central bank independence and economic performance

TRANSCRIPT

21

Patricia S. Pollard

Patricia S. Pollard is an economist at the Federal ReserveBank of St. Louis. Heather Deaton and Richard D. Taylorprovided research assistance.

11 Central Bank Independence andEconomic Performance

N RECENT YEARS MANY countries haveadopted or made progress toward adoptinglegislative proposals removing their centralbanks from government control, that is, makingthem independent. Between 1989 and 1991,New Zealand, Chile and Canada enacted legisla-tion that increased the independence of theircentral banks. The 1992 Treaty on EuropeanUnion (Maastricht Treaty) requires EuropeanCommunity (EC) members to give their centralbanks independence as part of establishing theEuropean Monetary Union. As a result, ECcountries that do not yet have strongly indepen-dent central banks have introduced legislationor announced their commitment to make theircentral banks more independent.1 Furthermore,in recent months the governments of Brazil andMexico have announced their intentions to in-troduce legislation to create more independentcentral banks.

In view of these developments, it might seemreasonable to conclude that unambiguous linkshad been established between economic perfor-

mance and the degree of central bank indepen-dence. Interestingly, however, the two post-World War II star performers among the indus-trialized economies—Germany and Japan—havedifferent levels of central bank independence.The German Bundesbank is viewed as one ofthe most independent central banks in theworld, whereas the Bank of Japan is seen asmore subject to government control. Thus thecontrast between the movement to grant centralbanks more independence and widely differentdegrees of independence across the major econ-omies raises several questions. Among these are:Why is the idea of an independent central bankpopular? Are there economic benefits of havingan independent central bank?

This paper examines empirical and theoreticalstudies of central bank independence to addressthese questions. Empirical researchers have de-vised measures of independence to focus on therelationship between central bank independenceand a country’s economic performance. Theo-retical studies have modeled the strategic be-

‘To meet the level of independence prescribed by the Maas-tricht Treaty, a central bank must be prohibited from takinginstructions from the government. The term for centralbank governors must be set at a minimum of five years,although it can be renewed. In addition, the central bankmust be prohibited from purchasing debt instrumentsdirectly from the government (that is, in the primarymarket) and from providing credit facilities to the govern-ment. Both Denmark and the United Kingdom havereserved the right to decline membership in the EuropeanMonetary Union. Thus neither country has introduced

legislation to ensure conformity of their central banks withthe Maastricht provisions.

For a detailed analysis of the institutional status of thecentral banks of the EC countries, see the Committee ofGovernors of the Central Banks of the Member States ofthe European Economic Community (1993).

22

havior of monetary and fiscal policymakers tohe able to compare an economys performancewhen policymakers cooperate in setting policiesurith its performance when they do notcooperate.

‘I’he next section of this paper presents a sur-vey and evaluation of empirical studies. -Next,theoretical studies are presented and evaluated.The final section examines the extent to whichthese studies either explain the current move-ment toward greater central bank independenceor highlight unresolved questions in this debate.

EMPIRICAL STUDIES: CENTRALBANK INDEPENDENCE ANDECONOMIC PERFORMANCE

Inflation and Central BankIndependence

As a broad generalization, interest in centralbank indeperide.nce was motivated by the beliefthat, if a central bank was free of direct politi-cal pressure, it would achieve lower and morestable inflation.’ Bade and Parkin (1985) con-ducted one of the first empirical studies of thislink. The authors used data for 12 Organizationfor Economic Cooperation and Development(OECD) countries in the post-Bretton Woods eraand measured the degree of central bank in-dependence according to the extent of govern-ment influence over the finances and policies ofthe central bank.’ i’he degree of financial in-fluence on the central hank was determined bythe government’s ability to set salary levels formember-s of the governing board of the centralbank, to control the central hank’s budget andto allocate its profits. The degree of policy in-tiuence was determined by the government’sability to appoint the members of the centralhank governing hoard, government representa-tion on this hoard, and whether the govern-ment or’ the central bank was the final policyauthority. Countries were given a rank of onethrough four in each category, with four beingthe highest level of central hank independence.

Bade and Parkin concluded that the degree offinancial independence of the central hank was

not a significant determinant of inflation in thepost-Bretton Woods period. Policy indepen-dence, however, was seen as an important de-terminant of inflation because the two countrieswith the highest degree of policy independence(Germany and Switzerland) had inflation ratessignificantly helow those of all other countriesin the sample. They found no significant differ-ences in inflation performance among countrieswith lower rankings of independence in thepost-Bretton Woods era.

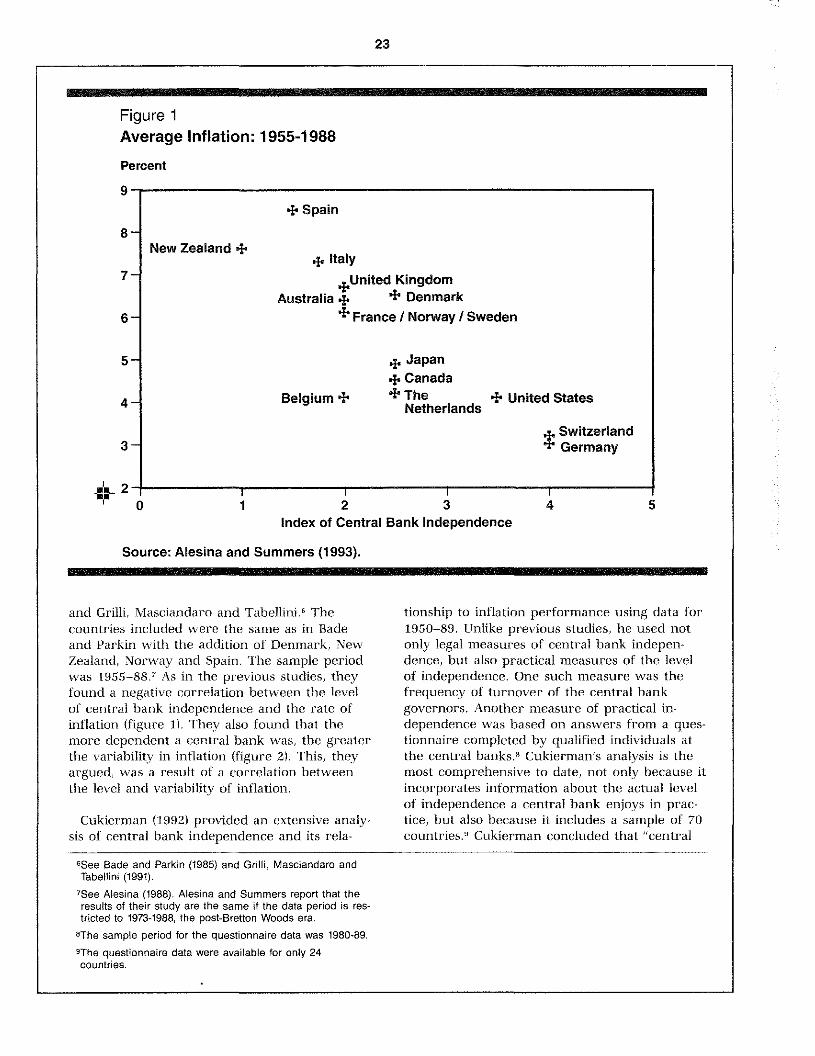

Alesina (1988) used the Bade and Parkin (1985)index hut added the following four countries:Denmark, New Zealand, Norway and Spain. Hefound, as hypothesized, that there was generallyan inverse relationship hetween average infla-tion rates and the level of central bank in-dependence.

Grilli, Masciandaro and Tabellini (1991) createdtwo indexes of central hank independence—onebased on economic measures of independence(with a scale ranging from zero to eight), andthe other based on political measures of in-dependence (with a scale ranging from zero toseven).~The political factors were similar tothose identified by Bade and Parkin, The eco-nomic factors considered were the ability of thegovernment to determine the conditions underwhich it can borrow from the central bank andthe monetary instruments under the control ofthe central hank. ‘rhe data set comprised isOECD countries over the period 1950—89.’ Forthe period as a whole, Grilli, Masciandaro andTahellini found that economic independencewas negatively related to inflation. Political in-dependence also had a negative correlation withinflation, but the relationship was not statistical-ly significant. Breaking the data into fourdecade-long subperiods, they found that neithermeasure of independence had a significant ef-fect on inflation in the fit’st two decades. In the1970s both measures of independence were sig-nificant, whereas in the 1 980s only the econom-ic independence measure was significant.

Alesina and Summers (1993) calculated ameasure of central hank independence by aver-aging the indexes created by Bade and Parkin,

‘Buchanan and Wagner (1977) point out that even an in-dependent central bank may not be immune from politicalpressures and thus exhibit an inflationary bias.‘The 12 OECD countries are Australia, Belgium, Canada,France, Germany, Italy, Japan, Netherlands, Sweden, Swit-zerland, United Kingdom, and United States.

4ln both measures the scale is increasing in the level of in-dependence.

5Grilli, Masciandaro and Tabellini add Austria, Denmark,Greece. New Zealand and Portugal to Bade and Parkin’sgroup of countries and eliminate Sweden.

Figure 1Average Inflation: 1 955—i 988

Percent

9—

8-

7-

~4_2- I I I

0 1 2 3Index of Central Bank Independence

Source: Alesina and Summers (1993).

and Grilli, Masciandaro and Tabellini.° Thecountries included were the same as in Badeand Parkin with the addition of Denmark, NewZealand, Norway and Spain. The sample periodwas 1955—88.’ As in the previous studies, theyfound a negative correlation between the levelof central hank independence arid the rate ofinflation (figure 1). They also found that themore dependent a central bank was, the greaterthe variability in inflation (figure 2). This, theyargued, was a result of a correlation betweenthe level and variability of inflation.

Cukiermnan (1992) provided an extensive analy-sis of central bank independence and its rela-

‘See Bade and Parkin (1985) and Grilli, Masciandaro andTabellini (1991).‘See Alesina (1988). Alesina and Summers report that theresults of their study are the same if the data period is res-tricted to 1973-1988, the post-Bretton Woods era.

‘The sample period for the questionnaire data was 1980-89.

tionship to inflation performance using data for’1950—89. Unlike previous studies, he used notonly legal measures of central bank indepen-dence, but also practical measures of the levelof independence. One such measure was thefrequency of turnover of the central bankgovernors. Another measure of practical in-dependence was based on answers from a ques-tionnaire completed by qualified individuals atthe central banksi’ Cukiet’man’s analysis is themost comprehensive to date, not only because itincorporates information about the actual levelof independence a central bank enjoys in prac-tice, but also because it includes a sample of 70countries.’ Cukierman concluded that “central

23

~~~~

New Zealand +

6-

5-

4-

3-

+ Spain

+ ItalyUnited Kingdom

Australia + + Denmark+ France I Norway I Sweden

+ Japan+ Canada

Belgium + + The + United StatesNetherlands

~.Switzerlandt Germany

4 5

‘The questionnaire data were available for only 24countries.

24

Figure 2Variance of Inflation: 1955-1988

Percent

40

30-

20-

10-

I I I

Index of Central Bank Independence

Source: Alesina and Summers (1993).

bank independence affects the rate of inflationin the expected direction.”°This result was alsofound by Cukierman, Webb and Neyapti(1992).”

Central Bank Independence andthe Real Economy

Although most of the empirical work focusedon the relationship between central bank in-dependence and the rate of inflation, somestudies examined the link between indepcn-

dence and economic output. if an independentcentral bank can produce lower inflation than adependent central bank, does this come at thecost of lower output? Conversely, are dependentcentral banks attempting to exploit a short-runPhillips Curve relationship, accepting higher in-flation in order to achieve higher output?

Grilli, Masciandaro and Tabellini (1991) foundno systematic effect of central bank indepen-dence (using either of their two indicators) onthe growth rate of real output. Alesina and

‘°Cukiermandid not actually use the rate of inflation, but therate of depreciation of the real value of money, defined bythe following formula:

d~— it~

I +

where a~is the inflation rate in period t. The use of d, asnoted by Cukierman, moderates the effects of hyper-inflation on the results.

“Capie, Mills and Wood (1992) also studied the link betweeninflation and central bank independence. Their data setconsisted of 12 countries, with the data series beginningbetween 1871 and 1916 and ending in 1987. Central

banks were classified as either dependent or independentaccording to the extent of their control over monetary poli-cy. The authors examined the relationship between the sta-tus of the central bank and inflation over the entire sampleperiod and four subsample periods—pre-World War I, theInterwar Years, Bretton Woods and post-Bretton Woods.Periods of hyperinflation, however, were excluded from thedata. In all sample periods, the countries with independentcentral banks were in the low inflation group. Nevertheless,some of the dependent central banks were also in thisgroup. The authors concluded that independence may be asufficient condition for low inflation but not a necessaryone.

Spain +

New Zealand +

+ Italy

+ United Kingdom+ Australia I France

+Swec~en

+ Japan

~ Canada‘r DenmarkNorwayBelgium

+ TheNetherlands

+ United States

Germany

0 1 2 3 4 5

25

Figure 3Average Real GNP Growth: 1955-1 987

Percent

7-

Summers (1993) likewise found no correlationbetween average economic growth or the varia-bility of growth and the level of central bankindependence (figures 3 and 4)12

De Long and Summers (1992) looked at therelationship between central bank independenceand output per worker while trying to eliminatedifferences between countries that were duesolely to convergence effects.” To do this, theyexamined the growth rate of real gross domes-tic product (GDP) per worker during 1955—90,controlling for the level of GDP per worker in1955.’~This procedure showed a positive rela-

tionship between central bank independenceand economic growth.” More precisely, theyfound that holding constant the 1955 level ofreal output per worker, a unit increase in theirindex of central bank independence was as-sociated with a 0.4 pem’centage point incm-ease ingrowth per year.”

In contrast, Cukierman, Kalaitzidakis, Summersand Webb (1993) found that output growth inindustrialized countries was unrelated to centralbank independence even after controlling forstructural factors that might influence growth.The factors they considered were the initial level

l2The results are the same if per capita gross nationalproduct (GNP) is used rather than GNP.

“Standard neoclassical growth models suggest that growthrates of economies tend to converge over time. Thus giventwo countries, the one with the lower per capita output willhave a higher growth rate than the other until their levelsof real output per capita converge.

‘~GDPper worker levels are based on the Summers andHeston (1991) estimates, which use purchasing powerparity conversions.

ISThis study does not take into account that the degree of in-dependence of the central bank of New Zealand changeddramatically in 1989. Furthermore, all of the studies, with theexception of Alesina (1988), do not take into account thatthere was an institutional change in the structure of theBank of Italy in 1981 that increased its independence. Thelatter change, however, was not as substantial as the former.

“De Long and Summers regress the average growth rate ofGDP per worker over the period 1955-90 on GDP per workerin 1955 and the central bank independence index.

6-

5-

4-

3-

2-

+ Japan

AustralialNorway +CanadatFrance

~ The NetherlandsDenmark

Spain +Italy +

New Zealand +

Belgium+

+ Sweden

+ United Kingdom

+ Germany

+United States+Switzerland

0 1 2 3 4 5Index of central Bank Independence

Source: Alesina and Summers (1993).

26

of a country’s GDP, its initial enrollment rates forprimary and secondary education, and changesin its terms of trade. The authors did find,however, using the turnover rate of centralbank governors as a proxy for independence,that central bank independence did have a posi-tive effect on growth in developing countries.

The difference in the results for industrializedcountries versus developing countries they ar-gue, may imply that “dependence on politicalauthorities is bad for growth only when the lev-el of independence is sufficiently high.” Cen-tral bank independence is higher’ in all theindustrialized countries than in most of the de-veloping countries.

Central Bank Independence andFiscal Deficits

Another area of empirical study has been therelationship between central hank independence

and fiscal deficits. The motivation for thesestudies is the belief that independent centralbanks should be better able to resist govern-ment efforts to have them monetize deficits.Thus governments realizing that there may hesome limit on their ability to issue bonds con-tinuously to finance deficits may decide to limitdeficit spending.

Parkin (1987) investigated this question for thesanie 12 countries as Bade and Parkin for theperiod 1955_83.18 lie found that there was someevidence of a negative relationship between cen-tral hank independence and the long-run be-havior of government deficits as a percent ofgross national product (GNP). The deficits ofSwitzerland and Germany, the countries with thehighest levels of central bank independence, hadlong-run equilibrium values near zero with littlevariance. However, other countries, notablyFrance, that had low levels of central bank in-

“See Bade and Parkin (1985).

Figure 4

Variance of Real GNP Growth: 1955-1 987

Percent

12,5

10—

7.5—

5—

2.5—

tJapan

+ Spain

The Netherlands* Denmark

New Zealand + + Italy

Australia * BelgiumUnited Kingdom I France+ + Canada

+ Sweden

+ Norway

+ Switzerland

+ + GermanyUnited States

“ I I I I0 1 2 3 4

Index of Central Bank Independence

Source: Alesina and Summers (1993).

S

“See Cukierman, Kalaitzidakis, Summers and Webb (1993),p. 42.

27

dependence also had small long-run deficits as apercent of GNP.

Masciandaro and Tabellini (1988) looked at fis-cal deficits as a percent of GDP in Australia,Canada, Japan, New Zealand and the UnitedStates during the period 1970—85.” They foundthat New Zealand, which had the lowest level ofcentral hank independence of the five countriesduring this period, had the highest fiscal deficitas a percent of GDP. The United States,however, with the highest level of central bankindependence among this group of countries,had a deficit/GDP ratio similar to those of theother countries.

Grilli, Masciandaro and Tahellini (1991) foundthat there was generally a negative correlationbetween the deficit/GNP ratio and the degree ofcentral hank independence. However, if politicalfactors, as well as central hank independence,were included in their regression, the lattervariable was insignificant.” Thus they concludethat an independent monetary authority appar-ently does not discourage the government fromrunning fiscal deficits.

A further examination of the relationship be-tween fiscal deficits and central hank indepen-dence, which is consistent with the work doneby Alesina arid Summer’s and Dc Long and Sum-mers, is presented here.21 Using the same indexof central bank independence and the same 16countries as these previous papers, there issome evidence of a negative correlation be-tween average deficits as a percent of GDP andcentral bank independence for the period1973—89, as shown in figure 5,22 The degree ofindependence, however, is not a statisticallysignificant (at a = .05) determinant of thedeficit/GDP ratio. The variability of deficits as apercent of GDP is also negatively correlatedwith central bank independence (figure 6) and

this relationship is statistically significant.

EVALUATION OF THE EMPIRICALSTUDIES

At first glance, these studies seem to indicatethat a country that wants to lower its inflationrate and do so without hurting growth shouldcreate an independent central hank. Such a cen-tral bank apparently could also help reduce fis-cal deficits and increase output. ‘These benefitswould explain the recent popularity of indepen-dent central banks. Thus Grilli, Masciandaroand Tahellini commented:

Having an independent central hank is almostlike having a fr-ce lunch; there are benefits hutno apparent costs in terms of macroeconomicperformance.”

Alesina and Summer-s (1993) went a step furtherin concluding their findings: “Most obviouslythey suggest the economic performance meritsof central hank independence.”~

A more careful analysis of these studies,however, indicates weaknesses that highlightthe need for fum’ther evidence before oneshould believe that creating an independent cen-tral hank will improve a country’s economicperformance. The following four weaknessesare considered: 1) the difficulty in measuringcentral bank independence; 2) the possibility ofa spurious relationship between independenceand economic performance; 3) the possible en-dogeneity of central bank independence; and 4)the inclusion of the fixed exchange rate periodin the sample data of some of the studies.

The measures of central hank independenceused in empirical studies have been determinedby establishing a set of factors thought to berelevant for independence and them) analyzingcentral bank charters and laws for compliancewith these factors. With the exception of the in-

“The deficits are as a percent of GNP for Japan.2oThese political factors include the frequency of government

changes, significant changes in the government and thepercent of governments in a given period supported by asingle majority party.

2’See Alesina and Summers (1993) and De Long and Sum-mers (1992).

‘2The 1989 ending date was chosen because of the changein the status of the Bank of New Zealand, which occurredin 1989. All data are from the International Monetary Fund,International Financial Statistics.

22See Grilli, Masciandaro and Tabellini (1991), p. 375.24See Alesina and Summers (1993), p. 159. Even the press

has picked up the banner of central bank independence. Arecent headline in The Washington Post proclaimed: “MoreIndependence Means Lower Inflation, Studies Show.” SeeBerry (1993).

28

Figure 5Average Deficit as a Percent of GDP: 1973-1 989

Percent

12.5-

+ Italy

10-

+ Belgium7.5-

New Zealand+ +Japan

tThe NetherlandsSpain + + ~ Canada

+ United StatesSweden I2.5- United Kingdom

+ Australia I France + GermanyNorway+ +Denmark

+ SwitzerlandC’—

I I I

0 1 2 3 4 5Index of Central Bank Independence

Figure 6Variance of Deficit as a Percent of GOP: 1973-1989

Percent

+ Sweden15—

+ Denmark+ Norway

New Zealand +10 + Belgium

United Kingdom +The NetherlandsSpain+ + +

Italy + Japan

Austria+ + Canada +United States+ France Germany

0 I I I

0 1 2 3 4 5Index of Central Bank Independence

29

dcx created by Cukierman, all of the indexes ofindependence apply equal weight to each factor-.Fom instance, the Grilli, Masciandaro and Tabelli-ni index based on political measures of indepen-dence gives a country one point if no one onthe central bank board is appointed by thegovernment and one point if the policy formu-lated by the central bank does not require ap-proval by the government. Although the lattercertainly places a greater constraint on the ac-tions of the central bank than the former, thetwo are treated the same empirically.

Another concern is that the studies are basedon a legal measure of independence that maynot reflect a bank’s de :racto level of indepen-dence. if there is a difference between legal andpractical independence, studies based on theformer type of measures may provide mislead-ing results. Cukierman (1992), in an attempt toaddress this possibility, uses central hankers’responses to a questionnaire to determine theactual degree of independence in the 1980s. Hefinds that the correlation between the legal in-dex and this practical index of independence is0.33 for developed countries, 0.06 for devel-oping countries and 0.04 overall.” This findingindicates, as Cukiermnan notes, that a legal indexof independence is not useful for studying de-veloping countries. It also indicates that a legalindex may he a weak measure of actual in-dependence for the developed countries.

There also may be hias in the factors selectedto measure independence. For’ example, Grilli,Masciandaro and Tahellini include: “statutory re-quirements that central hank pursues monetarystability amongst its goals” in their index.” Like-wise, a central hank is more independent underCukierman’s svstemn if price stability is its onlyobjective than if price stability is one of a num-ber of objectives or not an objective at all. Us-ing the goal of price stability as a measure ofcentral hank independence may result in a biasbetween the measure of independence and theinflation rate.

‘The problems in developing precise measuresof central bank independence are less important,however, if there is a consensus in ranking cen-tral banks within broad levels of independence.Table T lists 16 OECD countries along with their

abisComparison at Relative Rankings ofCentral %nk lndepen4ence

AtesIns and~Atesft*a $~znttme~ Ct4kIennan~

MistS 14 8 1SM9S s a 144ana* 4bm*mak 4mItts

1 1tt$y 13 1 12aNn $ 4 15ttatMrtwtsJttew ZeSlfl 14 tO 10*tway 0 S— 14 1 1

Saden 8 ‘tOSw teSt I

tedXnqdin 6 8 7t3rlted SMes

relative rankings as gi~en by Alesina, Cukierman,and Alesina and Summers.’ All agree that Swit-zerland and Germany have the most ‘ndependentcentral banks of the countries studied. Thereare, however, a few countries ~ hich are rankedquite differently by the authors. For e ample,Japan has the second louest le~el of indepen-dence of all 16 countries, according to Cukier-man, whereas Alesina, and Alesin r md Summersgive it a much higher level of independence.

This discrepancy over’ the degree of indepen-dence of the Bank of Japan is not due solely todifferences in factor-s considered in measuringindependence. The index used by Alesina isbased on the criteria of independence createdby Bade and l’arkin (1985). ‘[he index used byAlesina and Sumnmers is constructed by averag-ing the indexes created by Alesina, and Grilli,Masciandaro and Tahellini. Bade and Parkinclaim that the Bank of Japan is independentfrom the government in formulating and im-plementing monetary policy, and Grilli, Mascian-dat’o and Tabellini claim that there are noprovisions for handling policy conflicts betweenthe Bank of .lapan and the government. In con-trast, Cukierman claims that the Bank of Japanand the government formulate policy jointly and

“The correlations are based on the weighted indexes,Giving each factor related to independence an equalweight in the indexes results in a correlation of 0.01 for de-veloped countries and 0.00 for developing countries.

“See Grilli, Masciandaro and Tabellini (1991), p. 368.

27The measure of independence developed by Cukierman isbased on more factors than the measure used by Alesina,and Alesina and Summers. Thus Cukierman’s rankings aremore delineated than the other two.

30

further notes that in the case of a policy con-flict, the executive branch of the governmenthas final authority.”

Since most of the empirical studies consideronly centtal bank independence as a deter-mninant of economic performance, it is possiblethat if other factors are accounted for, theseresults could he spurious. Grilli. Masciandaroand Tahellini attempt to account for other fac-tors that could affect the rate of inflation by in-cluding political variables. ‘l’hey find that afteraccounting for political factors, central bank in-dependence was still negatively related to infla-tion in the countries studied over the period1950-~-89. The incorporation of political variablesis a step in the right direction, but other factorsalso should he considered. As noted by Cukier-man, “monetary policy is generally sensitive toshocks to government revenues and expendi-tures, employment, and the balance of pay-ments.” The types of shocks that a countryexperienced over the sample period and thereaction of the central bank to these shocks canaffect its economic performance. A study byJohnson and Siklos (1992) found that the reac-tions of centr’al banks (as measured by changesin interest rates) to shocks to unemployment in-flation and world interest rates were not closelyrelated to standard measures of central bank in-dependence.

Empirical use of these indexes may he proble-matic if central hank independence is an en-dogenous variable in the sense that countrieswith a commitment to pr-ice stability may have agreater’ propensity for independent centralhanks. If this is true, the mere establishmnent ofan independent bank without a commitment toprice stability will not bring inflation benefits toa country. In fact, a public aversion to inflationpredates the establishment of many independentcentm’al banks. This was true for the creation ofthe Bundesbank and more recently with respectto central banks in Chile and New Zealand. NewZealand had one of the highest inflation rates ofall industrialized countries in the 1980s. in 1989legislation was passed to increase the indepen-dence of its central bank substantially. This

change is often credited with bringing inflationdown to near- zero. ‘though the legislation cer-tainly formalized the country’s commitment toprice stability, Ne%v Zealand had succeeded inreducing its inflation i-ate from nearly 16 per-cent in 1987 to 6 pem’cent before the creation ofan independent central hank.

In theory, the degree of independence of acentral hank should not be a determinant of acountry’s inflation performance under a fixedexchange rate system because monetary policycannot be set exogenously.’° During the Bretton-Woods era, it is not clear that any central hank(with the possible exception of the U.S. FederalReserve) could be considered independent in thesense of an ability to pursue an independentmonetary policy.” Thus the empirical finding ofa negative relationship between independenceand inflation when the sample period extendsover both the Bretton Woods and post-BrettonWoods eras may indicateaflaw in these studies.To assess the effect of central bank indepen-dence on inflation, the data used in thesestudies could he divided into two periods. If noevidence of a relationship between indepen-dence and inflation is found in the BrettonWoods period, this would strengthen the under-lying argument of these studies that centralbank independence is a primary detem’minant ofa country’s inflation performance.” If, however,evidence is found of a relationship between cen-tm’al hank independence and inflation in theBretton Woods period, this would conflict withtheory and could indicate that the empiricalfindings are spurious.

THEORETICAL MODELS OF FIS—CAL AND MONETARY POLICY IN—TERACTIONS

In contrast to the empirical studies, the theo-retical studies of central bank independence andeconomic performance concentrate on the con-flicts that can arise when monetary and fiscalpolicy are delegated to independent institutions.in this literature an independent central bank isone that does not cooperate with the fiscal au-

“Aufricht (1961) reproduces the Bank of Japan charter andsubsequent changes in its governing regulations, whichsupport the conclusion reached by Cukierman.

“See Cukierman (1992), p. 438.‘°SeeMcCallum (1989), pp. 285-88, for an explanation of the

limitations on monetary policy under a fixed exchange ratesystem.

“Indeed, the primary argument in favor of a flexible ex-change rate system was that such a system would permitindividual countries to pursue independent monetary poli-cies. See, for example, Friedman (1953) and Johnson(1969).

“This is Grilli, Masciandaro and Tabellini’s finding (1991).

31

thorities in setting economic policy. A depen-dent central bank is one that cooperates withthe fiscal authority in setting policy.

ln examining the theoretical implications ofcentral bank independence, this paper focuseson models in which the policymaking process isdecentralized.” ‘The basic framework of thesemodels is as follows. The government controlsfiscal policy, and the central bank controlsmonetary policy. Both parties set goals for theeconomy (generally inflation and output targets)and assign priority to these goals. The goals andpriorities may differ across the policymakers.Each institution uses the instruments availableto it in an attempt to reach its goals. In mostmodels the central bank controls the growthr’ate of the monetary base and the governmentcontrols fiscal spending. There is an underlyingmodel of the economy that indicates how fiscaland monetary policy will affect the relevant eco-nomic variables. All of the models assume thatthere are no stochastic shocks to the economy.

The government and the central bank caneither cooperate in implementing their policiesor choose not to cooperate. If they do not co-operate, they either can set policies simultane-ously, or one party can set its policies first andthe other then adopts its policies in reaction tothese.

Consider Andersen and Schneider’s (1986) sim-ple model in which the government and thecentral bank establish targets for inflation andoutput.” ‘i’he further the actual level of outputand rate of inflation are from their respectivetargets, the more disutility each authority re-ceives. Thus, using the following equations,each authority can be modeled as setting policyto minimize its respective loss functions:”

(1) L1

= a1ly — y~’+ b1.U’r — it,.)’

(2)L,,, = a,,,(y—y,)’ +

(~)~ ~ Y~ y,,,

where~

is the fiscal authority’s loss functionL,,, is the monetary authority’s loss functiony is outputit is intlation

is the fiscal authority’s output targety~,is the monetary authority’s output tar-get

is the fiscal authority’s inflation targetTim ~5 the monetary authority’s inflation targeta is the weight placed on the output targetb is the weight placed on the inflation target

Andersen and Schneider compare the economicoutcomes under cooperation vs. noncooperationgiven three different models of the economy.‘The first model is Keynesian in nature. This is ashort-run model with price sluggishness so thateven anticipated changes in policy affect ag-gregate demand. The level of output and therate of inflation prevailing in the economy areaffected by both fiscal and monetary policies,which can he shown in a simple reduced formmodel with the following equations:where f is the fiscal policy instrument and m isthe monetary policy instrument.”

(4)y = y,f+ y,mn 0<y,<y0

(5) it 9,,f + Ow

in the second model, which Andersen andSchneider refer to as Keynesian-New Classical,anticipated monetary policy is neutral; it can af-fect only inflation. Thus in a world of certainty,equation (4) becomes the following:

(6) y =

(7) it =r~f+ in

“There have been studies concentrating solely on monetarypolicy that have shown that better economic outcomesresult from the policymaker placing a greater weight on in-flation than society as a whole. Rogoff (1985) argues thatthese results indicate the economic benefits of centralbank independence. These studies ignore the interaction offiscal and monetary policy in determining economic out-comes and thus are not discussed here.

“Generally it is assumed that the government places moreweight on meeting its output target than its inflation target,whereas the opposite holds for the central bank. Further-

more, it is generally assumed that the inflation and outputtargets set by the government are greater than or equal tothe targets set by the central bank,

“The quadratic nature of the loss functions, which is stan-dard in the macroeconomic game theory literature, impliesthat deviations on either side of the targets produce anequal loss to the policymaker.

“The restrictions in equations (4) and (5) imply that fiscalpolicy has a greater (lesser) effect on output (inflation) thandoes monetary policy.

In the third model, the economy is New Classicalin nature, characterized by perfect price flexibi-lity and national expectations. Anticipated policy,

a1 b1 both fiscal and monetary, affects only inflation,not output. The economy is modeled by the fol-

b,, a,,, lowing equations:

32

(8) y = it — it’

(9.) it — = !7Jff~+

where y now refers to output relative to capaci-ty and the superscript e refers to the expecta-tion of the variable. Output can be increasedabove capacity only tht-ough unanticipated infla-tion, and unanticipated inflation can occur onlythrough unanticipated changes in fiscal policy,monetary policy or both.

The relevant issue for policy is the size of theloss to each policymaker under cooper’ation andnoncooperation. Cooperation in the determina-tion of monetary and fiscal policies is modeledby the government and the central bank choos-ing the policy variables (f and m) to minimize aweighted average of their loss functions:

(10) win L = pL1 + (i’~~P)Lm

f,m

+ (1— p)[am(—j~)’ + bm(it —it,,,)’],

where the weight placed on each loss functionis determined by the relative bargaining strengthof the two parties. Solving this minimizationproblem yields the equilibrium values for outputand inflation, which can he substituted into theloss functions for the governmnent, equation (1),and the central bank, equation (2), to determinethe loss to each.

As noted ahove, noncooperation can he mnodel-ed in two ways. in the first, fiscal and monetarypolicies are chosen simultaneously; that is, thegovernment selects a level of spending to mini-mize its loss function, equation (T), taking asgiven the actions of the central bank. At thesame time, the central bank chooses the growthrate of the monetary base to minimize its lossfunction, equation (2), taking as given the actionsof the government. This structure is referred toas a Nash game and the resulting equilibrium iscalled a Nash equilibrium. In a Nash equilibrium,neither authority, taking the actions of the otheras given, can decrease its loss by unilaterallychanging its policy.

In the second model of noncooperation, onepolicy is set before the other is determined.This process is known as a Stackelberg game,and the policvmaker who moves first is known

as the Stackelberg leader, whereas the otherpolicymaker is known as the Stackelherg follow-er. The leader chooses its policy, and the fol-lower sets its policy in reaction. Furthermore,the leader, in choosing its policy, knows howthe follower will react.

Although the equilibrium level of output andthe rate of inflation vary depending on whichmodel of the economy is used, in all threemodels the cooperative solution is Pareto superi-or to the noncooperative solution. This result isinvariant to the structure of noncoopet’ation—Nash or Stackelherg. The performance of theeconomy is better under cooperation in thesense that the losses to the government and thecentral hank are each lower than they are un-der noncooperation. This result holds even ifthe government and the central bank each placethe same weight on meeting their inflation tar-

O p i gets relative to their output targets (a1=a,,, andb1=h,,,) hut maintain different targets.

Andersen and Schneider summarize theseresults by noting the following:

When we have two independent authoritieswho act in their own selfish interest, then wequite often observe a conflict over the “right”policy direction. This result should he kept inmind when quite often the argument is put for~ward that an independent monetary authorityshould be created Two independent policy-makers do not automatically guarantee a policyoutcome which is preferred to other outcomesunder different institutional solutions.’~

Alesina and ‘i’abeflini (1987) show that addingone more target to the loss functions of thegovernment and the central hank also does notchange the nature of the results. Noncooperationis once again suboptimal.

Adding a time dimension to the model alsodoes not change the basic result that coopera-tion can improve the outcome from the per-spective of both policymakers. Pindyck (1976)presents one of the first dynamic modelsanalyzing the strategic interaction of monetaryand fiscal policy. He argues that the

separation of monetary and fiscal control mayconsiderably limit the ability of either authorityto stabilize the economy, particularly when theconflict over objectives is at all significant.”

Petit (1989) examines the issue of policy coor-dination in a continuous time model. The

= p[a~y-y~’+

‘7See Andersen and Schneider (1986), p. 188. “See Pindyck (1976), p. 239.

33

government sets targets for output and inflation,giving higher priority to output. The centralbank targets inflation and the level of interna-tional reserves, giving higher priority to infla-tion.” As is standard, the government sets thelevel of public expenditures to minimize its lossfunction, whereas the central hank sets thegrowth of the monetary base to minimize itsloss function.

In this model, policies are set at the beginningand are unchanged over the period considered.Once again, cooperation is Pareto superior to theNash and the Stackelherg equilibriums. Further-more, cooperation in this dynamic system leadsto a decrease in the variability of the targets(particularly prices and international reserves),and raises the speed of adjustment of the sys-tem. The latter indicates that, given a shock tothe system, the economy will return morequickly to its long-run values of output and in-flation if the government and the central hankare coordinating their policies. Thus Petit con-chides that policymakers should coordinate theirpolicies.”

Other studies concentrate on the interactionof the government and the central bank infinancing fiscal deficits where the deficit mustbe financed through bonds, seignorage orboth.’’ Under the assumption that there is somelimit on the ability of a government to continu-ally issue bonds to finance its deficit, the needfor inflation revenues becomes important.~’Sar-gent and Wallace (1981) conducted the seminalresearch on this question and showed that ifthe government embarks on a path of unsus-tainable deficits, the central hank might eventu-ally he forced to inflate to fund the deficits. Ifthe public realizes that the government debt ison such a path, it will expect inflation to in-crease, which may cause inflation to increase

well before the debt limit has been reached.”This outcome is a result of the government be-ing able to set its policies and the central bankhaving to react to those policies (a Stackelherggame).”

En general, a con flict over the public debt canarise at any time when the government and thecentral hank are allowed to adopt independentpolicies. Tahellini (1986) develops a dynamicmodel in which the central bank sets targets forchanges in the monetary base and the stock ofoutstanding public debt while the governmentsets targets for’ the fiscal def’icit net of interestpayments and the stock of outstanding publicdebt. The target value of public debt is thesame for both authorities. In choosing the levelof the monetary base and the fiscal deficits, thetwo authorities are constrained by the govern-ment’s d namic budget constraint.” The stockof public debt as a proportion of income is con-sidered too high by both the fiscal and mone-tary authorities. In the noncooperative setting,however’, each authority ignores the benefit tothe other of its own actions to reduce the levelof debt. In the cooperative setting these benefitsare internalized, resulting in a lower level ofdebt.

‘I’ahellini (1987) and Loewy (1988) provide twomore examples of models examining the conflictbetween central banks and governments overfiscal policy. Both show that such a conflict canlead to an increase in government debt. As not-ccl by Blackburn and Christensen (1989), a con-flict will always arise between a central bankwhose goal is to maintain price stability and agovernment whose objective is to increase out-put and is pursuing this goal by running astream of large deficits. Such a macroeconomic

program is infeasible; one party will have to re-vise its strategy (give in). The conflict creates

“The target for international reserves reflects a balance ofpayments objective.

40Hughes Hallett and Petit (1990) also model the interactionof fiscal and monetary policy in a dynamic setting, reach-ing this same conclusion.

“Seignorage is the revenue received from the creation ofmoney. It occurs because base money costs only a fractionof its face value to produce.

“As the public debt grows, there may be increasing concernamong bondholders that the government will be unable torepay the bonds,

“As Sargent and Wallace note, if money demand today de-pends on inflationary expectations, then the price level to-day is a function of not only the current money supply, butalso expectations of the future levels of the money supply.

“The concern that undisciplined fiscal policies could resultin inflation was recognized by the EC in drafting the Treatyon European Monetary Union. In the regulations concern-ing the proposed European Central Bank, the bank is pro-hibited from financing fiscal deficits of the membercountries.

As pointed out by Sargent and Wallace, and expoundedon by Darby (1984), the need for the central bank to mone-tize government debt through an inflationary policy isbased on the assumption that the rate of growth of the realeconomy is less than the real rate of interest,

“Note that monetary base and fiscal deficits in this modelare both instruments and targets.

34

problems for the economy because of the un-certainty over the future course of policy: thepublic can expect higher inflation or higher tax-es, depending on which policymaker gives in.~’

EVALUATION OF THETHEORETICAL LITERATURE

The theoretical studies indicate that noncoor-dination of fiscal and monetary policies willresult in a suboptimal economic performancefrom the perspective of both the governmentand the central bank. Policy targets are moreclosely met when coordination occurs. Thus anindependent central bank is not conducive toachieving better policy outcomes.

However, the theoretical work, like the empir-ical studies, has its weaknesses. One criticism isthat the models are too simplistic. Neither thepreference structures of the two authorities,nor the models of the economy, are completelyspecified. Furthermore, most of the modelsoperate in a world of certainty. Policy, however,is not made in a world of certainty. Extrinsicuncertainty—shocks to the economy—can drivea wedge between the implementation of policyand its outcome. Intrinsic uncertainty—lack ofknowledge of the preferences of a policymaker—is incorporated only in Tabellini and Loewy’smodels.” As these two models illustrate, addinguncertainty can increase the policy conflict be-tween an independent central hank and fiscalauthority.

in addition to assuming certainty, the modelsalso omit one important player in these policygames—the public. Public perception of thecredibility of a macroeconomic program is im-portant to its results because the public canlimit the ability of policymakers to take advan-tage of an inflation/output tradeoff. If an in-dependent central bank can increase the publicperception of the credibility of policy, this inturn should produce better economic results.”

Another deficiency of this literature is itsfailure to address the feasibility of the policymak-ers’ goals. The output goals set by the govern-

ment, for example, may not be sustainablewithout accelerating inflation. Tax and expendi-tures plans, which lead to a stream of deficits,may also raise questions about the sustainahilityof fiscal policy. In this environment, an indepen-dent central bank could he useful if its crediblecommitment to price stability forced the govern-ment to evaluate the sustainahility of its policygoals. In contrast, centralization of policiesmight reduce the long-run economic perfor-mance of a country when the government’s fo-cus is short-run performance.

CENTRAL BANK INDEPENDENCEAND THE ECONOMY—WHAT DOWE KNOW?

This paper began with two questions: Why isthe idea of an independent central bank as pop-ular as it is? Are there economic bemiefits to begained fromn having an independent central bank?Unfortunately, the empirical and theoreticalstudies surveyed do not provide cleat- answers.The empirical studies find that there is a nega-tive correlation between central bank indepen-dence and long-run average inflation. They alsoshow a negative correlation between indepen-dence and long-run average government deficitsas a percent of GDP. In general, they find noevidence of a positive correlation between out-put growth amid central bank independence.These results all point in the same dim’ection yetdo not provide unequivocal evidence that an in-dependent central hank will lower inflation andgovernment deficits and raise a country’soutput.

In sum, these empirical studies provide evi-dence of a negative correlation between centralhank independence and inflation and centralbank independence and fiscal deficits, but theydo not provide evidence of causality. Countrieswith an aversion to inflation may formalize thisaversion through the creation of an independentcentral bank. If this is true, it is the inflationaversion, not the independence of the centralhank, that is the primary causal factor behindthe low inflation result. ‘the empirical measuresthemselves are biased toward the finding that

“A government may adopt a strategy of running deficits,through decreasing taxes, to force future governments tocut expenditures. Under this strategy, the governmentwould prefer an independent central bank, which will re-fuse to monetize the deficits and thereby increase thelikelihood that fiscal spending wilt be reduced. See Sargent(1985) for a discussion of this type of strategy.

“See Tabellini (1987) and Loewy (1988). In Tabellini’s modelthe government is initially unaware of the preferences ofthe central bank. In Loewy’s model both parties are initiallyunaware of the preferences of the other,

“This issue has been studied in the literature that focusesonly on monetary policy. See Blackburn and Christensen(1989) for a survey of this literature.

35

independence promotes low inflation. This is he-cause the measun’es place much weight on legalrequirements that a central hank pursue pruestahility and place this goal above all others.Cukierman is explicit in stating that his measureof independence:

is not the independence to dm~anything that thecentral bank pleases. It is rather the ability’ ofthe hank to stick to the price stability objectiveeven at the cost of other si,ort~termnreal ohjec-I t’,’es.”

Given such a definition of independence, it isnot sur’pm’ising that independence is equatedwith low inflation.

Theoretical studies indicate that an indepen-dent central hank can increase policy conflictswith the government whenever the preferencesof the two differ and, in so doing, worsen theeconomic performance of a country. Thesestudies, however, do not provide overwhelmingsupport for the idea that countries should placemonetary policy in the hands of the executive orlegislative branches of government. The simplestructure of these models ignores some factorsthat affect the outcome of policy decisions—for example, the role of the public and theoverall credibility of policy. Central bank in-dependence may enhance credibility and thusthe overall effectiveness of a policy program.

in sum then, in the empirical studies, empha-sis on price stability and freedom to pursue thisgoal are primary determinants of independence.In the theoretical studies independence is eq-uated with noncooperation between the fiscaland monetary authorities in policy implementa-tion. These different definitions of indepen-dence may partly explain the different results.Furthermore, countries that may he classified asindependent using the empirical definition mnayhe classified as dependent using the theoreticaldefinition. New Zealand is one such example.The 1989 Reserve Bank of New Zealand Actmade price stability the only goal of the centralbank, and the central hank is ft-ce to adopt poli-cies to achieve that goal. Thus according to theempirical definition of independence, the 1989act created an independent central hank in NewZealand. The central hank’s inflation target,hoivever, is established by the government for amulti-year period. The governor’ of the centralhank signs an agreement pledging the bank toadopt policies to meet this target. Such coopera-

tion hetween the monetary and fiscal policy-makers is consistent with a dependent centralhank in the theoretical models.

Altogether these studies indicate that we arefar from fully- understanding the role of centralbank independence in producing favorahie eco-nomnic outcomes.

REFERENCES

Alesina, Alberto. “Macroeconomics and Politics,” in StanleyFischer, ed, NBER Macroeconomics Annual (MIT Press,1988), pp. 13—52.

_______ and Lawrence H. Summers, “Central Bank In-dependence and Macroeconomic Performance: SomeComparative Evidence,” Journal of Money Credit and Bank-ing (May 1993), pp. 151—62.

_______ and Guido Tabeltini. “Rules and Discretion withNoncoordinated Monetary and Fiscal Policies,” EconomicInquiry (October 1987), pp. 619—30.

Andersen, Torben M., and Friedrich Schneider. “Coordinationof Fiscal and Monetary Policy Under Different InstitutionalArrangements,” European Journal of Political Economy(February 1986), pp. 169—91.

Aufricht, Hans, Central Banking Legislation (InternationalMonetary Fund, 1961).

Bade, Robert, and Michael Parkin. “Central Bank Laws andMonetary Policy,” unpublished manuscript, University ofWestern Ontario, 1985.

Berry, John M. “More Independence Means Lower Inflation,Studies Show[ The Washington Post (February 17, 1993).

Blackburn, Keith, and Michael Christensen, “Monetary Policyand Policy Credibility: Theories and Evidence,” Journal ofEconomic Literature (March 1989), pp. 1—45.

Buchanan, James M., and Richard E. Wagner. Democracy inDeficit (Academic Press, 1977).

Capie, Forrest H., Terence C. Mills, and Geoffrey E. Wood.“Central Bank Dependence and Inflation Performance: AnExploratory Data Analysis,” Centre for the Study of MonetaryHistory, City University Business School, Discussion PaperNo. 34 (March 1992).

Committee of Governors of the Central Banks of the MemberStates of the European Economic Community. AnnualReport 1992 (April 1993).

Cukierman, Alex. Central Bank Strategy, Credibility and In-dependence: Theory and Evidence (MIT Press, 1992).

_______ Steven B. Webb, and Bilin Neyapti. “Measuringthe Independence of Central Banks and Its Effect on PolicyOutcomes,” The World Bank Economic Review (September1992), pp. 353—98.

________ Pantelis Kalaitzidakis, Lawrence H. Summers, andSteven B. Webb. “Central Bank Independence, Growth, In-vestment, and Real Rate’ Carneg/e-Rochester ConferenceSer/es on Public Policy (autumn 1993).

Darby, Micftael R. “Some Pleasant Monetarist Arithmetic:’Federal Reserve Bank of Minneapolis Quarterly Review(spring 1984), pp. 15—20.

De Long, J. Bradford, and Lawrence H. Summers. “Macro-economic Policy and Long-Run Growth,” Federal ReserveBank of Kansas City, Economic Review (fourth quarter1992), pp. 5—30.

“See Cukierman (1992), p. 370.

36

Friedman, Milton. “The Case for Flexible Exchange Rates:’in Milton Friedman, ed, Essays in Positive Economics(University of Chicago Press, 1953), pp. 157—203.

Grilti, Vittorio, Donato Masciandaro, and Guido Tabellini. “Po-litical and Monetary Institutions and Public Financial Poli-cies in the Industrial Countries:’ Economic Policy 13(October 1991), pp. 341—92.

Hughes Hallett, Andrew and Maria Luisa Petit. “Cohabitationor Forced Marriage? A Study of the Costs of Failing toCoordinate Fiscal and Monetary Policies:’ Weltwirtschaft-liches Archiv (1990), pp. 662—89.

Johnson, David R., and Pierre L. Siklos. “Empirical Evidenceon the Independence of Central Banks:’ unpublishedmanuscript, Witfrid Laurier University (March 1992).

Johnson, Harry G. “The Case for Flexible Exchange Rates,1969,” this Review (June 1969), pp. 12—24.

Loewy, Michael B. “Reaganomics and Reputation Revisited:’Economic Inquiry (April 1988), pp. 253—63.

Masciandaro, Donato and Guido Tabeltini, “Monetary Regimesand Fiscal Deficits: A Comparative Analysis:’ in H. Cheng,ed. Monetary Policy in the Pacific Basin Countries (KtuwerAcademic Publishers, 1988), pp. 125—52.

McCallurn, Bennett T Monetary Economics: Theory and Policy(MacMillan, 1989).

Parkin, Michael. “Domestic Monetary Institutions andDeficits,” in J, M. Buchanan et al,, eds. Deficits (BasilBlackwelt, 1987), pp. 310—37.

Petit, Maria Luisa. “Fiscal and Monetary PolicyCo-ordination: ADifferential Game Approach,” Journal of Applied Economet-rics (April-June 1989), pp. 161—79.

Pindyck, Robert S. “The Cost of Conflicting Objectives inPolicy Formulation,” Annals of Economic and Social Meas-urement (May 1976), pp. 239—48.

Rogoff. Kenneth. “The Optimal Degree of Commitment to anIntermediate Monetary Target,” Quarterly Journal of Eco-nomics (November 1985), pp. 1169—90.

Sargent, Thomas J. “Reaganomics and Credibility,” in AlbertoAndo et at, eds., Monetary Policy in Our Times (MIT Press,1985), pp. 235—52.

Sargent, Thomas J., and Neil Wallace. “Some UnpleasantMonetarist Arithmetic,” Federal Reserve Bank of Minneapo-lis, Quarterly Review (tall 1981), pp. 1—17.

Summers, Robert, and Alan Heston. “The Penn World Table(Mark 5): An Expanded Set of International Comparisons,1950—88:’ Quarterly Journal of Economics (May 1991),pp. 327—68.

Tabellini, Guido, “Money, Debt and Deficits in a DynamicGame’ Journal of Economic Dynamics and Control(July 1986), pp. 427—42.

“Central Bank Reputation and the Monetization ofDeficits: The 1981 Italian Monetary Reform:’ Economic In-quiry (April 1987), pp. 185—200.