2016 aicpa bank - cecl governance

TRANSCRIPT

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

National Conference on Banks &

Savings InstitutionsCECL GovernanceJeff Honeycutt, Partner Grant Thornton LLP

Dorsey Baskin, Retired Partner

AIC

PA

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Jeff Honeycutt

Partner

National Bank Audit Practice Leader

Charlotte

704.632.6812

Dorsey Baskin

Retired Partner

Dallas

214.240-5515

Meet your presentersCECL Governance

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Disclaimer

This Grant Thornton LLP presentation is not a comprehensive analysis of the subject matters

covered and may include proposed guidance that is subject to change before it is issued in final

form. All relevant facts and circumstances, including the pertinent authoritative literature, need

to be considered to arrive at conclusions that comply with matters addressed in this

presentation. The views and interpretations expressed in the presentation are those of the

presenters and the presentation is not intended to provide accounting or other advice or

guidance with respect to the matters covered.

For additional information on matters covered in this presentation, contact your Grant Thornton

LLP adviser.

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

CECL Governance

• Explain the role of TCWG in the CECL process

– Specifically focusing on TCWG's role with

regard to:

• Model risk management

• ICFR

• Ongoing monitoring of the

CECL estimation process

Objectives

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

CECL Governance

• Introduction

• Model Risk Management

• ICFR

• Ongoing Monitoring

Agenda

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

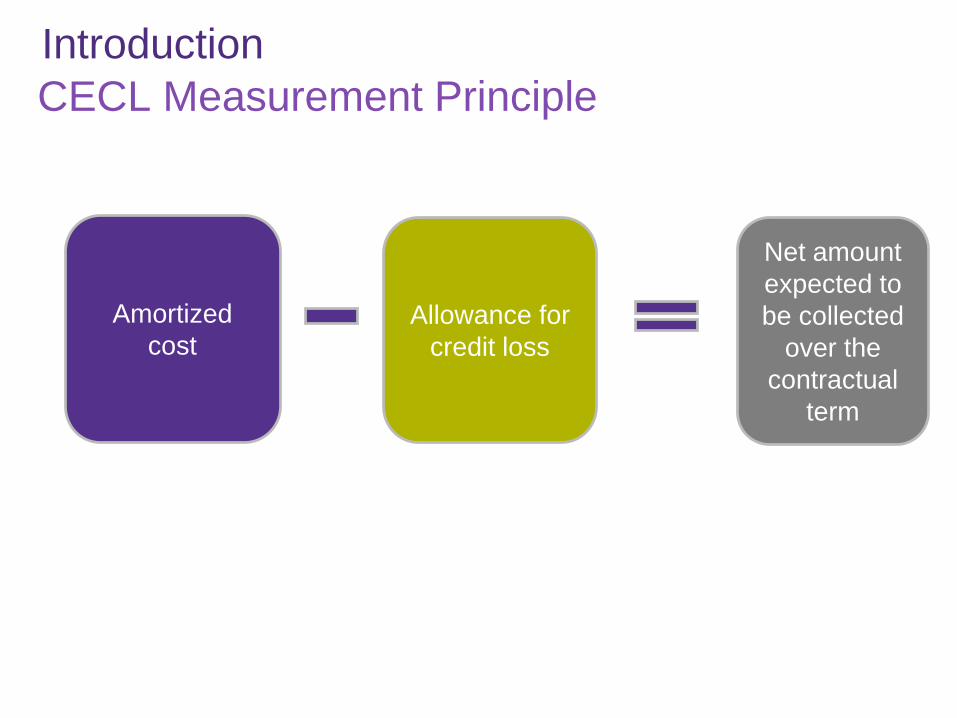

CECL Measurement Principle

Introduction

Amortized

cost Allowance for

credit loss

Net amount

expected to

be collected

over the

contractual

term

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Known losses

confirmed and

charged off

7

Introduction

The CECL model

The

allowance

for future

expected

losses

(reasonable /

supportable)

Unknown losses to the

measurement date –

for which the incurred

loss allowance is needed

Rate of lossChanging over time

Balance sheet date

Unknown future

losses –

included in the

Current Expected

loss allowance

Loan balance –

Assumes run off after

balance sheet date

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

CECL implementation processIntroduction

Scoping

• Inventory financial assets at amortized cost

• Identify primary drivers of credit risk

•Determine pools

Measurement Approaches

•For each pool, determine appropriate approach

•Necessary tools / capabilities

Data, Processes & Controls

•For each approach, determine necessary data

•Plan to get that data

• IT implications

Governance

•Steering committee

•Polices & Procedures

• ICFR

• Internal Audit

•Model Risk Management

•Role of TCWG

Engaging External Parties

•Auditors

•Regulators

•Financial Reporting

•SEC

Optimization

•Utilizing ACL information for management purposes

•Refining approach over time

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Steps to estimating CECLIntroduction

Step 1: Group financial assets with similar risk characteristics into pools

Step 2: Determine appropriate method for measuring losses

Step 3: Determine historical loss experience on the pools/asset being evaluated

Step 4: Adjust historical loss experience for current conditions and reasonable and supportable forecasts

Step 5: Revert to historical losses for periods for which reasonable and supportable forecasts cannot be made

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Introduction

• Are models used in the estimation of CECL:

•Conceptually sound?

•Fit for purpose?

•W/in risk tolerances?

•Subject to rigorous validation process?

•How do we know?

•Processes integral to CECL must be well controlled:

•Completeness and accuracy of data

• IT Governance

•Credit risk and other non-finance functional areas

•Financial reporting

•How do we know?

• Is management's CECL estimation process:

•Aligned with GAAP?

•Aligned with capital adequacy evaluation?

•Conceptually sound?

•Well documented?

•How do we know?

•Can TCWG effectively evaluate management?

•Key performance indicators

•Consistency of views on future economic conditions

•Basis for assumptions and projections

•Understand regulatory areas of focus

•How do we know? Ongoing Monitoring

Sound Design of

CECL Process

Model Risk Management

Controlled, Supported

and Disclosed

Role of TCWG in CECL

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Model Risk Management

Agenda topic

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Model Risk ManagementIn the News

12

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Model Risk ManagementEvolutionThe bar has been raised significantly with respect to the scope, formality, rigor and

prominence expected of bank's model risk management programs. A revised and

significantly expanded set of supervisory guidance was co-issued by the Federal

Reserve in April 2011 – FRB SR 11-07 and OCC 2011-2012.

Key aspects of effective model risk management is shown below:

Risk management functions through policies, procedures, allocation of resources and

mechanisms for testing so processes are carried out as specified

Disciplined standards and processes for model development, implementation and use that are

consistent with the situation and goals of the model user and with the banking organization's policy

Verification that models are performing as expected, in line with their design objectives,

business uses and regulatory guidance

Governance,

Policies and

Controls

Model

Development,

Use and

Implementation

Model Validation

13

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

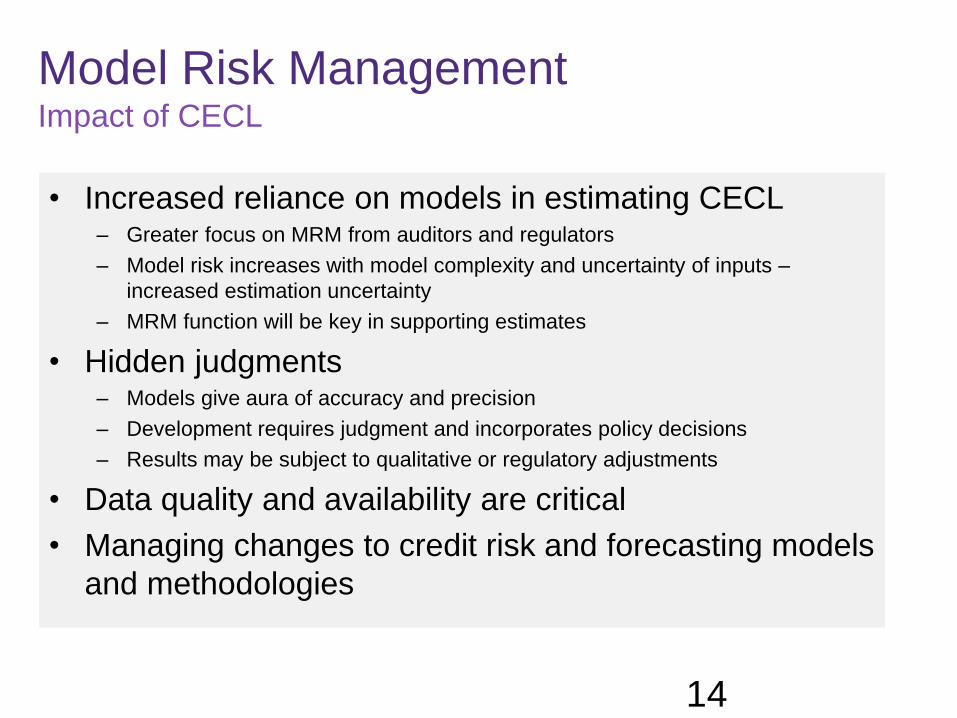

Model Risk ManagementImpact of CECL

• Increased reliance on models in estimating CECL– Greater focus on MRM from auditors and regulators

– Model risk increases with model complexity and uncertainty of inputs –

increased estimation uncertainty

– MRM function will be key in supporting estimates

• Hidden judgments– Models give aura of accuracy and precision

– Development requires judgment and incorporates policy decisions

– Results may be subject to qualitative or regulatory adjustments

• Data quality and availability are critical

• Managing changes to credit risk and forecasting models

and methodologies

14

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Model Risk ManagementHow does CECL integrate with DFAST & CCAR?

• Good basis for DFAST and CCAR

• DFAST and CCAR models may not comply with CECL

– DFAST and CCAR testing based on open book of business

(i.e., new loans made and existing payoffs within the stress

testing period)

– CECL is an estimate of specific set of loans at a specific date

• DFAST and CCAR – annualized loss assumptions

• CECL – life of loan assumptions

15

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Model Risk ManagementBCBS GCRAECL

Principle 5: A bank

should have policies

and procedures in

place to appropriately

validate models used

to assess and measure

expected credit losses.

16

Principle 2: A bank should adopt,

document and adhere to sound

methodologies that address

policies, procedures and controls

for assessing and measuring credit

risk on all lending exposures. The

measurement of allowances should

build upon those robust

methodologies and result in the

appropriate and timely recognition

of expected credit losses in

accordance with the applicable

accounting framework.

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Model Risk ManagementChallenges

• Complexity and volume of models subject to MRM

• MRM processes are historically manual and reactive

• Harmonizing loss forecasting model methodologies

across risk, finance and lines of business

• Considering DFAST top-down model methodologies vs

CCAR bottom-up model methodologies

• Volume of required documentation

• Data quantity and quality

17

How do we know?

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

ICFR

Agenda topic

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

ICFRCompleteness and Accuracy

Credit Risk, Forecasts, CCAR / DFAST, Historical

Loan Loss Data

ICFR: Ensure Completeness and

Accuracy of Data

Models & Processes: Turn Data into Estimates of

Lifetime ECL

ICFR: ITGC - Ensure Data Transfers Accurately,

Models Used as Designed,

Adjustments to Historical Experience Supported

CECL Estimate

ICFR: Financial Reporting –

Including Disclosure – is Clear, Complete and

Accurate

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

ICFR

• Data integrity

– Historical loan loss data

– Credit Risk data

• Forecasts

– Used accurately

– Well supported

– Consistent with other processes (CCAR/DFAST)

Completeness and Accuracy of Data

ICFR scrutiny expanded to new areas of organization

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

ICFR

• ITGCs: CECL models and system automation

– Data integrity between systems

– Change management

– Security administration

– Program maintenance

• Processes: Judgmental overlays

– Qualitative adjustments supported and documented

Models and Processes

Documenting Adjustments – Directional Consistency

and Quantitative Sufficiency

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

ICFR

• Results accurately incorporated into the financial

statements

• Disclosures clearly and completely communicate

uncertainty in CECL estimates

– Main assumptions / inputs

– Qualitative disclosure on forward-looking

Financial Reporting

Consider Enhanced Disclosure Task Force guidance

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Ongoing Monitoring

Agenda topic

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Ongoing MonitoringRole of TCWG in CECL – BCBS GCRAECL

Principle 1: A bank's

board of directors and

senior management are

responsible for

ensuring that the bank

has appropriate credit

risk practices,

including an effective

system of internal

control, to consistently

determine adequate

allowances…

24

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Ongoing Monitoring

• Greater importance of knowledgeable evaluation of

management assumptions / methodologies

– Evaluate consistency of views of risk across organization

• Be cognizant of potential for management bias

– Establish a recurring agenda to evaluate management

assumptions/methodologies on an ongoing basis

• Ensure TCWG have appropriate expertise

• Enabled by appropriate KPI reporting

Overseeing Management

How do we know?

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Ongoing Monitoring

• Establishment of key performance indicators

(KPIs) relating to CECL

– Tool used to challenge model effectiveness

– System to explain performance to others

– Timely reporting of KPIs

• Balancing expectations of auditors/regulators

– Regulatory pressure for allowance levels

– Auditor challenge of what is supportable

• PCAOB

• SEC

Overseeing Management

Consider guidance from BCBS, GPPC, EDTF

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Board Committees

• Consider formation of a dedicated, limited-life

board subcommittee

– Intense focus

– Non-executive membership

– Bridging audit, ERM and other needed committees

• Establish clear reporting lines to the special

committee

• Hold participants accountable

– Dedicated resources

Transition Considerations

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

Key Questions

Agenda topic

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

The Board and its Committees

• What plans are in place to conclude on:

– Key decisions?

– Build and test necessary models /

infrastructure?

– Execute dry / parallel runs?

Questions to Consider

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

The Board and its Committees

• Has the institution identified all short- and longer-

term changes to:

– Existing systems and processes?

– Data requirements and internal controls?

• How will reporting processes and control be

documented and tested?

– Have systems and data sources not previously

subject to audit been considered?

Questions to Consider

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd

The Board and its Committees

• What are the key accounting interpretations and

judgements and why are they appropriate?

• How will disclosure requirements be met and how

will those disclosures facilitate comparability?

• How will implementation decisions be monitored to

ensure they remain appropriate?

• What mechanisms will give us timely knowledge of

the ongoing status of all the processes and

controls?

Questions to Consider

© 2015 Grant Thornton LLP | All rights reserved | U.S. member firm of Grant Thornton International Ltd32

Questions from the audience?