broyhill am 2-1-10

TRANSCRIPT

8/14/2019 Broyhill AM 2-1-10

http://slidepdf.com/reader/full/broyhill-am-2-1-10 1/8

There’s Nothing Good Here The Investment Team at Broyhill huddles up at 6.30AM every Monday Morning, to review market action,various measures of sentiment, and portfolio positioning, to name a few. For the two hours leading up to ourMorning Macro Call, we scan dozens of charts, pour over piles of data and review all of the models critical toour investment strategy. Notes from our meetings are distributed internally and reviewed in aggregate at ourMonthly Macro Meeting.

We’ve noted a significant shift in the investment landscape over the course of the past few weeks, so wethought we’d share this morning’s Views from the Blue Ridge:

There’s Nothing Good Here

As we entered 2010, our work suggested the continuation of the reflation trade during the first half of the yearalongside of rising coincident indicators and increasing inflationary pressures. While risk assets are clearlyoverpriced, we’ve moved slowly to reduce exposure until now, as we did not anticipate a sharp correction untilleading economic indicators clearly rolled over.

That was our read of the tea leaves heading into the new year. Our investment posture, however, does not relyupon market forecasts or predictions. Instead, we take our evidence as it comes and make adjustmentsaccordingly, rather than stubbornly holding on to an outdated hypothesis. As John Maynard Keynes stated,“When the fact changes, I change my mind. What do you do, sir?”

Suffice it to say, that the facts have changed. We’ve provided a brief summary of John Hussman’s recentMarket Comments below, which we feel best illustrate this shift in investment climate:

Despite the recent decline, the Market Climate remains characterized by overvalued,(intermediate-term) overbought, overbullish and rising-yield conditions. Having broken anuptrend that has been largely intact since March, as well as a sideways range of support

established over the past few months, the natural tendency of the market after such a break is torecover back to the point of prior support, so we should not be surprised if the S&P 500 enjoys asharp recovery rally modestly above the 1100 level, even if the recent correction has further togo. If we observe a “recovery rally” of poor quality from the current short-term oversold conditions, we would be inclined to move to aggressively toward our “Safe Portfolio.”

Importantly, recent market action has historically been associated with a moderate continuationof upward stock market progress and a tendency to make successive but very marginal newhighs, typically followed by abrupt and often severe market losses within a time window of about 10-12 weeks.

The uptrend since the March low can be seen on the weekly chart below. Of equal importance is that the

market’s Price Momentum is very overbought and rolling over through its 10 EMA.

8/14/2019 Broyhill AM 2-1-10

http://slidepdf.com/reader/full/broyhill-am-2-1-10 2/8

The market’s “sideways range of support” is also shown on the daily chart below. You can clearly see thebreak below 1100, which should now become resistance.

Internal weakness is also confirmed by:

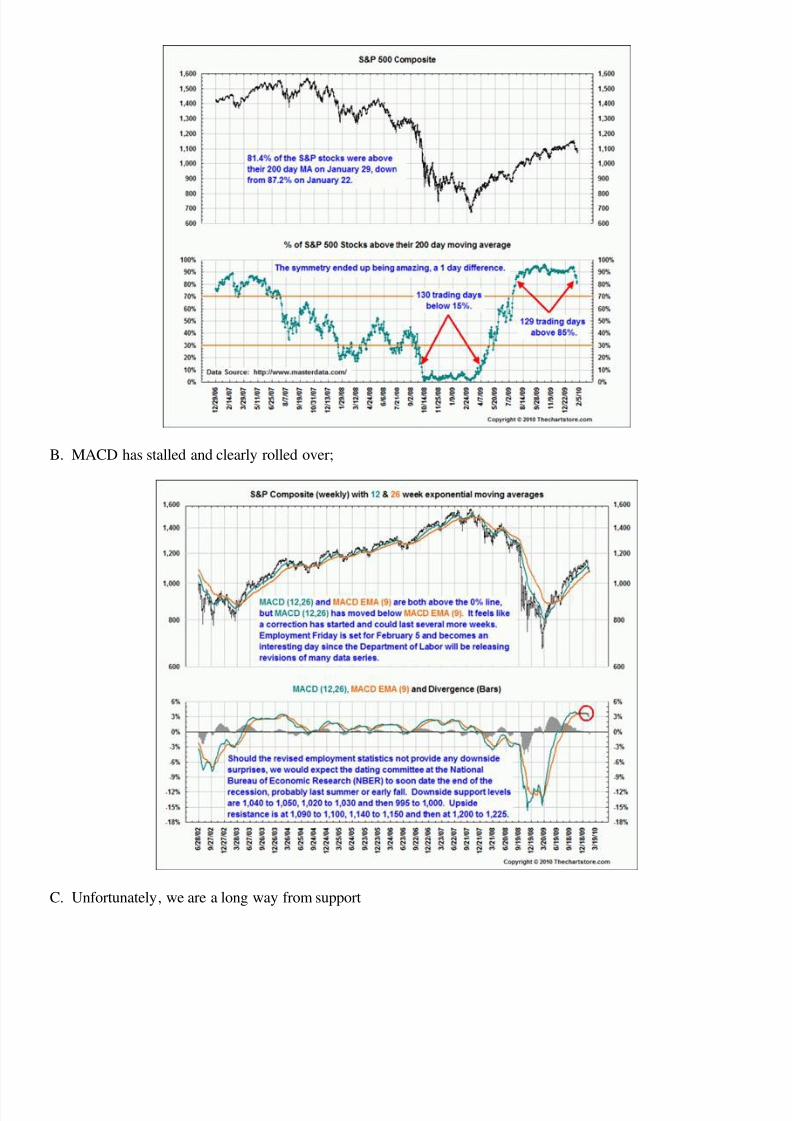

A. Percent of stocks above their 200 DMA rolling over;

8/14/2019 Broyhill AM 2-1-10

http://slidepdf.com/reader/full/broyhill-am-2-1-10 3/8

B. MACD has stalled and clearly rolled over;

C. Unfortunately, we are a long way from support

8/14/2019 Broyhill AM 2-1-10

http://slidepdf.com/reader/full/broyhill-am-2-1-10 4/8

8/14/2019 Broyhill AM 2-1-10

http://slidepdf.com/reader/full/broyhill-am-2-1-10 5/8

B. Dollar strength may be interpreted as a resurgence of deflationary pressures. Similar “Red-Flag Reversal”(MACD crossover) was last seen in early 2008;

C. Dollar strength predominantly expressed through a weakening Euro; More on this and other sovereign risksin the Broyhill Letter;

8/14/2019 Broyhill AM 2-1-10

http://slidepdf.com/reader/full/broyhill-am-2-1-10 6/8

The Tape moved from bullish to neutral – has cracks, but isn’t broken yet. Given the massive underlyingrisks from a macro perspective, it is prudent to leave the last ten percent for the next guy.

Short-term timing model is also neutral now. Watch closely for a “sell” signal, as this would mark the firstfrom the March lows. Percent of stocks above their 10-Week MA and 40-Week MA shows weakness acrossour Global Composite. Percent of new highs versus new lows is approaching it’s first ‘lower-low’ in almost ayear. This is a major reversal of a rising trend in new highs since the October 2008 “panic lows.”

Money supply growth is declining, perhaps as deflationary forces are taking hold again. Last year’s surge in themonetary base drove the broad based reflation in risk assets. Investors should ask themselves, what will supportstocks going forward?

8/14/2019 Broyhill AM 2-1-10

http://slidepdf.com/reader/full/broyhill-am-2-1-10 7/8

Growing red flags in the commodity space.

Commodity Model moved to neutral for the first time since the rally started. Internal model has clearly rolledwith external model starting to turn down as well. Equity weakness in the materials sector is also pointingtoward risks to commodity prices. We are still long commodities b/c inflation is still rising and historically,commodities have done best at this point in the cycle. But when CPI rolls, run for the exits!! We are rigorouslyrevisiting all of our exposures here and reviewing our thesis given underling weakness in the face of what

should be cyclical strength. Is the market already looking forward to a declining CPI in the H2-10 and thereturn of deflation?

Equity sentiment has gone from euphoric to optimistic levels, while the supply/demand story is ending.

At the same time, pessimism in treasury markets remains rampant, with over 80% of those surveyed looking foryields greater than 4% in 2010. We were looking for 4.25% before buying the long bond, but we may not getthere, if sovereign risks overshadow improving coincident indicators.

The Dow has continued to fail at the downtrend which started back in 2007 . . .

8/14/2019 Broyhill AM 2-1-10

http://slidepdf.com/reader/full/broyhill-am-2-1-10 8/8

At the same time the S&P is reversing course . . .

Watch the Yen/Euro Cross for an indication of investor’s willingness to assume risk. This picture is not prettytoday. “There’s nothing good here,” except for the potential for a short-term bounce from oversold levels.