centro mcs 34 - retail direct property · centro mcs 34 trust arsn 111 915 747 centro mcs 34 (new...

TRANSCRIPT

Responsible Entity: CPT Manager Limited

ABN 37 054 494 307 AFSL 238 454

December 2004

Centro MCS 34 Product Disclosure Statement & Prospectus

Centro MCS 34 Trust ARSN 111 915 747 Centro MCS 34 (New Zealand) Trust ARSN 109 043 674

Lismore CentralNew South Wales

Pirie PlazaSouth Australia

Coles MorwellVictoria

Pinelands PlazaQueensland

Woodcroft PlazaNew South Wales

Emerald VillageQueensland

Emerald Market Plaza Queensland

Centro MCS Manager Limited ABN 69 051 908 984

CPT Manager Limited Responsible Entity

ABN 37 054 494 307

Centro M

CS 34

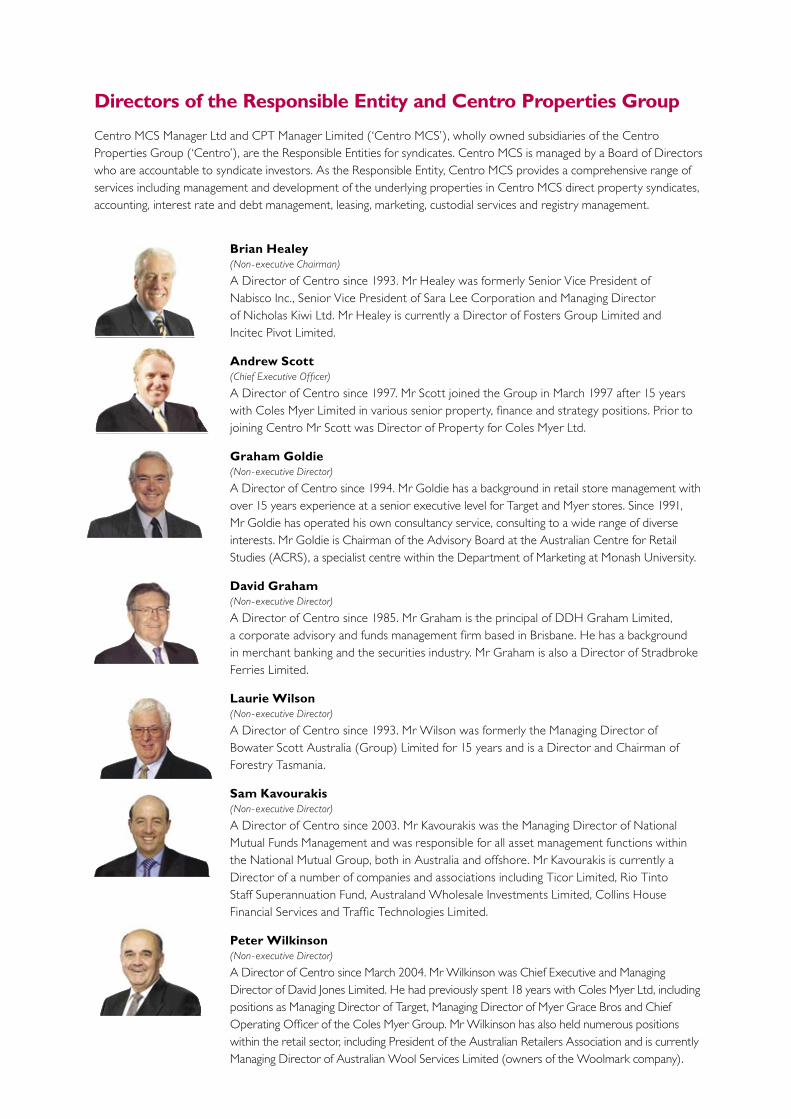

Brian Healey (Non-executive Chairman)

A Director of Centro since 1993. Mr Healey was formerly Senior Vice President of Nabisco Inc., Senior Vice President of Sara Lee Corporation and Managing Director of Nicholas Kiwi Ltd. Mr Healey is currently a Director of Fosters Group Limited and Incitec Pivot Limited.

Andrew Scott (Chief Executive Officer)

A Director of Centro since 1997. Mr Scott joined the Group in March 1997 after 15 years with Coles Myer Limited in various senior property, finance and strategy positions. Prior to joining Centro Mr Scott was Director of Property for Coles Myer Ltd.

Graham Goldie (Non-executive Director)

A Director of Centro since 1994. Mr Goldie has a background in retail store management with over 15 years experience at a senior executive level for Target and Myer stores. Since 1991, Mr Goldie has operated his own consultancy service, consulting to a wide range of diverse interests. Mr Goldie is Chairman of the Advisory Board at the Australian Centre for Retail Studies (ACRS), a specialist centre within the Department of Marketing at Monash University.

David Graham (Non-executive Director)

A Director of Centro since 1985. Mr Graham is the principal of DDH Graham Limited, a corporate advisory and funds management firm based in Brisbane. He has a background in merchant banking and the securities industry. Mr Graham is also a Director of Stradbroke Ferries Limited.

Laurie Wilson(Non-executive Director)

A Director of Centro since 1993. Mr Wilson was formerly the Managing Director of Bowater Scott Australia (Group) Limited for 15 years and is a Director and Chairman of Forestry Tasmania.

Sam Kavourakis (Non-executive Director)

A Director of Centro since 2003. Mr Kavourakis was the Managing Director of National Mutual Funds Management and was responsible for all asset management functions within the National Mutual Group, both in Australia and offshore. Mr Kavourakis is currently a Director of a number of companies and associations including Ticor Limited, Rio Tinto Staff Superannuation Fund, Australand Wholesale Investments Limited, Collins House Financial Services and Traffic Technologies Limited.

Peter Wilkinson (Non-executive Director)

A Director of Centro since March 2004. Mr Wilkinson was Chief Executive and Managing Director of David Jones Limited. He had previously spent 18 years with Coles Myer Ltd, including positions as Managing Director of Target, Managing Director of Myer Grace Bros and Chief Operating Officer of the Coles Myer Group. Mr Wilkinson has also held numerous positions within the retail sector, including President of the Australian Retailers Association and is currently Managing Director of Australian Wool Services Limited (owners of the Woolmark company).

Directors of the Responsible Entity and Centro Properties Group

Centro MCS Manager Ltd and CPT Manager Limited (‘Centro MCS’), wholly owned subsidiaries of the Centro Properties Group (‘Centro’), are the Responsible Entities for syndicates. Centro MCS is managed by a Board of Directors who are accountable to syndicate investors. As the Responsible Entity, Centro MCS provides a comprehensive range of services including management and development of the underlying properties in Centro MCS direct property syndicates, accounting, interest rate and debt management, leasing, marketing, custodial services and registry management.

CENTRO MCS SYNDICATES CENTRO MCS DIRECTORYResponsible EntityCPT Manager LimitedABN 37 054 494 307Centro MCS Manager LimitedABN 69 051 908 984

Board of DirectorsBrian Healey (Chairman)Andrew Scott (Chief Executive Officer)Graham GoldieDavid GrahamLaurie WilsonSam KavourakisPeter Wilkinson

Company SecretaryDanielle Rowe

Registered OfficeCorporate Offices, 3rd FloorCentro The Glen235 Springvale RoadGlen Waverley Victoria 3150Telephone +61 3 8847 0000Facsimile +61 3 9886 1234

For more information on this offer please contact:Investor ServicesGeneral Enquiries Telephone 1800 802 400Telephone +61 3 8847 0000 (International)Facsimile +61 3 9886 1234Email [email protected]

Registry & Holdings Enquiries for Centro MCS 34Computershare Investor Services Pty LtdGPO Box 2975EEMelbourne Victoria 3001Telephone 1300 555 079 (Australia)

0800 540 172 (New Zealand)+61 3 9415 4000 (International)

Facsimile +61 3 9473 2500www.computershare.com.au

Directory

Syndicate Prefix Syndicate Also Known As

Centro MCS 2 MCS2 John Martin’s Car Park & Retail Plaza JA

Centro MCS 3 MCS3 Nepean Square Shopping Centre JA

Centro MCS 4 MCS4 The Hills Shopping Centre JA

Centro MCS 5 MCS5 Coles & Kmart Centres JA

Centro MCS 6 MCS6 Melbourne-Brisbane Retail & Bulky Goods JA

Centro MCS 8 MCS8 1998 Retail Portfolio JA

Centro MCS 9 MCS9 1998 National Retail Portfolio DPI & UT

Centro MCS 10 MCS10 1999 Retail No.1 Portfolio DPI & UT

Centro MCS 11 MCS11 Paradise Centre DPI & UT

Centro MCS 12 MCS12 2000 Retail No.2 Portfolio DPI & UT

Centro MCS 14 MCS14 DPI & UT

Centro MCS 15 MCS15 DPI & UT

Centro MCS 16 MCS16 (Institutional/NZ) DPI & UT

Centro MCS 17 MCS17 DPI & UT

Centro MCS 18 MCS18 DPI & UT

Centro MCS 19 UT MCS19 Trust

Centro MCS 19 NZ/I MCS19 (NZ/Institutional) DPI

Centro MCS 20 MCS20 (International No.1) Trust

Centro MCS 21 Centro Property Syndicate No.1 (Roselands Syndicate)

Centro MCS 22 Centro Property Syndicate No.2 (Kidman Park Syndicate)

Centro MCS 23 Centro Property Syndicate No.3 (Prime Syndicate No.3)

Centro MCS 24 Centro Property Syndicate No.4 (Lake Macquarie Syndicate)

Centro MCS 25 Centro Property Syndicate No.5

Centro MCS 26 Centro Property Syndicate No.6

Centro MCS 27 Centro Property Syndicate No.7 (Sunshine MarketPlace Syndicate)

Centro MCS 28 Centro Property Syndicate No.8

Centro MCS 32 Centro MCS 32 – International No.2

Centro MCS 33 Centro MCS 33

Contents

Important Information 2

Chairman’s Letter 3

Investment at a Glance 4

Section 1 Key Benefits, Features and Risks 6

Section 2 Structure of this Investment 12

Section 3 Why Invest in Direct Property? 16

Section 4 The Properties 20

Section 5 Management 38

Section 6 Financial Information 42

Section 7 New Zealand Investors 52

Section 8 Keeping You Informed 60

Section 9 Additional Information and Fees Disclosure 62

Section 10 Glossary 74

Section 11 How to Invest 78

Application Forms 81

Directory Inside Back Cover

2 3

Important Information

This PDS was lodged with ASIC on 23 December 2004. ASIC takes no responsibility for the contents of this PDS or the merits of the investment to which this PDS relates.

This PDS is issued in accordance with the provisions of the Corporations Act 2001 by CPT Manager Limited a wholly owned subsidiary of Centro as Responsible Entity of the Syndicate and the NZ Trust. In relation to the Exit Mechanism this PDS is also issued by Centro.

Neither the Manager, Centro or their associates or Directors guarantees the success of the Syndicate or the NZ Trust, the repayment of capital or any particular rate of capital or income return. An investment in the Syndicate or the NZ Trust is subject to investment and other risks.

This PDS contains important information and Investors should read it carefully. In preparing this document, the Manager did not take into account the investment objectives, financial situation or particular needs of any particular person. Before making an investment decision, Investors should consider whether the investment is appropriate to their needs, objectives and circumstances. Investors are encouraged to obtain independent financial advice before making an investment decision.

Applications for Units or Stapled Securities can only be submitted on the relevant original Application Form attached to and forming part of, or accompanying, this PDS or accompanied by an electronic version of this PDS. The Corporations Act 2001 prohibits any person from passing on to another person the Application Form unless it is accompanied by or attached to a paper copy of this PDS or the complete and unadulterated electronic version of this PDS.

Applications under this PDS will not be processed by the Manager until after the expiry of the exposure period. The exposure period is seven days from the date of lodgement of the PDS with ASIC which may be extended by ASIC to a period of 14 days. No preference will be conferred on persons who lodge applications before expiry of the exposure period.

The Manager authorises this PDS for use by persons investing through an ‘Administration Service’ and professional and institutional investors. When investing through an Administration Service, this PDS should be read in conjunction with the current disclosure statement for the relevant Administration Service and applications must be made on the application form supplied by the Administration Service operator. The current disclosure document for the relevant Administration Service may be obtained from the relevant Administration Service operator.

The offer to which the electronic version of this PDS relates is only available to Australian and New Zealand residents receiving the electronic version of this PDS in Australia and New Zealand. The electronic copy of this PDS is available online at www.centro.com.au/centromcs. Paper copies of this PDS, including the accompanying Application Forms, are available free of charge by telephoning 1800 802 400 (Australia), +61 3 8847 0000 (International), or emailing [email protected]

This PDS does not constitute an offer or invitation in any place in which, or to any person to whom, it would not be lawful to make such an offer or invitation. No action has been taken to register or qualify the Units, the Stapled Securities or the Offer, or to otherwise permit a public offering of Units or Stapled Securities, in any jurisdiction outside Australia and New Zealand. The distribution of this PDS outside Australia and New Zealand may be restricted by law and persons who come into possession of this PDS outside Australia and New Zealand should seek advice on and observe such restrictions. Any failure to comply with these restrictions may constitute a violation of applicable securities laws.

You should read the whole of this PDS, and obtain your own professional advice.

CPT Manager Limited ABN 37 054 494 307 (‘the Manager’) brings you the opportunity to invest in the Centro MCS 34 Syndicate (‘the Syndicate’) or for New Zealand residents, Centro MCS 34 (New Zealand) (‘NZ Trust’) on the terms of this Product Disclosure Statement and Prospectus (‘PDS’).

At commencement of this Syndicate the role of Manager will be held by CPT Manager Limited, a wholly owned subsidiary of Centro, whose AFSL permits it to be the Responsible Entity of investments such as this. Centro MCS Manager Limited ABN 69 051 908 984, also a wholly owned subsidiary of Centro, has made an application to the Australian Securities and Investment Commission (‘ASIC’) for variation of its Australian Financial Services Licence (‘AFSL’) and when that variation has been granted, CPT Manager Limited will retire and Centro MCS Manager Limited will become Responsible Entity. From that time, this PDS will be deemed to have been issued by Centro MCS Manager Limited. The change of Manager will have no impact on Investors.

This PDS is dated 23 December 2004. The Offer under this PDS is available to Australian and New Zealand residents receiving the PDS within Australia and New Zealand and nothing in this PDS should be taken to indicate that the Offer is available to persons in any jurisdiction outside Australia and New Zealand. No application for Stapled Securities in the NZ Trust pursuant to this PDS will be accepted more than 13 months after the date of issue of this PDS.

If you wish to invest in the Syndicate or the NZ Trust, you must complete the relevant Application Form which accompanies this PDS.

Centro MCS 34Centro MCS 34 Trust ARSN 111 915 747

Centro MCS 34 (New Zealand) Trust ARSN 109 043 674

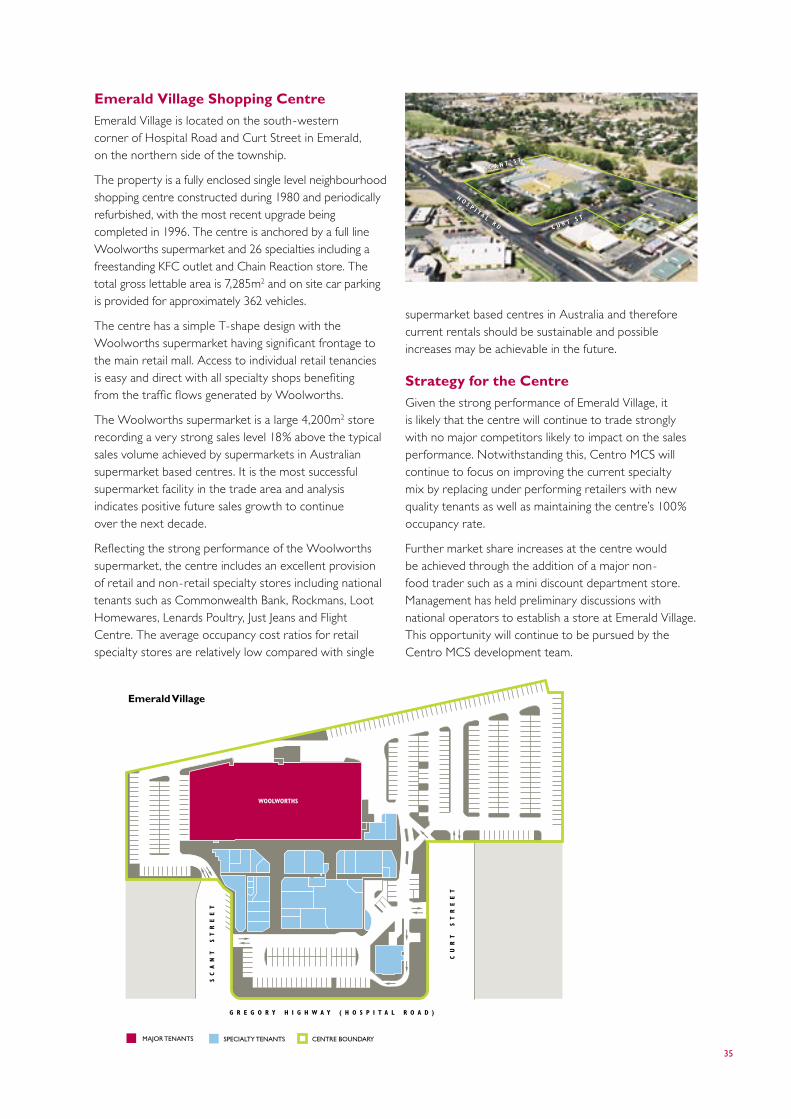

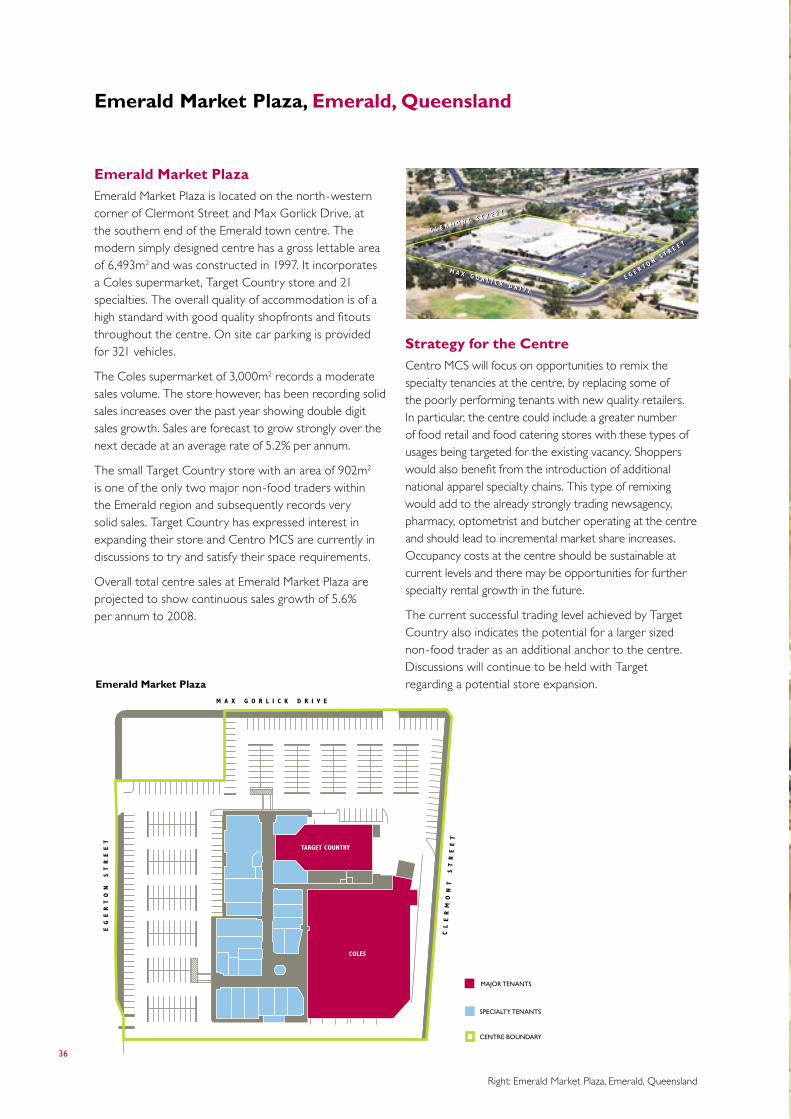

Emerald Market Plaza, Emerald, Queensland

2 3

CPT Manager LimitedResponsible Entity

ABN 37 054 494 307

Centro MCS Manager Limited ABN 69 051 908 984

Corporate Offices 3rd FloorCentro The Glen235 Springvale RoadGlen Waverley Victoria 3150

Telephone (03) 8847 0000Facsimile (03) 9886 1234Email [email protected] www.centro.com.au

Chairman’s Letter

22 December 2004

Dear Investor

Centro MCS are pleased to offer you an exciting opportunity to become an Investor in Centro MCS 34, an unlisted property syndicate. This investment opportunity offers Investors significant diversification benefits with exposure to seven neighbourhood shopping centres located in four states and over 170 tenants, including national anchor tenants such as Coles, Woolworths and Kmart.

Investors should also benefit from exposure to retail property which has outperformed other sectors of the property market as well as all other major asset classes over a 19 year period, delivering an average total return of 13.3% per annum, with the lowest risk rating of any comparable asset class (see page 18).

Centro MCS has a proud history of delivering value growth to investors and believes that capital growth opportunities may be realised through value adding strategies identified across the Syndicate property portfolio.

The Syndicate will have an initial maximum term of seven years after which time Investors will have the opportunity, guaranteed by Centro, to exit their investment at the Current Unit Value at that time. The average distribution yield for the first three and a half years is forecast at 7.90% per annum with significant tax advantages. Further distribution growth is then expected as trust income continues to grow.

Centro MCS is Australia’s largest direct property syndicate manager and currently manages 30 unlisted retail property syndicates valued at over $2.8 billion, with interests in 91 shopping centres across Australia, New Zealand and California (USA).

Centro MCS direct property syndicates have an impressive performance record. An equal investment in every Centro MCS direct property syndicate (managed for more than one year) would have earned a total return of 17.0% for the year ended 30 June 2004. Over the long term, an equal investment in every Centro MCS direct property syndicate since 1993 (being the date of inception of Centro MCS) to 30 June 2004 would have earned 18.3% per annum.* Of this return 11.2% per annum was attributable to income distributions and 7.1% per annum to capital growth.

Centro, or entities it manages or controls, intends to maintain an investment of 25% to 50% in the Syndicate. The Manager believes that Centro’s significant co-investment in the Syndicate benefits Investors by aligning Centro’s interests with the interests of Investors.

We strongly recommend that you read this document carefully. If you have any questions, please contact your financial adviser or Centro MCS Investor Services on 1800 802 400 (Australia) or +61 3 8847 0000 (International). We encourage you to participate in this opportunity and lodge your Application Form early.

Yours sincerely

Brian HealeyChairman

*Investors should note that past performance is not an indication of future performance.

4 5

Investment at a Glance

OVERVIEW

The Offer 37,884,293 ordinary Units at an issue price of $1.00 per Unit and 5,000,000 Equity Notes at an issue price of $1.00 per Equity Note.

Prized Retail Sector Retail property has outperformed all other asset classes including other sectors of the property market, with the lowest risk rating of any comparable asset class. Refer to Section 3 for further details.

Diversification Benefits An investment providing diversification benefits of seven properties and over 170 tenants spread across four states. Refer to Section 4 for further details.

Investment Objective To provide Investors with direct property exposure with strong and secure tax-advantaged returns, through an investment in seven quality retail properties.

Capital Growth Potential Centro MCS has a proven value adding track record and believes that capital growth opportunities should be available. Refer to Section 1.2 for further details.

Proven Manager Centro MCS currently manages 30 property syndicates and is Australia’s largest property syndicator with a proven track record of managing shopping centres and delivering strong total returns to Investors. Refer to Section 5 for further details.

Structure of Investment This Syndicate is a unit trust. Complying and self-managed superannuation funds may invest in the Syndicate. Refer to Section 2 for further details. NZ Investors refer to Section 7.

Minimum Investment AUD$10,000 with increments of AUD$1,000. Refer to Section 2 for further details. NZ Investors refer to Section 7.

Interest Hedging The interest rates on the Syndicate loan have been fully hedged for the seven year Syndicate term. Refer to Section 6.9 for further details.

Term of Investment The initial investment term is for a maximum period of seven years to 31 December 2011. Refer to Section 1 for further details.

Quarterly Distributions The first distribution payment will be for the period to 31 March 2005. Thereafter distributions will be paid quarterly. Refer to Section 2.4 for further details.

Centro Co-Investment Centro (or entities it manages or controls) intends to maintain an investment of 25% to 50% of the equity in the Syndicate of which approximately $5 million will be invested in the form of Equity Notes. Refer to Section 2.9 for further details.

Exit Mechanism Centro has agreed to provide an Exit Mechanism at the end of the Syndicate term. Refer to Section 2.6 for further details.

How to Invest Complete the relevant Application Form at the back of this PDS. Refer to Section 11 for further details.

4 5

ESTIMATED RETURNS TO INVESTORS

Period Ending 30 June 2005(1) 2006 2007 2008

SYNDICATE RETURNS

Forecast Annual Cash Distribution 7.70% 7.80% 7.95% 8.05%

Forecast Tax-Advantaged 100.00% 100.00% 88.00% 74.00%

Forecast Equivalent Pre-Tax Yield (based on a 48.5% tax payer)(2)

14.95% 15.15% 14.54% 13.64%

(1) Part year from 1 January 2005 to 30 June 2005.

(2) This calculation does not take into account potential capital gains or losses on the investment or tax resulting from reductions in the capital gains tax cost base.

Full details of Syndicate returns and tax-advantaged calculations are set out in Section 6. For risk factors and key assumptions please refer to Section 1.4 and Section 6.4 respectively. Investors in the NZ Trust, please refer to Section 7 for estimated returns.

THE PROPERTIES AT A GLANCEAn investment in seven convenience based neighbourhood shopping centres.

Centre State Type Value ($m)(1)

Ownership Proportion

% of Portfolio Majors

Pinelands Plaza QLD Neighbourhood $25.6 100% 25.1% Coles

Woodcroft Plaza NSW Neighbourhood $18.5 100% 18.1% Coles

Lismore Central NSW Neighbourhood $17.5 100% 17.2% Woolworths

Pirie Plaza SA Neighbourhood $13.0 100% 12.7% Coles, Kmart

Coles Morwell VIC Neighbourhood $11.1 100% 10.9% Coles

Emerald Village QLD Neighbourhood $9.9 50% 9.6% Woolworths

Emerald Market Plaza QLD Neighbourhood $6.5 50% 6.4% Coles

TOTAL $102.1 100%

(1) These values are based on the independent valuations excluding normal acquisition costs as summarised in Section 4.3.

LOCATION OF PROPERTIES

Investment at a Glance

Perth

WesternAustralia

NorthernTerritory

SouthAustralia

Queensland

New South Wales

AustralianCapital

Territory

Victoria

Tasmania

Adelaide

Melbourne

Hobart

CanberraSydney

Brisbane

Darwin

PIRIE

EMERALD MARKET

MORWELL

LISMORE

WOODCROFT

PINELANDS

EMERALD VILLAGE

6 7

Section 1 Key Benefits, Features and RisksColes Morwell, Morwell, Victoria

6 7

Section 1 Key Benefits, Features and Risks

1.1 INVESTMENT OBJECTIVEThe objective of this investment is to provide Investors with strong and secure tax-advantaged returns for the term of the Syndicate by investing in a diverse portfolio of Australian shopping centres.

Unless otherwise stated this PDS analyses the investment from the point of view of an Investor in the Syndicate. Those Investors who wish to invest via the NZ Trust should also read Section 7 as applicable, for details of the differences that will apply to them.

1.2 KEY BENEFITSThe key benefits of this investment are:

Secure and Diversified Income

Nearly 45% of the property income in the first year is secured from Australia’s largest retailers – Coles Myer (26%) and Woolworths (17%). The portfolio of seven shopping centres, with a total value of over $100 million, spread across four states in Australia also provides significant geographic and economic diversification (see Section 4 for further details).

Strong Tax-Advantaged Returns

Syndicate forecast distributions average 7.90% per annum for the first three and a half years to 30 June 2008.

The returns from direct property are further improved significantly if Investors take into account the tax effectiveness of this investment. For example the Manager expects that 100% of the income for the year ending 30 June 2006 will not be taxable in Investors’ hands in that year. This means a taxpayer on the top marginal rate of 48.5% would need to earn 15.15% per annum from a fully taxable investment to receive the same net annual distribution as the Syndicate.

Diversification Through Direct Property

The Manager believes that direct property is an essential part of any balanced investment portfolio. It is the only major asset class that has historically tended to move in different cycles to the other main asset classes of shares and bonds. This means that by including direct property in an investment portfolio, Investors benefit from the reduced risk that comes with diversification (see Section 3.1 for further details).

Centro Ownership Knowledge

All of the Syndicate properties were previously owned and managed by Centro. The depth of internal knowledge and consistency of ongoing management will

ensure a smooth property transfer into the Syndicate (see Section 5 for further details including the rationale of why Centro is selling the properties to the Syndicate).

Established Performing Properties

Each shopping centre is well located in an established trade area and is anchored by soundly performing national tenants. All centres are anchored by either a Coles or Woolworths supermarket with Pirie Plaza also anchored by a Kmart discount department store (see Section 4 for further details).

Capital Growth Potential

Centro MCS has a proud history of delivering value growth to investors and believes that capital growth opportunities may be realised through value adding strategies identified across the property portfolio. These strategies include:

• Renegotiation of new leases for majors at Pinelands Plaza, Lismore Central and Pirie Plaza over the next two years. Due to Centro MCS’s strong relationship with both Coles and Woolworths, Centro MCS will seek to enter into new long term leases at competitive rentals. Once leases are finalised, the improved lease expiry profile should assist in strengthening the property valuations;

• Potential expansion at Emerald Village to introduce a mini discount department store. Centro MCS is currently holding preliminary discussions with national operators;

• Acquisition of an adjoining tenanted property to Lismore Central. This excellent opportunity is underpinned by a strong long term lease and provides long term expansion potential;

• Leasing existing vacancies across the portfolio and tenancy remixing to improve the centre incomes. The Centro MCS leasing team has established strong relationships with national retailers and experienced leasing executives are located at all Centro state offices;

• Ongoing refurbishment opportunities to continually improve the presentation and customer facilities at the centres. Appropriate capital allowances have been made within the financial forecasts for this purpose.

Notwithstanding the above, the nature of retail property leases generally provide for annual rental increases. In addition some tenant rentals are tied to sales and as sales rise due to inflation or improved store performance rentals correspondingly increase. Frequently as rents increase the value of the property also goes up.

8 9

Section 1 Key Benefits, Features and Risks

Lower Transactional Costs

The structure of this sale and purchase transaction has enabled the Syndicate to save significant up front costs. Naturally a lower level of up front costs also enhances the potential for capital gains on the investment.

Non-Recourse Fully Hedged Finance

Borrowings for the Syndicate and the NZ Trust will be non-recourse to Investors. That means Investors are not at risk for any more than the equity subscribed by them on application plus any undistributed income. To reduce the interest rate exposure and further minimise risk, the Syndicate debt has fully hedged the Syndicate debt, fixing the rate for the total Syndicate term of seven years (see Section 6.9 for further details).

Prized Retail Sector

Retail property has outperformed all other asset classes including other sectors of the property market, as well as Listed Property Trusts (‘LPTs’). It has delivered an average total return of 13.3% per annum over the last 19 years, and importantly, has delivered this performance with the lowest risk rating of any comparable asset class (see Section 3.2 for further details).

Proven Manager with a Successful Track Record

Centro MCS is a proven and skilled manager of shopping centres with an impressive track record. Centro MCS is Australia’s largest direct property syndicate manager and currently has more than $2.8 billion of assets under management (see Section 5 for further details).

1.3 KEY FEATURES The key features of this investment are:

The Responsible Entity

The Responsible Entity of the Syndicate and the NZ Trust and the Issuer of this PDS is CPT Manager Limited (‘the Manager’), a wholly owned subsidiary of Centro (see Section 5). However, Centro MCS Manager Ltd has made an application to ASIC for variation of its AFSL to permit it to be the Responsible Entity of investments such as this, and when that variation has been granted, CPT Manager Limited will retire and Centro MCS Manager Ltd will become the Responsible Entity for both the Syndicate and the NZ Trust. CPT Manager Limited has obtained relief from ASIC to enable this to occur (see Section 5.6 for further details).

The Offer

The Syndicate will issue Australian Investors with units at an issue price of AUD$1.00 per Unit (‘Unit’).

The NZ Trust will participate in the Syndicate Offer by acquiring ordinary units and issue to NZ Investors Stapled Securities, comprising three ordinary units in the NZ Trust and two fully subordinated convertible unsecured notes (‘Unsecured Notes’) issued by the NZ Trust, permanently stapled together (‘Stapled Securities’) at an issue price of AUD$5.00 per Stapled Security (NZ Investors should see Section 7 for further details) .

How to Invest

Investors are requested to complete the relevant Application Form at the back of this PDS (see Section 11 for further details).

Minimum Investment

AUD$10,000 with increments of AUD$1,000. Refer to Section 2 for further details. NZ Investors should see Section 7.

Term of Investment

The initial term of this investment is expected to be for a maximum of seven years and a minimum of five years.

Exit Mechanism

Centro has provided an exit mechanism at the end of the Syndicate term (i.e. 31 December 2011) ensuring liquidity and enabling Investors to exit their investment at the Current Unit Value at that time (see Section 2.6 for further details).

Structure of Investment

The Syndicate is a unit trust. Complying and self-managed superannuation funds may participate in the Syndicate Offer (see Section 2 for Syndicate Investors and Section 7 for New Zealand Investors).

Fees

The fees payable in relation to this investment are set out and explained to Investors in Section 9.5. NZ Investors should also see Section 7.6.

Allotment

Units will be issued progressively (usually within five business days of acceptance of applications) and will participate in distributions on a daily pro-rata basis from the date of issue for the respective quarter.

8 9

Section 1 Key Benefits, Features and Risks

Distributions

The first distribution to be paid will be for the period to 31 March 2005. Thereafter distributions will be paid quarterly. Investors who apply prior to 1 January 2005 will receive a fixed, pro-rata distribution at the rate as forecast for the period to 30 June 2005 from the date of allotment of the application (usually within five business days of receipt of the application. See Section 2.4 for further details).

Flexible Trust Structure

The Syndicate structure has been created to allow flexibility in its ongoing management and to enable the Syndicate to take advantage of strategic opportunities that arise. The Manager has the power under its constitution to acquire adjacent or related properties for the Syndicate if they become available, which will protect Syndicate properties from development threats. It will also allow those properties to be expanded if this is considered desirable for the Syndicate.

For the same reasons the Manager may sell Syndicate properties if it considers this to be in the best interests of Investors. Proceeds from such a sale will be used to retire debt or returned to Investors or a combination of both. The Syndicate structure also provides for a merger in the future with other Centro MCS Syndicates, provided that an independent expert’s report concludes that this will be in the best interests of Investors.

Centro Co-Investment

Centro (or entities it manages or controls) intends to maintain an investment of 25% to 50% of the equity in the Syndicate of which approximately $5 million will be invested in the form of Equity Notes which share certain characteristics with ordinary equity held by Investors (see Section 2.9 for further details). The Manager believes that Centro’s significant co-investment in the Syndicate benefits Investors by aligning Centro’s interests with the interests of Investors.

1.4 RISK FACTORSAs with most investments, the future performance of the Syndicate can be influenced by a number of factors which are outside the control of the Manager. The level of future distributions, the value of the Syndicate properties and the value of Investors’ interests may be influenced by any of these risk factors, which include, without limitation, the following:

Property Associated CostsPurchasing property generally carries with it significant acquisition costs. These include stamp duties, legal fees on acquisition and due diligence costs (to ensure that the property is sound and the income stream upon which a purchase has been made is soundly based). Fees on sale typically include agency fees, advertising and legal expenses and in the case of New South Wales properties a potential vendor tax liability.

This means that to preserve the capital invested in a property, the property must generally be sold at a price which is considerably more than the price at which it was purchased. This risk can be managed or offset by:

• Taking into consideration the cyclical nature of the property market when concluding the investment;

• Allowing a longer time frame for the investment. This spreads the acquisition costs over a longer period of time and reduces the amount of capital growth that needs to be achieved each year; and

• By adding value to the investment through skilled management.

The structure of the Syndicate purchase transaction has saved significant up-front property associated costs, therefore reducing the quantum of this risk factor.

Property MarketAn investment in the Syndicate should be viewed as a medium to long term investment. Property values can fall as well as rise, leading to capital losses or capital gains. There is no certainty as to the state of the Australian property market throughout the term of the Syndicate. This, of course, is a consideration when investing in any asset class.

General Risks of Retail PropertyThere are a number of risks associated with an investment in retail property. These include, without limitation:

• The level of tenancy vacancies may fluctuate with market forces;

• A downturn in the economy;

• A downturn in the value of property, or in the property market in general;

• Interest rate fluctuations outside the fixed interest rates assumed in the Syndicate’s forecast;

• Adverse consequences of amendments to statutes and regulations affecting the Syndicate including changes in the tax regime;

10 11

• Pricing or competition policies of any competing properties or tenants;

• Increased competition from new or existing competing property;

• Changes in retail turnover and the consequential effect upon rental levels; and

• Longer term changes in consumer shopping habits.

Specific Tenancy Risks Property income depends upon tenants continuing to operate profitably and abiding by the terms and conditions of their tenancy arrangements. The ability to lease or re-lease to tenants upon expiry of their current leases, and the rent achieved, will depend upon prevailing market conditions at the relevant time, and these may be affected by economic conditions, competitive forces or other factors.

The most significant rental risk to the Syndicate is the risk of an anchor tenant defaulting on its rental obligations or vacating the centre at the expiration of the lease term. A lease expiry also provides an opportunity to renegotiate the lease on more favourable commercial terms.

Coles Myer and Woolworths represent the anchor tenants and are well established Australian retailers listed on the ASX. Both retailers are currently pursuing business growth opportunities resulting in the nationwide establishment of a number of new supermarkets and discount department stores in recent years.

Within the Syndicate, leases to Coles and Woolworths are due to expire within the next two years at Pinelands Plaza, Lismore Central and Pirie Plaza.

The leases of the Coles supermarket and Kmart at Pirie Plaza are due to expire in September 2005. Both leases contain an option to renew for a further term of five years at market rental. The Kmart is currently trading well above the Australian average for discount department stores and Coles’ sales level is substantial for a supermarket in a regional location. Both Coles and Kmart have indicated to Centro MCS that they wish to remain at the centre.

The Woolworths lease at Lismore Central is due to expire in December 2005. This lease also contains a five year option to market rental. Woolworths anchors this centre very strongly with the current turnover over 30% above the average for supermarkets in single supermarket centres. Woolworths have indicated they will commence negotiations closer to their lease expiry in late 2005.

The Coles lease at Pinelands Plaza expires in August 2006. Centro MCS is currently negotiating commercial terms with Coles who have expressed their intention to enter into a new lease. This supermarket has a solid sales performance above the average for major supermarkets across Australia.

Centro MCS believes that all of the major tenants will renew their leases at expiry. There can be no guarantee however, that any leases will be renewed or that the rent achieved will be in line with the Syndicate forecasts.

CompetitionA change in the competitive environment can impact on the trading performance of a shopping centre.

At Lismore Central an expansion is planned at the competing Lismore Shopping Square located approximately one kilometre east of Lismore Central. This development will add a new Big W and Woolworths supermarket from late 2005. The competitive impact is expected to progressively reduce the very strong sales of the Woolworths supermarket at Lismore Central during 2006 and 2007 to a level closer to the average for single supermarket based centres. Following this reduction, sales growth is again anticipated. The financial forecasts, the property valuation and the purchase price have accounted for this impact. The vendor has also provided additional security of $100,000 if required to maintain forecast distributions for the year ending 30 June 2007.

Capital ExpenditureThe need for unforeseen capital expenditure over the forecast period and the way in which the Syndicate funds this expenditure may also have an impact on the financial forecasts in this PDS. As part of Centro MCS’s management approach, an in house team of highly experienced and skilled fund and property managers will seek to minimise unforeseen capital expenditure as part of the property management process and leasing review strategy.

Debt FundingThis is an investment in income producing retail property, whose acquisition is funded partly by invested funds (equity) and partly of borrowed funds (debt). When a property investment is geared (i.e. purchased with debt) the potential for gains and losses is greater. Gearing also has the effect that acquisition costs, charges and fees represent a higher percentage of the equity in the purchase than they would if there was no mortgage and the property was purchased entirely with equity.

Section 1 Key Benefits, Features and Risks

10 11

The Syndicate debt has been fully hedged for the seven year Syndicate term. If the Syndicate term is extended for a further term and the Syndicate’s debt needs to be refinanced, interest rates may well be higher. If they are, then returns to Investors could be affected accordingly. If interest rates rose substantially, then refinancing may not be possible. In such an event, the properties may have to be sold at short notice and in a market that may not be conducive to a quick sale.

As part of the Syndicate debt strategy, the Manager may take steps to manage this risk by further hedging interest rates beyond the scheduled expiry date of the Syndicate (i.e. 31 December 2011). If the Syndicate did not rollover or the properties were sold before the end of the Syndicate term, the Syndicate may incur hedging termination costs if interest rates have risen from the date they were hedged.

Details of borrowings are set out in Section 6.6 to 6.10. The lender has no obligation to roll over this funding at the end of the loan period and so there is no certainty that the borrowings will be able to be replaced as their terms expire. If there is a breach of conditions of the borrowings, the lender may enforce its security and, amongst other things, sell the properties.

Due Diligence and Use of ExpertsIn acquiring the properties, the Manager has engaged appropriate experts to investigate the environmental, operational, structural and legal aspects of each of the properties. The Manager believes that these investigations are appropriate and complete. However, despite such investigations, the Manager cannot guarantee the identification and mitigation of all risks associated with these properties.

InsuranceIn preparing the financial forecasts, the nature and cost of insurance has been based upon the best estimate of likely circumstances. However, various factors may influence premiums to a greater extent than those forecast, which may in turn have a negative impact on the net income.

LiquidityAn investment in the Syndicate should be considered illiquid as it is unlikely that there will be a secondary market for the Units. No Investor has the right to redeem Units during the Syndicate term. However, under the Exit Mechanism, Investors have the right to sell their investment at the end of the initial Syndicate term (i.e. 31 December 2011), based on the Current Unit Value at that time.

Exit MechanismThe Investors’ ‘put’ option under the Exit Mechanism described in Section 2.6 will cease to apply if the Manager (or another member of Centro) is no longer the Responsible Entity for the Syndicate. However, if this occurs, Centro will remain entitled to exercise its ‘call’ option and may require all Investors to sell some or all of their Units on the same basis as at the end of the initial term of the Syndicate (i.e. 31 December 2011).

Taxation The Syndicate currently enjoys significant tax-advantages as outlined in Section 6.5. However, as with all tax legislation, it is possible that the rules may change in the future.

The effect of taxation on Investors in the Syndicate is complex and the summary in Section 6.5 is general in nature and as the circumstances for each Investor may vary, Investors should seek professional taxation advice in relation to their own position.

Taxation implications for the NZ Trust are discussed in Section 7.5.

Other Risk Factors• Natural disasters and man made disasters may occur

which are beyond the control of the Manager; and

• Building and refurbishment works that occur at the Syndicate properties during the Syndicate term will be contracted to experienced consultants engaged by the Manager to ensure that the works are completed in accordance with specifications, on time and within budget. However, there are always risks attached to building works in the form of delays, cost overruns, changes to proposed tenancies and prospective tenancies and risks relating to the quality of work performed.

Section 1 Key Benefits, Features and Risks

12 13

Section 2 Structure of this InvestmentPinelands Plaza, Sunnybank Hills, Queensland

12 13

�����������������

������������������

������������������ �����������

���������������������

�������������������������

���������������

�������������

Centro MCS 34

Syndicate

�����������

��������������

��������������������������������

������������������������������

Section 2 Structure of this Investment

2.1 OVERVIEWThis PDS offers Investors the opportunity to invest in the Syndicate, an unlisted property trust that has acquired an interest in the following seven shopping centres in Australia:

• Pinelands Plaza, Sunnybank Hills, Queensland

• Woodcroft Plaza, Woodcroft, New South Wales

• Lismore Central, Lismore, New South Wales

• Pirie Plaza, Port Pirie, South Australia

• Coles Morwell, Morwell, Victoria

• Emerald Village, Emerald, Queensland (50% ownership interest)(1)

• Emerald Market Plaza, Emerald, Queensland (50% ownership interest)(1)

(1) The remaining 50% is owned by the Centro MCS 25 Syndicate.

2.2 SYNDICATE STRUCTUREThe structure of the Syndicate is shown in the diagram below.

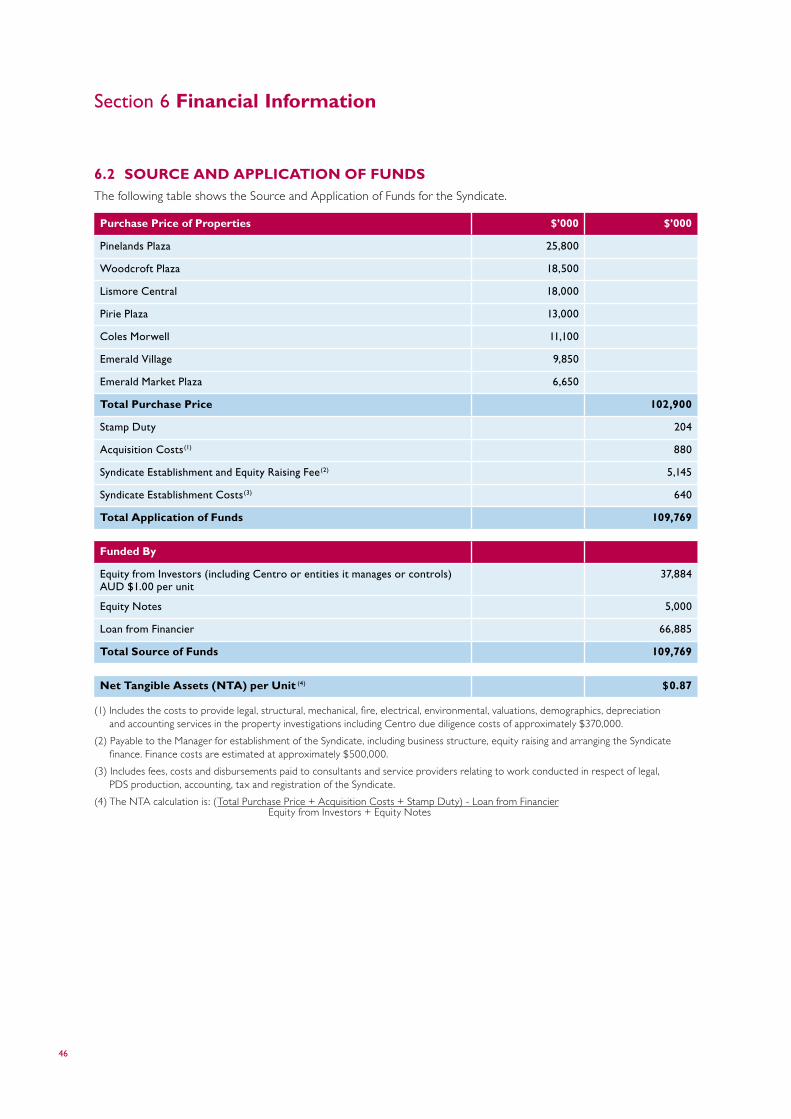

Total funding required by the Syndicate to acquire the properties and establish the Syndicate is approximately $109.8 million.

The Manager expects to arrange initial bank loan facilities (‘Loan’) for approximately $66.9 million to the Syndicate based on an initial loan to value ratio (‘LVR’) of approximately 65%. The Loan is secured on a non-recourse basis, (i.e., Investors are not at risk for any more than the equity subscribed by them on application plus any undistributed income).

In addition, operational capital and pre-leasing expenditure totalling $4.1 million has been forecast to be spent during the Syndicate’s initial seven year term and financed through borrowings (see Sections 6.6-6.10 for further details of the finance arrangements for the Syndicate).

The Syndicate is now seeking to raise the balance of approximately $42.9 million from Investors.

Centro (or entities it manages or controls) intends to maintain an investment of 25% to 50% of the equity in the Syndicate, of which approximately $5.0 million will be invested in the form of Equity Notes which share certain characteristics with ordinary equity held by Investors (see Section 2.9 for further details).

(1) The Syndicate holds its interest in this property through wholly owned subsidiary trusts.

(2) The Syndicate holds its interest in this property as a 300 year lease.

(3) The Syndicate has a 50% ownership interest in this property. The remaining 50% of this property is owned by the Centro MCS 25 Syndicate.

14 15

Section 2 Structure of this Investment

2.3 THE OFFERThe investment will be in the Syndicate, an unlisted property trust.

The Manager is offering approximately 37.9 million ordinary Units and 5.0 million Equity Notes in the Syndicate at the issue price of AUD$1.00 each.

This PDS will remain open to Investors subscribing for Units until the equity sought is fully subscribed. NZ Investors should see Section 7 for the structure of an investment in the NZ Trust. Applications for Stapled Securities from NZ Investors will be accepted until 13 months from the date of issue of this PDS.

As the properties have already been secured with funding provided by Centro, the Offer is not subject to receipt of any minimum level of applications. Investors are encouraged to apply early to avoid disappointment.

2.4 DISTRIBUTION POLICYThe forecast period commences at 1 January 2005 for the term of the Syndicate. The first distribution made to Investors will be for the period ending 31 March 2005. Investors who apply prior to 1 January 2005 will receive a fixed, pro-rata distribution at the rate as forecast for the period to 30 June 2005 from the date of allotment of the application (usually within five business days of receipt of the application).

Distributions will be made quarterly, as at the end of March, June, September and December, and will be paid to Investors within six weeks from the end of each distribution quarter.

Distributions will be based on the distributable income of the Syndicate and any additional return of capital as determined by the Manager.

2.5 SYNDICATE TERMINATION OR ROLLOVER

As Responsible Entity, it is the Manager’s intention to rollover (or extend) the Syndicate term at the end of the initial period of investment, provided that it is in the best interests of Investors at that time. Alternatively, the Manager may decide to restructure or terminate the Syndicate.

Details of any proposal to continue or restructure the Syndicate will be notified to Investors by no later than three months prior to the end of the Syndicate term. This will provide Investors who wish to exit the Syndicate sufficient opportunity to sell their Units to Centro via the Exit Mechanism.

2.6 EXIT MECHANISMCentro offers Investors the ability to exit their investment at the end of the initial term of the Syndicate (i.e. 31 December 2011) via the Exit Mechanism. This provides Investors with certainty in the planning of their financial affairs.

The Exit Mechanism works in the following way. At the end of the initial Syndicate term, Investors will have the right to sell (or ‘put’) their Units to Centro or its nominee at the Current Unit Value at that time. This value could be higher or lower than the issue price of the Units and will be based on an independent valuation of the properties as at the end of the Syndicate term. Centro, or its nominee(s), may choose, at Centro’s election, to pay for those Units with either cash, Centro Stapled Securities or a combination of both.

If Centro chooses to pay for the Units by issuing Centro Stapled Securities to Investors, those Centro Stapled Securities will be issued at a 0.5% discount to the weighted average ASX market price of all Centro Stapled Securities (adjusted for distribution differences) traded over the ten days prior to the date of issue of the Centro Stapled Securities, and application will be made for their quotation on the ASX within seven business days after the date of allotment or issue. The new Centro Stapled Securities will rank equally for distribution entitlements with existing Centro Stapled Securities then on issue.

If any Units are sold by Investors to Centro as outlined above, Centro may require that all Investors sell some or all of their Units on the same basis.

If Centro does not acquire some or all of the Units held by all Investors at the end of the Syndicate, Centro may decide that the Syndicate’s interest in the properties should be offered for sale on the open market. The net proceeds (after allowing for expenses) will be distributed to Investors in proportion to their Unitholdings.

Investors should note that an Investor’s ‘put’ option under the Exit Mechanism described above, will cease to apply if Centro MCS Manager Limited, CPT Manager Limited (or another member of Centro) ceases to be the Responsible Entity for the Syndicate. If this occurs, Centro will still remain entitled to require that all Investors sell some or all of their Units on the same basis at the end of the Syndicate term.

14 15

Section 2 Structure of this Investment

2.7 NO REDEMPTION OF UNITSThe Syndicate should be considered illiquid as it is unlikely that there will be a ready secondary market for the Syndicate’s Units. It should be noted that the Manager is not able to redeem Investors’ Units, except in so far as required in relation to the acquisition of Pirie Plaza. Refer to Sectio 9.13 for further details. Investors wishing to dispose of their Units should approach their financial adviser prior to approaching the Manager with a view to finding a buyer for the Units. Although the Manager has no obligation to buy or find a buyer, it may (subject to complying with applicable regulatory requirements) attempt to facilitate a sale, or may itself buy Units from Investors. In particular, where possible, the Manager seeks to assist the executors of deceased estates.

2.8 SALE OR TRANSFER OF UNITS DURING THE TERM OF THE SYNDICATE

Investors in the Syndicate must comply with the provisions of the Syndicate Constitution and the Corporations Act 2001 if they wish to transfer any of their Units during the term of the Syndicate. A transfer of Units must be in writing, signed by both the transferor and transferee before it is lodged with the Manager for registration.

The Manager is entitled to receive a fee in respect of administration costs incurred in transferring Units. This fee will be a maximum of 1% of the value of the interest transferred, with a minimum fee of $100. This fee does not apply to the Exit Mechanism.

2.9 EQUITY NOTESCentro (or entities it manages or controls) intends to maintain an investment of 25% to 50% in the Syndicate, of which approximately $5.0 million will be invested in the form of Equity Notes which share certain characteristics with ordinary equity held by Investors. The Manager believes that Centro’s significant co-investment in the Syndicate benefits Investors by aligning Centro’s interests with the interests of Investors.

The Equity Notes comprise a partly paid ordinary unit (paid up to one cent) (‘PPU’) and an unsecured subordinated debt obligation (‘DO’) owed by the Syndicate to the holder (being Centro or entities it manages or controls). The issue price of each Equity Note is $1.00, with one cent allocated to the PPU and the balance to the DO. The terms of issue of Equity Notes are set out on page 71.

Interest on the Equity Notes will accrue and be paid on the same basis as Units. However, Equity Notes will be entitled to a margin of 0.30% per annum above the annual cash distribution yield paid to Investors.

Centro (or entities it manages or controls) intends to maintain its holding of Equity Notes for the term of the Syndicate.

As the holders of the DOs do not enjoy the same tax-advantaged position, the issuing of Equity Notes provides Investors who have subscribed for ordinary equity with the benefit of a higher tax-advantaged component of income distribution than would otherwise apply.

Emerald Village, Emerald, Queensland

Woodcroft Plaza, Woodcroft, New South Wales

� � � � � � � � � � � � � �

� � � � � � � � � � � � � �

� � � � � � � � � � � � � � �

� � � � � � � � � � � � � � �

� � � � � � � � � � � � � � � � �

� � � � � � � � � � � � � � � � �

16 17

Section 3 Why Invest in Direct Property?Emerald Market Plaza, Emerald, Queensland

16 17

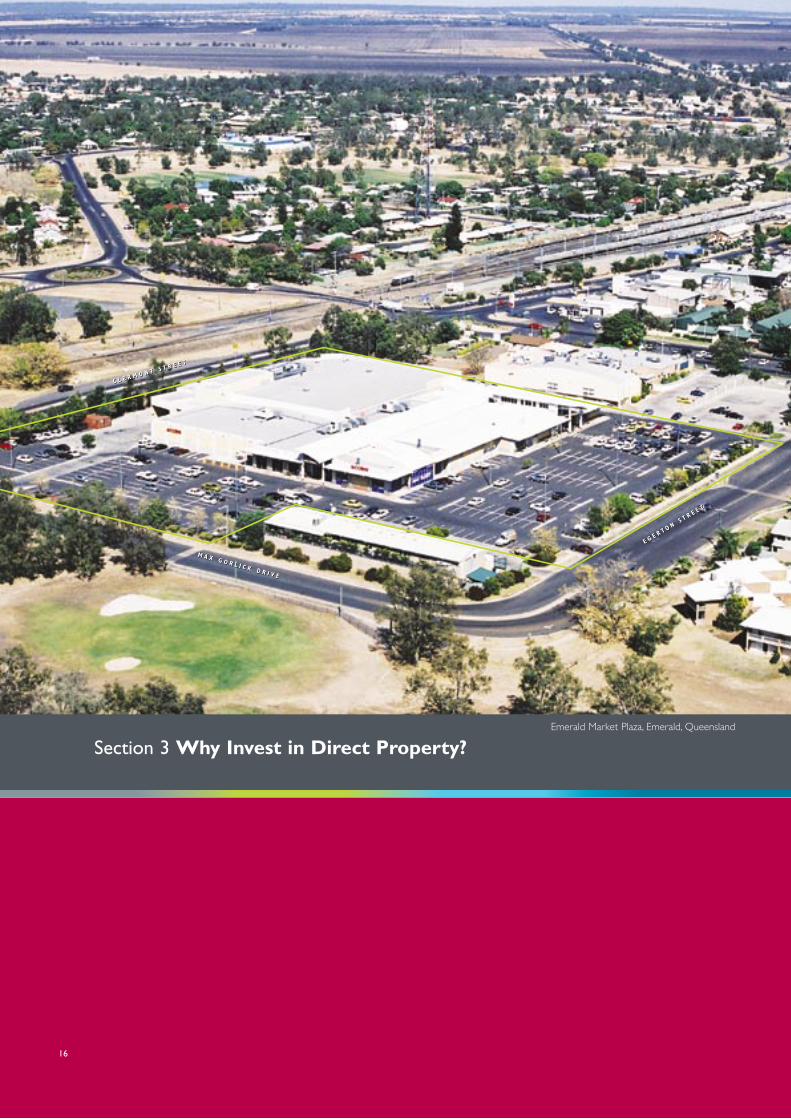

Section 3 Why Invest in Direct Property?

The direct property industry has expanded rapidly over the past five years as investors continue to fulfil their direct property investment needs through unlisted property funds. The growth in Centro MCS’s business reflects the strong demand from investors for quality, high yielding and tax effective retail direct property investments.

3.1 KEY BENEFITS OF INVESTING IN DIRECT PROPERTY

The Manager believes that the importance of direct property as an essential part of a well balanced investment portfolio continues to be reinforced for the following reasons:

Collective Investment

Direct property investment provides a way in which a number of investors, each investing different sums of money, can purchase quality property together as a group, which they may not have had the resources to secure or the expertise to manage on their own. The Manager considers that a direct property investment that offers co-investment with Centro, or entities it controls or manages is beneficial for Investors because it demonstrates a close alignment of Centro’s interests with Investors’ interests.

Tax Effective Returns

The performance of direct property is highlighted even further after taking into account the tax effectiveness of the investment. Tax plays a vital role in an Investor’s overall return. In a fully taxable investment, a 7.80% return to an Investor on the top marginal tax rate of 48.5% returns only 4.02% after tax. On the other hand, a 7.80% return which is 100% tax-advantaged is equivalent to an after-tax return of 7.80%. This equates to a pre-tax return of 15.15% in that year for Investors on the highest marginal tax rate in Australia.

The table below gives an example of an individual, in a tax-advantaged investment such as this, on the highest marginal tax rate of 48.5%.

Original Investment (for example) $100,000

Yield on Equity 7.80%

Distribution $7,800

Tax Advantaged Component 100%

Tax Advantaged Income $7,800

Taxable Income $0

Equivalent Pre-Tax Yield(1) 15.15%

(1) This calculation does not take into account potential capital gains or losses on the investment or tax resulting from reductions in the capital gains tax cost base.

Tax benefits flow from the tax deductions available from depreciation of buildings, plant and equipment and from the amortisation of establishment costs. Some of these benefits may reduce the cost base of the investment and accordingly attract capital gains tax when the Syndicate disposes of an asset or the Investor sells their investment. Even then, individuals may be entitled to a 50% exemption from capital gains tax, if the investment has been held for more than 12 months.

Hedge Against Inflation

Often, property rentals will increase in line with inflation. This means that rental income is keeping pace with rises in the cost of living and is therefore providing Investors with a natural hedge against inflation. Frequently, as rents increase, the value of the property goes up.

Diversification Benefits

It is possible to reduce risk by diversifying across investments. Direct property offers significant diversification benefits when it forms part of a balanced investment portfolio.

It is the only major asset class that actually delivers the fundamental goal that investors are trying to achieve through diversification – the increased safety that comes from owning assets that perform in different ways (i.e. in low or negative correlation) to shares and bonds. See chart entitled ‘Asset Class Comparison’ on the next page.

Pirie Plaza, Port Pirie, South Australia

18 19

Section 3 Why Invest in Direct Property?

Complements Investment in Other Asset ClassesDue to the counter-cyclical behaviour of different asset classes, direct property investment can assist in supporting overall income returns in investment portfolios by providing a less volatile income stream when other asset classes may be underperforming. Property is generally viewed as a long term investment and can complement assets with greater liquidity.

Importantly, the chart below demonstrates that direct property has outperformed the other asset classes at the most crucial time – when other asset classes were under pricing pressure.

Asset Class Comparison Rolling Annual Total Returns (December 1985 - June 2004)

���

���

���

���

���

����

����

Source: Atchison Consultants June 2004

������������������ ���������������� ���������������� ��������������

������ �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �������

����������������������������

3.2 KEY BENEFITS OF INVESTING IN THE RETAIL PROPERTY SECTOR

OutperformanceRetail property has outperformed all other asset classes including other sectors of the property market as well as LPTs. It has provided consistently high and stable returns over the last 20 years (see chart on page 19).

From December 1984 to June 2004 retail property delivered an average total return of 13.3% per annum with the lowest risk rating of any comparable asset class(see chart on the right).

���

���

���

���

���

��

��

���� �� �� �� �� ��� ��� ��� ��� ���

������������������������December 1984 - June 2004

���������������

���

����

����

����

����

��

�����������������

���������������

�������������������

��������������

���������������

���������������

�����������������

����������������

Source: Atchison Consultants June 2004

18 19

Section 3 Why Invest in Direct Property?

��������� �� �� �� �� �� �� �� �� �� �� �� �� �� �� �� ��

���

���

���

���

���

���

Total Returns (including Income and Capital Growth) December 1984 - June 2004

Source: Property Council of Australia – Investment Performance Index June 2004

���

���

�����

�����

�����

�� �� �� �������

�������������������

� ������� ������� ������������� ����������������������������� ��������������������������������

The Manager believes that an investment in retail property offers significant benefits by way of superior returns with low volatility.

Stable and Secure Income Quality retail property provides relatively stable and secure income. This is for two main reasons:

• Income is derived from a large diversified base of tenants – a large proportion of the Syndicate income is provided by Coles and Woolworths and other national retailers; and

• The income is indirectly driven by consumer spending – the Syndicate properties have a convenience food based focus, which tends to be largely non-discretionary. They are therefore less likely to be impacted by a change in economic conditions.

Spread of Risk A well constructed retail property portfolio will offer a complementary mix of retail tenants. This minimises reliance on any single key tenant for rental income.

Pinelands Plaza, Sunnybank Hills, Queensland

20 21

Section 4 The Properties Lismore Central, Lismore, New South Wales

20 21

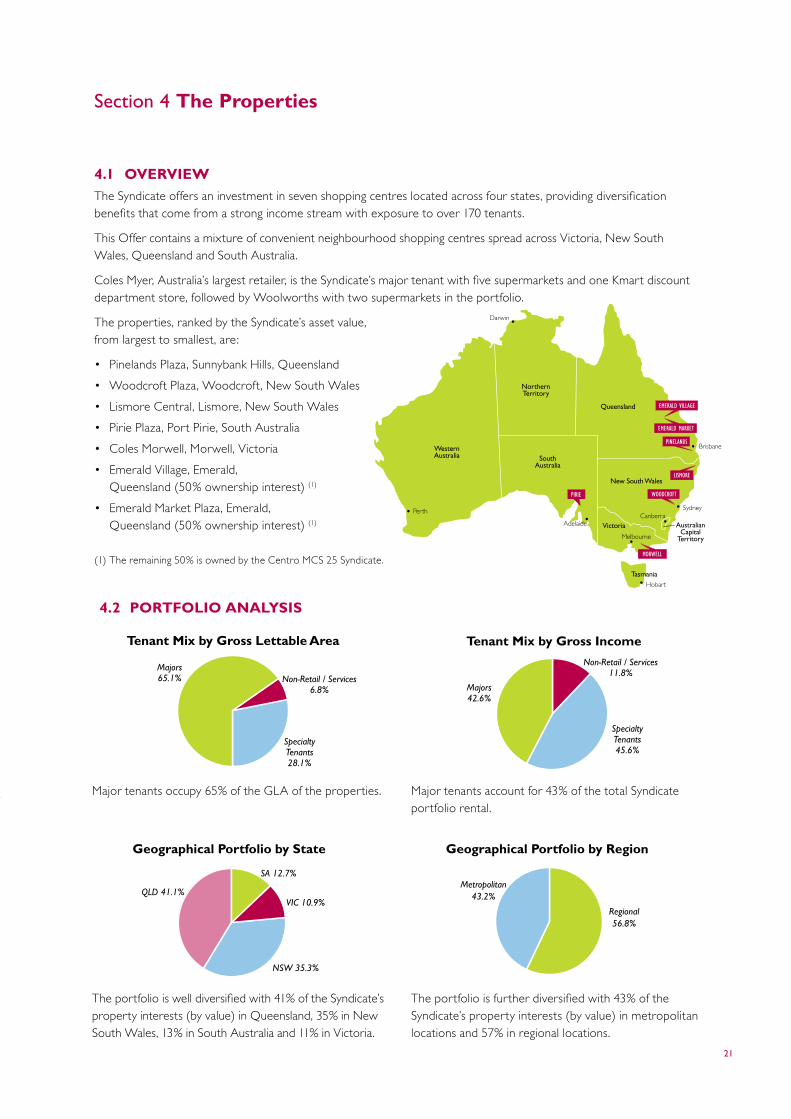

Section 4 The Properties

4.1 OVERVIEWThe Syndicate offers an investment in seven shopping centres located across four states, providing diversification benefits that come from a strong income stream with exposure to over 170 tenants.

This Offer contains a mixture of convenient neighbourhood shopping centres spread across Victoria, New South Wales, Queensland and South Australia.

Coles Myer, Australia’s largest retailer, is the Syndicate’s major tenant with five supermarkets and one Kmart discount department store, followed by Woolworths with two supermarkets in the portfolio.

The properties, ranked by the Syndicate’s asset value, from largest to smallest, are:

• Pinelands Plaza, Sunnybank Hills, Queensland

• Woodcroft Plaza, Woodcroft, New South Wales

• Lismore Central, Lismore, New South Wales

• Pirie Plaza, Port Pirie, South Australia

• Coles Morwell, Morwell, Victoria

• Emerald Village, Emerald, Queensland (50% ownership interest) (1)

• Emerald Market Plaza, Emerald, Queensland (50% ownership interest) (1)

(1) The remaining 50% is owned by the Centro MCS 25 Syndicate.

Perth

WesternAustralia

NorthernTerritory

SouthAustralia

Queensland

New South Wales

AustralianCapital

Territory

Victoria

Tasmania

Adelaide

Melbourne

Hobart

CanberraSydney

Brisbane

Darwin

PIRIE

EMERALD MARKET

MORWELL

LISMORE

WOODCROFT

PINELANDS

EMERALD VILLAGE

4.2 PORTFOLIO ANALYSIS

Major tenants occupy 65% of the GLA of the properties. Major tenants account for 43% of the total Syndicate portfolio rental.

Majors65.1%

SpecialtyTenants28.1%

Non-Retail / Services6.8% Majors

42.6%

SpecialtyTenants45.6%

Non-Retail / Services11.8%

Tenant Mix by Gross IncomeTenant Mix by Gross Lettable Area

�������������������������������

���������

���������

���������

��������

��������������������������������

�������������

�����������������

Majors65.1%

SpecialtyTenants28.1%

Non-Retail / Services6.8% Majors

42.6%

SpecialtyTenants45.6%

Non-Retail / Services11.8%

Tenant Mix by Gross IncomeTenant Mix by Gross Lettable Area

The portfolio is well diversified with 41% of the Syndicate’s property interests (by value) in Queensland, 35% in New South Wales, 13% in South Australia and 11% in Victoria.

The portfolio is further diversified with 43% of the Syndicate’s property interests (by value) in metropolitan locations and 57% in regional locations.

22 23

4.3 SUMMARY PROPERTY INFORMATION

Section 4 The Properties

Pinelands Plaza Woodcroft Plaza Lismore Central

Location Sunnybank Hills Woodcroft Lismore

State Queensland New South Wales New South Wales

Asset Type Neighbourhood Neighbourhood Neighbourhood

Purchase Price $25,800,000 $18,500,000 $18,000,000

Purchase Price Including Actual Acquisition Costs(1)

$25,930,000 $18,625,000 $18,125,000

Valuation Summary

Valuation (100%) $25,630,000 $18,500,000 $17,500,000

Valuation Including Normal Acquisition Costs (100%)(2)

$27,700,000 $19,600,000 $18,550,000

Valuation Firm Jones Lang LaSalle FPDSavills FPDSavills

Valuation Date 31 December 2004 31 December 2004 31 December 2004

Capitalisation Rate 7.50% 7.25% 8.50%

Discount Rate 9.25% 9.75% 10.25%

Syndicate Interest 100% 100% 100%

Site Area 18,270m2 13,540m2 8,293m2

Majors % of GLA 36.04% 56.76% 59.46%

Majors % of Passing Gross Rental

15.87% 28.31% 48.57%

Car Spaces 262 183 202

GLA 5,913m² 4,662m² 6,878m²

Occupancy Rate 96.93% 100.00% 98.87%

Major Tenants Coles Coles Woolworths

No. of Specialty Tenants 42 plus 1 ATM 24 plus 1 kiosk and 2 ATMs 22 plus 2 ATMs

Major Leases Coles Coles Woolworths

Term: 10 years (option) 15 years 20 years

Expiry Date: 23 August 2006 24 October 2008 3 December 2005

Options: Nil 2 x 5 years 2 x 5 years

Term:

Expiry Date:

Options:

(1) Includes acquisition costs and stamp duty as set out in Section 6.2. The structure of the purchase transaction has enabled the Manager to save significant up front costs.

(2) Includes estimates of normal acquisition costs including stamp duty, legal fees and due diligence costs incurred on purchase.

22 23

Section 4 The Properties

Pirie Plaza Coles Morwell Emerald Village Emerald Market Plaza

Port Pirie Morwell Emerald Emerald

South Australia Victoria Queensland Queensland

Neighbourhood Neighbourhood Neighbourhood Neighbourhood

$13,000,000 $11,100,000 $9,850,000 (50% of the property)

$6,650,000 (50% of the property)

$13,125,000 $11,225,000 $9,975,000(50% of the property)

$6,979,168(50% of the property)

$13,000,000 $11,100,000 $19,700,000 $13,000,000

$13,750,000 $11,700,000 $20,500,000 $13,600,000

FPDSavills m3property CB Richard Ellis CB Richard Ellis

31 December 2004 31 December 2004 31 December 2004 31 December 2004

8.25% 7.50% 7.75% 7.75%

9.50% 8.25% 9.75% 9.75%

100% 100% 50% 50%

33,590m2 11,114m2 24,400m2 20,970m2

88.72% 90.29% 57.65% 46.20%

69.55% 94.09% 44.30% 35.01%

640 259 362 321

8,640m² 5,267m² 7,285m² 6,493m²

98.42% 94.65% 100.00% 98.46%

Coles, Kmart Coles Woolworths Coles

13 plus 1 kiosk 7 25 plus 1 pad site 20 plus 1 mini major and 1 kiosk

Coles Coles Woolworths Coles

25 years 25 years 15 years 20 years

8 September 2005 14 June 2013 2 October 2011 26 October 2017

2 x 5 years Nil 2 x 5 years 4 x 5 years

Kmart

25 years

8 September 2005

2 x 5 years

24 25

Pinelands Plaza, Sunnybank Hills, Queensland

LocationSunnybank Hills is a well established residential suburb, located approximately 18 kilometres south-east of the Brisbane CBD.

Pinelands Plaza is situated on a prominent corner site at the intersection of Pinelands Road and Beenleigh Road.

The centre enjoys a high level of exposure with easy accessibility to the surrounding region. The site is also ideally positioned on the left hand side to serve homeward-bound traffic off Pinelands Road, and therefore the centre is extremely attractive for convenience food and grocery shopping.

Centre and its TenantsPinelands Plaza first opened in 1976 and was expanded and renovated in 1988 increasing the gross lettable area to 5,913m2. The centre comprises a single level retail facility with a Coles supermarket and 42 specialty tenancies all at ground level with open car parking for 262 vehicles. Car parking is easily accessible, with entry and exit points off both Pinelands Road and Beenleigh Road.

The shopping centre layout contains an external mall facing Pinelands Road with the Coles supermarket located at the southern end and specialty tenancies located to both the north and south. The overall standard of the centre is excellent, including a strong offer of both retail and non-retail tenancies. The non-retail tenancies such as banks, professional and medical offices, Australia Post and real estate agents create important destination points for Pinelands Plaza. There are presently three vacancies at the centre and Centro MCS is concentrating on securing new key retailers for these sites.

The Coles supermarket with an area of 2,131m2 trades strongly with sales turnover in excess of the industry benchmark. The Coles lease is due to expire in August 2006 and Centro MCS is confident, given Coles’ trading performance, that a new long term lease will be achieved. Coles has recently instigated negotiations with Centro MCS for a further term. These negotiations provide Centro MCS with an opportunity to potentially negotiate a higher rent than forecast in the Syndicate projections.

Centre sales at Pinelands Plaza are projected to show strong average sales growth of 4.3% per annum up to 2008.

Trade AreaThe Pinelands Plaza trade area has a population estimated at 46,390 including approximately 18,000 people in the main trade area. The main trade area encompasses the suburbs of Sunnybank Hills, Sunnybank, Runcorn, and Acacia Ridge with the customer profile described as cosmopolitan, including a high proportion of Asian born residents.

Demographics show that the average age of residents is slightly younger than the comparable Brisbane average, with income levels higher on a per household basis. The household structure typically comprises of couples with dependant children.

The trade area growth is typical of an established outer-suburban area although there is some new residential housing being constructed. Following strong population growth from 1996 to 2004 moderate growth of 0.7% per annum is now forecast over the next ten years.

� � � � � � � � � � � � � �� � � � � � � � � � � � � �

� � � � � � � �� � �

� � �

� � � � � � � �� � �

� � � � � � � � � � � � � � �� � � � � � � � � � � �

MAJOR TENANTS SPECIALTY TENANTS CENTRE BOUNDARY

F A R N E S T R E E T

P I N E L A N D S R O A D

BE

EN

LE

IG

H

RO

AD

Pinelands Plaza

COLES

24 25

CompetitionThe competition for Pinelands Plaza consists of a number of established shopping centres, providing a relatively stable competitive environment.

Westfield Garden City is one of the largest retail facilities in Brisbane with a total lettable area of approximately 78,000m2 and is located over five kilometres from Pinelands Plaza. Due to the large size of this centre it is a destination for both food and non-food shopping for residents throughout the surrounding region, including throughout the defined Pinelands Plaza trade area.

Other competing centres include Sunnybank Plaza, Sunnybank Hills Shoppingtown and Runcorn Plaza. Sunnybank Plaza is located approximately two kilometres north of Pinelands Plaza and is anchored by a Kmart discount department store and a Coles supermarket. Sunnybank Hills Shoppingtown is located three kilometres south of Pinelands Plaza and is anchored by a Pick ‘n’ Pay superstore and Woolworths supermarket. Runcorn Plaza is located approximately three kilometres east of Pinelands Plaza and is anchored by a Bi-Lo supermarket.

Centro MCS are not aware of any other significant shopping centre developments within the trade area that are planned or that compete directly with Pinelands Plaza.

Strategy for the Centre The short term strategy for Pinelands Plaza is to finalise the lease renewal for the Coles supermarket prior to lease expiry in August 2006. Discussions are already underway with Coles who have indicated their intention to enter into a new long term lease agreement.

The centre contains three vacancies and Centro MCS will be concentrating on securing new retailers to improve the property tenancy mix. Appropriate leasing up allowances and incentives have been budgeted to achieve these targets.

Mt Gravatt

Oxley

SunnybankHills

PINELANDS PLAZA

33

32

13

13

2

4

1

3

BRISBANE

1ALT

26 27

LocationWoodcroft is a recently developed suburb located some 38 kilometres west of the Sydney CBD. Blacktown is located approximately four kilometres to the south-east with Mt Druitt located approximately nine kilometres to the west.

The centre is located on the south-eastern corner of Richmond Road and Woodcroft Drive. Richmond Road is a major four-lane arterial road, connecting the satellite townships of Richmond and Windsor (to the north-east of Sydney) with the metropolitan area. Consequently, the centre has high exposure to a large number of vehicles travelling along this major arterial route.

Centre and its TenantsConstructed in 1993 Woodcroft Plaza is a modern neighbourhood shopping centre with a gross lettable area of 4,662m2. The centre is anchored by a Coles supermarket of 2,646m2 with an external Liquorland outlet. Coles and Liquorland are supported by 11 internal and 12 externally facing specialty stores, a kiosk and two ATM’s. In addition to the main retail centre, there are also adjacent peripheral retail facilities, which are not part of the centre ownership, including a modern BP service station and McDonalds restaurant. These outlets provide compatible uses which draw patrons indirectly to the centre.

Woodcroft Plaza is designed around a main internal north-south retail mall, with car parking for 183 vehicles provided on the northern and western sides of the centre, directly accessible off Woodcroft Drive. The overall high standard of the centre reflects current expectations of a modern convenience shopping centre in an outer suburban area.

The Coles supermarket trades strongly, above the average for major supermarkets throughout Australia and reflects the low provision of supermarket floor space in the surrounding region. Supermarket sales over the next decade are projected to grow strongly at an average rate of around 3.8% per annum.

Specialty tenants include a pharmacy, newsagency and a number of fashion and food retailers typically found in a neighbourhood shopping centre. The centre also includes a large portion of non-retail space such as real estate agents, a medical and dental centre, supporting and reinforcing the centre’s community focus.

Trade AreaThe trade area served by Woodcroft Plaza includes in its primary sector the suburbs of Woodcroft and Doonside with secondary sectors further to the north and west. The existing population is estimated at 39,000 people including 21,000 in the main trade area. The total population grew at approximately 2% per annum from 1996 to 2004, with the majority of growth recorded in the main trade area.

There are some further pockets of residential development occurring throughout the region especially to the north and north-west of the defined Woodcroft Plaza trade area which will accommodate a large proportion of Sydney’s future residential growth. This region, generally known as the North-West or Marsden Park region, is currently being reviewed by the Department of Infrastructure, Planning and Natural Resources to potentially accommodate an additional 300,000 residents.

The Woodcroft trade area is typical of a rapidly growing outer-suburban area comprising a large number of young families. The trade area population also has a high proportion of Asian born residents. This provides further opportunities to modify the retail mix to suit the local demographic base.

CompetitionWoodcroft Plaza is one of two key food and grocery shopping centres within the defined trade area, with Quakers Court being the other. Quakers Court is located one kilometre to the north of Woodcroft Plaza and is anchored by a Woolworths supermarket and includes 20 specialty shops. The region served by these two supermarket centres is separated from other competing supermarket centres by a number of natural and man made barriers such as railway lines, major roads and Eastern Creek.

Woodcroft Plaza, Woodcroft, New South Wales

R I C H M O N D R O A DR I C H M O N D R O A D

WOO

DC

RO

FT

DR

I VE

WOO

DC

RO

FT

DR

I VE

W O O D C R O F T D R I V E

MAJOR TENANTS SPECIALTY TENANTS CENTRE BOUNDARY

Woodcroft Plaza

COLES

26 27

The other competing shopping centres are the large regional and sub-regional shopping centres at Westpoint Blacktown, four kilometres south-east, and Plumpton Marketplace, approximately five kilometres west of Woodcroft Plaza.

Additional supermarket competition is likely in the future as a result of a major redevelopment underway at Westpoint Blacktown which will see an expansion of the 50,000m2 centre to around 90,000m2. This expansion will include a new Coles supermarket, as well as the relocation and expansion of several major retailers including Myer, Target, Woolworths, Big W, Franklins and a Hoyts cinema complex. The number of specialty shops at the centre will increase from 154 to more than 280. There is also the possibility of an additional second major supermarket at Plumpton. Centro MCS does not expect that these projects will significantly impact on Woodcroft Plaza which acts as a convenience neighbourhood shopping centre, providing for both the weekly and top-up shopping needs of surrounding residents.

Strategy for the Centre The strategy for Woodcroft Plaza is to concentrate on opportunities to improve the overall retail mix at

the centre. A greater number of national chains could be incorporated at the site, including non-retail tenants such as banks and Australia Post. These types of tenants will continue to be targeted to add to the community friendly focus of the centre.

As there is a high proportion of Asian born residents within the Woodcroft trade area the leasing strategy will also target some further Asian style stores to attract resident spending from throughout the region. Remixing and improving the existing specialty stores should improve the centre’s market share and profitability.

Bankstown

Parramatta

Blacktown Ryde

WOODCROFT PLAZA

44

SYDNEY

1

1

17

7

3

4 4

3

63

28 29

Lismore Central, Lismore, New South Wales

LocationLismore is a major township located 80 kilometres south of Coolangatta/Tweed Heads in northern New South Wales.