ch 8. stocks and their valuation. goals to understand characteristics of common and preferred stocks...

TRANSCRIPT

Ch 8. Stocks and Their Valuation

Goals

• To understand characteristics of common and preferred stocks

• To understand stock valuations

1. Common stock valuation:

Cash flow patterns from holding a stock:

Dividend payment & Capital gains

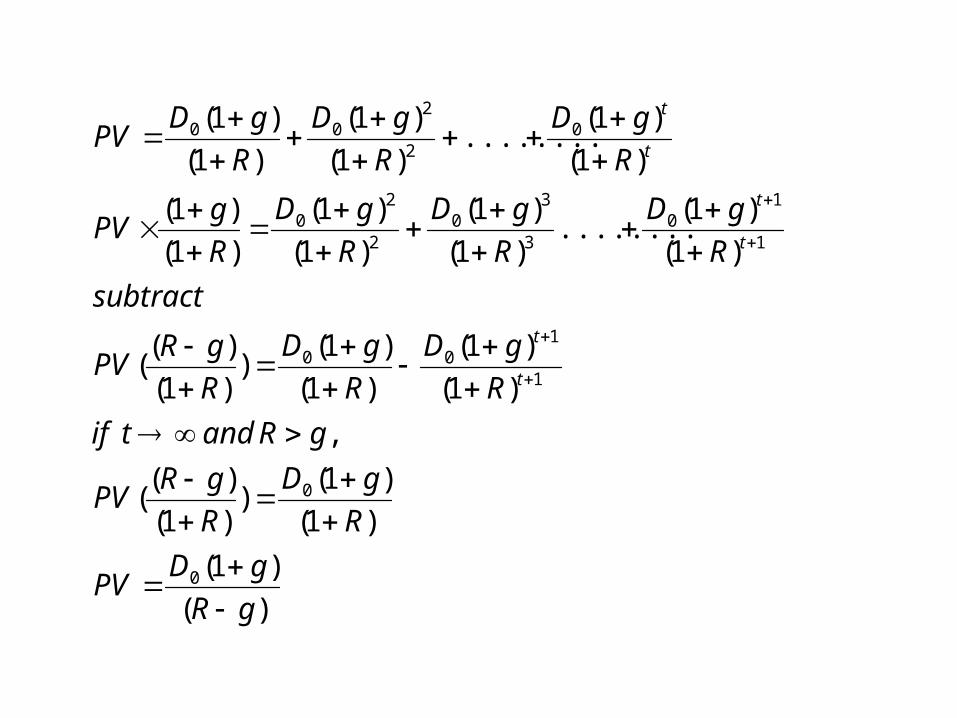

Basic starting formula:

..........)1/()1/()1/(

)1/()(

)1/()(

)1/()(

33

2210

332

221

110

RDRDRDPso

RPDP

RPDP

RPDP

• As shown before, stock prices mainly rely on the dividend payments. And depending on the patterns of dividend payments, we can come up with three types of stock pricing models.

• (1) Dividend Growth Model (Gordon Model)

• This model assumes that dividend payments will grow at a certain % every period

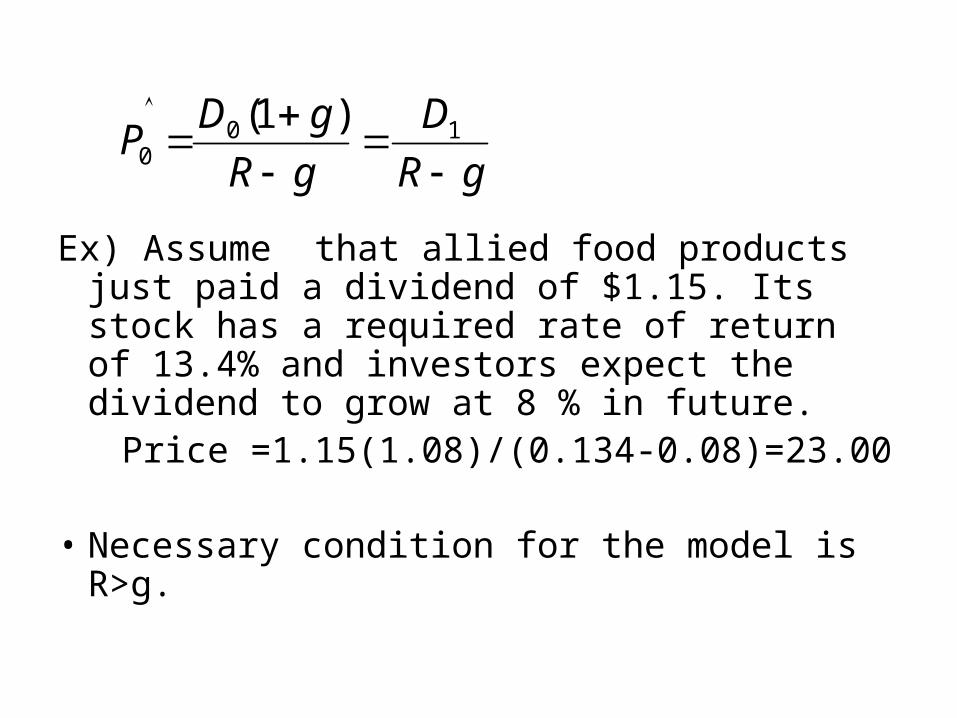

Ex) Assume that allied food products just paid a dividend of $1.15. Its stock has a required rate of return of 13.4% and investors expect the dividend to grow at 8 % in future.

Price =1.15(1.08)/(0.134-0.08)=23.00

• Necessary condition for the model is R>g.

gR

D

gR

gDP

100

)1(

)(

)1(

)1(

)1())1(

)((

,

)1(

)1(

)1(

)1())1(

)((

)1(

)1(........

)1(

)1(

)1(

)1(

)1(

)1(

)1(

)1(........

)1(

)1(

)1(

)1(

0

0

1

100

1

10

3

30

2

20

02

200

gR

gDPV

R

gD

R

gRPV

gRandtif

R

gD

R

gD

R

gRPV

subtract

R

gD

R

gD

R

gD

R

gPV

R

gD

R

gD

R

gDPV

t

t

t

t

t

t

• The dividend growth model is often appropriate for mature companies with a stable history of growth

• From the model, we are able to extract expected rate of return= expected dividend yield + expected growth rate (or capital gain yield)

(2) Zero Growth Model.• It assumes that dividend payment is constant.• P= D/R• It is used to evaluate the price of preferred stock

(3) Nonconstant Growth Model• It assumes no consistent patterns• Summation of present values has to be used to

calculate the stock price

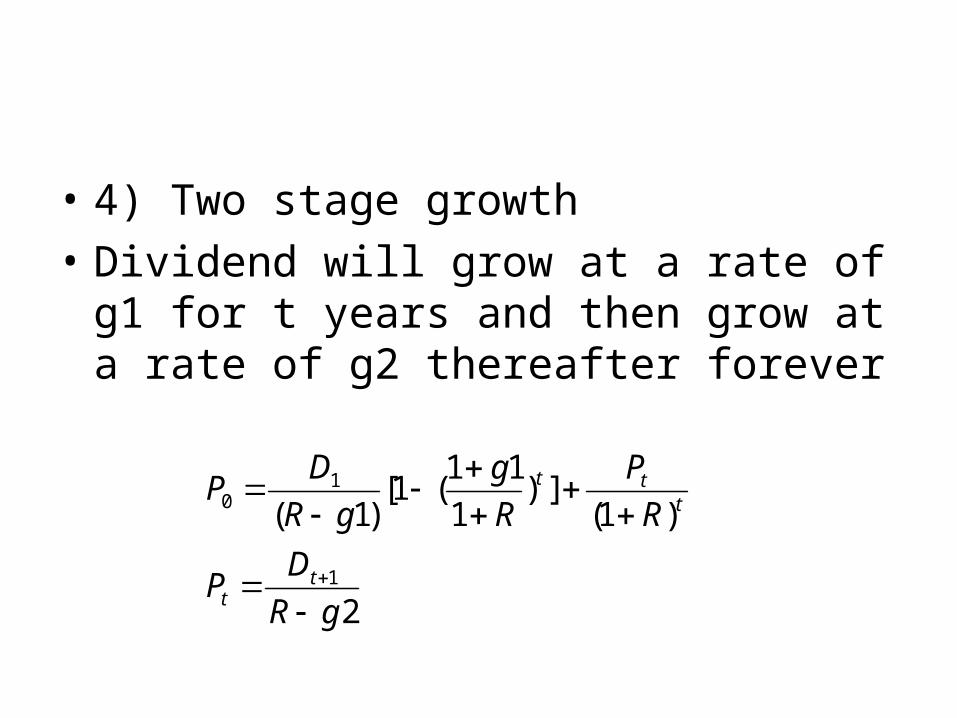

• 4) Two stage growth

• Dividend will grow at a rate of g1 for t years and then grow at a rate of g2 thereafter forever

2

)1(])

1

11(1[

)1(

1

10

gR

DP

R

P

R

g

gR

DP

tt

ttt

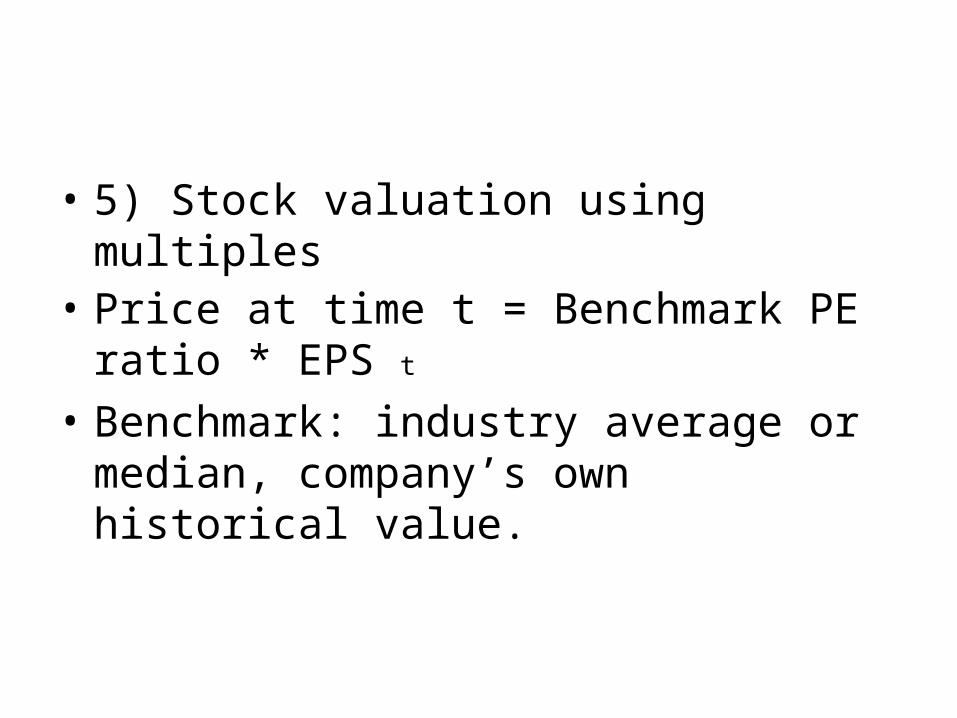

• 5) Stock valuation using multiples• Price at time t = Benchmark PE ratio *

EPS t

• Benchmark: industry average or median, company’s own historical value.

• 2. Components of the required rate of return

• R= D1/P0 + g

• = dividend yield + capital gains yield

• 3. Some features of common and preferred stocks

1) Common stock: equity without priority for dividends or in bankruptcy.

• Common stockholders with votes have the right to elect a firm’s directors who, in turn, elect the officers who manage the business.

• Each shares of stocks has one vote.• Two different voting procedures:• - Cumulative voting: after determining the

number of votes for each shareholder (usually number of shares * number of director candidates), then shareholders cast votes. If there are N directors up for election, then 1/(1+N) percent of the stock plus one share will guarantee you a seat. It is a common practice.

• - straight voting: a shareholder casts all votes for each director up for election. The only way to guarantee a seat is to own 50% + one share. It ignores the minority.

• Proxy: A grant of authority by a shareholder allowing another individual to vote his or her shares. Proxy fight: An attempt by a person or group to gain control of a firm by getting its stockholders to grant that person or group the authority to vote their shares to replace the current management.

• Classes of stocks: these classes (e.g. A, B) were created with unequal voting rights.

• Dividends: payments by a corporation to shareholders, made in either cash or stock.

• - the payment is at the discretion of board of directors. It is not a liability of the corporation.

• - the payment is not business expense.

• - dividends received are taxable.

• Other rights;

• - right to share proportionally in dividend paid

• - right to share proportionally in assets remaining after liabilities have been paid in a liquidation.

• - right to vote on stockholder matters of great importance, such as merger

• - sometimes, right to share proportionally in any new stock sold (preemptive right)

• 2) Preferred stock: stock with dividend priority over common stocks, normally with a fixed dividend rate, sometimes without voting rights.

• - stated value: it has a stated value, usually $100 per share. The cash dividend is described in terms of dollars per share.

• - cumulative and noncumulative dividends: if dividend is cumulative, unpaid dividend will be cumulative to next dividend payment. Common stock holders also must forgo dividends. Unpaid dividends are not debts.

• 4. The stock market: • Primary market: the market in which new

securities are originally sold to investors.• Secondary market: the market in which previously

issued securities are traded among investors.• Dealer: an agent who is ready to buy and sells

securities and maintains inventory. Source of profit to dealers is a bid-ask spread.

• Broker: an agent who arranges security transactions among investors. Brokers do not maintain an inventory.

• 1) NYSE (New York Stock Exchange Market).• Since 2006, it has become a public owned

corporation. Instead of purchasing seats, exchange members must purchase trading license whose number is limited to 1,366.

• Commission brokers: NYSE members who execute customer orders to buy and sell stock transmitted to the exchange floor.

• Specialists: NYSE members acting as dealers in a small number of securities assigned. They are market makers who has obligation to maintain a fair, orderly market for securities assigned to them, posting buying and selling prices.

• Floor brokers: NYSE members who execute order for commission brokers on a fee basis. Sometime, called $2 brokers.

• SuperDOT system: a system transmitting orders electronically directly to the specialists. Reducing the role of floor brokers.

• Floor traders: NYSE members who trade for their own accounts, trying to make profit over price fluctuation. Recently the number of floor traders dramatically reduce.

• 2) NASDAQ (National Association of Securities Dealers Automated Quotations System): computer network of securities dealers and others. NASDAQ dealers act as market makers with their own inventories, posting bid and ask prices.

• Differences between NASDAQ and NYSE:• - computer network and no physical location.• - multiple market maker system rather than

specialist system

•

• Over-the counter (OTC) market: securities market in which trading is almost exclusively done through dealers who buy and sell for their own inventories. NASDAQ was referred as OTC market before.

• NASDAQ is composed of three separate markets: NASDAQ Select Market (well known firms), NASDAQ Global Market (smaller size firms), and NASDAQ Capital Market (smallest size firms).

• ECNs (Electronic communications network): website that allows investors to trade directly with each other through NASDAQ.

• 3) Stock market reporting: Page 255