chapter 18 auditors reports association with financial414

TRANSCRIPT

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 1/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 2/38

ASSOCIATION WITH

FINANCIAL STATEMENTS

• An accountant (auditor) is associated with the financial

statements of an entity when he/she has:

– consented to the use of his/her name in a report,

document, or written communication containing the

financial statements, or

– submitted to his/her client or to others financial

statements that he/she has prepared or assisted in

preparing.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 3/38

ASSOCIATION WITH

FINANCIAL STATEMENTS

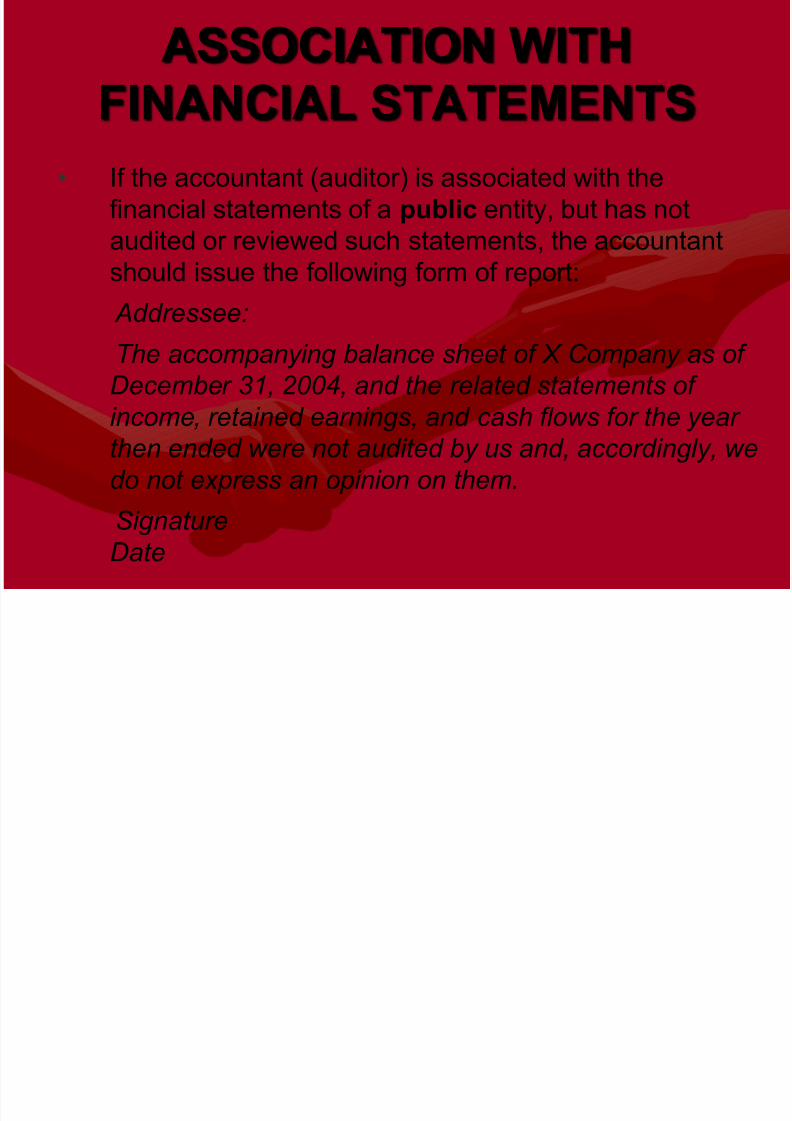

• If the accountant (auditor) is associated with the

financial statements of a public entity, but has not

audited or reviewed such statements, the accountant

should issue the following form of report: Addressee:

The accompanying balance sheet of X Company as of

December 31, 2004, and the related statements of

income, retained earnings, and cash flows for the yearthen ended were not audited by us and, accordingly, we

do not express an opinion on them.

Signature

Date

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 4/38

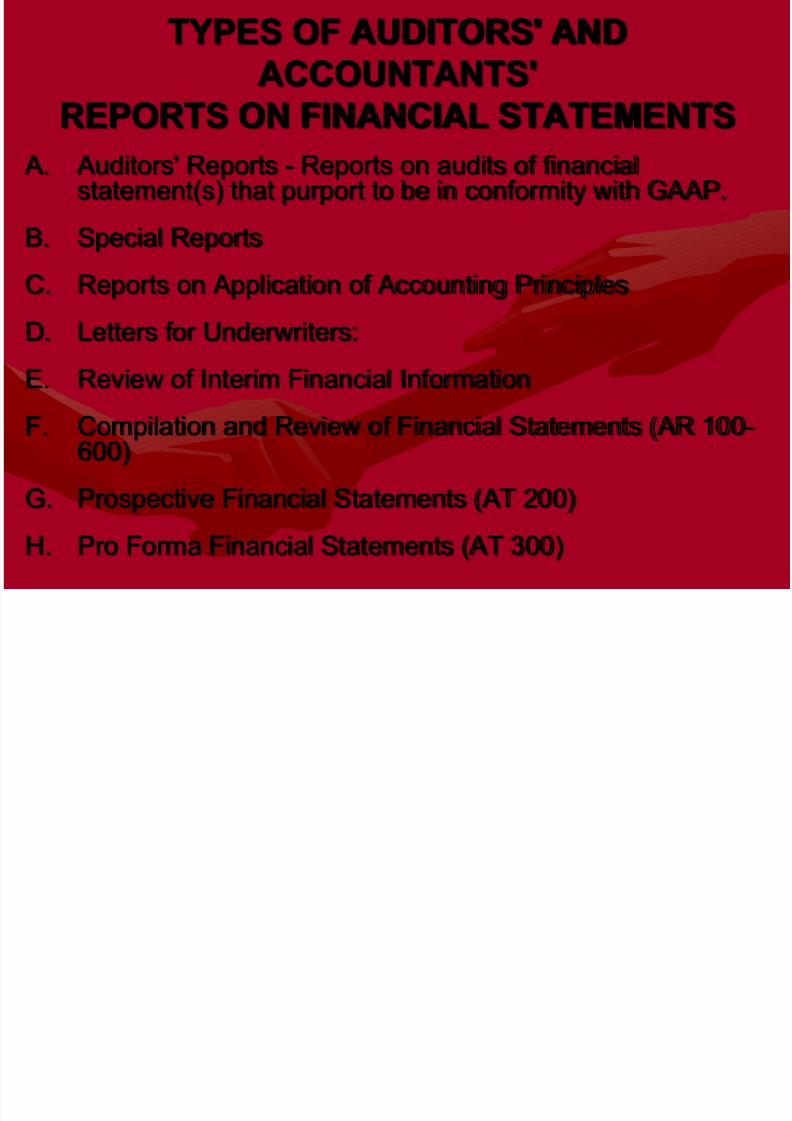

TYPES OF AUDITORS' AND

ACCOUNTANTS'

REPORTS ON FINANCIAL STATEMENTS

A. Auditors' Reports - Reports on audits of financialstatement(s) that purport to be in conformity with GAAP.

B. Special Reports

C. Reports on Application of Accounting Principles

D. Letters for Underwriters:

E. Review of Interim Financial Information

F. Compilation and Review of Financial Statements (AR 100-600)

G. Prospective Financial Statements (AT 200)

H. Pro Forma Financial Statements (AT 300)

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 5/38

TYPES OF AUDITORS' AND

ACCOUNTANTS'

REPORTS ON FINANCIAL STATEMENTS

I. Reports on the audit of a governmental entity’sfinancial statements performed in accordance with

one or more of the following: Generally Accepted Auditing Standards (GAAS)

Governmental Auditing Standards (GAS)

Single Audit Act of 1984

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 6/38

Types of Auditor Reports &

Opinions (see Table 1)

• Unqualified Opinion

– Standard report

– Report with explanatory language added that does not

affect the auditor’s unqualified opinion

• Qualified Opinion (sometimes called an Except for

Qualified Opinion):

– Material departure from GAAP (including inadequate

disclosure)

– Significant scope limitation.

• Adverse Opinion – Material departure from GAAP

• Disclaimer of Opinion Significant scope limitation

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 7/38

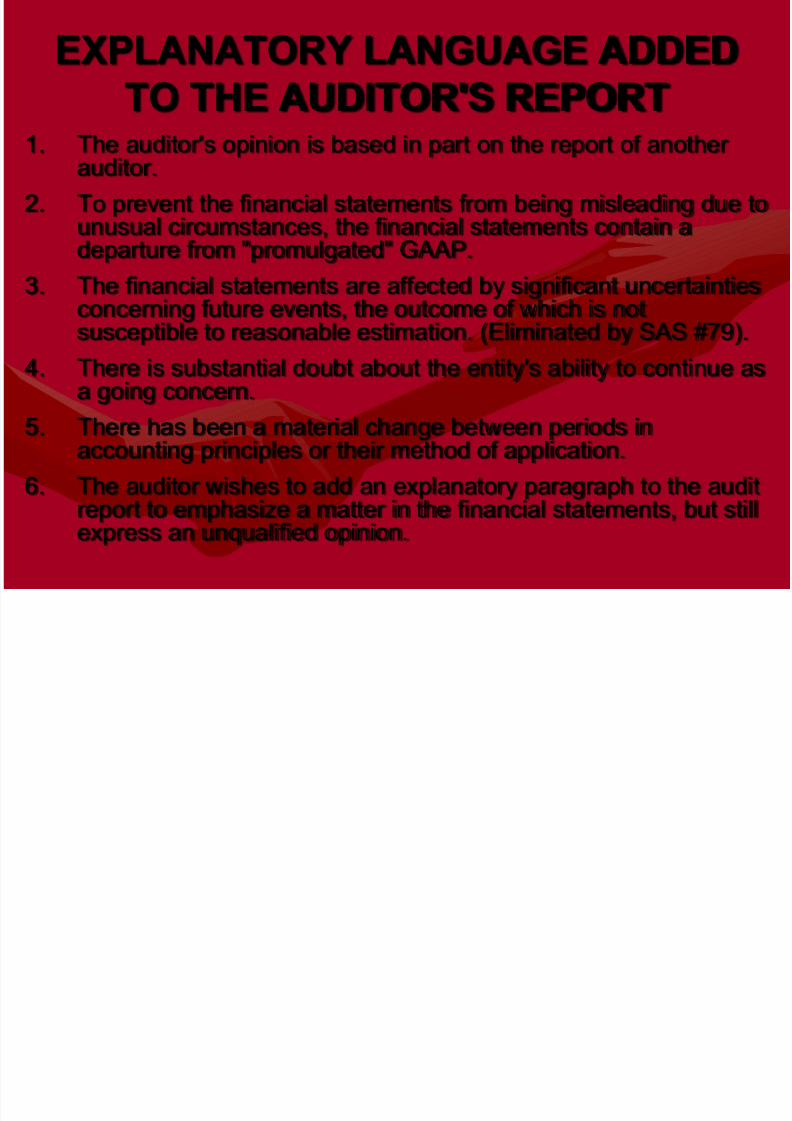

EXPLANATORY LANGUAGE ADDED

TO THE AUDITOR'S REPORT1. The auditor's opinion is based in part on the report of another

auditor.

2. To prevent the financial statements from being misleading due tounusual circumstances, the financial statements contain adeparture from "promulgated" GAAP.

3. The financial statements are affected by significant uncertaintiesconcerning future events, the outcome of which is notsusceptible to reasonable estimation. (Eliminated by SAS #79).

4. There is substantial doubt about the entity's ability to continue asa going concern.

5. There has been a material change between periods inaccounting principles or their method of application.

6. The auditor wishes to add an explanatory paragraph to the auditreport to emphasize a matter in the financial statements, but stillexpress an unqualified opinion.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 8/38

EXPLANATORY LANGUAGE ADDED

TO THE AUDITOR'S REPORT7. Certain circumstances relating to reports on comparative

financial statements exist.

8. Selected quarterly financial data required by SEC Regulation S-Khave been omitted or have not been reviewed.

9. Supplementary information required by the FASB or the GASB:

– Supplementary information has been omitted from the financialstatements, or

– Presentation of such information departs materially from FASB orGASB guidelines, or

– Auditor is unable to complete prescribed procedures with respect to

such information, or – Auditor is unable to remove substantial doubts about whether the

supplementary information conforms to FASB or GASB guidelines,or

– Other information in a document containing audited financialstatements is materially inconsistent with information appearing in

the financial statements.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 9/38

AUDITOR'S OPINION IS BASED IN

PART ON THE REPORT OF

ANOTHER AUDITOR• When a principal auditor decides to make reference to the

report of another auditor, he/she should:

– disclose this fact in the introductory paragraph of his or

her report by indicating the dollar amounts, or therelative percentages, of assets and revenues examined

by the other auditors,

– refer to the report of the other auditor in the scope

paragraph by inserting after "We believe that our audit"the phrase "and the report of the other audi tors,".

– refer to the report of the other auditor in the opinion

paragraph by inserting after "In our opinion," the phrase

"based on our audi t(s) and the report of the other

audi tors,".

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 10/38

Example of a Report Indicating

Division of Responsibility

Report of Independent Registered Public Accounting Firm

To the Board of Directors

of X Company

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 11/38

Example of a Report Indicating

Division of Responsibility - Intro

We have audited the accompanying balance sheets of XCompany as of December 31, 2004 and 2003, and the relatedstatements of income, shareholders’ equity, and cash flows foreach of the two years in the period ended December 31, 2004.

These financial statements are the responsibility of theCompany's management. Our responsibility is to express anopinion on these financial statements based on our audits. Wedid not audi t the f inancial statements o f B Company, awhol ly ow ned subsid iary, which statements ref lect tota lassets o f $______ and $_______ as of December 31, 2004

and 2003, respectively, and total revenues of $_______ and$_______ for the years then ended. Those statements wereaudi ted b y o ther audi tors whose report has been furn ishedto us, and ou r op inion , inso far as i t relates to the amountsinc luded for B Company, is based sole ly on the reports ofthe other audi tors .

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 12/38

Example of a Report Indicating

Division of Responsibility - Scope

We conducted our audits in accordance with the standardsof the Public Company Accounting Oversight Board (UnitedStates). Those standards require that we plan and perform

an audit to obtain reasonable assurance about whether thefinancial statements are free of material misstatement. Anaudit includes examining, on a test basis, evidencesupporting the amounts and disclosures in the financialstatements. An audit also includes assessing the

accounting principles used and significant estimates madeby management, as well as evaluating the overall financialstatement presentation. We believe that our audits and therepo rts of th e other aud i tor provide a reasonable basisfor our opinion.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 13/38

Example of a Report Indicating

Division of Responsibility - Opinion

In our opinion, based on our audi ts and thereports o f the other aud i tors, the financialstatements referred to above present fairly, in all

material respects, the financial position of XCompany as of December 31, 2004 and 2003, andthe results of operations and its cash flows foreach of the two years in the period endedDecember 31, 2004, in conformity with U.S.generally accepted accounting principles.

SignatureCity and State or Country)Date

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 14/38

TO PREVENT THE FINANCIAL STATEMENTS

FROM BEING MISLEADING DUE TO UNUSUAL

CIRCUMSTANCES, THE FINANCIAL

STATEMENTS CONTAIN A DEPARTURE FROM"PROMULGATED" GAAP

A. Management and the auditor must be able to

justify that, due to unusual circumstances,adherence to "promulgated" GAAP would bemisleading.

B. Though the auditor's report contains a departurefrom the standard report, the opinion expressedby the auditor is an unqualified opinion.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 15/38

TO PREVENT THE FINANCIAL STATEMENTS

FROM BEING MISLEADING DUE TO UNUSUAL

CIRCUMSTANCES, THE FINANCIAL

STATEMENTS CONTAIN A DEPARTURE FROM"PROMULGATED" GAAP

C. The auditor's report should include, in a separate

explanatory paragraph, in which the auditor describes the1. departure,

2. approximate effects, if practicable, and

3. reasons why compliance with promulgated GAAP wouldbe misleading.

D. The separate explanatory paragraph should precede theopinion paragraph.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 16/38

THERE IS SUBSTANTIAL DOUBT ABOUT

AN ENTITY'S ABILITY TO CONTINUE AS

A GOING CONCERN A. The following are audit procedures that may identify a going

concern problem:

1. Analytical procedures.

2. Review of subsequent events.3. Review of compliance with the terms of debt and loan

agreements.

4. Reading minutes of meetings of stockholders, board of

directors, and important committees of the board.

5. Inquiry of a client's legal counsel about litigation, claims,

and assessments.

6. Confirmation with related and third parties of the details

of arrangements to provide or maintain financial support.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 17/38

B. Conditions or Events That Could Cast SubstantialDoubt on a Client's Ability to Continue as a GoingConcern for a Reasonable Period of Time

1. Negativ e trends – such as operating losses,working capital deficiencies, negative cash flows,adverse key financial ratios

2. Other ind icat ions o f poss ib le f inanc iald i f f icu l t ies – such as default on bonds or loans,

denial of normal trade credit from suppliers,restructuring of debt, noncompliance with statutorycapital requirements

3. In ternal matters that have occurred such as workstoppages

4. Ex ternal matters that have occur red such aslitigations; loss of a key franchise, license or patent;loss of a principal customer; uninsured catastrophessuch as drought, flood, or earthquake.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 18/38

C. If the auditor concludes that there is substantial doubt

about the client's ability to continue as a going concern

for a reasonable period o f t ime , the auditor should

evaluate management’s plans to mitigate the effects ofthe adverse conditions or events. The following are

examples of mitigating factors:

1. Sale of assets

2. Reduction or postponement of discretionary

expenditures, such as expenditures for research and

development

3. Restructuring of existing debt4. Issuance of new debt

5. Issuance of capital stock

6. Reduce or eliminate dividends on common or

preferred stock

D If th dit l d th t th i b t ti l d bt b t

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 19/38

D. If the auditor concludes that there is substantial doubt aboutthe client's ability to continue as a going concern for areasonable period of time and the mitigating factors are notsufficient to remedy the substantial doubt, the auditor

should include an explanatory paragraph such as thefollowing in the report.

The accompanying financial statements have been prepared assuming that the X Company will continue as a

going concern. As discussed in Note X to the financialstatements, the X Company has suffered recurring lossesfrom operations and has a net capital deficiency that raisesubstantial doubts about its ability to continue as a goingconcern. Management's plans in regard to these matters

are also described in Note X. The financial statements donot include any adjustments that might result from theoutcome of this uncertainty .

E. The explanatory paragraph should follow the opinion

paragraph

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 20/38

There Has Been a Material Change Between

Periods in Accounting Principles or in Their

Method of Application

A. The auditor's standard report implies that the

auditor is satisfied that:1. The comparability of financial statements

between periods has not been materially

affected by changes in accounting principles,

and2. Such principles have been consistently

applied between or among periods.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 21/38

B. If (a) there has been a change in accounting principles or in themethod of their application that has a material affect on thecomparability of the client's financial statements and (b) ifmanagement has provided proper justification for the change, thenthe auditor would refer to the change in an explanatory paragraph inhis or her report.

1. The explanatory paragraph should follow the opinion paragraph.

2. The explanatory paragraph should identify the nature of thechange and refer the reader to the note in the financialstatements that discusses the change in detail.

3. The auditor's concurrence with the change is implicit unless he orshe takes exception to the change in expressing his or heropinion as to fair presentation of the financial statements.

4. The explanatory paragraph should be included in reports on thefinancial statements of subsequent years as long as the financialstatements for the year of the change is presented on a

comparative basis with the financial statements of subsequentyears.

5. The only exception to Part 4 above is when the change isaccounted for by retroactive restatement of the financialstatements affected. In this case, the explanatory paragraph isrequired only in the year of the change.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 22/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 23/38

E. If management is not able to provide reasonable

justification for the change, then the auditor would not

follow the guidance above. Instead, the auditor would

issue a short-form report that contains either a qualifiedopinion or an adverse opinion.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 24/38

Emphasis of a Matter

A. In certain circumstances, an auditor may wish to add anexplanatory paragraph to the audit report to emphasize a matter

in the financial statements, but still express an unqualifiedopinion.

B. For example, the auditor may wish to emphasize that:

1. The client is a component of a larger business enterprise.

2. The client has had significant transactions with relatedparties.

3. The financial statements disclose a highly materialuncertainty.

4. An unusually important subsequent event or an accounting

matter affects the comparability of the financial statementswith those of a preceding period.

C. Phrases such as "with the foregoing explanation" should notbe included in the opinion paragraph to refer to an explanatoryparagraph that emphasizes a matter.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 25/38

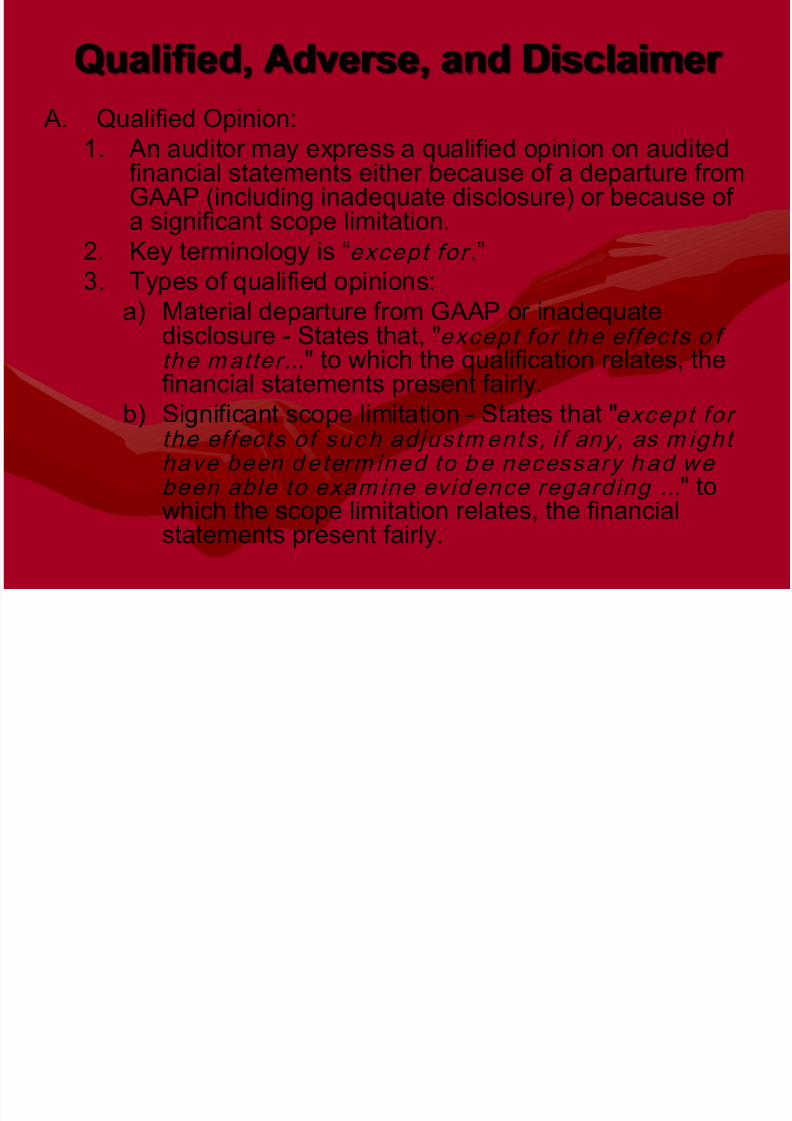

Qualified, Adverse, and Disclaimer

A. Qualified Opinion:

1. An auditor may express a qualified opinion on auditedfinancial statements either because of a departure fromGAAP (including inadequate disclosure) or because ofa significant scope limitation.

2. Key terminology is “except for .”

3. Types of qualified opinions:a) Material departure from GAAP or inadequate

disclosure - States that, "except for the effects o fthe matter..." to which the qualification relates, thefinancial statements present fairly.

b) Significant scope limitation - States that "except forthe effects of such adjustm ents, i f any, as m ighthave been determ ined to be necessary had webeen able to exam ine evidence regarding ..." towhich the scope limitation relates, the financialstatements present fairly.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 26/38

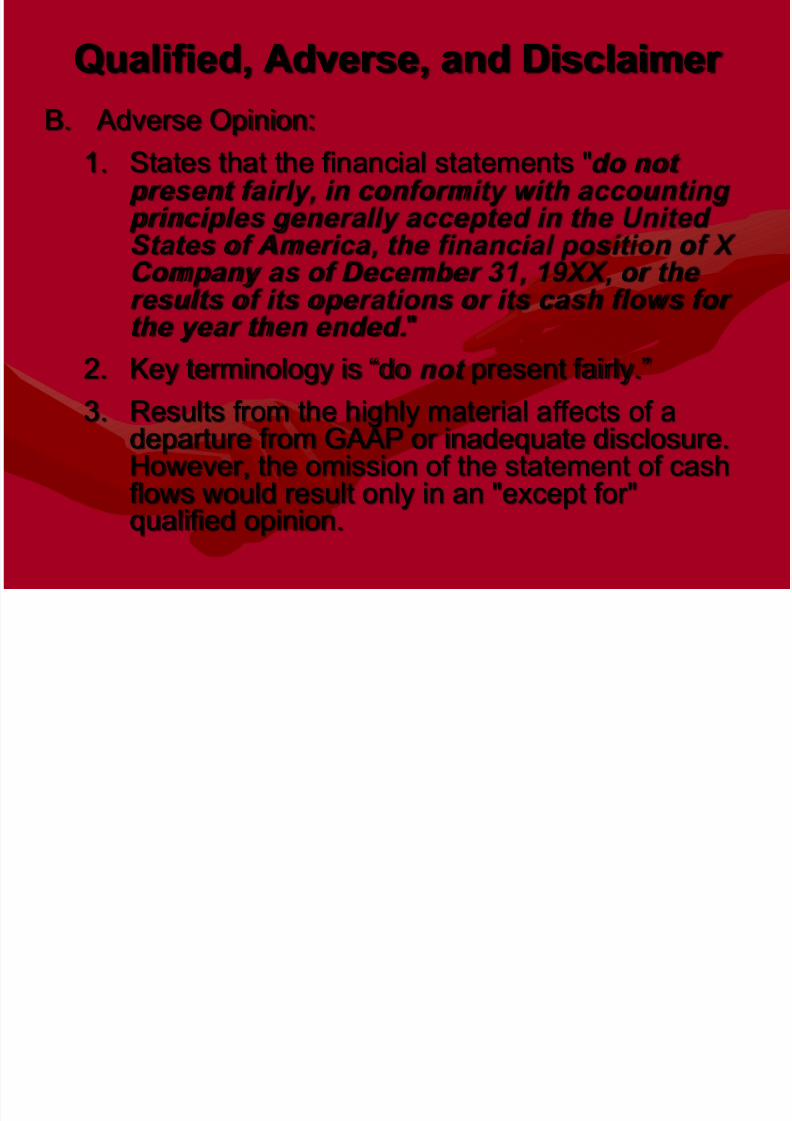

Qualified, Adverse, and Disclaimer

B. Adverse Opinion:

1. States that the financial statements "do notpresent fa ir ly , in conform i ty wi th account ingpr inc ip les general ly accepted in the UnitedStates o f Amer ica, the f inancial pos i t ion o f X

Company as of December 31, 19XX, or theresul ts o f i ts o perat ions o r i ts cash f lows forthe year then ended."

2. Key terminology is “do no t present fairly.”

3. Results from the highly material affects of adeparture from GAAP or inadequate disclosure.However, the omission of the statement of cashflows would result only in an "except for"qualified opinion.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 27/38

Qualified, Adverse, and Disclaimer

C. Disclaimer of Opinion:

1. States that the auditor has not performed anaudit that was "su ff ic ient to enable us toexpress, and we do no t exp ress , anop inion on these f inancial statements

."2. Key terminology is “does not express an

opinion.”

3. Results from a significant scope limitation orlack of independence relative to a publicly-held entity.

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 28/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 29/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 30/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 31/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 32/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 33/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 34/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 35/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 36/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 37/38

8/12/2019 Chapter 18 Auditors Reports Association With Financial414

http://slidepdf.com/reader/full/chapter-18-auditors-reports-association-with-financial414 38/38