fall 2002 - association of college & university auditors

TRANSCRIPT

Officers and DirectorsPRESIDENT

Robert Clark, Jr.Georgia Institute of TechnologyAtlanta, [email protected]

VICE PRESIDENT

Seth KornetskyTufts UniversitySomerville, [email protected]

IMMEDIATE PAST PRESIDENT

J. Michael PeppersUniversity of Texas Medical BranchGalveston, [email protected]

SECRETARY/TREASURER

Patrick ReedUniversity of CaliforniaOakland, [email protected]

BOARD MEMBERS-AT-LARGE

Tina AbdellaOhio UniversityAthens, [email protected]

Mary BarnettUniversity of RichmondRichmond, [email protected]

J. Richard DawsonUniversity of Texas at San AntonioSan Antonio, [email protected]

Nur ErengucUniversity of FloridaGainesville, [email protected]

Seth KornetskyTufts UniversitySomerville, [email protected]

Kim TurnerTexas Tech University SystemLubbock, [email protected]

Standing CommitteesACCOUNTING PRINCIPLES

Frank BossleJohns Hopkins UniversityBaltimore, [email protected]

Rick WhitfieldUniversity of PennsylvaniaPhiladelphia, [email protected]

AUDIT

Randall RossUniversity of North Carolina-CharlotteCharlotte, [email protected]

BEST PRACTICES

Steve JungStanford UniversityStanford, [email protected]

GOVERNMENTAL AFFAIRS

Mary Lee BrownUniversity of PennsylvaniaPhiladelphia, [email protected]

INFORMATION & TECHNOLOGY

Phillip W. HurdGeorgia Institute of TechnologyAtlanta, [email protected]

PROFESSIONAL EDUCATION

Nur Erenguc, ChairUniversity of FloridaGainesville, [email protected]

David P. Coury,Annual Conference DirectorFlorida State UniversityTallahassee, [email protected]

J. Richard Dawson,Regional Program DirectorUniversity of Texas at San Antonio6900 North Loop 1604 WSan Antonio, TX210-458-4237

James Hodge, Midyear Seminar DirectorUniversity of TennesseeKnoxville, [email protected]

PUBLICATIONS

J. Betsy BowersUniversity of West FloridaPensacola, [email protected]

FALL 2002 / 1

VVVVVol. 46, No. 3ol. 46, No. 3ol. 46, No. 3ol. 46, No. 3ol. 46, No. 3 FFFFFALL 2002ALL 2002ALL 2002ALL 2002ALL 2002

Contents

FeaturesPromotion of the Internal Audit Function in Higher Education ........................ 8The Changing Audit Framework for English Universities ................................. 9Internal Audit at the American University of Beirut ....................................... 11ACUA’s Own Serves on Executive Committee of IIA ................................... 13A Comprehensive Approach to Procurement Card Audits ............................. 15Fish Tales ....................................................................................................... 16

The Making of a Star ..................................................................................... 19

DepartmentsFrom the Editor ..................................................................................................2From the President ............................................................................................ 3Letters to the Editor ......................................................................................... 5Report from Headquarters ................................................................................ 6

MembershipMost Excellent Member Award Report .......................................................... 21Reflections on Member Excellence Award ...................................................... 22Member News ................................................................................................ 24New Members ................................................................................................ 242002 Conference Photos ................................................................................ 25

ACUA members are invited to submit letters, origi-nal articles, and notices to the editor. The copydeadline for the next issue is January 21, 2003.Please send your copy electronically to the editorin Word 95 (or higher) or text file format, or mailyour paper or 1.44 high-density floppy disk.

The editor reserves the right to reject, abridge,or modify any advertising, editorial, or other mate-rial. The editor is responsible for editing and proof-reading all material.

EditorJ. Betsy Bowers

University of West Florida(850) 474-2636

Features EditorBetty Favor, [email protected]

Department Editors Association News: Tracy Holter

[email protected] News: Sandra Fischer

Contributing Editors Education: Kathleen Miller

[email protected] Internal Audit: Sterling Roth

[email protected] Association Outreach: Jeff Jarvis

[email protected] Information Exchange: Wendy Lockwood

[email protected] Emerging Issues: Jake Godfrey

[email protected] Past President’s: Ray Cochran

Proofing TeamStacey Bozeman, Auburn UniversityKen Chambers, Florida State University

Virginia Key, Montana State University

For subscription and advertising information,contact Cindy Caron at (860) 586-7561 or [email protected].

ACUA342 North Main Street

West Hartford, CT 06117-2507Phone: (860) 586-7561

Fax: (860) 586-7550

Lorna M. Bolduc, Executive Director

Cynthia Caron, Association Administrator

Corinne C. Hobbs, Design and Layout

Lebon Press, Printing

College & University Auditor is the official publication of the Association of College & UniversityAuditors. It is published three times a year in West Hartford, CT as a benefit of membership. Articles inCollege & University Auditor represent the opinion of the authors and do not necessarily represent theopinion of governance, members, or the staff of the Association of College & University Auditors.Acceptance of advertising does not imply endorsement by ACUA. ©2002 Association of College &University Auditors.

2 / College & University Auditor

Excellence in Higher Education

By J. Betsy Bowers, Editor

From the EDITOR

The skills and techniquesThe skills and techniquesThe skills and techniquesThe skills and techniquesThe skills and techniques

of the internal auditor areof the internal auditor areof the internal auditor areof the internal auditor areof the internal auditor are

always being honed. Walways being honed. Walways being honed. Walways being honed. Walways being honed. Weeeee

never stop learning.never stop learning.never stop learning.never stop learning.never stop learning.

What a rejuvenatingtime I had in SaltLake City atACUA’s AnnualConference. Themany hours of plan-ning and preparationpaid off through stimulating educationalprograms and, of course, the networkingopportunities outside the classroom. (Yes,I hear a few of you chuckling.)

As each year transitions to new lead-ership, you—the member—are chal-lenged to assist in ACUA’s efforts. Ourpresident, Rob Clark, has a campaign toget YOU involved. Please heed closelyhis call to action in his column.

In this issue, we are highlightingACUA’s international influence, whichI hope you will find fascinating, as well aseducational. ACUA’s own BettyMcPhilimy (Northwestern University)being selected to the Institute of InternalAuditors Executive Committee is verynoteworthy. She shares with us her expe-rience traveling on behalf of the IIA toChina in September. Additionally, theinternal audit operations for the UnitedKingdom and Lebanon are awesome.

Excellence in higher education inter-nal auditing is another focus of this issue.Not only do we have the report by theMember Excellence Committee, we also

have articles written by the recipients ofthe award. In addition, we have an inno-vative marketing strategy employed by theUniversity of Texas Tech system that youwill find eye-opening in the “The Mak-ing of a Star” article.

The skills and techniques of the inter-nal auditor are always being honed. Wenever stop learning. Accordingly, this is-sue includes tools and tips for internalauditors: procurement card auditing andpromoting of internal audit.

We work in an industry that thrives onideas; they are important and the centerfocus for colleges and universities. Ideasfor articles and topics enter like the sunpeeking through the trees as a new daydawns. Occasionally, ideas strike us al-most breathless. They prompt us to bestill, to ponder wonderment, to imaginepossibilities and to make personal deci-sions about life or career directions andpaths. Accordingly, it was wonderful toinclude Letters to the Editor in this is-sue. I encourage YOU to write and letthe Publications Committee know whatwe can do to improve the CandU Audi-tor journal, as well as any ideas/leads youmay have for articles. Your participationwill help ACUA and your colleagues growpersonally and professionally. Who knowswhat “ah-ha” moments you could provideto a fellow ACUA member.

Hopefully, the Fall term began with abang at your schools. Some may be un-der new leadership, some may be facingbudgetary or enrollment challenges andothers may be maintaining the status quo.Whatever your situation, I hope you arebeing instrumental in making a differenceon your campus and being of service tothe institution.

ACUA EventsSave the Dates!

2003 Midyear SeminarApril 6-9Austin, TX

2003 Annual ConferenceSeptember 14-18Nashville, TN

2004 Midyear SeminarMarch 14-17Albuquerque, NM

2004 Annual ConferenceSeptember 19-23Arlington, VA

FALL 2002 / 3

Our Profession Is at a Crossroads

By Rob Clark, President

From the PRESIDENT

“Salt Lake City –from the Cross-roads to the Sum-mit” was the themeof our 2002 annualconference. Thoseof us who attendedfound just how ap-propriate that was.Salt Lake City isknown by many asthe “Crossroads tothe West.” As far as“summit,” one onlyneeded to step out-side the hotel, lookup and have the breath taken away at thebeautiful vistas afforded by the summitsof the Rocky Mountains.

The theme, I believe, was appropriatefor many more reasons. As I offered inmy remarks after receiving the president’sgavel from Mike Peppers, I believe ourprofession is indeed at a crossroads. Isthere one of us not faced with mountingfinancial constraints at our universities?Who among us is not being tested to stayabreast of the ever-increasing landscapeof risks facing our organizations? Aren’twe all striving to continually add value atour institutions in a manner that is bestserving our auditing committees and se-nior management?

There could be little argument that thisis a different world in which we find our-

selves auditing thanten, even five,years ago. “SameAs Last Year”might be acceptableas a tick-mark onour work papers,but it is likely to beless enthusiasticallyaccepted by our au-diting committeesand senior manage-ment as our phi-losophy on an over-all audit approach.Having a clear vi-

sion of how we should position ourselvesin the future is going to be key to ourcontinued success.

I’m pleased to say that the ACUAboard is keenly aware of this principle.The board has spent time reexamining thestrategic plan and revalidating the initia-tives. We have studied what has workedwell over the past year, what has not, andwhat needs to be done to revitalize im-portant projects. Through all of our dis-cussions, the consensus was that the stra-tegic direction of ACUA was still on tar-get. We are convinced that the plan, ifmet, will enable the association to makemarked progress toward increasing valu-able services to ACUA members.

We also emerged from our recent dis-cussions with the recognition that the plans

will be successfully carried out only if weapply sufficient resources. In some casesthe resources needed are funds to sup-port the initiatives. In most cases, how-ever, the necessary resources are purelythe increased volunteer efforts of ourmembers.

We are committed to managing the ex-isting revenues so that our current duesand conference fees will remain the samethis year. What we are hoping to do, how-ever, is increase the other assets — ourmembers’ collective expertise.

During the latter part of the businessmeeting, ACUA members had the op-portunity to visit with those overseeingmany of our strategic initiatives. Thoseheading up strategic plan components andour committee chairs were stationedaround the room so that members couldspeak directly with them. They were thereto answer questions and provide moreinformation about what the initiativesentailed. Members had an opportunity toindicate an interest in finding out howthey might be able to get more involvedin supporting these areas.

I was encouraged to see so many sign-ing up, not necessarily making a commit-ment to a pre-determined level of involve-ment, but rather, simply making the state-ment, “Yes, this is my association, myprofession, and I am willing to step for-ward to at least find out how I might beable to further support ACUA.”

Continued on page 4

4 / College & University Auditor

The areas represented were the fivestrategic initiatives plus other operationalareas.

Strategic Plan Areas:• Education

• Information Exchange

• Promotion of the Internal Audit func-tion in higher education

• Emerging Issues

• Association Outreach

Other Operational Areas:• Best Practices Committee

• Information Technology Committee

• Publications Committee (the Collegeand University Auditor)

• Professional Education Committee(Midyear and Annual conferences)

• Government Affairs Committee

• Accounting Principles Committee

• Audit Committee (for ACUA)

• Web site: www.acua.org

• Membership Committee

For those who did not have the oppor-tunity to attend or to yet indicate yourinterest in getting more involved in anyof these areas, I would ask that you con-tact me or any other member of the board.

We will put you in touch with the appro-priate person who can help to answer yourquestions, provide more information, anddetermine what might be applicable areasbased on your time limitations. We real-ize that everyone’s discretionary time isalready stretched thin. Could you, how-ever, find two-three hours a month or aquarter to advance your association andprofession? In most cases, that is all thatis needed.

One area, for example, on the ACUAWeb site, is Emerging Issues. The planis to expand the Members Only sectionof the site to provide pertinent, timelyinformation and resources on emergingissues affecting us as auditors. Currently,when you are faced with a question aboutsome emerging issue, where do you turnfor concise, sound, and applicable cover-age? You might put the question out onACUA-L or conduct an Internet searchon the subject. How much more efficientwould it be to have a repository of infor-mation on the ACUA Web site wherethis information would be housed, acces-sible 24/7?

We will be establishing points of con-tact within ACUA who will serve as liai-sons to pull together some of the exper-tise that already resides in our ACUAranks. They will be coordinating the in-formation into a common format to fa-cilitate ease of navigation. More infor-mation will be forthcoming on this butthe image at right captures the essence ofhow I am proposing that this be struc-tured.

For this plan and all of our other plansto come to fruition, it will take the in-volvement of many people, but without adramatic level of involvement from anysingle person. Sharing this effort amongmany is the model that I believe will workbest.

It is a tremendous privilege to be ableto serve as ACUA’s president this year.All of us stepping into positions of lead-ership want to determine how we are go-ing to make our mark. We want to knowthat when we pass the torch on to oursuccessors, we will be able to look withpride at all that has been accomplished

Our Profession Is at a CrossroadsContinued from page 3

Continued on page 14

FALL 2002 / 5

ACUA Auditor is RatedFirst Class By Readers

LETTERSto the Editor

Dear Editor:

I read your latest issue. It was well organized, well presented, and veryinformative. However, I saw no letters to the editor. Most of us like to seea little feedback and open exchange in a professional journal. It gives themagazine a little of the “Man or Woman on the Street” appeal. Have youtried encouraging these letters? I would not be subtle.

Sterling RothThe University of Alabama-Huntsville

Dear Editor,

I just finished reading the Summer 2002 edition of CandU Auditor andhave to say this is one of the best issues to date. Every article in it wastimely and relevant to issues I am currently dealing with at my campus. Thearticle on demystifying the USA-Patriot Act has really helped me focus onthose issues that will impact this campus without having to become an ex-pert on the entire act. “Ensuring Singular Success” helped me to realizethat I am on the right track as a small (i.e., 1.5 person) shop. We havebegun work on updating our ethics program and Richard Traver providedsome wonderful information on this issue. It is obvious that a lot of hardwork goes into making this magazine and just think it is all done by volun-teers!! Great Job!!

Penny HowardLongwood University

Dear Editor,

What a great job you and your team did on the last issue of the CandUAuditor. I was impressed with the diversity of the articles and challengespresented. This journal continues to reflect the growth of our profession. Itaddresses new areas, such as the article on the USA-Patriot Act by TracyMitrano, and revisits more traditional areas, such as Dick Traver’s articleon ethics. I can appreciate all the work it takes to coordinate and publishthe journal. Please know that we appreciate the effort because it is firstclass.

Rita RichardsonUniversity of Memphis

Adventuresin Juarez

By Cheri Jones,University of Louisville

When I was a novice internal auditor, I hadthe opportunity to audit my company’s sub-sidiary in Juarez, Mexico. Having never beento Mexico, I was truly excited. A team of sixwould spend a week performing a financial auditat two locations. Lucky for me, our managerwould be working for me as an assistant at oneof the locations. He had been to the locationbefore and assured me that we would not needa passport, customs would be a breeze, and hehad directions to the subsidiary.

The first day of fieldwork arrived. I washanded the keys to the rental car. My managerwould be the navigator and another co-workerwould practice his back seat driving skills. Themanager was right about customs. Going overthe Rio Grande Bridge was no problem; theonly challenge was avoiding the beggars andvendors. Once over the bridge, however, thehustle and bustle of the city and the modernstreets quickly gave way to sand and cactus.After driving through the desert for a while,we decided we missed our turn. I learned anew skill: making a u-turn. Four u-turns later, Ifinally asked to see the directions. “Oh, I donot have any written directions or maps,” mymanager confessed. “I am looking for the signthat was here during my last visit.” When wasthat? “Only five years ago!”

You guessed it; in a cost cutting measurethe company had removed the signs the previ-ous year. However, we learned a lot about Juarezand it’s suburbs that day. After several hoursof driving, we finally stumbled into the facility,three hours late just in time to prevent the callto the local police. Unfortunately, we were intime to meet the courier from the local borderoffice. The Mexican border office had beennotified that we were going to work in the coun-try for a few days. NAFTA had just beenenacted. Although a passport was not requiredto visit the country, you did need a permit towork there. To obtain a work permit, youneeded a passport or birth certificate. At leastthe boss was right about customs.

6 / College & University Auditor

Continued on page 7

Report from HEADQUARTERS

Putting Technology to Use the ACUA Way

By Lorna Bolduc, Executive Director

Technology is an important part ofACUA’s ability to deliver member ser-vices. ACUA’s use of technology hasgreatly improved communication to mem-bers, increased accessibility to informa-tion for both our members and our lead-ership and reduced the communicationcost and the time delay in getting infor-mation disseminated.

Electronic CommunicationWe have several means of communicatingvia e-mail. The board has a listserv thatis in constant use, keeping communica-tion open about everything from ACUA-L, messages with requests for informa-tion to the status of board-driven strate-gic objectives. It is difficult to imaginethe ACUA board operating without alist, although there was day when suchtechnology was not available and commu-nication did not flow as freely among allthose involved. Other lists used by theACUA leadership include a listserve forpast presidents, one for board membersand committee chairs and another for theProfessional Education Committee(PEC).

ACUA-L probably does not need anintroduction, but I am going to mentionit. Although we think it is well advertised,we did discover a member who did notknow about this list. ACUA-L has to beone of our best member benefits. It offersa place where members can discuss audit-ing issues, ask questions, get answers and

build professional relationships with theircolleagues. Reserved for institutional rep-resentatives and those people the institu-tional representatives approve to beadded, this list is more than 1,000 strong.If you are not on the list and would like tosubscribe, the rules are simple: the insti-tutional representative needs to make con-tact with Cindy Caron at ACUA Head-quarters and provide the e-mail addressesof those who should be added to the list.Cindy ’s contact information [email protected] or call (860) 586-7561.

Another communication method weuse is e-blasts. By using software designedfor this purpose, we send personalized e-mail messages to everyone who has an e-mail address included in our membershipd a t a b a s e .These personal-ized e-mails al-low us to com-municate withyou directlyabout news thatis important toyou. For ex-ample, as soonas the registra-tion form forone of ourevents is postedto our Website, we send an

e-mail broadcast alerting our members tothe registration form’s availability. Wehave used this e-blast software to commu-nicate about the strategic plan, the finan-cial reports, our events and the ACLtraining program.

It’s on the WebThe use of the Web has certainly im-proved our capability to disseminate in-formation to the membership. Access tosuch things as our membership databasewas nearly impossible before the Web.ACUA had a traditional directory ofmembers that, like most printed member-ship lists, are out-of-date the day they goto the printer. The printing, productionand mailing of such material is a greatexpense to the organization. Now the

FALL 2002 / 7

Putting Technology to Use the ACUA WayContinued from page 6

database is updated regularly at minimalcost and is available to our members whenneeded.

While the database is not the only thingthat is of value on the Web site, it is cer-tainly one of the most important memberbenefits. Access to the director y isthrough the password protected Mem-bers-Only section. The directory offersseveral options for searching including bylast name, institution, state or country.In an effort to identify the institutionalrepresentatives for our members, weadded an asterisk to their name.

Another important item in the mem-bership directory is the URL for ourmembers’ department Web site. Manymembers are interested in checking theWeb sites of other college and universityinternal audit departments. We encour-age you to forward yours to Cindy if yourWeb site is not listed in the directory.Improved compliance with this requestwill increase the benefit of the directoryexponentially for many of our members.

Also available from the Members-Onlysection is the library. This section offersinformation on a wide selection of top-ics. It is a great resource and anotherimportant member benefit.

The index for the Members-Only sec-tion is quite long. Peruse it. Let me knowif there is anything ACUA could add toimprove our service to you.

Other items on the Web site that youmay have missed include a link to the IIACPE online training. If you have notchecked into this, you should. Our boardmembers were delighted to offer you thisprogram because it is a great educationalresource for auditors. Distance learningis cost effective – no travel and it is avail-able when you have the time or need.

We have partnered with ACL to sig-nificantly reduce the cost of training fortheir software and to add as a benefit,training that has a higher education fo-cus. We plan to offer two classes a yearand will send an e-blast to let you knowwhen the registration form is available.

You can find general information aboutACUA on the site including our strate-gic plan, our membership categories, eventdates and locations and nomination formsfor our scholarship and awards programs.Which reminds me, if you or a memberof your staff is working toward an under-graduate or graduate degree, do not missthe opportunity to apply for a scholarship.The form is on the Web site and the schol-arships are awarded at our annual confer-ence.

Need to contact a board member orcommittee chair? Want to volunteer a littletime toward bettering your profession?Need to mail something to headquarters?It’s all on the ACUA Web site.

The Bottom LineCosts for postage and printed materialshave decreased over the years as ACUA

relies more and more on electronic com-munication for information dissemination.We rely on e-mail and lists to deliver in-formation to you. We also rely on you togo to the ACUA Web site to get the in-formation you need. The bottom line isnot only reduced printing and mailing costsbut also increased accessibility for ourmembers to the information they require.

What Do You Need?Please review the Web site and let meknow what ACUA might be able to pro-vide that would benefit you profession-ally. We would like to add information thatwould enhance benefits to the people weare here to serve, our members. My e-mail address is [email protected] or call(860) 586-7561. I look forward to hear-ing from you.

ACL on cd in bagNew ad coming will run 11/02, 3/03, 7/03

8 / College & University Auditor

Internet Security ADcoming will run 11/02

new ad coming for 3/03, 7/03

At the 2002 Annual Conference in SaltLake City, the ACUA Board of Direc-tors reaffirmed its commitment to its fivestrategic goals. One goal is the Promo-tion of Internal Audit in Higher Educa-tion. Last year, a group interested in thisinitiative dealt with questions about whatstrategies could be employed to furtherthis goal and attempted to identify an ac-tion plan. This year, more individualssigned up to be involved in this goal’simplementation. The group has not yethad a chance to discuss specifics, but con-versations during the ACUA conferencegenerated many ideas about how ACUAcould assist its membership in promotinginternal audit in their own institutions,as well as how ACUA could help pro-mote internal audit to a broader audience.

Here are a few ideas the group is con-sidering:External Promotion of Internal Audit:• Create a purpose statement for inter-

nal audit in higher education.

• Use experiences of one-person shopsto make the case that every campusneeds an independent, objective re-source to enhance operations.

• Compile positive, pragmatic examplesof what internal audit in higher edu-cation has done and is doing.

• Publish a white paper on the value ofinternal audit and the risks ofoutsourcing in light of recent account-ing scandals.

Promotion of the Internal Audit Functionin Higher EducationBy Sterling Roth, director of Internal Audit, University of Alabama-Huntsville andMarsha Payne, director of Internal Audit, University of California-Irvine

• Start a membership drive focused oninstitutions that do not currently haveinternal audit functions. Initiate amembership drive focused on commu-nity colleges.

Internal Promotion of Internal Audit:• Provide a generic marketing brochure

that small audit shops could personal-ize, avoiding having to start a brochurefrom scratch.

Continued on page 14

FALL 2002 / 9

Continued on page 10

The Government bodyresponsible for fundinghigher education in En-gland is reducing theamount of audit work itdoes in universities. Atthe same time, the inter-nal auditors in those universities are adopt-ing a more risk-based approach.

Universities and colleges of highereducation in England are experiencingmajor changes to the audit and account-ability framework in which they operate.There are 130 of these institutions, andwhile they can trace their independenceback to parliamentary authority, they areall dependent on and accountable fortaxpayer’s money. The catalyst for thechanges is the spread of corporate riskmanagement across the private and pub-lic sectors.

Changes in accountability are takingplace alongside fundamental changes inother ways. For example, the governmentis now committed to increasing the in-volvement of young people in higher edu-cation from the current level of 30% to50% by the year 2010. This expansionis in addition to many other changes overthe past decade and emphasizes the needfor the institutions to increase their ef-fectiveness if they are to deliver society’sand the government’s ambitious targets.

English higher education institutionscover a broad spectrum from major inter-

The Changing Audit Frameworkfor English UniversitiesBy Paul Greaves, Chief Auditor of the Higher Education Funding Council for England

national players such as Oxford and Cam-bridge universities through specialist bod-ies like the Royal Colleges of Art andMusic and the London School of Eco-nomics and Political Science to relativelynew, diverse universities, such as theManchester Metropolitan University andthe University of the West of England.Institutions vary in size from 150 stu-dents up to almost 30,000.

The Higher Education FundingCouncil for England (HEFCE,www.hefce.ac.uk)The HEFCE is a semi-governmentalentity that operates as a buffer betweenthe ministry (the Department for Educa-tion & Skills) and the institutions. It de-vises and operates formulae and other ar-rangements to distribute cash from the UKTreasury to the institutions. The HEFCEhas an annual budget of over US$7,000m, which constitutes less than halfof the total income for English universi-ties.

The HEFCE sets the framework ofaccountability for universities and colleges.To be eligible to receive public funding,the institutions have to comply with con-ditions of grants set out in a financialmemorandum (available on the HEFCEWeb site at publication number 2000/25) and these conditions include compli-ance with audit arrangements which in-clude:

• Each institution has to publish auditedfinancial statements. The bulk of in-stitutions are audited by major ac-countancy firms.

• Institutions are also required to havean internal audit service that meetsprofessional standards.

• Institutions must have an audit com-mittee, largely composed of membersof its governing body, the duties ofwhich are set out along with other re-quirements in the HEFCE AuditCode of Practice (HEFCE 2002/26).

There are separate arrangements forauditing or quality assuring academic ac-tivities. Teaching is assessed by a sepa-rate body, the Quality Assurance Agency.Research is assessed through a HEFCE-led research assessment exercise.

The HEFCE Audit ServiceThe HEFCE Audit Service is a smallteam of auditors which promotes the ef-fectiveness of, and assesses internal con-trol in the institutions. It does this bymonitoring a continuously evolving riskassessment of the institutions. The riskassessment is informed by:

• Information about financial healthsupplied by HEFCE colleagues whomonitor the operational, financial andstrategic progress of the institution.

10 / College & University Auditor

• Information and assurances from theinstitutions including the publishedfinancial statements and the annual re-ports of the external and internal au-ditors and the audit committees.

• A data audit undertaken by theHEFCE auditors designed to validatethe various data submitted in supportof funding claims and payments.

• A cycle of audit visits by HEFCEauditors.

Risk ManagementThe concept of risk management as anorganizational framework for improvinginternal control and a vehicle for enhancedfinancial reporting has spread throughoutall UK corporate sectors in recent years.The HEFCE has been working with in-stitutions to promote risk managementthrough publishing good practice guidesthat are available on the Web (HEFCE2001/28, for example). The HEFCEhas also agreed with the institutions thatpublished financial statements should in-clude, from 2003, the same sort of state-ments of corporate governance, internalcontrol and risk management that are re-quired of listed companies.

The audit professional bodies in En-gland have changed their standards relat-ing to internal audit so that practice isexpected to reflect risk management. In-ternal auditors are expected to assess andadvise on risk management and to basetheir planning on corporate risk manage-ment so long as they have confidence init. This major development in internalaudit practice has been reflected in theunique role of the HEFCE’s own audi-tors. In the past, these auditors have hada cyclical approach to their work: follow-ing the same audit program, for the samelength of time, at the same frequency ineach institution. In the context of riskmanagement and other factors, the audi-tors reflected on their practice, throughan analytical and consultative methodol-ogy, and decided to make their own workrisk based. The consequence is a consid-

erably reduced burden of governmentalaudit for most institutions.

The institutions are in turn expectedto develop effective risk management andto maintain high standards of corporategovernance. They are expected to reportto the taxpayer, through the HEFCE, thatthey have effective self-assessment regimesthat ensure the quality of internal con-trol. The various reports involved informrisk assessment by the HEFCE and thatin turn determines how closely each insti-tution needs to be monitored.

Internal Audit in InstitutionsEach institution has to have an internalaudit service that meets professional stan-dards. The requirements for the opera-tion and reporting of those internal audi-tors are set out in the Audit Code. ThisCode has been updated over the past yearto reflect the impact of risk management.It is now accepted, for example, that au-ditors can play a consultancy and advi-sory role to management in support ofimproved corporate governance, internalcontrol and risk management. In reality, anumber of auditors have been instrumen-tal in catalyzing the adoption and imple-mentation of corporate risk managementin their institutions.

Internal auditors are expected now tomove away from the idea of an audit strat-egy that seeks comprehensive coverage ofall systems over a cycle. Their plans shouldincreasingly reflect corporate risk manage-ment and they should place emphasis onmajor risks to the business. Of course,the auditors can only allow themselves tobe influenced by management’s percep-tion of risk if they are confident in thecorporate risk strategy. Therefore, theirwork needs to explicitly embrace an on-going assessment of corporate risk man-agement. Where they are not confidentabout management’s risk approach, theyshould report that fact to the audit com-mittee and base their planning on whatthey consider to be more important fac-tors.

This is a major challenge for institu-tional auditors. They have to become suf-ficiently expert in risk management to cata-lyze a risk strategy and then to judgewhether corporate risk management issound. The skills are present in the auditcommunity but the immediate challengeis to bring these skills into play.

ConclusionThe arrival of corporate risk managementfor English universities and colleges hasprovided an opportunity for central gov-ernment monitoring to be, on the whole,scaled back. In turn, institutions are ex-pected to develop effective risk manage-ment. Institutions’ internal auditors haveto change radically to embrace this newculture.

About the AuthorPaul Greaves is Chief Auditor of theHigher Education Funding Council forEngland. He is responsible for providingassurances on the use of public money inEngland’s 130 universities and highereducation colleges. Paul has degrees in eco-nomics and Irish history, and an MBAfrom the University of the West of England.He is a Fellow of the Institute of InternalAuditors – UK. You may e-mail him at:[email protected].

The Changing Audit Framework for English UniversitiesContinued from page 9

Internal auditors areInternal auditors areInternal auditors areInternal auditors areInternal auditors are

expected now to move awayexpected now to move awayexpected now to move awayexpected now to move awayexpected now to move away

from the idea of an auditfrom the idea of an auditfrom the idea of an auditfrom the idea of an auditfrom the idea of an audit

strategy that seeksstrategy that seeksstrategy that seeksstrategy that seeksstrategy that seeks

comprehensive coverage ofcomprehensive coverage ofcomprehensive coverage ofcomprehensive coverage ofcomprehensive coverage of

all systems over a cycle.all systems over a cycle.all systems over a cycle.all systems over a cycle.all systems over a cycle.

Their plans shouldTheir plans shouldTheir plans shouldTheir plans shouldTheir plans should

increasingly reflectincreasingly reflectincreasingly reflectincreasingly reflectincreasingly reflect

corporate risk managementcorporate risk managementcorporate risk managementcorporate risk managementcorporate risk management

and they should placeand they should placeand they should placeand they should placeand they should place

emphasis on major risks toemphasis on major risks toemphasis on major risks toemphasis on major risks toemphasis on major risks to

the business.the business.the business.the business.the business.

FALL 2002 / 11

Continued on page 12

Historical BackgroundThe rapid development of Lebanon as abanking and financial services center be-tween 1955 and 1975 was fueled byArabian oil revenues and encouraged bythe reputation of Beirut as the most cos-mopolitan and westernized city in theMiddle East. With its wonderful physi-cal climate, relaxed and relatively unregu-lated business climate, the country was amagnet for entrepreneurs of all types. Thebubble burst in 1975 with the outbreakof the Lebanese Civil War. Lebanon’sreputation changed from being abusinessman’s paradise to a country inchaos, and Beirut became synonymouswith terrorism and sudden death. By theend of the war in 1990, the country wasin ruins and the economy was largely de-stroyed.

Today, Lebanon and the city of Beirutare rising anew — not for the first timeas ancient remnants of Phoenician, Ro-man, Crusader and Ottoman buildings inthe city center attest. The banking sectorhas strengthened through mergers and gov-ernment regulations that include a re-quirement that banks establish an inter-nal audit function. The educational sec-tor has expanded rapidly. There are cur-rently 43 universities in Lebanon, ofwhich 35 offer instruction in English.Only two universities have an internalaudit function: the American Universityof Beirut (AUB) and the Lebanese

Internal Audit at theAmerican University of BeirutBy Internal Audit Office members, American University of Beirut

American University. AUB was foundedin 1866 by Dr. Daniel Bliss, a U.S. mis-sionary, and has 6,500 students in pro-grams modeled on the American liberalarts system. AUB is chartered in NewYork State and its registered office is inNew York City – the difference is thatthe campus is in Beirut, Lebanon.

Internal Audit at AUBThe Internal Audit Office was establishedat AUB in the early 1970s. Initially,audit functions were limited to the 400-bed Medical Center and it was not until1985 that the scope of work was extendedto cover the campus operations. However,the work tended to be limited to cashcounts, financial tests, inventory countsand attendance at tender openings. In1996, the trustees directed that the In-ternal Audit function be expanded andstrengthened. The office currently con-sists of a director, two audit managers andthree audit assistants.

In 1996 AUB was an institutioncaught in a 20-year time warp. Althoughthe university had managed to keep func-tioning throughout the Lebanese CivilWar, many had suffered and the majorityof the university’s foreign administratorsand faculty had fled the country. Thepresident’s office functioned from NewYork City and many administrative func-tions were moved to Cyprus when thefighting in Beirut threatened to overrunthe campus. Wartime necessities had al-

lowed a number of “informal” practicesto develop in place of the meticulouslydocumented policies and procedures thatdated from 1965. Internal controls wereno longer a priority and their purpose wasoften long forgotten.

In 1997 the Audit Committee of theBoard approved new Terms of Reference[ToR] for the Internal Audit Office.These ToR clearly established the man-date and the objectives of the office andemphasized the change in the role of in-ternal audit from policeman to consult-ant.

Association with ACUA was amongthe very first steps undertaken as a way totap into the knowledge and experience ofour peers. ACUA proved an excellentsource of audit programs and professionaldevelopment materials that were used to

Lebanon University

12 / College & University Auditor

TTTTTasks continued to be doneasks continued to be doneasks continued to be doneasks continued to be doneasks continued to be done

out of habit, often withoutout of habit, often withoutout of habit, often withoutout of habit, often withoutout of habit, often without

having any controlhaving any controlhaving any controlhaving any controlhaving any control

purpose or value.purpose or value.purpose or value.purpose or value.purpose or value.

Internal Audit at the American University of BeirutContinued from page 11

improve the skills and professional knowl-edge of the audit staff.

Assessing and improving the existingsystem of internal controls was a priority.This task was complicated by the onlypolicies and procedures in existence werefrom the 1960s. Consequently, testing forcompliance was often pointless. The pro-cedures had been written for systems thatwere primarily manual and two genera-tions of computerization had subsequentlybeen implemented. Amazingly, it wasfound that despite this computerizationthe forms and workflow had remained vir-tually unchanged for 30 years—with manyforms still having five copies that requiredthe use of carbon paper! Tasks continuedto be done out of habit, often withouthaving any control purpose or value.

To address this, Internal Audit con-centrated on operational audit work aimedat analyzing and improving workflow andcontrols. The positive approach ofconsultancy-based audits and “taking offthe police hat” has changed the way thatInternal Audit is perceived within theinstitution. This has increasingly resultedin departments requesting that InternalAudit review changes in their work pro-cesses to ensure that appropriate and ef-fective internal controls exist.

In 1998, the office introduced the firston-line policy and procedures manual atAUB. Since then many new manualshave been added and, eventually, all theuniversity’s manuals will be available online. The Internal Audit Office Manualwas published in 2000 based on the tem-plate obtained from the IIA.

In 2002, we introduced the conceptof Control Self Assessment (CSA), be-coming the first organization in Lebanonto do so. CSA has met with a favorable

response by management because it pro-vides an opportunity to mutually shareviews and ideas in an open environmentand also, among Internal Audit staff be-cause it is a very effective way to aug-ment traditional audit techniques.

Auditing and the Institute ofInternal Auditors in LebanonThe Lebanese Association of CPAs pro-vides professional certification in Leba-non. However, many Lebanese profes-sionals have also obtained certificationoverseas, the most common designationbeing the American CPA. All the majoraudit firms are established in Lebanon.Although the official language of Leba-non is Arabic, the operational languageof the profession is English, while Frenchis also commonplace. The majority ofLebanese professionals are proficient inall three languages.

The IIA, Lebanon Chapter, was in-corporated in 2000 and has contributedto promoting the Internal Audit functionin the country. The chapter started ad-ministering the CIA and CCSA certifi-cations in 2002. When established, therewere no CIAs among the founding mem-bers. Since then, the chapter has grownto almost 50 members including eightCIAs and one CSSA and includes allthe audit staff at AUB. At the 2002annual conference of the IIA in Wash-ington, DC, the Lebanon Chapter wasawarded the prize as the fastest growingchapter.

For more information about InternalAudit at AUB visit: http://departments.aub.edu.lb/~webaudit/. Youmay contact the Internal Audit manager,Sami Gheriafi, at: [email protected]

FALL 2002 / 13

Continued on page 14

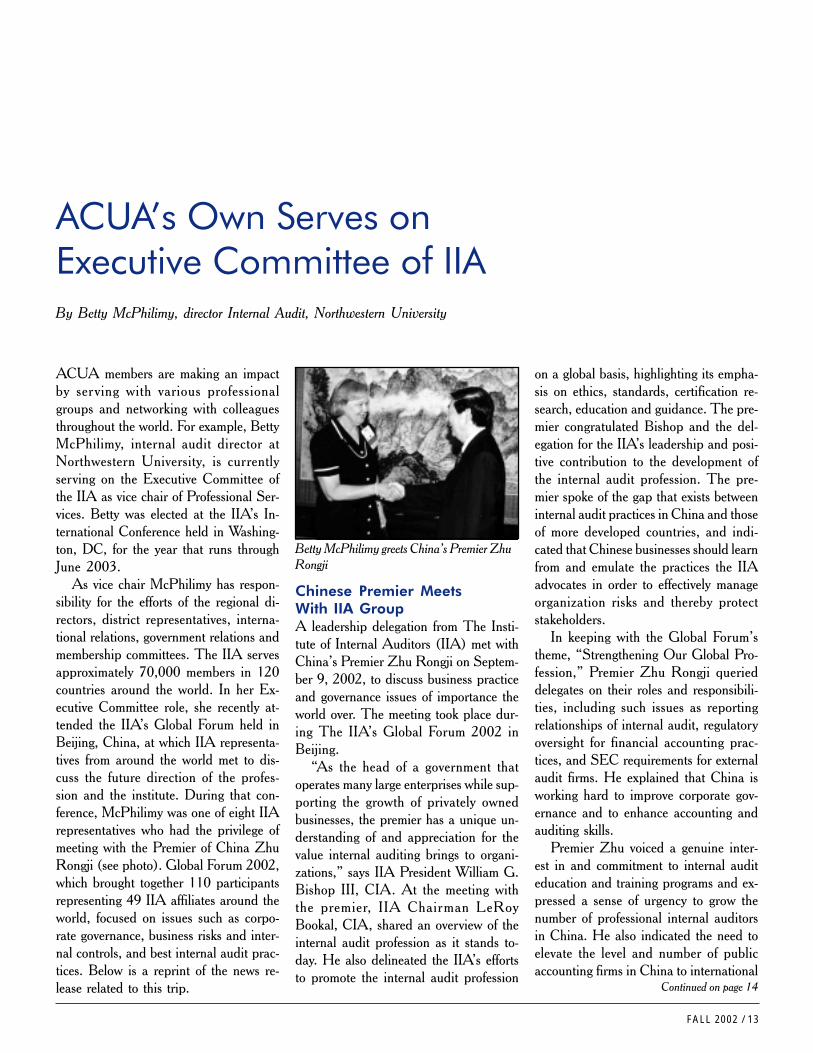

ACUA members are making an impactby ser ving with various professionalgroups and networking with colleaguesthroughout the world. For example, BettyMcPhilimy, internal audit director atNorthwestern University, is currentlyserving on the Executive Committee ofthe IIA as vice chair of Professional Ser-vices. Betty was elected at the IIA’s In-ternational Conference held in Washing-ton, DC, for the year that runs throughJune 2003.

As vice chair McPhilimy has respon-sibility for the efforts of the regional di-rectors, district representatives, interna-tional relations, government relations andmembership committees. The IIA servesapproximately 70,000 members in 120countries around the world. In her Ex-ecutive Committee role, she recently at-tended the IIA’s Global Forum held inBeijing, China, at which IIA representa-tives from around the world met to dis-cuss the future direction of the profes-sion and the institute. During that con-ference, McPhilimy was one of eight IIArepresentatives who had the privilege ofmeeting with the Premier of China ZhuRongji (see photo). Global Forum 2002,which brought together 110 participantsrepresenting 49 IIA affiliates around theworld, focused on issues such as corpo-rate governance, business risks and inter-nal controls, and best internal audit prac-tices. Below is a reprint of the news re-lease related to this trip.

ACUA’s Own Serves onExecutive Committee of IIABy Betty McPhilimy, director Internal Audit, Northwestern University

Chinese Premier MeetsWith IIA GroupA leadership delegation from The Insti-tute of Internal Auditors (IIA) met withChina’s Premier Zhu Rongji on Septem-ber 9, 2002, to discuss business practiceand governance issues of importance theworld over. The meeting took place dur-ing The IIA’s Global Forum 2002 inBeijing.

“As the head of a government thatoperates many large enterprises while sup-porting the growth of privately ownedbusinesses, the premier has a unique un-derstanding of and appreciation for thevalue internal auditing brings to organi-zations,” says IIA President William G.Bishop III, CIA. At the meeting withthe premier, IIA Chairman LeRoyBookal, CIA, shared an overview of theinternal audit profession as it stands to-day. He also delineated the IIA’s effortsto promote the internal audit profession

on a global basis, highlighting its empha-sis on ethics, standards, certification re-search, education and guidance. The pre-mier congratulated Bishop and the del-egation for the IIA’s leadership and posi-tive contribution to the development ofthe internal audit profession. The pre-mier spoke of the gap that exists betweeninternal audit practices in China and thoseof more developed countries, and indi-cated that Chinese businesses should learnfrom and emulate the practices the IIAadvocates in order to effectively manageorganization risks and thereby protectstakeholders.

In keeping with the Global Forum’stheme, “Strengthening Our Global Pro-fession,” Premier Zhu Rongji querieddelegates on their roles and responsibili-ties, including such issues as reportingrelationships of internal audit, regulatoryoversight for financial accounting prac-tices, and SEC requirements for externalaudit firms. He explained that China isworking hard to improve corporate gov-ernance and to enhance accounting andauditing skills.

Premier Zhu voiced a genuine inter-est in and commitment to internal auditeducation and training programs and ex-pressed a sense of urgency to grow thenumber of professional internal auditorsin China. He also indicated the need toelevate the level and number of publicaccounting firms in China to international

Betty McPhilimy greets China’s Premier ZhuRongji

14 / College & University Auditor

ACUA’s Own ServesContinued from page 13

standards. As a result, he is in the pro-cess of having three new Chinese account-ing/audit schools established. He invitedthe IIA to conduct future forums in Chinaand encouraged greater IIA coordinationwith its Chinese affiliate and interactionwith the China National Audit Office.

In addition to the IIA’s chairman andpresident, the delegation that met withPremier Zhu included Past IIA Chair-man Dave Richards, CIA; Senior ViceChairman Robert McDonald, CIA; ViceChairman-Professional Services BettyMcPhilimy, CIA; and Board of RegentsChairman Hans Spoel, CIA, who spokeof the importance of professional certifi-cation and of the growing number of Chi-nese—currently more than 2,200—whohave earned the Certified Internal Audi-tor (CIA) designation.

Also participating in the meeting withthe premier were IIA Director-at-largeStanley Chang, CIA, and North PacificRegional Director Naohiro Mouri. Rep-resenting IIA China were PresidentZheng Li, Secretar y General MaHuaiping, and Cao Zhiyong. AuditorGeneral Li Jinhua and Deputy AuditorGeneral Liu Jiayi represented the ChinaNational Audit Office.

Global Forum 2002, which broughttogether 110 participants representing 49IIA affiliates around the world, focusedon issues such as corporate governance,business risks and internal controls, andbest internal audit practices. A highlightof the forum was a keynote address byMer vyn King, chairman of SouthAfrica’s King Committee on CorporateGovernance and one of the world’s mostrespected authorities on the topic. Kinglauded internal auditing as a “vital ingre-dient” of an effective governance process.

• Create a library of marketing bro-chures for those who want to maketheir own and want ideas.

• Capture other approaches used to pro-mote the internal audit function.

• Employ peer reviews to transfer ele-ments of successful internal audit op-erations to institutions with less expe-rienced staff.

Some ideas may overlap with ideasrelated to other initiatives, so it is impor-tant that we continue an open dialogueabout our plans to avoid duplication ofefforts and benefit from the wealth of ideasfrom our colleagues.

If you are not already on the team andhave an interest in this initiative, pleasecontact one of the following:

Marsha PayneUC [email protected](949) 824-7855

Sterling RothUniversity of [email protected](256) 824-6037

Kim Turner, Board liaisonTexas Tech [email protected](806) 742-3220

“Promotion” has many meanings andconnotations. Let’s help each other as-pire to the best of them. All comments,opinions and materials are welcome.

Promotion of the Internal Audit Function in Higher EducationContinued from page 8

Our Profession Is at a CrossroadsContinued from page 4

during our tenure. I want to make surethat our plans are aggressive yet realis-tic.

Some of the highlights of our plansthis year include:• Significant enhancements to the

ACUA Web site – providing a com-mon source of valuable and timely in-formation for our members;

• Expanding our membership to ensurethat the association is reaching vir-tually every institution of higher edu-cation with an audit presence; and

• Furthering the strategic plan so thatwe are able to demonstrate notableprogress.

To accomplish these goals, it will takemore than the efforts of the talented anddedicated board members and commit-tee chairs. It will take the collective con-tributions and efforts of each of theACUA members.

At Georgia Tech, I am blessed to besurrounded by a talented staff – individu-als on whom I count to ensure the ac-

complishment of our annual audit plan.The same principle holds true for ACUA.The board and committee chairs have beenand will continue to be dedicated to serv-ing the membership by providing strate-gic direction. To make positive strides thisyear toward achieving our strategic goalsand adding more valuable services to youas members will take the involvement ofeach of us as constituents.

As Jay Morley, president ofNACUBO, said in his keynote address,“Has there ever been a better time to bean internal auditor?” I would add, hasthere ever been a better place to be aninternal auditor than in an institution ofhigher education? And finally, has thereever been a professional association moreappropriately positioned to provide valu-able services to its members than ACUA?

This is your association. It is yourprofession. We are positioned to do greatthings. Would you join me in helping tomake a mark on ACUA this year?

Editor ’s note: Contact Rob [email protected] or callhim at (404) 894-4606.

As a result, he is in theAs a result, he is in theAs a result, he is in theAs a result, he is in theAs a result, he is in the

process of having three newprocess of having three newprocess of having three newprocess of having three newprocess of having three new

Chinese accounting/auditChinese accounting/auditChinese accounting/auditChinese accounting/auditChinese accounting/audit

schools established.schools established.schools established.schools established.schools established.

FALL 2002 / 15

On May 1, 2002,Johnnie Frazier, in-spector general of theU.S. Department ofCommerce, ap-peared before a sub-committee of theHouse of Representatives and outlinedwhat he described as “the good, the badand the ugly” facts that had been learnedin an extensive review of the Departmentof Commerce (DOC) purchase card sys-tem. He explained that over the course ofthe 15 years that the purchase card sys-tem had been in place, many well-publi-cized examples of “irresponsible and ille-gal use” of purchase cards had given theprogram a negative image. Further, theprogram had grown in size to the pointwhere it presented a formidable risk.

“In fiscal year 2001, the CommerceDepartment averaged over 6,000 pur-chase cardholders at any particular time,and during this twelve-month period, thesecardholders completed over 330,000transactions valued at about $132 mil-lion. In short, the Commerce purchasecard program represents substantial pur-chasing power, and as a result—at leastfrom the Office of Inspector General(OIG) perspective—provides substantialopportunity for misuse and fraud.”

Mr. Frazier went on to cite specificexamples:

A Comprehensive Approach toProcurement Card AuditsBy Doug Burton, Account Executive for Healthcare, Education and Manufacturing, ACL

• A contract specialist fraudulently usedher government purchase card to buyapproximately $50,000 worth of cloth-ing, jewelry, electronic equipment, fur-niture, airline tickets, sporting eventtickets, concert tickets, household sup-plies, and hotel accommodations.

• A secretary used her card to purchasegroceries, school supplies, books, elec-tronics and bath supplies. She also usedthe card to pay for a luxury hotel onNew Year’s Eve. The secretary hadbeen intercepting her statement eachmonth and avoiding scrutiny. Onlyafter she went on extended leave due toan accident were the inappropriatetransactions discovered.

• In another case, a clerk used a co-worker’s card to purchase over $1,000in personal items including clothing,exercise equipment and toys.

It goes without saying that stories suchas these are by no means restricted togovernment service. Any organization orinstitution that uses purchase or procure-ment cards is at risk. The efficiency andconvenience of purchase card systemsbrings with it new opportunities for fraudand abuse.

Fortunately, in the same way that tech-nology has given rise to this new chal-lenge, technology can be used to addressit. Purchase card systems are, by theirvery nature, textbook opportunities for Continued on page 16

the effective application of interactive dataanalysis. With the appropriate software,high volumes of purchase transactionsmay now be reviewed and audited in greatdetail, resulting in the detection of abusesthat may have otherwise gone unnoticed.

It is assumed that any audit of a pur-chase card system will be conducted witha thorough understanding of existing con-trols, the rules and policies governing ac-ceptable use of the system, and the mea-sures being taken to communicate thesepolicies to the cardholders. Therefore, thisdiscussion primarily focuses on the analy-sis portion of the audit and how softwaretools can be used to maximum benefit.

Obtaining the DataOnce the planning of a purchase cardaudit has been completed, the first stepin the analysis phase is to obtain the nec-essary data. If you are used to leveragingdata analysis in your audits, you are prob-ably familiar with the challenges that fre-quently occur when trying to access and

The efficiency andThe efficiency andThe efficiency andThe efficiency andThe efficiency and

convenience of purchaseconvenience of purchaseconvenience of purchaseconvenience of purchaseconvenience of purchase

card systems brings with itcard systems brings with itcard systems brings with itcard systems brings with itcard systems brings with it

new opportunities for fraudnew opportunities for fraudnew opportunities for fraudnew opportunities for fraudnew opportunities for fraud

and abuse.and abuse.and abuse.and abuse.and abuse.

16 / College & University Auditor

and follow your intuition can yield verypositive results. In addition, you will natu-rally learn to think critically rather thanfollowing a prescribed plan.

After having explored the data for awhile, shift your focus to a more preciseform of investigation by using the appli-cation to filter for known problem trans-actions. These should reflect previousabuses that have been documented fromwithin your own organization. Addition-ally, you may have noted typically prob-lematic transaction profiles that you havepicked up from other sources such asbooks, presentations and advice from col-leagues. These primarily represent trans-actions that fail to follow defined policiesor in some way circumvent establishedcontrols. Examples may include:• Concentration of purchases immedi-

ately below a control limit;

• High number of purchases by thesame cardholder from a single vendor;

• Consecutive purchases to the samevendor on the same day (purchasesplitting);

• Purchases made on weekends or holi-days; or

• Purchases made by cardholders whoare no longer actively employed by theorganization.

Value Added AnalysisThese days, there is much debate onwhether auditors should act as consult-ants to their organizations; however, thereis great opportunity for adding value inall audits. While you are rummagingthrough all of these purchase card trans-

A Comprehensive Approach to Procurement Card AuditsContinued from page 15

define the appropriate data. If this hasbeen a stumbling block in past audits, takeheart. Your bank should be able to pro-vide complete purchase data in a formatthat can be read by ACL or your analy-sis tool of choice. The data may be pro-vided to you on a CD or in some casesyou may actually be able to download itin manageable blocks through a Web re-porting tool.

When you go to pull a data sample foranalysis, one word of advice—Don’t. Inother words, don’t think in terms of ex-tracting a sample that will give you a mean-ingful representation of the total popula-tion. Modern analysis tools are more thanable to handle as much data as you careto throw at them. Further, there is verylittle additional work involved in using allof the relevant data rather than just someof it. The advantage is that the more datayou work with, the greater the certaintyof your results. Why think in terms ofprobability when you can know for sure.

While we’re on the subject of data, youmay also want to pull related data fromyour accounting and HR systems as well.Every institution is different on this score,but you may find that payment or pur-chase order information from accountingcan be correlated to the purchase cardtransactions to lend additional insight intopossible risks and abuses.

Getting Down to BusinessThere are many different ways to ap-proach the analysis of purchase card data.To begin with, you may wish to “interro-gate” the data in order to build your un-derstanding of the size and scope of thepopulation and to catch any red flags thatbecome immediately apparent. This cantake the form of sorting and summarizingthe purchases in order to identify indica-tors such as:• Largest overall dollar purchases

• Largest purchase value by user

• Largest purchase value by department

• Largest number of transactions byuser/department

Tests such as these will bring the projectinto focus and give you your first indica-tions of where the risk areas lie and whereyou might want to focus your attention.Depending on the tool, you should be ableto “drill down” on any suspect areas andfocus your efforts momentarily on thatsubset of data.

During the planning phase, it is advis-able to closely review the list of purchasecategories that your bank has defined. Allpurchases are assigned a category or mer-chant code such as: travel agents, restau-rants, bookstores, etc. A quick look atthis list will immediately highlight poten-tial red flag categories such as nightclubsor other entertainment venues. Once youhave assembled a list of potentially prob-lematic categories you can use your soft-ware to filter for any transactions madefor those items. If you find the list of prob-lem categories too long to filter for indi-vidually, it is useful to classify the totalpopulation by purchase category in orderto get an overview of actual purchases.This will produce a long list that youshould be able to quickly peruse for itemsof interest.

Another approach to looking at ques-tionable purchases is to identify a shortlist of the categories that concern youmost and classify only those purchases bydepartment or user. If you identify a par-ticular department that shows a high fre-quency or dollar amount in a risky cat-egory, you may have something to inves-tigate.

With this type of analysis, it is impor-tant to give yourself enough time to playwith the data. Here’s why: experiencedanalysts will tell you that the work they dois part science and part art. There are anendless number of ways that you can ex-plore the data and it is important to giveyourself the freedom to explore and thinkcreatively. Most auditors have an extremeshortage of time and their first instinct isto check off the items on the audit planand move on. Giving yourself a set pe-riod of time to creatively explore the data

Continued on page 17

Giving yourself a set periodGiving yourself a set periodGiving yourself a set periodGiving yourself a set periodGiving yourself a set period

of time to creatively exploreof time to creatively exploreof time to creatively exploreof time to creatively exploreof time to creatively explore

the data and follow yourthe data and follow yourthe data and follow yourthe data and follow yourthe data and follow your

intuition can yield veryintuition can yield veryintuition can yield veryintuition can yield veryintuition can yield very

positive results.positive results.positive results.positive results.positive results.

FALL 2002 / 17

actions, you may want to watch for pat-terns that may indicate opportunities tochange purchasing policies to benefit theuniversity. For example, if large volumesof a particular item or category of itemsare noted, it may be worth pointing outto management that contract pricing couldpotentially be negotiated. In this samevein, you may wish to point out items thatare routinely purchased by card that wouldmore appropriately be purchased througha more formal process. These might in-clude higher risk items such as chemicalsor high dollar items such as lab equip-ment. Another angle on this test involvesreviewing purchases to determine whetheritems that are already being purchased bybulk contract are being mistakenly ob-tained in small volumes at a higher priceby unknowing card holders.

Recommendations such as these mayor may not be welcomed by your purchas-ing department but it is worth noting thatthe cost savings they will bring can in somecases be calculated down to the dollar. Itnever hurts the reputation of the auditdepartment to put a little cash back onthe bottom line.

Pointing to ProcessMany auditors feel that the analysis por-tion of an audit is exclusive and does nothave any connection to what some term“process audits.” To the contrary, thisproject (as with many others) demon-strates how the effective use of data analy-sis will often point to process issues thatmust be further investigated using moretraditional methods. For example, if pur-chase splitting is a common problem thatis exposed by analysis, control limits mayneed to be reevaluated. If there is a highincidence of inappropriate purchases ina certain department, it may indicate laxsupervision, poor tone from the top, or aneed for training. As another example,purchases made by terminated employeesmay indicate a need to overhaul termina-tion procedures and improve inter-depart-ment communication.

This is an excellent example of whereeven a traditional audit can benefit fromdata analysis. In the traditional scenario,the auditor would at some point randomlyapproach management and staff in theuniversity and ask them if they understandand comply with the policies and proce-dures governing process in question. Theanswer of course is normally an emphatic“Yes!”

When data analysis is properly applied,the auditor is able to target specific mem-bers of management and staff who havebeen shown to not understand the poli-cies or are disregarding them. One ap-proach deals with samples, questions andprobabilities; the other deals with firmnumbers, statements of fact and recom-mendations for change.

Other BenefitsAny discussion of purchasing in a highereducation environment can easily lead tothe issue of research grant compliance.This is another discussion entirely. How-ever, it is worth noting that depending onyour policies governing the use of pur-chase cards by faculty, your analysis ofthis data could yield some important in-sight into your compliance risks.

By isolating purchases to specific fac-ulty members and joining this data withgrant information, you may be able to doa partial grant compliance review. Forexample, look for capital purchases made

A Comprehensive Approach to Procurement Card AuditsContinued from page 16

When data analysis isWhen data analysis isWhen data analysis isWhen data analysis isWhen data analysis is

properly applied, theproperly applied, theproperly applied, theproperly applied, theproperly applied, the

auditor is able to targetauditor is able to targetauditor is able to targetauditor is able to targetauditor is able to target

specific members ofspecific members ofspecific members ofspecific members ofspecific members of

management and staff whomanagement and staff whomanagement and staff whomanagement and staff whomanagement and staff who

have been shown to nothave been shown to nothave been shown to nothave been shown to nothave been shown to not

understand the policies orunderstand the policies orunderstand the policies orunderstand the policies orunderstand the policies or

are disregarding them.are disregarding them.are disregarding them.are disregarding them.are disregarding them.

on the card that were outside the effec-tive dates or near the end of a grant. Re-view purchase categories that are incon-sistent with the limitations of the grant.There is a significant amount of specificinformation that is required to do a thor-ough compliance check on each grant.General ledger records, detailed purchas-ing records, effort reporting and other dataare required to do a thorough review inthis area. However, by taking advantageof the data you have available, you mightjust find something of serious interest tothe university without expending a sig-nificant amount of extra time and effort.

ConclusionIt bears repeating that effective data analy-sis is both an art and a science. Far frombeing just a pastime of “techies,” it is avaluable tool that can unlock your abilityto think critically and creatively. By elimi-nating many of the traditional limitationsof the auditor, data analysis allows you toflex your analytical muscles and demon-strate to the organization the unique valueof the auditor and the audit function.

About the AuthorDoug Burton is the Account Executive forHealthcare, Education and Manufactur-ing at ACL Services Ltd. He works exten-sively with senior management in manyof North America’s largest and most pres-tigious organizations, including Fortune500 companies. With over 15 years’ ex-perience in business process automation,Doug works closely with financial execu-tives and audit professionals to apply ACLBusiness Assurance solutions to identifyand address areas of business risk associ-ated with incomplete, inaccurate and in-consistent data.

Doug has also been a featured speakerat numerous seminars and conferences, in-cluding those sponsored by The IIA,ISACA, AHIA and ACUA. You mayreach him at: [email protected].

18 / College & University Auditor

Fish TalesPurchasing card reviews are fun, as you justnever know what you’re going to find!

During a P-card review a few yearsago I ran across a purchase from a petstore; further research determined that 30fish were purchased. As the P-card is heldby a member of the advancement team inour Law School, I was more than a littleintrigued. I called the woman (with whomI have always had a great relationship)and asked her: “What’s up with the fish?”

It seemed like such an innocent ques-tion.

Her first reaction, as expected, was,“I knew you were going to call me aboutthat!” and then the whole truth came out.They had hosted a fund-raising dinnerand she had the great idea of making cen-terpieces of clear vases filled with waterand colored glass pebbles, with a couplelong flower stalks, with each one having acolorful fish swimming around in it. Whata great idea! So the day of the event sheset up all the centerpieces, bought andinstalled the fish, and went home to dressfor the party. Now the story turns tragic:while she was home getting ready, she gota phone call from the caterers: The fishwere dying. One after another, floatingto the tops of the vases; still colorful, butnow dead.

She rushed back to school and com-menced fishing the carcasses out of thevases. (No, I did not ask how they weredisposed of, even though that could haveEPA implications!) Done barely in timefor the party to start, she said she wor-ried all evening that she might have missedone, and waited for someone to shriek,“There’s a dead fish in my vase!”

A Little HumorComing in theSpring 2003 Issue

Depositions & TestimonyWilliam C. Weaver, Ph.D., ForensicEconomist, University of Central Florida

Facilitating Organizational Change –From Review Through ProjectFollow-UpDonald Holdegraver, CPA, CFE

Risk Assessment and SellingInternal AuditVirginia Key, Internal Audit DirectorMontana State University

But the funniest part was something Ididn’t learn until months later when I madeher retell the story to a group of people Iknew would enjoy it. As it turns out, thefish in question weren’t goldfish, as I hadassumed; they were “fighting fish.” Youknow, suspiciously like sharks.

Did I mention this was a Law Schoolfunction?

FALL 2002 / 19

The Making of a Star

By Frances Grogan, CPA, managing director and Kim Turner, CPA, associate director, Texas Tech University

Continued on page 20

A Star Is BornTexas Tech brought its new brochure andfraud poster to the “Marketing the Inter-nal Audit Function” session of ACUAin Salt Lake City for the announced“show and tell.” We knew we had a win-ner (had there been a contest), but wewere not prepared for the attention thatthe poster received. The story behind theposter and its creation is almost as inter-esting as the poster itself. Some thingsjust seem to create themselves when thereis a need for them. Our poster and bro-chure did just that.

The Texas Tech Office of InternalAudit and Consulting has investigatedtwo major frauds during the past fiscalyear. Hundreds of thousands of dollarshad found their way into the pockets ofembezzlers rather than into universitybank accounts. As a result, cash controlsand fraud prevention have come to theforefront of the administrators’ minds aswell as auditors. Maybe that is the reasonwe sat up and took notice during a pre-sentation our News and Publications de-sign group made in a recent Board ofRegents meeting. They were showingsome of their award winning designs andhow they were being used across campusto impart necessary information. Someof their posters were receiving such un-expected attention they could not keep themon the bulletin boards. Students were rip-ping them off to hang in dorm rooms andapartments.

We started thinking that as a part of alarge university, essentially a conglomer-ate of small businesses, we had a giantresource at our disposal we would haveto pay mega bucks for in the private sec-tor. Our immediate thought was Newsand Publications could help us produceattractive audit reports or maybe help usmake our existing brochure a little slicker.In a meeting with the University CFO andthe VP for Operations discussing the lat-est fraud and ways we could address fraudprevention or early detection, an idea startedbuilding in our heads. Most fraud is dis-covered via tips, so why not encourage thegeneral campus community at the source ofthe problems to call in those tips? Postersin all cash handling offices could alert theentire community of their responsibility ofreporting suspicious behavior under theuniversity’s fraud policy. However, whowould read a boring poster talking aboutfraud policies and reporting thieves? Theproverbial light bulb clicked. We knew thatthis was a project for our News and Publi-cations design group. We mentioned thatpossibility in the meeting. The CFO toldus (knowing her pockets are deeper than

ours) if we could get it put together, theoperations division would underwrite aposter.

It helps to make friends across the cam-pus. When we approached the vice chan-cellor of News and Publications about thepossibility, she agreed to put her designgroup on it, even offering to provide theirservices free of charge. The only cost (tothe CFO) would be for printing. Thevice chancellor also agreed to turn ourdepartmentally published brochure into aprofessional publication for only the costof printing. We felt certain there wouldbe a limit to the generosity of the CFO,so we decided to dig into our budget forthe brochure cost.

Editor’s Note: To see the poster, goto Texas Tech’s Web site: http://www.ttuhsc.edu/pages/audit/index.html.The poster can be viewed under the fraudpolicy link there.

Our audit staff member, Doug Krause,volunteered to work with the design team.After meeting with the design group headand discussing what we wanted and why,the project was assigned to a junior staffdesigner. When we met for a second timeto see the first proof, we were totally blownaway by the attention-grabbing creativity.The designer said when her group hadbrainstormed, they decided fear of reper-cussions would be the biggest factor keep-ing people from reporting suspicious be-havior, particularly if their supervisor was

Frances Grogan Kim Turner

20 / College & University Auditor

The Making of a StarContinued from page 19

involved. Therefore, they emphasized theTexas Whistleblower Act, which assureswould-be informants that they would beprotected from loss of job or any otherretaliation by Texas Tech by followingthrough on their responsibility to reportfraud. The design team decided to makethe brochure and the poster companiondocuments in order to keep our imageconsistent. What had started as a fraudprevention project was turning into a top-notch marketing tool as well.

By taking advantage of university re-sources and reaping the benefits of yearsof relationship-building, we kept theproject affordable. The cost of enoughposters to hang in all critical officesacross all campuses (and wallpaper acouple of those offices, as we have threat-ened to do) was around $1,000; the costof enough brochures to spread around lib-erally for at least two years was around $750.

Like Noah Preparingfor the FloodWhile the posters and brochures were inproduction, we had to think about howour office would handle the potentialphone calls, letters and drop-in visits wewould receive as a result of our new cam-paign. As a first step, we developed a briefinformation (intake) form for our audi-tors to use when talking with a concernedstudent, employee or outside party. Alldepartment members were trained to takethese visits or calls. The form is designedas a simple tool to help auditors remem-ber to ask for pertinent information.

Our procedures include:• Recording on the information (intake)

form as many details as possible.• Ascertaining whether the suspicions

have been reported to others (super-visor, another department, universitypolice or local law enforcement).

• Evaluating the courses of action if priorreports have been made to others.

• Assuring confidentiality of complain-ant to fullest extent possible.

• Advising callers who are employeesof the protections under the TexasWhistleblower Act.