changes and configurations of accounting systemsestv.in/icai/idtc/pdf/changes and configurations...

TRANSCRIPT

Changes and Configurations of Accounting Systems

24th June, Saturday

By CA Venugopal Gella

1

Role of Technology in GST Implementation

2

CA. Venugopal G

Agenda1. Role of Technology in GST

2. Accounting + Software in GST

3. Reconciliations

4. Transitional Challenges in IT

5. Other areas – IT Support

3

4

1. Role of Technology in GST

Overview

• Technology or software is the backbone of GST

• Success or failure of implementation of GST is heavily dependent on technology

• GST will Create a paradigm shift in how Small Business “run their day to day business”

• Its not a Tax Reform, it’s a Business Reform

5

How digital India plays its role in GST?

• Communication with the department is in electronic form• Communication over e-mails - Registration till Assessments & Audit

• Notices are served in Electronic form

• Responses from assesse in Electronic form

• Signatures ( DSCs / e-sign /EVC)

• Mechanism of filing returns has completely changed in GST regime

6

Relevant Provisions to Know

• Act• CHAPTER VII : TAX INVOICE, CREDIT AND DEBIT NOTES (31-34)

• CHAPTER VIII : ACCOUNTS AND RECORDS (35&36)

• CHAPTER IX : RETURNS ( 37 – 48)

• Rules• Invoice Rules

• Payment Rules

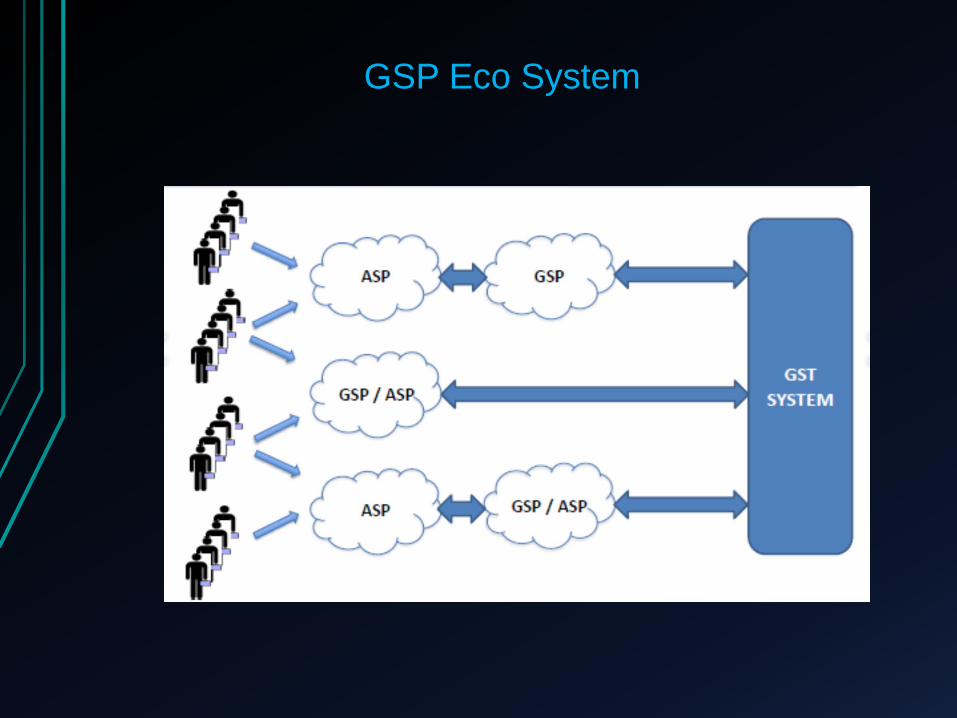

Modes available to file returns

1. GST Portal >> Form Entry / Excel Utility

2. GST Suvidha Providers (GSPs) >> GSTN

3. Offline/Online Utility thru (ASPs) >> GSP>>GSTN

4. Goods and services tax practitioners(GSTPs) >>ASP>>GSP>>GSTN

8

GSP Eco System

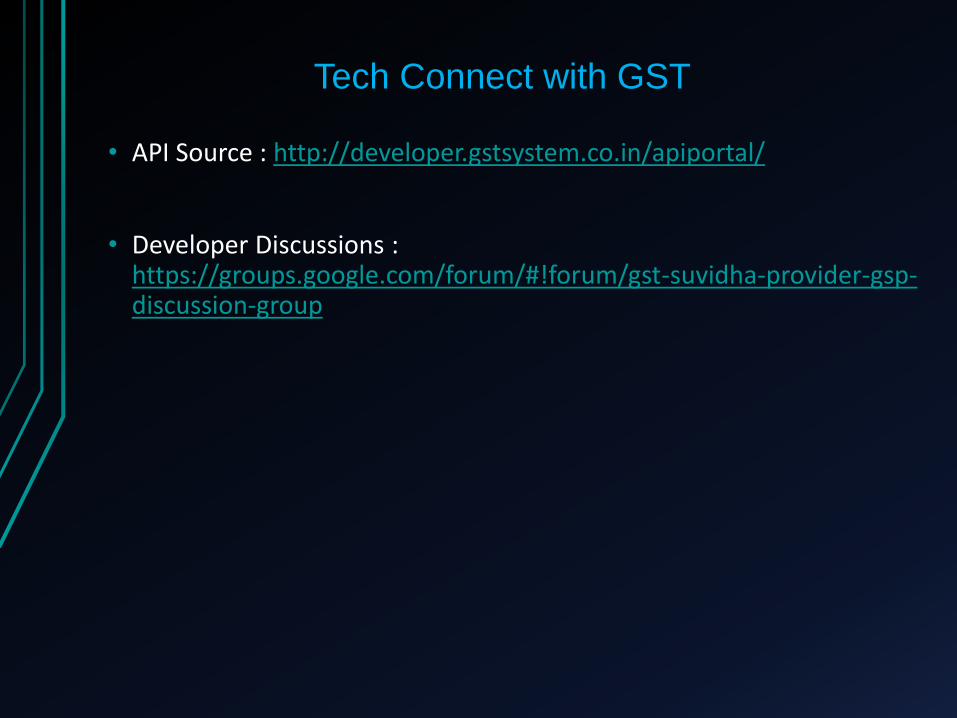

Tech Connect with GST

• API Source : http://developer.gstsystem.co.in/apiportal/

• Developer Discussions : https://groups.google.com/forum/#!forum/gst-suvidha-provider-gsp-discussion-group

API’s Available

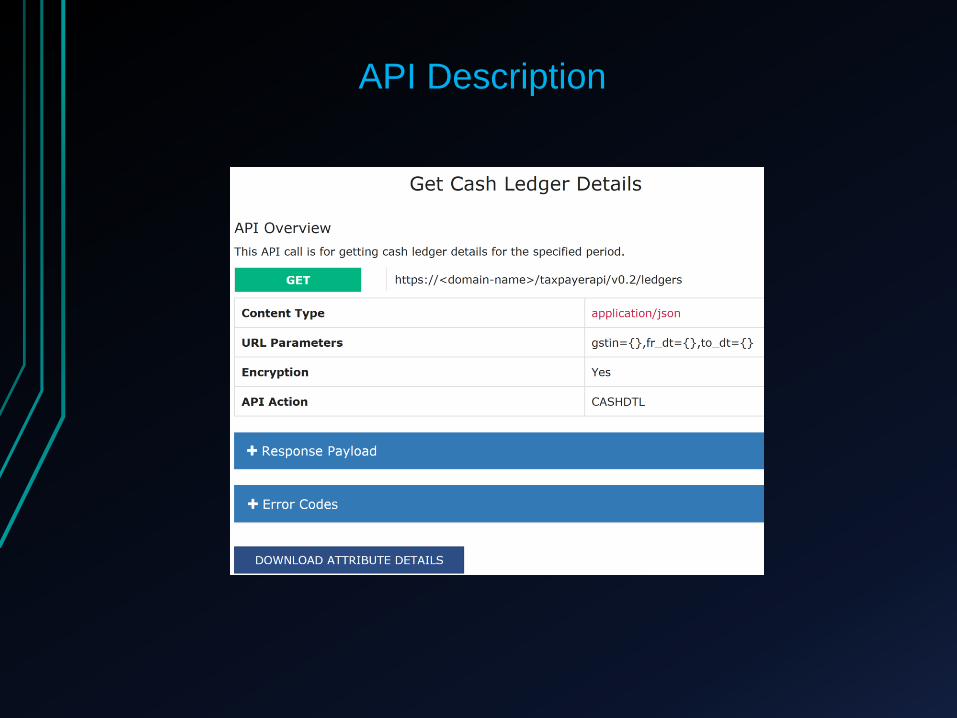

API Description

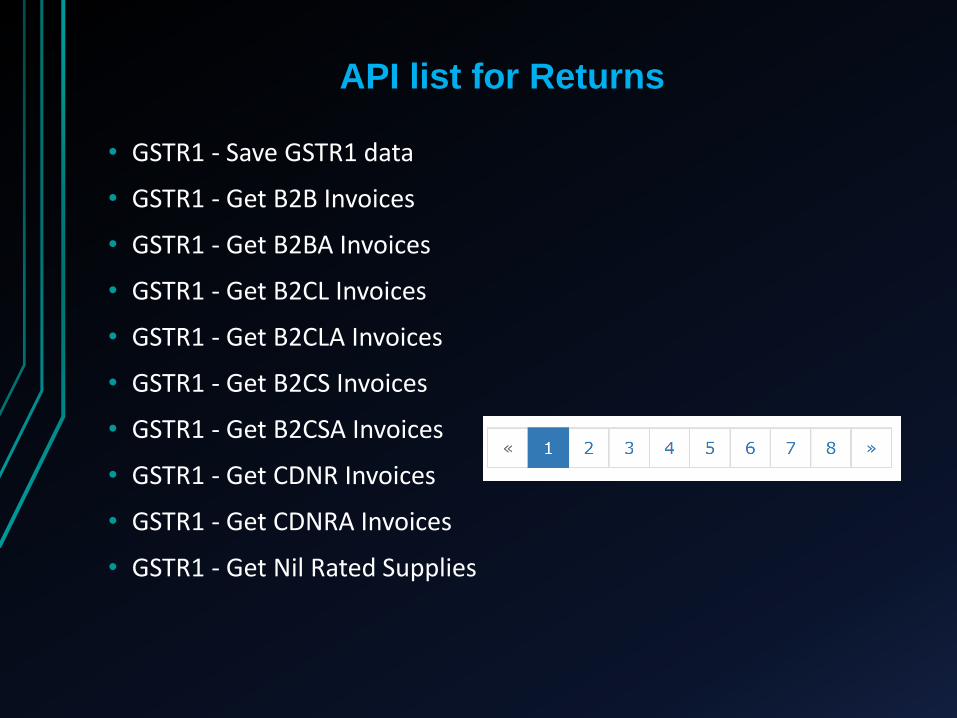

API list for Returns

• GSTR1 - Save GSTR1 data

• GSTR1 - Get B2B Invoices

• GSTR1 - Get B2BA Invoices

• GSTR1 - Get B2CL Invoices

• GSTR1 - Get B2CLA Invoices

• GSTR1 - Get B2CS Invoices

• GSTR1 - Get B2CSA Invoices

• GSTR1 - Get CDNR Invoices

• GSTR1 - Get CDNRA Invoices

• GSTR1 - Get Nil Rated Supplies

Schema / XML Fields

S No JSON attribute Description Format Sample Value

1 gstin GSTIN of the Tax Payer Alphanumeric with 15 characters 07CQZCD1111I4Z7

2 fp Return period String (MMYYYY) 082016

3 gt Gross Turnover in the preceding Financial Year Decimal(15, 2) 1000.00

4 cur_gt Gross Turnover - April to June, 2017 Decimal(15, 2) 1000.00

5 version Version of Application String GST1.00

6 hash Hash Code String

7 mode Mode of Application String (OFFLINE) of

8 b2b B2B Invoices B2B Invoice Data

9 b2cl B2C Large Invoices B2CL Invoice data

10 b2cs B2C Small Invoices B2CS Invoice Data

11 nil Nil Supplies Nil Rated Invoice Data

12 exp Exports Exp Invoice Data

13 at Advance Tax AT Invoice data

14 txpd Advance Adjusted Detail Advance Tax paid details

15 hsn hsn_summary_details HSNSUM

16 cdnr Credit and Debit Note CDNR

17cdnur

Credit and Debit Note for Unregistered

TaxpayersCDNUR

18 doc_Issue Document Issue Documents Issue

GSTR1 Data

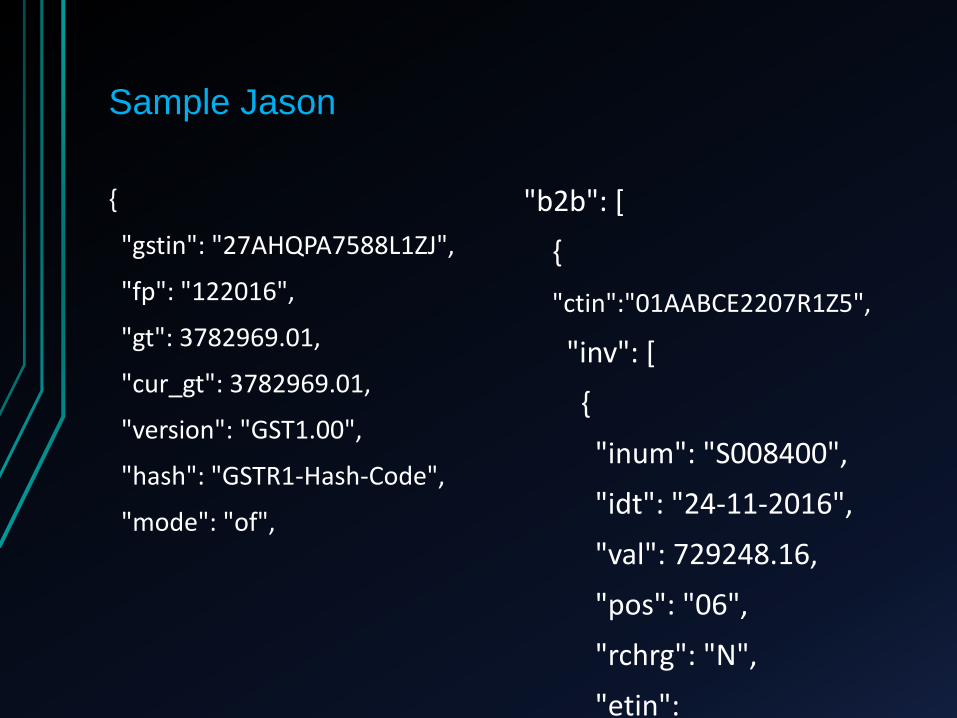

Sample Jason

{

"gstin": "27AHQPA7588L1ZJ",

"fp": "122016",

"gt": 3782969.01,

"cur_gt": 3782969.01,

"version": "GST1.00",

"hash": "GSTR1-Hash-Code",

"mode": "of",

"b2b": [

{

"ctin":"01AABCE2207R1Z5",

"inv": [

{

"inum": "S008400",

"idt": "24-11-2016",

"val": 729248.16,

"pos": "06",

"rchrg": "N",

"etin": "01AABCE5507R1Z4",

16

2. Accounting + Software in GST

ERP Accounting Application

1. SAP

2. Oracle

3. Microsoft

4. RAMCO

And Many other Proprietary Softwares

17

Some Accounting Applications used by- SME

And Many other Proprietary Softwares

18

Desktop Application Online Platform

Tally ERP Zoho

Profit Numberz

Marg Quick Books

Busy Xero

Saral Wave

GST Implementation Challenges

Is Accounting Software a Challenge ?

Or

Accounting / Data Capturing ?

19

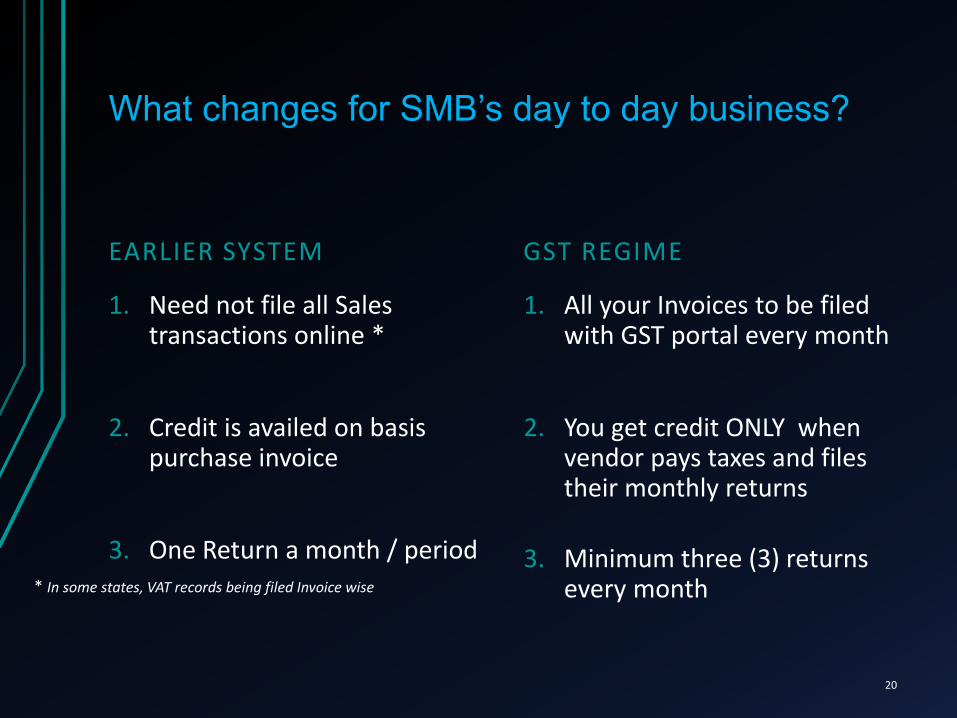

What changes for SMB’s day to day business?

EARLIER SYSTEM

1. Need not file all Sales transactions online *

2. Credit is availed on basis purchase invoice

3. One Return a month / period

GST REGIME

1. All your Invoices to be filed with GST portal every month

2. You get credit ONLY when vendor pays taxes and files their monthly returns

3. Minimum three (3) returns every month

20

* In some states, VAT records being filed Invoice wise

What changes for SMB’s day to day business?

EARLIER SYSTEM

4. Vendor follow-up mostly for ‘C’ Forms

5. Multiple Law Compliance

6. Error – Revised Returns

GST REGIME

4. Got to follow up with Vendor every Month.

5. Single Window Filings.

6. No Revised Return*

21

Master Record Changes

22

Master Related – Chart of Accounts

23

Current

Tax Ledgers

• Central Excise , PLA etc.

• VAT / Central Sales Tax

• Service Tax

• Cess

• Inventory

• May or may not integrated with books

GST

Tax Ledger

• CGST,SGST IGST

• Separate for each state

• Input; Output; Payment

• Inventory

• Inventory needs to be integrated in the ERP system

• Basis of HSN / SAC codes

Master Related - Chart of Accounts

24

Current

Vendor / Customer Masters

Customer / Vendor Code + Name

Address , Tax Jurisdictions

Payment Terms etc.

Taxation

Invoicing rates mostly at gross levels at end of invoice.

Point of Incidence – Tax calculation Logic for CE/VAT/ST

GST

Vendor / Customer Masters

Existing + GSTIN

Multiple GSTIN

Taxation

Line item level Rates with HSN/SAC

Destination based Taxation (CGST+SGST / IGST)

Transaction Changes –Outward Supply

25

Revenue Related Configurations

1. Supply Type• Independent / Composite /

Mixed

2. Type of Tax• C + S / { I }

3. Rate of Tax• Taxable / Exempted

4. Value of Tax• Transaction Value

• Taxable Value

5. Time of invoice• Due Date of Provision

6. Advance • Receipt + Adjustment

7. POS• If Interstate

• Bill to Ship to, Specific mention

8. HSN

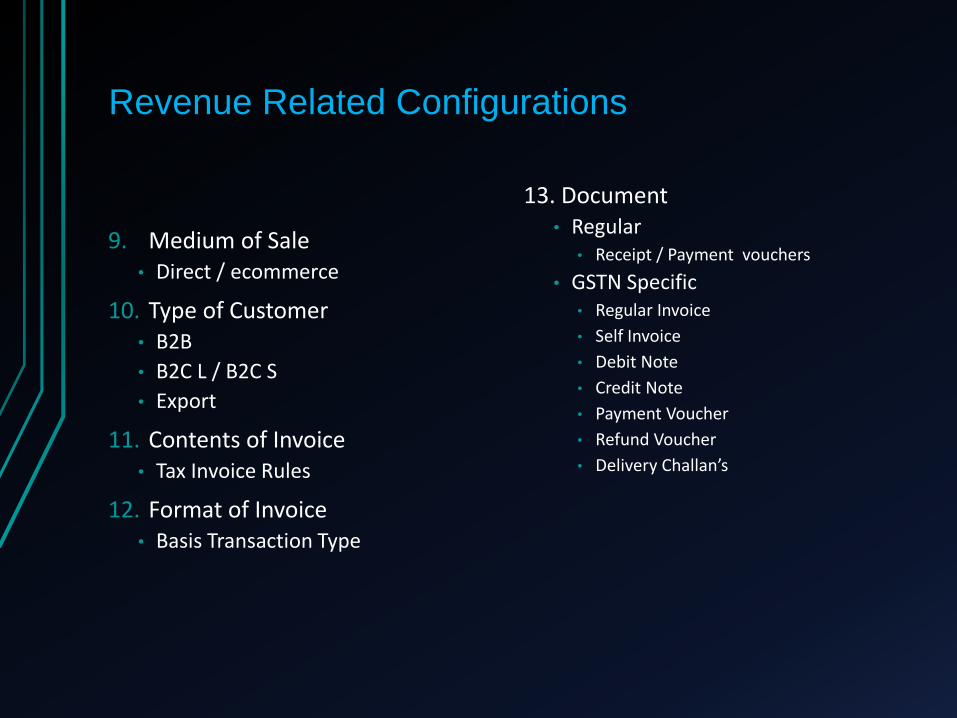

Revenue Related Configurations

9. Medium of Sale• Direct / ecommerce

10. Type of Customer• B2B

• B2C L / B2C S

• Export

11. Contents of Invoice• Tax Invoice Rules

12. Format of Invoice• Basis Transaction Type

13. Document• Regular

• Receipt / Payment vouchers

• GSTN Specific• Regular Invoice

• Self Invoice

• Debit Note

• Credit Note

• Payment Voucher

• Refund Voucher

• Delivery Challan’s

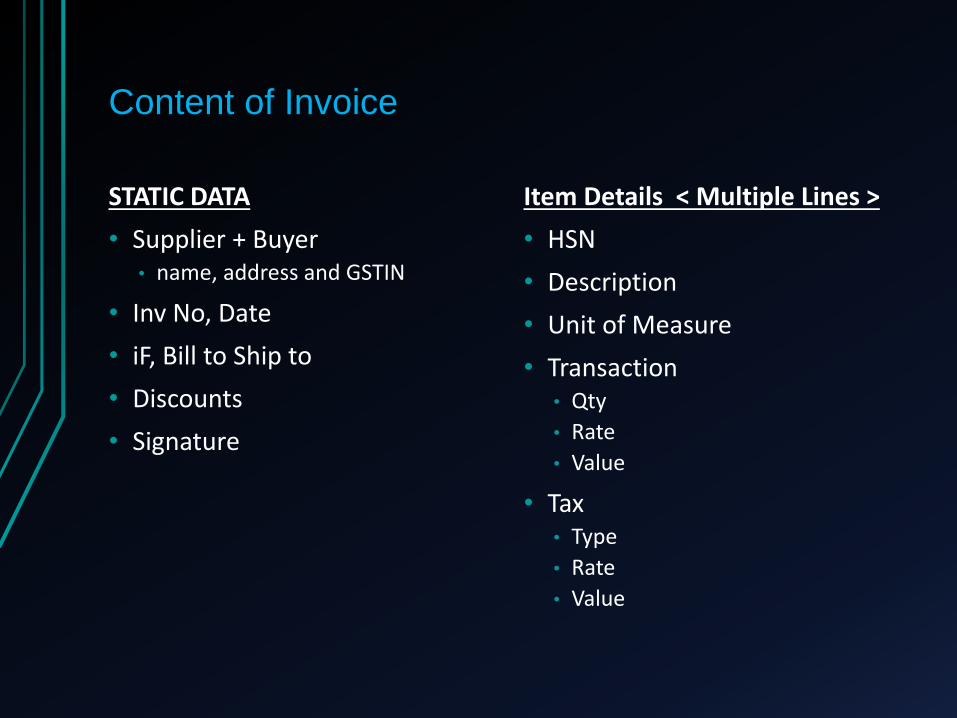

Content of Invoice

STATIC DATA

• Supplier + Buyer• name, address and GSTIN

• Inv No, Date

• iF, Bill to Ship to

• Discounts

• Signature

Item Details < Multiple Lines >

• HSN

• Description

• Unit of Measure

• Transaction• Qty

• Rate

• Value

• Tax• Type

• Rate

• Value

Sample Format

Composition supplier ?

Warranty ?

Taxable & Exempted supply In one Invoice ?

Composite supply/ Mixed Supply ?

Buy one get one offers ?

Works contractor on immovable ?

Discount through Tax Invoice / Discount after issuing Tax Invoice ?

GTA service ?

Bank ?

Passenger Transportation ?

B2B - over the counter purchases ?

Computer generated Invoice ?

Commission or packing charged in Invoice except pure agent ?

Transportation charges GST Rate ?

30

Multiple Formats

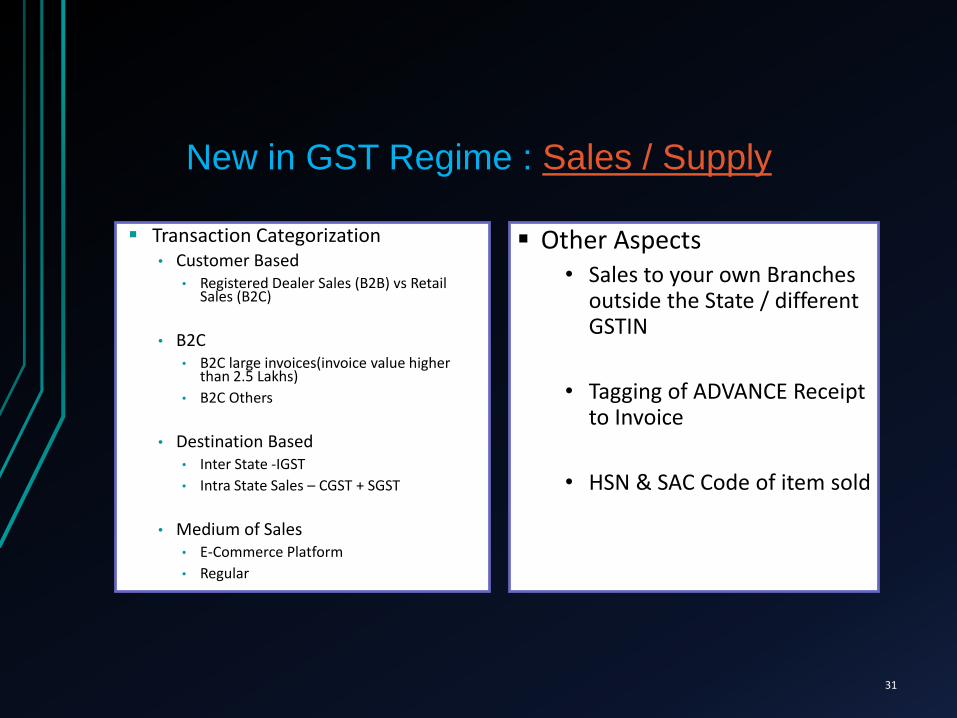

Other Aspects• Sales to your own Branches

outside the State / different GSTIN

• Tagging of ADVANCE Receipt to Invoice

• HSN & SAC Code of item sold

New in GST Regime : Sales / Supply

Transaction Categorization• Customer Based

• Registered Dealer Sales (B2B) vs Retail Sales (B2C)

• B2C• B2C large invoices(invoice value higher

than 2.5 Lakhs)

• B2C Others

• Destination Based• Inter State -IGST

• Intra State Sales – CGST + SGST

• Medium of Sales• E-Commerce Platform

• Regular

31

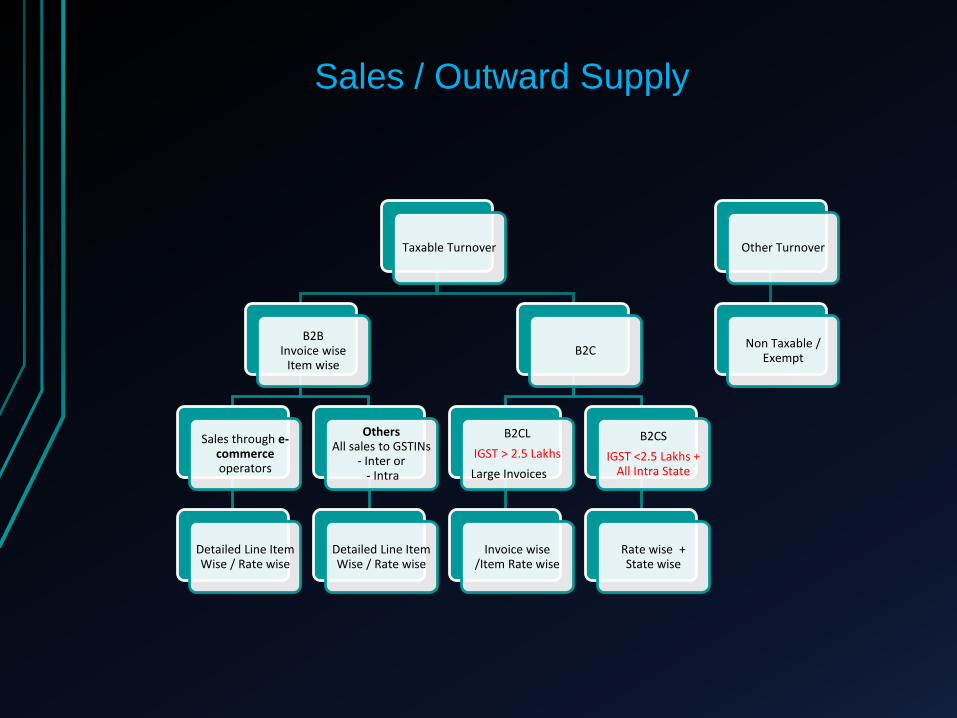

Sales / Outward Supply

Taxable Turnover

B2BInvoice wise

Item wise

Sales through e-commerce operators

Detailed Line Item Wise / Rate wise

Others All sales to GSTINs

- Inter or- Intra

Detailed Line Item Wise / Rate wise

B2C

B2CL

IGST > 2.5 Lakhs

Large Invoices

Invoice wise /Item Rate wise

B2CS

IGST <2.5 Lakhs + All Intra State

Rate wise + State wise

Other Turnover

Non Taxable / Exempt

For B2B – SUPPLY

Capture all the following details in the invoice

Additional Info• GSTIN/UIN of buyer

• Place of supply ( Bill to & Ship to – Different States)

• Description and HSN/SAC codes of the goods and services rendered

• Is the tax paid under reverse charge

• Is Transaction through E-Commerce portal

Regular Info• Invoice number, date and value of invoice and taxable value

• Tax rate and amount

33

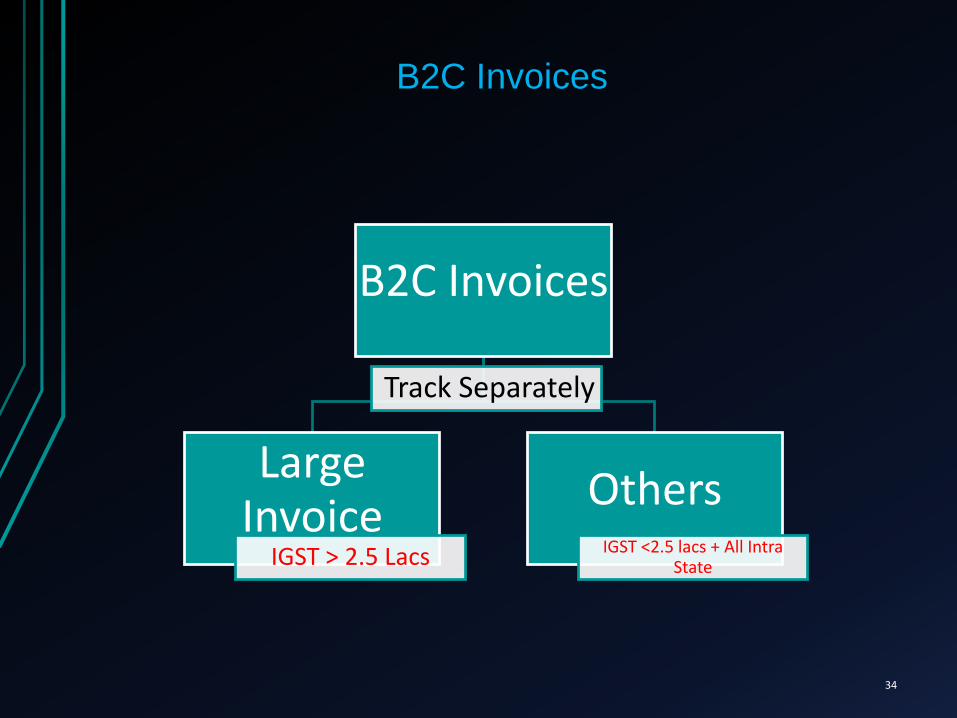

B2C Invoices

34

B2C Invoices

Track Separately

Large Invoice

IGST > 2.5 Lacs

OthersIGST <2.5 lacs + All Intra

State

Branch Transfer

In GST, Stock Transfer is treated as B2B Sales

Inter State : Transfer to its own branch/warehouse

located in other state

Intra State : If the Branch has separate GSTIN with

in the State

35

Old Law :This was considered as Stock Transfer earlier andNo Taxation

Branch Transfer - Accounting

Record Transaction effecting GST Liability in Supplier Branch

GST Input in Recipient Branch

Sales Accounting

If Consolidated Books – Contra Sales and Purchases

If Separate Set of Books – Record as Intercompany and eliminate in Consolidation

P&L Impact on Consolidation : Nil

36

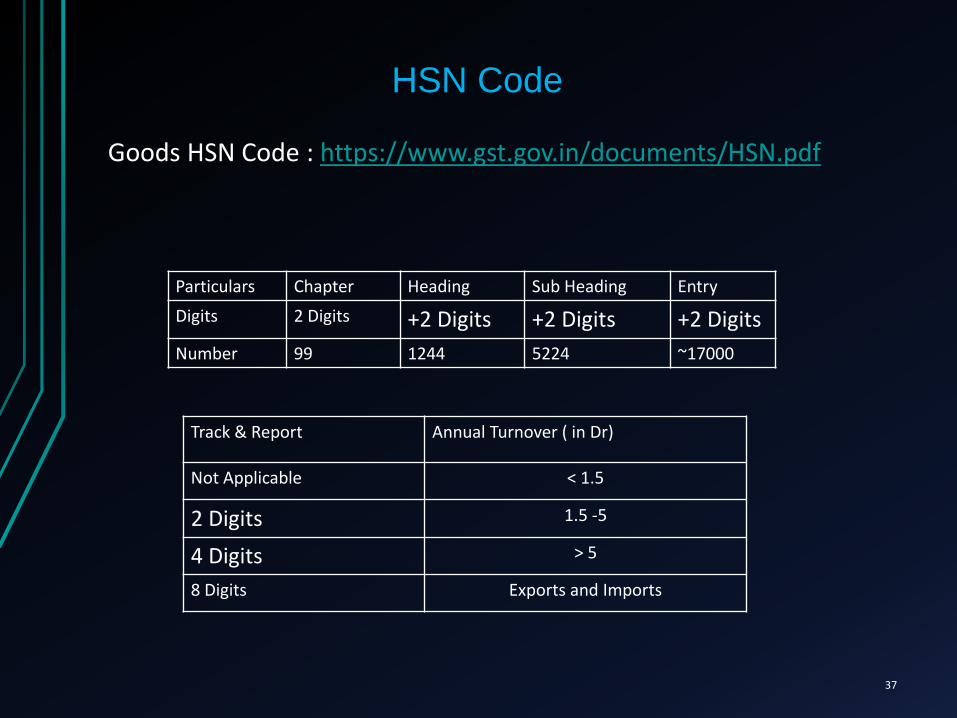

HSN Code

Goods HSN Code : https://www.gst.gov.in/documents/HSN.pdf

37

Track & Report Annual Turnover ( in Dr)

Not Applicable < 1.5

2 Digits 1.5 -5

4 Digits > 5

8 Digits Exports and Imports

Particulars Chapter Heading Sub Heading Entry

Digits 2 Digits +2 Digits +2 Digits +2 Digits

Number 99 1244 5224 ~17000

Services : SAC codes

The SAC is now Chapter 99 HSN list, released by CBEC

38

Annual Turnover( in Cr)

Reporting

< 1.5 Optional

> 1.5 Mandatory

ADVANCE Receipt – Invoice Mapping

• Month of Advance Receipt – Pay GST

<Key Element : Document Number>

• Month of Invoice – Reverse Receipt Paid Taxes, by referring <Document Number> + <Invoice Number>

39

Sales through e-commerce platform

E-Commerce operator collects 1% of the sale amount as TCS

TCS collected can be claimed against the Output Liability

Additional Data Capture :A. GSTIN of e-commerce operator

B. Merchant ID issued by e-commerce operator

40

Track & Report Invoice Series – Month on Month

Series of Invoices

Total Invoices

Cancelled Invoices

Net Invoices Issued

• From Number

• To Number

41

Transaction Changes – Inward Supply

42

GST Regime : Changes

• Seamless flow of Credit – Reduction in cost

• Vendor Management Crucial – Credit availed on time

• All eligible Inputs/Capital goods Credit eligible• previously VAT / Service Tax are not inter allowed

43

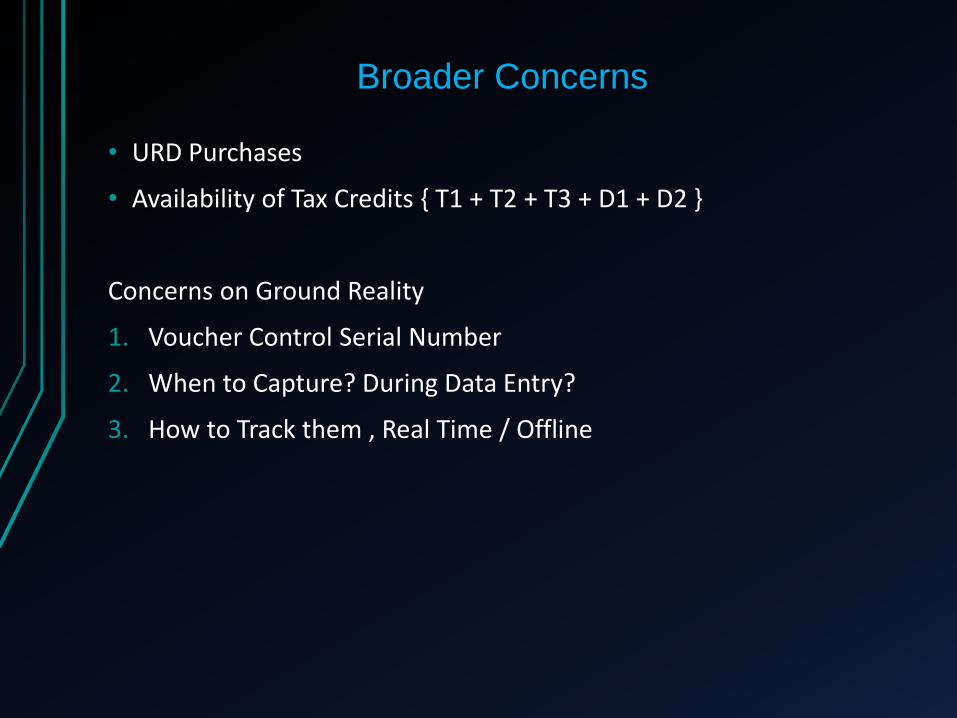

Broader Concerns

• URD Purchases

• Availability of Tax Credits { T1 + T2 + T3 + D1 + D2 }

Concerns on Ground Reality

1. Voucher Control Serial Number

2. When to Capture? During Data Entry?

3. How to Track them , Real Time / Offline

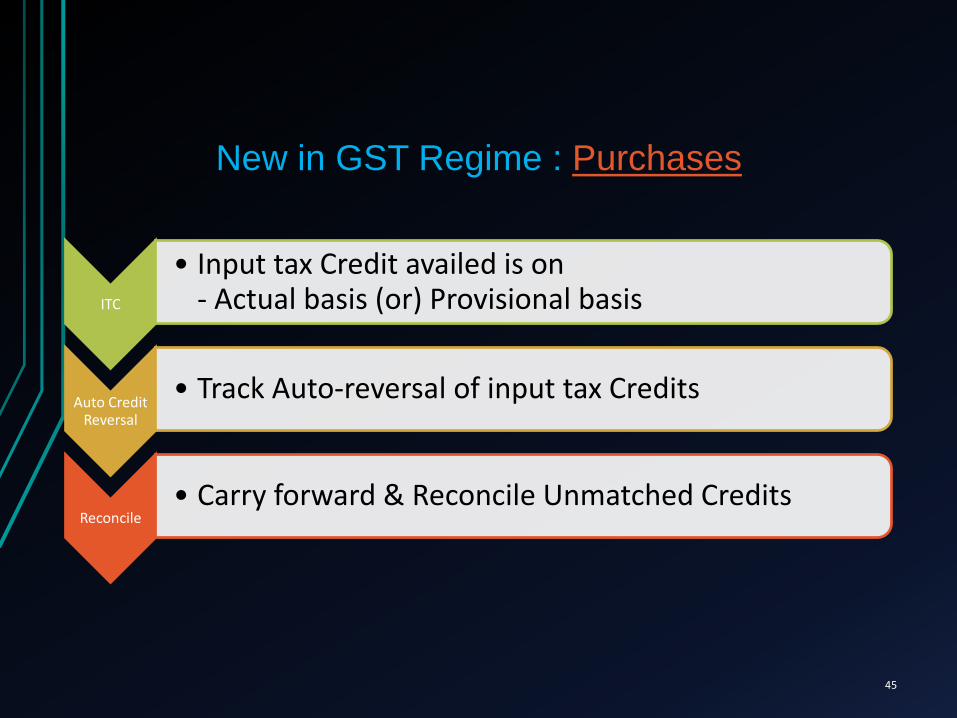

New in GST Regime : Purchases

ITC

• Input tax Credit availed is on - Actual basis (or) Provisional basis

Auto Credit Reversal

• Track Auto-reversal of input tax Credits

Reconcile• Carry forward & Reconcile Unmatched Credits

45

Additional details to be captured - Purchases

GSTIN

• GSTIN’s of Vendor to be captured in Tax Masters

Import of Goods

• Invoice Number, Date and value of Bill of entry, HSN/SAC

Reverse Charge

• Document Number and date

Credit

• Tax Credit segregated – ( Eligible / ineligible)

Segregate

• Input Tax Credit into -

• Input Goods / Services (or) Capital goods

46

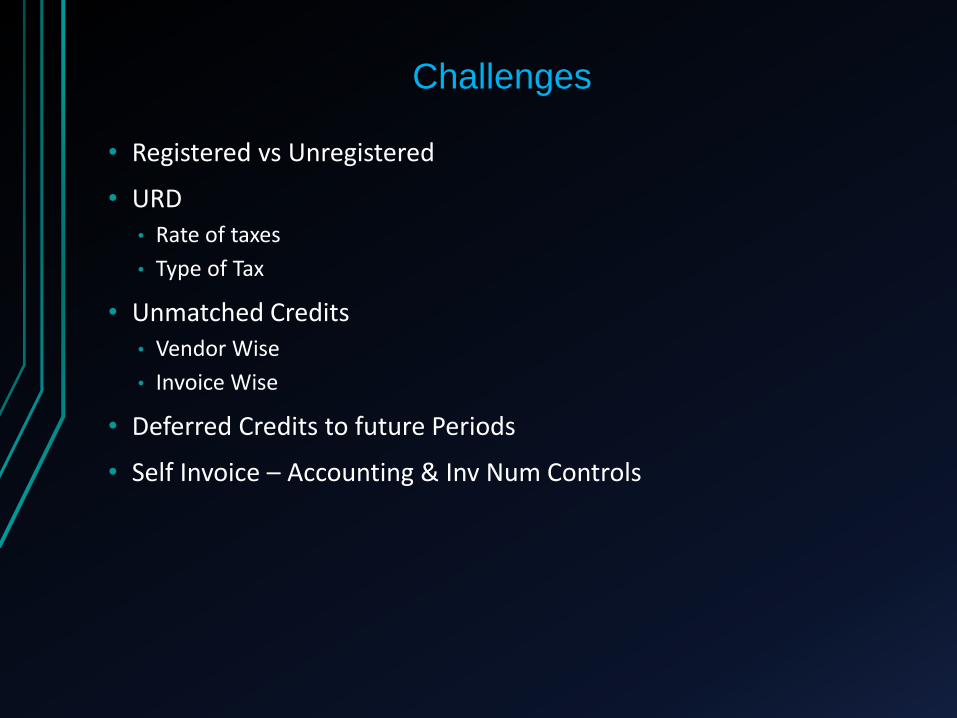

Challenges

• Registered vs Unregistered

• URD• Rate of taxes

• Type of Tax

• Unmatched Credits• Vendor Wise

• Invoice Wise

• Deferred Credits to future Periods

• Self Invoice – Accounting & Inv Num Controls

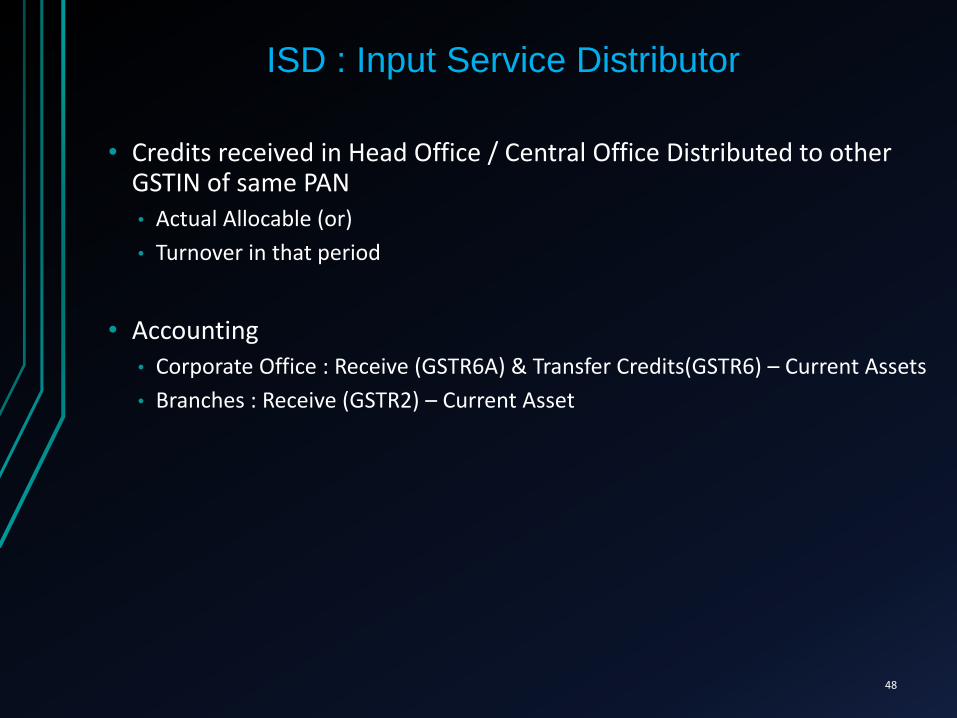

ISD : Input Service Distributor

• Credits received in Head Office / Central Office Distributed to other GSTIN of same PAN• Actual Allocable (or)

• Turnover in that period

• Accounting• Corporate Office : Receive (GSTR6A) & Transfer Credits(GSTR6) – Current Assets

• Branches : Receive (GSTR2) – Current Asset

48

TDS Credits

Additional details to be captured (these will be auto populated in returns)• GSTIN of deductor

• Date of payment received

• Value on which TDS deducted

Existing Information• Number, date and value of invoice

• Taxable value

• Tax rate and amount

Assesse can download certificate Form GSTR 7A from the portal.

49

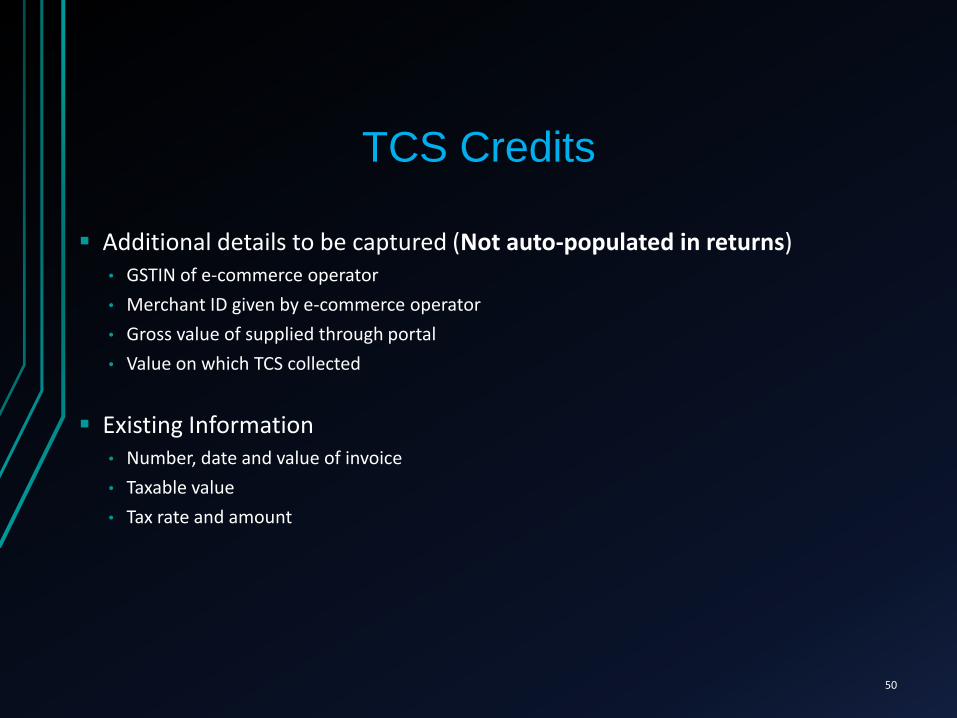

TCS Credits

Additional details to be captured (Not auto-populated in returns)• GSTIN of e-commerce operator

• Merchant ID given by e-commerce operator

• Gross value of supplied through portal

• Value on which TCS collected

Existing Information• Number, date and value of invoice

• Taxable value

• Tax rate and amount

50

Monthly Activities Summary

51

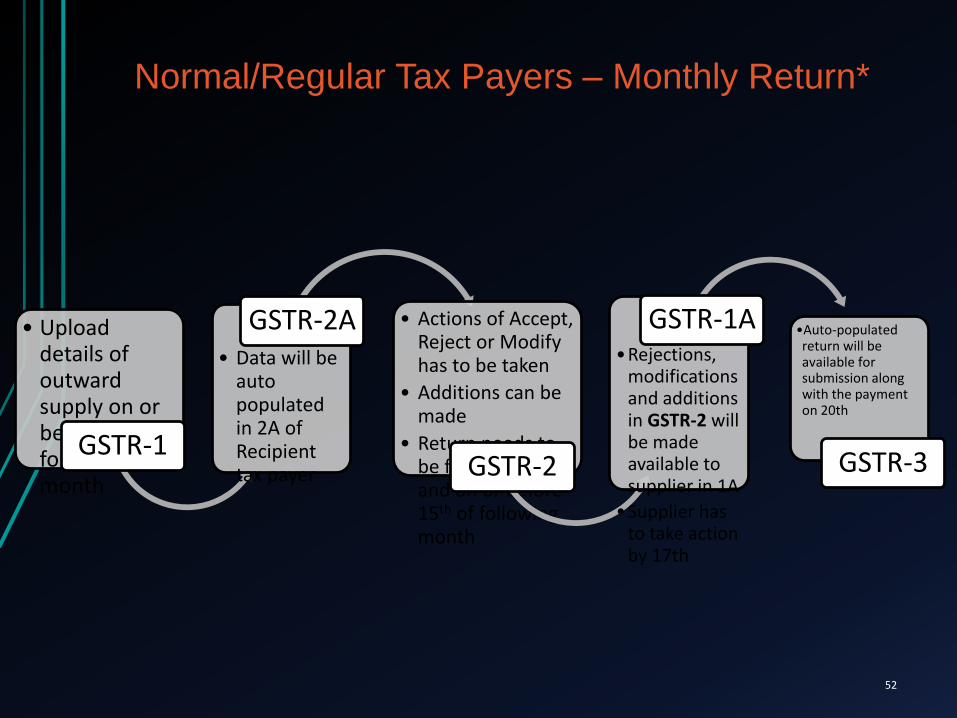

Normal/Regular Tax Payers – Monthly Return*

• Upload details of outward supply on or before 10th of following month

GSTR-1

• Data will be auto populated in 2A of Recipient tax payer

GSTR-2A • Actions of Accept, Reject or Modify has to be taken

• Additions can be made

• Return needs to be filed after 10th

and on or before 15th of following month

GSTR-2

•Rejections, modifications and additions in GSTR-2 will be made available to supplier in 1A

•Supplier has to take action by 17th

GSTR-1A •Auto-populated return will be available for submission along with the payment on 20th

GSTR-3

52

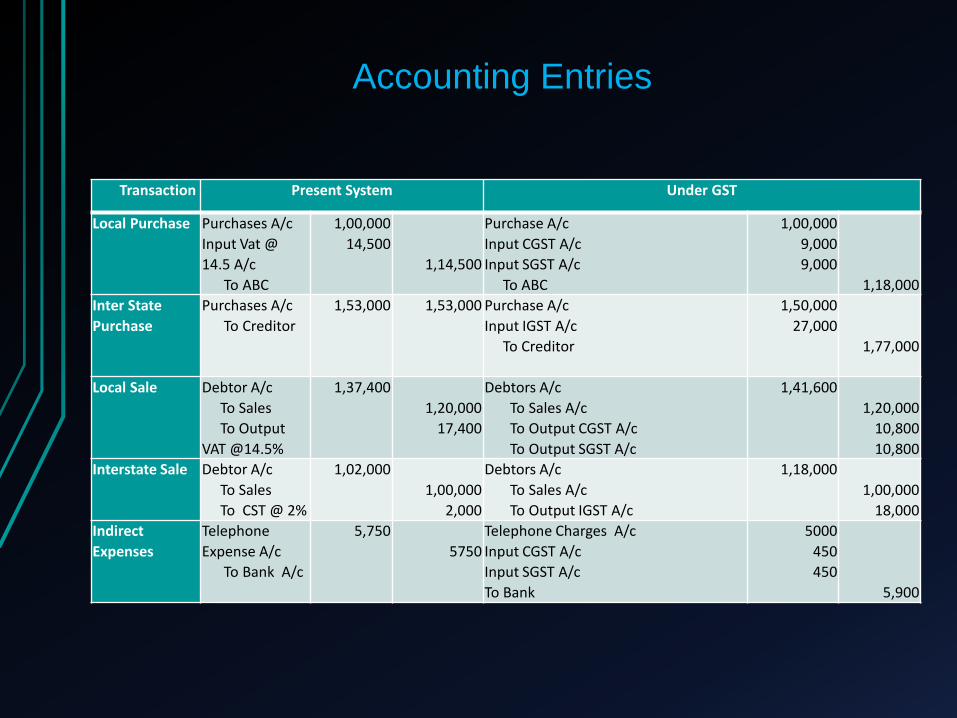

Sample Accounting Entries

53

Accounting Entries

Transaction Present System Under GST

Local Purchase Purchases A/c

Input Vat @

14.5 A/c

To ABC

1,00,000

14,500

1,14,500

Purchase A/c

Input CGST A/c

Input SGST A/c

To ABC

1,00,000

9,000

9,000

1,18,000

Inter State

Purchase

Purchases A/c

To Creditor

1,53,000 1,53,000 Purchase A/c

Input IGST A/c

To Creditor

1,50,000

27,000

1,77,000

Local Sale Debtor A/c

To Sales

To Output

VAT @14.5%

1,37,400

1,20,000

17,400

Debtors A/c

To Sales A/c

To Output CGST A/c

To Output SGST A/c

1,41,600

1,20,000

10,800

10,800

Interstate Sale Debtor A/c

To Sales

To CST @ 2%

1,02,000

1,00,000

2,000

Debtors A/c

To Sales A/c

To Output IGST A/c

1,18,000

1,00,000

18,000

Indirect

Expenses

Telephone

Expense A/c

To Bank A/c

5,750

5750

Telephone Charges A/c

Input CGST A/c

Input SGST A/c

To Bank

5000

450

450

5,900

Reconcile with GSTN

Up on GSTR -1 – Transfer to Liability Ledger

Dr Output CGST A/c

Dr Output SGST A/c

Dr Output IGST A/c

Cr Liability Ledger CGST A/c

Cr Liability Ledger SGST A/c

Cr Liability Ledger IGST A/c

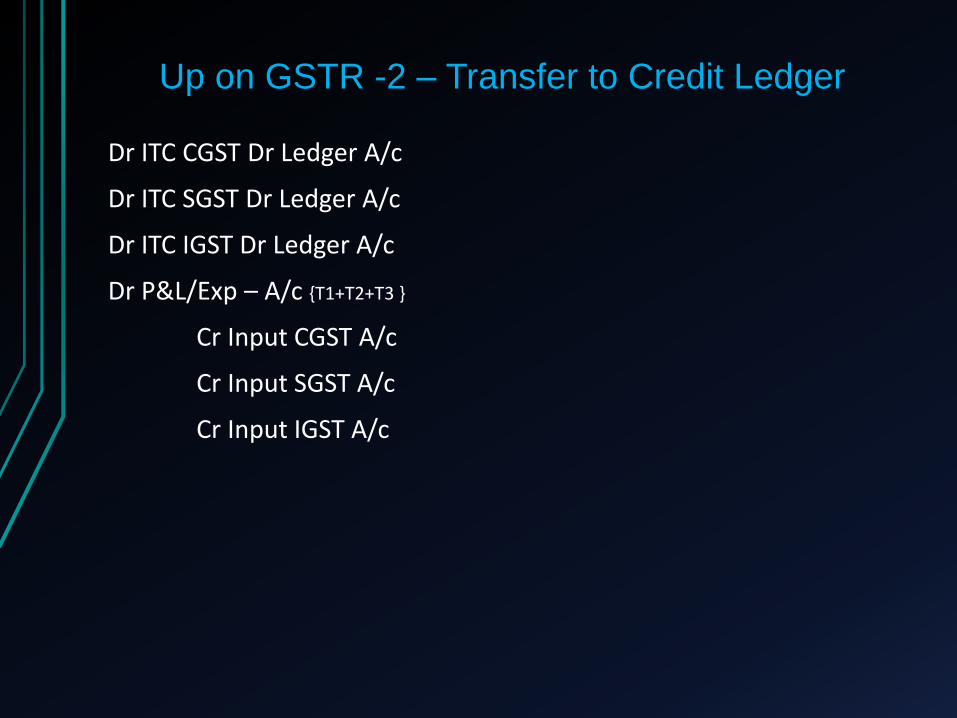

Up on GSTR -2 – Transfer to Credit Ledger

Dr ITC CGST Dr Ledger A/c

Dr ITC SGST Dr Ledger A/c

Dr ITC IGST Dr Ledger A/c

Dr P&L/Exp – A/c {T1+T2+T3 }

Cr Input CGST A/c

Cr Input SGST A/c

Cr Input IGST A/c

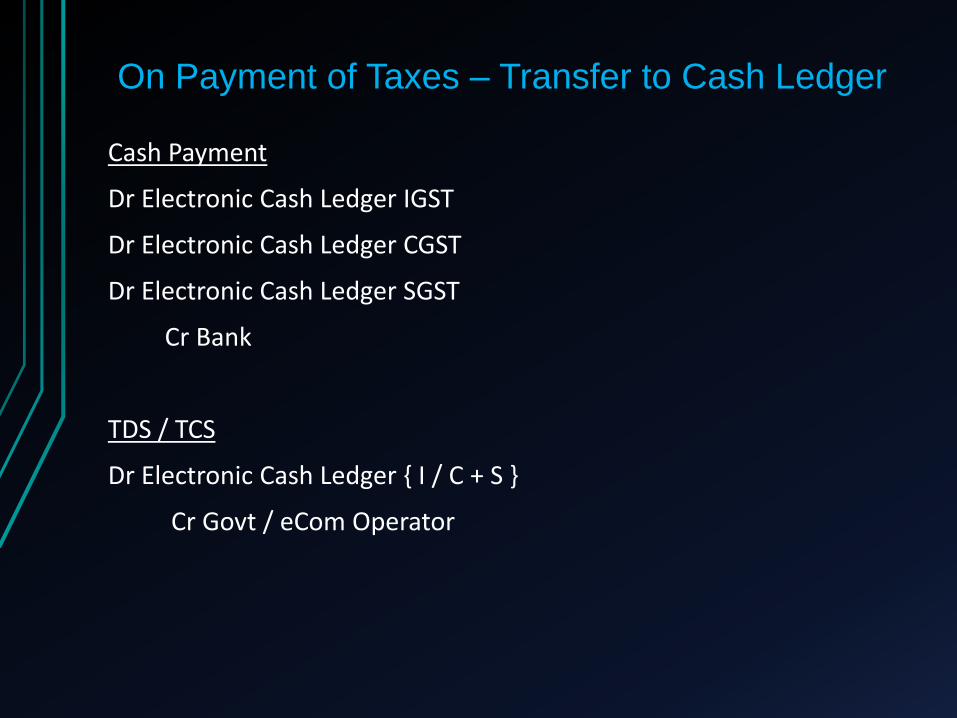

On Payment of Taxes – Transfer to Cash Ledger

Cash Payment

Dr Electronic Cash Ledger IGST

Dr Electronic Cash Ledger CGST

Dr Electronic Cash Ledger SGST

Cr Bank

TDS / TCS

Dr Electronic Cash Ledger { I / C + S }

Cr Govt / eCom Operator

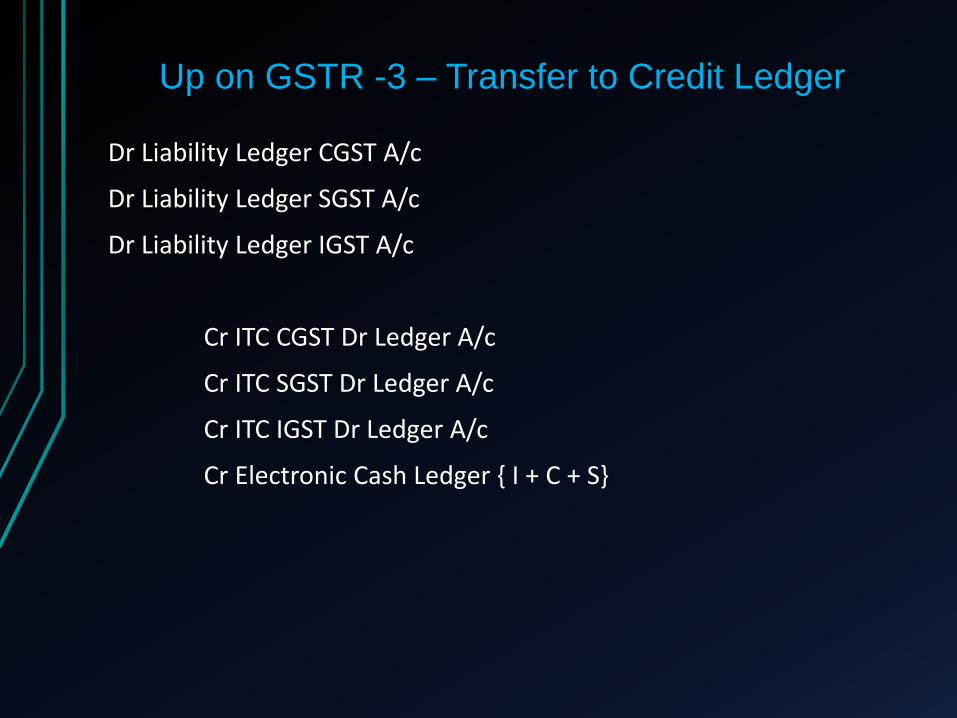

Up on GSTR -3 – Transfer to Credit Ledger

Dr Liability Ledger CGST A/c

Dr Liability Ledger SGST A/c

Dr Liability Ledger IGST A/c

Cr ITC CGST Dr Ledger A/c

Cr ITC SGST Dr Ledger A/c

Cr ITC IGST Dr Ledger A/c

Cr Electronic Cash Ledger { I + C + S}

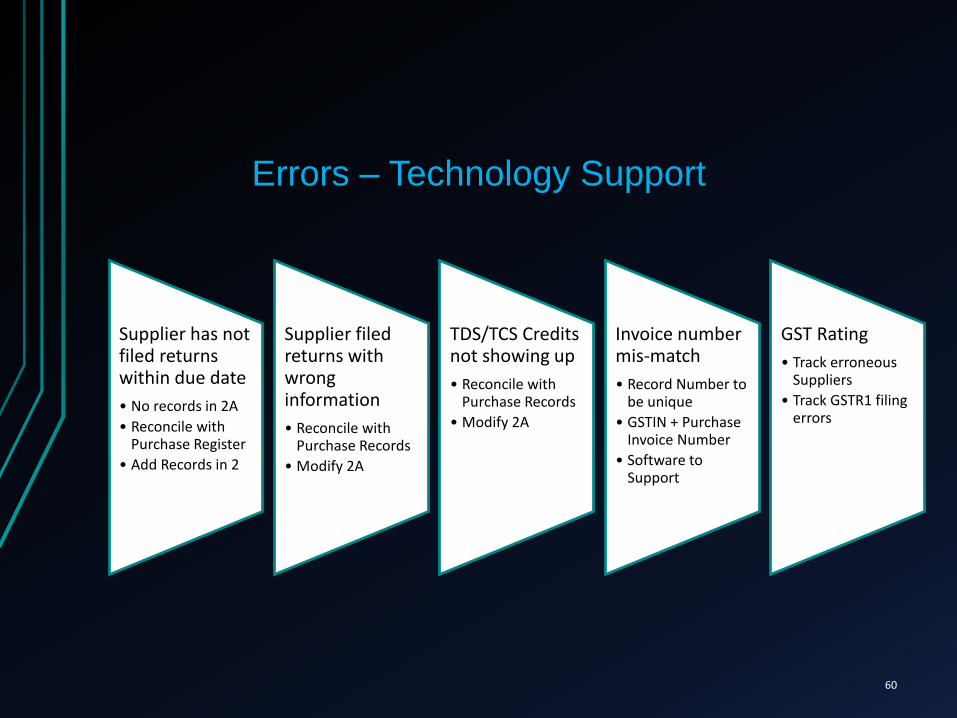

Errors – Technology Support

Supplier has not filed returns within due date

• No records in 2A

• Reconcile with Purchase Register

• Add Records in 2

Supplier filed returns with wrong information

• Reconcile with Purchase Records

• Modify 2A

TDS/TCS Credits not showing up

• Reconcile with Purchase Records

• Modify 2A

Invoice number mis-match

• Record Number to be unique

• GSTIN + Purchase Invoice Number

• Software to Support

GST Rating

• Track erroneous Suppliers

• Track GSTR1 filing errors

60

Consolidated Monthly Return - GSTR-3

Data from GSTR-1 and 2 auto-populates to GSTR-3

Accounting software should be Able to fetch data from the return

Auto reconcile with books of accounts

Estimate output tax Increase / Decrease considering rectification of communicated mismatches

Track and indicate NON RECTIFIED mismatches

61

Determine Liability

Liabilities can be Return related liabilities

Other than return related liabilities

Software should be able to track liabilities accordingly

Liability in GSTR-3 will be discharged utilising ITC - Credits from Electronic Credit Ledger

Electronic Cash Ledger-Balance Amount

62

Utilize ITC

Software must be able to track and consider restrictions on utilising Credits

63

Payments in GSTR-3

Utilising ITC, Software should be able to track and report Order of preference to utilise Credits

Provisional Credits, matched Credits, unmatched Credits and their reversal

Utilising Cash* Required amount of cash has to be deposited under CGST, SGST and IGST

Utilisation of the same can be made in GSTR-3

64

*Date of utilisation from cash ledger is the date of payment

Accounting Ledgers

Choice of Accounting

Consolidated

Vs

Detailed

List of Accounting Ledgers

+ Liability• Taxes Collected

• TDS Collected

• TCS Collected

• RCM Due

+ Input• Capital Goods

• Services

• Goods

Heads Tax Interest Penalty Fee Others

CGST

SGST

IGST

Cess

+ Payments Made

• Thru Cash

• TDS

• TCS

4 x5 Matrix

Setting of Liability by Period

Control Ledgers

• Credits• Suspense / Provisional Credits

• Credits Received in Advance

• Liabilities• Additional Recorded thru 1A

• Interest• Reversal – 42(9)

Reference to

• Party Wise / GSTIN

• Period Reference

69

3. RECONCILIATIONS

Reconciliation Books Vs Department

1. Registers1. FORM GST PMT-01 : Electronic tax Liability register

2. FORM GST PMT-02 : Electronic Credit Liability register

3. FORM GST PMT-05 : Electronic Cash Liability register

2. Forms1. FORM GST PMT-03 : Refund Rejected – Partially / Fully, communicated by

proper officer

2. FORM GST PMT-04 : Reporting any Discrepancy – Credit Ledger

3. FORM GST PMT-06 : Payment Challan

4. FORM GST PMT-07 : Reporting any Discrepancy – Cash Ledger

70

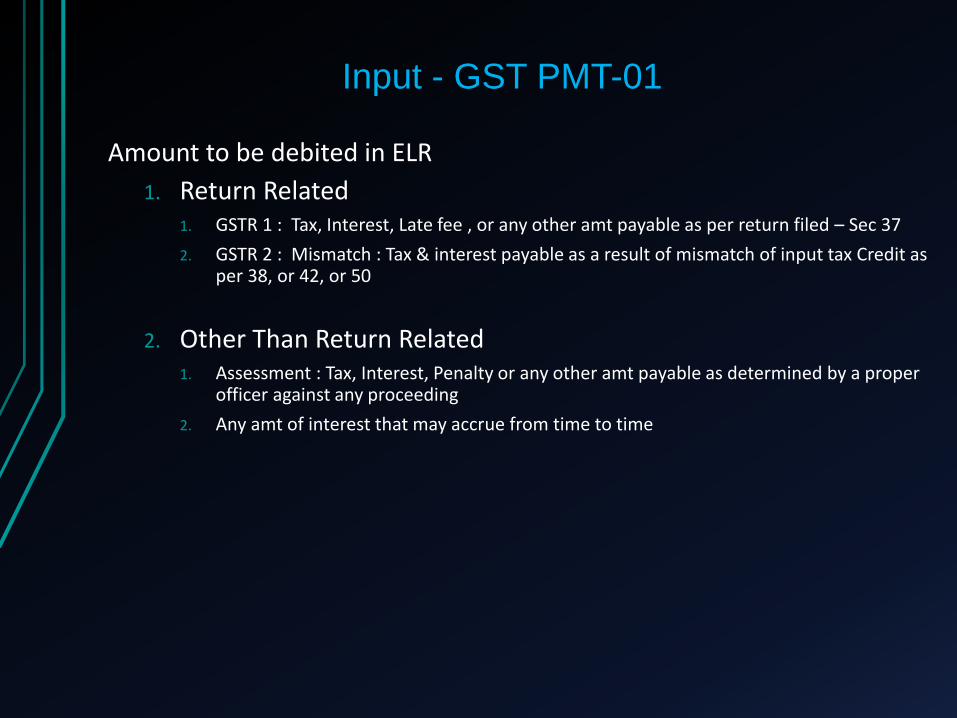

Electronic Tax Liability Register

Input - GST PMT-01

Amount to be debited in ELR

1. Return Related1. GSTR 1 : Tax, Interest, Late fee , or any other amt payable as per return filed – Sec 37

2. GSTR 2 : Mismatch : Tax & interest payable as a result of mismatch of input tax Credit as per 38, or 42, or 50

2. Other Than Return Related1. Assessment : Tax, Interest, Penalty or any other amt payable as determined by a proper

officer against any proceeding

2. Any amt of interest that may accrue from time to time

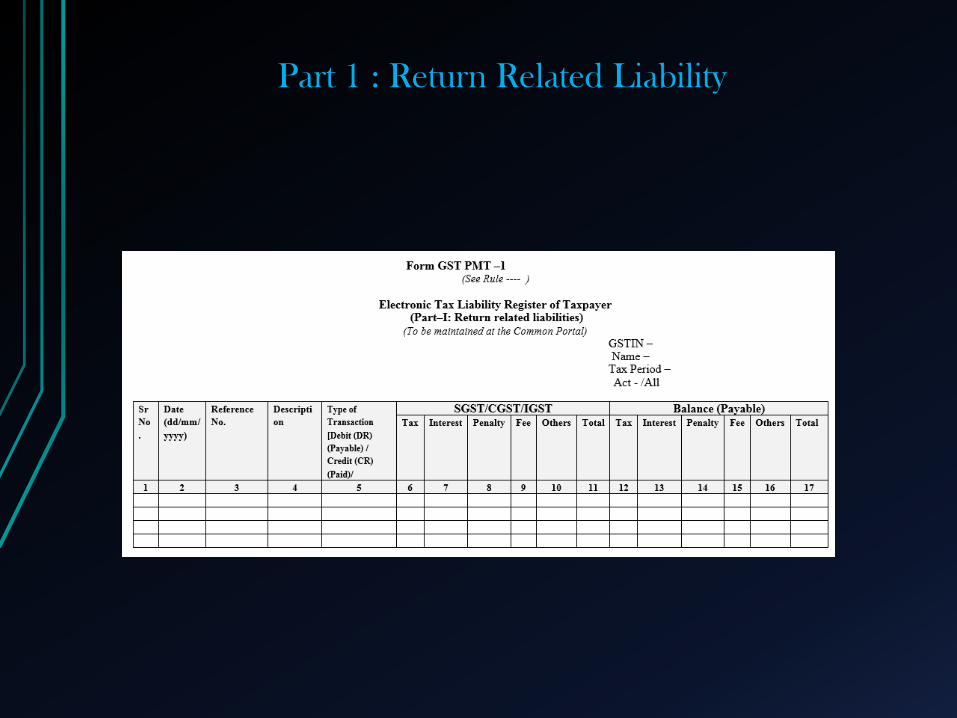

Part 1 : Return Related Liability

Part 2 : Other than Return Related Liability

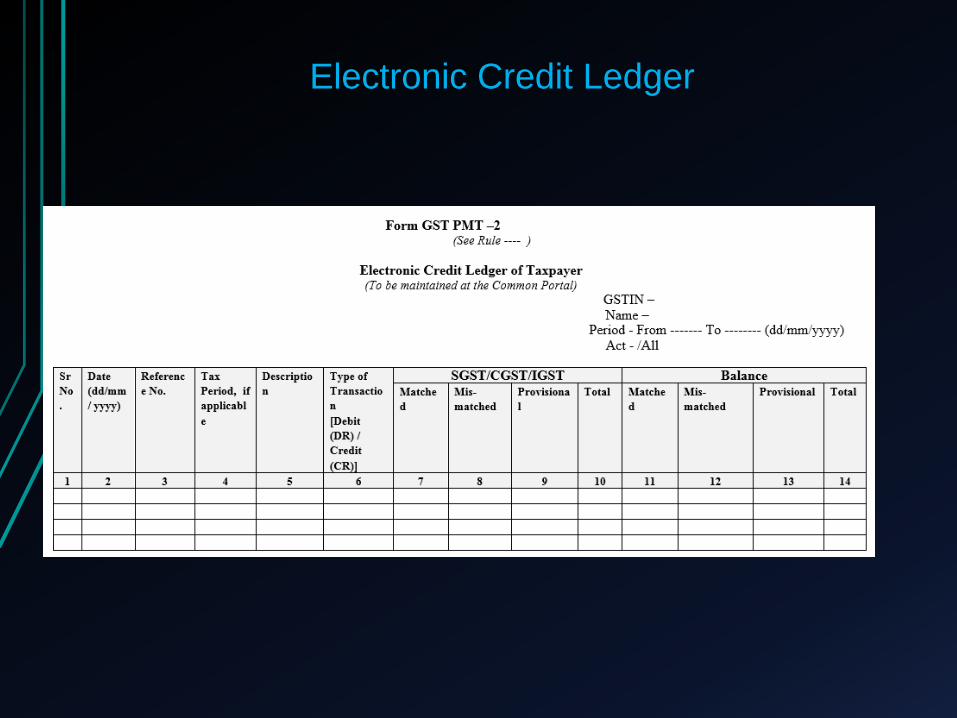

Electronic Credit Ledger

GST PMT-02 : Electronic Credit Ledger

Section 2(46) Electronic Credit ledger means the electronic Credit ledger referred to in section 49(2).

Provisional Credit up on filing of GSTR 2 Sec 41(1)

The following will recorder separately in the ledger,

Credit of inputs, capital goods, reverse charge claimed in return

Credit received through ISD

Credit on account of merger, pre-registration etc.

Utilisation of Credit from the same major head or from other major head (Cross utilization) will be recorded accordingly.

Utilisation of Credit for return and other than return related liabilities will be recorded separately.

Electronic Credit Ledger

Credits - Technology Support

Software must track the Credits appropriately. Credits can be Provisional Credits

Matched Credits and

Unmatched Credits

Software must track for Reversals of Credits with appropriate reasons

78

Electronic Cash Ledger

Cash ledger

Cash has to be deposited under respective heads

Cross utilisation between the ledgers with respect to Taxes, Interest, Fee, Penalty is not allowed

80

Major Heads Minor Heads

CGST Interest

SGST Penalty

IGST Fee

Cess Others

Payments – Technology Support

Electronic Cash Ledger Is like a e-wallet

Cash has to be deposited under relevant heads ONLY

And it shall be utilised accordingly for discharging liability

Date of deposit is not the date of payment

Date of utilisation from cash ledger is the date of the payment

81

GST PMT-05 : Electronic Cash Ledger

Section 2(43) Electronic cash ledger means the electronic cash ledger referred to in section 49(1)

Date of deposit = Date of Credit to the account of the appropriate Govt. in the authorised bank

Also Includes Sec 51 TDS & sec 52 TCS

Electronic Cash Ledger

Mismatch Reports

84

Mismatch Report – GSTN Portal

Captures mismatch reported by the Supplier Taxpayer & Receiver Taxpayer

Generated for every tax period on filing of valid GSTR 3 by the Taxpayer (or)

21st day of (M+1) whichever is later

Both supplier and receiver will be communicated on generation of mismatch report

85

Mismatch Report - Technology Support

Mismatch report with respect to taxable supplies will be Supplier mismatch < Out Put Tax Liability Addition >

Receiver mismatch < Input Tax Credit Mismatch >

E-Commerce mismatch

Accounting software to reconcile with the GSTN issued mismatch Report - ( Section A / B / C)

86

Understanding - Mismatch Report

Section A Elements in the transaction reported by receiver does not match with supplier

Addition/ modification of line items of invoices /debit notes issued by supplier, added by the receiver Taxpayer but not accepted by Supplier

ITC claimed in excess than reported by supplier

Section B Supplier has not filed return but receiver is claiming Credit

It is a mismatch resulting in Creation of output liability of receiver taxpayer due to reversal of ITC claimed by the receiver

For which the supplier has not paid tax by not filing valid GSTR 3

87

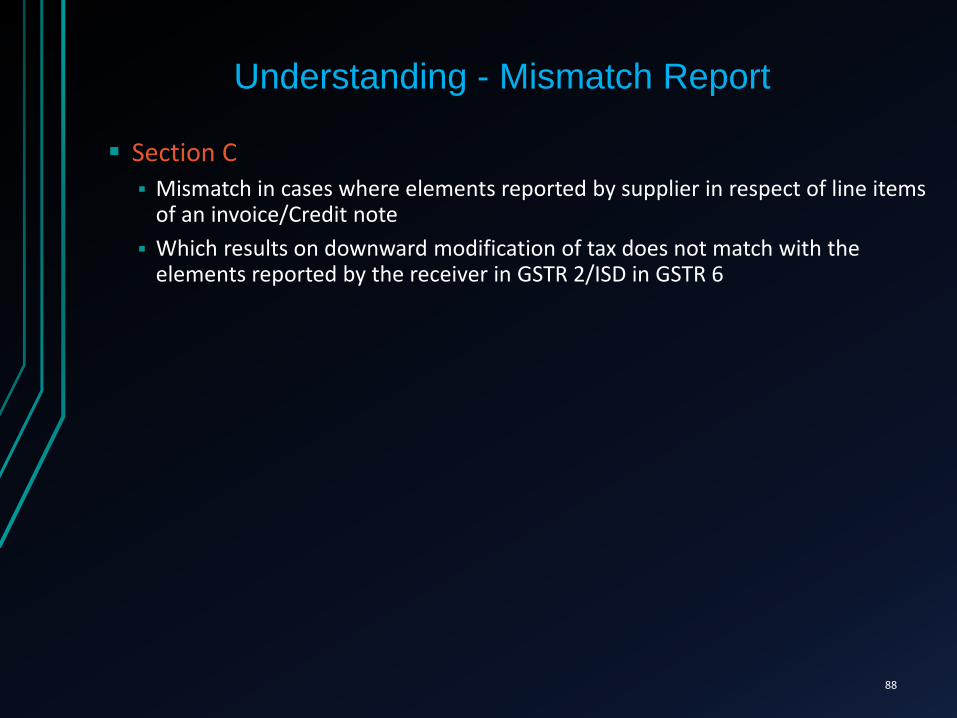

Understanding - Mismatch Report

Section C Mismatch in cases where elements reported by supplier in respect of line items

of an invoice/Credit note

Which results on downward modification of tax does not match with the elements reported by the receiver in GSTR 2/ISD in GSTR 6

88

89

4. Transitional Related Challenges

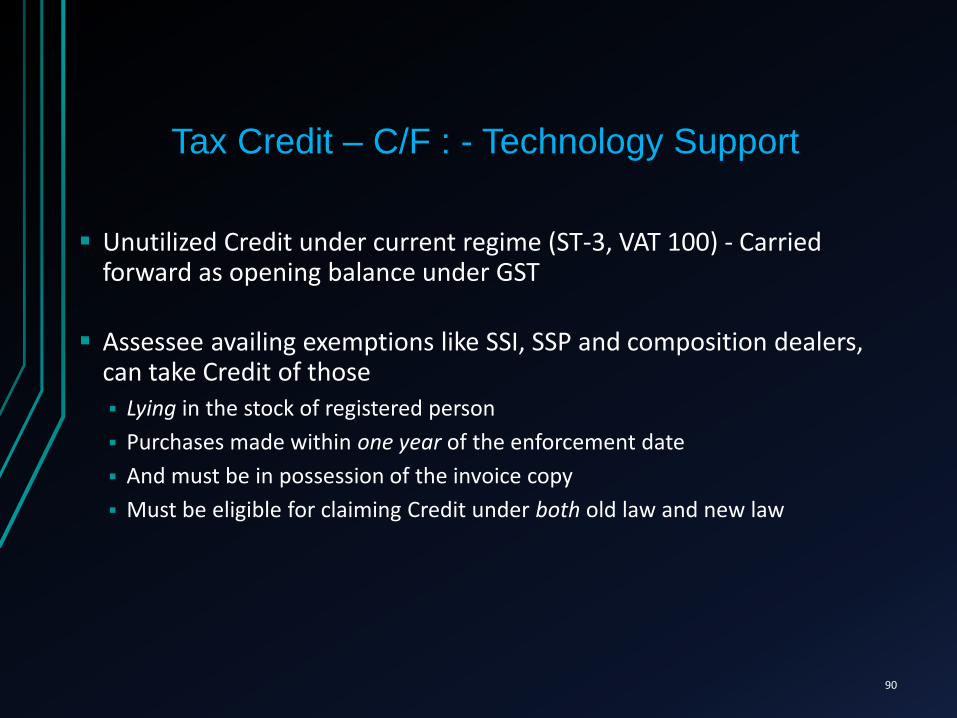

Tax Credit – C/F : - Technology Support

Unutilized Credit under current regime (ST-3, VAT 100) - Carried forward as opening balance under GST

Assessee availing exemptions like SSI, SSP and composition dealers, can take Credit of those

Lying in the stock of registered person

Purchases made within one year of the enforcement date

And must be in possession of the invoice copy

Must be eligible for claiming Credit under both old law and new law

90

Case 1- Manufacturer & Dealer

91

Particulars Rs

Cenvat Credit in last Excise Returns 150

Input Tax Credit available in last VATreturns

250

Tax incidence of Non submitting ofstatutory forms (C form to besubmitted for sale value of Rs.5,000/-)(5.5%-2%)

(175)

PRE GST POST GST

Particulars Rs

Input Credit available to CGST CreditLedger

150

Input Credit available to SGST CreditLedger

75(250-175)

CGST Credit ledger A/c Dr 150SGST Credit ledger A/c Dr 75

To CENVAT Credit A/c 150To Input Vat A/c 75

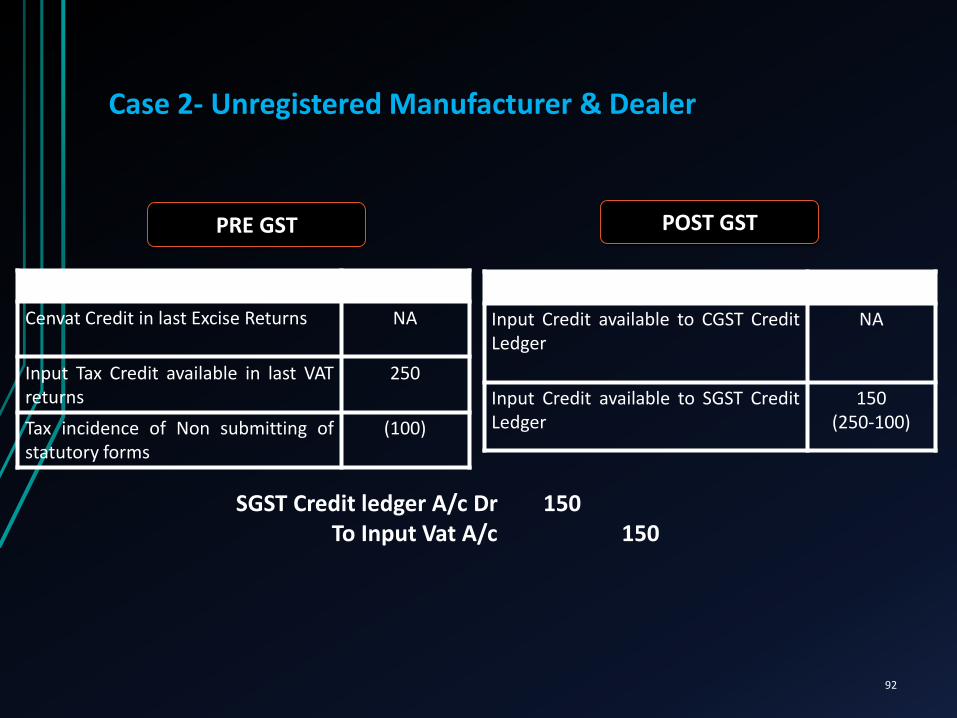

Case 2- Unregistered Manufacturer & Dealer

92

Particulars Rs

Cenvat Credit in last Excise Returns NA

Input Tax Credit available in last VATreturns

250

Tax incidence of Non submitting ofstatutory forms

(100)

PRE GST POST GST

Particulars Rs

Input Credit available to CGST CreditLedger

NA

Input Credit available to SGST CreditLedger

150(250-100)

SGST Credit ledger A/c Dr 150To Input Vat A/c 150

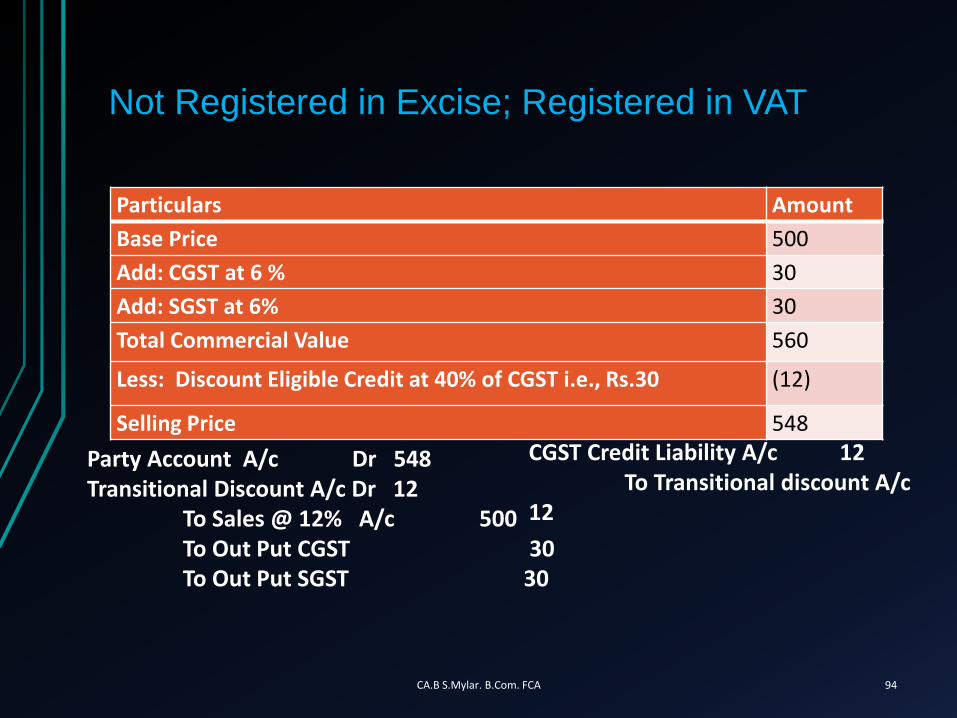

Not Registered in Excise; Registered in VAT

93

Supply Value GST Rate Type of tax CGST paid IGST PaidDeemed

Credit rateDeemed credit

value% on sale

value

10000 5% CGST 250 0 40% of CGST 100 1.00%

10000 12% CGST 600 0 40% of CGST 240 2.40%

10000 18% CGST 900 0 60% of CGST 540 5.40%

10000 28% CGST 1400 0 60% of CGST 840 8.40%

10000 5% IGST 0 500 20% of IGST 100 1.00%

10000 12% IGST 0 1200 20% of IGST 240 2.40%

10000 18% IGST 0 1800 30% of IGST 540 5.40%

10000 28% IGST 0 2800 30% of IGST 840 8.40%

Not Registered in Excise; Registered in VAT

CA.B S.Mylar. B.Com. FCA 94

Particulars Amount

Base Price 500

Add: CGST at 6 % 30

Add: SGST at 6% 30

Total Commercial Value 560

Less: Discount Eligible Credit at 40% of CGST i.e., Rs.30 (12)

Selling Price 548

Party Account A/c Dr 548Transitional Discount A/c Dr 12

To Sales @ 12% A/c 500To Out Put CGST 30To Out Put SGST 30

CGST Credit Liability A/c 12To Transitional discount A/c

12

95

5. Other areas

Supply - Technology Support

Supply can also be characterized into Mixed supply &

Composite supply

Software must be configured To determine the supply as mixed or composite

To provide for tax rates to be applied accordingly for such supplies

To adjust the stock quantity in the books accordingly (for mixed supply)

96

Job work - Technology Support

When goods/capital goods sent on Job work, control process to be:

Have a unique reference number(URN) with the due date to return back

Review & Report aging generated based on URNs

Squaring up the URNs once the consignment returned to factory

97

Business related issues – Pricing

Earlier there were multiple taxes levied and most of them were cost

GST is being rolled out with the concept of seamless Credit

Prices has to be reviewed to check the impact of the above

Any impact on margin must be actually passed on to the customers and the same is regulated by law

Re-engineering of pricing of product to be part of transition

98

Business related issues – Validating Creditors

Vendor selection plays crucial role, Since utilising credits are dependant on his compliances

Non Compliance by Vendor increase's

Working capital

Product Cost

Reconciliation & Manual efforts on Follow-up

Reduction in GST Ratings

Rating for every supplier are based on timely compliances & mismatches

99

Information Security

All data of business will be online, it is necessary to ensure software and system has adequate security

Ensure all terms and conditions are read while entering into a contract with GSPs/ASPs/GSTP

Ensure appropriate anti-malware's and antivirus software's are installed

Be aware of social engineering attempts

Ensure key information like user IDs and passwords are adequately secured

If any unauthorised account activity are suspected, appropriate security measures to be initiated

100

GST READINESS CHECK

104

Technology related GST Readiness

• Has applicable Provisions of the law configured in Software

• Is the team trained and aware of the Act & Use of Software

• Your Vendors are Educated and Tax compliant

• Do you have Customers GSTIN for B2B Supplies

• Do you have Vendors GSTIN for B2B Supplies

• Is the Rate mapping, Product Mapping HSN code complete

• Auto accounting of Stock movements & Credits for the Branch Transfer considered

105

GST Readiness (Contd….)

• Your Chart of Accounts/Accounting Entries / Notes updated

• Sufficient staff + Software Reports to reconcile and communicate with Vendor/Customer on Mis-match Reports

• Software to generate State wise GSTR returns

• ISD – Accounting & Auto Distribution of Credits

• Ability to assess revises Sale Price of your Goods

• Reconcile & Report Correctness of Returns filed.

106

Thank You

107