change in stance igl in equity january 12, 2016...

TRANSCRIPT

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

CHANGE IN STANCE IGL IN EQUITY January 12, 2016

Return of regulation We change our stance on IGL to BUY from Under Review (earlier SELL) given: a) recent regulatory/judicial activity will boost the CNG ecosystem driving double-digit volume growth; b) decline in LNG prices will again make IGL more competitive in industrial PNG; and c) inorganic growth catalysts will further add to volumes. Addition of more buses in public transport, conversion of diesel cabs to CNG alongside steps to enhance supporting infrastructure, are key enablers. Potential actions such as tax incentives to promote cleaner fuels (gas over fuel oil/diesel) and discouraging diesel vehicles can’t be denied for the NCR region. We raise our volume growth estimates for FY15-FY20 to 8% CAGR vs 3% CAGR earlier. Our TP moves to `715 implying 3.4x times P/B for core business. Competitive position: STRONG Changes to this position: POSITIVE Return of regulation IGL added about 1mmscmd of volume in each of the two time blocks of FY05-FY10 and FY10-FY13. These spurts were from infrastructure/public bus fleet addition and regulatory action leading to heightened public awareness. We believe IGL is entering into another 4-year phase where we see incremental catalysts around all three factors: a) judicial action banning 2000cc+ diesel vehicles and asking all diesel cabs to convert to CNG; b) actions such as odd-even leading to heightened public awareness/fear of regulation chasing private vehicle conversion; and c) the government allowing private vehicles to come under DTC fleet and judiciary taking active steps to iron out roadblocks. Infrastructure addition to enable growth of CNG Delhi government is already allowing private vehicles to take DTC permits at a fixed compensation without any risk of passenger load (fresh addition of 6,000 buses vs current base of 6,000), thus kick starting stagnant fleet since 2010. In addition, IGL has been allowed to tie up with OMCs to add 200 CNG pumps over next 2-3 years. Initiatives such as “Happy Hours” can resolve infrastructure constraints. Inorganic additions such as Gurgaon and Faridabad, new acquisitions/bidding for new GAs would also be volume + valuation drivers. No threat to competitive advantages; volumes can sustain/expand RoEs RoEs of IGL continue to remain healthy supported by strong moats: (a) regulatory compulsions and use of inexpensive domestic gas for its CNG business (76% of volumes) gives better pricing power; (b) virtual entry barriers as no competition enters post three years of exclusivity; and (c) pricing power given cost competitiveness of CNG vs petrol. We expect gas prices to decline faster than crude over the medium term and drive improved competitiveness.

Volume annuity to become bigger Consequent to factors stated above, we expect IGL’s CNG volumes to increase from 3mmscmd currently to 4.3mmscmd by FY20 building 11% volume CAGR over FY16-FY20. Given the annuity nature of these volumes, our revised DCF based TP is now `715 implying P/B of 3.4x for the core business + `67 valuation for its stake in other CGD entities. Potential catalysts could be higher taxation for diesel vehicles, crackdown on industrial usage of fuel oil.

Indraprastha GasBUY

Oil & Gas

Recommendation Mcap (bn): `83/US$1.2 6M ADV (mn): `283/US$4.2 CMP: `590 TP (12 mths): `715 Upside (%): 21

Flags Accounting: GREEN Predictability: GREEN Earnings Momentum: AMBER

Catalysts

Addition of new DTC buses

Implementation of ban on dieseldriven app based cabs

Regulatory crackdown on fuel oilusage

Performance (%)

Source: Bloomberg, Ambit Capital research

80

90 100

110

120 130

Jan-

15

Feb-

15

Mar

-15

Apr

-15

May

-15

Jun-

15

Jul-

15

Au

g-1

5

Sep-

15

Oct

-15

Nov

-15

Dec

-15

Sensex IGL

Analyst Details

Ritesh Gupta, CFA +91 22 3043 3242

Aakash Adukia

+91 22 3043 3273

Key financials Year end Mar FY14 FY15 FY16E FY17E FY18E

Sales (`m) 39,174 36,810 32,450 35,196 40,562

Recurring EPS (`) 25.7 31.3 30.5 37.8 44.1

PE (x) 22.9 18.9 19.4 15.6 13.4

PBV (x) 4.7 3.9 3.5 3.1 2.7

RoE (%) 22.1 22.7 19.2 21.1 21.7

RoCE (Post tax) (%) 16.2 17.3 15.5 17.4 18.2

Source: Company, Ambit Capital research

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 2

Snapshot of Company Financials Profit and loss Company Background Year end Mar FY16E FY17E FY18E

Net sales 32,450 35,196 40,562

Op. expenses 24,473 25,572 29,553

EBIDTA 7,977 9,624 11,009

Interest Expense 142 135 128

Depreciation 1,716 1,841 1,916

PBT 6,369 7,898 9,215

Tax (2,102) (2,606) (3,041)

Adj. PAT 4,267 5,292 6,174

EBIDTA Margin % 24.6 27.3 27.1

Adj PAT Margin % 13.1 15.0 15.2

P/E (X) 19.4 15.6 13.4

Dividend Yield (%) 1.8 2.2 2.6

Indraprastha Gas (IGL) was incorporated in December 1998 as a JV, with the partners being GAIL, BPCL and Government of Delhi. The objective was to supply CNG to the transport sector and PNG to the domestic and commercial sectors in the NCR region.

IGL was incorporated post the Supreme Court’s July 1998 order seeking all buses, three-wheelers and taxis in Delhi to adopt CNG as fuel. IGL has not only emerged as the sole supplier of CNG and PNG in the National Capital Territory (NCT) of Delhi but is also expanding its footprint in the National Capital Region (NCR) cities of Noida, Greater Noida, Ghaziabad and Faridabad.

Balance sheet Cash flow Year end Mar FY16E FY17E FY18E

Net Fixed Assets 20,342 21,001 20,584

Capital WIP 2,287 2,058 1,852

Investments 3,199 3,519 3,871

Working Capital

(1,892)

(2,277)

(2,597)

Cash 5,651 8,528 12,895

Total Assets 29,588 32,829 36,606

Shareholders’ fund 23,513 26,652 30,315

Debt 4,803 4,905 5,019

Total Liabilities 29,588 32,829 36,606

ROE % 19.2 21.1 21.7

ROCE (post tax) % 15.5 17.4 18.2

Net Debt/Equity (%) (4) (14) (26)

Equity/Total Assets 0.8 0.8 0.9

P/BV (X) 3.5 3.1 2.7

Year end Mar FY16E FY17E FY18E

Consolidated PAT 4,267 5,292 6,174

+ Depreciation 1,716 1,841 1,916

+ Deferred Tax Liability - - -

Cash profit 5,983 7,133 8,090

- Increase in Current Assets (557) 242 426

+ Increase in Current Liabilities 979 627 745

Operating cash flow 7,519 7,518 8,410

- Increase in Capex 2,246 2,271 1,294

Free cash flow 5,273 5,247 7,115

- Dividend 1,736 2,152 2,511

+ Debt raised 90 102 114

- Investments 291 320 352

Net cash flow 3,337 2,877 4,366

+ Opening Cash 2,315 5,651 8,528

Closing Cash 5,651 8,528 12,895

Improved margins have led to higher PAT growth despite stagnant volumes

RoE/RoCE to see slight moderation given rising PNG share

Source: Company, Ambit Capital research

0

1

2

3

4

5

6

4

5

5

6

6

7

FY10 FY12 FY14 FY16E FY18E

EBITDA (Rs/scm) Volume (mmscmd) (RHS)

0

5

10

15

20

25

FY14 FY15 FY16E FY17E FY18E

ROCE (post tax) ROE

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 3

CNG: Renewed regulatory push IGL is entering again into a high volume growth phase fielded by regulatory push. The company was born as an outcome of a court ruling which mandated the Delhi government to shift fuel usage in the public transport sector to CNG. As a result, volumes expanded from 0 mmscmd to 3 mmscmd in less than a decade. Over the last few years, as regulatory push subsided, we note a drop in incremental CNG adoption. Recent measures such as ‘odd-even’, ban on diesel vehicles etc. have created fresh awareness and a sense of ‘need for action’ amongst the public, judiciary and the government. Besides pollution control, these measures have highlighted the need to expand the public transport system in Delhi as well as expedite infrastructure expansion for CNG fueling.

The direct impact of this government drive thrusting CNG consumption is clearly visible with a ban on diesel cars for app-based taxis and also on 2000cc+ diesel vehicles. However, the drive also highlighted a couple of other invisible positives such as: a) the decision to include private buses in DTC’s fleet and expedite addition of new buses; b) Central government allowing using OMC pumps to expand the CNG fueling station network; c) innovative steps by IGL such as “Happy Hours” providing a marginal discount on refueling during odd hours to ease the load on pumps in peak hours; d) addition of new autos to boost public transport system e) Noida district magistrate directing local industries to switch to gas by end-March.

In the past few days multiple announcements have been made by the government, government bodies and the judiciary. The key measures announced that could curb pollution are:

Delhi moving to an odd/even movement system, wherein cars with odd-even number plates will ply on Delhi’s roads on alternative days. It was passed by the Delhi government and will be run as an experiment for 15 days in January 2016.

All private taxis converting to CNG by March 2016 as per the Delhi high court ruling, and re-affirmed by the Supreme court.

Supreme court banning registration of diesel SUV/commercial cars with engine capacity of more than 2000cc until March 2016 in NCR

National Green Tribunal (NGT) had earlier banned registration of all diesel vehicles until January 6, 2016 but reversed this order post the SC order.

Though we believe the odd-even rule will only remain an experiment, we see this as a structural positive for CNG. The renewed vigour to control pollution will expedite bus addition; conversion of app-based cabs and thrust usage of public transport.

Exhibit 1: IGL volumes ramped up nicely from FY05-FY11 and then growth rates started coming off due to lack of expansion of public transport network specifically buses. Recent odd-even regime exposed the need to augment Delhi’s public transport with judiciary taking cognizance and looking to remove bottlenecks

Source: Company, Ambit research

0%

5%

10%

15%

20%

25%

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16E

CNG Volumes (in mmscmd, LHS) Growth rate (in %, RHS)

Apart from pollution issue, this movement also exposed the need to expand public transport system in Delhi as well as to expand the infrastructure for CNG fueling.

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 4

Exhibit 2: Volume growth slowdown coincides with weaker addition in buses (number of buses)

Source: Company

Exhibit 3: Private cars don’t quite drive the addition of CNG volumes (number of cars)

Source: Company

Addition to DTC’s fleet to drive significant volumes

The Delhi Transport Corporation (DTC) has been planning the addition of new buses for a while now. As per the latest news reports, DTC plans to add ~2,000 buses (10% to its fleet) by the end of FY16; however, a tender for 1,380 buses has been delayed for a long time. In order to make the odd-even experiment successful, the Delhi government has added ~3,000 private buses. These buses are given special permissions and are paid on a per km basis. The implementation of odd-even rule clearly exposed the weakness of whole public transport system in Delhi. Even if the odd-even rule goes away, the problem of DTC bus addition still stays at the top of the to-do list of the Delhi government.

All India permit cabs (AITP) to convert to CNG

At present there are 35,000 AITP vehicles that are operated by players like Uber and Ola in Delhi; diesel cars constitute nearly 60% of this vehicle fleet. We believe that there is a strong possibility that 60% of 35,000 vehicles will have to get converted to CNG. We estimate a requirement of 0.4 mmscmd of CNG volumes (12% of CNG volumes in FY15) for these vehicles.

Exhibit 4: Sales mix - FY15

Source: Ambit Capital research, Company

Exhibit 5: CNG consumption driven by public transport

Source: Ambit Capital research

02000400060008000

100001200014000160001800020000

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

0

100000

200000

300000

400000

500000

600000

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

CNG76%

Comm./ Ind./Others

12%

Tradingwith Other CGDs 7%

Household5% Buses

25%

Private Cars35%

Taxi, Auto40%

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 5

Positive read across for CUGL and MNGL

Recently 13 Indian cities were ranked amongst the top 20 most polluted cities in the world by WHO. Delhi tops the list and is about six times more polluted than the prescribed limits of 2.5ppm by WHO. Other Indian cities included in the list were Patna, Gwalior, Raipur, Ahmedabad, Lucknow, Kanpur, Firozabad, Amritsar, Ludhiana, Allahabad, Agra, and Khanna. IGL has a presence in Kanpur through CUGL which could face similar government regulation in the future. Judicial activism through public interest litigation could drive the incremental ban on diesel vehicles in some of these cities. As per news flow, a PIL has already been filed in the Gujarat High Court to ban diesel commercial vehicles in that state.

Co-marketing with OMCs to help reduce the burden of infrastructure creation

As per management, IGL has already identified 150 locations for setting up CNG sales. IGL plans to add 50 stations in FY17 itself. Marketing through OMC will save IGL significant capex costs and also provide access to prime locations where setting up pure CNG pumps will not be feasible. The thrust to pump addition by itself will motivate private consumption, as it would reduce the refueling waiting time.

Happy Hours to improve pump utilisation

As per a directive by the petroleum minister, IGL has announced that it will offer a discount of `1.5/kg on the CNG that is sold at odd hours (midnight to 5 am) in order to manage the excess demand due to the odd-even rule. The CNG distribution capacity in Delhi is 6.8 million kg per day but the offtake is only 2.2 mn kg per day. The move will motivate the commercial users to refuel more during Happy Hours, increasing the convenience for private vehicle users during the day. On the margin front, we do not see any major impact, some of the discount was already due as IGL did not pass on all the benefits of the fall in domestic gas prices.

Judicial activism – likely to expedite bus addition The subject of addition of DTC buses has been pending for years – the reasons being a mix of failed tenders, lack of parking space etc. However, we believe judicial intervention can expedite things. We note under an earlier SC ruling, the Delhi government was asked to add more buses to the DTC fleet. Several trivial issues such as lack of parking space, which get stuck due to poor co-ordination among the various departments, can also be resolved with judicial intervention.

On buses, Salve told the Bench that the Delhi Government was under an obligation as per SC ruling of July 27, 1998 to increase public bus fleet from 5,000 to 10,000 to be achieved by April 2001. As on date, there are less than 5,000 buses run by Delhi Transport Corporation. In addition, there are 1,500 cluster buses. The Court asked both Delhi and Central Governments to respond on why the bus fleet had not been augmented.

For Delhi advocate Rahul Mehra said that space crunch for bus depots. The Delhi Government needs 500 acres land to park 10,000 buses. It blamed the Centre as the DDA, the land owning agency, refuses to grant possession of land. It cited a 70-acre plot, the possession of which is hanging fire despite being allotted to the Delhi Government. The Court directed Solicitor General to seek instructions and ask DDA to expedite the possession of 45 acres out of the 70-acre plot.

The court wants 10,000 more buses on the road and more Metro trains with increased frequency to cater to the increased load of commuters. A Bench of Chief Justice TS Thakur, Justices AK Sikri and R Banumathi said that efforts must be made to ensure passengers who travel by Delhi Metro get a place to sit instead of being jostled and heckled. It dropped the suggestion for introducing a special coach with premium fare, while leaving it to the Centre to hold discussions with DMRC in this regard.

Source: Media articles

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 6

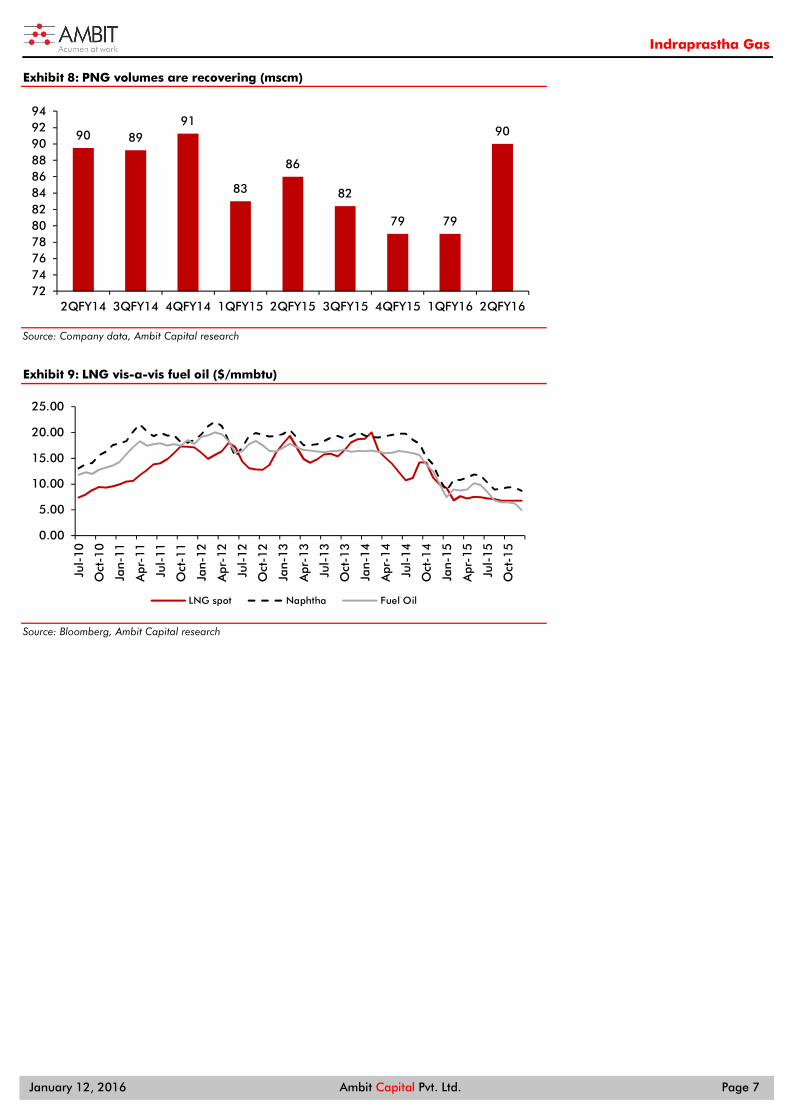

RasGas resolution to boost LNG cost competitiveness IGL has been witnessing a gradual slide in volumes for its industrial/commercial segment. Industrial demand for IGL depends on LNG’s competitiveness vs alternative fuels like fuel oil and naphtha. As industrial users do not have any domestic gas allocation, IGL addresses industrial demand through LNG. IGL procures most of its gas from GAIL under the RasGas long term contract.

Industries in Noida required to switch to natural gas

The problem of muted industrial/commercial PNG volumes was aggravated because most of IGL’s consumers fall in Noida (UP) specifically where VAT rates are high (26% for gas, 5% for fuel oil).

Recent media articles however highlight that the local administration has asked all industrial units in Noida to switch to natural gas by Mar 31 or face closure. As per rough estimates, there are about 8,000 industrial units operating in Noida and ~500 more in Greater Noida. As of now, only 330 industrial units are running on piped natural gas (PNG) in the district. Several units also appear to be using a mix of gas along with other fuels, given the weaker competitiveness of CNG.

IGL’s volumes to benefit from decline in long-term RasGas contract pricing

IGL’s 12% supply volume comes from GAIL via the long term contract with RasGas. Due to a steep fall in crude prices, the prices pf $12.6/mmbtu were significantly higher than the spot of $6.8/mmbtu. Despite spot LNG becoming cheaper, IGL was not able to seize the opportunity. As per the new agreement, the landed cost of LNG comes down to ~$6.6/mmbtu, which will significantly drive up competition. Captive power plant volumes are among the few alternative opportunities, which could drive up volumes. Likewise IGL saw a jump in 3Q volumes led by supplies to captive gas-based power plants in 3Q.

We build in volume growth of 2% for FY16 and 5% for FY17 versus the -3% growth in FY15 built in earlier.

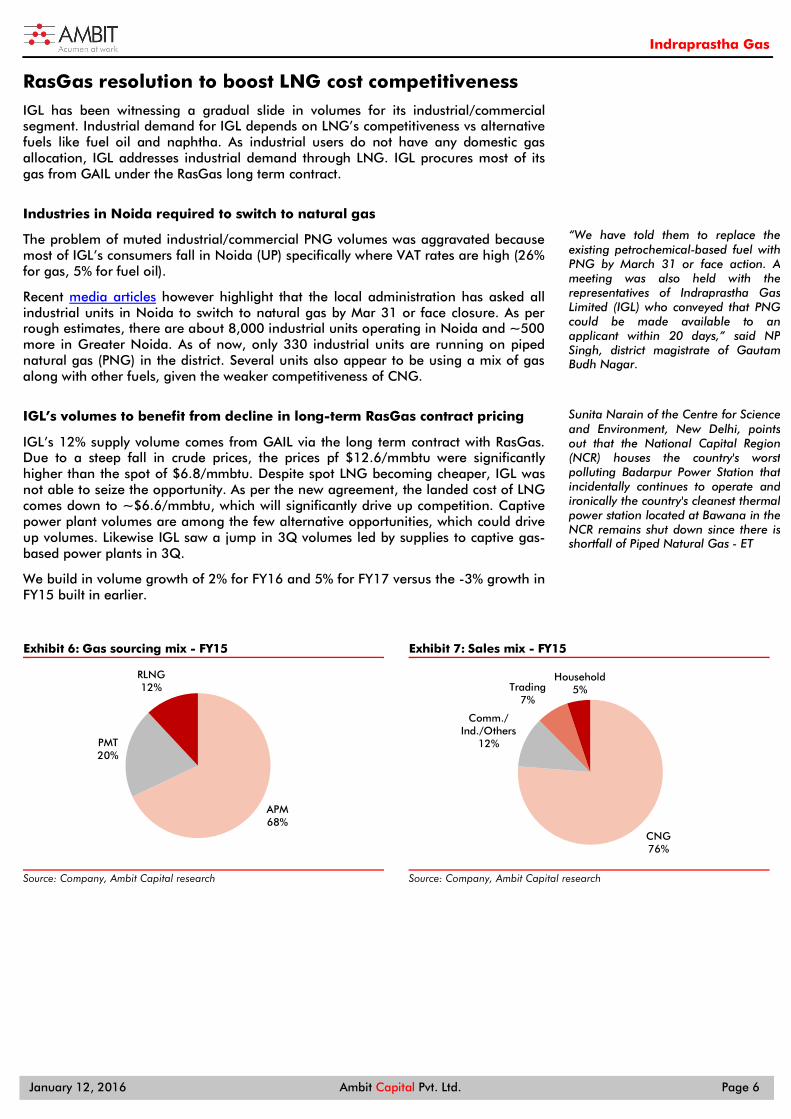

Exhibit 6: Gas sourcing mix - FY15

Source: Company, Ambit Capital research

Exhibit 7: Sales mix - FY15

Source: Company, Ambit Capital research

APM68%

PMT20%

RLNG12%

CNG76%

Comm./ Ind./Others

12%

Trading7%

Household5%

“We have told them to replace the existing petrochemical-based fuel with PNG by March 31 or face action. A meeting was also held with the representatives of Indraprastha Gas Limited (IGL) who conveyed that PNG could be made available to an applicant within 20 days,” said NP Singh, district magistrate of Gautam Budh Nagar.

Sunita Narain of the Centre for Science and Environment, New Delhi, points out that the National Capital Region (NCR) houses the country's worst polluting Badarpur Power Station that incidentally continues to operate and ironically the country's cleanest thermal power station located at Bawana in the NCR remains shut down since there is shortfall of Piped Natural Gas - ET

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 7

Exhibit 8: PNG volumes are recovering (mscm)

Source: Company data, Ambit Capital research

Exhibit 9: LNG vis-a-vis fuel oil ($/mmbtu)

Source: Bloomberg, Ambit Capital research

90 8991

83

86

82

79 79

90

727476788082848688909294

2QFY14 3QFY14 4QFY14 1QFY15 2QFY15 3QFY15 4QFY15 1QFY16 2QFY16

0.00

5.00

10.00

15.00

20.00

25.00

Jul-

10

Oct

-10

Jan-

11

Apr

-11

Jul-

11

Oct

-11

Jan-

12

Apr

-12

Jul-

12

Oct

-12

Jan-

13

Apr

-13

Jul-

13

Oct

-13

Jan-

14

Apr

-14

Jul-

14

Oct

-14

Jan-

15

Apr

-15

Jul-

15

Oct

-15

LNG spot Naphtha Fuel Oil

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 8

Margins supported by deregulation and access to cheaper domestic gas IGL’s margins are likely to be supported by two factors: (a) in the medium to long term from a virtual deregulation of marketing margins, as per the directive of the Supreme Court; and (b) in the short term, from lower gas prices. EBITDA per scm for IGL improved to `5.62 in 2QFY16 from `5.11 in 4QFY15, implying a 10% increase. We build in EBITDA of `5.9 per scm for FY16 and `6.1 for FY17 on the back of excess supply of natural gas globally, which will add to the pressure on global gas price benchmarks used for Indian gas price determination.

Decline in domestic gas prices to aid margins

Domestic gas prices are likely to come off gradually by 15%-20% over the next few quarters, as per the Government’s gas price formula, which works with a six-month lag. We expect IGL’s margins rather than its volumes to benefit from a fall in gas prices. IGL historically has been able to protect its margins by increasing prices. Given the inelastic demand for CNG, it seems unlikely that IGL will pass on this benefit to consumers. However, this is a short-term trigger from a valuation perspective.

Exhibit 10: Gross margins to improve by 7%/10% over FY16/FY17 (`/scm)

Source: Company data

Exhibit 11: Domestic gas prices will see a sharp decline over FY16-FY17, supporting expansion in EBITDA/scm ($/mmbtu)

Source: Company data

6.21

7.127.37

7.63

8.31 8.29

7.778.16

8.568.82

5.00

5.50

6.00

6.50

7.00

7.50

8.00

8.50

9.00

9.50

FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16E FY17E FY18E

4.2 4.2

4.8

4.2

3.7

4.5

33.23.43.63.8

44.24.44.64.8

5

FY13 FY14 FY15 FY16E FY17E FY20E

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 9

Exhibit 12: Quarterly EBITDA margin has come off from recent highs due to decline in industrial volumes; margins will revive as the decline in long term Rasgas contract prices (from US$12mmbtu to US$ 7/mmbtu) moderate

Source: Company

Exhibit 13: Annual EBITDA margin trend – EBITDA margin has been stagnant for the last 3 years; decline in domestic gas/LNG prices to aid margins

Source: Company, Ambit Capital research

0.005.0010.0015.0020.0025.0030.0035.00

0.001.002.003.004.005.006.007.00

2Q

FY1

1

4Q

FY1

1

2Q

FY1

2

4Q

FY1

2

2Q

FY1

3

4Q

FY1

3

2Q

FY1

4

4Q

FY1

4

2Q

FY1

5

4Q

FY1

5

2Q

FY1

6

EBITDA (Rs/scm) Overall (Rs/scm)

0

1

2

3

4

5

6

4

5

5

6

6

7

FY10 FY12 FY14 FY16E FY18E

EBITDA (Rs/scm) Volume (mmscmd) (RHS)

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 10

Volumes drive valuation upside Given the utility nature of IGL’s volumes (specifically for CNG volumes), we believe it would be incorrect to view IGL on a multiple basis. Any addition to volumes will add up to cash flow annuity and thereby lead to both earnings as well as multiple upgrades. Hence, we prefer DCF-based approach over the multiples-based one.

We believe IGL’s earnings stream will be strengthened with implementation of the stated round of regulatory/judicial action as this will likely lead to CNG/PNG volumes upgrading for the long term driven by -- addition of DTC buses/autos into the Delhi transport system, radio taxis converting to CNG and industrial units compulsorily shifting to cleaner fuel.

The visible volumes notwithstanding, the indirect benefits would be fast tracking of the stagnant issues which had been deterring CNG/PNG growth such as a) pending addition of DTC buses owing to lack of parking space (now there is a court directive asking the relevant authorities to look into it); b) addition of CNG pumps – MoPNG has identified 200 OMC sites where new pumps will be put in place with 50 being added in FY17 itself; c) likely settlement of the court case with respect to Gurgaon/Faridabad CGD rights; and d) allowing private bus owners to become a part of the DTC fleet.

Revising TP upward to `715

Our SOTP-based target price for IGL factors in `648 for the standalone business and `67 for IGL’s stake in MNGL and CUGL. Our DCF-based valuation of `648 values IGL’s standalone business (NCR) at a P/B of 3.4x FY17. We believe a multiple of 3.4x book is reasonable, given expectation of high volume growth and return ratios as CNG consumption increases driven by higher awareness and regulatory push. Based on the Gordon growth formula of (RoE-g)/(Ke-g), implied P/B multiple of 3.4x FY17 seems fare given volume growth high steady state RoE’s of 28% and long term earnings growth of 9%.

Our DCF valuation of MNGL and CUGL implies a P/E multiple of 24x FY17 earnings, which justifies the untapped potential and high growth phase of these companies. We apply a 30% holding discount for the fair value of IGL’s stake in these entities given IGL doesn’t exercise full control of these entities. GAIL along with other OMCs controls the operational management to a large extent. Tomorrow if IGL has to liquidate the financial value of these stakes, we believe this would be at a discount to fair value, given illiquidity and lack of operational control.

Exhibit 14: SOTP-based valuation (in `)

Equity Value (mn) Per share

IGL 90,833 649

MNGL (30% holding co. discount) 6,769 48

CUGL (30% holding co. discount) 2,599 19

100,201 716

Source: Ambit Capital research

Exhibit 15: IGL’s DCF valuation

Terminal FCF (` mn) 11,743

Terminal Growth Rate 3.0%

WACC 13.0%

Terminal Value (` mn) 121,223

PV of Terminal Value (` mn) (A) 38,034

PV of Cash Flow (` Mn) (B) 51,951

Enterprise Value (C=A+B) 89,984

Net Debt (Mar 2016 end) (D) (849)

Equity Value (` mn) (E=C-D) 90,833

No of shares (F) 140

Valuation (`) (G=E/F) 648

Source: Ambit Capital research

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 11

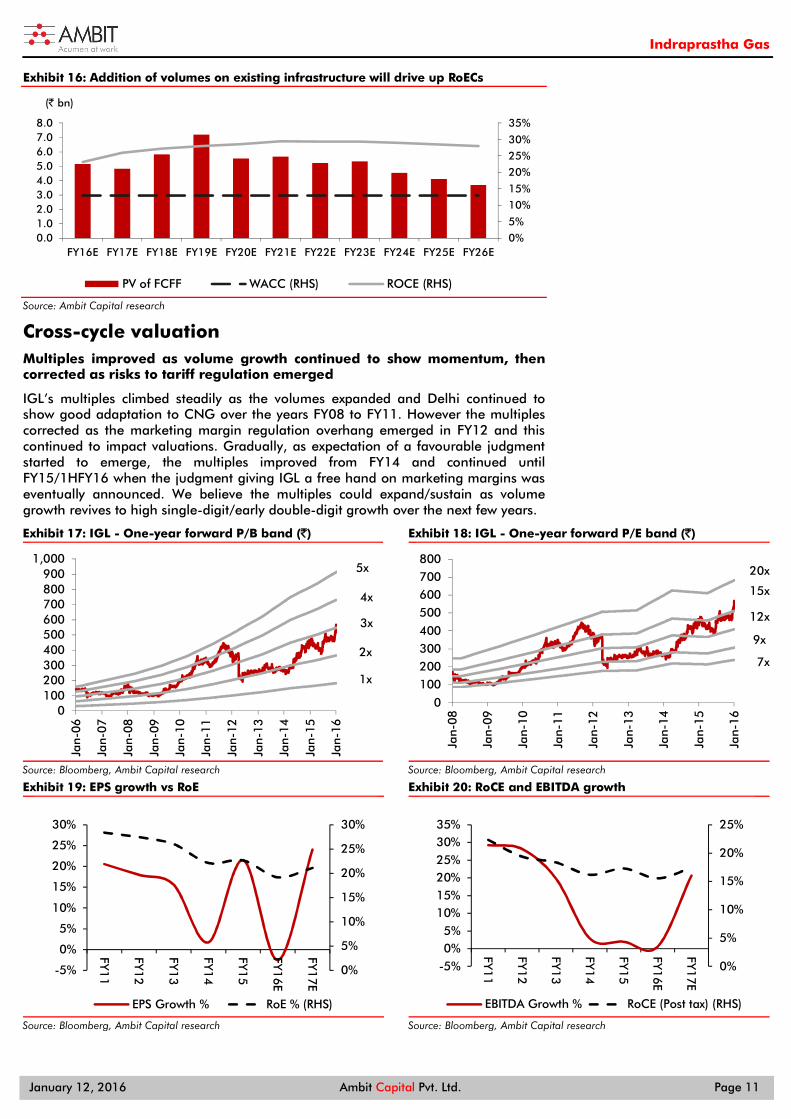

Exhibit 16: Addition of volumes on existing infrastructure will drive up RoECs

Source: Ambit Capital research

Cross-cycle valuation Multiples improved as volume growth continued to show momentum, then corrected as risks to tariff regulation emerged

IGL’s multiples climbed steadily as the volumes expanded and Delhi continued to show good adaptation to CNG over the years FY08 to FY11. However the multiples corrected as the marketing margin regulation overhang emerged in FY12 and this continued to impact valuations. Gradually, as expectation of a favourable judgment started to emerge, the multiples improved from FY14 and continued until FY15/1HFY16 when the judgment giving IGL a free hand on marketing margins was eventually announced. We believe the multiples could expand/sustain as volume growth revives to high single-digit/early double-digit growth over the next few years.

Exhibit 17: IGL - One-year forward P/B band (`)

Source: Bloomberg, Ambit Capital research

Exhibit 18: IGL - One-year forward P/E band (`)

Source: Bloomberg, Ambit Capital research

Exhibit 19: EPS growth vs RoE

Source: Bloomberg, Ambit Capital research

Exhibit 20: RoCE and EBITDA growth

Source: Bloomberg, Ambit Capital research

0%

5%

10%

15%

20%

25%

30%

35%

0.01.02.03.04.05.06.07.08.0

FY16E FY17E FY18E FY19E FY20E FY21E FY22E FY23E FY24E FY25E FY26E

PV of FCFF WACC (RHS) ROCE (RHS)

(` bn)

1x

2x

3x

4x

5x

0100200300400500600700800900

1,000

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

Jan-

16

9x

12x

15x

20x

7x

0

100200300400

500600700800

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

Jan-

16

0%

5%

10%

15%

20%

25%

30%

-5%

0%

5%

10%

15%

20%

25%

30%

FY11

FY12

FY13

FY14

FY15

FY16E

FY17E

EPS Growth % RoE % (RHS)

0%

5%

10%

15%

20%

25%

-5%0%5%

10%15%20%25%30%35%

FY11

FY12

FY13

FY14

FY15

FY16E

FY17E

EBITDA Growth % RoCE (Post tax) (RHS)

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 12

Our volume estimates are higher than the street Our revised volume estimates of 8% CAGR over FY15-20 (addition of 1.9 mmscmd) is significantly higher than our previous estimates of 3%. Near term volume catalysts for CNG are conversion of app based taxis (0.3-0.4 mmscmd), addition of DTC buses (another 0.5mmscmd). Industrial PNG would improve due to a) improved price competitiveness due to renegotiation with Ras Gas b) regulatory clampdown in case of industrial fuel as seen in case of Noida.

8% CAGR volume growth for CNG over FY15-20 We estimate CNG volumes to grow by 1.4 mmscmd over FY15-20. Out of the 1.4 mmscmd addition, we believe 0.3-0.4 mmscmd will solely be driven by the conversion of app based cabs. Earlier, there were some apprehensions regarding the conversion of taxis but reaffirmation by Supreme Court removes all doubt. Further, CNG usage favoring rules leading to fast track addition of DTC buses will provide significant growth. We expect the sheer addition of DTC buses will provide 0.5 mmscmd volumes. The last 0.5 mmscmd of volumes we expect to come from increased penetration in the private vehicles due to shift from Diesel to Petrol/CNG. We believe a unfavorable taxation for Diesel vehicles which will make people shift towards Petrol/CNG can’t be denied. Recently government had all the other users under the ambit of “odd even rule” though CNG cars were exempt.

Private vehicle consumption growth in Delhi has been facing two issues: 1) Competition from diesel vehicles and 2) low number of CNG pumps. Recent decisions tend to fix both of them. Recent ban on diesel vehicles with engine capacity of more than 2000cc will make buyers of diesel vehicles a little skeptical. Even if the ban is temporary in nature, long distance travelers within the city would choose to opt for CNG more in order to avoid any future anti-diesel regulations. Significant addition to CNG infrastructure will remove the mental blockage of the extra time required for CNG refueling.

Further, we do not build in the inorganic volume growth that may follow post the dispute resolution of the Gurgaon CGD. IGL has been in dispute with the Haryana Government for gas distribution rights. Gurgaon CGD is operated by Haryana City Gas and due to internal family disputes of the company; CNG infrastructure creation has been neglected. With rising judicial intervention, we believe will make the dispute resolution swift benefiting IGL’s volumes. Gurgaon holds significant potential from PNG point of view (both domestic and industrial)

7% CAGR volume growth for PNG over FY15-20 For PNG, our conviction is driven by regained cost competitiveness due to the Ras Gas renegotiation. IGL has a 10% share in the contract and the new rates of $6.6mmbtu against the earlier $12/mmbtu. We build in 0.4 mmscmd volume addition due to improved price competitiveness (0.2mmscmd) and some volume additions from the mandatory conversion of industrial users to PNG in cities like Noida (0.2mmscmd).

Exhibit 21: CNG volume growth trend

Source: Ambit Capital research

Exhibit 22: PNG volume growth trend

Source: Ambit Capital research

0%

2%

4%

6%

8%

10%

12%

14%

0

1

2

3

4

5

FY15 FY16 FY17 FY18 FY19 FY20

CNG (mmscmd) YoY Growth (RHS)

-10%

-5%

0%

5%

10%

15%

20%

0

0.2

0.4

0.6

0.8

1

1.2

1.4

FY15 FY16 FY17 FY18 FY19 FY20

PNG (mmscmd) YoY Growth (RHS)

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 13

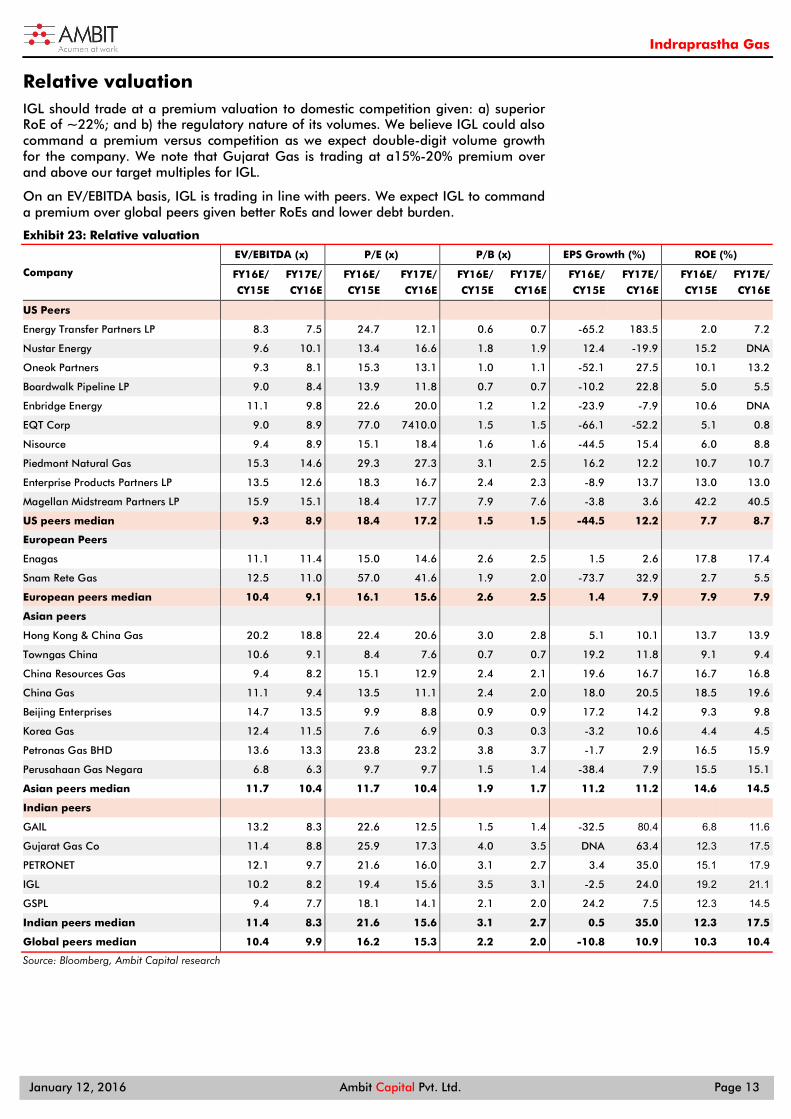

Relative valuation IGL should trade at a premium valuation to domestic competition given: a) superior RoE of ~22%; and b) the regulatory nature of its volumes. We believe IGL could also command a premium versus competition as we expect double-digit volume growth for the company. We note that Gujarat Gas is trading at a15%-20% premium over and above our target multiples for IGL.

On an EV/EBITDA basis, IGL is trading in line with peers. We expect IGL to command a premium over global peers given better RoEs and lower debt burden.

Exhibit 23: Relative valuation

Company

EV/EBITDA (x) P/E (x) P/B (x) EPS Growth (%) ROE (%)

FY16E/

CY15E

FY17E/

CY16E

FY16E/

CY15E

FY17E/

CY16E

FY16E/

CY15E

FY17E/

CY16E

FY16E/

CY15E

FY17E/

CY16E

FY16E/

CY15E

FY17E/

CY16E

US Peers

Energy Transfer Partners LP 8.3 7.5 24.7 12.1 0.6 0.7 -65.2 183.5 2.0 7.2

Nustar Energy 9.6 10.1 13.4 16.6 1.8 1.9 12.4 -19.9 15.2 DNA

Oneok Partners 9.3 8.1 15.3 13.1 1.0 1.1 -52.1 27.5 10.1 13.2

Boardwalk Pipeline LP 9.0 8.4 13.9 11.8 0.7 0.7 -10.2 22.8 5.0 5.5

Enbridge Energy 11.1 9.8 22.6 20.0 1.2 1.2 -23.9 -7.9 10.6 DNA

EQT Corp 9.0 8.9 77.0 7410.0 1.5 1.5 -66.1 -52.2 5.1 0.8

Nisource 9.4 8.9 15.1 18.4 1.6 1.6 -44.5 15.4 6.0 8.8

Piedmont Natural Gas 15.3 14.6 29.3 27.3 3.1 2.5 16.2 12.2 10.7 10.7

Enterprise Products Partners LP 13.5 12.6 18.3 16.7 2.4 2.3 -8.9 13.7 13.0 13.0

Magellan Midstream Partners LP 15.9 15.1 18.4 17.7 7.9 7.6 -3.8 3.6 42.2 40.5

US peers median 9.3 8.9 18.4 17.2 1.5 1.5 -44.5 12.2 7.7 8.7

European Peers

Enagas 11.1 11.4 15.0 14.6 2.6 2.5 1.5 2.6 17.8 17.4

Snam Rete Gas 12.5 11.0 57.0 41.6 1.9 2.0 -73.7 32.9 2.7 5.5

European peers median 10.4 9.1 16.1 15.6 2.6 2.5 1.4 7.9 7.9 7.9

Asian peers

Hong Kong & China Gas 20.2 18.8 22.4 20.6 3.0 2.8 5.1 10.1 13.7 13.9

Towngas China 10.6 9.1 8.4 7.6 0.7 0.7 19.2 11.8 9.1 9.4

China Resources Gas 9.4 8.2 15.1 12.9 2.4 2.1 19.6 16.7 16.7 16.8

China Gas 11.1 9.4 13.5 11.1 2.4 2.0 18.0 20.5 18.5 19.6

Beijing Enterprises 14.7 13.5 9.9 8.8 0.9 0.9 17.2 14.2 9.3 9.8

Korea Gas 12.4 11.5 7.6 6.9 0.3 0.3 -3.2 10.6 4.4 4.5

Petronas Gas BHD 13.6 13.3 23.8 23.2 3.8 3.7 -1.7 2.9 16.5 15.9

Perusahaan Gas Negara 6.8 6.3 9.7 9.7 1.5 1.4 -38.4 7.9 15.5 15.1

Asian peers median 11.7 10.4 11.7 10.4 1.9 1.7 11.2 11.2 14.6 14.5

Indian peers

GAIL 13.2 8.3 22.6 12.5 1.5 1.4 -32.5 80.4 6.8 11.6

Gujarat Gas Co 11.4 8.8 25.9 17.3 4.0 3.5 DNA 63.4 12.3 17.5

PETRONET 12.1 9.7 21.6 16.0 3.1 2.7 3.4 35.0 15.1 17.9

IGL 10.2 8.2 19.4 15.6 3.5 3.1 -2.5 24.0 19.2 21.1

GSPL 9.4 7.7 18.1 14.1 2.1 2.0 24.2 7.5 12.3 14.5

Indian peers median 11.4 8.3 21.6 15.6 3.1 2.7 0.5 35.0 12.3 17.5

Global peers median 10.4 9.9 16.2 15.3 2.2 2.0 -10.8 10.9 10.3 10.4

Source: Bloomberg, Ambit Capital research

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 14

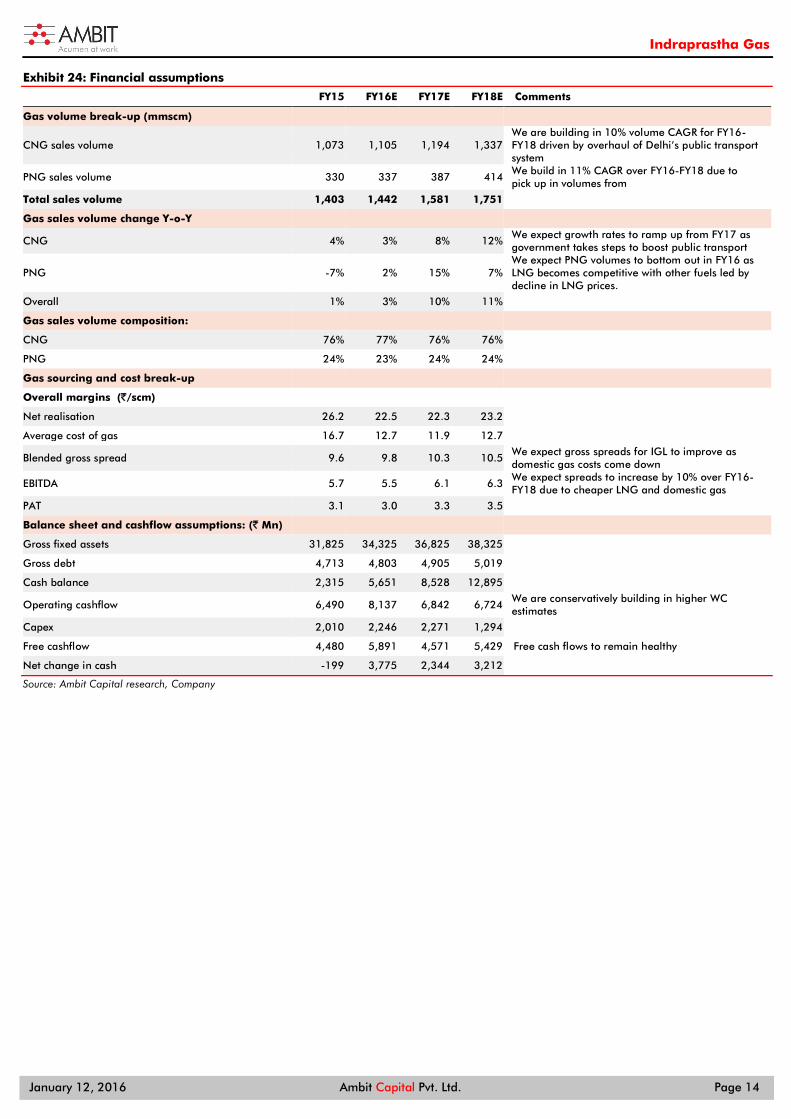

Exhibit 24: Financial assumptions

FY15 FY16E FY17E FY18E Comments

Gas volume break-up (mmscm)

CNG sales volume 1,073 1,105 1,194 1,337

PNG sales volume 330 337 387 414

We are building in 10% volume CAGR for FY16-FY18 driven by overhaul of Delhi’s public transport system We build in 11% CAGR over FY16-FY18 due to pick up in volumes from

Total sales volume 1,403 1,442 1,581 1,751

Gas sales volume change Y-o-Y

CNG 4% 3% 8% 12% We expect growth rates to ramp up from FY17 as government takes steps to boost public transport

PNG -7% 2% 15% 7% We expect PNG volumes to bottom out in FY16 as LNG becomes competitive with other fuels led by decline in LNG prices.

Overall 1% 3% 10% 11%

Gas sales volume composition:

CNG 76% 77% 76% 76%

PNG 24% 23% 24% 24%

Gas sourcing and cost break-up

Overall margins (`/scm)

Net realisation 26.2 22.5 22.3 23.2

Average cost of gas 16.7 12.7 11.9 12.7

Blended gross spread 9.6 9.8 10.3 10.5 We expect gross spreads for IGL to improve as domestic gas costs come down

EBITDA 5.7 5.5 6.1 6.3 We expect spreads to increase by 10% over FY16-FY18 due to cheaper LNG and domestic gas

PAT 3.1 3.0 3.3 3.5

Balance sheet and cashflow assumptions: (` Mn)

Gross fixed assets 31,825 34,325 36,825 38,325

Gross debt 4,713 4,803 4,905 5,019

Cash balance 2,315 5,651 8,528 12,895

Operating cashflow 6,490 8,137 6,842 6,724 We are conservatively building in higher WC estimates

Capex 2,010 2,246 2,271 1,294

Free cashflow 4,480 5,891 4,571 5,429 Free cash flows to remain healthy

Net change in cash -199 3,775 2,344 3,212

Source: Ambit Capital research, Company

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 15

Catalysts and risks Key catalysts to our BUY stance are

a) Addition of DTC buses according to plan: DTC is expected to add ~6,000 buses in its fleet according to an earlier proposal. Whilst discussions have been ongoing for the last few years, no fleet addition has been made given operational issues. We believe court intervention will likely expedite these issues. Recently the court has been intervening to the extent of coordinating between two different government agencies. We believe even if the company is successful in adding the buses over next five years, the company will meet our volume estimates assuming all else remains the same.

b) Crackdown on industrial usage of liquid fuels: PNG usage has very good potential in the industrial/commercial segments in Delhi NCR. However, lack of regulatory support has come in its way. Also, LNG prices having been on the higher side over last few years has not helped the conversions. Given that gas prices have declined substantially for both domestic gas as well as LNG, we expect growth rates of 5% on a base of 0.5-0.6 mmscmd. Regulatory support (as witnessed in the case of Noida) could drive further upside to these estimates.

c) Execution of shift of radio taxis to CNG: We believe the additional 0.3mmscmd-0.4 mmscmd can come only from these app-based taxi services as and when they shift to CNG. The judiciary appears firm on implementing this conversion; its successful execution by Mar-16 could add meaningfully to volumes.

Key risks to our SELL stance:

(a) Higher price cuts to pass on benefits of cheaper domestic gas: We build in higher gross margin of `10.14/10.44 in FY16/FY17 per unit of volume, assuming lower gas prices. We expect IGL to pass on 50% of the gas price benefit to the end consumers. However, IGL might have to take price cuts to arrest volume declines due to local government intervention, which may impact EBITDA margin on a unit volume basis.

(c) Higher shift towards Metro: Long-distance daily travellers shifting towards the time-efficient Delhi Metro with improved connectivity can impact IGL’s volumes over the medium to long term. However, we believe there is a space for both DTC buses as well as the Metro in public transportation. As car owners shift to using the Metro, they will also demand better connectivity to the Metro stations; this in turn could boost the addition of buses making up for the lost volumes.

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 16

Income Statement

Year end Mar FY15 FY16E FY17E FY18E

Sales volume (mmcmd) 3.84 3.95 4.33 4.80

Gross margin (`/scm) 9.55 9.76 10.33 10.46

EBITDA (`/scm) 5.65 5.53 6.09 6.29

Net Revenue 36,810 32,450 35,196 40,562

Total Expenditure 28,880 24,473 25,572 29,553

EBIDTA 7,930 7,977 9,624 11,009

EBITDA (%) 21.5 24.6 27.3 27.1

Depreciation 1,487 1,716 1,841 1,916

EBIT 6,443 6,261 7,783 9,093

Interest expense 298 142 135 128

PBT 6,490 6,369 7,898 9,215

Current Tax (2,113) (2,102) (2,606) (3,041)

Recurring PAT 4,377 4,267 5,292 6,174

Recurring EPS (`) 31.3 30.5 37.8 44.1

Source: Ambit Capital research, Company

Balance sheet

Year end Mar FY15 FY16E FY17E FY18E

Share Holders fund 20,981 23,513 26,652 30,315 Deposit from customers 3,260 3,422 3,594 3,773 Loans 1,453 1,380 1,311 1,246 Total Debt 4,713 4,803 4,905 5,019 Capital Employed 26,966 29,588 32,829 36,606 Gross Fixed Assets 31,825 34,325 36,825 38,325 Accumulated Depreciation 12,267 13,983 15,825 17,741 Net Fixed Assets 19,558 20,342 21,001 20,584 Capital WIP 2,541 2,287 2,058 1,852 Net Assets 22,099 22,629 23,059 22,437 Current Assets without cash 3,413 2,856 3,097 3,523 Current Liabilities 3,769 4,748 5,374 6,120 Net working capital (356) (1,892) (2,277) (2,597) Cash and bank balance 2,315 5,651 8,528 12,895 Capital Deployed 26,966 29,588 32,829 36,606 Source: Ambit Capital research, Company

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 17

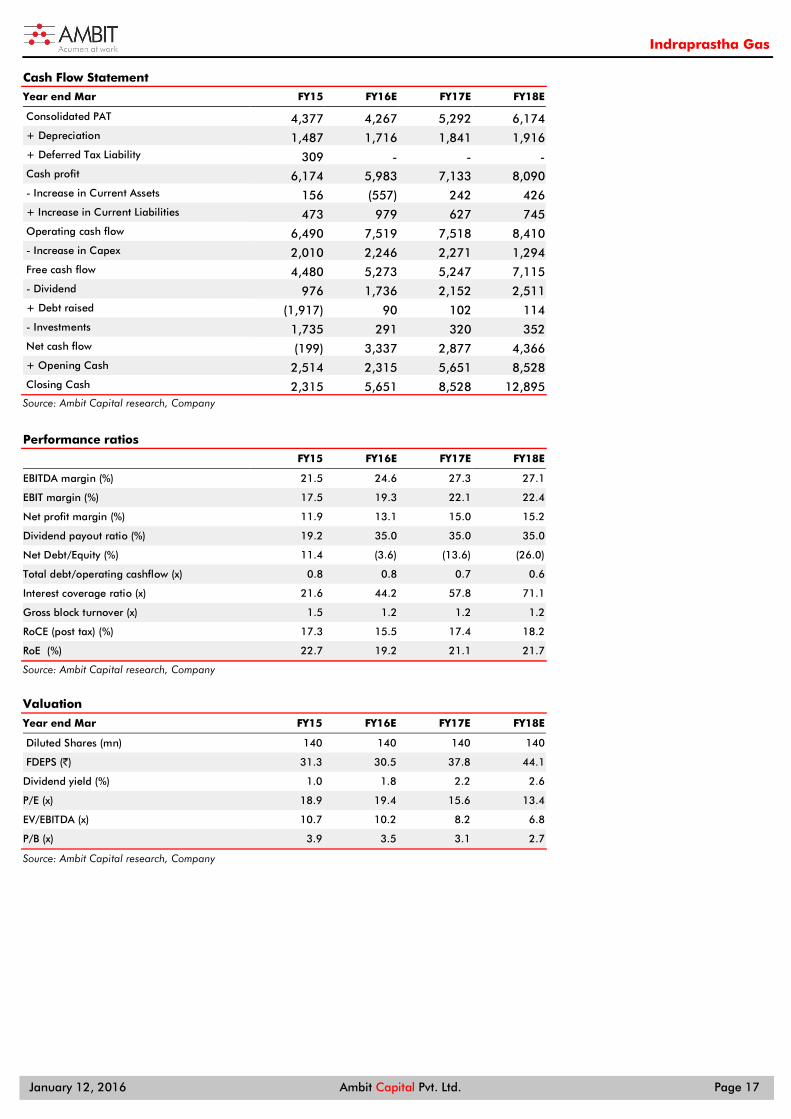

Cash Flow Statement

Year end Mar FY15 FY16E FY17E FY18E

Consolidated PAT 4,377 4,267 5,292 6,174

+ Depreciation 1,487 1,716 1,841 1,916

+ Deferred Tax Liability 309 - - - Cash profit 6,174 5,983 7,133 8,090

- Increase in Current Assets 156 (557) 242 426

+ Increase in Current Liabilities 473 979 627 745

Operating cash flow 6,490 7,519 7,518 8,410

- Increase in Capex 2,010 2,246 2,271 1,294

Free cash flow 4,480 5,273 5,247 7,115

- Dividend 976 1,736 2,152 2,511

+ Debt raised (1,917) 90 102 114

- Investments 1,735 291 320 352

Net cash flow (199) 3,337 2,877 4,366

+ Opening Cash 2,514 2,315 5,651 8,528

Closing Cash 2,315 5,651 8,528 12,895 Source: Ambit Capital research, Company

Performance ratios

FY15 FY16E FY17E FY18E

EBITDA margin (%) 21.5 24.6 27.3 27.1

EBIT margin (%) 17.5 19.3 22.1 22.4

Net profit margin (%) 11.9 13.1 15.0 15.2

Dividend payout ratio (%) 19.2 35.0 35.0 35.0

Net Debt/Equity (%) 11.4 (3.6) (13.6) (26.0)

Total debt/operating cashflow (x) 0.8 0.8 0.7 0.6

Interest coverage ratio (x) 21.6 44.2 57.8 71.1

Gross block turnover (x) 1.5 1.2 1.2 1.2

RoCE (post tax) (%) 17.3 15.5 17.4 18.2

RoE (%) 22.7 19.2 21.1 21.7

Source: Ambit Capital research, Company

Valuation

Year end Mar FY15 FY16E FY17E FY18E

Diluted Shares (mn) 140 140 140 140

FDEPS (`) 31.3 30.5 37.8 44.1

Dividend yield (%) 1.0 1.8 2.2 2.6

P/E (x) 18.9 19.4 15.6 13.4

EV/EBITDA (x) 10.7 10.2 8.2 6.8

P/B (x) 3.9 3.5 3.1 2.7

Source: Ambit Capital research, Company

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 18

Institutional Equities Team Saurabh Mukherjea, CFA CEO, Institutional Equities (022) 30433174 [email protected]

Research

Analysts Industry Sectors Desk-Phone E-mail

Nitin Bhasin - Head of Research E&C / Infra / Cement / Industrials (022) 30433241 [email protected]

Aadesh Mehta, CFA Banking / Financial Services (022) 30433239 [email protected]

Aakash Adukia Oil & Gas / Chemicals / Agri Inputs (022) 30433273 [email protected]

Abhishek Ranganathan, CFA Retail / Mid-caps (022) 30433085 [email protected]

Achint Bhagat, CFA Cement / Roads / Home Building (022) 30433178 [email protected]

Ashvin Shetty, CFA Automobile (022) 30433285 [email protected]

Bhargav Buddhadev Power Utilities / Capital Goods (022) 30433252 [email protected]

Deepesh Agarwal, CFA Power Utilities / Capital Goods (022) 30433275 [email protected] Dhiraj Mistry, CFA Consumer (022) 30433264 [email protected]

Gaurav Khandelwal, CFA Automobile (022) 30433132 [email protected] Girisha Saraf Mid-caps / Small-caps (022) 30433211 [email protected]

Karan Khanna, CFA Strategy (022) 30433251 [email protected]

Kushank Poddar Technology (022) 30433203 [email protected] Pankaj Agarwal, CFA Banking / Financial Services (022) 30433206 [email protected]

Paresh Dave, CFA Healthcare (022) 30433212 [email protected]

Parita Ashar, CFA Metals & Mining (022) 30433223 [email protected]

Prashant Mittal, CFA Derivatives (022) 30433218 [email protected]

Rahil Shah Banking / Financial Services (022) 30433217 [email protected]

Rakshit Ranjan, CFA Consumer (022) 30433201 [email protected]

Ravi Singh Banking / Financial Services (022) 30433181 [email protected]

Ritesh Gupta, CFA Oil & Gas / Chemicals / Agri Inputs (022) 30433242 [email protected]

Ritesh Vaidya, CFA Consumer (022) 30433246 [email protected] Ritika Mankar Mukherjee, CFA Economy / Strategy (022) 30433175 [email protected]

Ritu Modi Automobile (022) 30433292 [email protected]

Sagar Rastogi Technology (022) 30433291 [email protected]

Sumit Shekhar Economy / Strategy (022) 30433229 [email protected]

Utsav Mehta, CFA E&C / Industrials (022) 30433209 [email protected]

Vivekanand Subbaraman, CFA Media (022) 30433261 [email protected]

Sales

Name Regions Desk-Phone E-mail

Sarojini Ramachandran - Head of Sales UK +44 (0) 20 7614 8374 [email protected]

Dharmen Shah India / Asia (022) 30433289 [email protected]

Dipti Mehta India / USA (022) 30433053 [email protected]

Hitakshi Mehra India (022) 30433204 [email protected]

Krishnan V India / Asia (022) 30433295 [email protected]

Nityam Shah, CFA USA / Europe (022) 30433259 [email protected]

Parees Purohit, CFA UK / USA (022) 30433169 [email protected]

Praveena Pattabiraman India / Asia (022) 30433268 [email protected]

Shaleen Silori India (022) 30433256 [email protected]

Singapore

Pramod Gubbi, CFA – Director Singapore +65 8606 6476 [email protected]

Shashank Abhisheik Singapore +65 6536 1935 [email protected]

USA / Canada

Ravilochan Pola - CEO Americas +1(646) 361 3107 [email protected]

Production

Sajid Merchant Production (022) 30433247 [email protected]

Sharoz G Hussain Production (022) 30433183 [email protected]

Nikhil Pillai Database (022) 30433265 [email protected]

E&C = Engineering & Construction

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 19

Indraprastha Gas Ltd (IGL IN, BUY)

Source: Bloomberg, Ambit Capital research

0

100

200

300

400

500

600

Jan-

13

Mar

-13

May

-13

Jul-

13

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-

14

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-

15

Sep-

15

Nov

-15

INDRAPRASTHA GAS LTD

Indraprastha Gas

January 12, 2016 Ambit Capital Pvt. Ltd. Page 20

Explanation of Investment Rating

Investment Rating Expected return (over 12-month)

BUY >10%

SELL <10%

NO STANCE We have forward looking estimates for the stock but we refrain from assigning valuation and recommendation

UNDER REVIEW We will revisit our recommendation, valuation and estimates on the stock following recent events

NOT RATED We do not have any forward looking estimates, valuation or recommendation for the stock

Disclaimer

This report or any portion hereof may not be reprinted, sold or redistributed without the written consent of Ambit Capital. AMBIT Capital Research is disseminated and available primarily electronically, and, in some cases,

in printed form.

Additional information on recommended securities is available on request.

Disclaimer

1. AMBIT Capital Private Limited (“AMBIT Capital”) and its affiliates are a full service, integrated investment banking, investment advisory and brokerage group. AMBIT Capital is a Stock Broker, Portfolio Manager and Depository Participant registered with Securities and Exchange Board of India Limited (SEBI) and is regulated by SEBI

2. AMBIT Capital makes best endeavours to ensure that the research analyst(s) use current, reliable, comprehensive information and obtain such information from sources which the analyst(s) believes to be reliable. However, such information has not been independently verified by AMBIT Capital and/or the analyst(s) and no representation or warranty, express or implied, is made as to the accuracy or completeness of any information obtained from third parties. The information, opinions, views expressed in this Research Report are those of the research analyst as at the date of this Research Report which are subject to change and do not represent to be an authority on the subject. AMBIT Capital may or may not subscribe to any and/ or all the views expressed herein.

3. This Research Report should be read and relied upon at the sole discretion and risk of the recipient. If you are dissatisfied with the contents of this complimentary Research Report or with the terms of this Disclaimer, your sole and exclusive remedy is to stop using this Research Report and AMBIT Capital or its affiliates shall not be responsible and/ or liable for any direct/consequential loss howsoever directly or indirectly, from any use of this Research Report.

4. If this Research Report is received by any client of AMBIT Capital or its affiliate, the relationship of AMBIT Capital/its affiliate with such client will continue to be governed by the terms and conditions in place between AMBIT Capital/ such affiliate and the client.

5. This Research Report is issued for information only and the 'Buy', 'Sell', or ‘Other Recommendation’ made in this Research Report such should not be construed as an investment advice to any recipient to acquire, subscribe, purchase, sell, dispose of, retain any securities and should not be intended or treated as a substitute for necessary review or validation or any professional advice. Recipients should consider this Research Report as only a single factor in making any investment decisions. This Research Report is not an offer to sell or the solicitation of an offer to purchase or subscribe for any investment or as an official endorsement of any investment.

6. This Research Report is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied in whole or in part, for any purpose. Neither this Research Report nor any copy of it may be taken or transmitted or distributed, directly or indirectly within India or into any other country including United States (to US Persons), Canada or Japan or to any resident thereof. The distribution of this Research Report in other jurisdictions may be strictly restricted and/ or prohibited by law or contract, and persons into whose possession this Research Report comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition.

7. Ambit Capital Private Limited is registered as a Research Entity under the SEBI (Research Analysts) Regulations, 2014. SEBI Reg.No.- INH000000313. Conflict of Interests

8. In the normal course of AMBIT Capital’s business circumstances may arise that could result in the interests of AMBIT Capital conflicting with the interests of clients or one client’s interests conflicting with the interest of another client. AMBIT Capital makes best efforts to ensure that conflicts are identified and managed and that clients’ interests are protected. AMBIT Capital has policies and procedures in place to control the flow and use of non-public, price sensitive information and employees’ personal account trading. Where appropriate and reasonably achievable, AMBIT Capital segregates the activities of staff working in areas where conflicts of interest may arise. However, clients/potential clients of AMBIT Capital should be aware of these possible conflicts of interests and should make informed decisions in relation to AMBIT Capital’s services.

9. AMBIT Capital and/or its affiliates may from time to time have or solicit investment banking, investment advisory and other business relationships with companies covered in this Research Report and may receive compensation for the same.

Additional Disclaimer for U.S. Persons

10. The research report is solely a product of AMBIT Capital 11. AMBIT Capital is the employer of the research analyst(s) who has prepared the research report 12. Any subsequent transactions in securities discussed in the research reports should be effected through Enclave Capital LLC. (“Enclave”). 13. Enclave does not accept or receive any compensation of any kind for the dissemination of the AMBIT Capital research reports. 14. The research analyst(s) preparing the email / Research Report/ attachment is resident outside the United States and is/are not associated persons of any U.S. regulated broker-dealer and that therefore the analyst(s)

is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satisfy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securities held by a research analyst account.

15. This report is prepared, approved, published and distributed by the Ambit Capital located outside of the United States (a non-US Group Company”). This report is distributed in the U.S.by Enclave Capital LLC, a U.S. registered broker dealer, on behalf of Ambit Capital only to major U.S. institutional investors (as defined in Rule 15a-6 under the U.S. Securities Exchange Act of 1934 (the “Exchange Act”)) pursuant to the exemption in Rule 15a-6 and any transaction effected by a U.S. customer in the securities described in this report must be effected through Enclave Capital LLC (19 West 44th Street, suite 1700, New York, NY 10036).

16. As of the publication of this report Enclave Capital LLC, does not make a market in the subject securities. 17. This document does not constitute an offer of, or an invitation by or on behalf of Ambit Capital or its affiliates or any other company to any person, to buy or sell any security. The information contained herein has

been obtained from published information and other sources, which Ambit Capital or its Affiliates consider to be reliable. None of Ambit Capital accepts any liability or responsibility whatsoever for the accuracy or completeness of any such information. All estimates, expressions of opinion and other subjective judgments contained herein are made as of the date of this document. Emerging securities markets may be subject to risks significantly higher than more established markets. In particular, the political and economic environment, company practices and market prices and volumes may be subject to significant variations. The ability to assess such risks may also be limited due to significantly lower information quantity and quality. By accepting this document, you agree to be bound by all the foregoing provisions.

Additional Disclaimer for Canadian Persons

18. AMBIT Capital is not registered in the Province of Ontario and /or Province of Québec to trade in securities and/or to provide advice with respect to securities. 19. AMBIT Capital's head office or principal place of business is located in India. 20. All or substantially all of AMBIT Capital's assets may be situated outside of Canada. 21. It may be difficult for enforcing legal rights against AMBIT Capital because of the above. 22. Name and address of AMBIT Capital's agent for service of process in the Province of Ontario is: Torys LLP, 79 Wellington St. W., 30th Floor, Box 270, TD South Tower, Toronto, Ontario M5K 1N2 Canada. 23. Name and address of AMBIT Capital's agent for service of process in the Province of Montréal is Torys Law Firm LLP, 1 Place Ville Marie, Suite 1919 Montréal, Québec H3B 2C3 Canada. Additional Disclaimer for Singapore Persons 24. This Report is prepared and distributed by Ambit Capital Private Limited and distributed as per the approved arrangement under Paragraph 9 of Third Schedule of Securities and Futures Act (CAP 289) and Paragraph

11 of the First Schedule to the Financial Advisors Act (CAP 110) provided to Ambit Singapore Pte. Limited by Monetary Authority of Singapore. 25. This Report is only available to persons in Singapore who are institutional investors (as defined in section 4A of the Securities and Futures Act (Cap. 289) of Singapore (the “SFA”).” Accordingly, if a Singapore Person is

not or ceases to be such an institutional investor, such Singapore Person must immediately discontinue any use of this Report and inform Ambit Singapore Pte. Limited. Disclosures 26. The analyst (s) has/have not served as an officer, director or employee of the subject company. 27. There is no material disciplinary action that has been taken by any regulatory authority impacting equity research analysis activities. 28. All market data included in this report are dated as at the previous stock market closing day from the date of this report. 29. Ambit and/or its associates have financial interest/equity shareholding in GAIL. Analyst Certification Each of the analysts identified in this report certifies, with respect to the companies or securities that the individual analyses, that (1) the views expressed in this report reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly dependent on the specific recommendations or views expressed in this report. © Copyright 2015 AMBIT Capital Private Limited. All rights reserved.

Ambit Capital Pvt. Ltd. Ambit House, 3rd Floor. 449, Senapati Bapat Marg, Lower Parel, Mumbai 400 013, India. Phone: +91-22-3043 3000 | Fax: +91-22-3043 3100 CIN: U74140MH1997PTC107598 www.ambitcapital.com