carne allocators survey

TRANSCRIPT

Corporate governance in hedge funds:

Investor Requirements

Basis of Survey

• When: Spring /Summer 2011

• Who: Carne Group approached the top 100 allocators globally with respondents including Aberdeen, Amundi, AXA Fund of Hedge Funds, Barclays Wealth, CalPERS, FQS Capital, Gottex, Hermes

BPK, IAM, JPMorgan, Liongate, Mercer, Mesirow, Olympia, Permal, Pictet, Skandia, UBP and USS.

• How Much: Allocators accounting for over $600 billion in AUM, approximately 30% of all hedge fund allocations, are represented in this survey.

Analysis of Participants

The Participant Allocators were analysed by both primary activity in the hedge fund industryand total AUM to give a profile of the respondents

Importance of Corporate Governance Standards

How important is Corporate Governance?

Participants were asked how important corporate governance in hedge funds was to them. The answer was overwhelmingly that allocators considered Corporate Governance to be of extreme importance with 83% giving this answer.

Affecting the Investment Decision

Have you ever decided NOT to invest because of concerns over a funds corporate governance?

Yet again the response was hugely weighted towards the importance of governance with some 76% saying they had refrained from investing at least once due to corporate governance concerns.

Affecting the Investment Decision - II

Would you ever decide NOT to invest because of concerns over a funds corporate governance?

When further questioned 91% of allocators taking part in the survey confirmed that they would choose not to invest in a fund if there were corporate governance concerns. This is a clear indicator of the importance of corporate governance not only to allocators but to managers in fulfilling their capital raising plans.

Increasing Relevance

Has Corporate Governance become more of a focus in the past 3 years?

When asked if Corporate Governance had become more of an issue since 2008 the response was perhaps predictably positive in light of the difficulties and lessons learnt over this period. Almost 90% of respondents confirmed that they were more focused now on governance issues.

Rating Corporate Governance

How do you rate the average standard of fund corporate governance in the hedge fund industry?

The responses when allocators are asked to rate standards of corporate governance in the industry between “Excellent” and “Below Desired Levels and requiring improvement” point towards a clear desire on the part of allocators to see the standards raised.

Rating Corporate Governance Are you happy with overall governance levels in these domiciles?

63% of hedge fund allocators are unhappy with levels of fund governance in the Cayman Islands which is the least satisfactory jurisdiction according to our respondents.

By contrast to the Cayman Islands and, to a lesser extent, the Channel Islands, allocators are extremely satisfied with governance in both Luxembourg and Ireland, with high approval ratings for both jurisdictions.

Rating Corporate GovernanceRegional break down of satisfaction levels (rating out of 10):

Allocators were asked to rate their satisfaction with corporate governance arrangements by jurisdiction of investment manager domicile. As you can see, opposite, the results indicate that allocators are significantly more satisfied with the governance arrangements of funds promoted by managers domiciled in Europe than elsewhere which seems consistent with the previous slide.

Areas Requiring ImprovementWhich areas of fund governance require improvement?

Respondents were provided with a list of options to select from and the results, tabulated opposite, reveal that investors have a number of concerns not least of which are the number of appointments held by directors, the independence of directors and the extent of their activities.

Minimum standardsWhat aspects of corporate governance have you had difficulty obtaining information on?

Allocators were asked in which areas they had experienced the most difficulty when seeking governance-related information from managers and fund boards.Allocators want greater transparency on the part of many fund boards and are seeking clarity on many of the issues listed opposite in the normal course of their Due Diligence Process.

Minimum standardsHow many directorships should independent fund directors hold?

Most allocators we spoke to preferred to focus on manager relationships rather than the number of boards an independent director sits on as it is the key driver of directors’ time.

The majority of allocators – 58% - would prefer independent directors to limit themselves to 30 client relationships maximum.

Minimum StandardsMinimum number of board meetings per annum

Allocators were asked how many board meetings should be held annually, not surprisingly there was a clear preference for quarterly meetings.

This is indicative of the importance investors now ascribe to the regular meeting of the board in fulfilling its monitoring obligations.

Minimum StandardsMinimum number of meetings per annum held in person

Extending the prior question to physical, face to face, meetings it seems investors also place great importance on these events with almost 50% wanting 2 meetings in person per year and a convincing 90% arguing for the holding of at least one physical meeting.

Minimum StandardsMinimum number of directors on board:

Allocators were next asked about there preferences on board composition, starting with the number of directors comprising the board.

Over 90% wanted to see at least 3 directors.

Minimum StandardsMinimum number of independent directors on board

Over 90% of participants stated a preference for at least 2 independent directors.

Minimum StandardsProportion of independent directors on fund boards

Confirming our conclusions from the two previous questions 87% of allocators favour a majority independent board.

Minimum StandardsShould the chairman of the board be an independent director?

Continuing the theme of endorsing independent directors , their importance and authority in the board room of hedge funds allocators voted 80/20 in favour of appointing an independent chairman of the board.

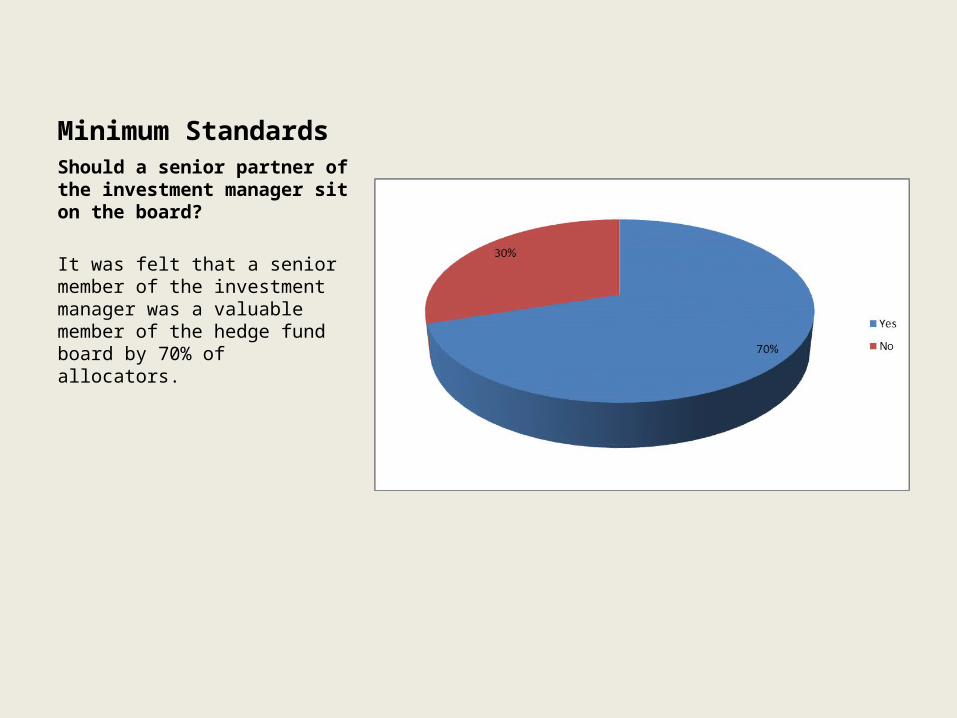

Minimum StandardsShould a senior partner of the investment manager sit on the board?

It was felt that a senior member of the investment manager was a valuable member of the hedge fund board by 70% of allocators.

Minimum Standards:What areas should boards consider at regular board meetings?

Allocators clearly fell that the board should be reviewing a wide range of operational areas of risk on a regular basis with over 65% of allocators considering that all the listed areas should be considered.

Minimum StandardsKey skills looked for from fund directors:

Allocators were presented with a list of skill sets and asked to indicate if they were desirable in an independent director. Interestingly Portfolio Management ranked last with investors feeling that this can be offered by investment manager attendance at board meetings. Legal skills were most desired although it is thought this represents a shortage of this skills et in the current market place rather than a distinct preference.

Minimum StandardsWhat is the minimum level of fund industry experience you would expect from independent directors?

Allocators indicated that they are looking for mature, experienced individuals to act as directors with a preference for the majority of at least 10 years relevant experience.

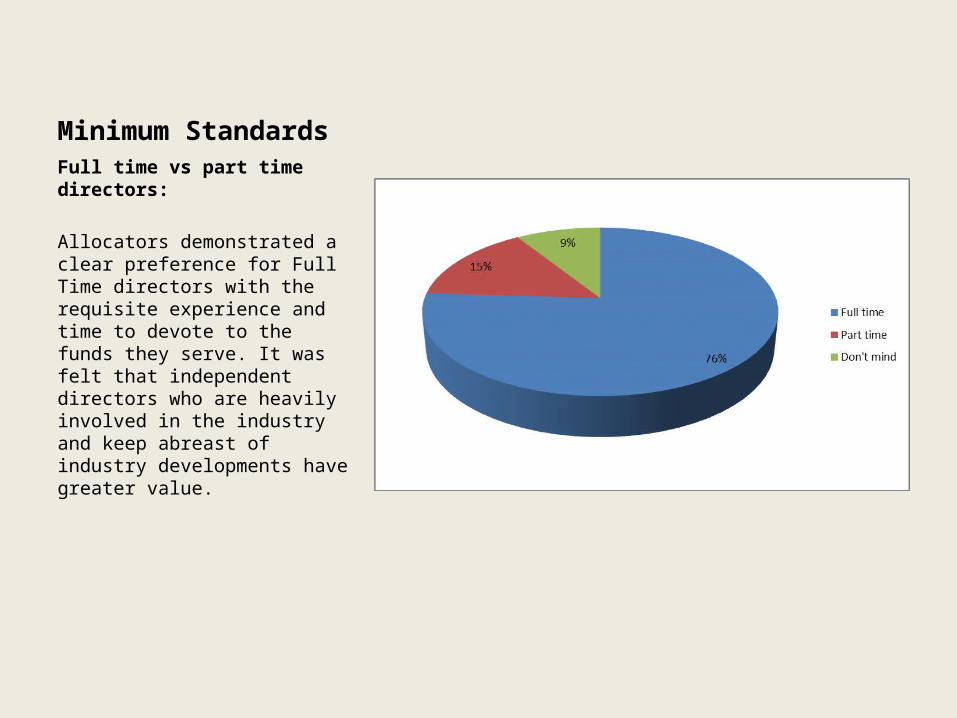

Minimum StandardsFull time vs part time directors:

Allocators demonstrated a clear preference for Full Time directors with the requisite experience and time to devote to the funds they serve. It was felt that independent directors who are heavily involved in the industry and keep abreast of industry developments have greater value.

Minimum StandardsShould a fund have a director resident in the domicile of the fund for tax/domicile purposes?

This is an area of more importance to allocators with UK-based managers in their portfolios, due to potential UK tax risks to the funds but nonetheless 63% of allocators would prefer to have a director resident in the fund’s jurisdiction of domicile.

Transparency and Conflicts of InterestWould you consider any of the following as independent directors if related to:

Yet again the allocators questioned showed a strong preference for independence with over 60% indicating that they DO NOT consider directors related to service to be truly independent.

Summary Findings

• Independent directors should have no more than 20-30 client relationships, and definitely no more than 30 to 40;

• Boards should have at least THREE directors and the majority should be independent;

• Independence is defined as free from conflicts of interest or where it is unlikely that material risks could be incurred by that director’s presence. Directors from service providers are not considered to be independent by a majority of allocators;

• Directors should be experienced and knowledgeable, with a minimum of 10 to 15 years of experience in the funds industry;

• There should be a minimum of THREE full board meetings per annum and at least one with directors and manager physically present. All service providers should present reports to the boards;

• Board agendas should cover key areas including conflicts, material risk areas, audit findings, financial accounts, adequacy of disclosure, and compliance (including manager compliance);

• Potential conflicts of interest of directors are a key issue for investors. They would like to see a written potential conflicts analysis and policy including the relevant interests of directors (e.g. other directorships) and service providers. The policy should include the identification and handling of conflicts when they arise;

• Transparency is an issue with nearly all investors interviewed for this survey.

Taking a consensus view of the responses to the survey the following become key points when new or existing managers are considering the composition, structure and operation of the boards of funds they promote. Allocators interviewed have demonstrated a keen interest in this area and make it clear in their responses that corporate governance is an increasing area of focus that WILL affect the decision to invest.