cbe16 - funding sources and considerations

TRANSCRIPT

Finance, the other F Word

Jeff Clark

Live Oak Bank Wine & Craft Beverage

John Fisher

Fisher & Company

Don Winkle

Spaulding McCullough & Tansil LLP

Craft Beverage Expo 2016

© 2015 Live Oak Banking Company. All rights reserved. Member FDIC

Equity vs. Debt

Equity = No Collateral = No Secondary

Source of Repayment

Value of Collateral = How Liquid Is It?

3

Degree of Liquidity by Asset Class

In Descending Order

Cash

Marketable Securities

Accounts Receivable – Purchase Orders

Finished Goods – Case Goods

Bulk Wine – Aging Spirits

Equipment

Real Estate

Collectables – Art, Rare Items, etc.

Lottery Tickets

Penny Stocks

4

Equity

5

Risk to Lender– Highest

Minimal collateral if any

Cost to Company – High

Dilution of profits

Potential reduction in decision making process

Advantages

Sometimes the only source of capital available

Often far more capital available than can be provided by debt

Synergies of experience, industry connections

Asset Based Lender

Risk to Lender – High

Mitigated by collateral value

Cost to Company – Higher than conventional lender

Lower advance rates

Control of working capital

More frequent reporting

Advantages

Less reliant on cash flow

Generally will take more risk than conventional lender

6

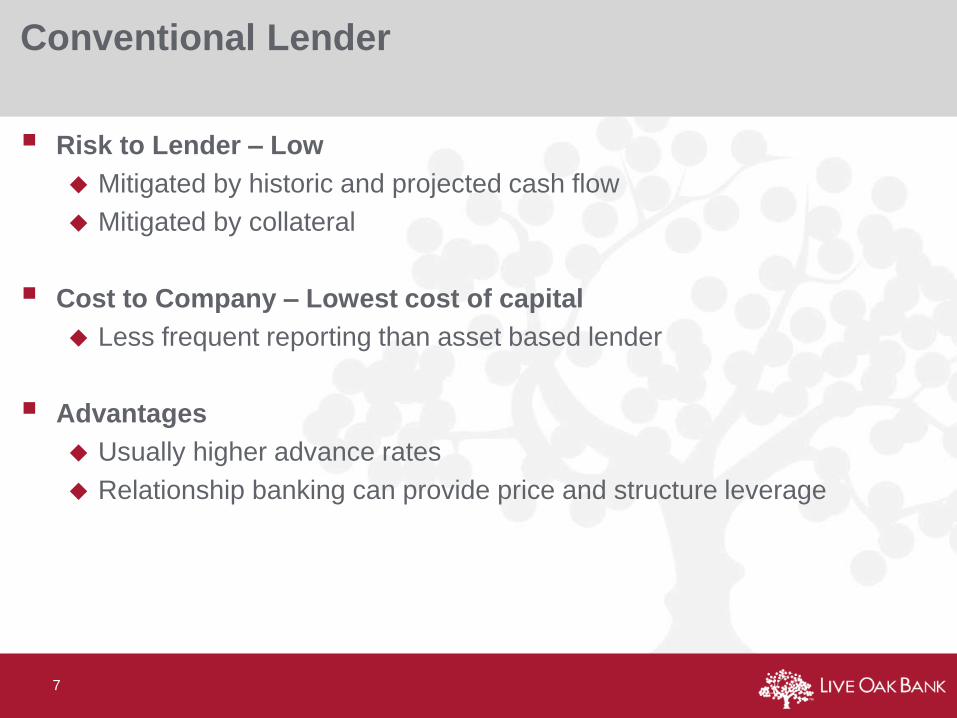

Conventional Lender

Risk to Lender – Low

Mitigated by historic and projected cash flow

Mitigated by collateral

Cost to Company – Lowest cost of capital

Less frequent reporting than asset based lender

Advantages

Usually higher advance rates

Relationship banking can provide price and structure leverage

7

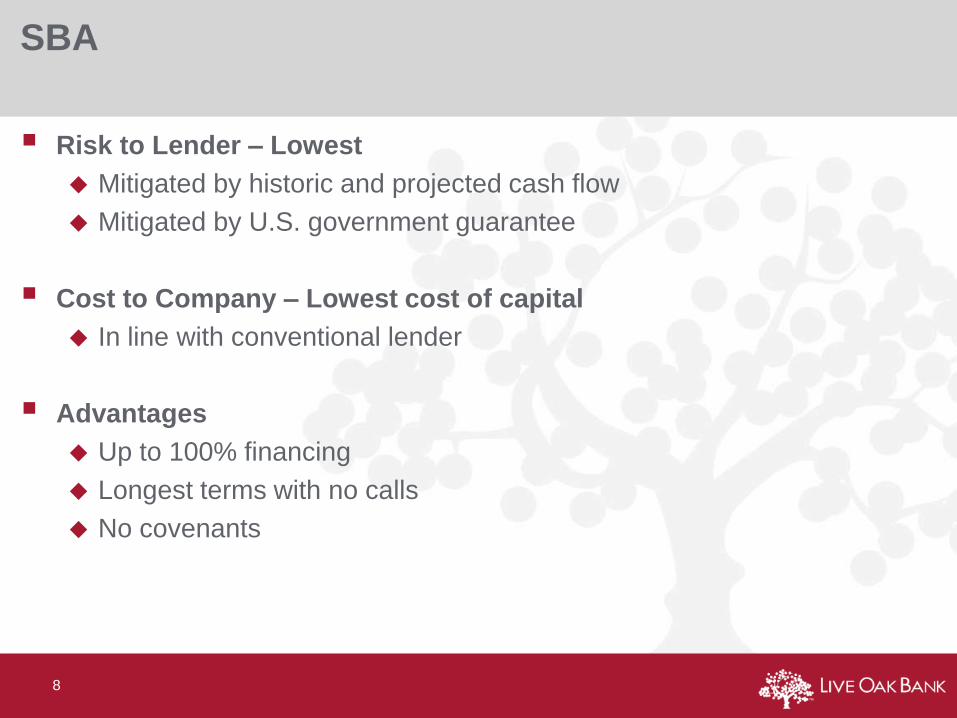

SBA

Risk to Lender – Lowest

Mitigated by historic and projected cash flow

Mitigated by U.S. government guarantee

Cost to Company – Lowest cost of capital

In line with conventional lender

Advantages

Up to 100% financing

Longest terms with no calls

No covenants

8

What do Equity Investors and

Lenders Seek?

Acceptable Return on Investment

Repaid as Agreed

Risk = Reward

9

Management

Industry experience

Marketing, Sales, Operations, Finance

Strategic Partners – Distributor, Accountant, Attorney, Consultants

Regulatory and Compliance

10

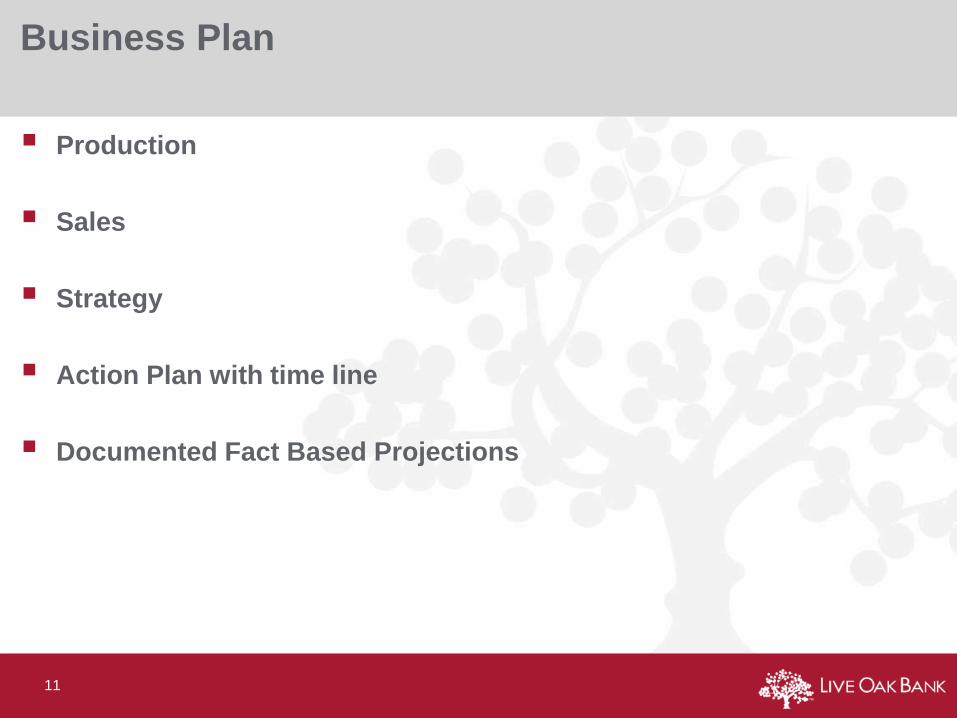

Business Plan

Production

Sales

Strategy

Action Plan with time line

Documented Fact Based Projections

11

Reporting Capabilities

Quarterly or Monthly

Accounts Receivable

Accounts Payable

Inventory

Income Statement

Balance Sheet

Annual

Compiled, Reviewed, Audited and Tax Returns

Projections

12

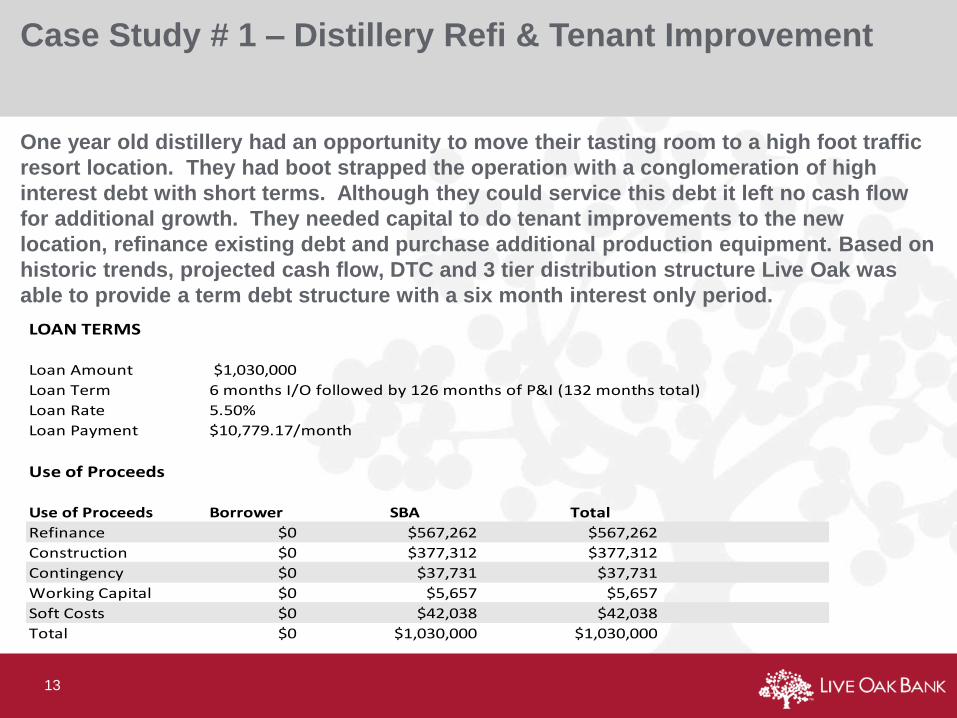

Case Study # 1 – Distillery Refi & Tenant Improvement

One year old distillery had an opportunity to move their tasting room to a high foot traffic

resort location. They had boot strapped the operation with a conglomeration of high

interest debt with short terms. Although they could service this debt it left no cash flow

for additional growth. They needed capital to do tenant improvements to the new

location, refinance existing debt and purchase additional production equipment. Based on

historic trends, projected cash flow, DTC and 3 tier distribution structure Live Oak was

able to provide a term debt structure with a six month interest only period.

13

LOAN TERMS

Loan Amount $1,030,000

Loan Term 6 months I/O followed by 126 months of P&I (132 months total)

Loan Rate 5.50%

Loan Payment $10,779.17/month

Use of Proceeds

Use of Proceeds Borrower SBA Total

Refinance $0 $567,262 $567,262

Construction $0 $377,312 $377,312

Contingency $0 $37,731 $37,731

Working Capital $0 $5,657 $5,657

Soft Costs $0 $42,038 $42,038

Total $0 $1,030,000 $1,030,000

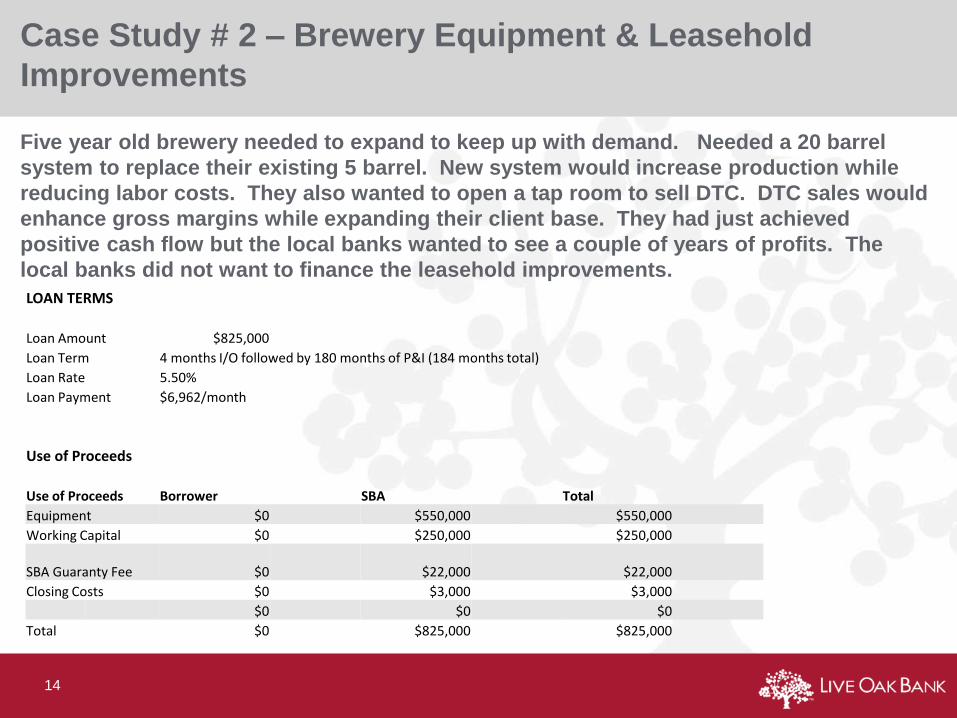

Case Study # 2 – Brewery Equipment & Leasehold

Improvements

Five year old brewery needed to expand to keep up with demand. Needed a 20 barrel

system to replace their existing 5 barrel. New system would increase production while

reducing labor costs. They also wanted to open a tap room to sell DTC. DTC sales would

enhance gross margins while expanding their client base. They had just achieved

positive cash flow but the local banks wanted to see a couple of years of profits. The

local banks did not want to finance the leasehold improvements.

14

LOAN TERMS

Loan Amount $825,000

Loan Term 4 months I/O followed by 180 months of P&I (184 months total)

Loan Rate 5.50%

Loan Payment $6,962/month

Use of Proceeds

Use of Proceeds Borrower SBA Total

Equipment $0 $550,000 $550,000

Working Capital $0 $250,000 $250,000

SBA Guaranty Fee $0 $22,000 $22,000

Closing Costs $0 $3,000 $3,000

$0 $0 $0

Total $0 $825,000 $825,000

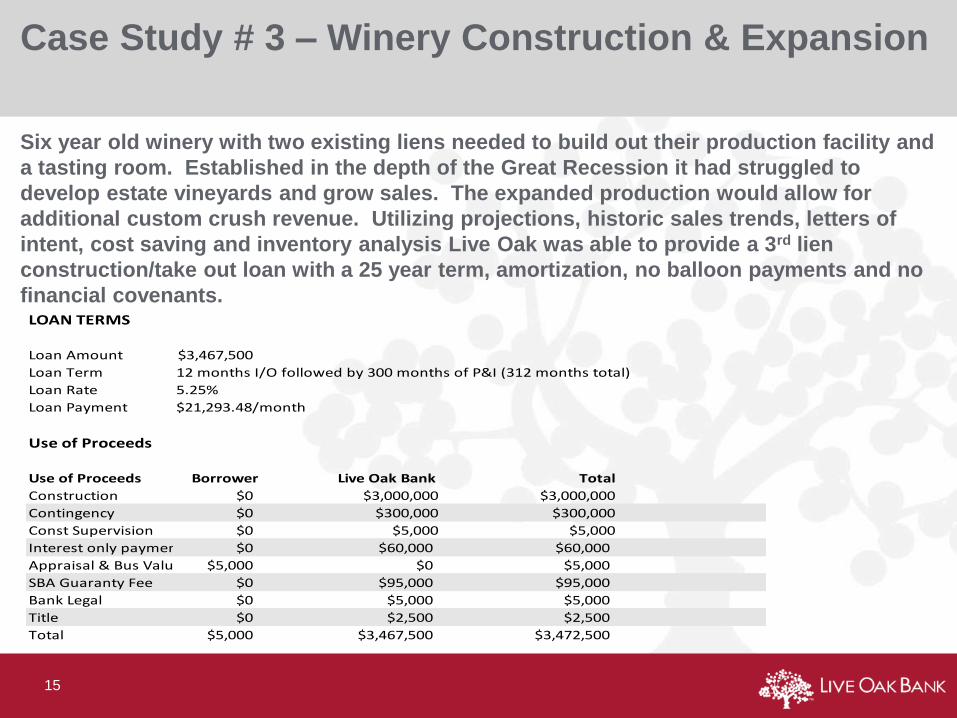

Case Study # 3 – Winery Construction & Expansion

Six year old winery with two existing liens needed to build out their production facility and

a tasting room. Established in the depth of the Great Recession it had struggled to

develop estate vineyards and grow sales. The expanded production would allow for

additional custom crush revenue. Utilizing projections, historic sales trends, letters of

intent, cost saving and inventory analysis Live Oak was able to provide a 3rd lien

construction/take out loan with a 25 year term, amortization, no balloon payments and no

financial covenants.

15

LOAN TERMS

Loan Amount $3,467,500

Loan Term 12 months I/O followed by 300 months of P&I (312 months total)

Loan Rate 5.25%

Loan Payment $21,293.48/month

Use of Proceeds

Use of Proceeds Borrower Live Oak Bank Total

Construction $0 $3,000,000 $3,000,000

Contingency $0 $300,000 $300,000

Const Supervision $0 $5,000 $5,000

Interest only payments $0 $60,000 $60,000

Appraisal & Bus Valuation$5,000 $0 $5,000

SBA Guaranty Fee $0 $95,000 $95,000

Bank Legal $0 $5,000 $5,000

Title $0 $2,500 $2,500

Total $5,000 $3,467,500 $3,472,500

© 2013 Live Oak Banking Company. All rights reserved. Member FDIC