cecl implementations gather steam amid uncertainty › content › dam › advisory › ... · kpmg...

TRANSCRIPT

kpmg.com

KPMG CECL survey 2017

CECL implementations gather steam amid uncertainty

1FASB Accounting Standards Codification Topic No. 326 Financial Instruments – Credit Losses

KPMG LLP (KPMG) surveyed banks, insurers, and specialty finance companies in June of 2017 to assess progress toward implementation of the Current Expected Credit Loss (CECL)1 standard and to gain insights into the issues and concerns of the institutions affected. Overall, the results show progress toward implementation, but widespread uncertainty regarding key decisions concerning accounting, modeling, and data inputs has slowed overall implementation efforts.

U.S. Financial Instruments Accounting Change Leader Reza van Roosmalen notes that in large measure this uncertainty stems from the open-ended nature of the CECL standard. “There is a lot of optionality in this standard, and implementing CECL requires companies to put their stake in the ground and build their processes around it.” But he notes it’s not very often for a U.S. generally accepted accounting principle or GAAP standard to enable institutions

to pursue their own unique path to compliance. Thus, the high degree of judgment requires up-front involvement and management decision making.

This concern is not without effect. For most public companies, CECL becomes mandatory in January 2020. While this may seem like a long way off, the reality is that time is precariously short for implementing such a far-reaching standard. Van Roosmalen says CECL comes at a time when many financial institutions—following years of regulatory directives in the wake of the financial crisis—have outdated finance and risk systems. “For many, this means the CECL implementation requires a large, transformational investment in risk and accounting

software without a firm grasp of exactly what needs to be built. So in this regard, the openness of the CECL standard is slowing, if not stalling, implementations.”

One likely outcome is a rush to the finish line for the implementation of CECL, especially among smaller institutions. As a comparison, IFRS (International Financial Reporting Standards) 92, which is the parallel standard promulgated by the International Accounting Standards Board (IASB) and set for implementation beginning 2018, may offer some insights. Commenting on the results of a February 2017 survey of banks, the European Banking Authority (EBA) said, “Although the smaller banks in the sample have advanced significantly in the implementation of IFRS 9 since the previous EBA exercise, they are still lagging behind in their preparation compared with larger banks in this sample.”

We completed our survey in June, 2017 and the results reflect input from 130 companies in the financial services industry. Among the institutions that participated were 98 banks, 28 insurers, and 17 specialty finance companies.3 These institutions were categorized into four groups: less than $10 billion in assets, $10 billion to $49.9 billion in assets, $50 billion to $200 billion in assets, and more

than $200 billion in assets. A variety of professionals participated in the survey including C-suite executives in accounting, finance, and risk as well as vice presidents in these same disciplines along with controllers and treasurers.

The breakdown of results by title was, in our view, important because it enabled us to identify areas within organizations where the thinking regarding CECL implementation converged and where it diverged. For instance, it appears the downstream effect of CECL implementation on items such as

regulatory capital or income volatility were consistently ranked as having a greater potential impact by risk personnel than by finance or accounting staffers.

Overall, we view CECL as not just an accounting change, but a fundamental shift in how financial services companies measure and manage credit risk. As such, the many impacted parties that span the enterprise will need to come together to address the challenges

in a targeted way to ensure all concerns are addressed.

The balance of this paper summarizes some of our findings in key areas and some of our insights from these findings.

2International Financial Reporting Standard No. 9 Financial Instruments (Issued July 2014) 3130 companies were surveyed, but responses were greater due to questions with multiple responses

Overall, we view CECL as not just an accounting change, but a fundamental shift in how financial services companies measure and manage credit risk.

At what stage is your CECL project currently?

May not equal 100% due to rounding | n: Total = 130, Banking= 98, Insurance = 28, Specialty Finance = 17

2KPMG CECL Survey 2017

AccountingWe observed decision-making paralysis take hold among institutions that were implementing IFRS 9, and this paralysis put pressure on deadlines and threatened the success of the accounting change at large.

Paralysis with respect to CECL is likely, though at this juncture it is difficult to project how widespread this paralysis may be. As a standard, CECL is open ended and already we are seeing divergence in its adoption. As of yet, no consensus views exist yet on almost all key CECL decisions. For instance, in response to the question, “What is the most important CECL accounting decisions to make/that you have made

at this point in time?,” 30 percent of all respondents answered that they were not sure, which may indicate a delayed response in decision making.

Among banks, many had yet to identify commitments where the unfunded amounts are unconditionally cancelable, a key CECL variable. For instance 68 percent of institutions with assets between $10 and $49.9 billion had not identified these commitments, or were not sure. For banks with assets between $50 and $200 billion, 42 percent answered no or not sure. And 64 percent of banks with assets greater than $200 billion had not identified these commitments, or were not sure.

Has your company identified commitments where the unfunded amounts are unconditionally cancelable?

May not equal 100% due to rounding n: Total = 130, Less than $10B = 57, $10B to $49.9B = 35, $50B to $200B = 24, Over $200B = 14

By company size

We found these results to be surprising given a similar analysis is required under the Basel III standard which many of these banks already comply with. We believe these results may reflect a smaller sample size of the larger banks in our survey. But sample size aside, the high percentage of $200 billion-plus institutions that had not identified unfunded amounts that were unconditionally cancelable suggests the CECL steering committee may not have connected yet with the other areas of the organization that are doing the same or similar work, and which ultimately will need to be drawn into the CECL implementation.

In total, the results indicate a lack of preparedness for early adoption because a number of key decisions have not been made, and this phenomena was observed across institutions of all asset sizes. We find this to be in contrast to what we have been hearing in the market as we met with institutions during the latter part of 2016 and first half of 2017, with most indicating at the time that they wanted to be ready for early adoption if necessary. Not surprisingly though, if institutions have yet to make key accounting decisions that will shape the modeling, data needs, and system and process decisions downstream,

time is starting to run out on being able to meet the demands of early adoption.

As a result, we now believe a small percentage of institutions will early adopt. The largest percentage by far, will use a portion of, but not all of 2019 to run some form of dress rehearsal. This time frame means that the remainder of 2017 and early in 2018 will be a critical time for making important accounting-related CECL decisions to allow for design, build, and implementation of the process to facilitate some level of parallel testing prior to adoption.

With respect to accounting decisions, we believe the high degree of judgment requires up-front involvement and timely decision making. The open-ended nature of the CECL standard means that rather than getting the “right” answers on complex accounting and valuation matters, as historically determined by comparing a company’s accounting conclusion to prescriptive guidance in the accounting literature, organizations will need to focus energy on putting together thoughtful robust documentation that supports the decisions made along with the underlying process and judgments used to arrive at these decisions.

For the Current Expected Credit Loss model, is your company:

May not equal 100% due to rounding | n: Total = 130, Less than $10B = 57, $10B to $49.9B = 35, $50B to $200B = 24, Over $200B = 14

By company size

4KPMG CECL Survey 2017

InfrastructureThe systemic shift in monitoring and reporting brought on by CECL raises important infrastructure issues for financial services organization. In particular, smaller institutions may need to consider their data and system capabilities in complying with the CECL standard, while larger institutions will want to determine how to leverage infrastructure that has been put in place in response to far-reaching regulation and rule making over the past 8 to 10 years.

Regarding this latter point, survey results show that as institution size increases, by asset size, they tended to speed up the amount of time it takes to complete their Allowance for Loan and Lease Losses (ALLL) reporting. But only to a point. Institutions with assets in excess of $200 billion reported longer processing times when compared to institutions with less than $200 billion in assets.

How long does it take to produce the ALLL report for financial reporting with your present systems?

May not equal 100% due to rounding n: Total = 130, Less than $10B = 57, $10B to $49.9B = 35, $50B to $200B = 24, Over $200B = 14

By company size

We believe these longer time frames for larger institutions are not due to a lack of investment in infrastructure, but rather to the complexities that are part and parcel of achieving their size: acquisitions, geographically and systemically diverse operations, and product expansion. Accordingly, we feel that the preparation leading up to the CECL transition may require institutions with more than $200 billion in assets to consider a review and reengineering of their current finance and risk integration architecture and infrastructure and consider new tools, technologies, and automation aspects to improve their efficiency.

Some banks use a time lag in their data inputs today in order to be able to meet ALLL reporting deadlines. With CECL being more data intensive and more complex, it is possible that some banks may need to increase the lag to try to manage reporting deadlines. This should be a key concern for management when

assessing the impact of CECL on financial reporting as we expect that without significant change, institutions that already have a highly demanding reporting schedule due in part to ALLL, could find that CECL may put reporting deadlines in jeopardy.

The survey results also indicated that many smaller institutions with assets less than $50 billion may not yet recognize the reporting period data lag that may materialize when producing CECL reporting versus the current ALLL reporting. But with CECL, forecasting is required, and by definition, this introduces the need for additional and/or external data. However, with none of the survey respondents at institutions smaller than $10 billion assets anticipating any increase in lag for CECL reporting, it suggests they are not yet focusing on this infrastructure element of the overall CECL reporting implementation.

Do you expect to continue with a lag on future forecasting processes?

May not equal 100% due to rounding n: Total = 55, Less than $10B = 21, $10B to $49.9B = 13, $50B to $200B = 14, Over $200B = 7

By company size

6KPMG CECL Survey 2017

DataOur expectation is that banks have data quality issues of varying severity, which was reflected in the survey results. Respondents all noted issues relating to data reliability, completeness, or both.

Specifically, 54 percent of respondents in banking, insurance, and specialty finance expressed some degree of doubt regarding the completeness or

reliability of their historical data and 15 percent had not yet evaluated their data. A starting point for addressing data quality issues would be to build a CECL data dictionary with the list of critical data elements needed for CECL accounting, modeling, and disclosure reporting along with identification of requisite quality controls.

Which of the following best describes the data quality of your future CECL source system(s)?

May not equal 100% due to rounding n: Total = 130, Banking = 98, Insurance = 28, Specialty Finance = 17 8KPMG CECL Survey 2017

The survey results indicate that the institutions plan to use multiple data sources to meet CECL modeling and reporting obligations. While the institutions have a consensus on the need of consolidated risk and finance data information to support CECL implementation, the implementation approach would vary from using a single data warehouse to using multiple data warehouses. Among all financial institutions, 35 percent intend to use multiple source systems and just 6 percent anticipate deploying single source systems. The remaining 59 percent are looking at new data structures for CECL reporting or considering single and multiple data warehouse

architectures. The survey results indicate that the institutions continue to approach the CECL data requirements in a generic way by focusing on the implementation of a risk data warehouse to support modeling needs. In looking at the data, one could interpret that the institutions are not doing a holistic data impact assessment for specific CECL requirements, such as addressing reasonable and supportable economic forecasts, reversion to historical information, accounting system attributes to report asset values, and supporting new credit decision reporting as per CECL methodology.

Which of the following describes your existing data source(s) for use as future CECL inputs? (select all that apply)

n: Total = 130, Banking = 98, Insurance = 28, Specialty Finance = 17

This intention implies that CECL data models need to be reengineered to account for data integration from multiple source systems as well as ensuring consistent definitions and tight integration between risk and finance data. Tools and systems supporting the data integration and consumption from this model need to be evaluated for scalability and performance.

Survey results show the asset level historical data availability is more deficient in the short term than

in the longer term. Specifically, only 8 percent of banks, insurance and specialty finance companies had asset level data for periods of one to three years that could be used for CECL loss projections. Another 50 percent had data for four to nine years while 32 percent had asset level data for periods longer than 10 years. These results notwithstanding, our expectation is that data quality varies inversely with age and this is a critical concern for banks.

Over what historical time period does your institution currently maintain asset level data which could be used as part of the CECL loss projection calculations? (if multiple answers apply, please select the option that encompasses most of your portfolio)

In light of this, most institutions would benefit from a gap analysis of the amount of current and historical data and specific elements required for CECL compared to what their data systems contain today. Further, for institutions where historical data is not available, there will be a need to supplement data with relevant external datasets to meet CECL

modeling requirements, a task which will take time, planning, and resources. It is also expected that the institutions design an optimal data control framework that can define the appropriate control metrics as per the institutions’ preferences regarding data intensiveness, auditability, management involvement, cost, complexity, and resulting allowance levels.

n: Total = 130, Banking = 98, Insurance = 28, Specialty Finance = 17

10KPMG CECL Survey 2017

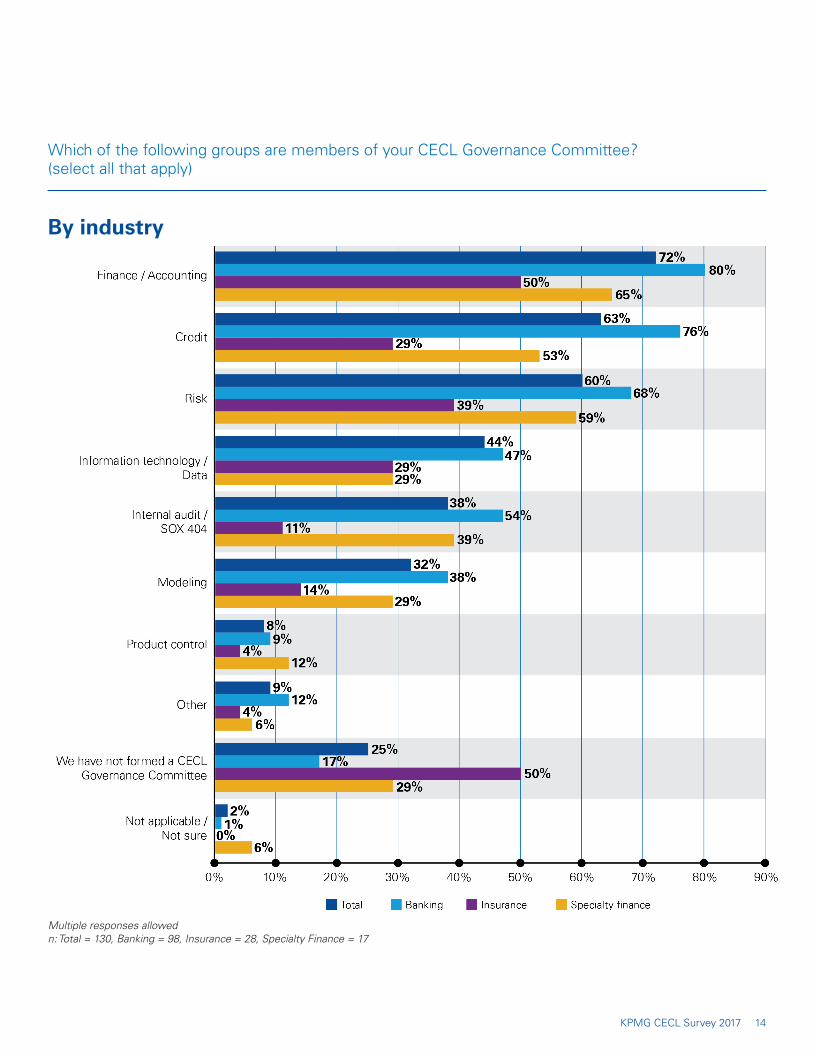

GovernanceAlignment between financial and regulatory reporting surfaced as a key issue among respondents underscoring the importance of identifying a strong leader for CECL who can be effective across boundaries and departments within an organization. In our view, a best practice would involve joint leadership between risk and accounting functions; however, one department leading with active participation from the other is also likely to be a successful formula.

Leading up to implementation, we believe a CECL governance committee represented by risk, accounting, credit, IT, IA, modeling and product control, is important, though one in four survey respondents have no such committee.

The importance of alignment was readily apparent in the survey results. Specifically, 70 percent of financial services companies intend to align CECL with internal and external reporting.

Multiple responses allowed n: Total = 130, Banking = 98, Insurance = 28, Specialty Finance = 17

Given other business uses of forecasting, will your company: (select all that apply)

12KPMG CECL Survey 2017

For banks, where CCAR and Dodd-Frank Act Stress Test (DFAST) reporting comes into play, 57 percent said they will seek to achieve alignment with regulatory requirements. We view this as significant because regulators and auditors are likely to want banks to explain how to reconcile the regulatory and financial reporting credit loss numbers. Further, banks that would like to use one model for everything (CECL and CCAR for example) will need to know which “levers” to pull in their models in order to be able to produce the right reports and disclosures.

Alignment will likely produce consistency from a governance standpoint and will likely lower governance costs as there will be less divergence to be governed, managed, and controlled. But alignment presents additional complications as well. Specifically, flexibility will need to be built into CECL processes, and this will impact time lines for implementation and

execution. Further, organizations may find themselves in a “no man’s land,” mixing perspectives and purpose between financial reporting and regulatory compliance.

Also notable among the governance related survey results was the role of Internal Audit in CECL implementation to date. Combined, IA was a member of the CECL governance committee just 38 percent of the time among financial services companies. Insurance companies exhibited the lowest IA participation at just 11 percent, while the banks had the highest IA participation at 47 percent. When looked at by asset size, institutions with assets over $200 billion had the lowest participation by IA on the CECL governance committee at 21 percent, and institutions between $10 billion and $50 billion exhibited the highest at 49 percent.

Which of the following groups are members of your CECL Governance Committee? (select all that apply)

By industry

Multiple responses allowed n: Total = 130, Banking = 98, Insurance = 28, Specialty Finance = 17

14KPMG CECL Survey 2017

The low IA participation rate on CECL governance committees may be indicative of the tendency to de-emphasize controls during the implementation process. However, the complexity of CECL merits the inclusion of IA earlier than might otherwise prevail in accounting and modeling decisions to facilitate efficient and effective IA procedures later.

If you have estimated the total cost of the CECL accounting change from assessment through to implementation, what is the total budget? (Total budget should reflect internal and external costs)

May not equal 100% due to rounding | n: Total = 130, Less than $10B = 57, $10B to $49.9B = 35, $50B to $200B = 24, Over $200B = 14

By company size

16KPMG CECL Survey 2017

ModelingAs banking institutions intensify their CECL implementations, the shortcomings of relying on regulatory models for financial reporting are becoming increasingly apparent. For example, CCAR and DFAST focus on the adequacy of capital and the ability of banks to withstand economic stress and are based on scenarios provided by regulators. In contrast, loss forecasts under CECL are meant to reflect management’s estimate based on current conditions and reasonable and supportable forecasts.

While in most cases model selection has not been made, just over half, or 52 percent of institutions will leverage existing ALLL models as their starting point for building CECL models. Small banks were more likely to rely on their existing ALLL framework for CECL, which is consistent with our expectations but also fraught with challenges as ALLL is an incurred loss model while CECL requires a forward-looking lifetime estimate of losses.

What is your institution’s starting point for building CECL models? (select all that apply)

By company size

Multiple responses allowed n: Total = 130, Less than $10B = 57, $10B to $49.9B = 35, $50B to $200B = 24, Over $200B = 14

If you have performed some level of quantification for the impact of CECL, by what percentage do you e xpect your existing allowance for credit losses to change when CECL becomes effective?

Among banks of all asset sizes, 40 percent reported they would rely on DFAST/CCAR models. We believe this figure may continue to drift downward over time. This is consistent with our belief that shortcomings

of relying on regulatory models for financial reporting become increasingly apparent as CECL implementations near.

Interestingly, a majority (52 percent) of all respondents stated they planned to leverage existing ALLL models. About one-quarter of respondents plan to build new models from scratch or purchase modeling capabilities. Fifty percent of respondents from insurance companies planned to use other loss forecasting models already in place, compared to just 14 percent of banking respondents, suggesting that although CECL is not a contributor to divergence, divergence in practice between industry sectors will likely continue and may even increase under CECL.

In our view, existing ALLL and other loss forecasting models may provide a useful starting point for CECL modeling, but require careful consideration to determine whether they adequately achieve the objective of estimating future credit losses.

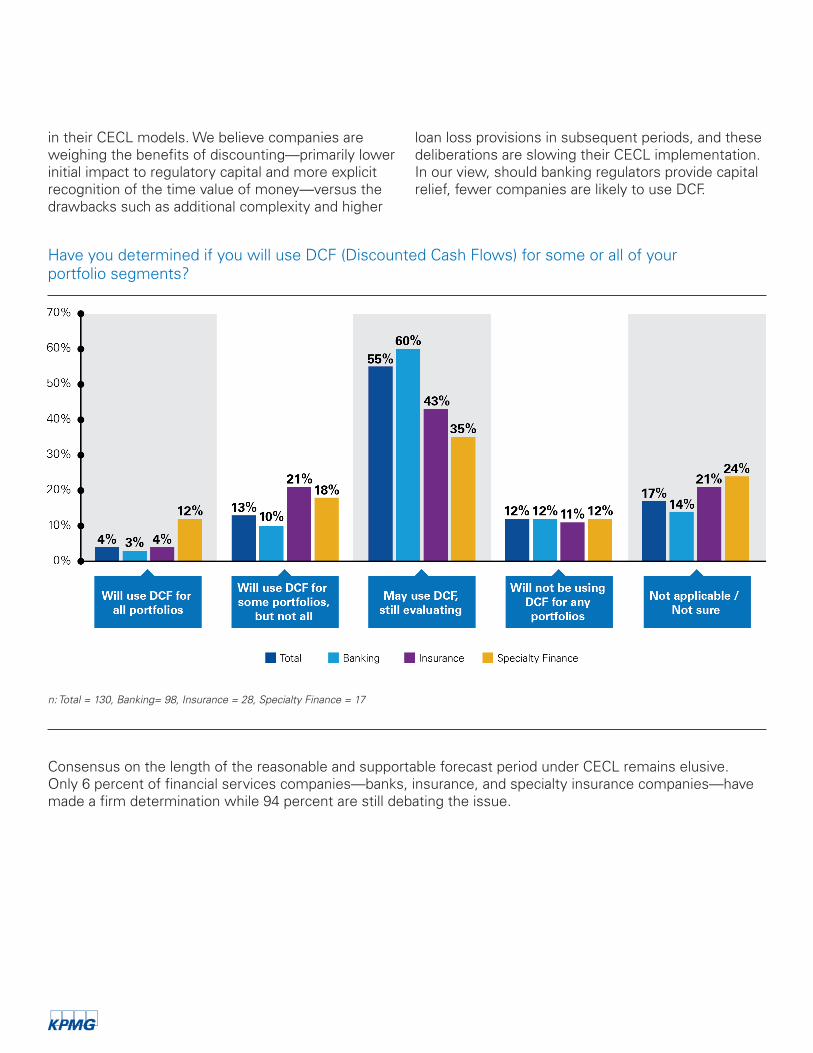

Only 4 percent of financial institutions have determined they will use discounted cash flows (DCF) for some or all of their portfolios, while 12 percent of survey responders will not be using discounted cash flows at all for CECL. Approximately 68 percent of survey respondents are evaluating the use of DCFs

May not equal 100% due to rounding n: Total = 15, Banking = 13, Insurance = 3, Specialty Finance = 4

18KPMG CECL Survey 2017

in their CECL models. We believe companies are weighing the benefits of discounting—primarily lower initial impact to regulatory capital and more explicit recognition of the time value of money—versus the drawbacks such as additional complexity and higher

loan loss provisions in subsequent periods, and these deliberations are slowing their CECL implementation. In our view, should banking regulators provide capital relief, fewer companies are likely to use DCF.

Have you determined if you will use DCF (Discounted Cash Flows) for some or all of your portfolio segments?

Consensus on the length of the reasonable and supportable forecast period under CECL remains elusive. Only 6 percent of financial services companies—banks, insurance, and specialty insurance companies—have made a firm determination while 94 percent are still debating the issue.

n: Total = 130, Banking= 98, Insurance = 28, Specialty Finance = 17

Have you determined the length of the reasonable and supportable forecast period under CECL?

Our experience, based on discussions with clients and regulators, indicates a great deal of diversity around forecasting periods. Some companies favor short time frames while others believe they can forecast for most if not all of the estimated lives of some instruments. And still others believe that DFAST/CCAR practices create a presumption that the reasonable and supportable period must be at least nine quarters.

This diversity has far-reaching consequences for the application of CECL, and decisions about the length of reasonable and supportable forecasting periods can affect both the complexity of economic models and their sensitivity to changes in current economic conditions.

Similarly, large majorities of respondents in all industries surveyed are still evaluating whether to use a single best estimate of economic conditions versus multiple economic scenarios. Also under evaluation is the manner and method in which financial institutions plan to revert to historical loss information beyond the reasonable and supportable loss period.

At this critical juncture in CECL implementation, we believe financial services companies must engage in interaction with their peers to help drive consensus. Equally productive perhaps is dialog with regulators. Their industry-wide oversight gives them a wide purview, and they can share with institutions what their peers as a group are doing and which assumptions and decisions constitute outlier positions.

n: Total = 130, Banking= 98, Insurance = 28, Specialty Finance = 17

20KPMG CECL Survey 2017

Business impacts While survey respondents are concerned about income volatility and regulatory capital and related ratios, they were generally less concerned about second order impacts such as pricing changes, balance sheet management, lending strategy, and terms and conditions.

In our view, monitoring the size of the allowance from period to period and the interrelated impact on income are the primary business impacts of the CECL standard that companies will need to address. Management will need to consider how to simultaneously comply with the CECL standard while considering CECL’s potentially negative implications to capital and period earnings volatility. The challenge of CECL will be managing these business impacts on and after adoption of CECL, and decisions made during the implementation phase will directly impact the business.

That said, the downstream impacts of CECL on income volatility and regulatory capital are top concerns for all financial institutions but for banks in particular. After all, the CECL standard creates a Day 1 allowance upon origination or acquisition of the asset and, in most cases, will dramatically increase credit losses compared to coverage levels under current U.S. GAAP. It is understandable that survey respondents expressed concern about how CECL may impact profitability and regulatory capital metrics and even how companies do business.

Overall, larger institutions seemed less concerned about the impact of CECL on regulatory capital than small institutions, with just 29 percent of institutions with assets over $200 billion expecting it to be significant. Conversely, 66 percent of institutions with

assets of $10 billion to $50 billion, and 53 percent of institutions with less than $10 billion in assets, felt the impact of regulatory capital would be significant. Since a low number of institutions responded to this particular question, one hypothesis of these results is that larger institutions believe that they are better able to absorb the potential reduction in capital ratios through existing capital buffers; smaller institutions may not believe they have the same level of cushion.

As we move closer to the effective date of CECL, some of the second-order impacts noted above will become more significant. For instance, survey respondents indicated that the impact to product

pricing is a relatively low priority at this stage. As CECL implementation efforts progress closer to adoption of the standard, pricing may become a more significant concern. Similarly, CECL may eventually cause institutions to modify terms/conditions of financial products or revise portfolio mix of certain types of products. At this stage of implementation, it is understandable that these second-order business impacts have taken a “back seat” to modeling and other implementation considerations.

Also notable among the results was an apparent dichotomy in thinking between credit risk personnel and finance/accounting personnel. In almost every downstream business impact contemplated in the survey, including income, capital and pricing, among others, a higher percentage of credit personnel ranked the impacts of CECL to be significant compared with assessment of impact by accounting/finance personnel. The only exception was asset/liability matching where finance/accounting personnel believe the impact of CECL will be more significant than did the risk personnel.

In our view, monitoring the size of the allowance from period to period and the interrelated impact on income are the primary business impacts of the CECL standard that companies will need to address.

May not equal 100% due to rounding

Where do you consider the most significant downstream business impact of CECL will be? (Rate each from 1 to 5, 1 being the least significant and 5 being the most significant)

n: Total = 130, Credit risk = 27, Finance / Accounting = 85

22KPMG CECL Survey 2017

Part of this may simply be the “nature of the beast.” After all, with more than two years until the standard’s effective date for most institutions, finance/accounting personnel may not yet be as in-tune to the significance of CECL’s impact on credit loss reserves and period profitability. Credit risk personnel may have a deeper understanding of the modeling, data, and other complexities that CECL presents, and thus may be in a better position to predict the significance of these downstream business impacts.

There is a potential risk here that the differing interpretations on the impacts of CECL within institutions between risk and accounting functions may create problems in implementation. It is critical that management leading the accounting change understand the views of different parts of the business to make an accurate determination of impacts of CECL and be able to take appropriate action to mitigate them.

John LyonsAccounting Advisory Services Director

212-954-6804 [email protected]

Authors

Michael OhlweilerNational ALLL Group Leader

716-796-6029 [email protected]

Reza van RoosmalenFinancial Instruments, Accounting Change Leader

212-954-6996 [email protected]

ContributorsScott Bain • Joe Bielecki • Brandon Isaacs • Samir Kamat • Alan Kuska Tim Pardoel • Jack Pohlman • Mike Riechers • Nilotpal Roy • Matthew Wray

KPMG: an experienced cross-functional team, a global networkKPMG’s CECL specialists combine industry knowledge and technical experience to provide companies with holistic advice on uncovering how accounting and financial reporting policies, processes, and systems will need to change to comply with the new rules.

Our global network of professionals has helped a number of companies to understand the impact of these new rules and to implement the required changes; our experience has provided us the insights into how companies in various industries will be affected and the steps that they can take now to help ease transition to the new standards.

About KPMG

How KPMG can help

Ahead-of-the-curve experience KPMG has been helping leading financial institutions with IFRS 9 expected credit loss (ECL) modeling and accounting services for the last several years, beginning with a number of U.S. clients with IFRS reporting jurisdictions. We have first-hand knowledge of industry leading practices, and real-world, practical experience helping implement the technical applications required by these new credit loss accounting changes.

We have helped identify and transform the requisite data, develop the models, design and implement the risk modeling and KPMG gCLAS accounting software, integrate the necessary systems, and identify the business impacts and strategic opportunities that CECL affords.

Please visit our website for the following:

KPMG’s suite of services per implementation phase

Technical insights and Webcast opportunities

Additional CECL thought leadership

http://cecl.kpmg.com

24KPMG CECL Survey 2017

The KPMG name and logo are registered trademarks or trademarks of KPMG International.

© 2017 KPMG LLP, a Delaware limited liability partnership and the U.S. member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in the U.S.A.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act upon such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.com/socialmedia

Some or all of the services described herein may not be permissible for KPMG audit clients and their affiliates.