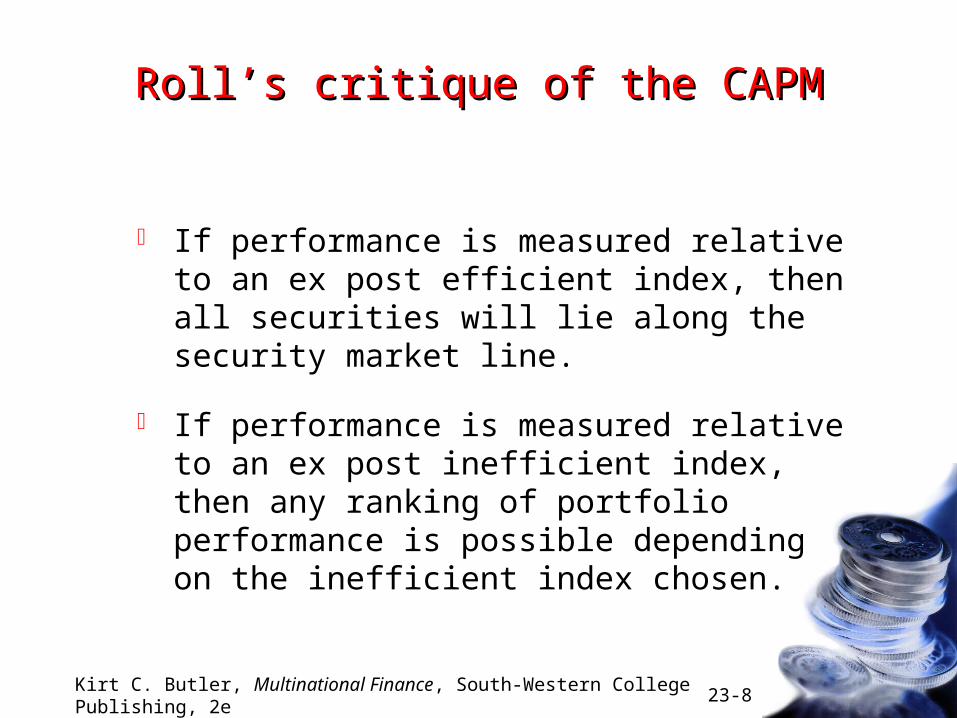

Roll’s critique of the CAPMRoll’s critique of the CAPM

If performance is measured relative to an ex post efficient index, then all securities will lie along the security market line.

If performance is measured relative to an ex post inefficient index, then any ranking of portfolio performance is possible depending on the inefficient index chosen.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-9

Roll’s critique of the CAPMRoll’s critique of the CAPM

Because of home asset bias, investors do not hold the world market portfolio.

Consequently, market beta may be of little use in measuring risk in a globally diversified portfolio.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-10

Arbitrage pricing theory (APT)Arbitrage pricing theory (APT)

Rj = j + 1jF1 + ... + KjFK + ej

(23.5)

where Rj = the random rate of return on asset j

j = the mean or expected return on asset j

kj = the sensitivity of asset j to factor k where k=1,...,K

Fk = systematic risk factor k

ej = a random error term

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-11

The one-factor market modelThe one-factor market model

One-factor market model

Rj = j + jRM + ej (23.6)

Subtracting asset j’s mean return j = j + j M from both sides of (23.6) yields a one-factor market model in excess return form.

Rj = j + jFM + ej (23.7)

where FM = (RM - M)

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-12

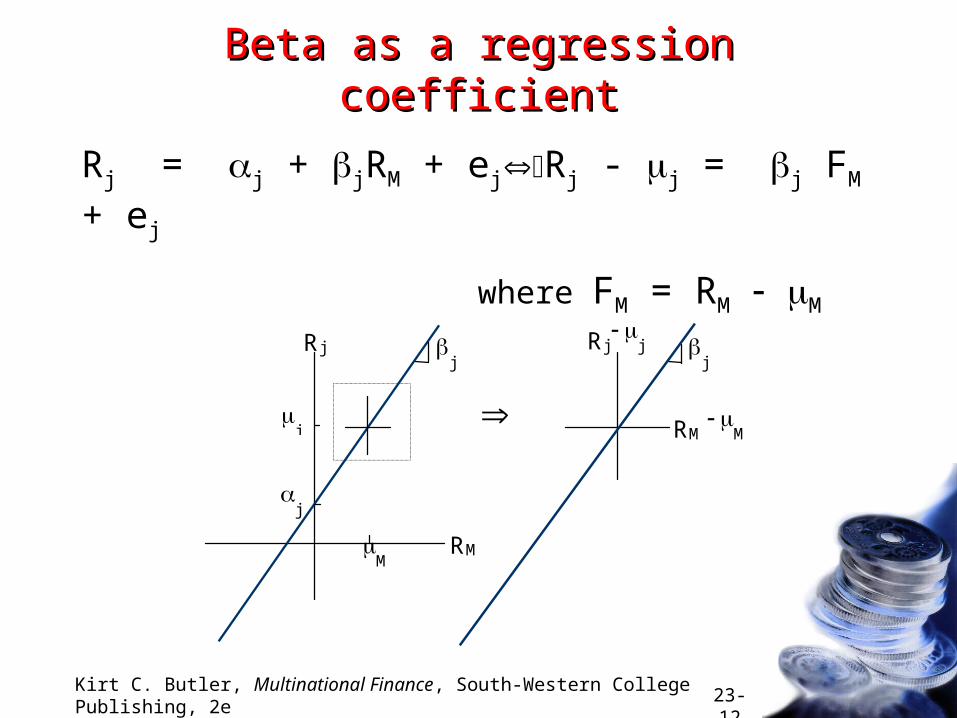

Beta as a regression coefficientBeta as a regression coefficient

Rj = j + jRM + ejRj - j = j FM + ej

where FM = RM M

RM

Rj

RM

M

j

M

j

j

Rj

j

j

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-13

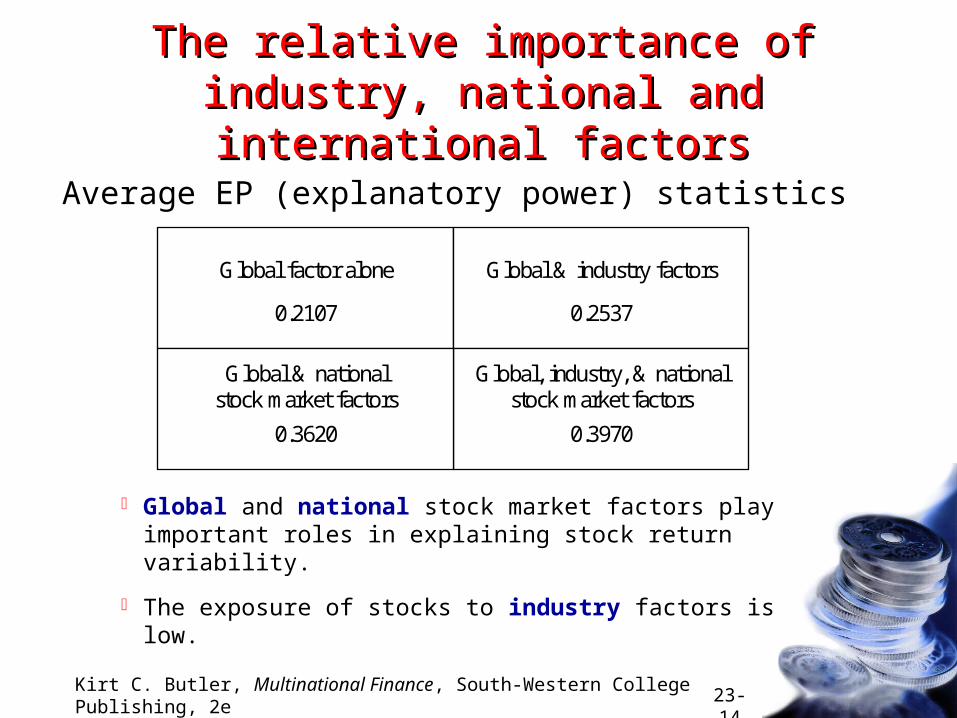

The relative importance of industry, national The relative importance of industry, national and international factorsand international factors

Rj = M + CjFCj + IjFIj + ej (23.9)

where Rj = local currency excess return to stock j

M = return to the global market factor

FCj = return to stock j’s country factor

and FIj = return to stock j’s industry factor

Beckers, Connor and Curds, “National versus Global Influences on Equity Returns,” Financial Analysts Journal 52, March/April 1996.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-14

The relative importance of industry, The relative importance of industry, national and international factorsnational and international factors

Global factor alone

0.2107

Global & industry factors

0.2537

Global, industry, & nationalstock market factors

0.3970

Global & nationalstock market factors

0.3620

Average EP (explanatory power) statistics

Global and national stock market factors play important roles in explaining stock return variability.

The exposure of stocks to industry factors is low.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-15

Exposure to currency riskExposure to currency risk

Rd = d + f sd/f + ed

Rd

sd/f

ExportersImporters

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-16

The diversifiability of currency risk exposureThe diversifiability of currency risk exposure

U.S. exporter’s Swiss importer’s Risk profile risk profile risk profile of combined position

V$/SFr V$/SFr V$/SFr

S$/SFr S$/SFr S$/SFr

SFr100,000 SFr100,000

SFr100,000 SFr100,000

+ =

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-17

APT factorsAPT factors

Chen, Roll and Ross identify five APT factors:*

Rj = j + 1jF1 + 2jF2 + 3jF3 + 4jF4 + 5jF5 +ej

Fj: industrial production

F2: risk premia (corporate government bond yield)

F3: term premia (long-term government T-bill yield)

F4: expected inflation

F5: unexpected inflation

When the market return is included as a sixth factor, its coefficient is not significant.

* Nai-Fu Chen, Richard Roll, and Stephen A. Ross, “Economic Forces

and the Stock Market,” Journal of Business, July 1986.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-18

Does currency risk matter in U.S. markets?Does currency risk matter in U.S. markets?

Jorion added a currency risk factor to the one-factor market model and the five-factor model of Chen, Roll and Ross?*

Rjd = j

d + 1j (RMd M

d) + 2jf sd/f + ej

d (23.13)

Rjd = j

d + 1jF1d + 2jF12

d + ... + 5jF5d + 6j

fsd/f + ejd (23.14)

» In actively traded U.S. markets, the currency risk factor

is subsumed into the other factors.

» Nevertheless, there is considerable cross-sectional

variation among U.S.-based MNCs.

* Philippe Jorion, “The Pricing of Exchange Rate Risk in the Stock Market,”

Journal of Financial and Quantitative Analysis, September 1991.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-19

Does currency risk matter in non-U.S. markets?Does currency risk matter in non-U.S. markets?

De Santis and Gérard estimated a conditional version of a two-factor (market and currency risk) model.*

– Conditional asset pricing models allow risks (ie., currency and market risks) to vary over time.

– Different national markets had different exposures to currency risks.

» Currency risk was a small fraction of total risk in the United States

» Currency risk was a significant percentage of total risk in Germany, Japan, and the United Kingdom

* Giorgio De Santis and Bruno Gérard, “How Big is the Premium for

Currency Risk,” Journal of Financial Economics 49, September 1998.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-20

The value premium and the size effectThe value premium and the size effect

Fama and French fit a three-factor model:*

Rj = j + j (RM - M) + Zj FSize + Dj FDistress + ej

» Market factor (RM-M) = excess return on the market

» Firm size FSize = the difference in mean return between

the smallest 10% and the largest 10% of firms.

» Relative financial distress FDistress = the difference in

mean return between value stocks (high equity book-to-market ratios) and growth stocks (low equity book-to-market ratios)

* Eugene F. Fama and Kenneth R. French, “The Cross-Section of Expected Stock Returns,” Journal of Finance, June 1992.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-21

The value premium and the size effectThe value premium and the size effect

Firm size: Small firms outperformed large firms by an average of 7 percent per year.

Relative financial distress: Value stocks (high equity book-to-market stocks) outperformed growth stocks by an average of 12 percent per year.

After controlling for size and relative financial distress, the market factor contributed nothing to the explanatory power of the regression.

* Eugene F. Fama and Kenneth R. French, “The Cross-Section of Expected Stock Returns,” Journal of Finance, June 1992.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-22

The value premium in U.S. stocksThe value premium in U.S. stocks

0%

5%

10%

15%

20%

25%

1 2 3 4 5 6 7 8 9 10

Annualized return

Portfolios ranked on book-to-market equity

High Low

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-23

The international value premiumThe international value premium

Fama and French then extended their study to international stocks:*

» Value (low MV/BV) stocks have higher mean returns than growth (high MV/BV) stocks in 12 of 13 international markets.

» The difference in mean return is 7.60% per year.

* Eugene F. Fama and Kenneth R. French, “Value versus Growth: The International Evidence,” Journal of Finance 53 (December 1998).

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-24

The international value premiumThe international value premium

The Difference in Annual Dollar Returns in Excess of the U.S. T-Bill Rate for Value and Growth Stock Portfolios

-10%

-5%

0%

5%

10%

15%A

ustr

alia

Bel

gium

Fra

nce

Ger

man

y

Hon

g K

ong

Ital

y

Japa

n

Net

herl

ands

Sin

gapo

re

Sw

eden

Sw

itze

rlan

d

Uni

ted

Kin

gdom

Uni

ted

Sta

tes

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-25

Momentum strategiesMomentum strategies

Momentum (or relative strength) strategies selectively buy or sell securities based on their recent price performance.

Jegadeesh and Titman categorized stocks into ten equal-sized portfolios according to return over the preceding six months.*

» Winners are stocks with the highest six-month returns

» Losers are stocks with the highest six-month returns

* Narasimhan Jegadeesh and Sheridan Titman, “Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency,” Journal of Finance, March 1993.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-26

Momentum in U.S. stocksMomentum in U.S. stocks

United States+1.0%

12

Months relative to portfolio formation

0.0%

-1.0%

24 36

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-27

Momentum in international stocksMomentum in international stocks

Rouwenhorst examined momentum in 12 European stock markets:*

» Past Winners outperformed Losers by more than 1 percent per month after correcting for risk.

» Return continuation lasts for about one year, and then is partially reversed.

* K. Geert Rouwenhorst, “International Momentum Strategies,” Journal of Finance, February 1998.

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-28

Momentum in international stocksMomentum in international stocks(monthly returns to Winner-minus-Loser portfolios)(monthly returns to Winner-minus-Loser portfolios)

Europe+1.0%

12

Months relative to portfolio formation

0.0%

-1.0%

24

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-29

International momentumInternational momentum(cumulative returns to Winner-minus-Loser portfolios)(cumulative returns to Winner-minus-Loser portfolios)

-5%

0%

5%

10%

15%

0 12 24 36

Months relative to portfolio formation

EuropeUnited States

Kirt C. Butler, Multinational Finance, South-Western College Publishing, 2e 23-30

Momentum in international stocksMomentum in international stocks(average monthly returns to Winner-minus-Loser portfolios)(average monthly returns to Winner-minus-Loser portfolios)

0.0%

0.5%

1.0%

1.5%

Au

stria

Be

lgiu

m

De

nm

ark

Fra

nce

Ge

rma

ny

Ita

ly

Ne

the

rlan

ds

No

rwa

y

Sp

ain

Sw

ed

en

Sw

itze

rlan

d

Un

ited

Kin

gd

om