builder’s risk insurance - policyholderinsurancelaw.com · builder’s risk insurance: what...

TRANSCRIPT

Builder’s Risk Insurance:Builder s Risk Insurance: What Owners and Contractors Need to Know

Seth D. LamdenNeal, Gerber & Eisenberg LLP

Insurance Policyholder Practice GroupInsurance Policyholder Practice GroupTwo N. LaSalle St.Chicago, IL 60602312.269.8052

WPL Publishing – March 27, 2014

h i ild ' i k ?What is Builder's Risk Insurance?

2© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

What Builder's Risk Insurance is Not:What Builder s Risk Insurance is Not:

d d d f ll hStandardized, one‐size‐fits‐all insurance that covers everything that could go wrong during constructionconstruction

3© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Structure of a Builder's Risk Policy

4© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

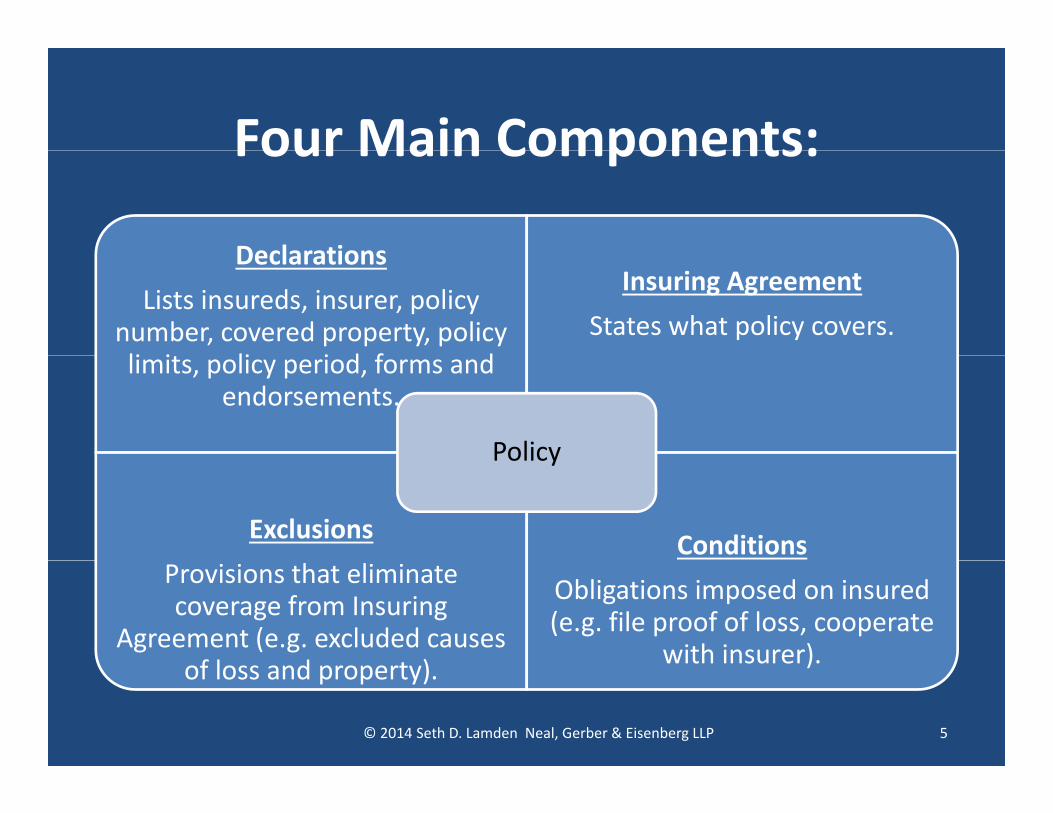

Four Main Components:Four Main Components:

DeclarationsDeclarationsLists insureds, insurer, policy

number, covered property, policy li i li i d f d

Insuring AgreementStates what policy covers.

limits, policy period, forms and endorsements.

Policy

Exclusions Conditions

Policy

Provisions that eliminate coverage from Insuring

Agreement (e.g. excluded causes f l d t )

Obligations imposed on insured (e.g. file proof of loss, cooperate

with insurer).of loss and property). with insurer).

5© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Additional Parts of Policy:Additional Parts of Policy:

Definitions Coverage ExtensionsDefinitionsCertain policy terms are

expressly defined in the policy.

Coverage ExtensionsOptional coverages added to the policy, usually for additional

premiumpremium.

Policy

Endorsements Schedules

Policy

EndorsementsForms added to policy that alter

or modify coverage.

SchedulesMay list named insureds or

covered property.

6© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Every word has meaning:Every word has meaning: Coverage for hundreds of millions of dollars of construction losses has turned on how courts interpreted the following terms (not a complete list):on how courts interpreted the following terms (not a complete list):“Collapse”“Arising out of”“Caused by”

“Structure”“Dwelling”“Policy”

“Property of Others for Which You are Liable”“Completed value”y

“Occurrence”“Sudden and accidental”“And”“Or”

y“Application”“Property damage”“Subcontractor”“Materialman”

p“Construction”“Physical loss or damage”“Work”“Contractor”“Or”

“Workmanship”“Building materials”“Pollutant”

“Materialman”“Making good”“Resulting Damage”“Occupancy”

“Contractor”“Builder”“Owned by the insured”“Similar property”

“You”“Accident”“Complete falling in”

“Roof”“Covered Property”“Loss”

7© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Covered Parties

8© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Who Should Be an Insured?Who Should Be an Insured?

P ti ith “i bl i t t” i thParties with an “insurable interest” in the project, materials, and equipment.

Project owner, general contractor, subcontractors, and sub‐subcontractors.

Lenders? Other parties bearing risk of loss?

9© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Be Named as an InsuredBe Named as an Insured

K Ri ht t fil l i di tlKey reasons: Right to file claim directly against insurer and subrogation protection.

Confirm status as named insured on declarations and endorsements.

Note: A “loss payee” is not an insured.

10© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

dCovered Property

11© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Don’t Assume all Property Is CoveredDon t Assume all Property Is Covered

Oth th j t it lf dOther than project itself, covered property can vary from policy to policy.

Look at "Covered Property" and "Property Not Covered" sections of the policy.

Read descriptions of covered property in policy very carefully.

12© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Commonly Covered Property: y p y

• Building or structure under construction

• Property stored off‐site• Property of othersconstruction

• Foundations• Fixtures and machinery

• Property of others• Office trailers• Underground pipes

• Building materials and supplies onsite

Underground pipes• Landscaping materials• Personal property of insured

• Temporary structures• Property in transit

or within insured’s care, custody and control (could include contractor’s tools)include contractor s tools)

13© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Commonly Excluded Property: y p y

• Existing property • Contractors tools equipment

• Water • Animals• Contractors tools, equipment,

and machinery (consider separate policy or coverage

)

• Animals • Waterborne and/or airborne property

extension)• Land, including fill and backfill materials at project site prior

• Motor vehicles, aircraft, and watercraft Simaterials at project site prior

to commencement of the project

• Signs • Transmission or distribution lines, poles, towers and

• Landscaping materials, including trees, grass, shrubbery, etc.

lines, poles, towers and attached equipment

• Accounts, bills, currency, d

14

y,• Timber and crops

money, and securities

© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

d fCovered Causes of Loss

15© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Two Forms of Builder's Risk Policies:Two Forms of Builder s Risk Policies:

“All Ri k” C di t h i l l f“All Risk”: Covers direct physical loss from all causes except those that are expressly

l d d i h liexcluded in the policy.

“Specified Peril” or “Named Peril”: Covers direct physical loss from causes that are p yexpressly stated in the policy.

16© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

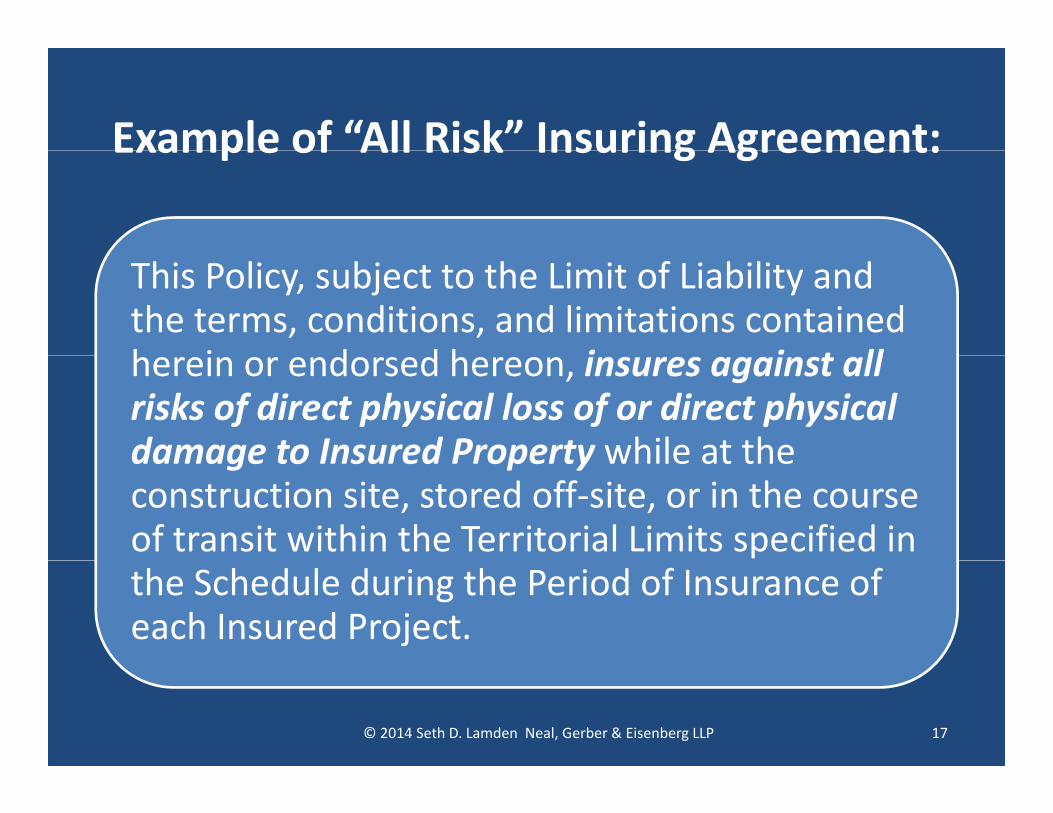

Example of “All Risk” Insuring Agreement:Example of All Risk Insuring Agreement:

This Policy, subject to the Limit of Liability and the terms, conditions, and limitations contained h i d d h i i t llherein or endorsed hereon, insures against all risks of direct physical loss of or direct physical damage to Insured Property while at thedamage to Insured Property while at the construction site, stored off‐site, or in the course of transit within the Territorial Limits specified in the Schedule during the Period of Insurance of each Insured Project.

17© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Commonly Excluded “Risks” or “Perils”:

• Dishonest acts of the insured• Wear and tear, gradual

d i i i

• Increased cost of construction due to law or ordinancel d d lid b kdeterioration, corrosion, etc.

(except ensuing loss)• Settling, cracking, expansion,

• Flood, mudslide, sewer backup, and seepage of water

• Earth movementetc. (except ensuing loss)

• Freezing (unless proper precautions have been taken)

• Mechanical breakdown, electrical injury, boiler explosion

• Faulty workmanship, design or • Asbestos • Release of pollutants, unless

resulting from specified perils

materials (except ensuing loss)• Collapse, except from specified

causes • Delay and consequential losses • Loss covered under guarantee,

warranty, or obligation of manufacturer or supplier

18© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

C f L C d BCoverage for Losses Caused By Defective Design or Workmanship

19© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Defective Design and Workmanship:Defective Design and Workmanship:

Most policies exclude coverage for some losses caused by faulty design and workmanship.

Wording (and scope of coverage) can vary significantly from policy to policy.

A few words could be the difference between full coverage and no coverage.

20© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

First, what is “workmanship”?First, what is workmanship ?

Defective completed product or performance of work (e.g. accident or equipment malfunction)?

Only defective completed product?Only defective completed product?

Ambiguous?

21© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 1: Insured Seeks Coverage for Cleanup Costs and Delay Damages

Policy Exclusion:

g p y gCaused by Crane Collapse at Worksite Due to Operator’s Negligence

“This Policy does not insure against physical loss or damage caused by or resulting from . . . errors or defects in design or specification, faulty workmanship or faulty materials . . . .”

Insured’s Interpretation of Exclusion:Damage is covered because “faulty workmanship” only means defects in a age s co e ed because au ty o a s p o y ea s de ectscompleted work.

’ i f l iInsurer’s Interpretation of Exclusion:Damage is not covered because “faulty workmanship” means either: (1) defects in completed work; and (2) accidents or equipment malfunctions during construction.

22© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 1: Insured Seeks Coverage for Cleanup Costs and Delay Damages g p y g

Caused by Crane Collapse at Worksite Due to Operator’s Negligence

Court’s Interpretation of Exclusion:

Insured wins: Losses caused by crane collapse were covered because “faulty workmanship” refers to flawed products, not process of performing workperforming work.

See 1765 First Associates, LLC v. Cont’l. Cas. Co., 817 F. Supp. 2d 374 (S D NY 2011)(S.D.N.Y. 2011)

Note: One month earlier, the Nevada Supreme Court had held that a contractor’s failure to properly secure a tarp, which resulted in water p p y p,damage, was “faulty workmanship” because “workmanship” includes both defective products and defective processes.

Fourth St. Place v. Travelers Indem. Co., 270 P.3d 1235 (Nev. 2011) 23© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

London Market Design Exclusions (DE) and L d E i i G (LEG) M d l E l iLondon Engineering Group (LEG) Model Exclusions

DE1: Outright Defect

DE2: Extended Defective

DE3: Limited Defective

DE4:Defective Part

DE5: Design

ImprovementExclusion Condition Exclusion Condition Exclusion Exclusion Improvement Exclusion

LEG 1/96 LEG 2/96 LEG 3/06

Least coverage Most coverage

LEG 1/96‘Outright’ Defects

Exclusion

LEG 2/96 –‘Consequences’ Defects

Exclusion

LEG 3/06‘Improvement’ Defects

Exclusion

24© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 2: Mere Presence of Defect in Design, Plan, Specification, Materials, or g , , p , ,

Workmanship (New tower being built in Pisa, Italy).

“I skimped a little on the foundation, but no one will ever know it!!"

25© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 2: Mere Presence of Defect in Design, Plan, Specification, Materials, or g , , p , ,

Workmanship (New tower being built in Pisa, Italy).

DE1 (1995) Outright Defects Exclusion: Covered DamageDE1 (1995) Outright Defects Exclusion: Covered Damage

“This policy excludes loss of or damage to the Property Insured due to defective design, plan, specification, materials, or workmanship.”

None

p

DE2 (1995) Limited Defective Condition Exclusion:DE3 (1995) Limited Defective Condition Exclusion:

None

DE4 (1995) Defective Part Exclusion:DE5 (1995) Design Improvement Exclusion:

“For the purpose of the Policy and not merely this Exclusion, the d h ll b d d l d d l lProperty Insured shall not be regarded as lost or damaged solely

by virtue of the existence of any defect in design, plan, specification, materials, or workmanship in the Property Insured or any part thereof.”y p

26© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

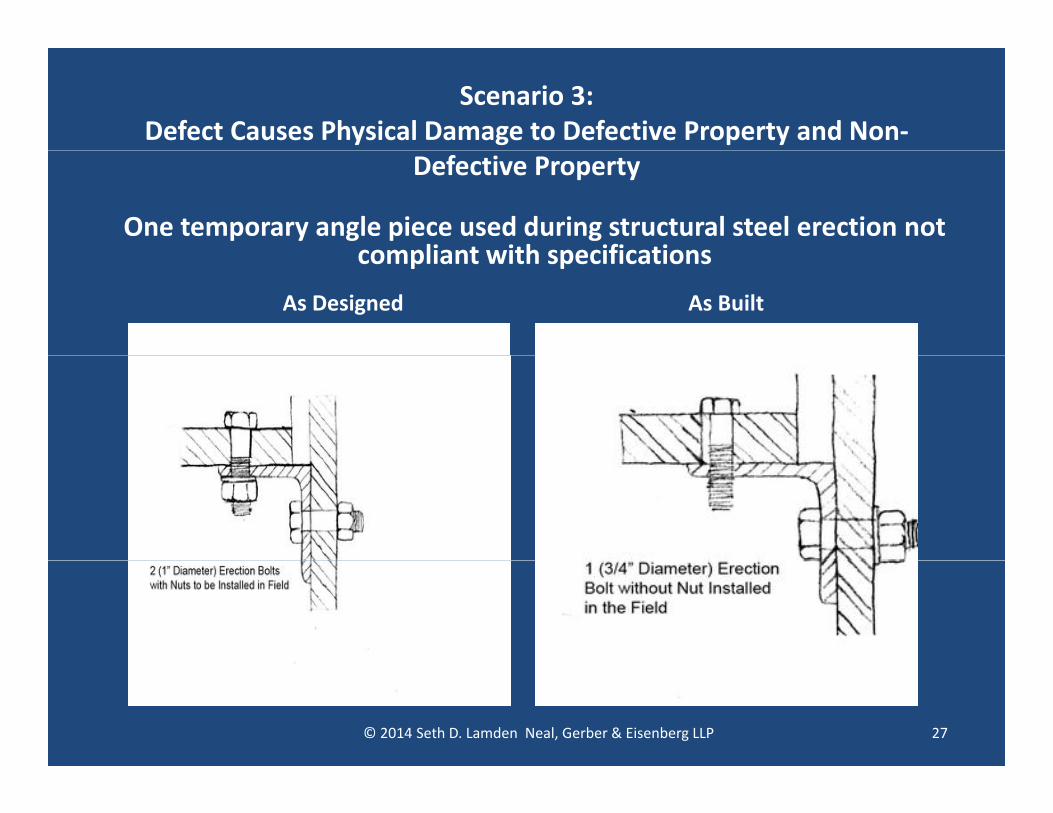

Scenario 3: Defect Causes Physical Damage to Defective Property and Non‐

Defective Property

One temporary angle piece used during structural steel erection not compliant with specificationscompliant with specifications

As Designed As Built

27© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 3: Defect Causes Physical Damage to Defective Property and Non‐

•Angle piece fails, which leads to collapse of steel

Defective Property

leads to collapse of steel beam held in place by defectively‐installed piece.•Collapsed beam was on•Collapsed beam was on highest level of structure.•Weight of falling beam causes other beams tocauses other beams to collapse, and also damages other property. •It is possible that otherIt is possible that other angle pieces were installed in the same defective manner.

28© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 3: Defect Causes Physical Damage to Defective Property and Non‐

DE1 (1995) Outright Defects Exclusion Covered Damage

“ h l l d l f d h d

y g p yDefective Property

“This policy excludes loss of or damage to the Property Insured due to defective design, plan, specification, materials, or workmanship.”

None

29© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 3: Defect Causes Physical Damage to Defective Property and Non‐

DE2 (1995) Extended defective condition exclusion Covered Damage

y g p yDefective Property

“This policy excludes loss of or damage to and the cost necessary to replace, repair or rectify:(a) Property Insured which is in a defective condition due to defect in design, plan, specification, materials, or workmanship of such Property

Not Covered:•Defective angle piece(s) that have not failed.

Insured or any part thereof;(b) Property Insured which relies for its support or stability on (a) above;(c) Property Insured lost or damaged to enable the replacement, repair,

•Defective angle piece that failed.•Steel beam supported by angle

rectification of Property Insured excluded by (a) and (b) above Exclusion (a) and (b) above shall not apply to other Property Insured which is free of the defective condition but is damaged in consequence thereof.

piece that failed.

Covered:All other property

For the purpose of the Policy and not merely this Exclusion, the Property Insured shall not be regarded as lost or damaged solely by virtue of the existence of any defect in design, plan, specification, materials, or workmanship in the Property Insured or any part thereof.”

damage resulting from failed angle piece.

30© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 3: Defect Causes Physical Damage to Defective Property and Non‐

DE3 (1995) Limited Defective Condition Exclusion Covered Damage

y g p yDefective Property

“This policy excludes loss of or damage to and the cost necessary to replace, repair, or rectify:

(a) Property Insured which is in a defective condition due to a defect indesign, plan, specification, materials, or workmanship of such Property

Not Covered:•Defective angle piece(s) that have not failed.g , p , p , , p p y

Insured or any part thereof;

(b) Property Insured lost or damaged to enable the replacement, repair, rectification of Property Insured excluded by (a) above

E l i ( ) b h ll l h P I d hi h i f

•Defective angle piece that failed.

Exclusion (a) above shall not apply to other Property Insured which is free of the defective condition but is damaged in consequence thereof.

For the purpose of the Policy and not merely this Exclusion the Property Insured shall not be regarded as lost or damaged solely by virtue of the

Covered:All other property damage resulting from failed angle

l dexistence of any defect in design plan specification material or workmanship in the Property Insured or any part thereof.”

piece, including steel beam held in place by angle piece that failed.

31© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 3: Defect Causes Physical Damage to Defective Property and Non‐

DE4 (1995) Defective Part Exclusion Covered Damage

y g p yDefective Property

“This policy excludes loss of or damage to and the cost necessary to replace, repair, or rectify:

(a)Any component part or individual item of the Property Insured which is

Not Covered:•Defective angle piece(s) that have not failed.

defective in design, plant, specification, materials, or workmanship; or

(b)Property Insured lost or damaged to enable the replacement, repair or rectification of Property Insured excluded by (a) above.

•Defective angle piece that failed.

Exclusion (a) above shall not apply to other Property Insured which is free of the defective condition but is damaged in consequence thereof.

Covered:All other property damage resulting from failed angle

For the purpose of the Policy and not merely this Exclusion, the Property Insured shall not be regarded as lost or damaged solely by virtue of the existence of any defect in design, plan, specification, materials, or workmanship in the Property Insured or any part thereof.”

piece, including steel beam held in place by angle piece that failed.

32© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 3: Defect Causes Physical Damage to Defective Property and Non‐

DE5 (1995) Design Improvement Exclusion Covered Damage

“ h l l d d

y g p yDefective Property

“This policy excludes:

(a) The cost necessary to replace repair or rectify any Property Insured which is defective in design, plan, specification, materials, or workmanship.(b) d h d d bl l

Not Covered:•Defective angle piece(s) that have not failed.

(b) Loss or damage to the Property Insured caused to enable replacement repair or rectification of such defective Property Insured.

But should damage to the Property Insured which is free of such defective di i ( h h d d fi d i (b) b ) l f h

Covered:All other property d l icondition (other than damage as defined in (b) above) result from such a

defect this exclusion shall be limited to the costs of additional work resulting from and the additional costs of improvement to the original design plan specification materials or workmanship.

damage resulting from failed angle piece, includingsteel beam held in l b l

For the purpose of the policy and not merely this Exclusion the Property Insured shall not be regarded as lost or damaged solely by virtue of the existence of any defect in design plan specification materials or

k hi i h P I d h f”

place by angle piece that failed and defective angle piece that failed.

workmanship in the Property Insured or any part thereof.”

33© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Scenario 3: Defect Causes Physical Damage to Defective Property and Non‐

What if the policy also excludes loss caused by “collapse” . . .

y g p yDefective Property

“We will not pay for loss caused by or resulting from . . . collapse, except as provided for in Coverage Extensions. But if loss by a Covered Cause of Loss results in collapse at the location(s) described in the Declarations, we will pay for that resulting loss.”

And defective workmanship is not a “covered cause of loss”?

“For the purpose of the policy and not merely this Exclusion the Property Insured shall not be regarded as lost or damaged solely by virtue of the existence of any defect in design, plan, specification, materials, or workmanship in the Property Insured or any part thereof.”

•Is this policy ambiguous?•Is this policy ambiguous?•Is there coverage if it is ambiguous?

34© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Coverage Extensions

35© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Coverage Extensions:Coverage Extensions:

Can provide coverage for types of property or loss that would not otherwise be covered.

Some exclusions can be “bought back ”Some exclusions can be bought back.

Often subject to sub‐limits

36© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Coverage For Construction Delays

37© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Coverage For Construction DelaysCoverage For Construction Delays

Most policies expressly exclude soft cost coverage, but coverage can be purchased.

Even without express exclusion, coverage often limited “h ” ( f h l l )to “hard costs” (repair of direct physical loss).

Costs included in insured value?

38© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Example of “Soft Cost” Exclusion:Example of Soft Cost Exclusion:

“This policy excludes consequential loss, damage or expense of any kind or description including p y p gbut not limited to loss of market or delay, liquidated damages, performance penalties, penalties for non‐completion, delay in completion, or non compliance with contract conditions whether caused by a peril insured orconditions, whether caused by a peril insured or otherwise.”

39© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Elements of a Covered Delay Claim:Elements of a Covered Delay Claim:

S ft C tCovered Damage

Delay in Schedule

Soft Costs Caused by Delay*

*Although policy language varies, in general, soft costs must be:g p y g g , g ,•Resulting from covered physical damage;•Specifically described in the policy;

ll d b d•Actually incurred by insured;•Necessary and reasonable; and•Would not have been incurred but for the delay.y

40© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Duration of Delay Coverage:Duration of Delay Coverage:

Covered Physical Loss

Time Deductible

Covered Delay Period

Project Completion

41© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

fAmount of Coverage: Limits, Sublimits and Deductibles,

42© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

HowMuch Coverage Do You Need?How Much Coverage Do You Need?

Full value of completed construction project.

Policy may include an escalation clause that increases the coverage limits (and premium) if change orders or othercoverage limits (and premium) if change orders or other factors increase the completed value of the project.

“Actual cash value” v. “replacement cost” coverage: Difference is deduction of physical depreciation.

43© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

SublimitsSublimits

Lower limits that apply to loss resulting from a specific peril or type of property.

44© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Common Sublimits: Location:

• Property at the construction site • Property in transitProperty in transit• Property at off‐site storage locations

Coverage Extensions:• Debris removalDebris removal• Acceleration

Specified Peril:• EarthquakeEarthquake• Named storm

Type of Property:• Scaffolding• Scaffolding• Temporary structures

45© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

How Does a Deductible Work?How Does a Deductible Work?Insured pays

Insurer pays$10M

$1MExample:

•Covered $12M Loss

Insured pays

$10M

$

•$1M Deductible

•$10M Policy Limit$1M

y

46© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

DeductiblesDeductibles

Almost always “per occurrence” deductible that applies to all losses.

May include separate, higher deductibles for specified perils such as flood, theft, etc.

If delay coverage, time‐based deductible often applies.

47© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

When Does Coverage End?

48© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Wh D C E d?When Does Coverage End?

Substantial Acceptance Certificate of End of Maintenance

Policy ExpirationCompletion? by Purchaser? Occupancy? Maintenance

Period?Expiration Date?

49© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Example of Policy Termination Clause:Example of Policy Termination Clause:

Coverage will end when one of the following first occurs:a. This policy expires or is cancelled;b The covered structure or building is accepted byb. The covered structure or building is accepted by

the purchaser;c. Your interest in the property ceases;d. You abandon the construction with no intention

to complete it; e The structure of building has been completed fore. The structure of building has been completed for

more than 90 days;f. No work has been performed for at least 90 days.

50© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

When Does Coverage End?When Does Coverage End?

Event that terminates coverage should be stated clearly in the policy and should match the parties’clearly in the policy, and should match the partiescontractual obligations.

Completion, occupancy, etc. may not always be d t i d b f ll bj tidetermined by a fully objective measure.

51© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Using Commercial Property InsuranceUsing Commercial Property Insurance to Cover Construction Risks

52© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Commercial Property InsuranceCommercial Property Insurance

Lack of adequate coverage including for property located offLack of adequate coverage, including for property located off premises and while in transit. (i.e. lower limits, fewer specified perils, etc.).

Contractor is not an insuredContractor is not an insured.

Claims could lead to increased premiums for owner, or disputes with contractor if owner does not want to make claim.

53© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Buying a Builder’s Risk Policy

54© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Buying a Builder’s Risk PolicyInsureds

• Project owner•All contractors and

Property and Locations

• Structure/construction site• Fixtures

Covered Causes of Loss

• Named peril or all risk?• Faulty design and

Amount of Coverage

• Actual cash value or replacement value•All contractors and

subcontractors (except soft cost/delay)

•Other stakeholders?

Fixtures• Scaffolding and temporary structures

• Tools and equipment• Off‐site storage• Property in transit

Faulty design and workmanship –ensuing loss

• Testing• Boiler and machinery• Collapse

p• Demolition and increased cost of construction

• Limits, sublimits and deductibles: per occurrence and aggregateE i d l

p y• Existing property and land • Earth movement

• Wear and tear – ensuing loss

• Estimated value or contract price

Additional Coverage Subrogation Termination of Delay in CompletionAdditional Coverage

•Debris removal• Expediting expenses• Expense to reduce

Subrogation

• Insured permitted to waive recovery rights against others before l

Coverage

•Policy expiration•Occupancy•Acceptance by owner

Delay in Completion

• Loss of income/rent• Soft costs• Expense incurred to p

loss or delay•Pollution• Terrorism• Law and ordinanceCl i i

loss•Waiver of subrogation

p y•Other specified event

preduce delay

• Indemnity period: commencement and expiration

•Claim preparation expenses

55© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Drafting Insurance Specifications

56© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Drafting Insurance SpecificationsDrafting Insurance Specifications

•Who buys coverage/pays premiums?•Who pays deductibles?p y•Types of coverage•Identity of insureds•Deductibles and SIRs•Limits and deductibles•Priority of coverage•Failure to provide insuranceFailure to provide insurance•Waiver of subrogation•Notice of cancellation•Evidence of insuranceEvidence of insurance•Acceptability of insurers•Duration of coverage (including possibly post-completion maintenance)maintenance)

57© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

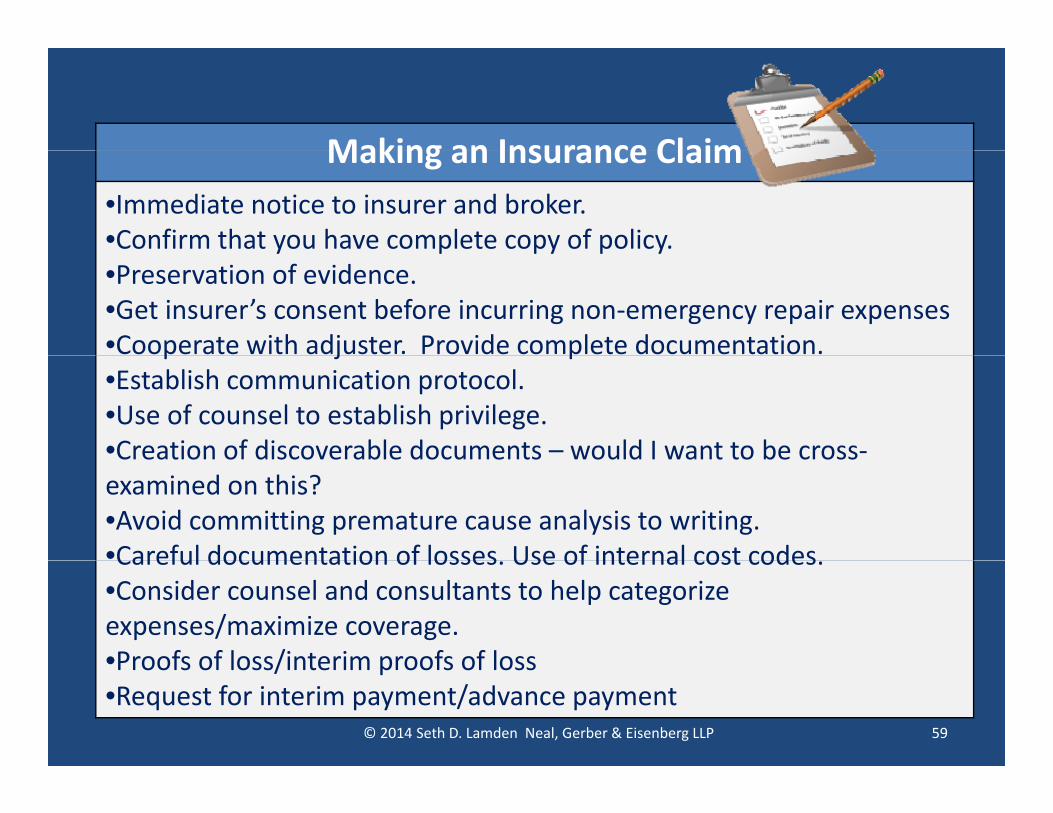

Making an Insurance Claim

58© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Making an Insurance ClaimMaking an Insurance Claim•Immediate notice to insurer and broker.•Confirm that you have complete copy of policy.y p py p y•Preservation of evidence. •Get insurer’s consent before incurring non‐emergency repair expenses•Cooperate with adjuster. Provide complete documentation.p j p•Establish communication protocol. •Use of counsel to establish privilege.•Creation of discoverable documents – would I want to be cross‐Creation of discoverable documents would I want to be crossexamined on this?•Avoid committing premature cause analysis to writing. •Careful documentation of losses Use of internal cost codesCareful documentation of losses. Use of internal cost codes.•Consider counsel and consultants to help categorize expenses/maximize coverage.•Proofs of loss/interim proofs of loss•Proofs of loss/interim proofs of loss•Request for interim payment/advance payment

59© 2014 Seth D. Lamden Neal, Gerber & Eisenberg LLP

Builder’s Risk Insurance:Builder s Risk Insurance: What Owners and Contractors Need to Know

Seth D. LamdenNeal, Gerber & Eisenberg LLP

Insurance Policyholder Practice GroupInsurance Policyholder Practice GroupTwo N. LaSalle St.Chicago, IL 60602312.269.8052

WPL Publishing – March 27, 2014