cfpb integrated mortgage disclosure presentation by orntic

TRANSCRIPT

Copyright 2014 ORNTIC

Copyright 2014 ORNTIC

Integrated Mortgage Disclosure Rule

Jack O’Donohue, Esq. O’Donohue Law, LLC

(978) 475-4896 [email protected]

Copyright 2014 ORNTIC

Copyright 2014 ORNTIC

The Final Rule 2013

Copyright 2014 ORNTICCopyright 2014 ORNTIC

ScopeExpanded to cover most closed-end mortgages except:

– Reverse mortgages – HELOC – Mobile home – Commercial purpose loans – Creditors making five or fewer loans per year – Certain no-interest, subordinate special purpose loans

Copyright 2014 ORNTICCopyright 2014 ORNTIC

Effective Dates Most provisions apply to applications

received by creditor or mortgage broker on and after 8/1/15

Some provisions take effect 8/1/15 without receipt of application state law exemption clarification requests use of estimates

What can you do now?

Copyright 2014 ORNTICCopyright 2014 ORNTIC

The New Jargon

▪ “Lender” is now “Creditor” ▪ “Borrower” is now “Consumer” ▪ TILA and GFE are now the Loan Estimate ▪ HUD1 is now the Closing Disclosure ▪ “Closing/Settlement” is now

“Consummation”

Copyright 2014 ORNTICCopyright 2014 ORNTIC

Loan Estimate Early Disclosure Form

Delivered within three business days of application and at least seven days prior to consummation*

Estimates allowed “Reasonably Available Standard” Acting in good faith, exercise due diligence, may

rely on other parties and must be labeled as “estimate”

*business day for LE purposes: any day company offices are open to the public conducting substantially all company business

Copyright 2014 ORNTIC

Reliance on the Real Estate Professionals

▪ Creditor may rely on third parties to obtain information for Loan Estimate

▪ “For example, the creditor might look to …. Realtors for taxes and escrow fees.”

Transfer taxes Seller credits Home warranties Personal property purchases HO Association fees Home Owner’s Insurance Flood Insurance

Copyright 2014 ORNTICCopyright 2014 ORNTIC

Change of Circumstance

1. Information provided by consumer inaccurate 2. Extraordinary event

3. Discovery of new info specific to consumer or transaction

4. Revision requested by consumer 5. On day of locking rate 6. After 10-day expiration

*Disclosure required within three days of knowledge but not on same day as Closing Disclosure

Copyright 2014 ORNTICCopyright 2014 ORNTIC

Preparation of Closing Disclosure

Final Rule determination: Creditors can continue to rely on settlement agents Gives creditors flexibility to divide responsibilities Suggested creditors provide Disclosure while

settlement agents make corrections at consummation

Creditor retention of liability

Copyright 2014 ORNTICCopyright 2014 ORNTIC

3-Day Review Period

Three business days* in advance of consummation** with limited re-disclosure requirements

*business day for CD purposes: all days except Sunday and 10 federal holidays

**consummation is defined as “the time that a consumer becomes contractually obligated on a credit transaction”

Copyright 2014 ORNTICCopyright 2014 ORNTIC

Delivery Defined

Hand delivery: immediate (deliver on Monday, close

on Thursday) US Mail: assumed receipt three days after placed in mail Email: with receipt confirmed by consumer after

approval to use email method of delivery (if not, assumed three days to open email)

Overnight Delivery: with consumer confirmed receipt

Copyright 2014 ORNTICCopyright 2014 ORNTIC

Re-disclosure Requirements

Requiring additional three-day review period

1. Inaccurate APR 2. Change in loan product 3. Prepayment penalty added

Copyright 2014 ORNTICCopyright 2014 ORNTIC

Waiver

Consumer may waive waiting period if they have a bona fide personal financial emergency. No waiver afforded for seller’s financial emergency.

Purposely narrow definition by example: an imminent sale of consumer’s home at foreclosure. Bureau chose not to expand definition.

Copyright 2014 ORNTICCopyright 2014 ORNTIC

Seller Closing Disclosure Seller provided Closing Disclosure by

settlement agent at consummation.

Nothing prohibits settlement agent from creating a

separate form for seller purposes only

Copyright 2014 ORNTICCopyright 2014 ORNTIC

Owner’s Title Insurance Modifier

Requires inclusion of the word “Optional” after Owner’s Title Insurance on Loan Estimate

and Closing Disclosure

Only protection afforded consumer You are the professional if you suggest the

protection is not necessary you may have just self insured.

Copyright 2014 ORNTIC

Copyright 2014 ORNTIC

The Loan Estimate Form

Copyright 2014 ORNTIC

Loan Estimate Form – Page 1

Copyright 2014 ORNTIC

Loan Estimate Form – Page 2

Copyright 2014 ORNTIC

Copyright 2014 ORNTIC

The CLoSING DISCLOSURE

Copyright 2014 ORNTIC

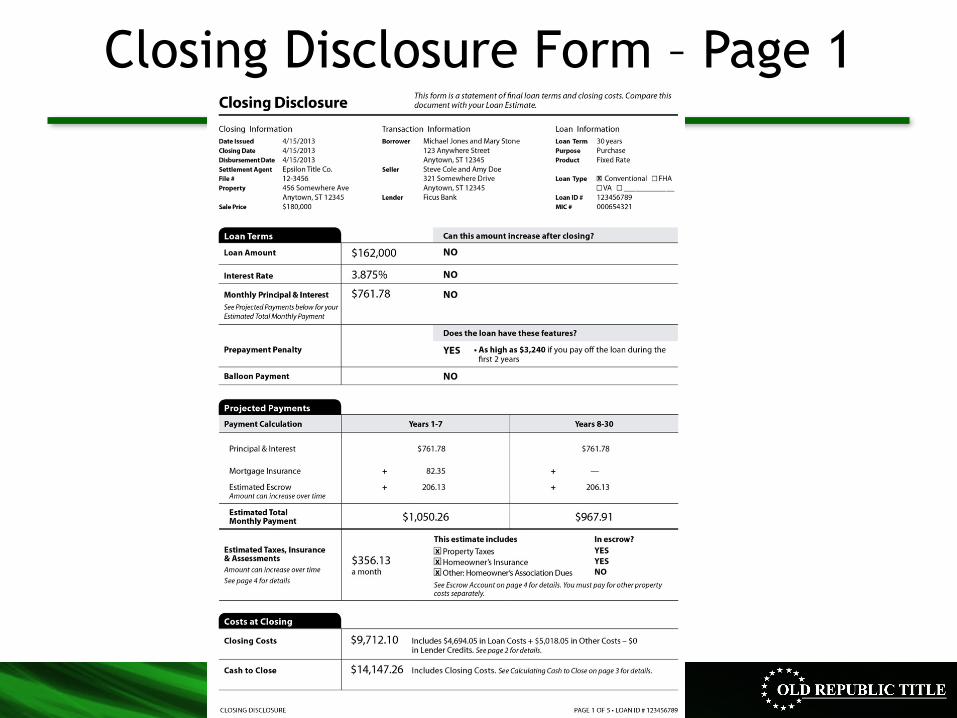

Closing Disclosure Form – Page 1

Copyright 2014 ORNTIC

Closing Disclosure Form – Page 2

Copyright 2014 ORNTIC

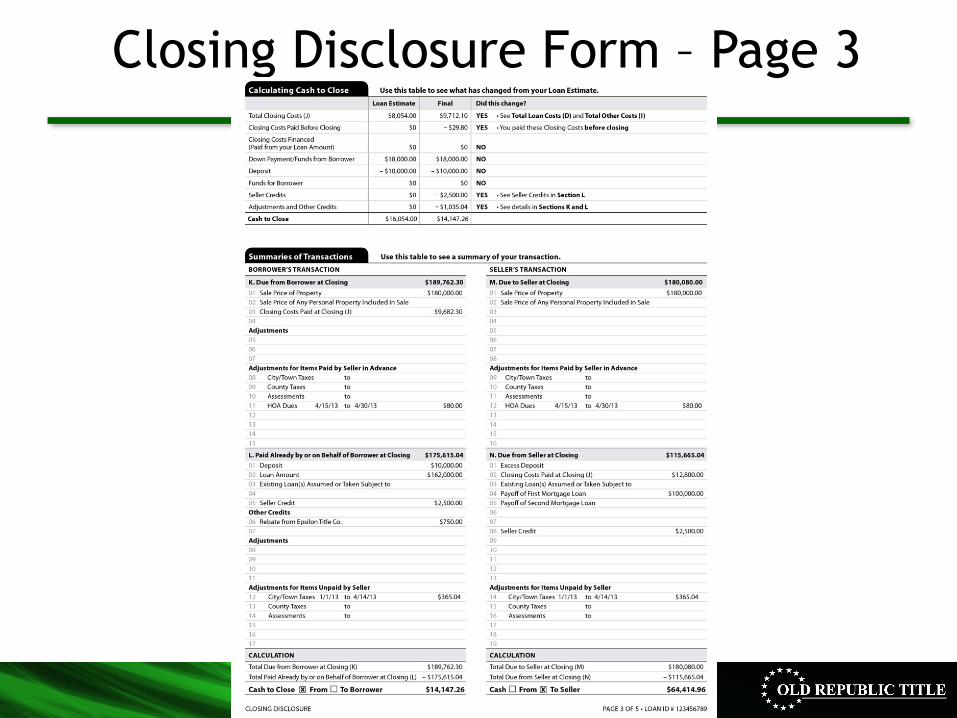

Closing Disclosure Form – Page 3

Copyright 2014 ORNTIC

Closing Disclosure Form – Page 5

Copyright 2014 ORNTIC

What you can start doing now

▪ Develop systems of communication with lenders ▪ Develop systems of communication with closing

company well in advance of closing ▪ Learn the forms ▪ Assure your title entities are preparing ▪ Review technology available to lenders ▪ Review change of circumstance triggers

Copyright 2014 ORNTICCopyright 2014 ORNTIC

THANK YOU! Jack O’Donohue, Esq. O’Donohue Law, LLC (978) 475-4896 [email protected]