captives continue rising - vanbreda€¦ · captives in 2016. debbie liebeskind ... goldman sachs...

TRANSCRIPT

Captives Continue Rising

ADVERTISING SUPPLEMENT

INDEPENDENT GLOBAL EXPERTS WITH LOCAL EXPERTISE

R&Q Quest Management Services is a leading

and major domiciles worldwide.

independent and balanced advice to clients.

Nick Frost +1 441 247 8301 email [email protected]

www.rqquestbermuda.com

“

ADVERTISING SUPPLEMENT

2016 3

CUSTOMMEDIAGROUP

This special advertising supplement is not created, written or produced by the editors of Business Insurance and does not represent the views or opinions of the publication or its parent company, Crain Communications Inc.

SPONSORS

Delaware Captive Insurance Association

4023 Kennett Pike, Box 801

Wilmington, DE 19807

888-413-7388

www.delawarecaptive.org

Delaware Bureau of Captive &

Financial Insurance Products

The Nemours Building

1007 Orange Street, Suite 1010

Wilmington, DE 19801

Phone: 302-577-5280

Fax: 302-577-3057

www.captive.delawareinsurance.gov

R&Q Quest Management Services Ltd.

F.B. Perry Building

40 Church Street

P.O. Box HM2062

Hamilton HM HX

Bermuda

441-247-8301

www.rqquestbermuda.com

Towers Watson

175 Powder Forest Drive

Weatogue, CT 06089-9658

860-843-7012

www.towerswatson.com

Two trends will continue to drive interest in funding employee benefit risks through captives in 2016.Debbie LiebeskindSenior consultant and life/health actuary with Towers Watson in Parsippany, N.J.

“

”

CONTENTSSmall captives, benefits interest fueling global growth 4

25 years of captive history 4

Domicile choices abound worldwide 7

Fronting, ROI hard for captives 8

Benefit captives expected to soar 10

FOUNDING PARTNERS DIAMOND SPONSOR

4 ADVERTISING SUPPLEMENT

2016

SMALL CAPTIVES, BENEFITS INTEREST

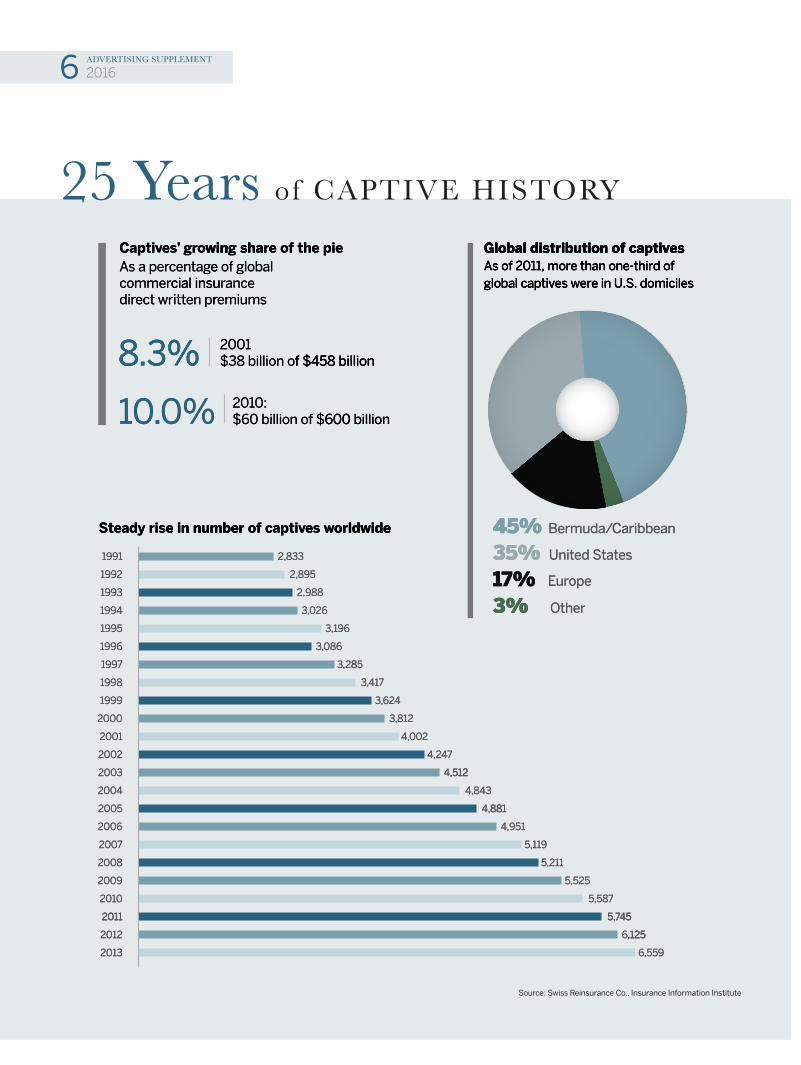

The growth of captive insurance entities over the past quarter-century has been remarkably steady, captive industry data shows. From a worldwide total of about 2,800 in1991 to nearly 7,000 licensed captives today, the captive movement is stronger than ever. Here are some of the highlights of the captive industry during the past 25 years:

The Internal Revenue Servicestates that companies can deductgroup term life premiums paid tocaptives because the premiumsrepresent unrelated business.

General Electric Co. captive Electric Mutual LiabilityInsurance Co., redomiciles to Bermuda and subsequently declares itself to be underreservedfor GE asbestos and environmental liability claimsand insolvent by more than $500 million. EMLICO is sued by its reinsurers, which chargethat GE and the captive planned the collapse, butEMLICO prevails and enters liquidation.

Columbia Energy Group gains approval to fund U.S. employeebenefit risks through its Vermontbranch captive. This precedentblazes a trail for other captiveowners to follow.

Vermont’s captives generate premium volume exceeding $1 billion.

Goldman Sachs & Co. establishesArrow Reinsurance Co. Ltd., a special-purpose reinsurer in Bermuda that marks the first Bermuda reinsurer owned by an investment bank. Lehman Brothersfollows suit a few months later with Lehman Re Ltd.

The Sept. 11, 2001, terrorist attackson the World Trade Center and the Pentagon create one of the worst-everloss events, more than $20 billion intotal insured losses. Uncertainty anddelay in establishing a permanentfederal government backstop for terrorism risk prompt some businessesto fund their terrorism risks throughcaptives.

Bermuda’s Segregated Accounts Companies Act permits registration of protected-cell captives, paving the way for more captive formations.

Captive owners obtain a favorable rulingfrom the 11th U.S. Circuit Court of Appeals in United Parcel Service vs. Commissioner on the tax deductibility ofpremiums paid to captives. UPS built onthe landmark 1987 Tax Court ruling in Humana vs. Commissioner, which recognized the tax deductibility of captivepremiums under certain circumstances.

1992

1991

1995

1998

2000

2000

2001

2001

9911

9951

0002

0012

00122991 2

9981

0002

0012

The global captive industry has come a long way since the first World Captive Forum 25 years ago.

The number of captives in 1991 wasslightly more than 2,800 worldwide, basedin a small number of domiciles. Today,there are at least 71 domiciles and morethan 6,800 licensed captives globally.

The growth in overall numbers has beenaccompanied by the diversification of typesof captives, making captive insurance anoption for organizations of virtually all sizes,from small businesses and nonprofit entitiesto global multinational corporations.

Growth in the captive industry today islargely coming from companies formingsmaller captives, as well as from multinationalcompanies that are expanding, said NicholasFrost, president of R&Q Quest ManagementServices Ltd. in Bermuda.

“We’re seeing a lot of interest from LatinAmerica,” said Frost. “As these markets mature,Latin American clients are looking to set up inBermuda, enjoying the multitude of opportu-nities afforded by owning a captive, which caninclude improved coverage, lower cost of riskand direct access to leading reinsurance. Untilvery recently, the majority of interest from the

region was from Colombia and Mexico, whilenow we are seeing interest across the widerregion, including Chile. We are also seeingmore interest from companies in Canada.”

Steve Kinion, director of the Bureau of Cap-tive and Financial Insurance Products at theDelaware Department of Insurance, is seeing“a proliferation of captives in the past fiveyears, especially microcaptives, in manydomiciles. Delaware is indicative of that growth.”

Microcaptives, typically formed by smallerparent organizations, are those that elect notto pay taxes on underwriting income underthe Internal Revenue Code 831(b). The InternalRevenue Service permits such captives toseek an exemption provided that their premiumvolume is below $1.2 million. Microcaptivesdo pay taxes, however, on investment income.

As of 2013, “about 80% of Fortune 500companies had a captive of some type, sothat’s an 80% market penetration. Only 20%or so of small to midsize companies hadcaptives. While that has increased to 20% to25% now, there still is tremendous opportu-nity for growth in this area,” Mr. Kinion said.

25 YearsOF CAPTIVE HISTORY Milestones mark steady growth in captive industry since 1991

5ADVERTISING SUPPLEMENT

2016 5

FUELING GLOBALGROWTH

Vermont, with more than500 captives, becomes thethird-largest domicile in theworld, behind Bermuda andthe Cayman Islands.

The U.S. Department of Labor approvesArcher Daniels Midland Co.’s petition toreinsure group life benefits through itscaptive. This decision, on the heels ofthe Columbia Energy decision in 2000,paves the way for other captive ownersto seek fast-track approval from the department.

The number of licensed captives worldwide surpasses 5,000 for the first time, according to Business Insurance’sannual ranking.

Captive premiums account for10% of global commercial insurance premiums, or about $60 billion, according to an estimate by Swiss Reinsurance Co.

The IRS begins looking closer at captives formedunder Section 831(b) of the Internal Revenue Code,which dates back to 1986, for abusive practices. Theintent of the law was to extend the tax benefits of self-insurance to smaller and midsize entities. By2014, however, the IRS grew concerned that many831(b) captives were formed not for self-insurancebut to avoid tax.

The IRS rules that an innovative plan by The Coca-Cola Co. to fund retiree health care benefits throughits captive qualifies as insurance. Observers hail theruling as expanding the types of benefits risksthat captive parents can fund through their captives.

2002

2003

2007

2010

2014

2014

20027002 4102

410202 300

0102

4102

He attributes the growth in captives bysmaller entities to the expansion of differenttypes of captives. “It’s like the chips and sodaaisle in the grocery store – there are manymore choices today than there were in the1990s. Just as we’ve seen boutique or nicheproducts in different industries, now we’reseeing more choices in types of captives: cells,series, group captives and association captives,”Mr. Kinion explained. “There’s a captive typesomewhere that will fit your needs. That helpsbusinesses to be more productive.”

Large companies based in Delaware also aresponsoring captives, Mr. Kinion said. “Delawareis the home of 64% of the U.S. Fortune 500, andwe are seeing growth in captives owned byDelaware-domiciled corporations,” he said.

Captives funding new risksAs the types of captive entities have expanded,

so too have the types of risks that captiveowners have sought to fund through thosestructures. What risks a captive owner choosesto fund depend largely on the owner’s needs.

For some, a captive is useful for financing theworking-layer risks in a property or casualtyprogram, to increase attachment points forcommercial insurance and therefore reducethe costs of coverage. For others, the captivecan provide coverage for which there are fewcommercial options, or where capacity islimited or expensive.

“Today there is a tremendous amount ofdifference in the coverages that a captiveprovides,” compared with a few years ago, Mr.Kinion said. “In the last 12 months, there hasbeen a real proliferation of cyber risk funded incaptives,” he said. For example, some ownersare using their captives to reimburse theparent companies for expenses related tothird-party liability, which frequently occur indata breaches, he explained.

“And it’s not just retailers looking to usecaptives for these expenses. It could beplumbing contractors or other servicebusinesses that observe breaches and wantto protect themselves,” Mr. Kinion said. “Risksfor cyber are changing all the time, and the cost

of cyber breaches keeps going up. Companiessee this and say to themselves, ‘We need tocover our exposure.’”

For the past several years, an increasingnumber of captive owners have expressedinterest in funding U.S. employee benefitsthrough their captives. But funding thosebenefits requires U.S. Department of Laborapproval (see story, page 10).

Only a few dozen large employers haveobtained approval to finance U.S. benefits incaptive programs, but industry observersexpect that number to grow significantly.

Delaware’s Bureau of Captive and FinancialProducts estimates that the total market forbenefits that are eligible for captive coverage isabout $800 billion, Mr. Kinion said. “Thereobviously is a tremendous growth opportunityin funding benefits through captives, and onlya fraction of it has been served so far,” he said.“The last two months have seen a spike in inter-est in funding benefits in Delaware captives. I ex-pect to see a lot of new developments in benefitfinancing in the coming years.” •

6 ADVERTISING SUPPLEMENT

2016

Global distribution of captivesAs of 2011, more than one-third of global captives were in U.S. domiciles

Steady rise in number of captives worldwide

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2,833

2,895

2,988

3,026

3,196

3,086

3,285

3,417

3,624

3,812

4,002

4,247

4,512

4,843

4,881

4,951

5,119

5,211

5,525

5,587

5,745

6,125

6,559

45% Bermuda/Caribbean

35% United States

17% Europe

3% Other

Captives’ growing share of the pieAs a percentage of global commercial insurance direct written premiums

8.3% 2001$38 billion of $458 billion

2010:$60 billion of $600 billion10.0%

.3%8

ren ptect writrdicial insurommec

e gatencrs a peAwing shaor g’sevveCapti

0012

emiumsre canrcial insu

al bf glooe f the pieoe rwing sha

global captives were in U.S. domicilesAs of 2011, more than one-third of Global distribution of captives

global captives were in U.S. domicilesAs of 2011, more than one-third of Global distribution of captives

global captives were in U.S. domicilesAs of 2011, more than one-third of Global distribution of captives

0%.01

.3%8

f $600 billiono$60 billion 0:102

f $458 billiono$38 billion

f $600 billion

f $458 billion

9951

9941

3991

2991

9911

e in number sady rietS

orldwidews evapticf oe in number

96

1,3

620,3

2,988

958, 2

833,2

orldwide

3%135%45%

Other3%ope ruE%7117

setated St Uni35%Cari//CaribbermudaB45%

aneCaribb

3002

2002

0012

0002

9991

9981

7991

9961

8,23

086,3

,5124

742,4

200,4

812,3

426,3

714,3

58

0112

0102

0092

0082

7002

0062

0052

0042

8814,

8434,

,512

4575

78,55

,5255

,2115

91,15

,9514

881

3102

0122

0112

,1256

457,5

95,56

,125

Source: Swiss Reinsurance Co., Insurance Information Institute

25 Years of CAPTIVE HISTORY

ADVERTISING SUPPLEMENT

2016 7

CAPTIVES IN 2014

Bermuda

Cayman Islands

Vermont

Utah

Anguilla

Delaware

Guernsey

Nevis

Barbados

Luxembourg

World’s largest captive domiciles

DOMICILE

Source: Business Insurance

800

759

584

422

379

333

281

271

224

321

A critical step in the decision to form a captive entity is the choice of domicile: where it will be licensed and where it will operate.

There are dozens of jurisdictions around theworld with captive insurance laws. As a result,there are lots of choices on where to base acaptive, said Nicholas Frost, president of R&QQuest Management Services Ltd. in Bermuda.

“Most clients want to go where there isgood infrastructure for captives,” he said. Theproliferation of captive domiciles, especiallyin the United States over the past 10 years,has increased the number of onshore optionsfor captive owners. “Establishing a captive ju-risdiction has become popular, but you can’tjust pass a law and expect people to show up,”Frost said. “Successful domiciles have thelegal and financial infrastructure to support

captives – managers, lawyers and auditorswho all understand what a captive is.”

Most of R&Q Quest’s clients are inBermuda, the world’s largest captive domicile,where the firm has been based for the past40 years, Mr. Frost said. “But there are manyother domiciles with strong regulations andinfrastructure. Selecting a domicile tends tobe driven by the client,” he said.

According to Business Insurance researchdata, more than 60% of the world’s captivesare based in the 10 largest domiciles, severalof which — including Bermuda, the CaymanIslands and Vermont — have operated fordecades. •

Domicile choices abound

WORLDWIDE

8 ADVERTISING SUPPLEMENT

2016

Even though the options for formingcaptives and interest in doing so have neverbeen greater, owning a captive is not necessarilyeasy. Many captive parents face challenges,from finding suitable fronting services toachieving investment income targets, observerssay.

Running a business that intentionallytakes risk on its balance sheet requiresowners to temper their expectations with aclear understanding of the long-term benefitsof a captive, which include reduced cost ofrisk, less volatility in risk transfer andenhanced organizational risk management.

Return on investment with a captive, es-pecially in the form of investment income, canbe a challenge for captive owners, notedNicholas Frost, president of R&Q Quest Man-agement Services Ltd. in Bermuda.

One trend that R&Q Quest has seen ismore conservative underwriting by captives.“Captives today are writing more conserva-tively. For example, in Bermuda you can writeon a 5:1 premium-to-capital ratio,” Mr. Frostsaid. That is partly because investment incometo offset underwriting results is scarce, henoted.

In the 1990s, companies “could get hugeamounts of investment income. That’s nothappening now. Companies are not makinginvestment income” in the current market,Mr. Frost explained.

Historical data support this trend. The

Insurance Information Institute (III), forexample, found that commercial property/ca-sualty insurers’ net income rose steadily from1993 to 1997, fell slightly in the ensuing yearsand spiked from 2004 to 2006 before goingflat in 2007. The III’s analysis showed P/Cinsurers’ net investment income grew 3.3%in 2010 before three straight years of invest-ment income declines. When net income isexpressed as a percentage of equity, property/casualty insurers lag well behind Fortune 500industrial and service businesses. The IIIfound that, in 2014, the rate of return for P/Cinsurers on a generally accepted accountingprinciples basis was 7.5%, while the Fortune500 group’s rate of return was 14.2%.

Fronting woesInsurance regulators require captives that

write certain risks, such as workerscompensation and third-party liabilitybusiness, to use fronting arrangements withapproved insurance companies. Fronting ischallenging for captive owners, because thereare few strong fronting companies, Mr. Frostsaid. The largest players currently have beenproviding such services for many years andhave the lion’s share of the market.

“It’s very difficult for a new entity to frontcaptives. The margins are not there, and thatcan be hard to explain to a board,” Mr. Frostsaid.

Regulators require fronting insurance

Fronting, ROI

ADVERTISING SUPPLEMENT

2016 9

companies to guarantee the payment ofclaims. If the fronted captive becomes insolvent,the fronting company is responsible. Somefronts share risks with captives, and some-times 100% of the risks are ceded back to thecaptive. In addition to fees, fronting compa-nies generally require captive owners to col-lateralize their expected liabilities through aletter of credit (LOC) or provide securitywith other assets.

Such requirements can pose a challengeto captive owners. “An LOC to support afronted captive can cost more than the cashgenerated by investments,” Mr. Frost said.

Stop-loss in crosshairs?Steve Kinion, director of the Bureau of

Captive and Financial Products at theDelaware Department of Insurance, said hehas observed strong interest by captive ownersin medical stop-loss arrangements. Using acaptive to write medical stop-loss coverage isviewed as an effective way for employers thatself-fund employee benefits to reduce therisk of high-cost claims. The National Asso-ciation of Insurance Commissioners, how-ever, is considering changes to its Credit forReinsurance Model Act that would authorize in-surance regulators to reduce or eliminate thecredit for reinsurance retroactively, or imple-ment additional requirements, Mr. Kinion said.These could include measures that discouragefronting insurers from participating in

medical stop-loss arrangements that coversmaller employers, he cautioned.

Credit for reinsurance is an importantfinancial benefit of fronting. When an insurancecompany cedes risk to a reinsurer, it is entitledto take a credit on its balance sheet for thereinsurance. Conversely, the reinsurer mustreport the assumed risk as a liability on itsbalance sheet. In medical stop-loss arrange-ments, Mr. Kinion explained, a captive acts asthe reinsurer, and when more lives are coveredunder the reinsurance, the fewer are coveredby the commercial market.

“There has been strong proliferation ofstop-loss in captives. Some regulators mightdecide that’s hurting the small-group marketfor health care insurance,” Mr. Kinion said.“The proposed changes may dissuadefronting companies from getting involved infunding medical stop-loss. We typically don’tsee retroactive application of NAIC modellaw.”

Regulatory scrutinyOne other challenge that Mr. Kinion sees,

as a regulator and longtime observer of thecaptive industry, is the growth of regulation.“Increased scrutiny at both the federal andstate levels will be a challenge,” he said. “Captiveinsurance is no longer a small industry with afew domiciles. As more jurisdictions look atcaptives, I think you’ll see increased regula-tory issues in the future.” •

hard for captivesAs more jurisdictions look at captives, I think you’ll see increased regulatory issues in the future.Steve KinionDirector of the Bureau of Captive and Financial Products at the Delaware Department of Insurance

“

”

10 ADVERTISING SUPPLEMENT

2016

BENEFIT CAPTIVE INNOVATIONS

Two trends will continue to drive interestin funding employee benefit risks throughcaptives in 2016, said Debbie Liebeskind, asenior consultant and life/health actuary withTowers Watson in Parsippany, N.J.

One is that the U.S. Department of Laborhas resumed its fast-track approval program,known as ExPro, for employers seeking to fundU.S. benefits in their captives, she said. TheLabor Department suspended ExPro in 2012while it reviewed the criteria for fast-track ap-proval. It continued to consider individual em-ployer applications for funding benefits andreinstated the fast-track process in 2015.

The other trend, Ms. Liebeskind said, isthat benefit plan sponsors are experiencingmore volatility in their health plans as theAffordable Care Act has eliminated annualand lifetime maximums, which means thatmedical benefit plans can no longer cap theircoverage. Such coverage maximums havetraditionally been used to mitigate high-costclaims, she said. With those maximumsremoved, plan sponsors are more eager toexplore ways to reduce the volatility; captivesare increasingly entering the conversation,she added.

Steve Kinion, director of the Bureau ofCaptive and Financial Products at theDelaware Department of Insurance, agreedthat benefit captives are poised for rapidgrowth.

“Since ExPro has returned, we’re seeingmore interest by captive owners in Delawarein funding benefits,” he said. “In 2016, we’llsee those captives forming. There’s a longercycle for licensing benefit captives. Next yearshould be a strong year for benefits fundingin captives.”

New benefit risksEmployee benefit coverages that are being

funded in captives include life and accidentaldeath and dismemberment, for both activeemployees and retirees. But other benefitrisks are also beginning to enter captives,observers note.

“Some smaller companies are puttingloss of key employee and loss of key supplierpolicies into their captives,” which is a relativelynew development, said Nicholas Frost,president of R&Q Quest Management ServicesLtd. in Bermuda.

More companies are looking at fundingcyber liability coverage through their captives,Mr. Frost said. “Whether it’s a large nationalentity or a small entity with either healthrecords or an abundance of credit cardtransactions, risk managers are trying to gettheir arms around this relatively new riskexposure and how to finance it through thecaptive,” he said.

“Medical stop-loss is one growth area forcaptives. There is a lot of that going on now.People are looking to fund that through a cap-tive. Smaller employers, however, are not put-ting benefits into captives,” said Mr. Frost.

Towers Watson’s Ms. Liebeskind said thatmedical stop-loss is “quite easy to getstarted” through a captive because it doesnot require U.S. Department of Labor approval.Medical stop-loss coverage is not considereda benefit under the Employee Retirement In-come Security Act, or ERISA, and thereforedoes not require approval. Medical and retire-ment benefits governed by ERISA, however,are subject to Department of Labor approval.

With increasing claim volatility in healthplans, more employers are saying, “We hadn’tthought about medical stop-loss before butnow we need it as we are concerned aboutpaying for high-cost claims through the humanresources budget,” she explained. A captive canprovide more financially viable ways to fund the

risk, Ms. Liebeskind pointed out.“In fact, January is not too early to start

thinking about stop-loss,” she said. “Thinkingabout that option in the beginning of the planyear is a good idea, though a feasibility studyfor funding benefit risks can be conducted atany time during the plan year,” she added.

One of the advantages of feasibility studiesis their actuarial analysis of claims data todetermine the cost of coverage at differentattachment points. “If expected claims arepredictable, you might not have to buy stop-loss coverage at all. If the claims show volatility,then you can utilize your captive. One otheradvantage of funding stop-loss is that ittypically is not correlated with any other risksin the captive,” which can help with liquidityand capital requirements, Ms. Liebeskindsaid.

“For ERISA benefits, the first quarter in acalendar year is a great time to conduct afeasibility study. It enables employers toconduct procurement to find a frontingcarrier and coordinate with plan enrollment,”Ms. Liebeskind said.

The most cost-effective benefit risks tofund through captives “tend to be the oneswith long tails, such as long-term disabilityand life insurance with waiver of premium,”she suggested.

Stop-loss medical insurance for activeemployees is an area of growing interest.Stop-loss comes in two forms: specific stop-loss, which is triggered when claims exceed apredetermined cap placed on individualscovered by the plan; and aggregate stop-loss,which typically kicks in when claims in theplan year exceed 125% of the expectedamount. For self-funding employers with asmaller number of lives covered in their plans,specific stop-loss can be more economicalthan aggregate coverage. •

Benefits CAPTIVES Expected to SOAR

Interest in funding benefit risks through captives continues to grow, and helping fuelthat interest are innovative approaches in recent years by high-profile employers.

For example, The Coca-Cola Co. uses its South Carolina-based captive, Red Re Inc., to fund international life, disability and medical insurance.In 2013, Atlanta-based Coca-Cola obtained permission from the Labor Department to fund AD&D benefits for U.S. employees. In 2014, theInternal Revenue Service ruled that Coca-Cola’s innovative plan to fund retiree health care benefits through a voluntary employees’ benefi-ciary association does constitute insurance. The IRS ruling not only gives Coca-Cola tax advantages but also opens the door for other em-ployers to pursue similar captive benefit strategies.

In an example of scale, Detroit-based General Motors Corp. funds life and health insurance, and other employee benefits, for 85% of itsnon-U.S. employees through its Bermuda-based captive, General International Ltd. The captive helps the giant automaker to save tens ofmillions of dollars annually while providing promised benefits.

“People have looked at what Coca-Cola and General Motors have done with their captives, and those are areas that I think we’ll see a lotof growth and interest in, now that ExPro is back,” said Steve Kinion, director of the Bureau of Captive and Financial Products at the DelawareDepartment of Insurance.

Innovative captive programs can be complex and difficult to understand. “It’s important to have knowledgeable regulators,” Mr. Kinionsaid. He has a practice of meeting periodically with the U.S. Department of Labor staff to discuss captive trends and share things he learns.

NEW & EMERGING RISKSIndustry leaders convene at this domicile-neutral conference to discuss strategies and best practiceson Benefits and Property/Casualty captives. Registration includes four days of roundtablediscussions and keynotes coupled with unrivaled networking opportunities for executives whoseorganizations have risks insured by a captive or who are exploring the formation of one.

� Accountable Care…Accountable Captives: The Changing Landscape of Health Care Liability

� Hedging their Bets? Reinsurance and Fronting Market Update� Captives in Latin America: Growth and Challenges� Using Group Captives to Manage Medical Stop-Loss� "Small" Captives and Cells

SPONSORS

PROPERTY/CASUALTY SESSIONS INCLUDE:

FOUNDING PARTNERS

REGISTER: businessinsurance.com/WCF2016

DIAMOND

LUNCHEON SPONSOR

GOLD

SILVER