captives: an introduction - john hancock financial · captives: an introduction brian mccarthy ......

TRANSCRIPT

Insert logo of client, prospect, consultant, network partner(to be done in the slide master)

Captives: An Introduction

Brian McCarthyAssistant Vice PresidentIGP Boston

IGP Seminar – Boston 2012

Agenda

• Introduction to Captive Reinsurance

• IGP Experience & Organization

• IGP Captive Capabilities

• Further Considerations…

2

Introduction: What is a Captive?

“A closely held insurance company whose business is primarily provided by and controlled by its owners, and in which the

original insureds are the principal beneficiaries”

• Group’s subsidiary acting as (re-)insurance company

• Providing coverage for risks emanating from the activities of the group• Collecting premiums• Handling of claims• Establishing reserves

• Separate legal entity

3

Introduction: What is a Captive?

• There are several forms of Captives:• 100% subsidiary of the self-insured parent company• a "mutual" captive insuring the collective risks of members

of an industry• an "association" captive which self-insures individual risks

of the members of a professional, commercial or industrial association.

• Rent-a-Captive / Protected Cell Companies (PCC)

4

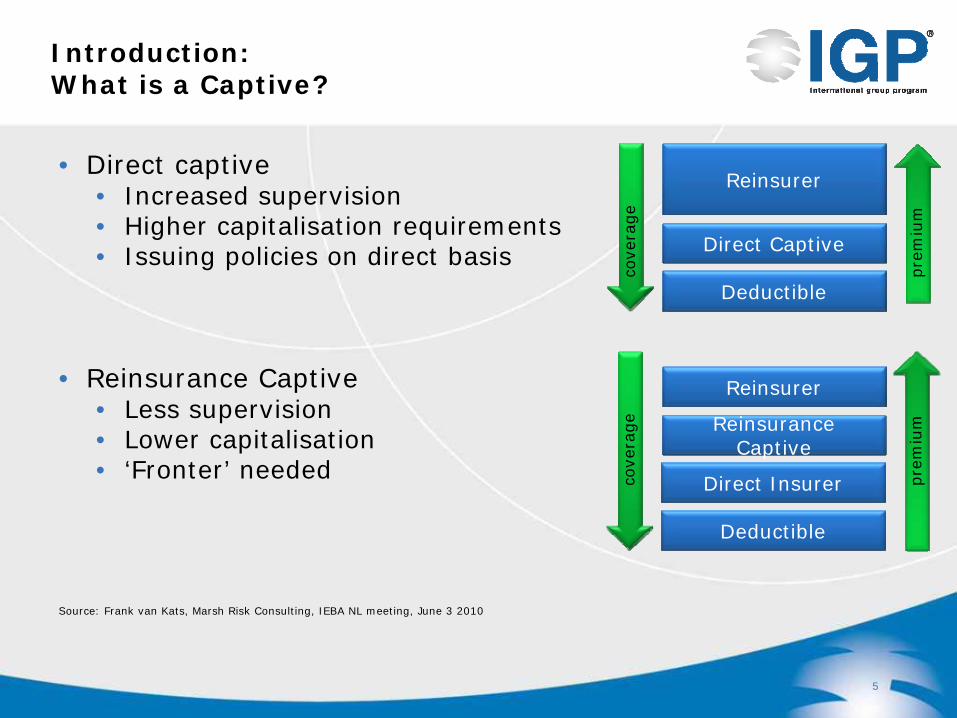

Introduction: What is a Captive?

• Direct captive• Increased supervision• Higher capitalisation requirements• Issuing policies on direct basis

• Reinsurance Captive• Less supervision• Lower capitalisation• ‘Fronter’ needed

Source: Frank van Kats, Marsh Risk Consulting, IEBA NL meeting, June 3 2010

5

Deductible

Direct Captive

Reinsurer

pre

miu

m

cove

rage

Deductible

Direct Insurer pre

miu

m

cove

rage Reinsurance

Captive

Reinsurer

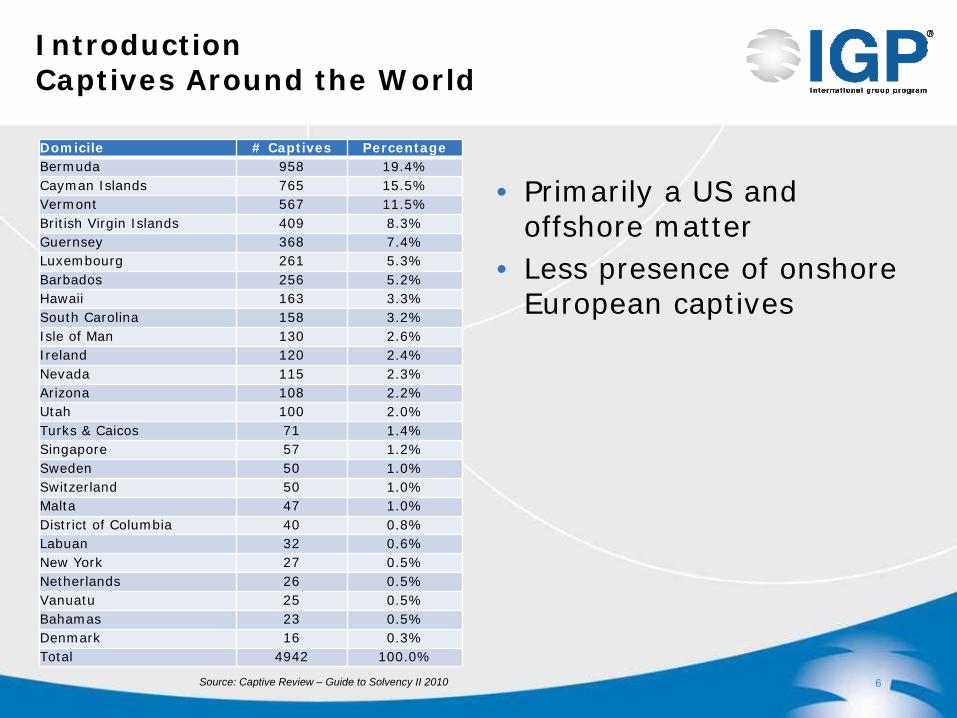

IntroductionCaptives Around the World

Domicile # Captives PercentageBermuda 958 19.4%Cayman Islands 765 15.5%Vermont 567 11.5%British Virgin Islands 409 8.3%Guernsey 368 7.4%Luxembourg 261 5.3%Barbados 256 5.2%Hawaii 163 3.3%South Carolina 158 3.2%Isle of Man 130 2.6%Ireland 120 2.4%Nevada 115 2.3%Arizona 108 2.2%Utah 100 2.0%Turks & Caicos 71 1.4%Singapore 57 1.2%Sweden 50 1.0%Switzerland 50 1.0%Malta 47 1.0%District of Columbia 40 0.8%Labuan 32 0.6%New York 27 0.5%Netherlands 26 0.5%Vanuatu 25 0.5%Bahamas 23 0.5%Denmark 16 0.3%Total 4942 100.0%

• Primarily a US and offshore matter

• Less presence of onshore European captives

6Source: Captive Review – Guide to Solvency II 2010

Introduction: Captive - Lines of Insurance

• Property damage

• Public and product liability

• Professional indemnity,

• Employers' liability,

• Workers’ compensation

• Motor insurance

• and … employee benefits!

7

Example Captive Company ABCLines of Business

8

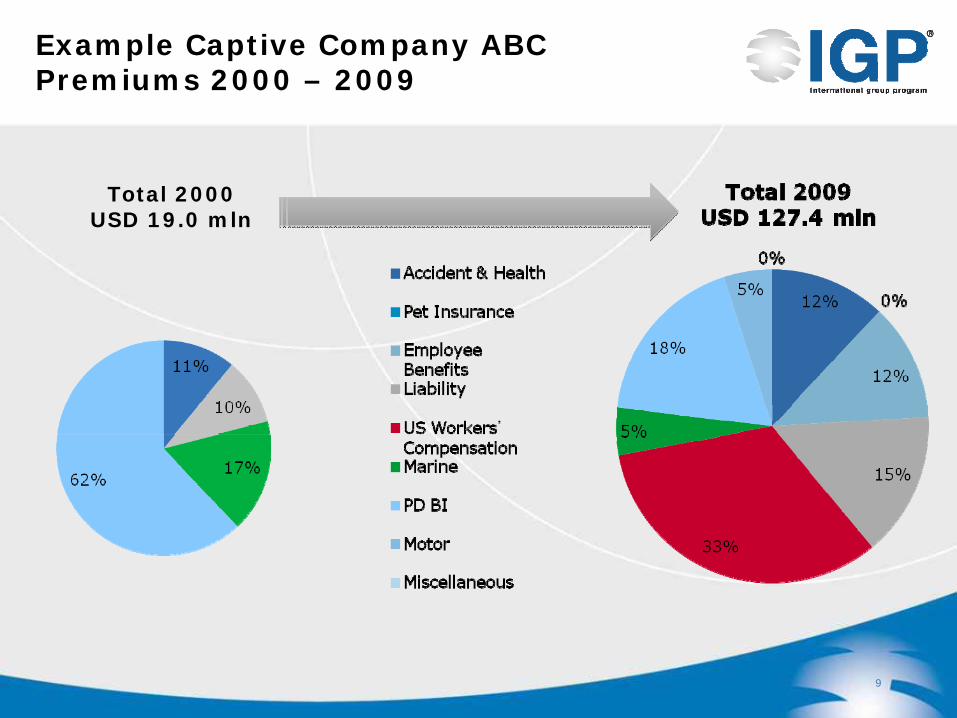

Example Captive Company ABCPremiums 2000 – 2009

9

Total 2000USD 19.0 mln

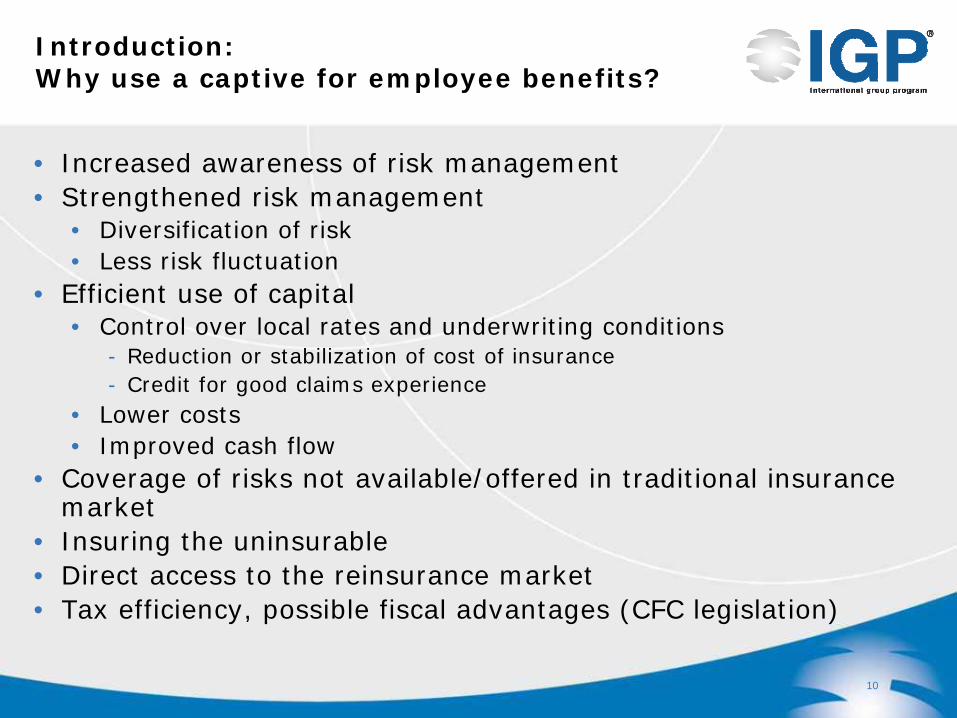

Introduction: Why use a captive for employee benefits?

• Increased awareness of risk management • Strengthened risk management

• Diversification of risk• Less risk fluctuation

• Efficient use of capital• Control over local rates and underwriting conditions

- Reduction or stabilization of cost of insurance- Credit for good claims experience

• Lower costs• Improved cash flow

• Coverage of risks not available/offered in traditional insurancemarket

• Insuring the uninsurable• Direct access to the reinsurance market• Tax efficiency, possible fiscal advantages (CFC legislation)

10

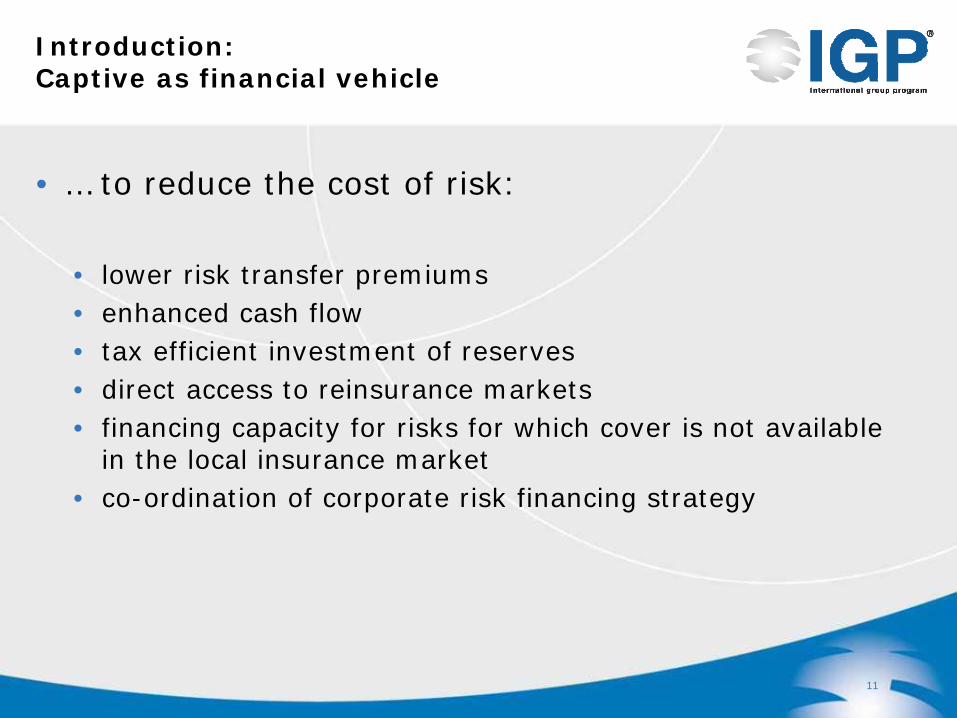

Introduction: Captive as financial vehicle

• … to reduce the cost of risk:

• lower risk transfer premiums• enhanced cash flow • tax efficient investment of reserves• direct access to reinsurance markets• financing capacity for risks for which cover is not available

in the local insurance market• co-ordination of corporate risk financing strategy

11

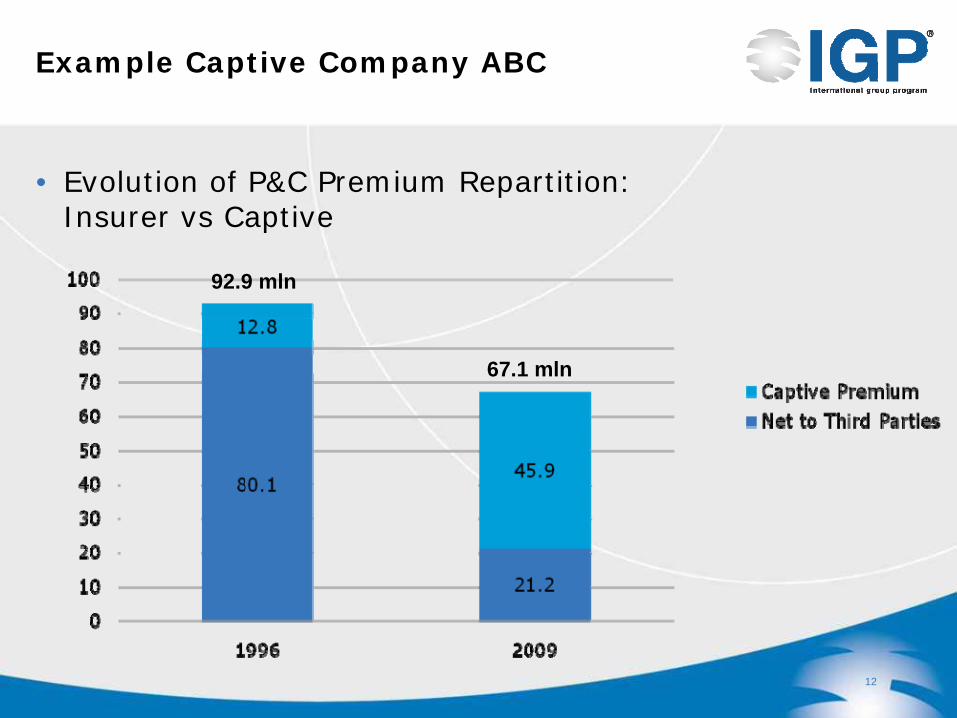

Example Captive Company ABC

• Evolution of P&C Premium Repartition:Insurer vs Captive

12

92.9 mln

67.1 mln

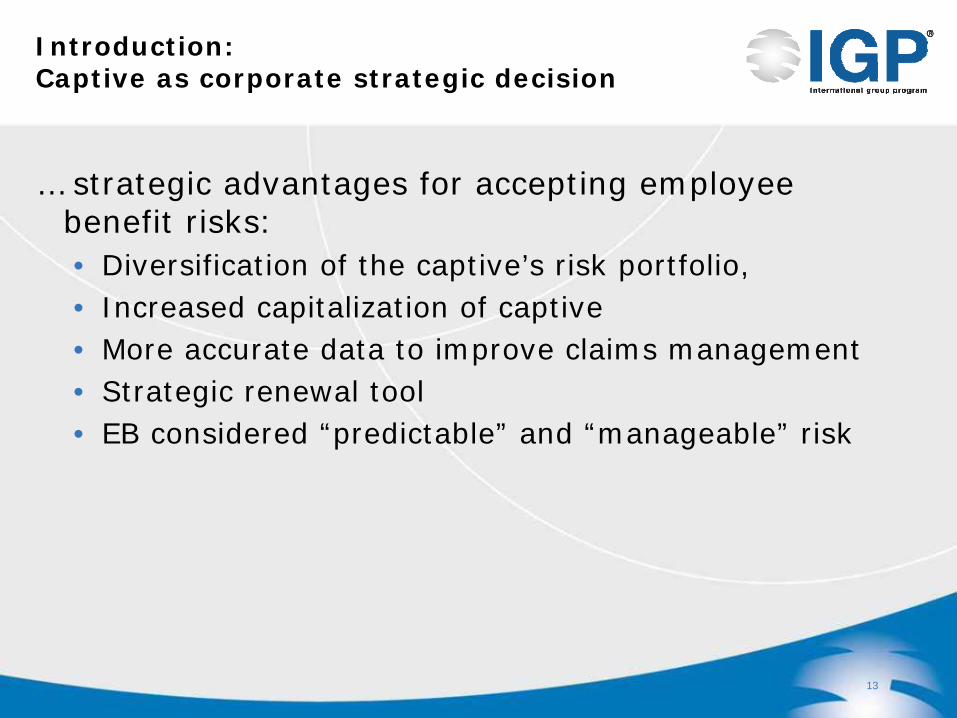

Introduction: Captive as corporate strategic decision

… strategic advantages for accepting employee benefit risks:• Diversification of the captive’s risk portfolio,• Increased capitalization of captive• More accurate data to improve claims management• Strategic renewal tool• EB considered “predictable” and “manageable” risk

13

Agenda

• Introduction to Captive Reinsurance

• IGP Experience & Organization

• IGP Captive Capabilities

• Further Considerations…

14

IGP Experience & Organisation

• IGP systems geared to captive retrocession through reinsurance system• Assuming reinsurance on more than 5,000 employee

benefits programs in over 60 countries.• Retro-ceding reinsurance on hundreds of employee

benefits programs

• Involved in captive reinsurance since 1981

• Systems and procedures in place for years

15

IGP’s Captive CapabilitiesRetrocession Agreement

• IGP Reinsurance Agreements between John Hancock and the IGP Network Partners continue to apply• Local plans are insured with Network Partners, and reinsured

to John Hancock• One single Retrocession Agreement

• Between- John Hancock Life Insurance Company (U.S.A.)

• subject to the laws of the state of Massachusetts- Client’s Captive

• Covers...- Inclusion of coverages- Transferred/Retained Premium coverage- International Year End Statements & Settlements- Minimum Requirements for Transfer of Premium- Initial Reports and Other Data- Duration & Termination

16

IGP Experience & OrganisationOur Role

• John Hancock is the contractual partner to the Captive

• John Hancock is the network leader• Inform and instruct Network Partners

• John Hancock acts as Third Party Administrator• Premium Transfer• Claims reimbursement• End-of-Year Settlement• Monitoring Performance

• IGP Network Partners = fronting insurers• Competitive & tailor-made quotations• Transferring premiums and reporting claims to IGP

17

IGP Experience & OrganisationA Dedicated Account Management Team

• Role of the IGP Account Team:• “Single” point of contact for the client & consultant• Proactively support client & consultant in line with the set

Captive (& Pool) Strategy• Co-ordinate action plan, reporting, proposal requests with

client, consultant and IGP Network Partners• Maintain regular communication with client & consultant

• Support from Special Projects Team since 2010

18

ImplementationIGP’s Captive Specialist Team

19

Captive Project Management•Brian McCarthy•Director Account Development•+1 617 572 86 55•[email protected]

Captive Project Management•Brian McCarthy•Director Account Development•+1 617 572 86 55•[email protected]

Captive Project Management•Tamara Laanen•Assistant Director Sales & Service•+32 2 775 29 61•[email protected]

Captive Project Management•Tamara Laanen•Assistant Director Sales & Service•+32 2 775 29 61•[email protected]

• Winston Richie• Director Technical Services• +1 617 572 86 55• [email protected]

• Winston Richie• Director Technical Services• +1 617 572 86 55• [email protected]

• Colby Johnston• Director Administration Services• +1 617 572 50 63• [email protected]

• Colby Johnston• Director Administration Services• +1 617 572 50 63• [email protected]

• Deborah Griffin• Assistant Legal Counsel• +1 617 572 99 13• [email protected]

• Deborah Griffin• Assistant Legal Counsel• +1 617 572 99 13• [email protected]

• Inge Luyten• Senior Marketing Specialist• +32 2 775 29 51• [email protected]

• Inge Luyten• Senior Marketing Specialist• +32 2 775 29 51• [email protected]

Agenda

• Introduction to Captive Reinsurance

• IGP Experience & Organization

• IGP Captive Capabilities

• Further Considerations…

20

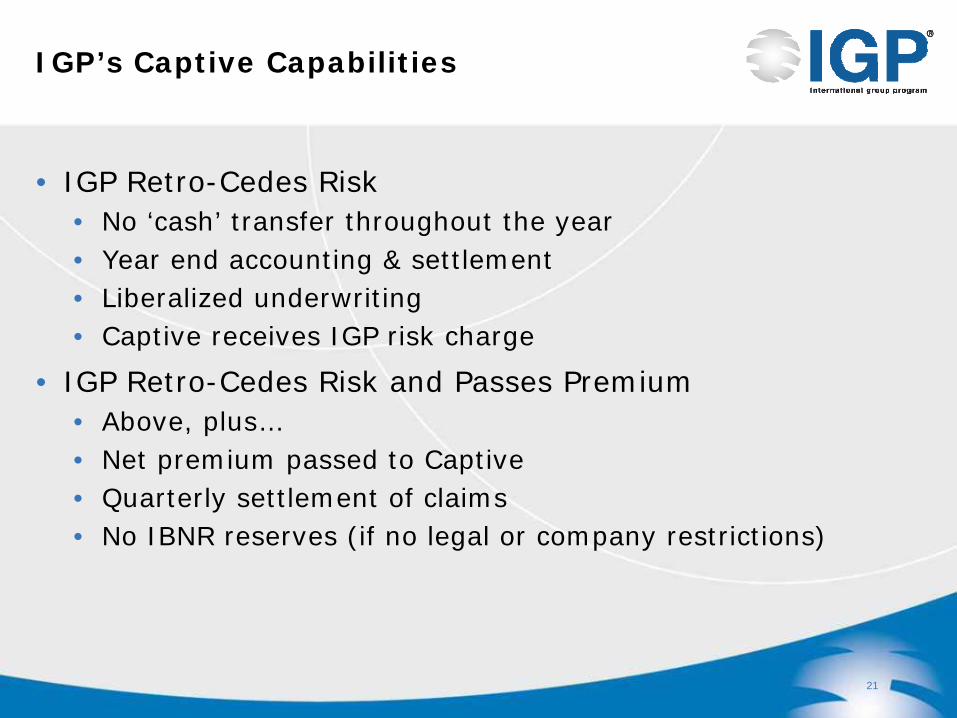

IGP’s Captive Capabilities

• IGP Retro-Cedes Risk• No ‘cash’ transfer throughout the year• Year end accounting & settlement• Liberalized underwriting• Captive receives IGP risk charge

• IGP Retro-Cedes Risk and Passes Premium• Above, plus…• Net premium passed to Captive• Quarterly settlement of claims• No IBNR reserves (if no legal or company restrictions)

21

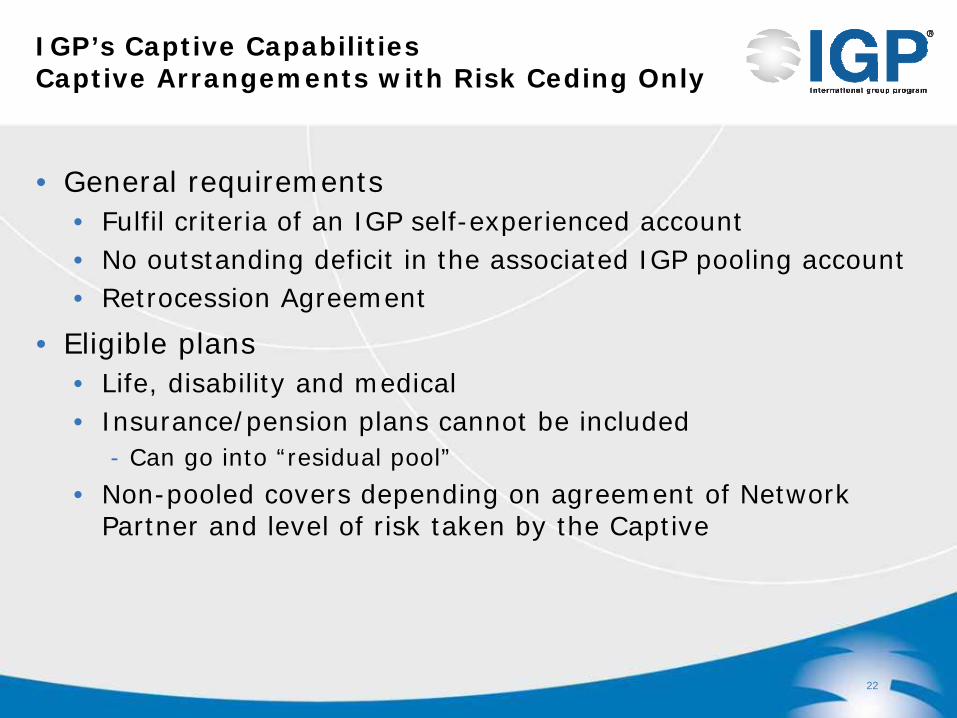

IGP’s Captive CapabilitiesCaptive Arrangements with Risk Ceding Only

• General requirements• Fulfil criteria of an IGP self-experienced account• No outstanding deficit in the associated IGP pooling account • Retrocession Agreement

• Eligible plans• Life, disability and medical• Insurance/pension plans cannot be included

- Can go into “residual pool”

• Non-pooled covers depending on agreement of Network Partner and level of risk taken by the Captive

22

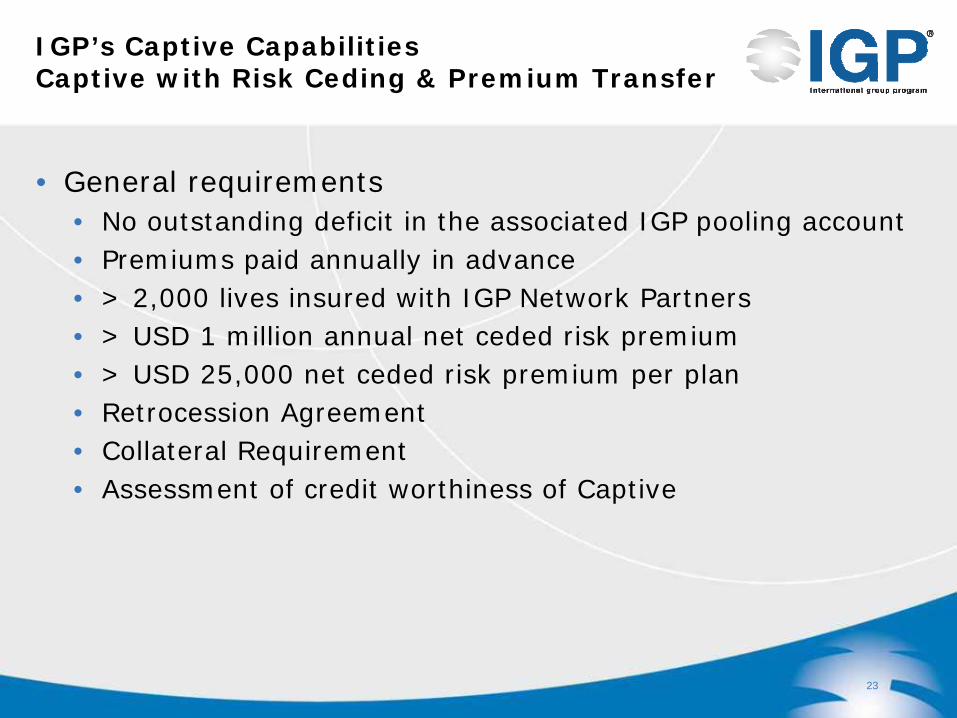

IGP’s Captive CapabilitiesCaptive with Risk Ceding & Premium Transfer

• General requirements• No outstanding deficit in the associated IGP pooling account• Premiums paid annually in advance• > 2,000 lives insured with IGP Network Partners• > USD 1 million annual net ceded risk premium• > USD 25,000 net ceded risk premium per plan• Retrocession Agreement• Collateral Requirement• Assessment of credit worthiness of Captive

23

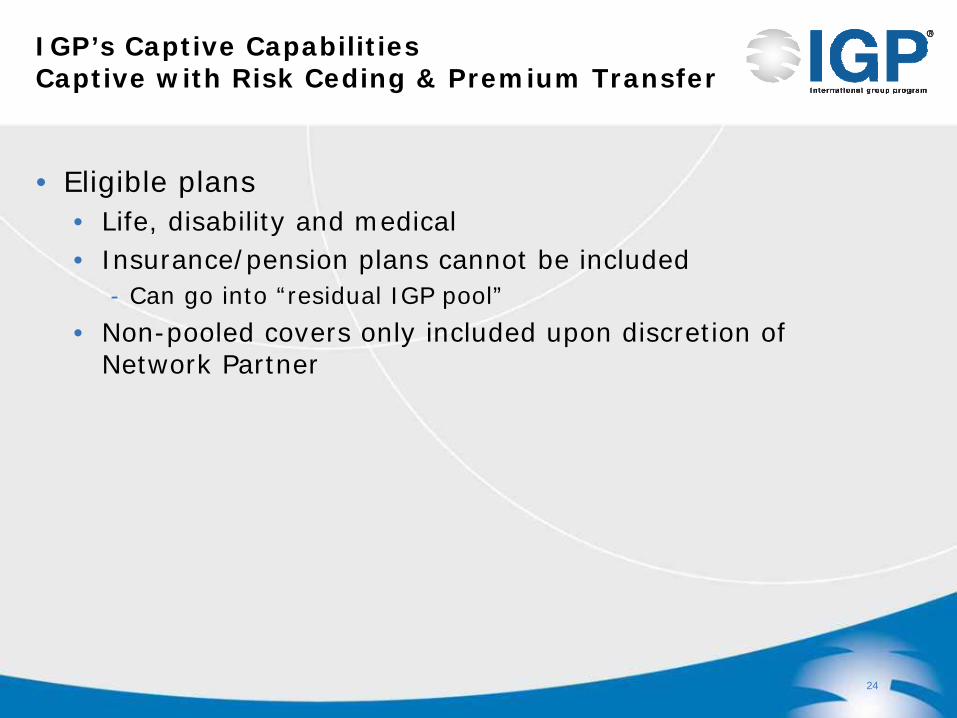

IGP’s Captive CapabilitiesCaptive with Risk Ceding & Premium Transfer

• Eligible plans• Life, disability and medical• Insurance/pension plans cannot be included

- Can go into “residual IGP pool”

• Non-pooled covers only included upon discretion of Network Partner

24

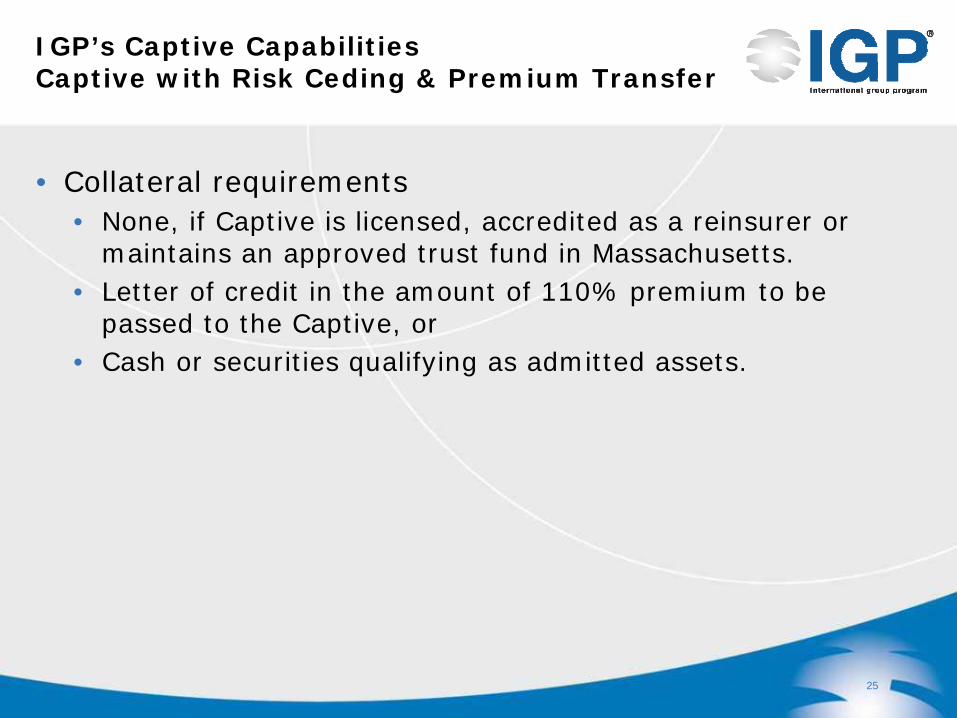

IGP’s Captive CapabilitiesCaptive with Risk Ceding & Premium Transfer

• Collateral requirements• None, if Captive is licensed, accredited as a reinsurer or

maintains an approved trust fund in Massachusetts. • Letter of credit in the amount of 110% premium to be

passed to the Captive, or• Cash or securities qualifying as admitted assets.

25

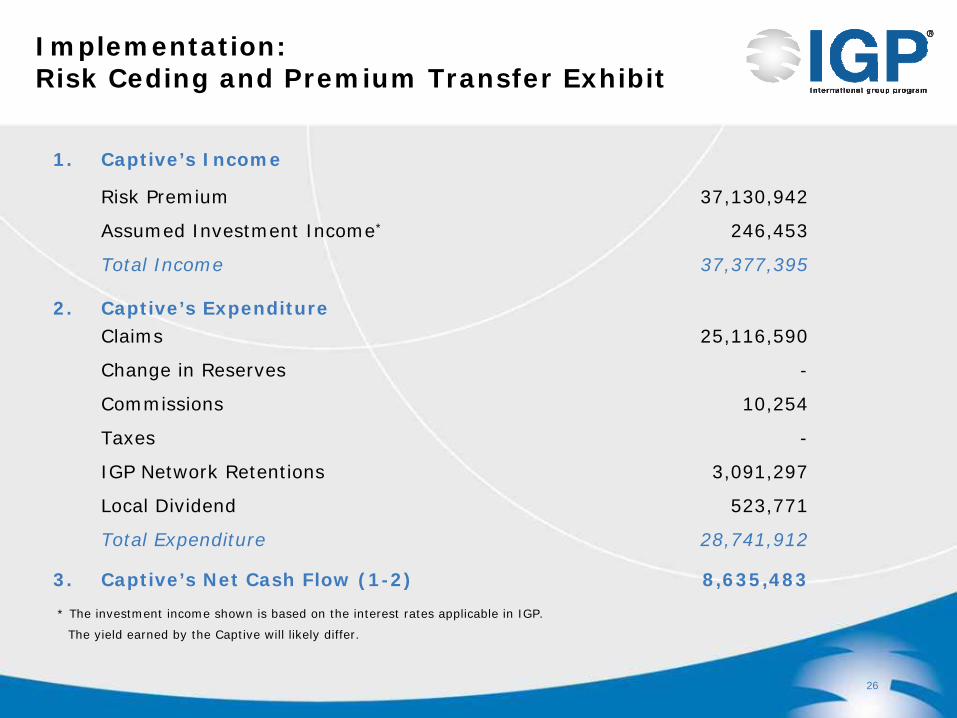

Implementation: Risk Ceding and Premium Transfer Exhibit

26

1. Captive’s Income

Risk Premium 37,130,942

Assumed Investment Income* 246,453

Total Income 37,377,395

2. Captive’s ExpenditureClaims 25,116,590

Change in Reserves -

Commissions 10,254

Taxes -

IGP Network Retentions 3,091,297

Local Dividend 523,771

Total Expenditure 28,741,912

3. Captive’s Net Cash Flow (1-2) 8,635,483

* The investment income shown is based on the interest rates applicable in IGP.

The yield earned by the Captive will likely differ.

Agenda

• Introduction to Captive Reinsurance

• IGP Experience & Organization

• IGP Captive Capabilities

• Further Considerations…

27

Further considerations...Captive Feasibility Study

• Time commitment

• Capital and solvency requirements

• Fiscal considerations / legislations

• Cooperation between HR and Risk Management

• Collateral requirements

Source: Frank van Kats, Marsh Risk Consulting, IEBA NL meeting, June 3 2010

28

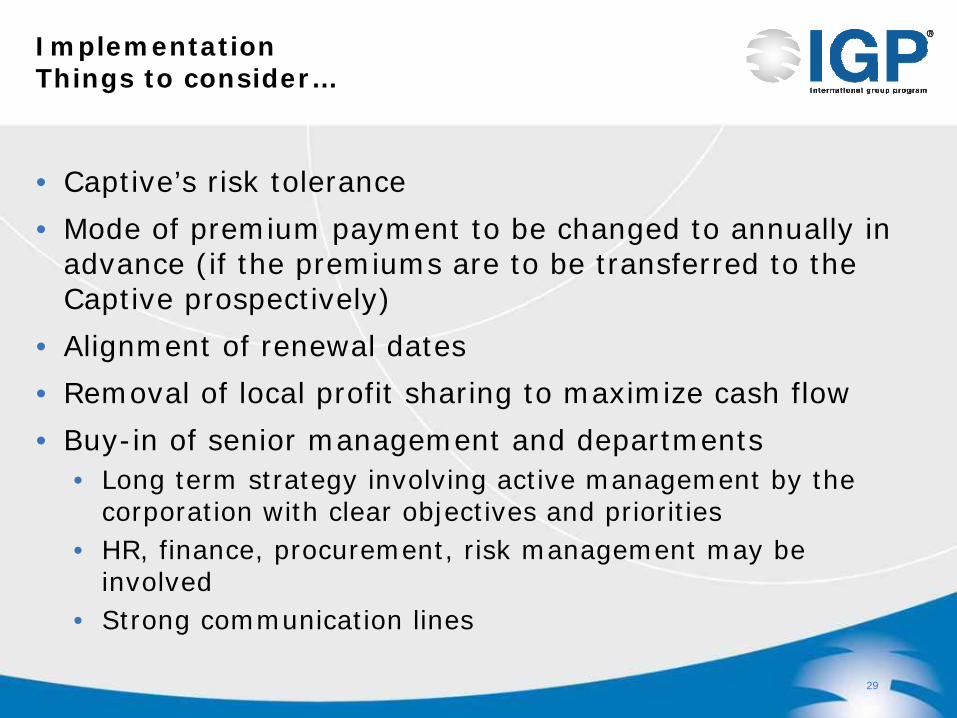

ImplementationThings to consider…

• Captive’s risk tolerance

• Mode of premium payment to be changed to annually in advance (if the premiums are to be transferred to the Captive prospectively)

• Alignment of renewal dates

• Removal of local profit sharing to maximize cash flow

• Buy-in of senior management and departments• Long term strategy involving active management by the

corporation with clear objectives and priorities• HR, finance, procurement, risk management may be

involved• Strong communication lines

29

Thank your for your attention.

• “IGP team showed flexibility and the willingness to listen to client preferences, even though these were not standard to IGP”

(Quote Consultant)

• “Excellent Relationship between client’s HQ and IGP. IGP showed eagerness to continue the relationship, and committed to delivery of results”

(Quote Consultant)

• “...Global IGP Captive Solution...best option”(Quote Client)

• “...IGP offers a long-term solution with a flexible structure...”(Quote Client)

30

Client Satisfaction...