capital link shipping weekly markets reportmaritime-connector.com/documents/capital link shipping...

TRANSCRIPT

1

Tuesday, January 19, 2016 (Week 3)

1

Tuesday, January 19, 2016 (Week 3)

IN THE NEWS Latest Company News

“Shipping Oracles event- an overview” by Barry Parker

CAPITAL MARKETS DATA Currencies, Commodities & Indices

Shipping Equities – Weekly Review

Dividend Paying Shipping Stocks

Weekly Equity Trading Statistics – by KCG

Global Shipping Company Bond Data

SHIPPING MARKETS Global Shipping Company Bond Profiles

Weekly Market Report – Allied Shipbroking Inc

Stifel Shipping Markets

Weekly Tanker Market Opinion, by Poten & Partners

Tanker Market - Weekly Highlights, by Charles R. Weber Company

Dry/Wet & TC Rates – Alibra Shipping

TERMS OF USE & DISCLAIMER

CONTENT CONTRIBUTORS

Capital Link Shipping

Weekly Markets Report

REGISTER

Capital Link - New York - London - Athens - Oslo New York - 230 Park Avenue, Suite 1536, New York, NY, 10169 Tel.: +1 212 661 7566 Fax: +1 212 661 7526London - Longcroft House,2-8 Victoria Avenue, London, EC2M 4NS, U.K Tel. +44(0) 203 206 1320 Fax. +44(0) 203 206 1321 Athens - 40, Agiou Konstantinou Str, Suite A 5, 151-24 Athens, Greece Tel. +30 210 6109 800 Fax +30 210 6109 801 Oslo - Raadhusgaten 25 P.O. Box 1904 Vika N-0116 Oslo, Norway

www.capitallink.comwww.capitallinkforum.com

www.CapitalLinkShipping.comA web based resource that provides information on the major shipping and stock market

Investor Relations & Financial Advisory

indices, as well as on all shipping stocks. It also features an earnings and conference call calendar, industry reports from major industry participants and interviews with CEOs, analysts and other market participants.

www.CapitalLinkWebinars.comSector Forums & Webinars: Regularly, we organize panel discussions among CEOs, analysts, bankers and shipping industry participants on the developments in the various shipping sectors (containers, dry bulk, tankers) and on other topics of interest (such as Raising Equity in Shipping Today, Scrapping, etc).

Capital Link Investor Shipping ForumsIn New York, Athens and London bringing together investors, bankers, financial advisors, listed companies CEOs, analysts, and shipping industry participants.

www.MaritimeIndices.comCapital Link Maritime Indices: Capital Link developed and maintains a series of stock market maritime indices which track the performance of U.S. listed shipping stocks (CL maritime Index, CL Dry Bulk Index, CL Tanker Index, CL Container Index, CL LNG/LPG Index, CL Mixed Fleet Index, CL Shipping MLP Index – Bloomberg page: CPLI. The Indices are also distributed through the Reuters Newswires and are available on Factset.

Capital Link Shipping Weekly Markets ReportWeekly distribution to an extensive audience in the US & European shipping, financial and investment communities with updates on the shipping markets, the stock market and listed company news.

Operating more like a boutique investment bank rather than a traditional Investor Relations firm, our objective is to assist our clients enhance long term shareholder value and achieve proper valuation through their positioning in the investment community. We assist them to determine their objectives, establish the proper investor outreach strategies, generate a recurring information flow, identify the proper investor and analyst target groups and gather investor and analyst feedback and related market intelligence information while keeping track of their peer group. Also, to enhance their profile in the financial and trade media.

Capital Link is a New York-based Advisory, Investor Relations and Financial Communications firm. Capitalizing on our in-depth knowledge of the shipping industry and capital markets, Capital Link has made a strategic commitment to the shipping industry becoming the largest provider of Investor Relations and Financial Communications services to international shipping companies listed on the US and European Exchanges. Capital Link's headquarters are in New York with a presence in London and Athens.

In our effort to enhance the information flow to the investment community and contribute to improving investor knowledge of shipping, Capital Link has undertaken a series of initiatives beyond the traditional scope of its investor relations activity, such as:

...Linking Shipping and Investors Across the GlobeCapital Link Shipping

2

Tuesday, January 19, 2016 (Week 3)

Monday, January 11, 2016

Gener8 Maritime, Inc. Announces Delivery of the Gener8 Apollo

and the Gener8 Supreme

Gener8 Maritime, Inc. (NYSE: GNRT), a leading U.S.-based provider

of international seaborne crude oil transportation services,

announced that it took delivery of the "ECO" VLCCs the Gener8

Apollo on January 5, 2016 and the Gener8 Supreme onJanuary 6,

2016 from Daewoo Shipbuilding & Marine Engineering and Shanghai

Waigaoqiao Shipbuilding Co., Ltd., respectively. The Gener8

Apolloand the Gener8 Supreme represent the fourth and fifth of 21

"ECO" VLCCs expected to be delivered into Gener8 Maritime's fleet.

Upon delivery, the Gener8 Apollo and Gener8 Supreme were

entered into Navig8's VL8 Pool.

http://ir.gener8maritime.com/2016-01-11-Gener8-Maritime-Inc-

Announces-Delivery-of-the-Gener8-Apollo-and-the-Gener8-Supreme

Don't ignore fleet age and new market dynamics, says Dorian

LPG

Older vessels can make room for new, and cargo demand is rising,

says one of the world's leading VLGC owners. The very large gas

carrier fleet includes more than 40 vessels over 20 years old, which

would be ideal candidates to be displaced if the influx of new

tonnage is not completely absorbed by increased demand, according

to leading VLGC owner Dorian LPG.

http://dorianlpg.investorroom.com/2016-01-11-Dorian-LPG-Dont-

Ignore-Fleet-Age

KNOT Offshore Partners LP Announces Fourth Quarter 2015

Earnings Results Conference Call

KNOT Offshore Partners LP (NYSE:KNOP) plans to release its

financial results for the fourth quarter of 2015 before opening of the

market on Thursday, February 18, 2016.

http://ir.knotoffshorepartners.com/investor-relations/Investor-

Information/news-releases/news-details/2016/KNOT-Offshore-

Partners-LP-Announces-Fourth-Quarter-2015-Earnings-Results-

Conference-Call/default.aspx

Tuesday, January 12, 2016

Scorpio Bulkers Inc. Announces Purchase of Common Shares

by Scorpio Services Holding Limited

Scorpio Bulkers, Inc. (NYSE: SALT) announced that Scorpio

Services Holding Limited ("SSH") has purchased an aggregate of

338,436 common shares of the Company at an average price of

$4.64 per share in the open market since the Company's previous

announcement on October 1, 2015. The Company currently has

28,697,366 common shares outstanding, of which SSH owns

2,238,228 or 7.80%.

http://ir.scorpiobulkers.com/press-releases/scorpio-bulkers-inc-

announces-purchase-of-common-shares-by-scorpio-services-hold-

nyse-salt-1238558

Seaspan Declares Quarterly Dividends on Common and

Preferred Shares

Seaspan Corporation (NYSE:SSW) announced that the Company's

Board of Directors has declared cash dividends on its common and

preferred shares

http://seaspan.mwnewsroom.com/Files/a8/a84b8ba9-7ffb-4272-

b46f-be98733ff7b7.pdf

Star Bulk Provides Updated Corporate Presentation

Star Bulk Carriers Corp. (Nasdaq: SBLK) a global shipping company

providing transportation solutions in the dry bulk sector, announced

that the Company has uploaded an updated corporate presentation

on the Company’s website, including updated cash and debt figures

as of December 31, 2015 and latest Capex schedule.

http://www.starbulk.com/UserFiles/sblk011216.pdf

Tsakos Energy Navigation Limited Declares Dividend on its

8.00% Series B and 8.875% Series C Cumulative Redeemable

Perpetual Preferred Shares

Tsakos Energy Navigation Limited (NYSE: TNP), a leading crude,

product, and LNG tanker operator, announced that its Board of

Directors declared regular quarterly cash dividends of $0.50 per

share for its 8.00% Series B Cumulative Redeemable Perpetual

Preferred Shares (the “Series B Preferred Shares”; NYSE; TNPPRB)

and approximately $0.5547 per share for its 8.875% Series C

Cumulative Redeemable Perpetual Preferred Shares (the “Series C

Preferred Shares”; NYSE; TNPPRC).

http://www.tenn.gr/en/about.html

Wednesday, January 13, 2016

Atwood Oceanics Announces First Quarter Earnings Guidance

Atwood Oceanics, Inc. (NYSE: ATW) provided earnings guidance for

its fiscal year 2016 first quarter ended December 31, 2015 due to

unusual market volatility.

http://ir.atwd.com/file.aspx?IID=4010374&FID=32527953

Diamond Offshore To Release Fourth Quarter 2015 Results on

February 8

Diamond Offshore Drilling, Inc. (NYSE: DO) announced that it will

issue a press release and host a conference call and webcast

related to its fourth quarter 2015 operating results on Monday,

February 8, 2016. The conference call and webcast will begin at

7:30 a.m. CST and will include a discussion by management

regarding the Company's results of operation.

http://investor.diamondoffshore.com/phoenix.zhtml?c=78110&p=irol-

newsArticle&ID=2128904

Noble Corporation plc to Announce Fourth Quarter and Full

Year 2015 Results

Noble Corporation plc (NYSE: NE) announced it plans to report

financial results for the fourth quarter and full year 2015 on

Wednesday, February 3, 2016, after the close of trading on the New

York Stock Exchange. Copies of the Company's press release will

be available on the Noble Web site at www.noblecorp.com.

http://phx.corporate-ir.net/phoenix.zhtml?c=98046&p=irol-

newsArticle&ID=2128961

Scorpio Tankers Announces Upsizing of a Previously

Announced Credit Facility

Scorpio Tankers Inc. (NYSE: STNG) announced the upsizing of its

Latest Company News

IN THE NEWS

3

Tuesday, January 19, 2016 (Week 3)

previously announced ING Credit Facility.

http://ir.scorpiotankers.com/press-releases/scorpio-tankers-

announces-upsizing-of-a-previously-announced-credit-facility-nyse-

stng-1238833

Thursday, January 14, 2016

Diana Shipping Inc. Announces Time Charter Contract for m/v

Nirefs with Transgrain

Diana Shipping Inc. (NYSE: DSX), a global shipping company

specializing in the ownership of dry bulk vessels, announced that,

through a separate wholly-owned subsidiary, it entered into a time

charter contract with Transgrain Shipping B.V., Rotterdam, for one of

its Panamax dry bulk vessels, the m/v Nirefs. The gross charter rate

is US$4,600 per day, minus a 5% commission paid to third parties,

for a period of minimum eleven (11) months to about fourteen (14)

months. The charter is expected to commence tomorrow.

http://www.dianashippinginc.com/news/news-diana-shipping-inc-

announces-time-charter-contract-for-m-v-nirefs-with-transgrain

Ensco Rated #1 Offshore Driller for Sixth Consecutive Year in

Independent Customer Satisfaction Survey

For the sixth consecutive year, Ensco plc (NYSE: ESV) has earned

first place for total customer satisfaction in the Offshore Drilling

segment of the Oilfield Products & Services Customer Satisfaction

Survey conducted by EnergyPoint Research. The annual survey is

the industry benchmark for customer satisfaction in the global

oilfield.

http://www.enscoplc.com/news-and-media/press-releases/press-

release-details/2016/Ensco-Rated-1-Offshore-Driller-for-Sixth-

Consecutive-Year-in-Independent-Customer-Satisfaction-

Survey/default.aspx

Noble Corporation plc Provides Fleet Contract Status Update

Noble Corporation plc (NYSE:NE) today announced that its report of

drilling rig status and contract information has been updated as of

January 14, 2016. The report, titled "Fleet Status Report," can be

found on the Company's Web site www.noblecorp.com, under the

"Investor Relations" section of the Web site.

http://phx.corporate-ir.net/phoenix.zhtml?c=98046&p=irol-

newsArticle&ID=2129510

Overseas Shipholding Group Announces Waiver of

Supplemental Indenture Condition and Extension of Expiration

Date of Tender Offer and Consent Solicitation for Its 7.50%

Senior Notes Due 2024

Overseas Shipholding Group, Inc. (NYSE MKT:OSG, OSGB)

announced the further extension of the previously announced tender

offer (the “Tender Offer”) for any and all of its 7.50% Senior Notes

due 2024 (the “Notes”) and the solicitation of consents (“Consents”)

from registered holders of the Notes (the “Consent Solicitation”) to

amend the indenture governing the Notes to affirm that for the

purposes of the restriction in such indenture on the Company’s

ability to dispose of assets, the Company’s international operations,

held through its subsidiary OSG International, Inc., do not constitute

substantially an entirety of the Company’s assets (the “Proposed

Amendment”).

http://ir.osg.com/phoenix.zhtml?c=82053&p=irol-

newsArticle&ID=2129535

Safe Bulkers, Inc. Declares Quarterly Dividend on its 8.00%

Series B Cumulative Redeemable Perpetual Preferred Shares;

8.00% Series C Cumulative Redeemable Perpetual Preferred

Shares; 8.00% Series D Cumulative Redeemable Perpetual

Preferred Shares

Safe Bulkers, Inc. (NYSE: SB), an international provider of marine

drybulk transportation services, announced that the Company's

Board of Directors has declared:

• A cash dividend of $0.50 per share on its 8.00% Series B

Cumulative Redeemable Perpetual Preferred Shares (the “Series B

Preferred Shares”) (NYSE: SB.PR.B) for the period from October 30,

2015 to January 29, 2016;

• A cash dividend of $0.50 per share on its 8.00% Series C

Cumulative Redeemable Perpetual Preferred Shares (the “Series C

Preferred Shares”) (NYSE: SB.PR.C) for the period from October 30,

2015 to January 29, 2016;

• A cash dividend of $0.50 per share on its 8.00% Series D

Cumulative Redeemable Perpetual Preferred Shares (the “Series D

Preferred Shares”) (NYSE: SB.PR.D) for the period from October 30,

2015 to January 29, 2016.

http://www.safebulkers.com/sbpr011416.pdf

Friday, January 15, 2016

Diana Shipping Inc. Announces Time Charter Contract for m/v

Aliki with SwissMarine

Diana Shipping Inc. (NYSE: DSX), a global shipping company

specializing in the ownership of dry bulk vessels, announced that,

through a separate wholly-owned subsidiary, it entered into a time

charter contract with SwissMarine Services S.A., Geneva, for one of

its Capesize dry bulk vessels, the m/v Aliki. The gross charter rate is

US$5,300 per day, minus a 5% commission paid to third parties, for

a period of minimum eleven (11) months to maximum fourteen (14)

months. The charter is expected to commence tomorrow.

http://www.dianashippinginc.com/news/news-diana-shipping-inc-

announces-time-charter-contract-for-m-v-aliki-with-swissmarine

Dryships Announces Availability of Notice of Special Meeting

and Proxy Statement

DryShips Inc. (NASDAQ: DRYS), an international owner of drybulk

carriers and offshore support vessels, announced the availability of

the Notice of Special Meeting and Proxy Statement for the

Company’s Special Meeting of Shareholders, to be held at the

Company’s offices located at 109 Kifisias Avenue & Sina Street, GR

151 24, Marousi, Athens, Greece, on Friday, February 19, 2016 at

4:00 p.m., local time. The Notice of Special Meeting and Proxy

Statement were mailed on or about January 15, 2016 to

shareholders of record as of January 8, 2016, and can also be found

on the Company’s website at:

http://dryships.irwebpage.com/2016_Special_Meeting_of_Sharehold

ers.html.

http://dryships.irwebpage.com/press/dryspr011516.pdf

Trading Update

Euronav NV (NYSE: EURN & Euronext: EURN) takes the

opportunity to update investors on current market conditions in the

Latest Company News

IN THE NEWS

4

Tuesday, January 19, 2016 (Week 3)

large tanker market.

http://www.euronav.com/Documents/IR/Press%20Releases/2016011

5_Trading%20Update.pdf

SDRL - Announces Agreement with DSME Shipyard

Seadrill Limited ("SDRL") announces that an agreement with DSME

shipyard has been reached to defer the delivery of two ultra-

deepwater drillships, the West Aquila and West Libra, until the

second quarter of 2018 and first quarter of 2019 respectively.

http://www.seadrill.com/investor-relations/news/pr-

story.aspx?ResultPageURL=http://cws.huginonline.com/S/135817/P

R/201601/1979043.xml

Safe Bulkers, Inc. Receives Share Price Continued Listing

Standard Notice from NYSE

Safe Bulkers, Inc. (NYSE: SB), an international provider of marine

drybulk transportation services, announced that the Company was

notified by the New York Stock Exchange (“NYSE”) that the trading

price of shares of the Company’s common stock, listed on the NYSE

as “SB”, is not in compliance with the NYSE’s continued listing

standard that requires a minimum average closing price of $1.00 per

share over a period of 30 consecutive trading days. The NYSE

notification has no impact on the Company’s business operations.

http://www.safebulkers.com/sbpr011516.pdf

KNOT Offshore Partners LP Announces Fourth Quarter 2015

Cash Distribution

KNOT Offshore Partners LP (NYSE:KNOP) announced that its

Board of Directors has declared a quarterly cash distribution with

respect to the quarter ended December 31, 2015, of $0.52 per unit.

http://ir.knotoffshorepartners.com/investor-relations/Investor-

Information/news-releases/news-details/2016/KNOT-Offshore-

Partners-LP-Announces-Fourth-Quarter-2015-Cash-

Distribution/default.aspx

Monday, January 18, 2016

Scorpio Tankers Inc. Announces an Update on Its Securities

Repurchase Program

Scorpio Tankers Inc. (NYSE: STNG) announced an update on its

Securities Repurchase Program.

http://ir.scorpiotankers.com/press-releases/scorpio-tankers-inc-

announces-an-update-on-its-securities-repurchase-program-nyse-

stng-1239405

Latest Company News

IN THE NEWS

5

Tuesday, January 19, 2016 (Week 3)

IN THE NEWS

Contributed by

Barry Parker Barry Parker is a financial writer and

analyst. His articles appear in a number of

prominent maritime periodicals including

Lloyds List, Fairplay, Seatrade, and

Maritime Executive and Capital Link

Shipping.

New York Maritime Inc. (NYMAR) hosted a session billed as “The Oracles

of shipping: A look at 2016”. kicking off its schedule of events for the new

year. A quick brush-up on Greek lore suggests that the wisdom imparted

by the ancient Greek oracles, most notably from Delphi, required some

parsing; ie it was not “actionable” at the outset. So it goes with NYMAR;

there was a lot of knowledge on the panel, but some review and

interpretation is necessary the wisdom of NYMAR’s sages may need

further evaluation, and interpretation. Like everything with shipping, there

are nuances. What a great event though. The investment bank Jefferies

provided both the venue, and the moderator- shipping banker Jeff Pribor.

The panel of Oracles covered the entire waterfront- ranging from drybulk,

tankers, containers, banking with a splash of offshore oil and marine

insurance.

Bob Burke, the Chief Executive Officer of Ridgebury Tankers, was looking

ahead to clear sailing in both the crude and product tanker sectors, which

he described as “inter-related”, “unless the orderbook is overheating.” He

talked about the entire oil distribution system being clogged, noting that

1.5 million barrels/ day of crude oil production in excess of demand must

be stored, including on tankers. The lifting of the Iranian embargo may

have been mentioned- if so, for just a millisecond and I missed it- its

possible impacts are presently confounding tanker market watchers as

the hires have backed down. There’s uncertainty concerning cargo flows;

how fast will Iran ramp up (some experts suggest that they can get to

500,000 barrels/ day quickly)? And then we have that Iranian tanker fleet-

will those vessels come onto the spot market, and if so, what exactly is

their deliverability? Or, will those holding barrels in storage continue to

hold them? We invited opinions on the Iran situation from experts on

economics and statistics related to vessels; nothing heard back. By the

way, Mr. Burke continues to look for a low oil price throughout 2016; he

was at the low end of the range in a poll of the Oracles on the likely oil

price at end 2016; guesses ranged from $25/barrel to $60/barrel. Mr.

Burke also opined on the newly allowed U.S. crude oil exports, saying that

with they would bring no benefit to the tanker market right now- with the

price of U.S. oil (West Texas Intermediate) at parity with the worldwide

market (Brent oil). Based on this view, the spread would probably not

deviate too far from parity- so if this line of Oracling is correct- don’t look

for headlines in the shipping media, or the mainstream media, on the topic

of U.S. crude exports.

A U.S. Merchant Marine Academy classmate of Bob Burke’s, maritime

lawyer Peter McLauchlan, partner in the Houston law office of Gardere

Wynne & Sewell LLP, talked about the energy space, where there is

something like “$70 billion of active bankruptcy filings” as participants in

all aspects of production, including the offshore energy sector, restructure.

It was not all doom and gloom. When talking about big offshore projects

(such as those undertaken by the energy majors in the Gulf of Mexico), he

acknowledged that “…multi-year projects just don’t stop.” The panel also

included insurance representative Joe Hughes, from the Shipowners

Claims Bureau- the managers of the American Club (based downtown),

who talked about insurance being “…a bright spot for shipowners”- with

relatively benign increases in recent years.

Kevin Kennedy, another classmate of Burke’s from Kings Point (and later

a colleague at GE Capital, where Burke worked prior to striking out on his

own) who is now Managing Director of container shipping fund packager

MC Seamax, described a gloomy outlook for the container sector, which

he described as “driven by oversupply”. Mr. Kennedy, who was

Shipping Oracles event- an overview

previously the CFO at Seaspan, waxed enthusiastic on shipowners who

charter vessels out…”the liners generally pay”. He noted a bifurcation

among listed companies, with dividends to shareholders being sustained

by some, in spite of the weak markets.

The Oracles also delved heavily into ship finance, which was what much

of NYMAR ‘s membership, heavily involved in finance and capital raising,

had really come to hear. Banker Martin Lunder, from Nordea, emphasized

his bank’s participation in a large tanker financing, but acknowledged that

“…we’ll be busy with amendments and waivers…” when it comes to

drybulk, a sector clearly in trouble. The question of new capital sources

for shipping is often discussed at such venues as the industry has been

taking $100 billion of new debt each year, according to his numbers. Mr.

Lunder said that Export Credit Agencies (ECAs) have filled part of the

funding vacuum as shipping banks have pulled back; The panelists then

discussed the impact of professional investors owning ships; Kevin

Kennedy noted much more liquid markets for trading debt than previously

(indeed such liquidity has been the cornerstone of various “loan to own”

schemes that have enabled a number of once high flyers to restructure,

and live to fight another day, albeit with different owners).

Distressed selling of assets is another topic that comes up frequently at

such events. The moderator, Jeff Pribor , postulated what might happen

in the realm of asset sales, where non-emotional private equity investors

are involved. Unlike family businesses, the traditional model for shipping

company ownership, professional investors might not be positioning for

the next cycle (unlike closely owned companies which will wait out bad

markets before handing off the helm to the next generation). Lambros

Papaeconomou, an excellent analyst and, these days, a top shipping

journalist, implored companies to recognize their problems, and then

suggested that: “Chapter 11 is not the worst thing…” for companies that

are restructuring their debt.

Hamish Norton, President of Star Bulk Carriers (and previously a shipping

banker at Jefferies) summarized drybulk with a well known Monty Python

skit that evokes images of the Black Death, on a video clip. No

Powerpoints for this group! After the chants of “…almost dead…” Mr.

Norton added that the market is as bad as Mr. Petros Pappas (a longtime

shipping man, now the Chairman at Star Bulk, a listed entity) can

remember.

So, what to make of the Oracles, and all the folks in the standing room

only conference room who came to listen to them? Yogi Berra quotes, like

difficulties forecasting the future, come quickly to mind. But the evening

was about much more than predicting oil prices (there was some of that)

and levels of the Baltic Dry Index. New York has a vibrant community of

finance, legal and other specialists who are devoted to maritime

businesses. But, despite adversity plaguing parts of the market (not all),

the culture is “half full”, rather than half empty, full of clever professionals

who can see the positives in the murky atmosphere that true Oracles must

breath from, and turn them into real action.

6

Tuesday, January 19, 2016 (Week 3)

Dividend Paying Shipping Stocks Stock Prices as of January 15, 2016

CAPITAL MARKETS DATA

Company Name Ticker Quarterly

Dividend

Annualized

Dividend

Last Closing Price

(January 15, 2016)

Annualized

Dividend Yield

Container

Costamare Inc CMRE $0.29 $1.16 6.93 0.17

Diana Containerships DCIX $0.0025 $0.01 0.54 0.02

Global Ship Lease GSL $0.10 $0.40 1.79 0.22

Seaspan Corp SSW $0.375 $1.50 14.06 0.11

Dry Bulk

Navios Maritime Holdings Inc. NM $0.06 $0.24 0.86 0.28

Safe Bulkers Inc. SB $0.01 $0.04 0.35 0.11

Tankers

Ardmore Shipping Corp. ASC $0.31 $0.40 9.20 0.13

DHT Holdings, Inc. DHT $0.18 $0.72 5.51 0.13

Euronav NV EURN $0.62* $1.24 10.09 0.12

Navios Maritime Acquisition Corp NNA $0.05 $0.20 2.07 0.10

Nordic American Tankers Limited NAT $0.38 $1.52 13.03 0.12

Scorpio Tankers Inc STNG $0.125 $0.50 5.74 0.09

Teekay Tankers Ltd TNK $0.03 $0.12 4.23 0.03

Tsakos Energy Navigation Ltd TNP $0.06 $0.24 5.66 0.04

Mixed Fleet

Ship Finance International Limited SFL $0.45 $1.80 13.40 0.13

Teekay Corporation TK $0.55 $2.20 6.18 0.36

LNG/LPG

GasLog Ltd GLOG $0.14 $0.56 6.34 0.09

Golar LNG GLNG $0.45 $1.80 13.56 0.13

Maritime MLPs

Capital Product Partners L.P. CPLP $0.2385 $0.954 3.73 0.26

Dynagas LNG Partners DLNG $0.4225 $1.69 7.31 0.23

GasLog Partners LP GLOP $0.478 $1.912 11.13 0.17

Golar LNG Partners, L.P. GMLP $0.5775 $2.31 10.18 0.23

Hoegh LNG Partners HMLP $0.3375 $1.35 13.58 0.10

KNOT Offshore Partners L.P. KNOP $0.52 $2.08 10.89 0.19

Navios Maritime Partners L.P. NMM $0.2125 $0.85 1.92 0.44

Navios Maritime Midstream Partners NAP $0.4225 $1.69 8.15 0.21

Teekay LNG Partners L.P. TGP $0.70 $2.80 9.99 0.28

Teekay Offshore Partners L.P. TOO $0.56 2.24 3.52 0.64

Offshore Drilling

Atwood Oceanics, Inc. ATW $0.075 $0.30 6.07 0.05

Diamond Offshore Drilling DO $0.125 $0.50 16.91 0.03

Ensco plc ESV $0.15 $0.60 10.30 0.06

Noble Corporation NE $0.15 $0.60 7.79 0.08

Rowan Companies RDC $0.10 $0.40 12.19 0.03

*Semi-annual dividend

7

Tuesday, January 19, 2016 (Week 3)

(1) Annual dividend percentage based upon the liquidation preference of the preferred shares.

* Prices reflected are since inception date:

Costamare Series D - 5/6/2015

Dynagas LNG Partners Series A – 7/13/2015

GasLog Series A – 3/30/2015

Teekay Offshore Series B – 4/13/2015

Tsakos Energy Series D – 4/22/2015

.

CAPITAL MARKETS DATA

Company Ticker

Amount

Issued

($m)

Type Annual

Coupon

Offer

Price

Current

Price

1/15/2016

Current Yield

(annualized)

%

change

last

week

52-week

range*

Costamare Series B CMRE PRB 50 perpetual 7.625% $25.00 $8.43 25.94% -19.02% $14.01-$26.20

Costamare Series C CMRE PRC 100 perpetual 8.50% $25.00 $40.05 23.72% -13.98% $15.26-$27.09

Costamare Series D CMRE PRD 100 perpetual 8.75% $25.00 $40.00 22.50% -15.02% $15.05-$25.05*

Diana Shipping Series B DSXPRB 65 perpetual 8.875% $25.00 $3.57 61.27% -14.58% $9.58-$25.59

Dynagas LNG Partners

Series A DLNGPRA 75 perpetual 9.000% $25.00 $2.70 79.86% -17.91% $14.80-$24.75*

GasLog Series A GLOGA 111 perpetual 8.75% $25.00 $19.54 10.24% -21.32% $15.61-$26.10*

Global Ship Lease

Series B GSLB 35 perpetual 8.75% $25.00 $6.84 29.24% -24.57% $8.43-$23.94

International

Shipholding Series A ISHPRA 25 perpetual 9.50% $100.00 $6.79 29.46% -18.27% $35.00-$105.00

Navios Maritime

Holdings Series G NMPRG 50 perpetual 8.75% $25.00 $24.45 9.71% -14.89% $25.00-$101.98

Navios Maritime

Holdings Series H NMPRH 120 perpetual 8.625% $25.00 $23.52 8.45% -39.90% $3.57-$26.50

Safe Bulkers Series B SBPRB 40 perpetual

step up 8.00% $25.00 $23.22 8.88% -51.87% $2.70-$22.37

Safe Bulkers Series C SBPRC 58 perpetual 8.00% $25.00 $11.00 16.48% -1.86% $13.00-$25.20

Safe Bulkers Series D SBPRD 80 perpetual 8.00% $25.00 $12.57 21.60% -17.09% $6.84-$21.28

Seaspan Series C SSWPRC 100 perpetual

step up 9.50% $25.00 $22.28 8.98% -17.70% $6.29-$21.30

Seaspan Series D SSWPRD 128 perpetual 7.95% $25.00 $21.25 10.44% -2.00% $24.36-$27.35

Seaspan Series E SSWPRE 135 perpetual 8.25% $25.00 $17.82 16.23% -1.09% $21.46-$26.60

Teekay Offshore Series

A TOOPRA 150 perpetual 7.25% $25.00 $8.43 25.94% -1.65% $22.92-$26.51

Teekay Offshore Series

B TOOPRB 125 perpetual 8.50% $25.00 $40.05 23.72% -16.98% $10.67-$23.67

Tsakos Energy Series B TNPPRB 50 perpetual

step up 8.00% $25.00 $40.00 22.50% -16.64% $12.57-$25.05*

Tsakos Energy Series C TNPPRC 50 perpetual 8.875% $25.00 $3.57 61.27% -7.17% $21.85-$25.80

Tsakos Energy Series D TNPPRD 85 perpetual 8.75% $25.00 $2.70 79.86% -10.67% $21.00-$26.42

Preferred Shipping Stocks Stock Prices as of January 15, 2016

8

Tuesday, January 19, 2016 (Week 3)

Indices Week ending January 15, 2016

CAPITAL MARKETS DATA

MAJOR INDICES

CAPITAL LINK MARITIME INDICES

America Symbol 1/15/2016 1/8/2016 % Change YTD % Change 2-Jan-15

Dow Jones INDU 15,988.08 16,346.45 -2.19 -10.35 17,832.99

Dow Jones Transp. TRAN 6,689.06 6,946.36 -3.70 -26.49 9,098.98

NASDAQ CCMP 4,488.42 4,643.63 -3.34 -5.04 4,726.81

NASDAQ Transp. CTRN 3,041.92 3,123.89 -2.62 -22.73 3,936.65

S&P 500 SPX 1,880.33 1,922.03 -2.17 -8.64 2,058.20

Europe Symbol 1/15/2016 1/8/2016 % Change YTD % Change 2-Jan-15

Deutsche Borse Ag DAX 9,545.27 9,849.34 -3.09 -2.25 9,764.73

Euro Stoxx 50 SX5E 2,952.48 3,033.47 -2.67 -5.96 3,139.44

FTSE 100 Index UKX 5,804.10 5,912.44 -1.83 -11.36 6,547.80

Asia/Pacific Symbol 1/15/2016 1/8/2016 % Change YTD % Change 2-Jan-15

ASX 200 AS51 4,892.80 4,990.84 -1.96 -9.99 5,435.93

Hang Seng HSI 19,520.77 20,453.71 -4.56 -18.18 23,857.82

Nikkei 225 NKY 17,147.11 17,697.96 -3.11 -1.74 17,450.77

Index Symbol 1/15/2016 1/8/2016 % Change YTD %

Change 2-Jan-15

Capital Link Maritime Index CLMI 836.86 952.53 -12.14 -63.13 2,270.00

Tanker Index CLTI 658.65 786.22 -16.23 -50.21 1,322.86

Drybulk Index CLDBI 164.79 225.80 -27.02 -73.53 622.45

Container Index CLCI 1,000.27 1,034.55 -3.31 -32.01 1,471.29

LNG/LPG Index CLLG 1,053.62 1,197.32 -12.00 -65.82 3,082.31

Mixed Fleet Index CLMFI 1,000.20 1,142.61 -12.46 -59.04 2,441.80

MLP Index CLMLP 856.53 1,024.19 -16.37 -70.29 2,882.73

*The Capital Link Maritime Indices were updated recently to adjust for industry changes. Dorian LPG Ltd (NYSE:LPG) became a member of Capital

Link LNG/LPG Index, GasLog Partners L.P. (NYSE:GLOP) became a member of Capital Link LNG/LPG Index and Capital Link MLP Index, Navios

Maritime Midstream Partners (NYSE:NAP) became a member of Capital Link MLP Index, Euronav NV (NYSE: EURN) became a member of Capital

Link Tanker Index, and Gener8 Maritime (NYSE: GNRT) became a member of Capital Link Tanker Index. Additionally, Capital Link Dry Bulk Index

reflects the stock name change of Baltic Trading Ltd (NYSE: BALT) to Genco Shipping & Trading Limited (NYSE: GNK).

9

Tuesday, January 19, 2016 (Week 3)

CAPITAL MARKETS DATA

TRANSPORTATION STOCKS

DRYBULK TICKER 1/15/2016

Friday

1/8/2016

Friday

Change

%

52 week

high

52 week

low 1/2/2015

Three Month

Avg. Volume

Genco Shipping & Trading Ltd GNK $1.01 $1.26 -19.84% N/A N/A N/A 268,327

Diana Shipping Inc DSX $2.48 $3.46 -28.32% $8.11 $2.15 $6.65 574,789

DryShips Inc DRYS $0.10 $0.12 -12.59% $1.06 $0.08 $1.13 4,621,186

Eagle Bulk Shipping Inc EGLE $2.05 $2.66 -22.93% $12.90 $2.05 $14.42 36,052

FreeSeas Inc FREE $0.44 $0.64 -30.90% $2,475.00 $0.31 $32.93 259,460

Globus Maritime Ltd GLBS $0.09 $0.20 -54.89% $2.35 $0.09 $2.30 14,687

Golden Ocean Group GOGL $0.71 $0.73 -2.16% $5.73 $0.64 $4.27 349,960

Navios Maritime Holdings Inc NM $0.86 $0.99 -13.15% $4.59 $0.72 $4.09 1,166,532

Navios Maritime Partners LP NMM $1.92 $2.37 -18.99% $13.89 $1.78 $11.01 1,060,199

Paragon Shipping Inc PRGN $0.11 $0.14 -21.43% $2.01 $0.09 $2.66 131,543

Safe Bulkers Inc SB $0.35 $0.46 -24.50% $4.00 $0.34 $3.84 399,240

Scorpio Bulkers SALT $3.65 $4.89 -25.36% $33.12 $3.01 $1.95 248,110

Seanergy Maritime SHIP $1.64 $2.89 -43.25% $6.75 $1.64 $0.90 2,549

Star Bulk Carriers Corp SBLK $0.43 $0.44 -3.18% $4.64 $0.36 $6.12 530,244

BALTIC INDICES

Index Symbol 1/15/2016 1/8/2016 % Change YTD %

Change 2-Jan-15

Baltic Dry Index BDIY 373 429 -13.05 -51.62 771

Baltic Capesize Index BCIY 198 343 -42.27 -56.58 456

Baltic Panamax Index BPIY 381 434 -12.21 -53.93 827

Baltic Supramax Index BSI 394 430 -8.37 -55.43 884

Baltic Handysize Index BHSI 245 256 -4.30 -49.80 488

Baltic Dirty Tanker Index BDTI 897 1,016 -11.71 1.36 885

Baltic Clean Tanker Index BCTI 707 716 -1.26 -8.77 775

TANKERS Ticker 1/15/2016 1/8/2016 Change % 52 wk

high

52 wk

low 1/2/2015

3-Month

Avg. Vol.

Ardmore Shipping Corp ASC $9.20 $10.83 -15.05% $14.79 $9.01 $12.00 321,211

Capital Product Partners LP CPLP $3.73 $4.74 -21.31% $9.94 $3.67 $7.97 539,933

DHT Holdings Inc DHT $5.51 $7.10 -22.39% $8.90 $5.51 $7.71 1,777,620

Euronav NV EURN $10.09 $12.07 -16.40% $16.32 $10.09 N/A 730,833

Frontline Ltd/Bermuda FRO $2.03 $2.45 -17.14% $3.54 $2.03 $2.51 2,456,444

Gener8 Maritime Inc GNRT $6.35 $7.99 -20.53% $14.37 $6.20 N/A 215,277

KNOT Offshore Partners KNOP $10.89 $13.88 -21.54% $26.42 $10.87 $23.21 125,854

Navios Acquisition NNA $2.07 $2.48 -16.53% $4.33 $2.07 $3.76 412,630

Navios Midstream Partners NAP $8.15 $8.66 -5.89% $17.70 $6.77 $13.39 107,465

Nordic American NAT $13.03 $14.65 -11.06% $17.27 $9.41 $10.21 1,827,108

Overseas Shipholding OSGB $2.84 $3.14 -9.55% $4.76 $2.84 $5.28 37,480

Scorpio Tankers Inc STNG $5.74 $6.55 -12.37% $11.55 $5.69 $8.54 2,549,853

Teekay Offshore Partners LP TOO $3.52 $4.68 -24.79% $24.42 $3.39 $26.00 929,590

Teekay Tankers Ltd TNK $4.23 $5.50 -23.09% $8.39 $4.22 $5.22 2,539,528

Top Ships TOPS $0.25 $0.30 -16.67% $1.26 $0.25 $1.11 20,537

Tsakos Energy Navigation Ltd TNP $5.66 $6.79 -16.64% $10.32 $5.64 $6.96 541,584

10

Tuesday, January 19, 2016 (Week 3)

CAPITAL MARKETS DATA

LPG/LNG Ticker 1/15/2016 1/8/2016 Change % 52 wk

high

52 wk

low 1/2/2015

3-Month

Avg. Vol.

Dynagas LNG Partners DLNG $7.31 $9.06 -19.32% $20.68 $6.86 $17.23 140,944

GasLog Ltd GLOG $6.34 $7.47 -15.13% $23.41 $6.34 $20.08 935,008

Gaslog Partners GLOP $11.13 $12.91 -13.79% $29.28 $10.99 $26.41 164,192

Golar LNG Ltd GLNG $13.56 $15.91 -14.77% $50.85 $13.26 $35.71 1,847,665

Golar LNG Partners LP GMLP $10.18 $11.70 -12.99% $29.70 $8.66 $31.93 527,022

Hoegh LNG Partners HMLP $13.58 $17.13 -20.72% $23.25 $12.84 $20.48 47,456

Navigator Gas NVGS $12.01 $12.28 -2.20% $22.06 $11.44 $20.19 208,533

StealthGas Inc GASS $2.72 $2.89 -5.88% $7.02 $2.63 $6.33 48,242

Teekay LNG Partners LP TGP $9.99 $11.97 -16.54% $40.69 $9.01 $42.91 587,285

MIXED FLEET Ticker 1/15/2016 1/8/2016 Change % 52 wk

high

52 wk

low 1/2/2015

3-Month

Avg. Vol.

Euroseas Ltd ESEA $2.36 $2.45 -3.67% $8.40 $2.31 $7.53 3,914

Ship Finance International Ltd SFL $13.40 $15.48 -13.44% $17.69 $13.30 $14.67 817,171

Teekay Corp TK $6.18 $7.89 -21.67% $50.88 $5.89 $50.05 2,215,555

MLPs Ticker 1/15/2016 1/8/2016 Change % 52 wk

high

52 wk

low 1/2/2015

3-Month

Avg. Vol.

Capital Product Partners CPLP $3.73 $4.74 -21.31% $9.94 $3.67 $7.97 539,933

Dynagas LNG Partners DLNG $7.31 $9.06 -19.32% $20.68 $6.86 $17.23 140,944

GasLog Partners GLOP $11.13 $12.91 -13.79% $29.28 $10.99 $26.41 164,192

Golar LNG Partners LP GMLP $10.18 $11.70 -12.99% $29.70 $8.66 $31.93 527,022

Hoegh LNG Partners HMLP $13.58 $17.13 -20.72% $23.25 $12.84 $20.48 47,456

Knot Offshore Partners KNOP $10.89 $13.88 -21.54% $26.42 $10.87 $23.21 125,854

Navios Maritime Midstream NAP $8.15 $8.66 -5.89% $17.70 $6.77 $13.39 107,465

Navios Partners NMM $1.92 $2.37 -18.99% $13.89 $1.78 $11.01 1,060,199

Teekay Offshore TOO $3.52 $4.68 -24.79% $24.42 $3.39 $26.00 929,590

Teekay LNG TGP $9.99 $11.97 -16.54% $40.69 $9.01 $42.91 587,285

OFFSHORE DRILL RIGS Ticker 1/15/2016 1/8/2016 Change % 52 wk

high

52 wk

low 1/2/2015

3-Month

Avg. Vol.

Atwood Oceanics ATW $6.07 $8.54 -28.92% $35.35 $5.83 $28.67 3,750,256

Diamond Offshore Drilling DO $16.91 $18.33 -7.75% $36.95 $16.72 $37.23 2,676,853

Ensco International ESV $10.30 $12.79 -19.47% $31.93 $9.80 $30.17 6,302,218

Hercules Offshore HERO $1.12 $1.81 -38.12% $276.79 $1.12 $276.79 75,527

Noble Corp. NE $7.79 $9.10 -14.40% $19.51 $7.77 $16.84 8,532,385

Ocean Rig UDW Inc ORIG $1.24 $1.41 -12.06% $9.29 $1.21 $9.42 1,070,325

Pacific Drilling PACD $0.35 $0.64 -46.06% $4.86 $0.35 $4.71 615,867

Rowan Companies RDC $12.19 $14.34 -14.99% $24.88 $11.89 $23.72 3,220,178

Seadrill Ltd. SDRL $2.34 $2.82 -17.02% $15.00 $2.33 $12.01 9,052,274

Transocean RIG $9.86 $10.75 -8.28% $21.39 $9.55 $18.12 10,476,684

Vantage Drilling Company VTGDF $0.00 $0.00 -52.24% $0.60 $0.00 $0.49 2,281,070

CONTAINERS Ticker 1/15/2016 1/8/2016 Change % 52 wk

high

52 wk

low 1/2/2015

3-Month

Avg. Vol.

Box Ships Inc TEUFF $0.12 $0.16 -23.42% $1.06 $0.12 $0.89 110,756

Costamare Inc CMRE $6.93 $8.19 -15.38% $20.35 $6.72 $17.61 248,801

Danaos Corp DAC $4.82 $5.16 -6.59% $6.62 $4.57 $5.57 30,708

Diana Containerships Inc DCIX $0.54 $0.66 -18.88% $2.66 $0.51 $2.03 88,139

Global Ship Lease Inc GSL $1.79 $2.51 -28.69% $6.29 $1.79 $4.65 119,924

Seaspan Corp SSW $14.06 $14.63 -3.90% $20.77 $14.06 $18.39 295,724

11

Tuesday, January 19, 2016 (Week 3)

OFFSHORE SUPPLY Ticker 1/15/2016 1/8/2016 Change % 52 wk

high

52 wk

low 1/2/2015

3-Month

Avg. Vol.

Gulfmark Offshore GLF $2.82 $3.16 -10.76% $21.83 $2.60 $24.80 574,568

Hornback Offshore HOS $7.34 $8.40 -12.62% $24.73 $7.01 $24.77 1,140,103

Nordic American Offshore NAO $3.60 $4.29 -16.08% $11.61 $3.56 $12.51 179,385

Tidewater TDW $5.49 $5.91 -7.11% $33.24 $5.22 $32.33 1,577,111

Seacor Holdings CKH $44.45 $45.92 -3.20% $77.65 $43.93 $74.10 147,641

OSLO-Listed Shipping Comps

(currency in NOK) Ticker 1/15/2016 1/8/2016 Change %

52 wk

high

52 wk

low 1/2/2015

3-Month

Avg. Vol.

Golden Ocean GOGL $6.79 $6.60 2.88% $44.80 $5.68 N/A N/A

Stolt-Nielsen Ltd. SNI $95.25 $102.50 -7.07% $142.50 $94.75 $124.50 34,953

Frontline Ltd. FRO $17.80 $21.85 -18.54% $28.93 $17.75 $19.40 3,308,582

Jinhui Shpg. & Trans JIN $5.97 $6.75 -11.56% $14.40 $5.58 $12.50 64,859

Odfjell (Common A Share) ODF $26.30 $26.80 -1.87% $29.50 $18.60 $31.00 109,151

American Shipping Co. AMSC $23.50 $24.30 -3.29% $43.97 $23.30 $33.30 112,518

Hoegh LNG HLNG $86.25 $90.75 -4.96% $132.50 $76.00 $84.75 125,292

I.M. Skaugen IMSK $1.90* $1.95 -2.56% $3.95 $1.87 $4.68 25,569

Western Bulk WBULK $1.35 $1.40 -3.57% $4.50 $1.27 $4.51 148,488

*As of 1/14/2016.

12

Tuesday, January 19, 2016 (Week 3)

Shipping Equities: The Week in Review SHIPPING EQUITIES UNDERPERFORM THE BROADER MARKET

During last week, shipping equities underperformed the broader market, with the Capital Link Maritime Index

(CLMI), a composite index of all US listed shipping stocks, down 12.14%, compared to the S&P 500 dropping

2.17%, Nasdaq decreasing 3.34%, and Dow Jones Industrial Average (DJII) diminishing 2.19%.

Container stocks were the best performers during last week, with Capital Link Container Index down 3.31%,

followed by Capital Link LNG/LPG Index decreasing 12.00%. Dry Bulk equities were the least performer during

last week, with Capital Link Dry Bulk Index falling 27.02%.

During last week, Dry Bulk shipping stocks underperformed the physical market, with Baltic Dry Index (BDI)

diminishing 13.05%, compared to the Capital Link Dry Bulk Index slumping 27.02%.

During last week, Baltic Dirty Tanker Index (BDTI) decreased 11.71%, and Baltic Clean Tanker Index (BCTI)

dropped 1.26%, compared to Capital Link Tanker Index falling 16.23%.

The Trading Statistics supplied by KCG Holdings, Inc. provide details of the trading performance of each

shipping stock and analyze the market’s trading momentum and trends for the week and year-to-date.

The objective of the Capital Link Maritime Indices is to enable investors, as well as all shipping market

participants, to better track the performance of listed shipping stocks individually, by sector or as an industry.

Performance can be compared to other individual shipping stocks, to their sector, to the broader market, as well

as to the physical underlying shipping markets or other commodities. The Indices currently focus only on

companies listed on US Exchanges providing a homogeneous universe. They are calculated daily and are

based on the market capitalization weighting of the stocks in each index. In terms of historical data, the indices

go back to January 2, 2005, thereby providing investors with historical performance.

There are seven indices in total; the Capital Link Maritime Index comprised of all 45 listed shipping stocks, and

six Sector Indices, the CL Dry Bulk Index, the CL Tanker Index, the CL Container Index, the CL LNG / LPG

Index, the CL Mixed Fleet Index and the CL Maritime MLP Index.

The Index values are updated daily after the market close and can be accessed at

www.CapitalLinkShipping.com or at or www.MaritimeIndices.com. They can also be found through the

Bloomberg page “CPLI” and Reuters.

CAPITAL MARKETS DATA

Get your message across to

36,000 weekly recipients around the globe

Join a select group of shipping & financial industry’s advertisers by promoting your

brand with Capital Link’s Shipping Weekly Markets Report.

For additional advertising information and a media kit, please contact/email:

Capital Link at +1 212 661-7566 or [email protected]

13

Tuesday, January 19, 2016 (Week 3)

MARITIME INDEX DAILY COMPARISON CHARTS (52 -WEEK )

*SOURCE: BLOOMBERG

CAPITAL MARKETS DATA

*Teekay Corp was removed from the Capital Link Tanker Index on Aug 28, 2014.

14

Tuesday, January 19, 2016 (Week 3)

Custom Statistics Prepared Weekly for Capital Link Shipping

BROAD MARKET

Percent Change of Major Indexes for the Week Ending Friday, January 15, 2016

Name Symbol Close Net Gain Percent Gain

S&P 500 Index SPX 1880.29 -41.74 -2.17%

Dow Jones Industrial Average Index INDU 15988.08 -358.37 -2.19%

Russell 1000 Index RUI 1038.02 -25.53 -2.40%

Russell 3000 Index RUA 1103.34 -28.24 -2.50%

Nasdaq-100 Index NDX 4141.08 -129.70 -3.04%

Nasdaq Composite Index COMPX 4488.42 -155.21 -3.34%

Russell 2000 Index RUT 1007.84 -38.36 -3.67%

Dow Jones Transportation Index TRAN 6689.06 -257.30 -3.70%

SHIPPING INDUSTRY DATA (43 Companies)

Moving Averages

• 2.50% closed > 10D Moving Average.

• 2.50% closed > 50D Moving Average.

• 2.50% closed > 100D Moving Average.

• 0.00% closed > 200D Moving Average.

Top Downside Momentum* (Issues with the greatest 100 day

downward momentum*)

*Momentum: (100D % change) + 1.5*(50D % change) + 2.0*(10D

% change) for each stock then sort all names that have a negative value in ascending order and report the top 10.

Symbol Close Weekly %

Change

50-Day %

Change

SB 0.35 -23.91% -88.67%

SALT 3.65 -25.36% -76.05%

GLBS 0.09 -55.00% -85.00%

TOO 3.52 -24.79% -77.58%

TK 6.18 -21.67% -81.07%

NM 0.86 -13.13% -57.00%

EGLE 2.05 -22.93% -65.02%

SBLK 0.43 -2.27% -71.14%

NMM 1.92 -18.99% -65.53%

DSX 2.48 -28.32% -60.76%

SHIPPING MARKETS

Top Consecutive Lower Closes

Symbol Close Up Streak

DAC 4.82 -2

FRO 2.03 -2

SHIP 1.64 -2

NAT 13.03 -2

NNA 2.07 -2

DCIX 0.54 -3

GLBS 0.09 -3

PRGN 0.11 -3

CPLP 3.73 -5

GSL 1.79 -6

15

Tuesday, January 19, 2016 (Week 3)

Top Largest Weekly Trading Losses

Symbol Close One

Week Ago

Today

Close

Net

Change % Change

GLBS 0.2 0.09 -0.11 -55.00%

SHIP 2.89 1.64 -1.25 -43.25%

GSL 2.51 1.79 -0.72 -28.69%

DSX 3.46 2.48 -0.98 -28.32%

SALT 4.89 3.65 -1.24 -25.36%

TOO 4.68 3.52 -1.16 -24.79%

SB 0.46 0.35 -0.11 -23.91%

TNK 5.5 4.23 -1.27 -23.09%

EGLE 2.66 2.05 -0.61 -22.93%

DHT 7.1 5.51 -1.59 -22.39%

Top Largest Monthly Trading Gains (A month has been

standardized to 20 trading days)

Top Largest Monthly Trading*Losses (A month has been

standardized to 20 trading days)

Stocks Nearest to 52-Week Highs Stocks Nearest To 52-Week Lows

Symbol Close One

Month Ago

Today

Close

Net

Change % Change

FREE 0.02 0.4405 0.42 2102.50%

PRGN 0.1 0.11 0.01 10.00%

DRYS 0.1 0.101 0.00 1.00%

Symbol Close One

Month Ago

Today

Close

Net

Change % Change

TK 17.49 6.18 -11.31 -64.67%

SB 0.95 0.35 -0.60 -63.16%

GLBS 0.21 0.09 -0.12 -57.14%

TOO 7.8 3.52 -4.28 -54.87%

SALT 7.92 3.65 -4.27 -53.91%

SHIP 3.35 1.64 -1.71 -51.04%

TGP 18.38 9.99 -8.39 -45.65%

TNK 7.34 4.23 -3.11 -42.37%

GSL 2.94 1.79 -1.15 -39.12%

EGLE 3.34 2.05 -1.29 -38.62%

Symbol 52W Low % Away

ESEA 2.30 2.61%

GLOG 6.17 2.76%

GSL 1.74 2.87%

TNP 5.40 4.81%

KNOP 10.37 5.01%

DAC 4.56 5.70%

SB 0.33 6.06%

DLNG 6.76 8.14%

SFL 12.29 9.07%

MATX 33.43 10.94%

SHIPPING MARKETS

Symbol 52W High % Away

NAT 16.61 -21.54%

SFL 17.32 -22.62%

DAC 6.70 -28.06%

SSW 20.02 -29.76%

MATX 53.18 -30.26%

DHT 8.59 -35.89%

ASC 14.67 -37.31%

FRO 3.61 -43.73%

TNP 10.34 -45.24%

NVGS 22.31 -46.17%

16

Tuesday, January 19, 2016 (Week 3)

SHIPPING MARKETS

Symbol Close Net % Change Run Rate

SALT 3.65 -25.36% 9.2847

SHIP 1.64 -43.25% 8.2740

FREE 0.4405 4305.00% 2.6919

DSX 2.48 -28.32% 2.4715

SFL 13.4 -13.44% 2.3210

TK 6.18 -21.67% 2.2033

GSL 1.79 -28.69% 2.1793

GLBS 0.09 -55.00% 2.0786

STNG 5.74 -12.37% 2.0475

CPLP 3.73 -21.31% 1.9651

Top Stocks with Highest Weekly Volume Run Rate* > 1

*The Volume Run Rate is calculated by divided the current week's volume by the average volume over the last 20 weeks. For example, a run rate of 2.0 means the stock traded twice its average volume.

Top Year-To-Date Gainers

Symbol YTD Decline %

SALT -63.09%

SB -56.79%

SHIP -51.76%

NM -50.86%

TOO -45.68%

DSX -42.99%

EGLE -41.76%

DRYS -40.59%

TNK -38.52%

TK -37.39%

The following are the 43 members of this group: Symbol - Name: ASC – Ardmore Shipping Corp; BALT - Baltic Trading Ltd; CMRE - Costamare Inc;

CPLP - Capital Product Partners LP; DAC - Danaos Corp; DCIX - Diana Containerships Inc.; DHT - DHT Maritime Inc; DLNG - Dynagas LNG Partners LP;

DRYS - DryShips Inc; DSX - Diana Shipping Inc; EGLE - Eagle Bulk Shipping Inc; ESEA - Euroseas Ltd; FREE - FreeSeas Inc; FRO - Frontline Ltd; GASS -

StealthGas Inc; GLBS - Globus Maritime Limited; GLNG - Golar LNG Ltd; GLOG - GasLog Ltd.; GMLP - Golar LNG Partners LP; GSL - Global Ship Lease

Inc; KNOP - KNOT Offshore Partners LP; MATX - Matson, Inc.; NAT - Nordic American Tanker Shipping; NM - Navios Maritime Holdings Inc; NMM - Navios

Maritime Partners LP; NNA - Navios Maritime Acquisition Corp; NVGS - Navigator Holdings Ltd.; PRGN - Paragon Shipping Inc; SALT - Scorpio Bulkers; SB -

Safe Bulkers Inc; SBLK - Star Bulk Carriers Corp; SFL - Ship Finance International Ltd; SHIP - Seanergy Maritime Holdings Corp; SSW - Seaspan Corp;

STNG - Scorpio Tankers Inc; TEU - Box Ships Inc.; TGP - Teekay LNG Partners LP; TK - Teekay Corp; TNK - Teekay Tankers Ltd; TNP - Tsakos Energy

Navigation Ltd; TOO - Teekay Offshore Partners LP; TOPS - TOP Ships Inc; VLCCF - Knightsbridge Tankers Ltd;

DISCLAIMER: This communication has been prepared by Knight Capital Americas LLC.s ("KCA"), trading, market making and/or sales personnel

(collectively, "KCG Traders") to compile commentary received from either particular KCG Traders providing their personal perspectives on the markets,

sectors and general news or third party sources. The information set forth above has been obtained from or based upon sources believed by the KCG Traders

to be reliable, but each KCG Trader and KCG (as defined below) does not represent or warrant its accuracy or completeness and is not responsible for losses

or damages arising out of errors or omissions, delays in the receipt of this information, or any actions taken in reliance thereon. Opinions, historical price(s) or

value(s) are as of the date and, if applicable, time indicated. KCG does not accept any responsibility to update any opinions or other information contained in

this communication. The information provided herein is not intended to provide a sufficient basis on which to make an investment decision. It is intended only

to provide observations and views of individual KCG Traders, which may be different from, or inconsistent with, the observations and views of KCG and/or its

affiliates, officers, directors and/or employees (including other KCG Traders). The communication is for your general information only and is not an offer or

solicitation to buy or sell any security or product. KCG Traders may, from time to time express indications of interest to potentially buy or sell a particular

security. These indications of interest are not firm orders or quotes, and may not be current. Accordingly, please contact your KCG representative if you have

any interest or questions relating to these indications of interest or to any information provided herein. KCA most likely makes a market in the securities

mentioned in this document. KCG and/or its affiliates, officers, directors and employees, including persons involved in the preparation or issuance of this

material, may, from time to time, have long or short positions in, or buy or sell (on a principal basis or otherwise) the securities mentioned in this

communication which may be inconsistent with the views expressed herein. Questions regarding the information presented herein or to request a copy of this

document should be referred to your KCG Representative.

This document is a product of KCG Holdings, Inc. ("KCG") and its affiliates and subsidiaries (collectively "KCG"). KCG Holdings, Inc. ("KCG") is comprised of

trading and related entities under common control such as Knight Capital Americas, LLC, KCG Europe Limited (a U.K. registered broker-dealer) and KCG

Hotspot FX LLC.

© 2013 KCG Holdings, Inc. ("KCG") All rights reserved. Provided by Knight Capital Americas LLC, member of FINRA and SIPC.

17

Tuesday, January 19, 2016 (Week 3)

17

Global Shipping Company Bond Data

Contributed by Stifel Nicolaus & Co, Inc.

SHIPPING MARKETS

18

Tuesday, January 19, 2016 (Week 3)

Aggregate Price Index

15 Jan ±∆ ±%Capesize 38 q -2 -6.1%

Panamax 35 q 0 -0.9%

Supramax 38 q -1 -3.5%

Handysize 46 q -1 -1.6%

M-O-M change

SHIPPING MARKETS

Contributed by

Allied Shipbroking Inc

48 Aigialeias Str. 151 25 Maroussi

Athens, Greece

Phone: +30 2104524500

Website: www.allied-shipbroking.gr

Weekly Market Report Market Analysis

With the big news this weekend being the lifting of Iran’s international

sanctions, the crude oil market was spooked by the prospects of further

supply glut hitting the scene, while many see this 12 year low in crude oil

prices being only a small chapter in the upcoming developments to be

noted over the course of the year.

During the course of the past 12 months, crude oil supply brought about

mainly by the decision by OPEC members has created one of the

biggest and longest price drops in the history of crude oil trading. This

strategy, which has been in part to help OPEC members regain market

share, has come at a great cost and despite all efforts many of the

targeted high priced oil producers continue to operate. It is by no

coincidence that the U.S. announced that it would lift its ban on oil

exports, allowing its excess production from shale oil to spill over to

other markets.

In the midst of all this OPEC now forecasts that oil supply from non-

member countries will post a decline of 660,000 barrels per day within

2016 (almost double its previous forecast) as the new price reality of

below US$ 30 a barrel (the price fell to US$28 a barrel which is the

lowest recorded since 2003) squeezes ever more producers out of

competition. Yet many in the market see this as only a start to further

price drops, with many quoting a new price norm of around US$ 20 per

barrel. This in part will surely be supported by the supply impact of

500,000 bpd coming into play within 2016. At the same time estimates

for demand within 2016 is set to be close to the 1.26 million bpd, a

notable slowdown from the 1.54 million bpd estimated for 2015.

All this turns up the heat on most of these OPEC member countries

many of which have seen a large chunk of their cash reserves sapped

and most of their generous welfare systems (most notably in recent

news reports the situation faced by Venezuela). Saudi Arabia as well as

the rest of the five Gulf Cooperation Council members have announced

that they are preparing to announce considerable spending cuts in their

annual government budgets, while many expect an even tougher year in

terms of their earnings. All this points to extended tensions that will arise

during the next biannual meeting of the OPEC members, while it will be

hard to ascertain the true success of their original decision back in 2014.

What is becoming ever certain now is that it will be hard to head back to

the hay days of US$ 80-140 per barrel, while the recent advancements

in oil production brought about by the technologies behind shale oil has

meant that production is more flexible to price changes then ever before.

The big challenge moving forward will be a demand one, with strategic

reserves by most countries having peaked to some of their highest

levels ever, it is difficult to see were all this new excess supply will be

absorbed. What’s more is that despite the fact that energy commodity

prices have dipped by so much, there is still plentiful efforts being put on

new technologies which provide ever higher efficiencies in consumption,

leaving all to believe that we will likely see a stagnation in demand over

the coming years. This stagnation is by no means limited to the OECD

economies but is likely to effect the fast paced emerging economies as

well, as they leapfrog straight from their low oil consumption per capita

onto oil consumption dictated by energy efficient technologies which are

equally available. After all, all new cars purchased in China or India are,

if not on par, of almost equal energy efficiency ratings as the ones being

bought in the U.S. and Europe.

Dry Bulk Freight Market

Secondhand Market

Newbuilding Market

Demolition Market

Tanker Freight Market

15 Jan ±∆ ±%BDI 373 q -56 -13.1%

BCI 198 q -145 -42.3%

BPI 381 q -53 -12.2%

BSI 394 q -36 -8.4%

BHSI 245 q -11 -4.3%

W-O-W change

15 Jan ±∆ ±%BDTI 897 q -119 -11.7%

BCTI 707 q -9 -1.3%

W-O-W change

Avg Price Index (main 5 regions)

15 Jan ±∆ ±%Dry 222 q -3 -1.3%

Wet 242 q -3 -1.2%

W-O-W change

Aggregate Price Index

15 Jan ±∆ ±%Bulkers 79 q 0 -0.2%

Cont 100 u 0 0.0%

Tankers 101 q 0 -0.1%

Gas 100 u 0 0.0%

M-O-M change

VLCC 112 p 4 3.3%

Suezmax 101 p 3 3.4%

Aframax 123 p 3 2.4%

MR 129 p 7 5.8%

19

Tuesday, January 19, 2016 (Week 3)

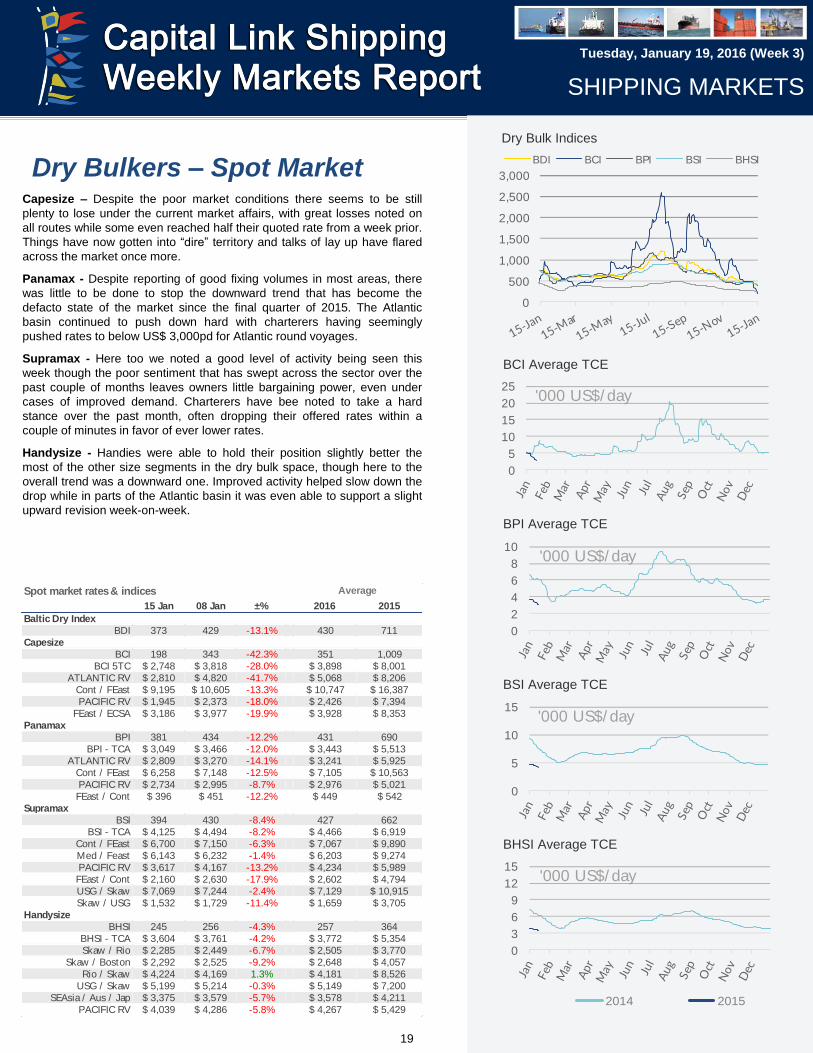

Dry Bulkers – Spot Market

SHIPPING MARKETS

Capesize – Despite the poor market conditions there seems to be still

plenty to lose under the current market affairs, with great losses noted on

all routes while some even reached half their quoted rate from a week prior.

Things have now gotten into “dire” territory and talks of lay up have flared

across the market once more.

Panamax - Despite reporting of good fixing volumes in most areas, there

was little to be done to stop the downward trend that has become the

defacto state of the market since the final quarter of 2015. The Atlantic

basin continued to push down hard with charterers having seemingly

pushed rates to below US$ 3,000pd for Atlantic round voyages.

Supramax - Here too we noted a good level of activity being seen this

week though the poor sentiment that has swept across the sector over the

past couple of months leaves owners little bargaining power, even under

cases of improved demand. Charterers have bee noted to take a hard

stance over the past month, often dropping their offered rates within a

couple of minutes in favor of ever lower rates.

Handysize - Handies were able to hold their position slightly better the

most of the other size segments in the dry bulk space, though here to the

overall trend was a downward one. Improved activity helped slow down the

drop while in parts of the Atlantic basin it was even able to support a slight

upward revision week-on-week.

2014 2015

BCI Average TCE

BPI Average TCE

BSI Average TCE

BHSI Average TCE

Dry Bulk Indices

15 Jan 08 Jan ±% 2016 2015

Baltic Dry Index

BDI 373 429 -13.1% 430 711

Capesize

BCI 198 343 -42.3% 351 1,009

BCI 5TC $ 2,748 $ 3,818 -28.0% $ 3,898 $ 8,001

ATLANTIC RV $ 2,810 $ 4,820 -41.7% $ 5,068 $ 8,206

Cont / FEast $ 9,195 $ 10,605 -13.3% $ 10,747 $ 16,387

PACIFIC RV $ 1,945 $ 2,373 -18.0% $ 2,426 $ 7,394

FEast / ECSA $ 3,186 $ 3,977 -19.9% $ 3,928 $ 8,353

Panamax

BPI 381 434 -12.2% 431 690

BPI - TCA $ 3,049 $ 3,466 -12.0% $ 3,443 $ 5,513

ATLANTIC RV $ 2,809 $ 3,270 -14.1% $ 3,241 $ 5,925

Cont / FEast $ 6,258 $ 7,148 -12.5% $ 7,105 $ 10,563

PACIFIC RV $ 2,734 $ 2,995 -8.7% $ 2,976 $ 5,021

FEast / Cont $ 396 $ 451 -12.2% $ 449 $ 542

Supramax

BSI 394 430 -8.4% 427 662

BSI - TCA $ 4,125 $ 4,494 -8.2% $ 4,466 $ 6,919

Cont / FEast $ 6,700 $ 7,150 -6.3% $ 7,067 $ 9,890

Med / Feast $ 6,143 $ 6,232 -1.4% $ 6,203 $ 9,274

PACIFIC RV $ 3,617 $ 4,167 -13.2% $ 4,234 $ 5,989

FEast / Cont $ 2,160 $ 2,630 -17.9% $ 2,602 $ 4,794

USG / Skaw $ 7,069 $ 7,244 -2.4% $ 7,129 $ 10,915

Skaw / USG $ 1,532 $ 1,729 -11.4% $ 1,659 $ 3,705

Handysize

BHSI 245 256 -4.3% 257 364

BHSI - TCA $ 3,604 $ 3,761 -4.2% $ 3,772 $ 5,354

Skaw / Rio $ 2,285 $ 2,449 -6.7% $ 2,505 $ 3,770

Skaw / Boston $ 2,292 $ 2,525 -9.2% $ 2,648 $ 4,057

Rio / Skaw $ 4,224 $ 4,169 1.3% $ 4,181 $ 8,526

USG / Skaw $ 5,199 $ 5,214 -0.3% $ 5,149 $ 7,200

SEAsia / Aus / Jap $ 3,375 $ 3,579 -5.7% $ 3,578 $ 4,211

PACIFIC RV $ 4,039 $ 4,286 -5.8% $ 4,267 $ 5,429

Spot market rates & indices Average

0

5

10

15

20

25'000 US$/ day

0

2

4

6

8

10'000 US$/ day

0

5

10

15'000 US$/ day

0

3

6

9

12

15'000 US$/ day

0

500

1,000

1,500

2,000

2,500

3,000

BDI BCI BPI BSI BHSI

20

Tuesday, January 19, 2016 (Week 3)

Tankers – Spot Market

SHIPPING MARKETS

Crude Oil Carriers - It seems as though the recent drop in crude oil prices

has caused a bit of a disturbance in the market for crude oil tankers, with

demand dropping notably during the past couple of days. Although this may

well have been a temporary shock influenced in part by the lifting of the

sanctions on Iran, there has started to emerge a sense that the January

program may well fall short on expectations keeping these new downward

revised figures in place over the next two weeks give or take.

Oil Products - On the basis of mixed emotions in the crude oil space,

product tankers have also felt a halt in their previous upward momentum,

with demand slowing down this week giving a sense that the market held

over flat in terms of given rates. However with the given repositioning that

has been reported in the market this past week, expectations are that

things may turn around soon possibly giving ample room for another round

of freight rate improvements over the coming weeks.

2014 2015

VLCC Average TCE

Suezmax Average TCE

Aframax Average TCE

MR Average TCE

Tanker Indices

15 Jan 08 Jan ±% 2016 2015

Baltic Tanker Indices

BDTI 897 1,016 -11.7% 980 820

BCTI 707 716 -1.3% 700 637

VLCC

WS 43.42 55.67 -22.0% 54.72 36.36

$/ day $ 32,796 $ 45,649 -28.2% $ 46,548 $ 31,968

WS 61.04 95.61 -36.2% 89.17 64.43

$/ day $ 54,104 $ 92,461 -41.5% $ 84,315 $ 61,629

WS 59.79 94.11 -36.5% 87.80 63.09

$/ day $ 48,198 $ 81,773 -41.1% $ 78,334 $ 68,288

WS 74.50 106.50 -30.0% 99.05 72.72

$/ day $ 101,820 $ 150,087 -32.2% $ 138,799 $ 76,589

SUEZMAX

WS 95.00 115.00 -17.4% 109.09 81.13

$/ day $ 63,072 $ 78,256 -19.4% $ 73,748 $ 46,404

WS 122.05 141.59 -13.8% 129.63 91.34

$/ day $ 54,712 $ 66,323 -17.5% $ 60,430 $ 46,346

AFRAMAX

WS 113.33 117.22 -3.3% 116.42 111.01

$/ day $ 33,608 $ 35,159 -4.4% $ 35,632 $ 37,053

WS 128.94 146.50 -12.0% 140.25 112.26

$/ day $ 29,672 $ 34,204 -13.2% $ 33,394 $ 31,406

WS 131.94 118.33 11.5% 123.63 133.63

$/ day $ 28,692 $ 23,555 21.8% $ 26,353 $ 37,962

WS 92.78 94.44 -1.8% 93.20 92.57

$/ day $ 36,254 $ 36,345 -0.3% $ 36,774 $ 43,406

DPP

WS 145.00 150.00 -3.3% 142.95 138.77

$/ day $ 37,415 $ 39,135 -4.4% $ 36,809 $ 30,727

WS 140.00 139.50 0.4% 138.35 122.73

$/ day $ 41,809 $ 41,742 0.2% $ 41,270 $ 30,281

WS 122.88 140.38 -12.5% 133.81 110.54

$/ day $ 31,393 $ 36,668 -14.4% $ 35,551 $ 35,804

WS 101.89 115.39 -11.7% 113.69 108.70

$/ day $ 22,753 $ 27,670 -17.8% $ 28,587 $ 35,902

CPP

WS 136.67 148.28 -7.8% 139.72 105.50

$/ day $ 30,842 $ 33,510 -8.0% $ 32,001 $ 28,796

WS 154.09 149.54 3.0% 147.88 134.68

$/ day $ 19,693 $ 18,503 6.4% $ 18,645 $ 18,755

WS 147.50 155.00 -4.8% 143.64 134.05

$/ day $ 28,607 $ 30,540 -6.3% $ 27,685 $ 22,099

WS 100.00 110.00 -9.1% 109.84 96.47

$/ day $ 10,795 $ 12,092 -10.7% $ 12,583 $ 12,481

BALTIC-UKC

ARA-USG

Spot market rates & indices Average

MED-MED

CONT-USAC

USG-CONT

MEG-USG

MEG-SPORE

WAF-USG

BSEA-MED

MEG-SPORE

MEG-JAPAN

WAF-USAC

NSEA-CONT

CARIBS-USG

CARIBS-USAC

SEASIA-AUS

MEG-JAPAN

CARIBS-USAC

250

450

650

850

1,050

1,250

BDTI BCTI

-10

10

30

50

70

90

110'000 US$/ day

-25

0

25

50

75

100'000 US$/ day

0

20

40

60

80

100'000 US$/ day

5

10

15

20

25

30

35'000 US$/ day

21

Tuesday, January 19, 2016 (Week 3)

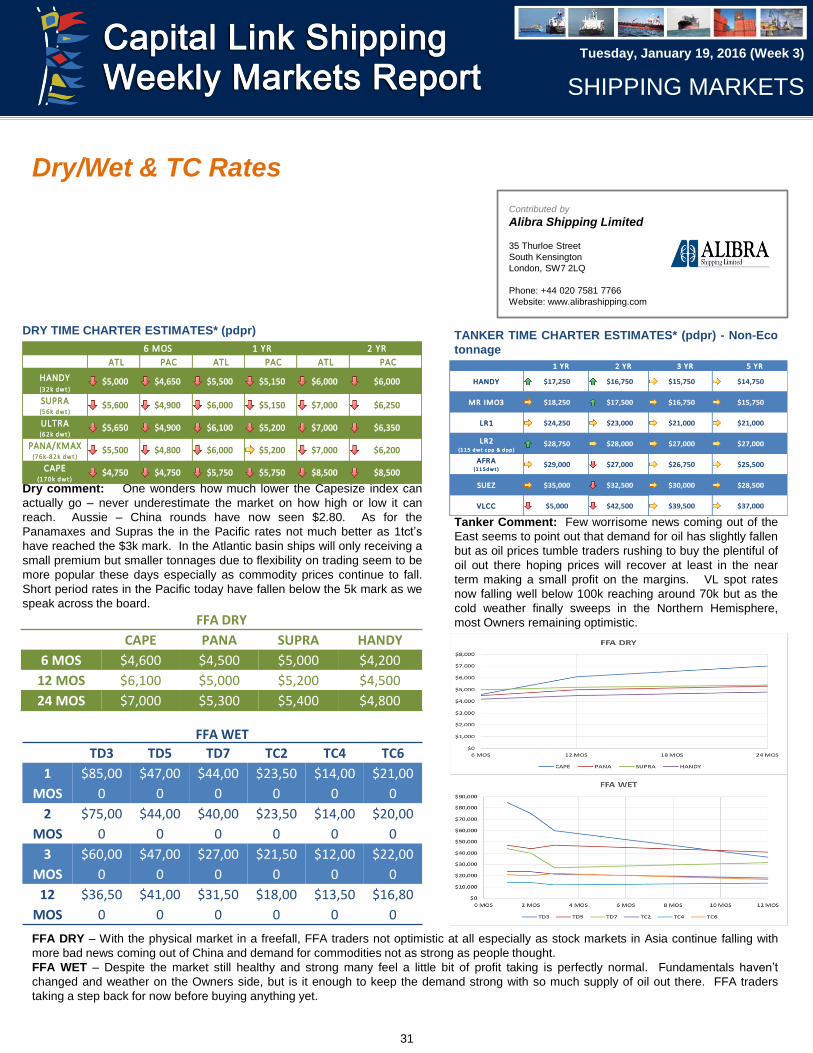

Period Charter Market

SHIPPING MARKETS

Capesize Panamax

Dry Bulk 12 month period charter rates (USD ‘000/day)

VLCC Suezmax

Tanker 12 month period charter rates (USD ‘000/day)

Supramax Handysize

Aframax MR

Latest indicative Dry Bulk Period Fixtures

Latest indicative Tanker Period Fixtures

last 5 years

15 Jan 11 Dec ±% Min Avg Max

Capesize

$ 6,500 $ 7,000 -7.1% $ 6,450 $ 15,724 $ 31,450

$ 8,000 $ 7,000 14.3% $ 6,950 $ 16,270 $ 25,200

Panamax

$ 5,500 $ 6,500 -15.4% $ 5,450 $ 10,949 $ 18,700

$ 6,750 $ 7,250 -6.9% $ 6,700 $ 11,457 $ 16,700

Supramax

$ 5,000 $ 6,000 -16.7% $ 4,950 $ 10,794 $ 15,950

$ 7,000 $ 7,250 -3.4% $ 6,950 $ 11,048 $ 15,450

Handysize

$ 5,500 $ 6,000 -8.3% $ 5,450 $ 8,893 $ 12,950

$ 6,000 $ 6,500 -7.7% $ 5,950 $ 9,411 $ 12,950

36 months

12 months

36 months

36 months

12 months

36 months

12 months

12 months

Dry Bulk period market TC rates

last 5 years

15 Jan 11 Dec ±% Min Avg Max

VLCC

$ 57,500 $ 55,000 4.5% $ 18,000 $ 28,996 $ 57,750

$ 44,000 $ 42,500 3.5% $ 22,000 $ 31,097 $ 45,000

Suezmax

$ 40,000 $ 38,000 5.3% $ 15,250 $ 22,472 $ 42,500

$ 33,500 $ 33,500 0.0% $ 17,000 $ 24,126 $ 35,000

Aframax

$ 30,000 $ 30,000 0.0% $ 13,000 $ 17,463 $ 30,000

$ 26,750 $ 26,750 0.0% $ 14,750 $ 18,628 $ 27,000

MR

$ 19,000 $ 18,500 2.7% $ 12,500 $ 14,833 $ 21,000

$ 18,000 $ 17,500 2.9% $ 14,000 $ 15,204 $ 18,250

12 months

36 months

Tanker period market TC rates

12 months

36 months

12 months

36 months

12 months

36 months

5

7

9

11

13

15

17

19

21

5

6

7

8

9

10

11

12

5

6

7

8

9

10

11

5

6

7

8

9

10

20

25

30

35

40

45

50

55

60

15

20

25

30

35

40

45

12

17

22

27

32

1213141516171819202122

M/ T ''BW UTAH'', 299500 dwt, built 2001, $44,500, for 18 months trading,

to SHELL

M/ T ''GERD KNUTSEN'', 155000 dwt, built 1996, $30,000, for 6+3 months

trading, to ISS

M/ T ''PANTELIS'', 114500 dwt, built 2004, $37,000, for 3 months trading,

to LITASCO

M/ T ''HAFNIA LEO'', 52300 dwt, built 2013, $18,850, for 1 year trading, to

TRAFIGURA

M/ T ''HAFNIA ROBINSON'', 40000 dwt, built 2004, $17,500, for 1 year

trading, to TRAFIGURA

M/ V ''ALIKI'', 180435 dwt, built 2005, dely Baoshan spot, $5,300, for 11/ 14

months trading, to SwissMarine

M/ V ''NIREFS'', 75311 dwt, built 2001, dely Rizhao 12/ 16 Jan, $4,600, for

11/ 14 months trading, to Transgrain

M/ V ''GENEVA QUEEN'', 81361 dwt, built 2012, dely retro Dhamra 19

December, $5,100, for 4/ 6 months trading, to Phaethon

M/ V ''NCS BEIJING '', 81508 dwt, built 2009, dely Kinuura 20/ 25 Jan,

$5,400, for 4/ 8 months trading, to Chart Not Rep

M/ V ''MONA FRONTIER'', 172865 dwt, built 2001, dely Lanshan 20/ 25

Jan, $4,250, for 4/ 6 months trading, to Rio Tinto

22

Tuesday, January 19, 2016 (Week 3)

Indicative Tanker Values (US$ million)

15 Jan 11 Dec ±% Min Avg Max

VLCC

310k dwt Resale 100.0 100.0 0.0% 80.0 95.3 108.5

310k dwt 5 year old 83.0 80.0 3.8% 55.0 70.0 87.0

250k dwt 10 year old 58.0 55.0 5.5% 33.8 45.9 62.0

250k dwt 15 year old 39.5 38.0 3.9% 16.9 27.1 41.0

Suezmax

160k dwt Resale 70.0 70.0 0.0% 53.0 63.9 73.0

150k dwt 5 year old 62.0 60.0 3.3% 38.0 49.8 62.0

150k dwt 10 year old 44.5 42.0 6.0% 24.0 33.5 44.5

150k dwt 15 year old 23.0 22.0 4.5% 14.0 18.6 23.3

Aframax

110k dwt Resale 56.0 56.0 0.0% 39.0 48.4 57.0

110k dwt 5 year old 47.5 46.0 3.3% 27.0 36.7 47.5

105k dwt 10 year old 32.0 31.0 3.2% 16.0 23.9 33.0

105k dwt 15 year old 17.5 17.0 2.9% 8.0 13.0 18.5

MR

52k dwt Resale 38.5 38.5 0.0% 32.0 36.9 39.3

52k dwt 5 year old 31.0 29.0 6.9% 22.0 26.9 31.0

45k dwt 10 year old 21.0 19.5 7.7% 14.0 17.8 21.0

45k dwt 15 year old 13.0 12.0 8.3% 9.0 10.9 13.5

last 5 years

Indicative Dry Bulk Values (US$ million)

15 Jan 11 Dec ±% Min Avg Max

Capesize

180k dwt Resale 36.0 39.0 -7.7% 36.0 49.4 65.0

170k dwt 5 year old 23.0 26.0 -11.5% 23.0 38.2 53.0

170k dwt 10 year old 13.0 13.0 0.0% 13.0 26.4 39.0

150k dwt 15 year old 7.5 7.5 0.0% 7.5 16.0 25.0

Panamax

82k dwt Resale 24.0 24.5 -2.0% 24.0 31.3 43.0

76k dwt 5 year old 11.5 11.5 0.0% 11.5 22.9 36.8

76k dwt 10 year old 7.3 7.3 0.0% 7.3 17.1 29.3

74k dwt 15 year old 4.5 4.5 0.0% 4.5 11.3 22.0

Supramax

62k dwt Resale 21.0 23.0 -8.7% 21.0 29.3 36.8

58k dwt 5 year old 11.0 11.0 0.0% 11.0 22.0 30.5

52k dwt 10 year old 6.5 6.5 0.0% 6.5 16.1 24.3

52k dwt 15 year old 4.5 4.5 0.0% 4.5 10.8 19.0

Handysize

37k dwt Resale 19.0 19.0 0.0% 19.0 23.5 30.0

32k dwt 5 year old 9.0 9.0 0.0% 9.0 18.1 25.5

32k dwt 10 year old 7.0 7.5 -6.7% 7.0 13.6 19.5

28k dwt 15 year old 4.0 4.0 0.0% 4.0 9.2 14.5

last 5 years

Secondhand Asset Values

SHIPPING MARKETS

On the dry bulk side, there was a fair amount of activity being reported in

the capesize sector, with a number of deals indicating to another

softening in prices. With talks now mounting in terms of putting up

tonnage for cold lay-up, it looks as though things are set to get even

tougher over the coming days with further price drops now clearly in

sight.

On the tanker side, there was a slight calm with lower then average

volume seen in reported transactions, while there still seems to be a

strong holding for the firm prices to continue. Freight rates may have

stumbled slightly this week, yet it looks as though there is still firm

demand out there for tonnage. Expectations are not for any great

increases in terms of pricing, especially given the fact that more and

more will be driven towards the new ordering option given the price gap

quoted under the current market.

Capesize Panamax

Supramax Handysize

VLCC Suezmax

Aframax MR

Price movements of 5 year old Dry Bulk assets

Price movements of 5 year old Tanker assets

-12%

-34%

-26%

-36%-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

1 month diff 3 months diff6 months diff 12 months diff

+0%

-36%

-30%

-39%-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

1 month diff 3 months diff6 months diff 12 months diff

+0%

-31%

-24%

-42%-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

1 month diff 3 months diff6 months diff 12 months diff

+0%

-31% -31%

-44%-50%

-45%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

1 month diff 3 months diff6 months diff 12 months diff

+4% +4%

-1%

+4%

-1%

-1%

0%

1%

1%

2%

2%

3%

3%

4%

4%

1 month diff 3 months diff6 months diff 12 months diff

+3% +3% +3% +3%

0%

1%

1%

2%

2%

3%

3%

4%

1 month diff 3 months diff6 months diff 12 months diff

+3%

+6%

+4%

+3%

0%

1%

2%

3%

4%

5%

6%

1 month diff 3 months diff6 months diff 12 months diff

+7% +7%

+15% +15%

0%

2%

4%

6%

8%

10%

12%

14%

16%

1 month diff 3 months diff6 months diff 12 months diff

23

Tuesday, January 19, 2016 (Week 3)

Newbuilding Market

SHIPPING MARKETS

Tanker Newbuilding Prices

Dry Bulk Newbuilding Prices

Demolition Market

Wet Scrap Prices

Dry Scrap Prices

Indicative Dry Prices ($/ ldt) last 5 years

15 Jan 08 Jan ±% Min Avg Max

Indian Sub Continent

Bangladesh 280 285 -1.8% 250 413 515

India 275 280 -1.8% 270 420 525

Pakistan 275 280 -1.8% 270 416 510

Far East Asia

China 125 125 0.0% 120 320 455

Mediterranean

Turkey 155 155 0.0% 155 271 355

Indicative Wet Prices ($/ ldt) last 5 years

15 Jan 08 Jan ±% Min Avg Max

Indian Sub Continent

Bangladesh 305 310 -1.6% 280 435 540

India 300 305 -1.6% 295 443 550

Pakistan 300 305 -1.6% 295 440 525

Far East Asia

China 145 145 0.0% 140 338 485

Mediterranean

Turkey 160 160 0.0% 160 281 355

Indicative Dry NB Prices (US$ million) last 5 years

15 Jan 11 Dec ±% Min Avg Max

Dry Bulkers

Capesize (180,000dwt) 46.0 46.5 -1.1% 46.0 50.6 58.0

Kamsarmax (82,000dwt) 26.3 26.3 0.0% 26.3 29.2 36.5

Panamax (77,000dwt) 25.8 25.8 0.0% 25.8 28.3 34.5

Ultramax (64,000dwt) 24.3 24.3 0.0% 24.3 26.5 31.0

Handysize (37,000dwt) 20.5 20.5 0.0% 20.5 22.5 26.5

Container

Post Panamax (9,000teu) 88.0 88.0 0.0% 76.5 86.6 94.5

Panamax (5,200teu) 56.0 56.0 0.0% 48.6 57.2 65.6

Sub Panamax (2,500teu) 29.5 29.5 0.0% 29.5 33.2 41.0

Feeder (1,700teu) 20.5 20.5 0.0% 20.5 24.6 29.4

Indicative Wet NB Prices (US$ million) last 5 years

15 Jan 11 Dec ±% Min Avg Max

Tankers

VLCC (300,000dwt) 93.5 94.0 -0.5% 89.5 96.4 104.0

Suezmax (160,000dwt) 63.0 63.0 0.0% 55.8 61.5 66.0

Aframax (115,000dwt) 52.0 52.0 0.0% 47.0 51.9 56.0

LR1 (75,000dwt) 45.8 45.8 0.0% 40.5 43.9 47.0

MR (56,000dwt) 35.5 35.5 0.0% 33.5 35.3 37.3

Gas

LNG 160k cbm 199.0 199.0 0.0% 198.0 200.1 203.0

LPG LGC 80k cbm 77.0 77.0 0.0% 70.0 74.1 80.0

LPG MGC 55k cbm 67.5 67.5 0.0% 62.0 64.5 68.5

LPG SGC 25k cbm 45.0 45.0 0.0% 41.0 44.1 46.5

10

20

30

40

50

60

Capesize Panamax Supramax Handysize

US$ million

30

50

70

90

110

VLCC Suezmax Aframax LR1 MR

US$ million

100150200250300350400450500

Bangladesh India Pakistan China Turkey