chap 9 · web viewwork-in-process—goods in the process of being manufactured finished...

TRANSCRIPT

Chapter 8: Cost-Based Inventories and Cost of Sales

Suggested TimeCase 8-1 Ashwin Book Corporation

8-2 Siegfried Air Control Ltd.8-3 Centennial Farms

Assignment 8-1 Inventory cost—items to include in inventory... 108-2 Inventory cost—items to include in inventory... 208-3 Inventory discounts and rebates......................... 108-4 Inventory policy issues...................................... 208-5 Accounting policies........................................... 308-6 LC/NRV............................................................. 108-7 LC/NRV—direct writedown vs. allowance....... 208-8 removed 8-9 LC/NRV—allowance method (*W).................. 208-10 LC/NRV—two ways to apply............................ 208-11 LC/NRV—income effects................................. 158-12 LC/NRV and foreign currency—income effects 258-13 Loss on purchase commitment........................... 108-14 Inventory—error correction............................... 158-15 Inventory error................................................... 58-16 Inventory-related errors..................................... 108-17 Gross margin method......................................... 108-18 Gross margin method (*W)............................... 208-19 Retail inventory method..................................... 158-20 Retail inventory method (*W)........................... 308-21 Gross margin and retail inventory methods....... 358-22 Inventory concepts—recording, adjusting,

closing, reporting....................................... 358-23 Cash flow statement........................................... 208-24 Perpetual inventory—FIFO vs. average cost..... 358-25 Inventory cost methods (*W)............................. 208-26 Inventory cost methods...................................... 408-27 Inventory cost methods...................................... 308-28 Inventory policy comparison............................. 30

*W The solution to this exercise/problem is on the text Web site and in the Study Guide. This solution is marked WEB.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-1

Questions

1. Inventory is important because it is a material high-risk current asset, and, if properly managed, inventory systems can be used to enhance profits.

2. Trading EntityMerchandise Inventory—Goods on hand purchased for resale.

Manufacturing EntityRaw Materials Inventory—Goods held for manufacturing productsWork-in-Process—Goods in the process of being manufacturedFinished Goods—Goods completed by the manufacturing processProduction Supplies Inventory—Items needed to perform plant maintenance.

Both entities could have miscellaneous inventories (e.g., office supplies)

3. a Include in inventoryb Excludec Exclude*d Include**e Includef Include***g Includeh Include

* Do not include in regular inventory. If the goods can be returned make no entry. If the goods cannot be returned, the purchaser should include the damaged goods in a special inventory—damaged goods.

** Inclusion or exclusion depends on the provisions of the sale agreement. This answer assumed returns are allowed.

*** Not yet unrevocably sold; answer may depend on past history of sales (and revenue recognition policy).

4. The purpose of the LC/NRV rule is to avoid overstating the future economic benefit of inventory.

5. Raw material is used in production of a final product. If the NRV of the final product is greater than the total cost of production, the full cost of the raw materials will be recovered in the final sale. Therefore, the raw material should not be written down.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-2 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

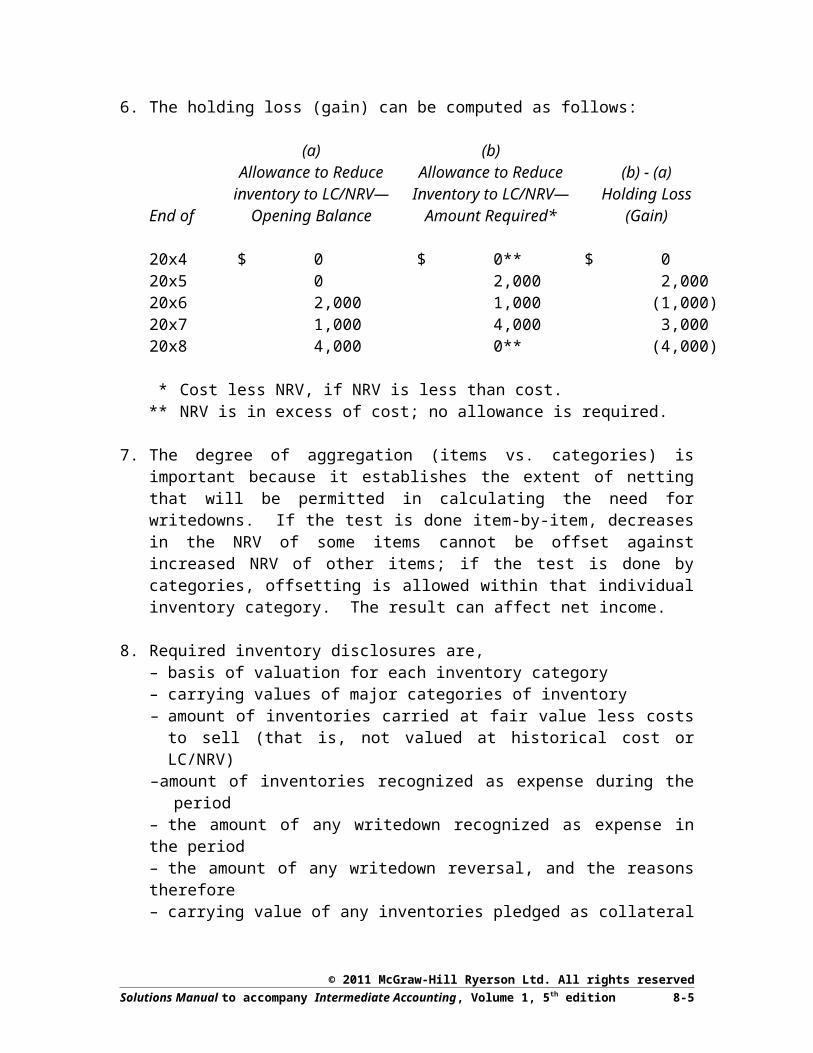

6. The holding loss (gain) can be computed as follows:

(a) (b)Allowance to Reduce Allowance to Reduce (b) - (a)

inventory to LC/NRV— Inventory to LC/NRV— Holding LossEnd of Opening Balance Amount Required* (Gain)

20x4 $ 0 $ 0** $ 020x5 0 2,000 2,00020x6 2,000 1,000 (1,000)20x7 1,000 4,000 3,00020x8 4,000 0** (4,000)

* Cost less NRV, if NRV is less than cost.** NRV is in excess of cost; no allowance is required.

7. The degree of aggregation (items vs. categories) is important because it establishes the extent of netting that will be permitted in calculating the need for writedowns. If the test is done item-by-item, decreases in the NRV of some items cannot be offset against increased NRV of other items; if the test is done by categories, offsetting is allowed within that individual inventory category. The result can affect net income.

8. Required inventory disclosures are,– basis of valuation for each inventory category– carrying values of major categories of inventory– amount of inventories carried at fair value less costs to sell (that is, not valued at

historical cost or LC/NRV)–amount of inventories recognized as expense during the period– the amount of any writedown recognized as expense in the period– the amount of any writedown reversal, and the reasons therefore– carrying value of any inventories pledged as collateral

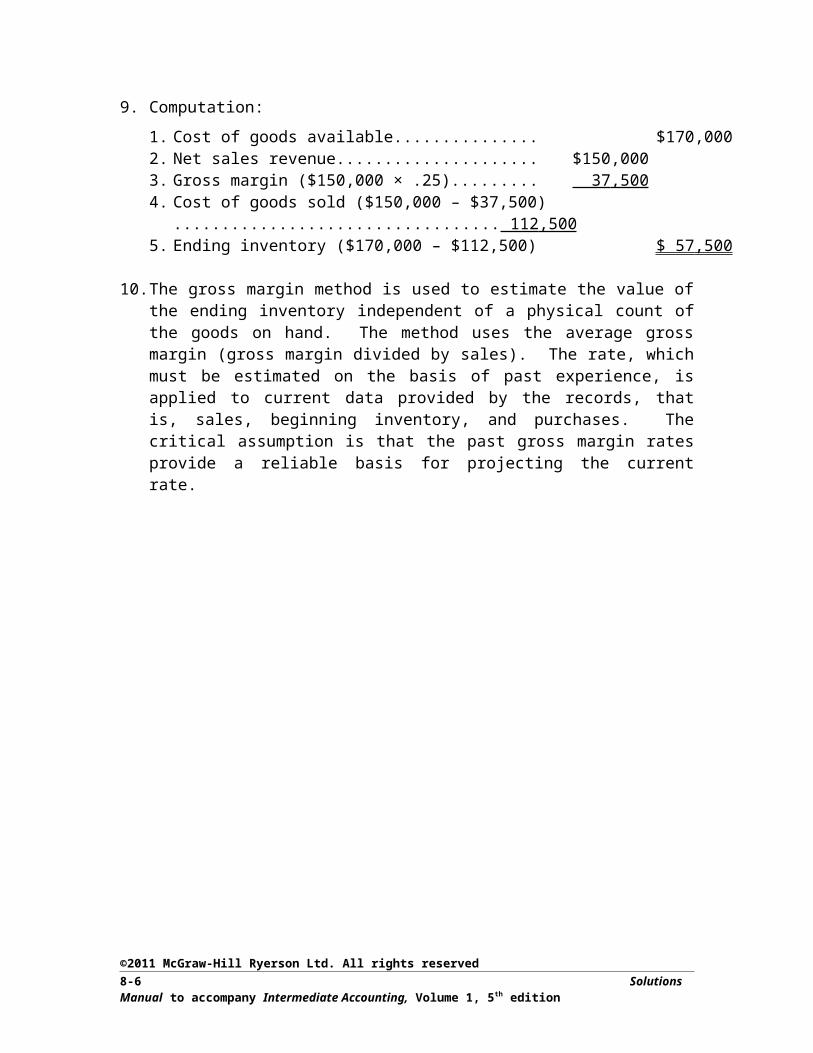

9. Computation:

1. Cost of goods available...................................................... $170,0002. Net sales revenue............................................................... $150,0003. Gross margin ($150,000 × .25).......................................... 37,5004. Cost of goods sold ($150,000 – $37,500).......................... 112,5005. Ending inventory ($170,000 – $112,500).......................... $ 57,500

10. The gross margin method is used to estimate the value of the ending inventory independent of a physical count of the goods on hand. The method uses the average gross margin (gross margin divided by sales). The rate, which must be estimated on the basis of past experience, is applied to current data provided by the records, that is, sales, beginning inventory, and purchases. The critical assumption is that the past gross margin rates provide a reliable basis for projecting the current rate.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-3

11. The approach of the retail method of estimating inventories is to account for merchandise activities at retail and cost. From such data, a cost/retail ratio is used to convert retail amounts to cost. It is necessary to maintain a record of the beginning inventory, purchases, and adjustments thereto at both cost and retail. With this data, the average relationship between cost and retail (i.e., the cost ratio) can be computed on the basis of actual data for the period. The total goods available for sale at retail is reduced by the sales amount, giving the ending inventory valued at retail prices. The cost ratio is then applied to the retail value to provide the estimated ending inventory at cost.

12. The year-end inventory cut-off is important because it affects inventories, receivables, revenues and cost of sales. The goods shipped must correspond to the goods invoiced during the periods. If goods are invoiced to the customer (and included in the sales revenue) but not shipped until after the cut-off date (and therefore not included in cost of sales), matching will not be achieved and net income will be misstated.

13. NRV value is an acceptable valuation basis for biological harvests and primary products, and also for extracted minerals and mineral products. This is permitted only if (1) there is an active market for the commodity or product and (2) NRV value is widely-used as the inventory valuation method in that industry.

14. Under a periodic inventory system, the ending inventory each period is determined by a physical count; the unit costs are then applied by using one of the inventory cost flow policies. Cost of goods sold is calculated only after a physical count.Under a perpetual inventory system, all receipts and issues of inventory items are directly recorded in detailed inventory records so that a continuous inventory balance is maintained in the records. Cost of goods sold is recorded after each sale. Any one of the inventory cost flow policies may be used.Perpetual systems are more expensive to maintain, and are common when an entity needs to know detailed information on a daily basis regarding specific inventory units and costs. It is also more common when accurate interim (monthly) results are needed. Otherwise, periodic systems are used.

15. A perpetual inventory system does not eliminate the need for a physical count of inventories. To verify the accuracy of the perpetual inventory records, it is necessary that physical inventory counts be taken from time to time. This should be done annually or on a rotation basis throughout the year. Any errors found in the perpetual inventory records are corrected so that such records agree with the physical count.

16. Cost of goods sold can be measured using the following cost flow assumptions:

a) Specific identification – Cost of specific items sold is expensedb) FIFO – Oldest costs are expensed, recent purchases retainedc) Average cost – Average cost of purchases is used to value inventory

and cost of goods sold.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-4 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

When prices are rising, FIFO will always result in the highest net income, as old cheaper units are expensed. Specific identification may have the same result, but not “always”, depending on the exact units sold. Average cost blends the various levels of cost, which yields a higher inventory level and lower net income than FIFO.

17. The weighted-average method is used with a periodic inventory system. A weighted-average is computed at the end of the period by using total purchase costs, beginning inventory costs, and the number of units in the beginning inventory and purchases. It is used because it is theoretically sound and systematic, and it is relatively easy to apply when the periodic inventory system is used.

The moving-average method is used with a perpetual inventory system. A new average is computed after each purchase to allow recognition of cost of goods sold at the most recent average cost after each sale.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-5

Cases

Case 8-1 — Ashwin Book Corporation

Overview

This case raises several issues, some of which are obvious and some are less obvious. The issues are:

Inventory valuation Revenue recognition Expense recognition Intangible assets and deferred charges

If TTI acquires ABC, ABC will need to change its policies to conform with IFRS since ABC will be consolidated into TTI’s results, and therefore must follow IFRS.

There is some conflict between the accounting policies that ABC will have to adopt in the future and TTI’s immediate objective to establish a bid price based on earnings projects. A bid price would be based on TTI’s evaluation of (1) earnings potential and (2) volatility of earnings and/or cash flows. High earnings is good, but volatility is bad—the risk vs. return trade-off

Report to Mrs. O’Malley

Dear Mrs. O’Malley:

I am pleased to report my findings concerning Ashwin Book Corporation’s accounting policies and practices. I believe that it will be necessary to make some adjustments to ABC’s reported numbers for 20X3, and take some additional factors into account when we project the company’s earnings into the future in order to establish a bid price.

One overriding consideration is that ABC, as a private company, seems to use an amalgam of Canadian accounting standards for private enterprises and some eclectic accounting policies that appear to be rather unorthodox. In effect, ABC uses a disclosed basis of accounting. If we acquire ABC, the company will need to change its accounting policies to conform with IFRS, since we use IFRS and we will need to consolidate ABC.

My discussion of the major issues is as follows:

a. Inventory valuation. ABC develops and produces its own books. All of each title’s development, production, and printing costs are included in inventory and allocated over the number of copies in each editions’ initial press run. The result is that the first print run has a huge unit cost while succeeding press runs (if any) bear only the cost of that particular print run. As a result, cost of goods sold will be very high for the initial run, quite likely yielding a negative gross margin for that initial run, even for a very successful book. For performance evaluation and for earnings prediction, these numbers are apt to be very misleading. As well, loading all of these costs into the

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-6 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

inventoriable cost will usually result in an inventory value that is significantly higher than net realizable value. Therefore, the development costs should be removed from inventory and accounted for separately.

b Development and production costs. We have a dichotomy in this regard. For financial reporting purposes, ABC will have to change their accounting policy for development costs to accord with IFRS, once we acquire them. One option is to expense development costs when they are incurred—even for historically successful books. An edition’s success may not be predictable with assurance, because new competitors enter the market regularly.

On the other hand, spreading the development and production costs over the 3-year life span of the book will assist with our prediction of future earnings (on which we base the bid price) as well as ongoing evaluation of ABC’s management. However, it is questionable as to whether these costs can properly be considered as an intangible asset, and thereby capitalized and amortized. IFRS discourages treating expenditures for new products as intangible assets (IAS 38, paragraph 69). Every new edition is, in effect, a new product, and therefore I recommend that ABC’s policy for these costs should be to expense them when incurred.

For our analytical purposes in developing a bid price, however, I suggest that we remove development and pre-production costs from inventories in recent prior years and amortize them over 3-year periods just so we can discern the underlying earnings. Then we can look at the cash flow volatility over the years to measure the risk potential of the erratic production levels.

c. Revenue recognition. ABC recognizes revenue when books are shipped. However, there is a 6-month official return policy that is unofficially stretched for college and university bookstores, which account for 90% of total sales. The return rate seems to be difficult to predict. If it is not feasible to make a reliable estimate of the return rate, either overall for book-by-book, revenue recognition probably should be deferred until the 6-month “official” return period has ended.

d. Supporting material for instructors. The cost of providing free supporting materials for instructors can be considerable. They have no inventory value in the usual sense because their net realiable value is zero (except to students who would love to get their hands on solutions manuals). The significant cost of these items suggests that instead of inventorying the costs, ABC should instead defer some of the revenue and treat each book’s sale as really being a multi-deliverable contact: (1) a book delivered to the students when they buy them, and (2) supporting material prepared and made available for instructors. While there is no measurable value for the second deliverable, an allocation of revenue could be based on the relative costs of the two deliverables. ABC shouldn’t be pouring more money into production and support than can be received in revenue. Such a revenue allocation would give ABC managers a better idea of the “real” price that they should be charging for the book.

e. Inventory valuation of returned books. ABC restores returned books to inventory at the unit cost they originally bore. This has two problems: (1) the original assigned cost is too high, as discussed above, and (2) if large quantities of a book are returned,

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-7

it probably indicates that the book is unsuccessful and therefore that its net realizable value is much lower than the original unit cost. We will need to determine how much of the current inventory is comprised of returned books, and probably write off those books for our estimation process.

f. Inventory of old editions. An inventory of old editions should not be assigned any value as assets. By definition, they are obsolete, even if there may be some residual sales. By retaining some inventory at normal cost, ABC management may be tempted to retain more than necessary in order to avoid depressing earnings by a write-down.

g. Website development costs. It is doubtful that these costs would qualify as an intangible asset under IFRS. The success of the website is not predictable with reasonable assurance. The costs should be expensed when incurred. However, we should take into account in our projects that delivering support material electronically will significantly reduce the cost of printing and distributing instructors’ supporting materials. That cost reduction may be offset, however, by the necessity to put more resources into development of electronic learning aids in order to keep up with the competition.

h. Sales discounts. The company currently is charging “discounts taken” on accounts receivable to interest expense. Instead, the discounts should be deducted from revenue.

I hope that I have identified the major issues that I see with ABC accounting. If you wish me to pursue any of these matters further, I will be happy to visit the company again and take a closer look at their accounting records.

Sincerely,

Ian Fenwick

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-8 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Case 8-2 — Siegfried Air Control Ltd.

Overview

This case focusses on inventory valuation and related aspects such as (1) lower of cost or NRV, (2) unrealized foreign currency gains/losses and hedges thereof, and (3) revisions of cost estimates on uncompleted projects. It provides a overview of material covered in Chapter 3 (other comprehensive income) and Chapter 6 (revenue recognition for contracts). The issues presented in the case can be treated individually.

1. The company seems not to be including any overhead in the cost of manufacturing and inventory. Overhead should be charged as a manufacturing (and inventory) cost, not only direct materials and direct labour. Overhead should be charged to inventory on a normal-capacity basis, with no increase in charges due to idle capacity.

2. SAC has an unrealized foreign currency gain of $156,000. On the balance sheet date, the account payable must be restated. However, since the Euro payable has been hedged, the gain cannot be recognized in income. Instead, the unrealized gain is credited to accumulated other comprehensive income and reported as a component of other comprehensive income for 20X5.

3. The practice of charging warranty costs to expense when incurred may be justified when the costs are immaterial or are difficult to predict. Historically, that seems to have been the case. With the new units, however, it seems that a significant portion of the sales revenue is actually going to providing servicing under provisions of the warranty. This suggests that the company should take an alternative approach and start deferring a portion of the sales revenue and allocating it over the warranty period. Incurred warranty costs would then be recognized directly as expenses on the income statement, deducted from the deferred revenue recognized in the period. This change would be a change in accounting policy, however, and should be implemented in the next fiscal year, not in the current year.

Based on experience to date, SAC should estimate the costs of servicing under warranty for the remaining warranty period of Sigmunds (the new model) that installed as of the end of 20X5.

4. The older model (Erda) is about to become obsolete by legislation in Ontario. Some may still be sold in Ontario prior to the effective date of the new legislation, and it still can be sold in the U.S. at a reduced price (wholesale). The Erdas must be written down to lower of cost or NRV. The writedown should be 10% of the current book value plus the estimated average cost of shipping the units to the the U.S. Although some units may still be sold domestically, they probably will need to be discounted as well. Therefore, all remaining Erda inventory should be written down.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-9

5. There are two issues concerning this project: (1) whether to recognize any revenue and profit from this contract, and (2) the value of inventory relating to this project at the end of the year.

The original estimate was that the project would earn SAC a profit of $200,000 (that is, $1,200,000 contract price minus $1,000,000 estimated cost)The project supervisor estimates that the project is 40% complete, which implies the possibility of recognizing 40% of the profit. However, estimated total costs have risen to $1,150,000, leaving a potential profit of $50,000. Of the estimated total costs, SAC has incurred $600,000, or 52% of estimated total costs. The 40% estimate is based on physical work (i.e., labour cost). Either percentage could be used to estimate the proportion of profit to the recognized in 20X5.

The company has incurred costs of $600,000 so far, including the major materials cost of the compression and air-handling equipment. There is no indication of whether overhead is included in the $350,000 of non-equipment costs.* If not, then overhead should be added to that amount. The question then becomes whether the full estimated cost of the project can be recovered. If more than $50,000 in overhead is added to the inventory amount, the company would suffer a loss on the project and the inventory should be written down to an amount equal to $1,200,000 minus the estimated cost to complete.

* That is, the $600,000 in total costs minus the $250,000 in equipment costs.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-10 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Case 8-3 — Centennial Farms

Dear John:

This letter answers the questions you had concerning the banker’s request for information.

You now use your financial statements as a basis for measuring your performance and for filing your income tax returns. Your banker uses the financial statements in two ways. First, he is interested in predicting the cash flows from your operations to judge whether you can meet your loan payments on time. Second, he is interested in the security or collateral you have available in case you default on the loan. These are the reasons why he is requesting the additional information.

You have an ethical responsibility to provide complete and accurate information, as well as the obligation to yourself to pay the minimum amount of tax annually, in legal compliance with the Income Tax Act.

Cash basis vs. accrual basis of accounting

Your banker wants you to switch from a cash basis of accounting to an accrual basis. In the past, you have prepared your financial statements on a cash basis because this is acceptable for your tax returns. However, there are problems in using the cash basis to evaluate performance because it does not take into account items such as your accounts payable or accounts receivable at the end of the year.

The accrual basis of accounting provides information to the banker that is useful in predicting your cash flows and debt capacity. It tries to match your expenses to the revenue you generate in a period. Therefore, it considers such items as accounts receivable, inventory and accounts payable at the end of the year. This information is necessary to predict your future cash flows and will be helpful to you when you evaluate the performance of the farm for the year.

Accrual accounting is used by most profit-oriented companies. Therefore, if you switch to accrual accounting, your banker will be able to compare your operations with those of other companies. However, if you switch to accrual accounting for the banker but continue to prepare your financial statements on a cash basis for taxes, we will have to prepare two sets of financial statements.

I recommend that:

• we provide your statements on an accrual basis, as requested by the bank, and• we file your tax returns using accrual accounting (but see the next comment).

By following these two recommendations, you will avoid the expense of our having to prepare two financial statements.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-11

We should first, however, make sure that it won’t result in paying more tax, sooner. If that is the case, the expense of preparing two sets of financial statements would be justified and is quite ethical, as the different statements are used for different purposes.

NRV value vs. historical cost

The banker’s second request is that you provide market values so that he can evaluate the security behind your loan. You are accustomed to providing information on an historical basis. There are advantages and disadvantages to both approaches.

Using market values has some advantages. Historical costs are difficult to accumulate because the costs – for example, labour, feed and overhead – are subjective. Unlike historical costs, market values for cattle are easy to obtain, as cattle are a commodity and commodity values are widely published. You would find market values helpful in evaluating your farm because they provide you with the current value of your investment. You would use the current value in judging the return you are receiving.

Market values currently are required for companies that report in accordance with international financial accounting standards (IFRS). Those companies are likely to be large corporate operations, perhaps international in scope, some of which may even be publicly-traded enterprises in their home countries. Although there is no need for you to follow IFRS, the fact that IFRS requires market valuations for all biological assets means that market values (technically, net realizable values) have become the accepted standard for reporting. That may be one of the reasons that your banker wants you to report market values instead of historical costs. Also, the banker needs to know whether he can get his money back when you sell your cattle (or the milk from your cows). He doesn’t want to be putting more money into your farm than you can possibly pay back by selling your animals or animal products.

I recommend that we use market values from now on, not only to satisfy the banker, but also so that you can see what your livestock is worth. Don’t worry, though—the tax people won’t tax you on increases in market value; they just want their share of the cash when you do sell milk or cattle.

Best wishes,Efrim Boris

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-12 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Assignments

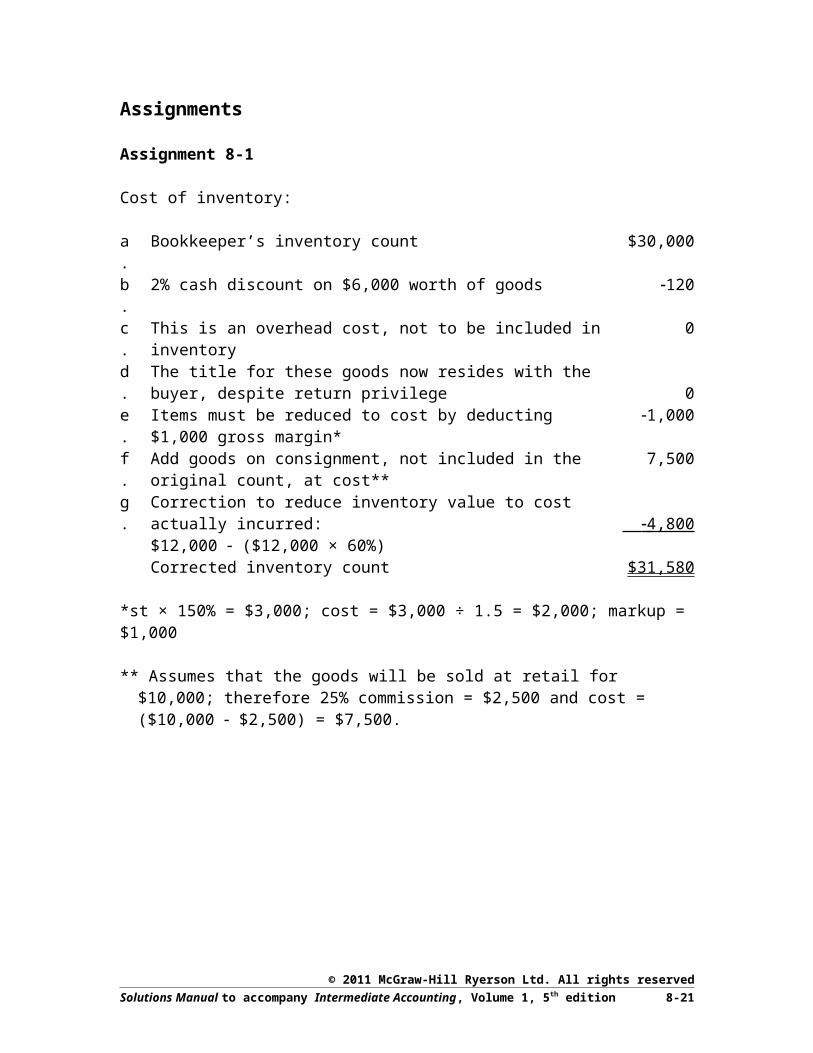

Assignment 8-1

Cost of inventory:

a. Bookkeeper’s inventory count $30,000b. 2% cash discount on $6,000 worth of goods 120c. This is an overhead cost, not to be included in inventory 0d. The title for these goods now resides with the buyer, despite return

privilege 0e. Items must be reduced to cost by deducting $1,000 gross margin* 1,000f. Add goods on consignment, not included in the original count, at

cost**7,500

g. Correction to reduce inventory value to cost actually incurred:$12,000 ($12,000 × 60%) 4,800 Corrected inventory count $31,580

*st × 150% = $3,000; cost = $3,000 ÷ 1.5 = $2,000; markup = $1,000

** Assumes that the goods will be sold at retail for $10,000; therefore 25% commission = $2,500 and cost = ($10,000 $2,500) = $7,500.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-13

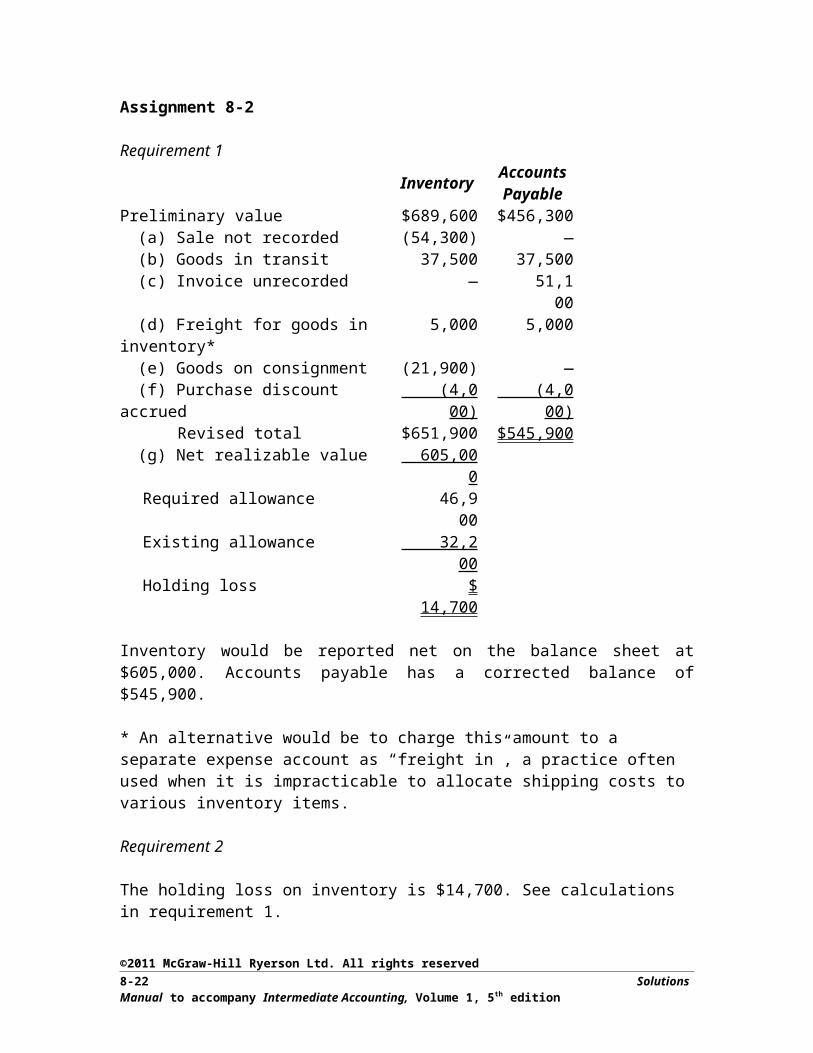

Assignment 8-2

Requirement 1

Inventory AccountsPayable

Preliminary value $689,600 $456,300(a) Sale not recorded (54,300) —(b) Goods in transit 37,500 37,500(c) Invoice unrecorded — 51,100(d) Freight for goods in inventory* 5,000 5,000(e) Goods on consignment (21,900) —(f) Purchase discount accrued (4,000) (4,000)

Revised total $651,900 $545,900(g) Net realizable value 605,000

Required allowance 46,900 Existing allowance 32,200 Holding loss $ 14,700

Inventory would be reported net on the balance sheet at $605,000. Accounts payable has a corrected balance of $545,900.

* An alternative would be to charge this amount to a separate expense account as “freight in”, a practice often used when it is impracticable to allocate shipping costs to various inventory items.

Requirement 2

The holding loss on inventory is $14,700. See calculations in requirement 1.

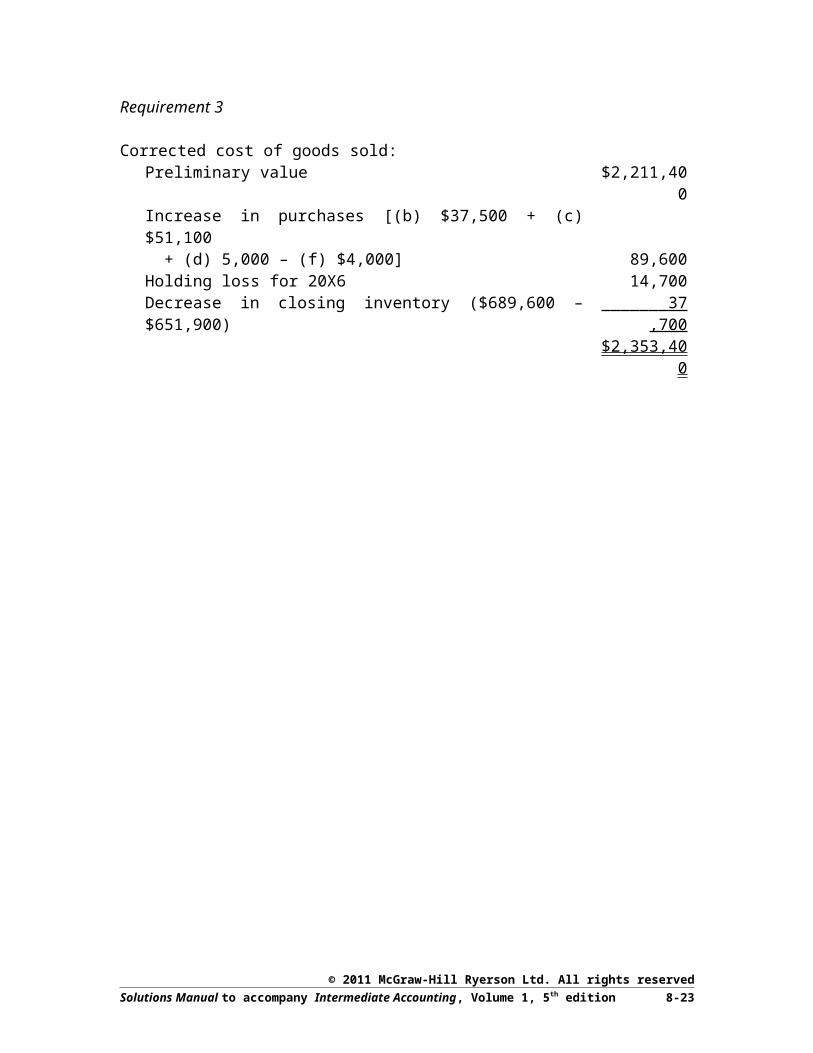

Requirement 3

Corrected cost of goods sold:Preliminary value $2,211,400Increase in purchases [(b) $37,500 + (c) $51,100 + (d) 5,000 – (f) $4,000] 89,600Holding loss for 20X6 14,700Decrease in closing inventory ($689,600 – $651,900) 37,700

$2,353,400

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-14 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

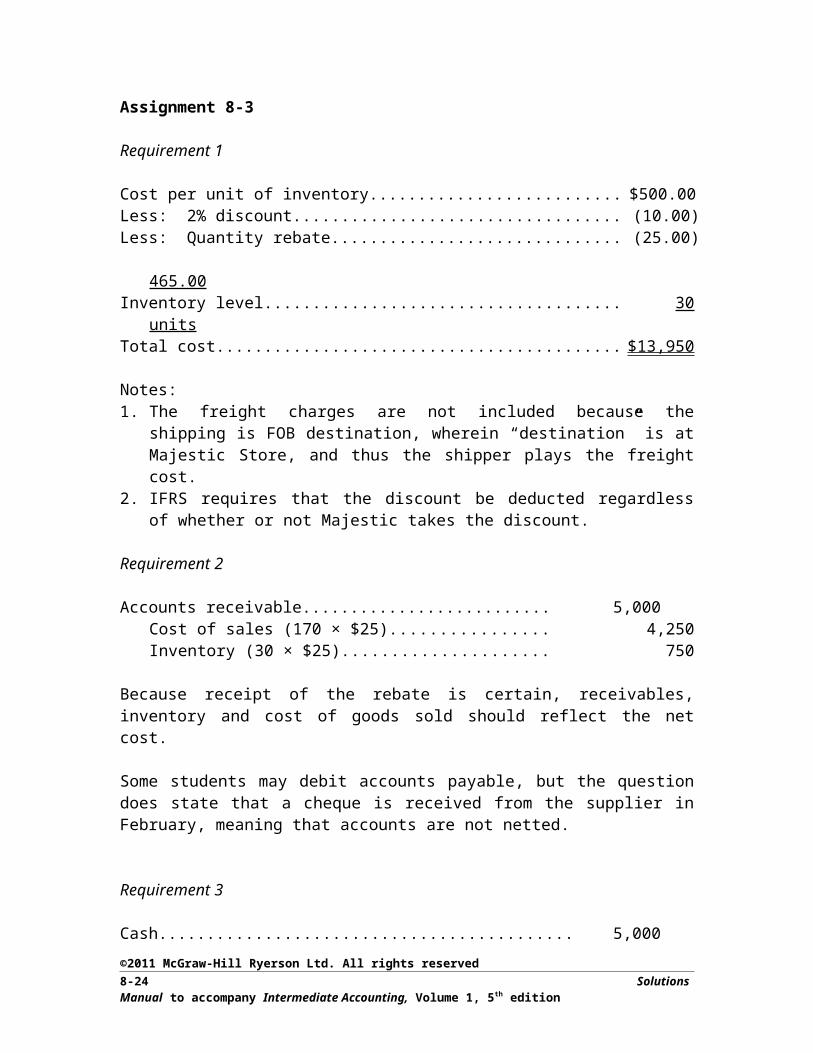

Assignment 8-3

Requirement 1

Cost per unit of inventory.................................................................................... $500.00 Less: 2% discount............................................................................................... (10.00)Less: Quantity rebate.......................................................................................... (25.00)

465.00Inventory level..................................................................................................... 30 unitsTotal cost.............................................................................................................. $13,950

Notes: 1. The freight charges are not included because the shipping is FOB destination,

wherein “destination” is at Majestic Store, and thus the shipper plays the freight cost.2. IFRS requires that the discount be deducted regardless of whether or not Majestic

takes the discount.

Requirement 2

Accounts receivable........................................................................... 5,000Cost of sales (170 × $25)............................................................ 4,250Inventory (30 × $25)................................................................... 750

Because receipt of the rebate is certain, receivables, inventory and cost of goods sold should reflect the net cost.

Some students may debit accounts payable, but the question does state that a cheque is received from the supplier in February, meaning that accounts are not netted.

Requirement 3

Cash.......................................................................................................... 5,000Accounts receivable (consistent with requirement 2)........................ 5,000

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-15

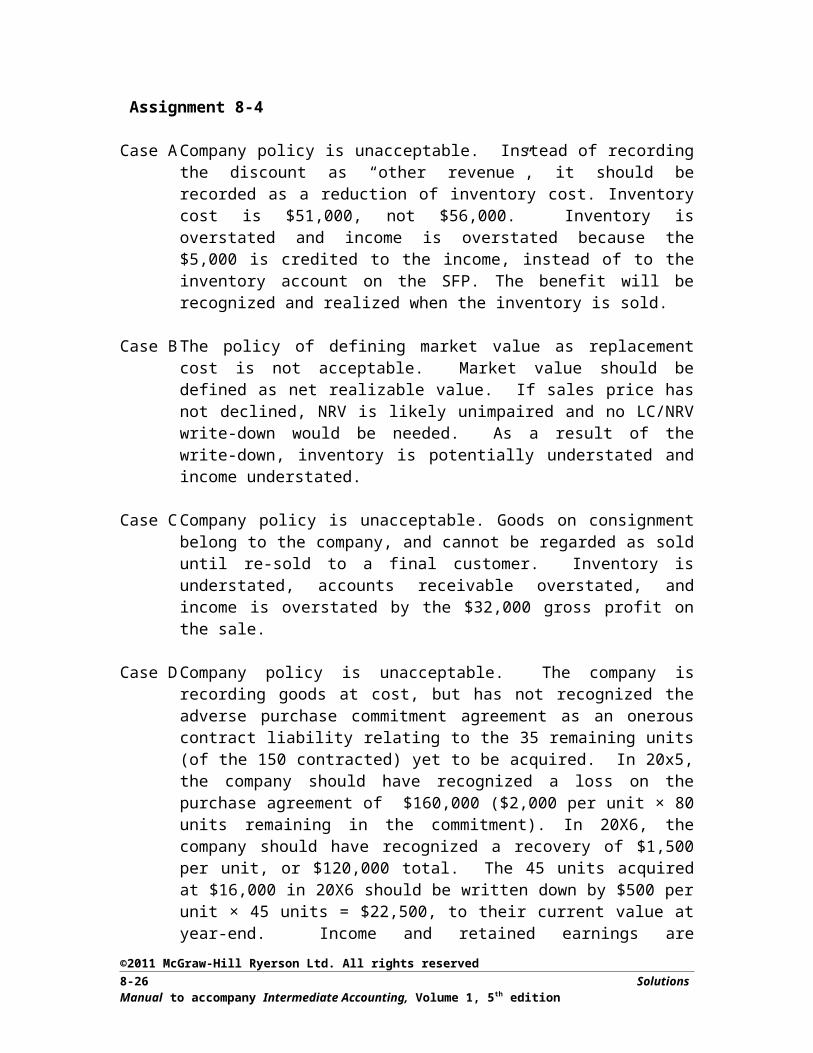

Assignment 8-4

Case A Company policy is unacceptable. Instead of recording the discount as “other revenue”, it should be recorded as a reduction of inventory cost. Inventory cost is $51,000, not $56,000. Inventory is overstated and income is overstated because the $5,000 is credited to the income, instead of to the inventory account on the SFP. The benefit will be recognized and realized when the inventory is sold.

Case B The policy of defining market value as replacement cost is not acceptable. Market value should be defined as net realizable value. If sales price has not declined, NRV is likely unimpaired and no LC/NRV write-down would be needed. As a result of the write-down, inventory is potentially understated and income understated.

Case C Company policy is unacceptable. Goods on consignment belong to the company, and cannot be regarded as sold until re-sold to a final customer. Inventory is understated, accounts receivable overstated, and income is overstated by the $32,000 gross profit on the sale.

Case D Company policy is unacceptable. The company is recording goods at cost, but has not recognized the adverse purchase commitment agreement as an onerous contract liability relating to the 35 remaining units (of the 150 contracted) yet to be acquired. In 20x5, the company should have recognized a loss on the purchase agreement of $160,000 ($2,000 per unit × 80 units remaining in the commitment). In 20X6, the company should have recognized a recovery of $1,500 per unit, or $120,000 total. The 45 units acquired at $16,000 in 20X6 should be written down by $500 per unit × 45 units = $22,500, to their current value at year-end. Income and retained earnings are overstated in 20x5 and liabilities are understated. Currently, inventory is overstated in 20x6; the impairment must be recorded.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-16 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

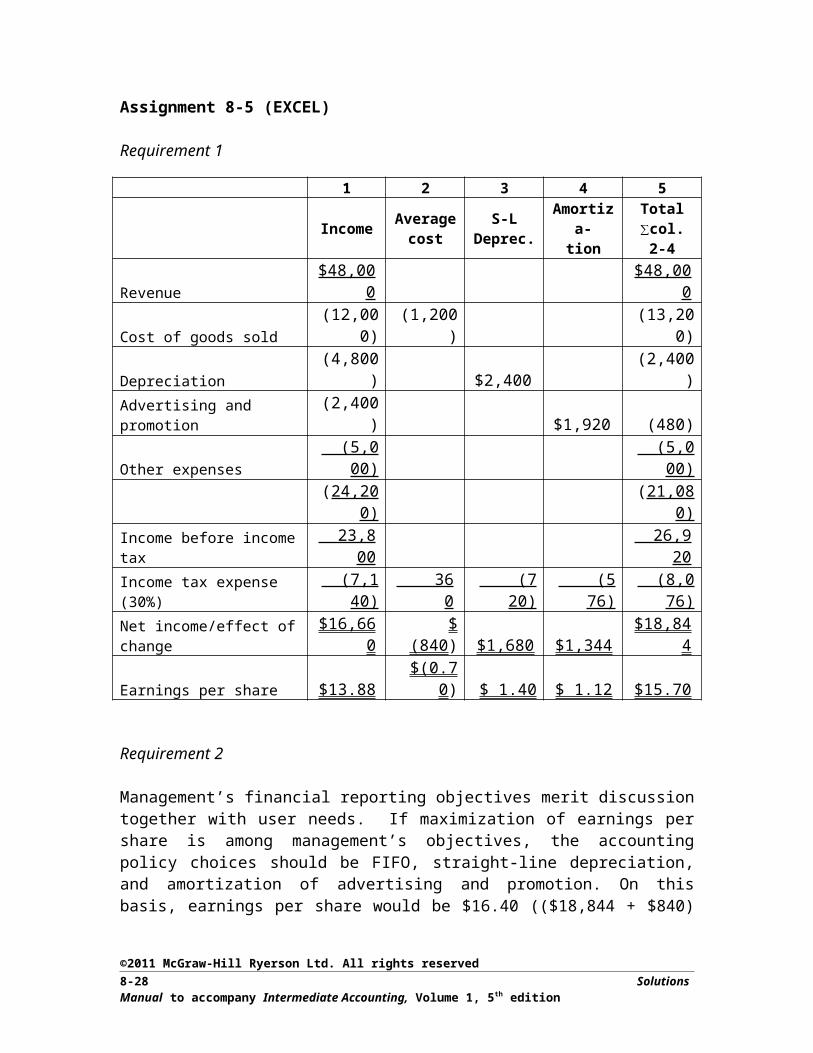

Assignment 8-5 (EXCEL)

Requirement 1

1 2 3 4 5

Income Average cost

S-LDeprec.

Amortiza-tion

Total∑col. 2-4

Revenue $48,000 $48,000Cost of goods sold (12,000) (1,200) (13,200)Depreciation (4,800) $2,400 (2,400)Advertising and promotion (2,400) $1,920 (480)Other expenses (5,000) (5,000)

(24,200) (21,080)Income before income tax 23,800 26,920Income tax expense (30%) (7,140) 360 (720) (576) (8,076)Net income/effect of change $16,660 $ (840) $1,680 $1,344 $18,844

Earnings per share $13.88 $(0.70) $ 1.40 $ 1.12 $15.70

Requirement 2

Management’s financial reporting objectives merit discussion together with user needs. If maximization of earnings per share is among management’s objectives, the accounting policy choices should be FIFO, straight-line depreciation, and amortization of advertising and promotion. On this basis, earnings per share would be $16.40 (($18,844 + $840) ÷ 1,200), an increase of approximately 18 % over the $13.88 amount reported in column (1).

Alternative accounting principles confer considerable latitude on management with respect to the specifics of income measurement. This latitude, however, is constrained by the accounting standard of consistency.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-17

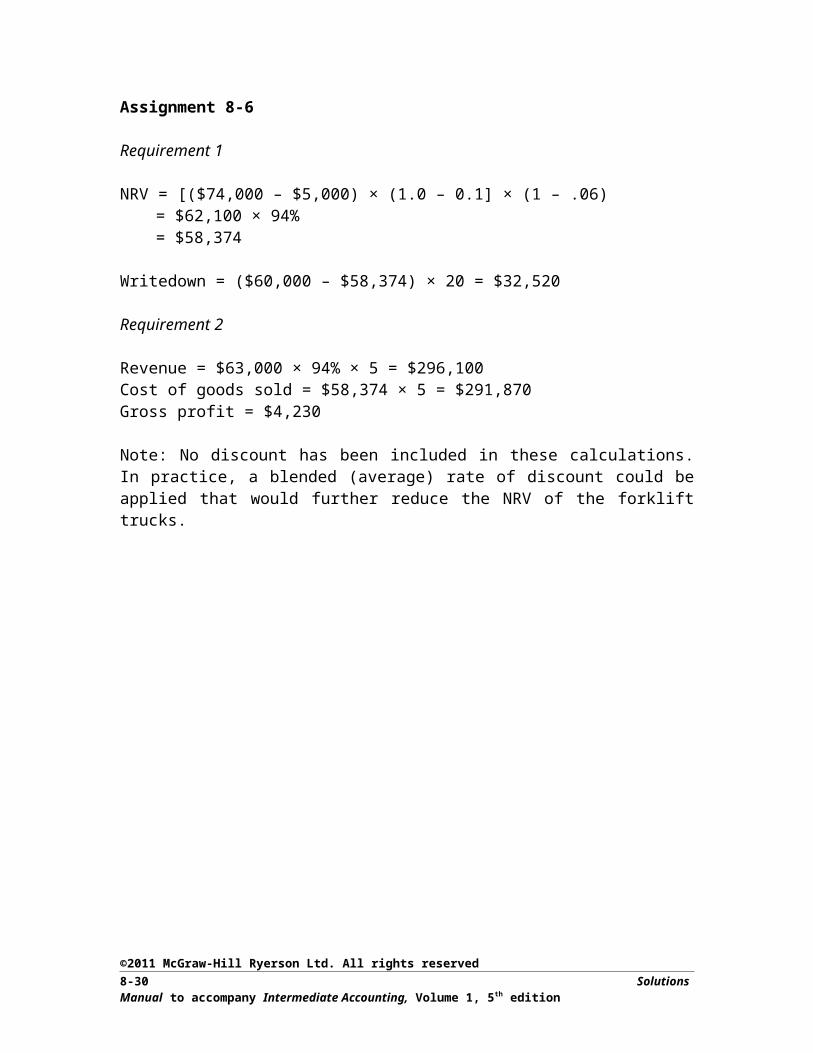

Assignment 8-6

Requirement 1

NRV = [($74,000 – $5,000) × (1.0 – 0.1] × (1 – .06)= $62,100 × 94%= $58,374

Writedown = ($60,000 – $58,374) × 20 = $32,520

Requirement 2

Revenue = $63,000 × 94% × 5 = $296,100Cost of goods sold = $58,374 × 5 = $291,870Gross profit = $4,230

Note: No discount has been included in these calculations. In practice, a blended (average) rate of discount could be applied that would further reduce the NRV of the forklift trucks.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-18 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

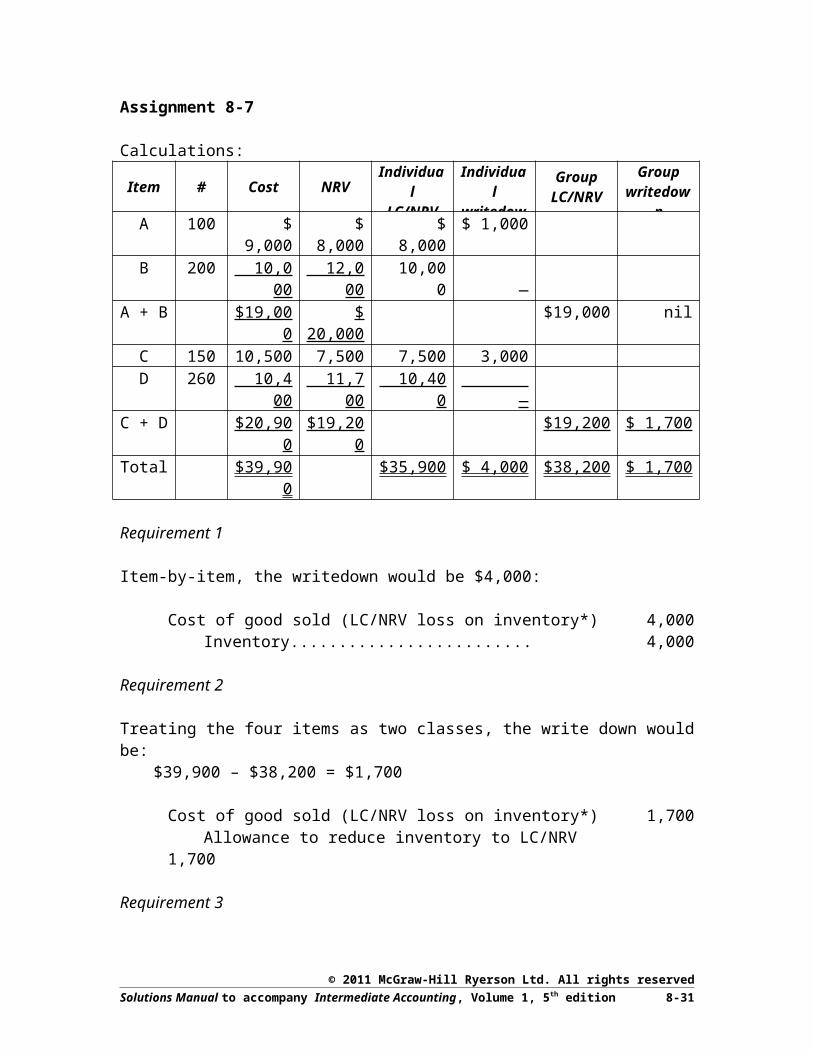

Assignment 8-7

Calculations:

Item # Cost NRV IndividualLC/NRV

Individual writedown

GroupLC/NRV

Groupwritedown

A 100 $ 9,000 $ 8,000 $ 8,000 $ 1,000B 200 10,000 12,000 10,000 —

A + B $19,000 $ 20,000 $19,000 nil

C 150 10,500 7,500 7,500 3,000D 260 10,400 11,700 10,400 —

C + D $20,900 $19,200 $19,200 $ 1,700

Total $39,900 $35,900 $ 4,000 $38,200 $ 1,700

Requirement 1

Item-by-item, the writedown would be $4,000:

Cost of good sold (LC/NRV loss on inventory*).............. 4,000Inventory.................................................................. 4,000

Requirement 2

Treating the four items as two classes, the write down would be: $39,900 – $38,200 = $1,700

Cost of good sold (LC/NRV loss on inventory*).............. 1,700Allowance to reduce inventory to LC/NRV............. 1,700

Requirement 3

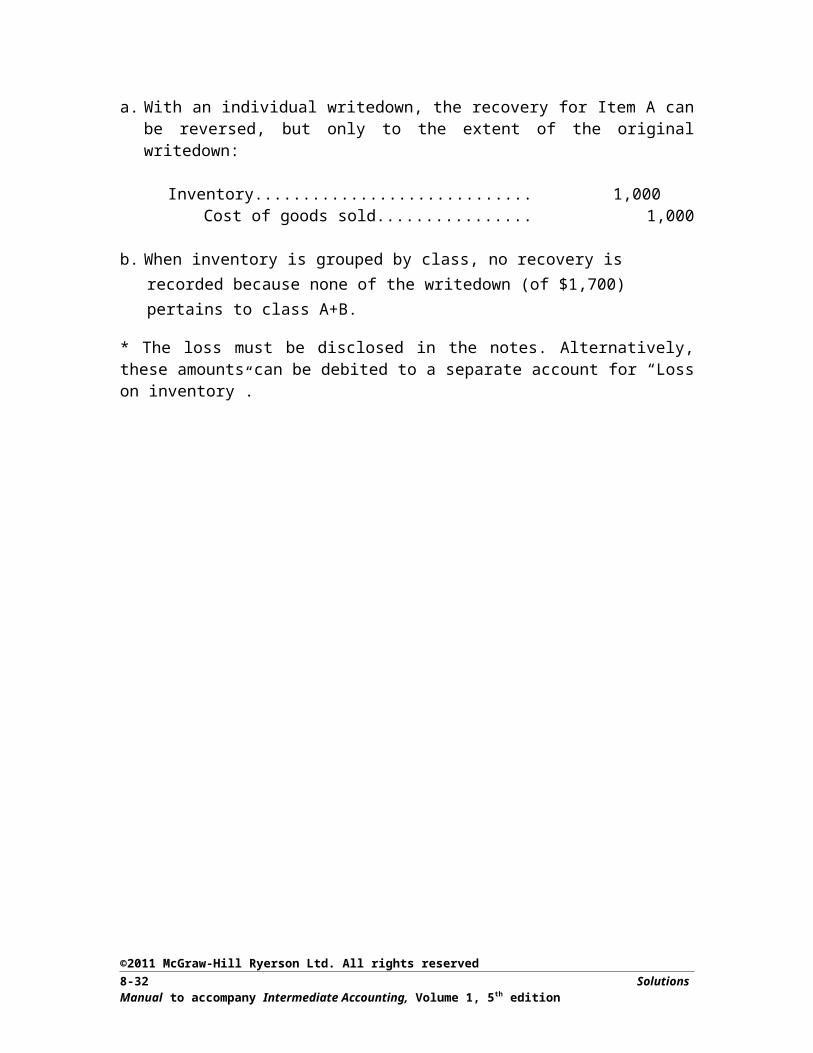

a. With an individual writedown, the recovery for Item A can be reversed, but only to the extent of the original writedown:

Inventory........................................................................... 1,000Cost of goods sold.................................................... 1,000

b. When inventory is grouped by class, no recovery is recorded because none of the writedown (of $1,700) pertains to class A+B.

* The loss must be disclosed in the notes. Alternatively, these amounts can be debited to a separate account for “Loss on inventory”.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-19

Requirement 4

The advantage of using an allowance is that the individual subsidiary inventory records do not need to be adjusted for the writedown (nor for any subsequent recovery in value). The allowance method is essential when LC/NRV is performed by inventory class rather than item-by-item, because there would be no way to make the detailed inventory records conform to the general ledger control account.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-20 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Assignment 8-8 - removed

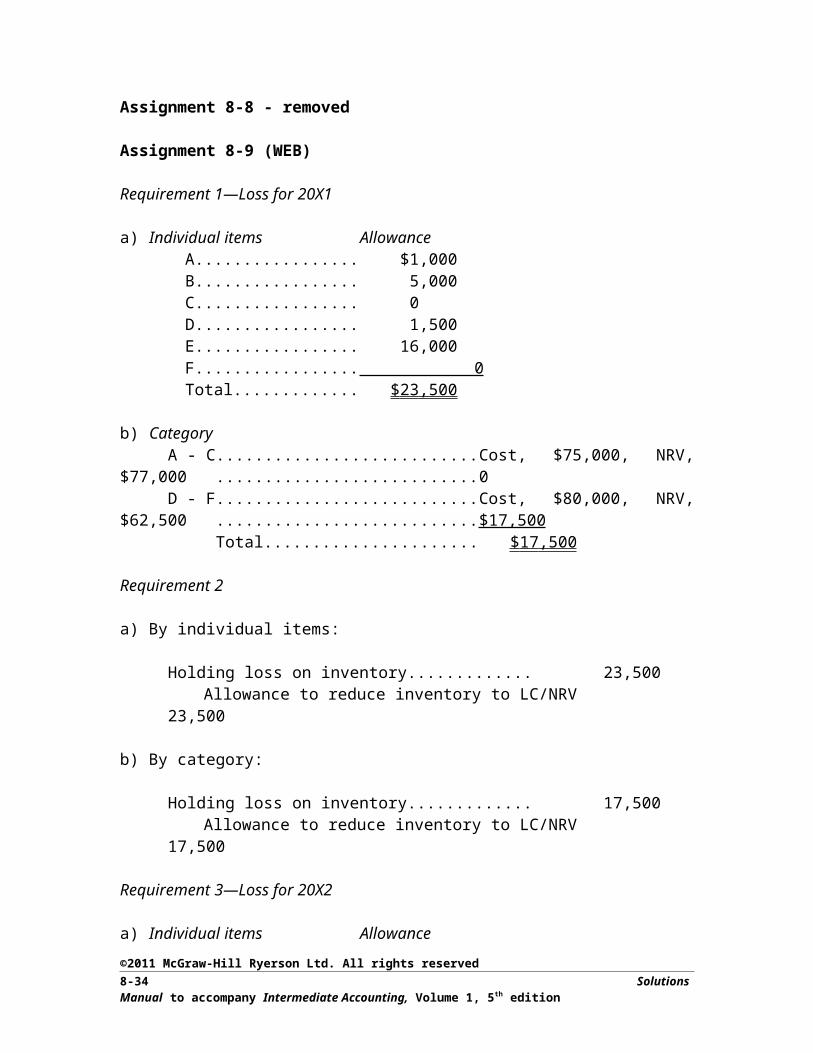

Assignment 8-9 (WEB)

Requirement 1—Loss for 20X1

a) Individual items AllowanceA........................................ $1,000B......................................... 5,000C......................................... 0D........................................ 1,500E......................................... 16,000F......................................... 0Total................................... $ 23,500

b) CategoryA - C Cost, $75,000, NRV, $77,000.................. 0D - F Cost, $80,000, NRV, $62,500.................. $17,500

Total......................................................... $ 17,500

Requirement 2

a) By individual items:

Holding loss on inventory................................................. 23,500Allowance to reduce inventory to LC/NRV............. 23,500

b) By category:

Holding loss on inventory................................................. 17,500Allowance to reduce inventory to LC/NRV............. 17,500

Requirement 3—Loss for 20X2

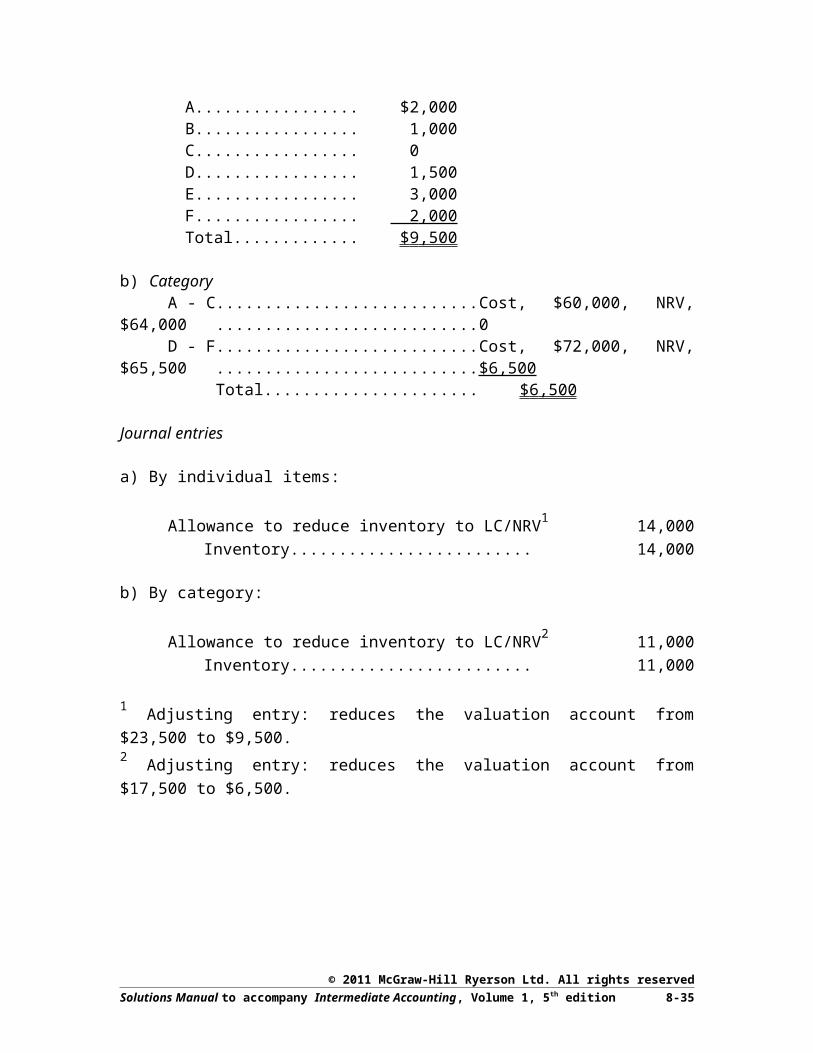

a) Individual items AllowanceA........................................ $2,000B......................................... 1,000C......................................... 0D........................................ 1,500E......................................... 3,000F......................................... 2,000Total................................... $ 9,500

b) CategoryA - C Cost, $60,000, NRV, $64,000.................. 0D - F Cost, $72,000, NRV, $65,500.................. $6,500

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-21

Total......................................................... $ 6,500

Journal entries

a) By individual items:

Allowance to reduce inventory to LC/NRV1 ................... 14,000Inventory.................................................................. 14,000

b) By category:

Allowance to reduce inventory to LC/NRV2.................... 11,000Inventory.................................................................. 11,000

1 Adjusting entry: reduces the valuation account from $23,500 to $9,500.2 Adjusting entry: reduces the valuation account from $17,500 to $6,500.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-22 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

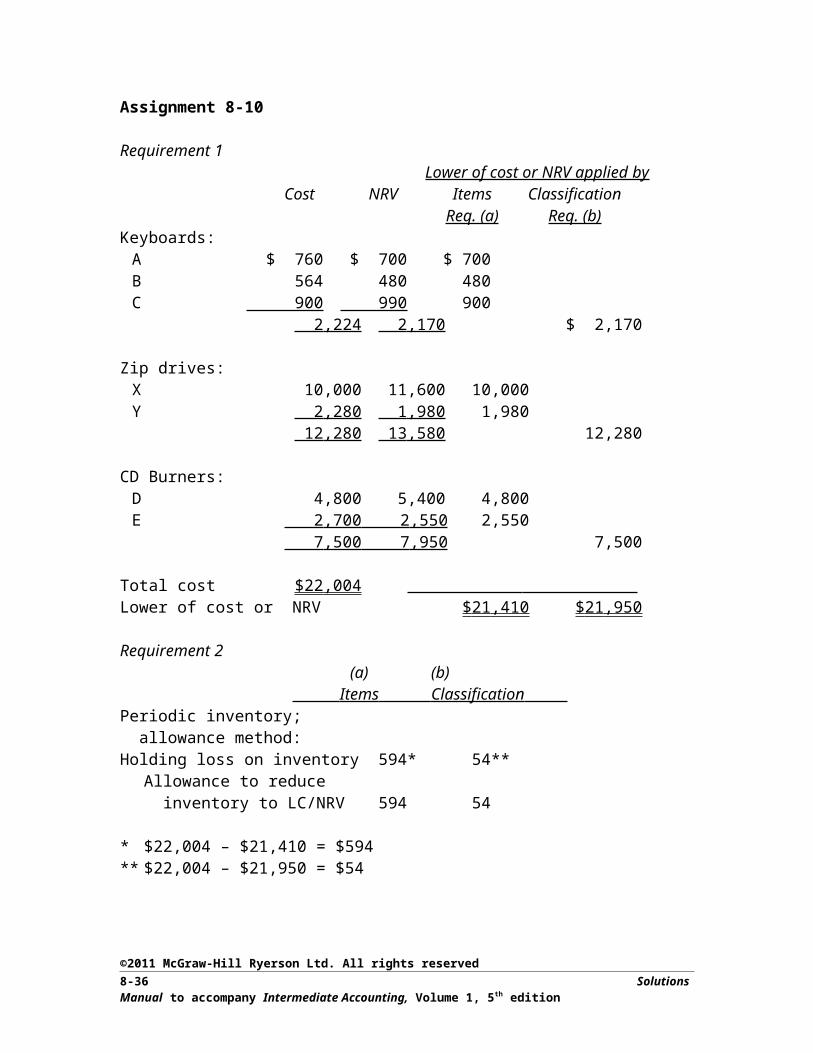

Assignment 8-10

Requirement 1Lower of cost or NRV applied by

Cost NRV Items ClassificationReq. (a) Req. (b)

Keyboards:A $ 760 $ 700 $ 700B 564 480 480C 900 990 900

2,224 2,170 $ 2,170

Zip drives:X 10,000 11,600 10,000Y 2,280 1,980 1,980

12,280 13,580 12,280

CD Burners:D 4,800 5,400 4,800E 2,700 2,550 2,550

7,500 7,950 7,500

Total cost $22,004 Lower of cost or NRV $ 21,410 $ 21,950

Requirement 2(a) (b)

Items Classification Periodic inventory; allowance method:Holding loss on inventory 594* 54**

Allowance to reduce inventory to LC/NRV 594 54

* $22,004 – $21,410 = $594** $22,004 – $21,950 = $54

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-23

Requirement 3

The application of lower of cost or NRV to individual items may be theoretically preferable because this represents a pure application of the method and is entirely consistent with the concepts underlying the method.

In some cases, however, the difference in inventory valuations produced by the two alternatives may be so small as to make the item-by-item applications not practicable. This is particularly true when items within a category are homogeneous, which means that the computations of “cost” and “NRV” may be conducted at a broader level of aggregation. In this particular situation, this appears to be the case; therefore, both applications derive very similar results. Of course, this difference also should be compared to cost of goods sold and net income, etc., in assessing its materiality.

Another factor to consider is the reliabilty of estimates; use of categories rather than individual items may compensate for imprecision of estimated values.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-24 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

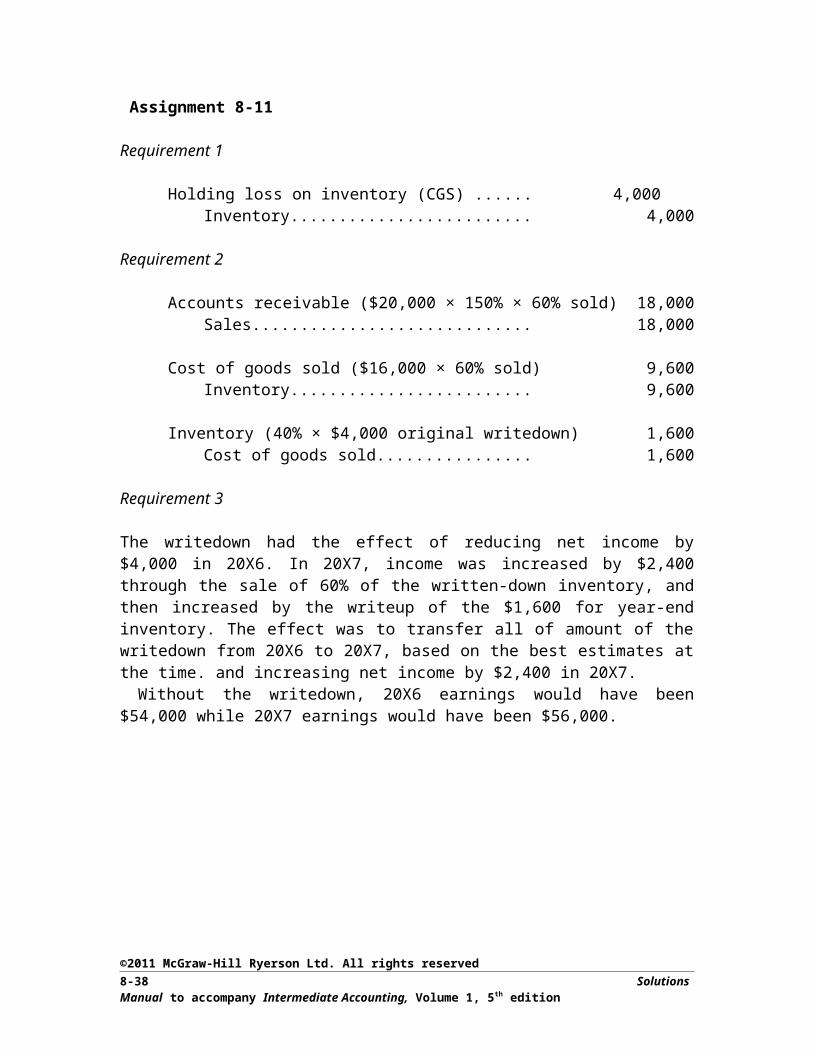

Assignment 8-11

Requirement 1

Holding loss on inventory (CGS) ..................................... 4,000Inventory.................................................................. 4,000

Requirement 2

Accounts receivable ($20,000 × 150% × 60% sold)......... 18,000Sales.......................................................................... 18,000

Cost of goods sold ($16,000 × 60% sold)......................... 9,600Inventory.................................................................. 9,600

Inventory (40% × $4,000 original writedown).................. 1,600Cost of goods sold.................................................... 1,600

Requirement 3

The writedown had the effect of reducing net income by $4,000 in 20X6. In 20X7, income was increased by $2,400 through the sale of 60% of the written-down inventory, and then increased by the writeup of the $1,600 for year-end inventory. The effect was to transfer all of amount of the writedown from 20X6 to 20X7, based on the best estimates at the time. and increasing net income by $2,400 in 20X7.

Without the writedown, 20X6 earnings would have been $54,000 while 20X7 earnings would have been $56,000.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-25

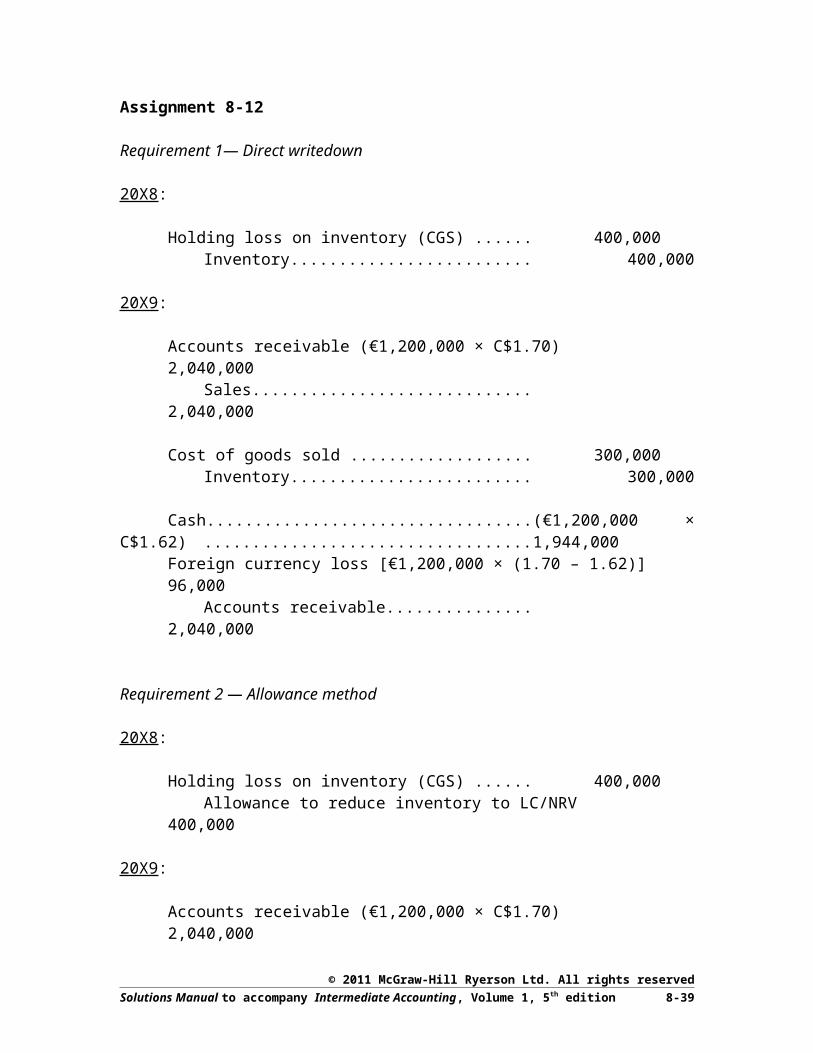

Assignment 8-12

Requirement 1— Direct writedown

20X8:

Holding loss on inventory (CGS) ..................................... 400,000Inventory.................................................................. 400,000

20X9:

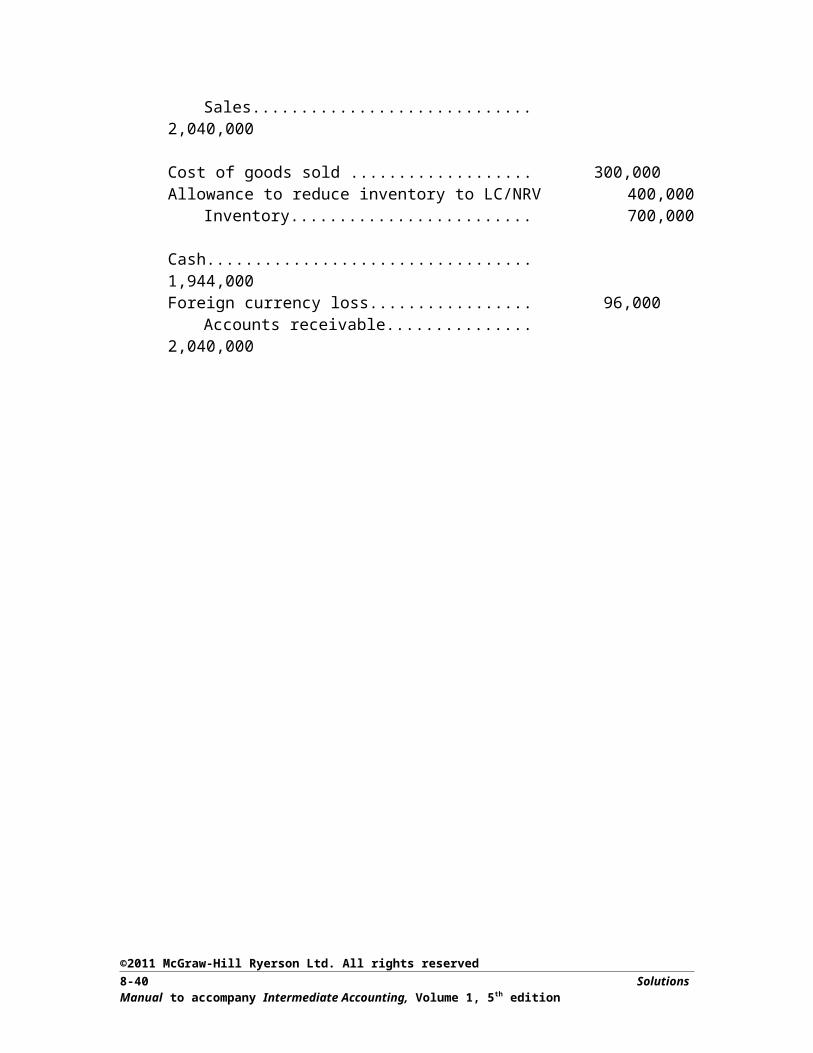

Accounts receivable (€1,200,000 × C$1.70)..................... 2,040,000Sales.......................................................................... 2,040,000

Cost of goods sold ............................................................ 300,000Inventory.................................................................. 300,000

Cash (€1,200,000 × C$1.62)............................................. 1,944,000Foreign currency loss [€1,200,000 × (1.70 – 1.62)].......... 96,000

Accounts receivable................................................. 2,040,000

Requirement 2 — Allowance method

20X8:

Holding loss on inventory (CGS) ..................................... 400,000Allowance to reduce inventory to LC/NRV............. 400,000

20X9:

Accounts receivable (€1,200,000 × C$1.70)..................... 2,040,000Sales.......................................................................... 2,040,000

Cost of goods sold ............................................................ 300,000Allowance to reduce inventory to LC/NRV...................... 400,000

Inventory.................................................................. 700,000

Cash .................................................................................. 1,944,000Foreign currency loss........................................................ 96,000

Accounts receivable................................................. 2,040,000

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-26 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

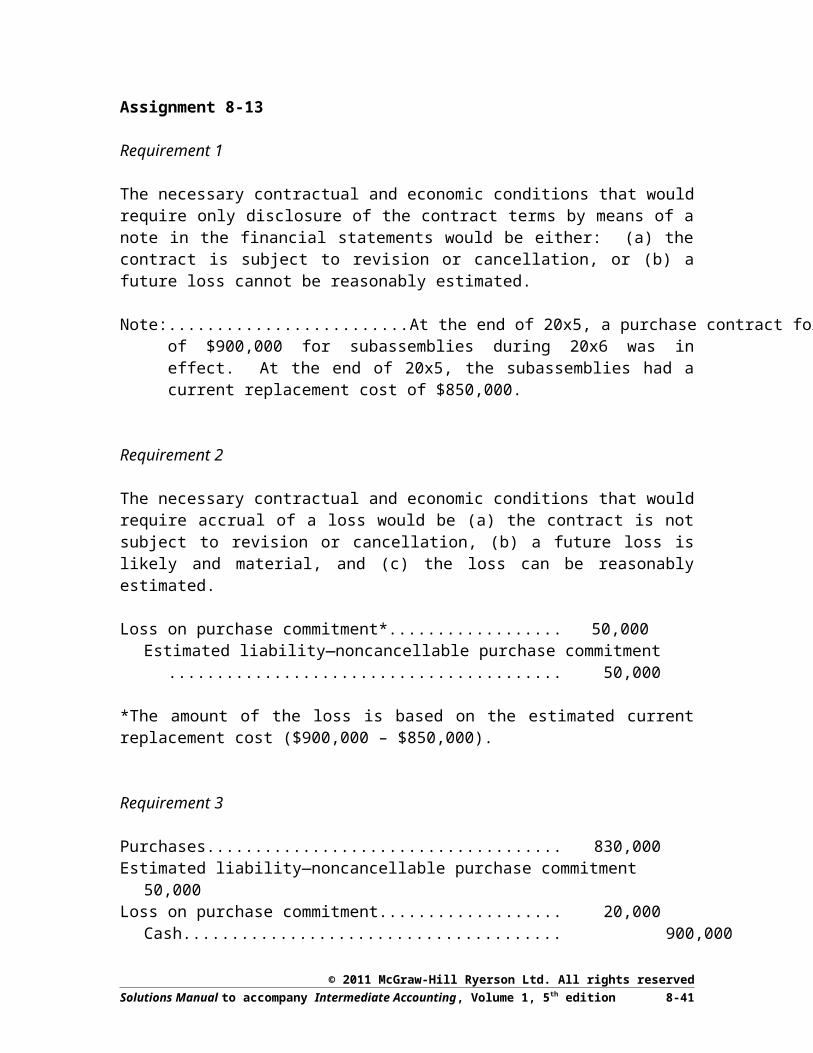

Assignment 8-13

Requirement 1

The necessary contractual and economic conditions that would require only disclosure of the contract terms by means of a note in the financial statements would be either: (a) the contract is subject to revision or cancellation, or (b) a future loss cannot be reasonably estimated.

Note: At the end of 20x5, a purchase contract for a maximum of $900,000 for subassemblies during 20x6 was in effect. At the end of 20x5, the subassemblies had a current replacement cost of $850,000.

Requirement 2

The necessary contractual and economic conditions that would require accrual of a loss would be (a) the contract is not subject to revision or cancellation, (b) a future loss is likely and material, and (c) the loss can be reasonably estimated.

Loss on purchase commitment*............................................................ 50,000Estimated liability—noncancellable purchase commitment........... 50,000

*The amount of the loss is based on the estimated current replacement cost ($900,000 – $850,000).

Requirement 3

Purchases............................................................................................... 830,000Estimated liability—noncancellable purchase commitment................. 50,000Loss on purchase commitment.............................................................. 20,000

Cash................................................................................................. 900,000

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-27

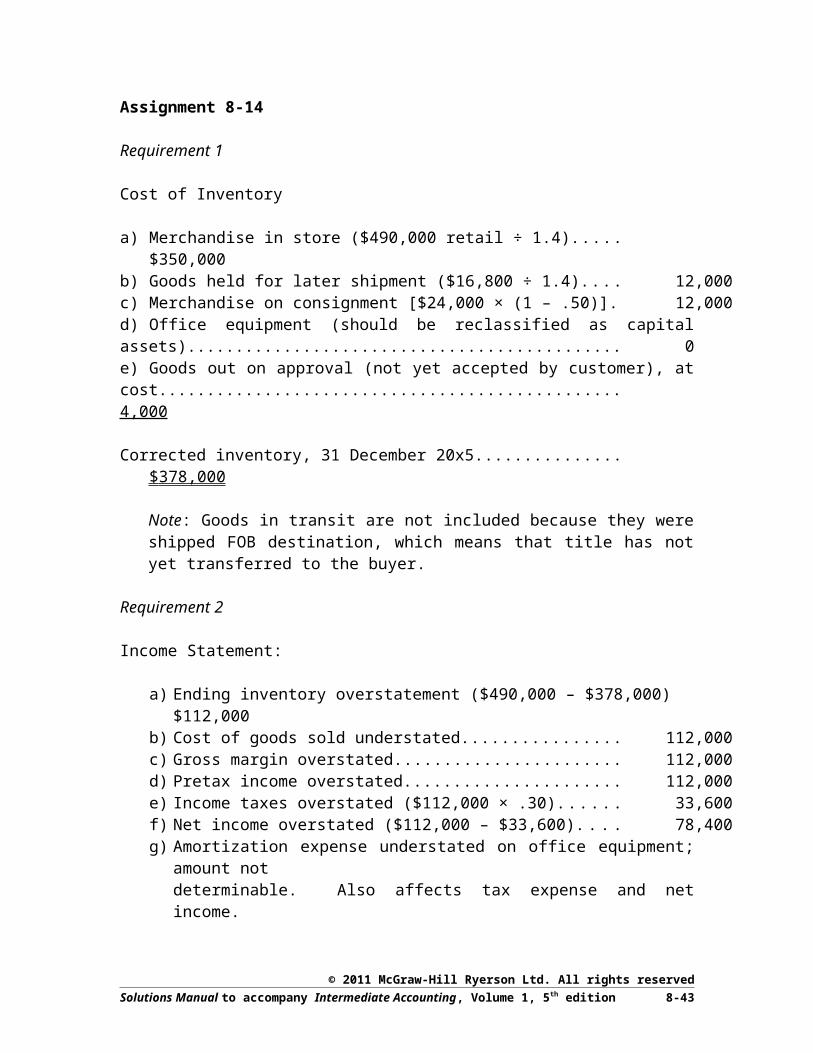

Assignment 8-14

Requirement 1

Cost of Inventory

a) Merchandise in store ($490,000 retail ÷ 1.4)................................................ $350,000b) Goods held for later shipment ($16,800 ÷ 1.4)............................................. 12,000c) Merchandise on consignment [$24,000 × (1 – .50)].................................... 12,000d) Office equipment (should be reclassified as capital assets)......................... 0e) Goods out on approval (not yet accepted by customer), at cost................... 4,000

Corrected inventory, 31 December 20x5............................................................. $ 378,000

Note: Goods in transit are not included because they were shipped FOB destination, which means that title has not yet transferred to the buyer.

Requirement 2

Income Statement:

a) Ending inventory overstatement ($490,000 – $378,000)....................... $112,000b) Cost of goods sold understated............................................................... 112,000c) Gross margin overstated......................................................................... 112,000d) Pretax income overstated........................................................................ 112,000e) Income taxes overstated ($112,000 × .30).............................................. 33,600f) Net income overstated ($112,000 – $33,600)......................................... 78,400g) Amortization expense understated on office equipment; amount not

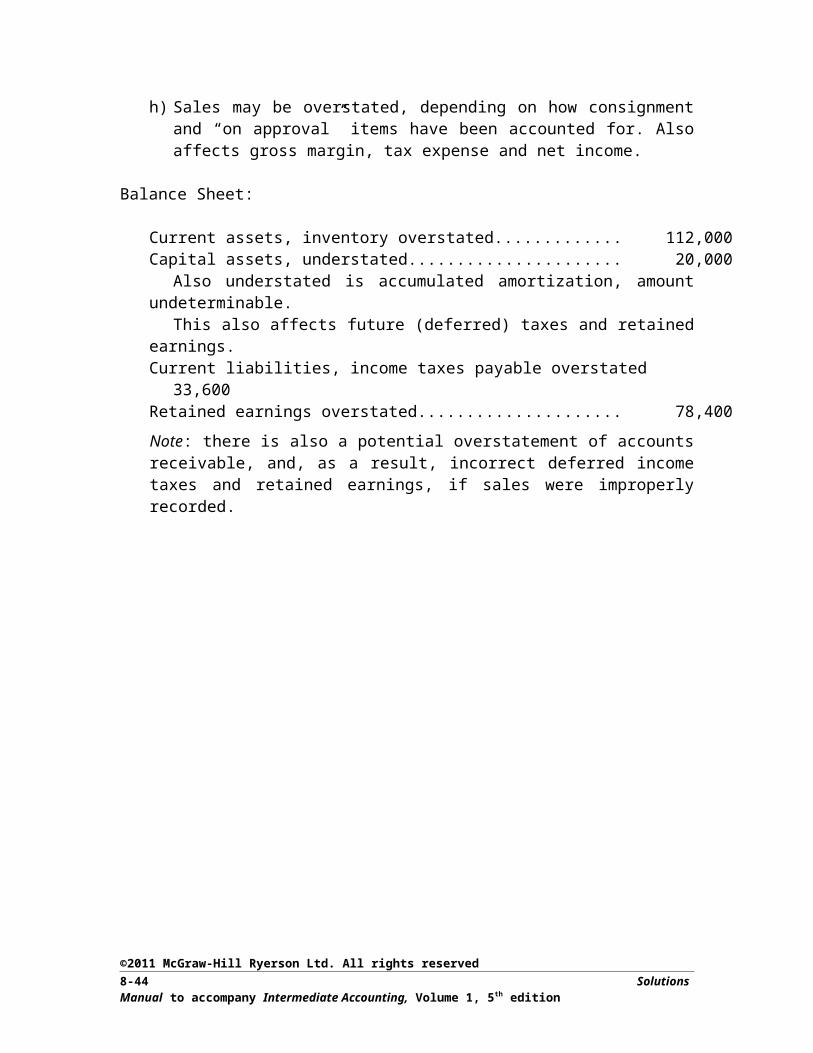

determinable. Also affects tax expense and net income.h) Sales may be overstated, depending on how consignment and “on approval”

items have been accounted for. Also affects gross margin, tax expense and net income.

Balance Sheet:

Current assets, inventory overstated............................................................. 112,000Capital assets, understated............................................................................ 20,000

Also understated is accumulated amortization, amount undeterminable. This also affects future (deferred) taxes and retained earnings.

Current liabilities, income taxes payable overstated.................................... 33,600Retained earnings overstated........................................................................ 78,400

Note: there is also a potential overstatement of accounts receivable, and, as a result, incorrect deferred income taxes and retained earnings, if sales were improperly recorded.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-28 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

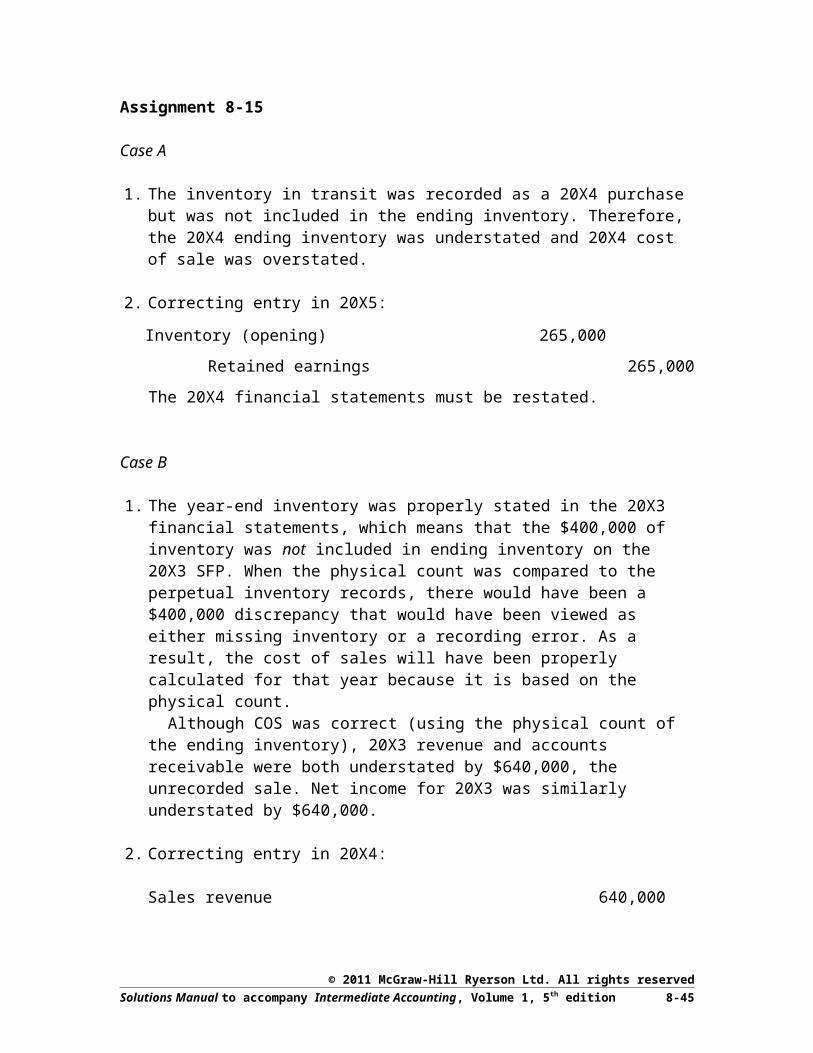

Assignment 8-15

Case A

1. The inventory in transit was recorded as a 20X4 purchase but was not included in the ending inventory. Therefore, the 20X4 ending inventory was understated and 20X4 cost of sale was overstated.

2. Correcting entry in 20X5:

Inventory (opening) 265,000

Retained earnings 265,000

The 20X4 financial statements must be restated.

Case B

1. The year-end inventory was properly stated in the 20X3 financial statements, which means that the $400,000 of inventory was not included in ending inventory on the 20X3 SFP. When the physical count was compared to the perpetual inventory records, there would have been a $400,000 discrepancy that would have been viewed as either missing inventory or a recording error. As a result, the cost of sales will have been properly calculated for that year because it is based on the physical count.

Although COS was correct (using the physical count of the ending inventory), 20X3 revenue and accounts receivable were both understated by $640,000, the unrecorded sale. Net income for 20X3 was similarly understated by $640,000.

2. Correcting entry in 20X4:

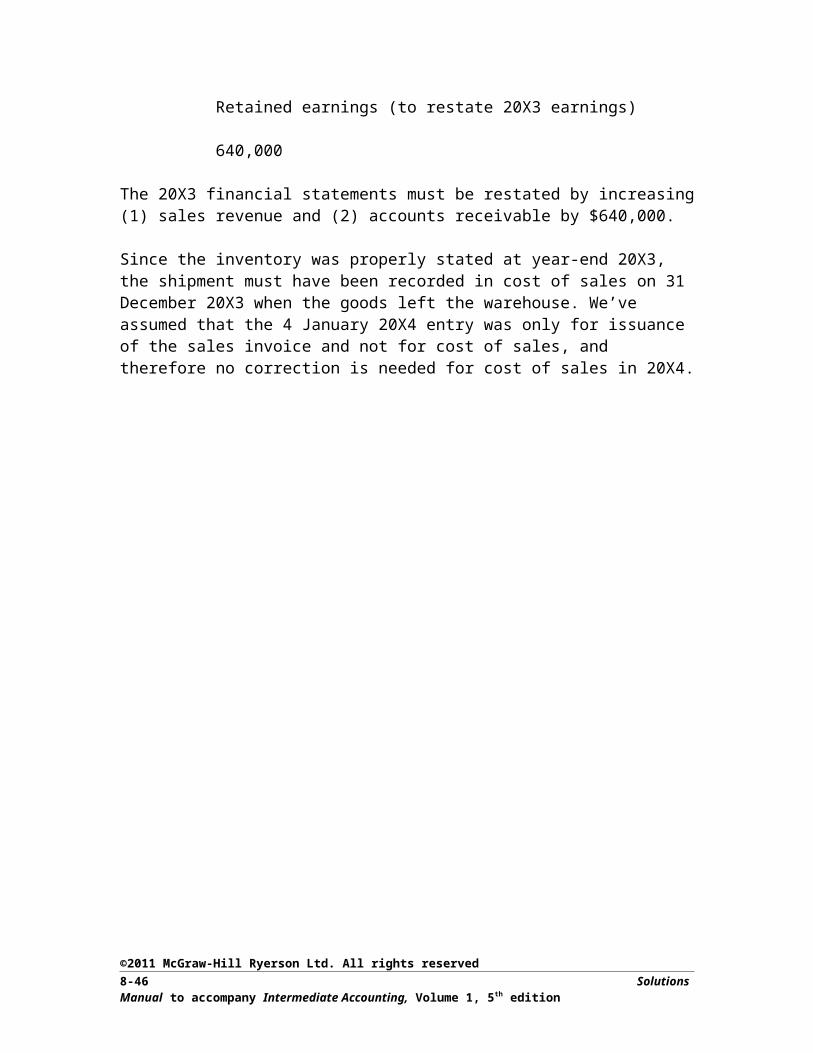

Sales revenue 640,000Retained earnings (to restate 20X3 earnings) 640,000

The 20X3 financial statements must be restated by increasing (1) sales revenue and (2) accounts receivable by $640,000.

Since the inventory was properly stated at year-end 20X3, the shipment must have been recorded in cost of sales on 31 December 20X3 when the goods left the warehouse. We’ve assumed that the 4 January 20X4 entry was only for issuance of the sales invoice and not for cost of sales, and therefore no correction is needed for cost of sales in 20X4.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-29

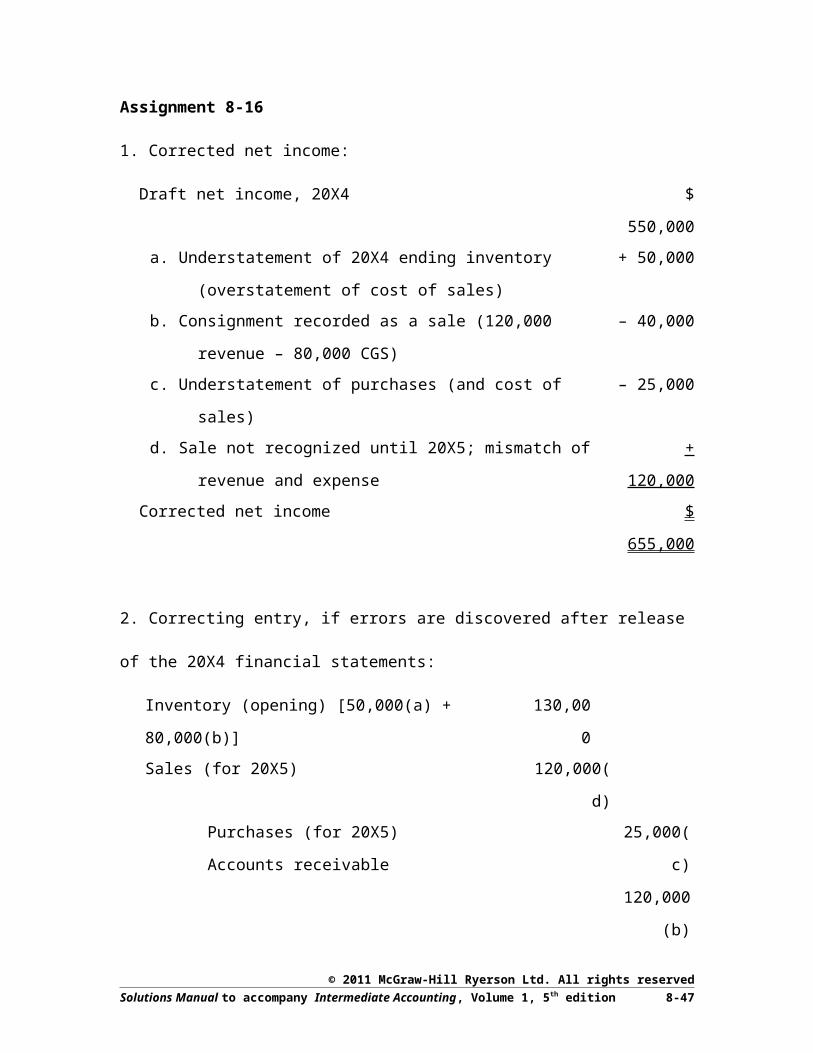

Assignment 8-16

1. Corrected net income:

Draft net income, 20X4 $ 550,000

a. Understatement of 20X4 ending inventory (overstatement of cost

of sales)

+ 50,000

b. Consignment recorded as a sale (120,000 revenue – 80,000 CGS) – 40,000

c. Understatement of purchases (and cost of sales) – 25,000

d. Sale not recognized until 20X5; mismatch of revenue and expense + 120,000

Corrected net income $ 655,000

2. Correcting entry, if errors are discovered after release of the 20X4 financial statements:

Inventory (opening) [50,000(a) + 80,000(b)] 130,000

Sales (for 20X5) 120,000(d)

Purchases (for 20X5)

Accounts receivable

25,000(c)

120,000(b)

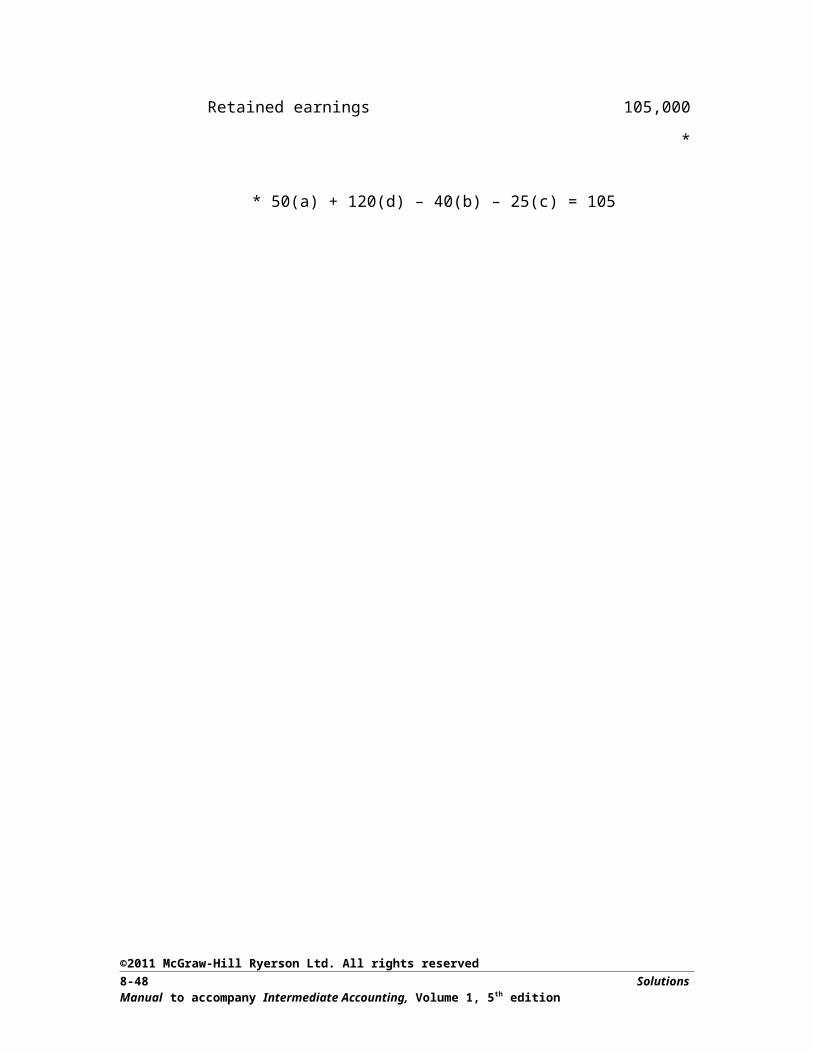

Retained earnings 105,000*

* 50(a) + 120(d) – 40(b) – 25(c) = 105

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-30 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

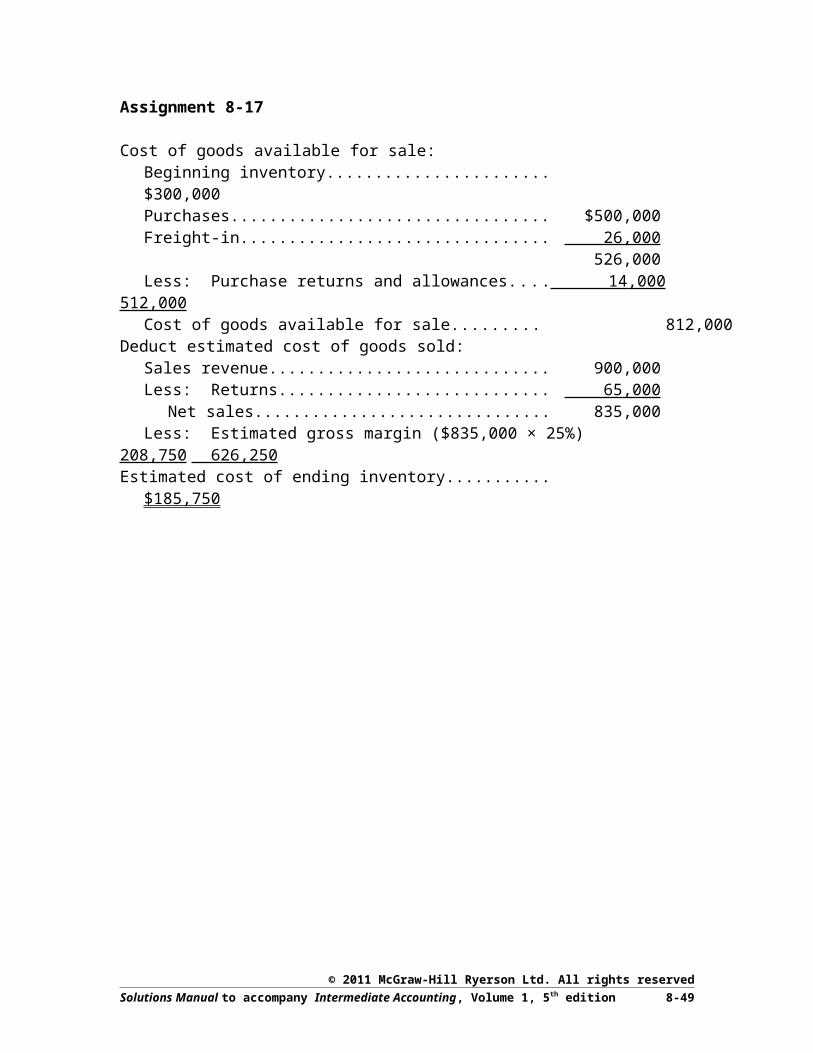

Assignment 8-17

Cost of goods available for sale:Beginning inventory..................................................................... $300,000Purchases...................................................................................... $500,000Freight-in...................................................................................... 26,000

526,000Less: Purchase returns and allowances....................................... 14,000 512,000Cost of goods available for sale.................................................. 812,000

Deduct estimated cost of goods sold:Sales revenue............................................................................... 900,000Less: Returns............................................................................... 65,000

Net sales................................................................................. 835,000Less: Estimated gross margin ($835,000 × 25%)....................... 208,750 626,250

Estimated cost of ending inventory.................................................... $185,750

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-31

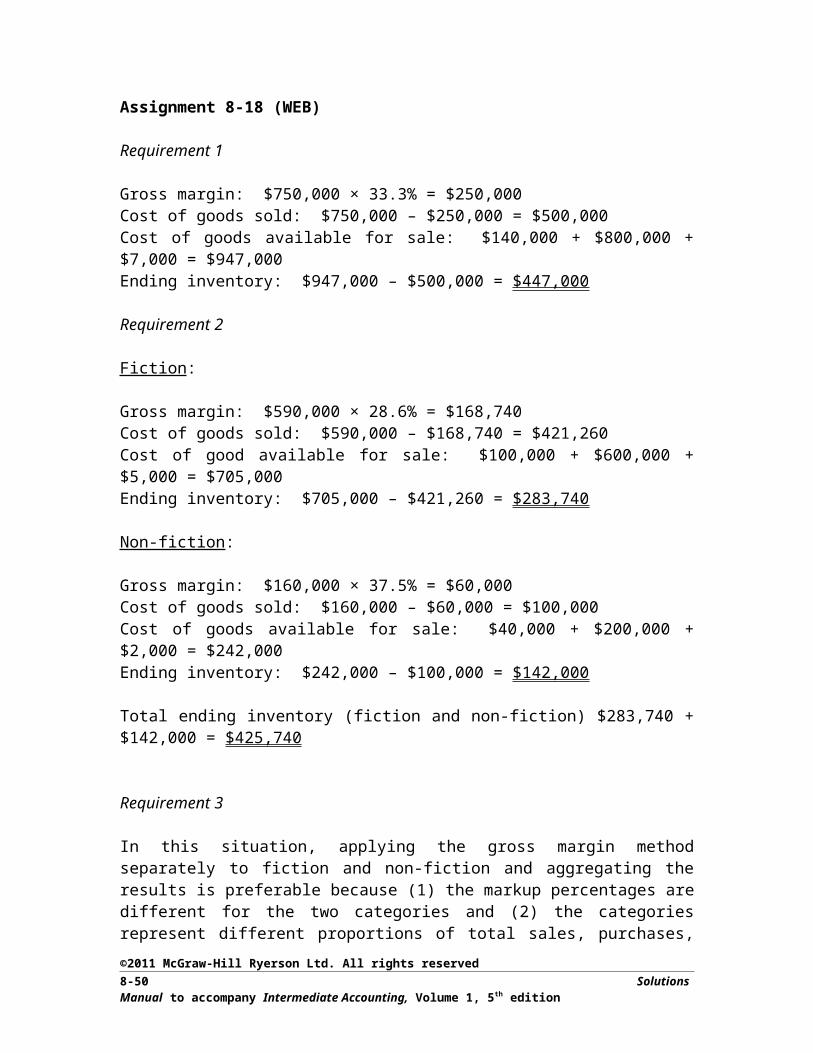

Assignment 8-18 (WEB)

Requirement 1

Gross margin: $750,000 × 33.3% = $250,000Cost of goods sold: $750,000 – $250,000 = $500,000Cost of goods available for sale: $140,000 + $800,000 + $7,000 = $947,000Ending inventory: $947,000 – $500,000 = $447,000

Requirement 2

Fiction:

Gross margin: $590,000 × 28.6% = $168,740Cost of goods sold: $590,000 – $168,740 = $421,260Cost of good available for sale: $100,000 + $600,000 + $5,000 = $705,000Ending inventory: $705,000 – $421,260 = $283,740

Non-fiction:

Gross margin: $160,000 × 37.5% = $60,000Cost of goods sold: $160,000 – $60,000 = $100,000Cost of goods available for sale: $40,000 + $200,000 + $2,000 = $242,000Ending inventory: $242,000 – $100,000 = $142,000

Total ending inventory (fiction and non-fiction) $283,740 + $142,000 = $425,740

Requirement 3

In this situation, applying the gross margin method separately to fiction and non-fiction and aggregating the results is preferable because (1) the markup percentages are different for the two categories and (2) the categories represent different proportions of total sales, purchases, and inventory on hand. A physical count should be much closer to the separate application of the gross margin method ($425,740) than the aggregate application ($447,000).

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-32 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Assignment 8-19

Requirement 1

At Cost At Retail

Inventory, 1 June $ 226,000 $ 336,000+ Purchases 519,600 940,000– Purchase returns and allowances (9,000) (16,000)+ Markups (net) ($122,000 – $38,000) 84,000

Retail value goods available for sale 1,344,000– Markdowns (net) ($88,000 – $43,000) (45,000)

Goods available for sale $ 736,600 $ 1,299,000– Sales (net of returns: $1,050,000 – $50,000) (1,000,000)

Inventory, 30 June, at retail $ 299,000Inventory, 30 June, at cost:

($299,000 × 55 % cost ratio*) $ 164,450

* Cost ratio = $736,600 ÷ $1,344,000 = 54.8%

Since the retail method is an estimate, there is no point in carrying the cost ratio out to more than two significant digits.

Requirement 2

If the estimate of ending inventory were based on the ratio between cost and retail value, the estimated inventory would reflect approximate purchase cost. However, the retail method increases the ratio by deducting markdowns from the denominator of the cost ratio. The resulting cost ratio takes into account that some goods have been marked down, and thus approximates lower of cost or NRV valuation.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-33

Assignment 8-20 (WEB)

Requirement 1At Cost At Retail

Goods available for sale:Beginning inventory.......................................................... $ 180,500 $ 300,000Purchases (net).................................................................. 955,000 1,453,000Freight-in........................................................................... 15,000Additional markups........................................................... 31,000Additional markup cancellations....................................... (14,000)Markdowns........................................................................ (8,000)Employee discounts (a markdown)................................... (2,000 )

Total goods available for sale....................................... $ 1,150,500 1,760,000Cost ratio $1,150,500/($1,760,000 + $10,000) = 65%Deduct:

Sales.................................................................................. (1,300,000)Ending inventory

At retail.............................................................................. 460,000At cost, ($460,000 × 65%)................................................ 299,000

Ending inventory per physical count:At retail.............................................................................. 475,000At cost, ($475,000 × 65%)................................................ 308,750

Indicated excess:At retail.............................................................................. $ 15,000At cost............................................................................... $ 9,750

Requirement 2

The above computations indicate a general correspondence between the two independently derived totals. The difference, at cost, of $9,750 is only 3.16% of the cost of the inventory from the physical count; thus, this difference would probably not be investigated at great length because it is not material. Nevertheless, the auditor would consider whether:

a) The physical count was correct. Presumably, the auditors observed the physical count and made their own test counts. In this follow-up phase of the audit, attention will be given to any items for which the audit test counts disagreed with those of the client.

b) The ending inventory in fact comprises items which have the average cost/retail ratio for the period. (Note that use of this estimation method implicitly assumes that the ending inventory comprises the average merchandise available during the period.) In the case of Acton for this period, the ending inventory may comprise goods with a lower than average cost/retail ratio. This could account for the fact that the computed estimate of ending inventory is less than the total per the physical count.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-34 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

(Note that the physical count includes the specific units that are on hand at year-end—not necessarily an average of the units available during the period.)

c) The book data used in the above analysis is valid.

In summary, the auditor would in general place greater confidence in the physical count total, unless there were clear reasons to suspect that it was not correct. This conclusion is strengthened in this case because the count exceeds the estimated total. Do not overlook the fact that the retail method computations are estimates.

Requirement 3

Based on the above reasoning, the $9,750 discrepancy would probably not be accorded any accounting treatment (i.e., no entry) because (a) the count total is more reliable than the estimated total and (b) the difference is not material in amount.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-35

Assignment 8-21 (EXCEL)

Requirement 1

Net Sales................................................................. $798,000Opening Inventory.................................................. $ 45,000Net purchases1........................................................ 464,300

509,300Gross Margin ($798,000 × .51).............................. 406,980Cost of Goods Sold ($798,000 – $406,980)........... $ 391,020 Ending Inventory ($509,300 – $391,020)............... $ 118,280

1$459,500 + $7,000 – $2,200 = $464,300

Requirement 2At Cost At Retail

Goods available for sale:Beginning inventory....................................... $ 45,000 $ 80,000Purchases........................................................ 459,500 850,000Purchase returns............................................. (2,200) (4,000)Freight on purchases...................................... 7,000Additional markups........................................ 9,000Additional markup cancellations................... (5,000 )

930,000Markdowns.................................................... (7,000)Markdown cancellations................................ 3,000

Total goods available for sale.................... $ 509,300 926,000Cost ratio = $509,300 ÷ $930,000 = .548Deduct:

Sales............................................................... $800,000Less: Sales returns......................................... (2,000)

Net sales..................................................... (798,000)Ending inventory (at retail).................................. $ 128,000 Ending inventory (at cost) $128,000 × .548........ 70,144Cost of goods sold ($509,300 – $70,144)............ $ 439,156 Actual gross margin achieved, ($798,000 – $439,156) ÷ $798,000.................... 44.97%

Requirement 3

The gross profit method yields an inventory cost that approximates average cost. In contrast, the retail method estimates inventory at lower of cost or fair value because it excludes markdowns in calculating the cost ratio but then applies that cost ratio to the retail inventory including markdowns. As well, the retail sales method is likely to be more accurate as it uses the actual mark-up for the current year, not last year. The

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-36 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

difference between last year and this (54.8% vs. 51%) explains the $48,136 ($118,280 – $70,144) difference (approximately 6% of $798,000) in ending inventory.

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-37

Assignment 8-22

Requirement 1

Current entries:

a) No entry required for beginning inventory.

b) Purchases ($200,000 × 98%).................................................... 196,000Cash ($196,000 × 85%)........................................................ 166,600Accounts payable ($196,000 × 15%)................................... 29,400

c) Purchases (or Freight-in)........................................................... 10,000Cash...................................................................................... 10,000

d) Accounts payable ($29,400 × 40%).......................................... 11,760Cash...................................................................................... 11,760

e) Cash ($3,000 × 98%)................................................................ 2,940Purchase returns................................................................... 2,940

f) Cash........................................................................................... 333,000Accounts receivable.................................................................. 37,000

Sales revenue........................................................................ 370,000

g) Inventory—damaged goods...................................................... 180*Loss on goods returned............................................................. 220

Cash...................................................................................... 400

*Sales price............................ $240Repair costs............................ (50)Selling costs........................... (10)Net realizable value................ $ 180

h) Operating expenses................................................................... 120,000Cash...................................................................................... 120,000

i) Purchases................................................................................... 7,000Accounts payable................................................................. 7,000

(Ownership has passed by 31 December 20x5)

j) Inventory—damaged goods...................................................... 50Cash...................................................................................... 50

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-38 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

k) Cash........................................................................................... 245Inventory—damaged goods ($180 + $50)........................... 230Operating expenses (selling expenses allocated and assumed to have been previously recorded when paid). . 10Gain on sale of damaged goods............................................ 5

Requirement 2

Entries at end of period:

Ending inventory, at cost ($110,000 (l) + $7,000 (i))...................... 117,000Cost of goods sold............................................................................ 198,060Purchase returns............................................................................... 2,940

Purchases ($196,000 + $10,000 + $7,000)............................... 213,000Beginning inventory, at cost..................................................... 105,000

Holding loss on inventory (LC/NRV).............................................. 3,000Allowance to reduce inventory to LC/NRV............................. 3,000

($110,000 + $7,000) – ($107,000 + $7,000) = $3,000

Income tax expense (from income statement, Req. 3)..................... 19,494Income taxes payable................................................................ 19,494

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-39

Requirement 3GAMIT COMPANY

Income StatementFor Year Ended 31 December 20x5

Sales revenue.................................................................................... $370,000Cost of goods sold:

Beginning inventory.................................................................. $105,000Plus: Purchases......................................................................... 213,000Less: Purchase returns.............................................................. (2,940)Goods available for sale............................................................ 315,060Less: Ending inventory............................................................ 117,000 198,060

Gross margin.................................................................................... 171,940Holding loss on inventory (LC/NRV)....................................... (3,000)*Gain on sale of damaged goods.............................................. 5*Loss on goods returned........................................................... (220)Operating expenses ($120,000 – $10)...................................... (119,990)

Income before income taxes............................................................. 48,735Less: income tax expense ($48,735 × .40)...................................... 19,494Net income....................................................................................... $ 29,241

*Shown separately for illustrative purposes.

Earnings per share on common stock outstanding:Net income, $29,241 ÷ shares outstanding, 20,000 = $1.46

Requirement 4GAMIT COMPANY

Balance SheetAt 31 December 20x5

Current Assets:Inventory, at cost.............................................................................. $117,000

Less: Allowance for reduction to NRV................................... (3,000 ) Inventory, at LC/NRV...................................................................... $114,000*

*May also be shown net.

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-40 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Assignment 8-23

Requirement 1—indirect method

Operating ActivitiesAdd back: non-cash charges relating to inventories

Loss on purchase commitment............................................. 8,000Add/(deduct)

Increase in inventories (net)............................................. (110,000)Increase in accounts payable............................................ 20,000

Total adjustment............................................................ $ (82,000)

Requirement 2—direct method

Cash paymentsCost of goods sold, excluding change in LC/NRV allowance [$4,900,000 – ($65,000 – $46,000)]................................. $4,881,000

Less: loss on purchase commitment........................................... (8,000)Less: increase in accounts payable............................................. (20,000)Plus: increase in inventories (at cost)

($951,500 + $65,000) – ($841,000 + $46,000).................. 129,000Net cash out flow for inventory purchases.................................. $4,982,000

Alternatively:$4,900,000 – $20,000 – $8,000 + $110,000 = $4,982,000

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-41

Assignment 8-24

Requirement 1—FIFO, perpetual inventory

Under FIFO, perpetual and periodic yield the same results. Therefore, the calculation is straightforward for the 8,300 units actually in the physical inventory:

4,300 units @ $13.60 $ 58,4804,000 units @ $13.25 53,000

111,480Writedown to LC/NRV:

4,300 × ($13.60 – $13.25) (1,505)Ending inventory, LC/NRV $ 109,975

Cost of sales:

Opening inventory $ 95,040Purchases 399,960Available for sale (given in problem) 495,000Less: ending inventory at cost (above)* (111,480)Cost of sales at purchase price 383,520Adjustment for LC/NRV writedown:

4,300 × ($13.60 – $13.25) 1,505Cost of sales using LC/NRV inventory $ 385,025

*Including shrinkage, 500 units

Requirement 2—Average cost, periodic method

The average cost can be calculated from the information on total quantities and total cost given in the problem:

Average cost = $495,000 ÷ 36,800 = $13.4511 (rounded)

Ending inventory at cost = 8,300 units × $13.4511 = $111,644

Ending inventory at LC/NRV = $111,644 – [4,300 × ($13.4511 – $13.25)] = $111,644 – $865 = $110,779

Cost of sales = 28,500* × $13.4511 + $865 = $384,221*Including shrinkage of 500 units

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-42 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Assignment 8-25 (WEB)

a) Weighted average (periodic inventory system):Goods available for sale:

Units Unit Cost Amount

1. Inventory........................................................... 30 $19.00 $ 5702. Purchase............................................................ 45 20.00 9003. Purchase............................................................ 50 20.80 1,0404. Purchase............................................................ 50 21.60 1,080

Goods available for sale............................... 175 $3,590

$3,590 175 = $20.51 per unit

Goods available for sale.......................................... 175 $20.51 $3,590Ending inventory..................................................... 75 20.51 1,538Cost of goods sold (includes rounding error)......... 100 $2,052

b) Moving average (perpetual inventory system):Moving

Units Average Amount

1. Inventory........................................................... 30 $19.00 $ 5702. Purchase............................................................ 45 20.00 900

Balance......................................................... 75 19.60 1,4703. Sale.................................................................... (50) ( 980)

Balance......................................................... 25 19.60 4904. Purchase............................................................ 50 20.80 1,040

Balance......................................................... 75 20.40 1,5305. Sale.................................................................... (50) (1,020)

Balance.............................................................. 25 20.40 5106. Purchase............................................................ 50 21.60 1,080

Balance......................................................... 75 21.20 $1,590

Goods available for sale.......................................... 175 $3,590Ending inventory..................................................... 75 1,590Cost of goods sold................................................... 100 $2,000*

*$980 + $1,020 = $2,000

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-43

c) FIFO:Units Amount

Goods available (from above).................. 175 $3,590Ending inventory (75 units):

50 units × $21.60................................. (50) (1,080)25 units × $20.80................................. ( 25) 75 ( 520) $1,600

Cost of goods sold........................... 100 $1,990

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-44 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Assignment 8-26

Requirement 1

Ending Cost of GrossInventory Goods sold Margin

a) FIFO........................................................ $51,750 $180,150 $280,350b) Weighted average................................... 47,970 183,885 276,615c) Moving average...................................... 50,790* 181,110 279,390

*Rounded.

Computations:

a) FIFO:

Goods available for sale: Units Unit Cost Amount

1. Inventory............................................... 3,000 $5.00 $ 15,0002. Purchase................................................ 27,000 5.20 140,4004. Purchase................................................ 9,000 5.50 49,5006. Purchase................................................ 4,500 6.00 27,000

Total................................................. 43,500 231,900

Ending inventory (43,500 – 34,500 = 9,000 units):Out of (6) 4,500 at $6.00....................... (4,500) (27,000) $51,750Out of (4) 4,500 at $5.50....................... (4,500) (24,750)Cost of goods sold................................. 34,500 $ 180,150

Cost of sales:10,500 × $13.00 = $ 136,50024,000 × $13.50 = 324,000

460,500Cost of good sold 180,150Gross margin $ 280,350

b) Weighted average (rounding error in cost of goods sold):Average unit cost = $231,900 ÷ 43,500 = $5.33

Ending inventory, 9,000 units: Cost of goods sold:9,000 units × $5.33 = $ 47,970 34,500 units × $5.33 = $183,885Sales $460,500Cost of goods sold 183,885Gross margin $ 276,605

c) Moving average:

© 2011 McGraw-Hill Ryerson Ltd. All rights reservedSolutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition 8-45

MovingUnits Average Amount

1. Inventory........................................................ 3,000 $5.00 $ 15,0002. Purchase......................................................... 27,000 5 .20 140,400

Balance...................................................... 30,000 5.18 155,4003. Sale................................................................. (10,500) (54,390 )

Balance...................................................... 19,500 5.18 101,0104. Purchase......................................................... 9,000 5 .50 49,500

Balance...................................................... 28,500 5.28 150,5105. Sale................................................................. (24,000) (126,720 )

Balance...................................................... 4,500 5.28 23,7906. Purchase......................................................... 4,500 6 .00 27,000

Ending inventory....................................... 9,000 $5.64 $ 50,790

Cost of goods sold:$231,900 – $50,790 = $ 181,110

Sales $460,500Cost of goods sold 181,110Gross margin $ 279,390

©2011 McGraw-Hill Ryerson Ltd. All rights reserved8-46 Solutions Manual to accompany Intermediate Accounting, Volume 1, 5th edition

Requirement 2

Weighted Average Moving AveragePeriodic Perpetual

1. Opening inventory, both methods.... 15,000 15,000

2. Purchases (27,000 × $5.20).............. 140,040Inventory........................................... 140,040

Accounts payable......................... 140,040 140,040

3. Accounts receivable.......................... 136,500 136,500Sales (10,500 × $13).................... 136,500 136,500

Cost of goods sold............................ N/A 54,390Inventory (10,500 × $5.18).......... 54,390

4. Purchases.......................................... 49,500Inventory (9,000 × $5.50)................. 49,500

Accounts payable......................... 49,500 49,500

5. Accounts receivable.......................... 324,000 324,000Sales (24,000 × $13.50)............... 324,000 324,000

Cost of goods sold............................ N/A 126,720Inventory (24,000 × $5.28).......... 126,720

6. Purchases.......................................... 27,000Inventory (4,500 × $6)...................... 27,000

Accounts payable......................... 27,000 27,000

7. Cost of goods sold ........................... 183,570* N/AInventory, closing (9,000 × $5.33).. . 47,970

Inventory, opening....................... 15,000Purchases...................................... 216,540

*(34,500 × $5.33); rounded

Requirement 3