challenges & opportunities for cil

TRANSCRIPT

Challenges and Opportunities before Coal

India

09.05. 2016K D PRASAD

General Manager(M)/(ViG) BCCL

Challenges• Diminishing Reserve of shallow cover• Retirement of experienced work force• Increasing demand of energy • Outdated production technology• Competition from China • Devaluation Indian Currency• Less FDI in coal industry

Challenges

• Poor strength of ruling party in Rajya Sabha• Poor Moral Value of Indians• Corruption• Bureaucratic delays as quoted by Coal

Secretary 5 C’s ( CAG, CIC, CVC, CBI & Court)• Democratic government • Judicial Activism• Political Activism

Challenges

• NGO funded by non friendly countries• Naxalite movement• RTI Activist with vested interest• Politically motivated medias• Lack in Co-ordination between State Govt and

Central Govt in some states• Legislation lagging behind technology• Poor civic sense in Indians

4th COAL SUMMIT 2012

Strategy for Bridging the Gap to meet the future need

of Coal Industry in India

20th Nov, 2012

N Kumar Director (Tech)

Coal India Limited

INDIAN COAL RESOURCES (Bt) - As on 01.04.2012

Type -wise Proved Indicated Inferred Total %

Coking 17.93 13.65 2.11 33.69 11.48

Non-Coking 99.62 128.42 30.28 258.32 88.00

Tertiary 0.59 0.10 0.80 1.49 0.52

Total 118.14 142.17 33.18 293.50

Depth -wise0- 300 91.92 71.46 10.76 174.14 59.33

300- 600 11.04 58.42 16.26 85.72 29.21

0 – 600(Jharia coalfield only)

13.71 0.50 0.00 14.21 4.84

600 – 1200 1.47 11.79 6.17 19.43 6.62

Coal Resource Availability/ distribution Scenario (As on 01.04.12)

Total Resource (Bt) 293.50

CIL Command area 66.00

Captive allocation 45.00

Power 28.00

Others 17.00

Others 12.00

Captive (Unallocated) 22.00

104.50Unblocked

ALL INDIA DEMAND / SUPPLY SCENARIO- Past Trend

Figs in Mt TY IX Plan

TY X Plan

XI Plan

01-02 06-07 07-08 08-09 09-10 10-11 11-12

(Act) (Act) (Act)

Demand 354 474 493 550 598 656 650

CAGR % 2.32 6.00 6.52

Demand Materialization

352 464 504 549 588 593 636

Through Ind. Supply

331 421 454 490 515 524 537

CAGR % 2.15 4.93 4.98Through Import 21 43 50 59 73 69 99

Coking 11 18 22 21 25 20 30Non-coking 10 25 28 38 48 49 69

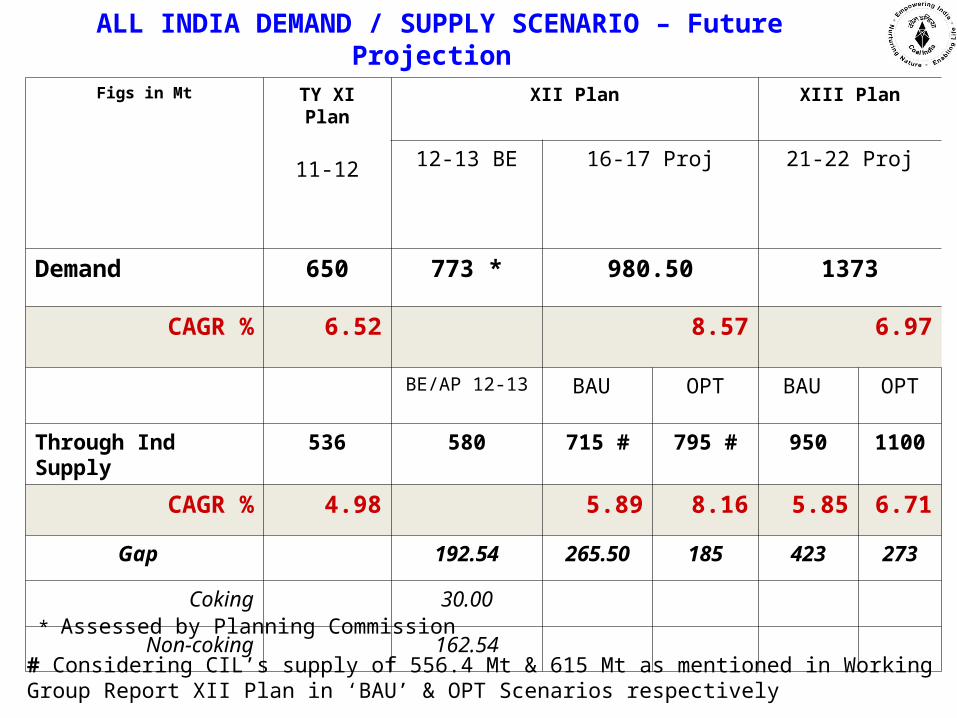

ALL INDIA DEMAND / SUPPLY SCENARIO – Future Projection

Figs in Mt TY XI Plan

11-12

XII Plan XIII Plan

12-13 BE 16-17 Proj 21-22 Proj

Demand 650 773 * 980.50 1373CAGR % 6.52 8.57 6.97

BE/AP 12-13 BAU OPT BAU OPTThrough Ind Supply

536 580 715 # 795 # 950 1100

CAGR % 4.98 5.89 8.16 5.85 6.71Gap 192.54 265.50 185 423 273

Coking 30.00Non-coking 162.54

* Assessed by Planning Commission# Considering CIL’s supply of 556.4 Mt & 615 Mt as mentioned in Working Group Report XII Plan in ‘BAU’ & OPT Scenarios respectively

Year-wise/Sector-wise Coal Consumption/Demand-Mt

Sector TY X Plan

XI Plan XII Plan

06-07 07-08 08-09 09-10 10-11 11-12 12-13 16-17

(Actual) TGT/AP12-13

PROJ

Steel 35.17 39.00 37.66 41.14 36.81 42.08 52.30 67.20

Power (U)

307.92 332.40 362.08 378.30 390.09

399.09 512.00 682.08

CAGR % 4.32 5.32 11.31

Others 120.78 132.89 149.28 167.77 166.10 194.45 208.54 231.22

Total 463.87 504.29 549.02 587.81 593.00

635.62 772.84 980.50

CAGR % 5.70 6.50 9.06

Source-wise Production (Mt) – Past Trend & Programme for 12-13 & XII Plan (Mt)

TY of VIII Plan

(96-97

TY of IX Plan

(01-02)

TY of X Plan

(06-07)

TY XI Plan(11-12)

XII Plan (12-13)

XII Plan (16-17)(BAU)

XII Plan (16-17)(OPT)

Production Actual TGT PROJ

CIL 250.62 279.65 360.91 435.84 464.10 556.40 615.00 #

CAGR % 4.19 2.22 5.23 3.84 ( 6.48)* 5.00 7.13

Non-CIL 38.70 48.14 69.92 103.95 110.30 158.60 180.00

All India 289.32 327.79 430.83 539.79 574.40 715.00 795.00

CAGR % 4.44 2.53 5.62 4.61 (6.42)* 5.78 8.05

11

* Growth% over previous year# The production in Optimistic Scenario is available only if the requisite clearances are processed in fast-tracked route and delivered within the specified time schedule. The issues affecting land acquisition, R & R, law & order and evacuation infrastructure in particular will also have to be addressed in a time bound manner

12

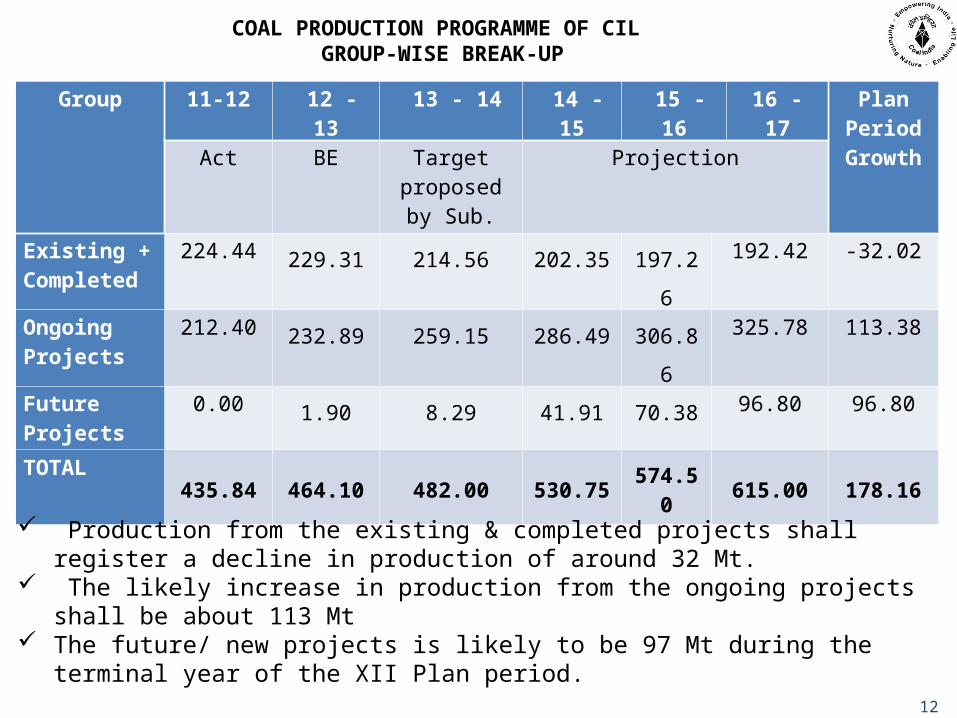

COAL PRODUCTION PROGRAMME OF CIL GROUP-WISE BREAK-UP

Group 11-12 12 - 13 13 - 14 14 - 15

15 - 16 16 - 17 Plan Period GrowthAct BE Target

proposed by Sub.

Projection

Existing + Completed

224.44 229.31 214.56 202.35 197.26 192.42 -32.02

Ongoing Projects

212.40 232.89 259.15 286.49 306.86 325.78 113.38

Future Projects

0.00 1.90 8.29 41.91 70.38 96.80 96.80

TOTAL435.84 464.10 482.00 530.75 574.5

0 615.00 178.16

Production from the existing & completed projects shall register a decline in production of around 32 Mt.

The likely increase in production from the ongoing projects shall be about 113 Mt

The future/ new projects is likely to be 97 Mt during the terminal year of the XII Plan period.

ON-GOING PROJECTS

• 147 Projects & approved schemes are under execution (Ultimate Capacity – about 437 Mty, approved Capital – Rs30,000 Crs) projected to contribute 333 Mt in 16-17.

• Plan period growth – 115 Mt.• Bulk of incremental production to come from 54 projects -

incremental production - 190 Mt.• Out of these 147 projects required clearances are available

in 82 projects, 34 projects are awaiting forestry clearances, 13 projects are awaiting environmental clearances & 18 projects require both the environmental & forestry clearances. About 42 major projects are affected due to delays in Land acquisition.

• All identified activities of these 54 projects to achieve desired level of production are being monitored stringently at appropriate level.

NEW / EXPANSION PROJECTS – XII Plan

• Envisaged to take up 126 new projects in XII Plan . (58

spill-over from XI Plan + 63 new)

• PR Cap – 422 mty ., Env. Cap Inv – 85,000 Crs

• 60 projects(PR cap- 214 Mty) to contribute around 93

Mt

• Projected production - 98 Mt in 16-17.

• Bulk of projected growth will come from - from

coalfields of N.Karanpura, Ib, Talcher & Mand-Raigarh.

Based on LOA’s granted by SLC(LT) & other commitments, the future coal balance for CIL is to a large extent (-) ve

The envisaged production of CIL is

less than the commitments already made

The peak deficit of (447 Mt) 96 % is in

FY 2013This necessitates to

augment the domestic coal

production. Increase in domestic

production is very much uncertain and

as such requires enhance import

facilities

911 913 917 922 926

-447 -425 -387 -347 -311

96 87 73 60 51

615575531488464

-600

-400

-200

0

200

400

600

800

1000

12-13 13-14 14-15 15-16 16-17

Projected Production Total Commitment based on LoAs

Coal Balance Ratio of Coal Deficit to Proj Prod

Figs in Mt 12-13 13-14 14-15 15-16 16-17Projected Production 464 488 531 575 615Total Commitment based on LoAs 911 913 917 922 926Coal Balance -447 -425 -387 -347 -311Ratio of Coal Deficit to Proj Prod 96 87 73 60 51

The responsibility of CIL will be huge given the New Coal Distribution Policy which envisage total demand of the country to be met by CIL including coal imports, if required.

Challenges for Enhancing Domestic Coal Production

Performance Indicator Reason for Delay Under the XI Plan, the envisaged

land acquisition was > 62 Thousands Ha Against it, during XI Plan, CIL

was able to acquire only approx 25,000 Ha, i.e. ~ 40 % of the target

Under the XII Plan, envisaged land acquisition is approx 65 Thousands Ha

Bulk of land envisaged for acquisition in XI plan was tenancy land

However, going ahead the proportion of forest land will increase It is understood that from the

present proportion of 30 %, the forest land will increase to 50 % in the future years

Forest Land

Involvement of multiple state and central government agencies in forest land acquisition leading to inordinate procedural delay

Tenancy Land

Proper Record of Rights (RoR) not being available with State Governments for identification of ownership of land causes problems in ascertaining the actual ownership of the land. This complicates the R & R process thus delaying the land acquisition.

• Land Acquisition is the biggest bottleneck in coal mining operations– CIL has faced prolonged delays in many of its projects leading to loss of production– Even after acquisition, possession of land presents another problem to the company

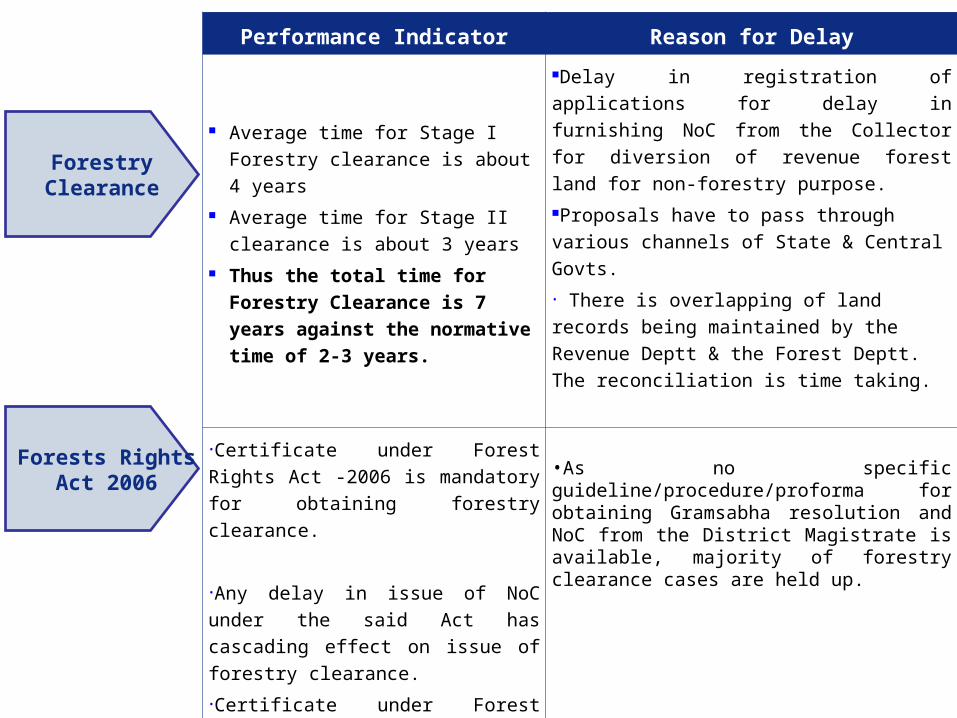

Forests Rights Act 2006

Performance Indicator Reason for Delay

Average time for Stage I Forestry clearance is about 4 years

Average time for Stage II clearance is about 3 years

Thus the total time for Forestry Clearance is 7 years against the normative time of 2-3 years.

Delay in registration of applications for delay in furnishing NoC from the Collector for diversion of revenue forest land for non-forestry purpose.Proposals have to pass through various channels of State & Central Govts. • There is overlapping of land records being maintained by the Revenue Deptt & the Forest Deptt. The reconciliation is time taking.

•Certificate under Forest Rights Act -2006 is mandatory for obtaining forestry clearance.

•Any delay in issue of NoC under the said Act has cascading effect on issue of forestry clearance.•Certificate under Forest Rights Act -2006 has been made mandatory even for renewal cases of Forest Clearances also.

•As no specific guideline/procedure/proforma for obtaining Gramsabha resolution and NoC from the District Magistrate is available, majority of forestry clearance cases are held up.

Forestry Clearance

Performance Indicator Reason for Delay

For every coal project it is mandatory.

It takes long time than statute

Considerable time is taken in obtaining ‘Consent to Establish’ and ‘Consent to Operate’ certificates.

Delay occurs in receipt of TOR. Delay in holding the public consultation

process. EIA 2006 indicates a time limit of 45 days for completion of the “Public Consultation Process” which is not fulfilled.

Environment Clearance is normally granted up-to a certain peak capacity (projected peak production) for a specific project. Capacity enhancement of any project requires further environment clearance for the enhanced capacity from MoEF, which is also time consuming.

Environmental Clearance

Performance Indicator Reason for Delay

In last 7 years coal stock was increased by approx 48 Mt due to non-availability of, Sufficient railway rakes Matching feeder lines

as well as loading facilities in IB Valley, Korba & N.Karanpura fields

Bulk of future production will come from 5 coal fields of CIL and it is imperative that continuous investment is made in logistics infrastructure

The progress of new railway line projects related to coal evacuation have not achieved the desired progress in the last few years (Tori-Shivpur-Hazaribagh, Angul-Kalinga, Gopalpur-Manoharpur,

Non-availability of sufficient number of railway rakes. This has improved in 2012-13 because of monitoring at the level of Chairman, Railway Board. CCL , MCL & BCCL are

particularly facing the problems in dispatch of coal and increasing coal inventory levels

Evacuation Infrastructure

Identification of Projects

58 coal projects of XI Plan spilled over to XII Plan and about 68 new projects tentatively identified for XII Plan period.

CIL Vision 2020

~ CIL, has formulated Vision 2020 document in view of the increasing requirements on the organization.

~ Six Strategic Themes has been identified, namely, Scalability of Production, Operational Excellence, Employer of Choice, Sustainability, Customer Orientation and Diversification.

~ Multiple initiatives have been discussed under each strategic theme to bring about the transformational change in the organization.

Exploration Activities

CIL is taking initiatives to enhance annual drilling capacity to 0.70 mn meters by FY2013 from 0.498 mn meters achieved in FY2012The company has intends to achieve conversion of inferred and indicated to proved reserves 3 times the historical performance. CIL is also undertaking systematic exploration to arrive at reliable estimate of coal reserves and application of information technology to create geo database.

INITIATIVES FROM CIL TO MEET GROWING DEMAND

Initiatives continued…

Implementation of Master Plans

CIL is actively working various control measures currently available for controlling underground mine fire (in Jharia and Raniganj) delineated in Master Plans. Implementation of Master Plan towards fire control, surface stabilization, rehabilitation with an estimated capital out lay to the tune of Rs.7112.11 crores, in turn CIL may able to recover locked coal to the tune of 1453 Mt to the possible extent.

At the time of Nationalisation, no of fires were 70. Affected surface area was 17.32 Km². After taking proper mitigation measures, the affected area reduced to 8.90 Km²

Coal Beneficiation

As on date, CIL is operating 17 washeries with cumulative throughput capacity of 39.04 Mty.

CIL is going to set up another 20 integrated coal washaries with total capacity of 111.10 Mty to supply washed metallurgical as well as thermal coal to consumers.

This will not only save transportation cost of high amount of ash contained in Indian coal but also able to supply coal with much higher calorific value vis-a-vis higher fixed carbon contained in steel and power sectors.

Underground Mining

CIL has turned its focus back on UG Mining for sustainable development.

It has identified a number of UG Greenfield properties. Envisaged to enhance production of about 55 Mt in 16-17 from

existing level of 40 Mt.

Initiatives continued…

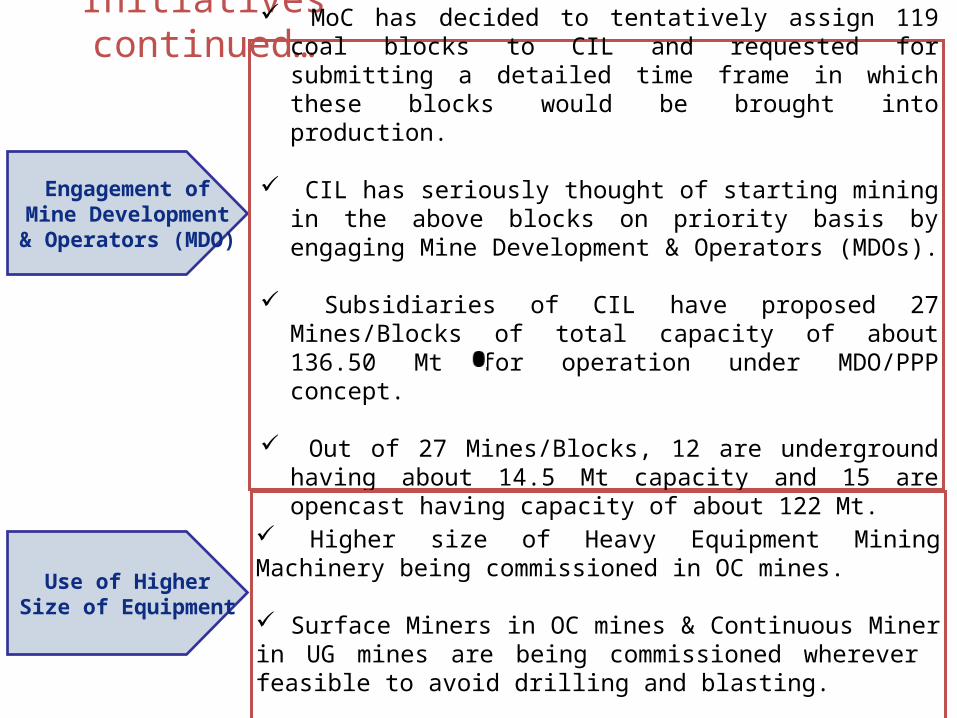

Engagement of Mine Development &

Operators (MDO)

MoC has decided to tentatively assign 119 coal blocks to CIL and requested for submitting a detailed time frame in which these blocks would be brought into production.

CIL has seriously thought of starting mining in the above blocks on priority basis by engaging Mine Development & Operators (MDOs).

Subsidiaries of CIL have proposed 27 Mines/Blocks of total capacity of about 136.50 Mt for operation under MDO/PPP concept.

Out of 27 Mines/Blocks, 12 are underground having

about 14.5 Mt capacity and 15 are opencast having capacity of about 122 Mt.

Use of Higher Size of Equipment

Higher size of Heavy Equipment Mining Machinery being commissioned in OC mines.

Surface Miners in OC mines & Continuous Miner in UG mines are being commissioned wherever feasible to avoid drilling and blasting.

BUSINESS MODEL:• Equity Model

– Stake with off take contract in brown field assets

– 100% or majority stake in green field assets

• Off-take Model :

– Long term contract essentially with coal miners– Short term contract

TARGET PRODUCTS & DESTINATIONS:

• Mozambique – Coking & thermal from own assets

• Indonesia - Thermal coal [ > 4000 kcal/kg (ARB)]

• South Africa - Thermal Coal [ > 5500 kcal/kg(ARB)]

• USA - Thermal Coal [ > 6000 kcal/kg(ARB)]

• Australia - Thermal Coal [ > 5500 kcal/kg(ARB)] 23

Foreign Acquisitions - Strategy Framework

Mozambique: 2 coal blocks acquired in Mozambique , Area - 224 sq km Location – Moatize district, Tete Province Wholly owned subsidiary Coal India Africana Limitada

registered in Mozambique, Office opened in Tete in March 2012 Team of senior officers posted

Drilling started

24

Initiatives taken so far – Equity Model

25

Initiatives taken so far – Equity Model

South Africa: MoU signed with Provincial Govt. of Limpopo in 2011 Strategic alliance for exploration and development of coal

assets in Limpopo Province Potential zones for coal resources identified

CIL Vision 2020, adopted by the Board of Coal India, makes several fundamental suggestions to improve domestic supply

Recommendations Key actions

Establishment of a Project Management Office (PMO) for large future projects

• Increased delegation of power of a Multi-Tier Org spanning CIL level, Subsidiary HQ and Project

• Specialized training (PMP certifications etc.) and full-staffing of all roles• Modern way of working

Development of Contractor Market

• Attractive contract terms to encourage private sector participation, esp. those with superior technologies and good practices

• Road-shows to attract potential partners (esp. in UG mining, exploration & technical services etc.)

Investment in Logistics • Investment in last-mile connectivity• Improvement of pit-head to siding infrastructure• Creation of logistics as a separate function to build expertise• Formation of suitable JVs to execute projects

Continuous Improvement Program

• Improvements linked to incentives to increase motivation for participation• Large scale up-gradation of employee-skills to detect and report inefficiencies• Strong knowledge management

Other Actions Suggested

• Flexibility and independence in setting R&R policies and land compensation• More thrust on mechanization and commercialization of R&D partnerships• Focus on staffing of key roles (e.g. in E&F and L&R departments)• Thrust on exploration etc.

Actions being taken by Coal India to enhance domestic supply• Capacity augmentation by 180 MT planned during the 12th Plan period• Investment of Rs. 7500 Crores in Logistics over the next plan period• Road show for partners in UG Mining• New flexible R&R policy has been framed• Focus has been given on increased capacity of washed coal - tenders for 4

washeries (22.5 MT) out of 20 planned during the 12th plan completed• Special focus is being given to recruitment and back-fill of open positions in

critical departments• CIL is engaged with Governments to a greater degree to expedite various

clearances (PMO intervention sought for 178 clearances)• Pooling of coal prices may pave the way for linkage rationalization

Opportunities

• Educated Youth Population• Absolute majority Government in centre• Volatile world economy compared to stable

Indian Economy• Maha Ratna Status of Coal India• Less dependence on coal for energy of

developed countries• Merging of Energy, Coal and Power Ministry

Opportunities

• Outsourcing of work• MDO mode of contract• Employing mass production technology in UG

mines• Thrust on clean coal and renewable energy• Lifting of sanction from Iran and development

of CHARBAHAR Port in Iran by India

THANK YOU