brighter skies ahead: asia pacific aviation

TRANSCRIPT

Asia Pacific AviationBrighter Skies Ahead

Andrew HerdmanAndrew HerdmanDirector General

Association of Asia Pacific AirlinesAssociation of Asia Pacific Airlines

Willis Asia Pacific Insurance Conference3-5 March 20103 5 March 2010

Overview• Asia Pacific aviation

• Current challenges

Gl b l l i• Global regulatory issues

• Brighter skies beyond• Brighter skies beyond

• Sustainable AviationSustainable Aviation

Asia Pacific

• Diverse geographic regionDiverse geographic region• Home to 4 billion people

- 62% of the world’s population

• Generates 27% of global GDP• Wide range of income levels• Dynamic economies leading the y g

global recovery• Aviation widely recognised as a key y g y

contributor to economic and social development

Asia Pacific Aviation

US$ 128 billion revenue$

647 million passengers421 million domestic226 million international226 million international

15 million tonnes of cargo

4,300 aircraft

Asia Pacific carriers overall market share:Asia Pacific carriers overall market share:29% of global passenger traffic40% f l b l t ffi

Data: 2009 Estimate Source: Combined AAPA + non-AAPA airlines GMT+5 to GMT+12

40% of global cargo traffic

Current Challengesg• Fragile recovery in progress

• Asia Pacific leading the way

• Yields still under pressure

• Oil & currency volatility

• Restoring profitability

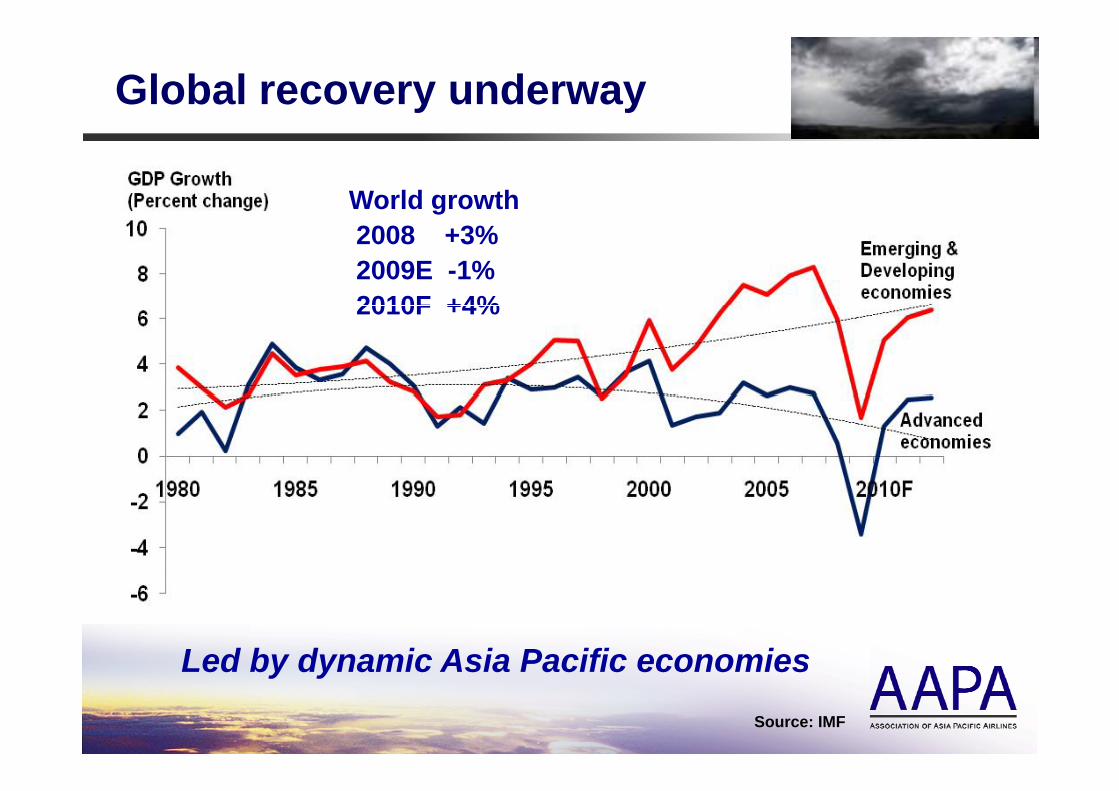

Global recovery underway

World growth2008 +3%2009E -1%2010F +4%2010F +4%

Led by dynamic Asia Pacific economiesSource: IMF

Led by dynamic Asia Pacific economies

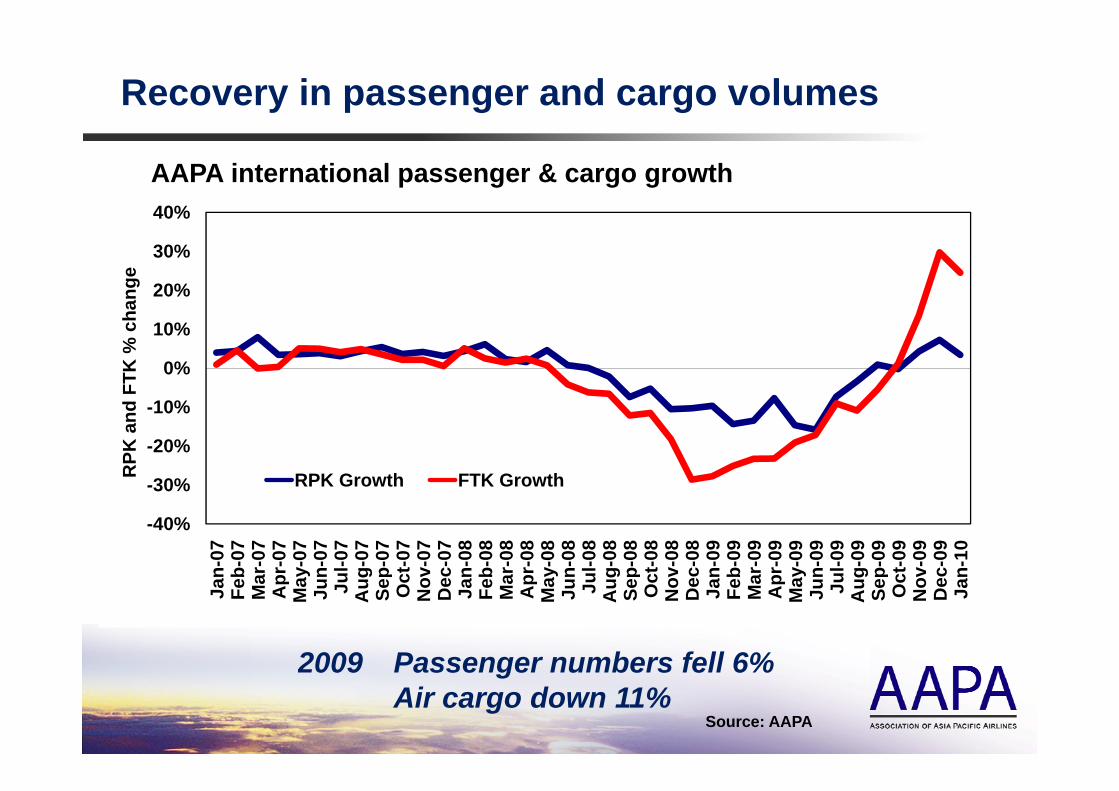

Recovery in passenger and cargo volumes

AAPA international passenger & cargo growth40%

20%

30%

40%

ange

0%

10%

FTK

% c

ha

-30%

-20%

-10%

RPK

and

RPK Growth FTK Growth

-40%

-30%

n-07

b-07

ar-0

7pr

-07

y-07

n-07

ul-0

7g-

07p-

07ct

-07

v-07

c-07

n-08

b-08

ar-0

8pr

-08

y-08

n-08

ul-0

8g-

08p-

08ct

-08

v-08

c-08

n-09

b-09

ar-0

9pr

-09

y-09

n-09

ul-0

9g-

09p-

09ct

-09

v-09

c-09

n-10

RPK Growth FTK Growth

2009 Passenger numbers fell 6%

Jan

Feb

Ma

Ap

May Jun

Ju Aug Se

pO

cN

ov Dec Jan

Feb

Ma

Ap

May Jun

Ju Aug Se

pO

cN

ov Dec Jan

Feb

Ma

Ap

May Jun

Ju Aug Se

pO

cN

ov Dec Jan

2009 Passenger numbers fell 6%Air cargo down 11%

Source: AAPA

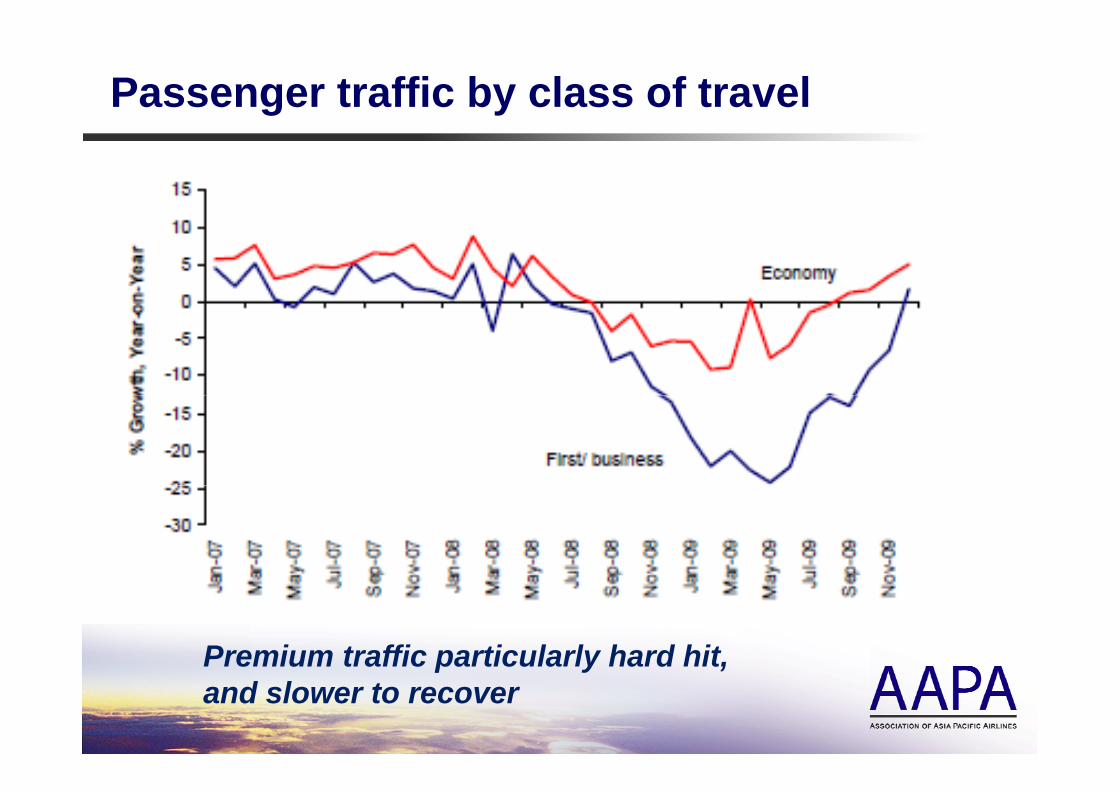

Passenger traffic by class of travel

Premium traffic particularly hard hit,Premium traffic particularly hard hit, and slower to recover

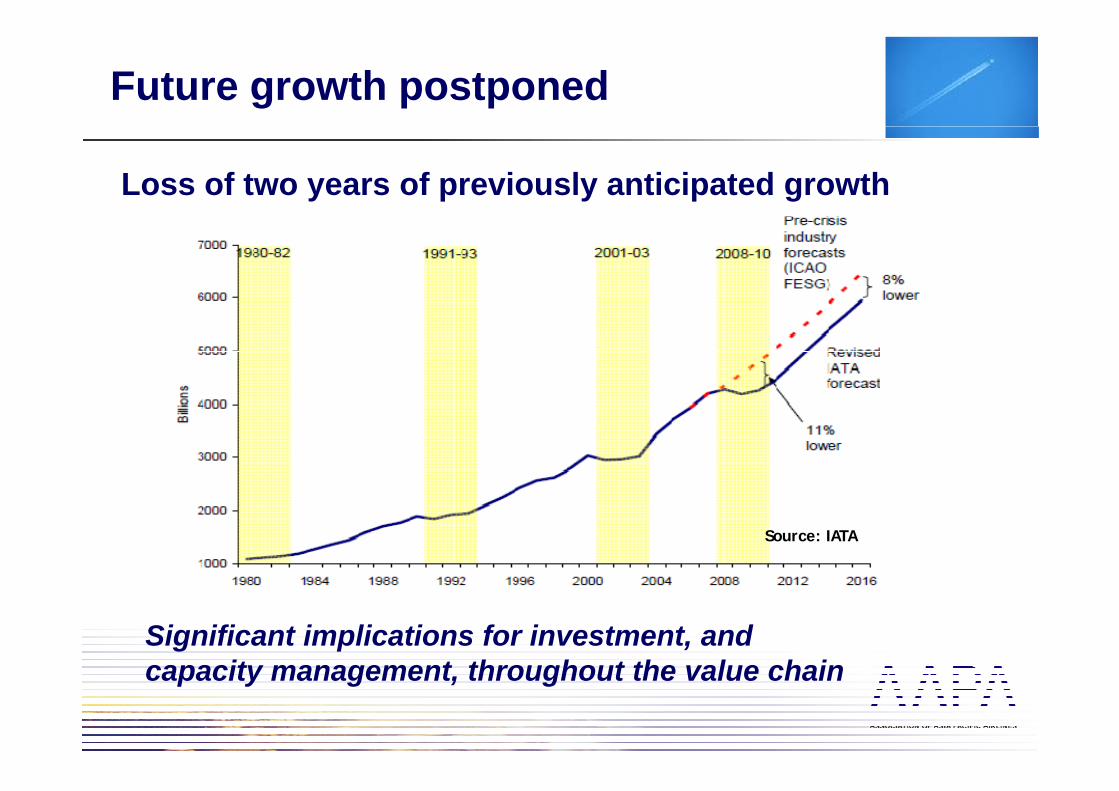

Future growth postponed

Loss of two years of previously anticipated growth

Source: IATA

Significant implications for investment, and it t th h t th l h icapacity management, throughout the value chain

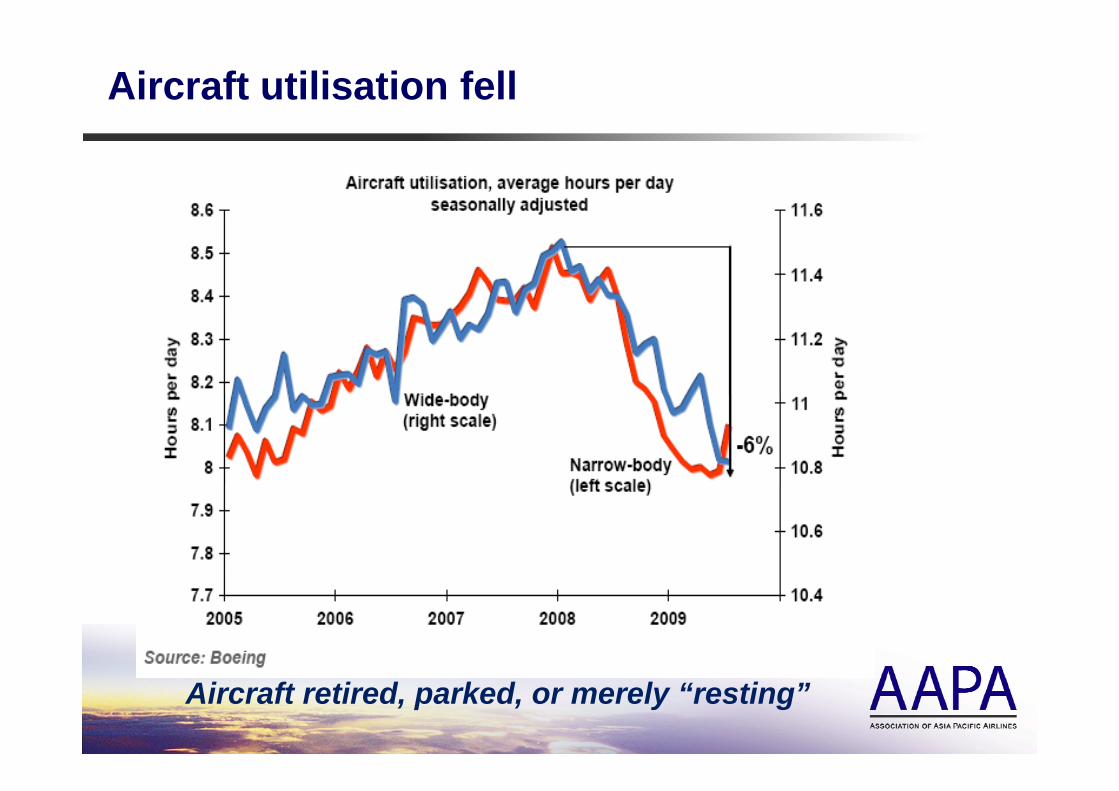

Aircraft utilisation fell

Aircraft retired, parked, or merely “resting”

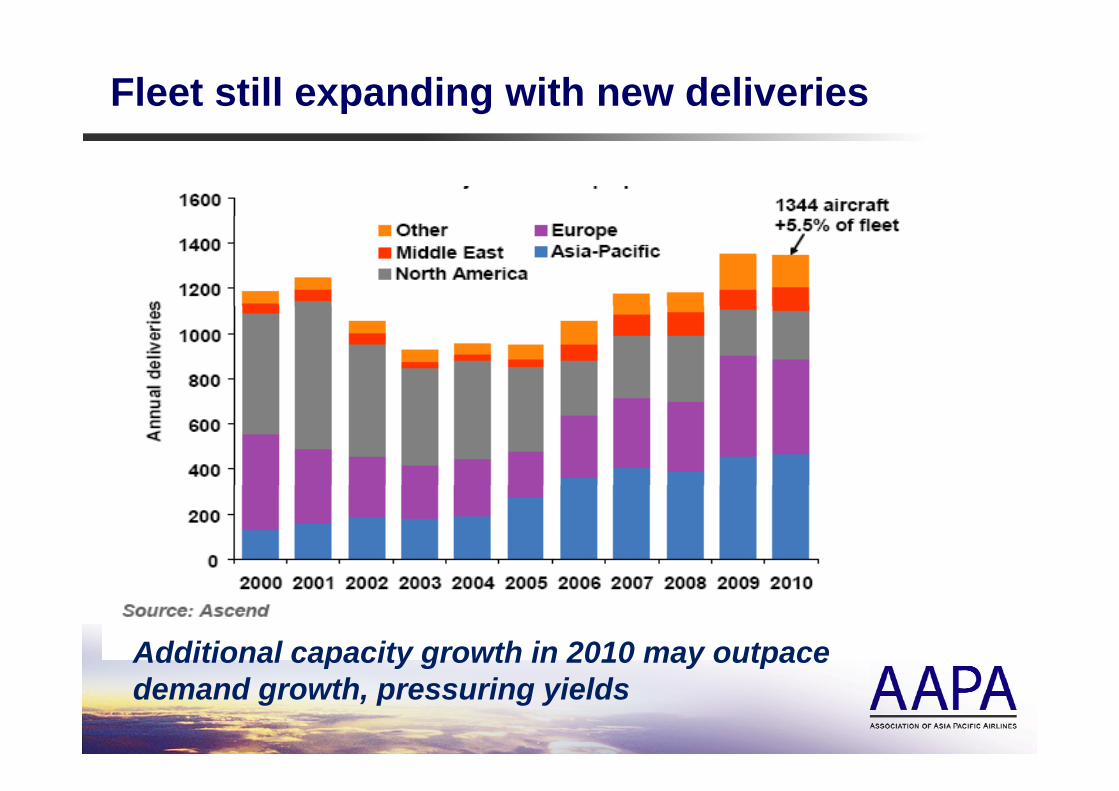

Fleet still expanding with new deliveries

Additional capacity growth in 2010 may outpace p y g y pdemand growth, pressuring yields

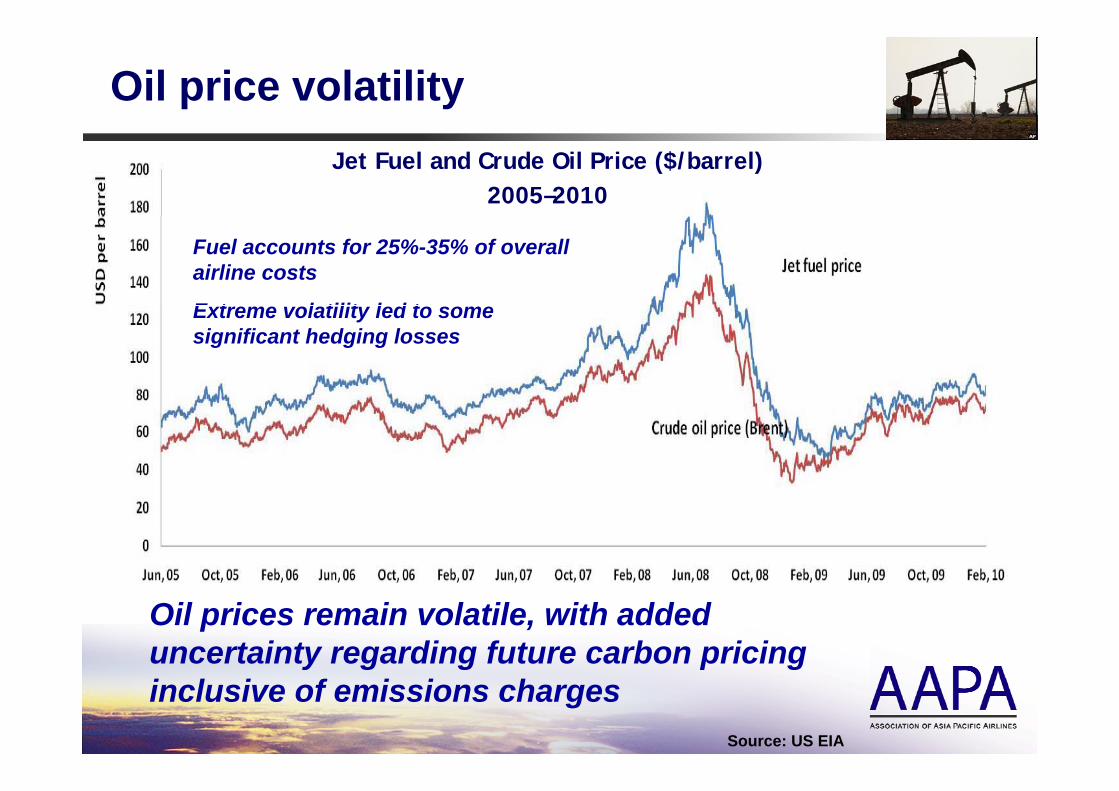

Oil price volatilityJet Fuel and Crude Oil Price ($/barrel)

2005–2010

Fuel accounts for 25%-35% of overall airline costs

E t l tilit l d tExtreme volatility led to some significant hedging losses

Oil prices remain volatile, with added uncertainty regarding future carbon pricing y g g p ginclusive of emissions charges

Source: US EIA

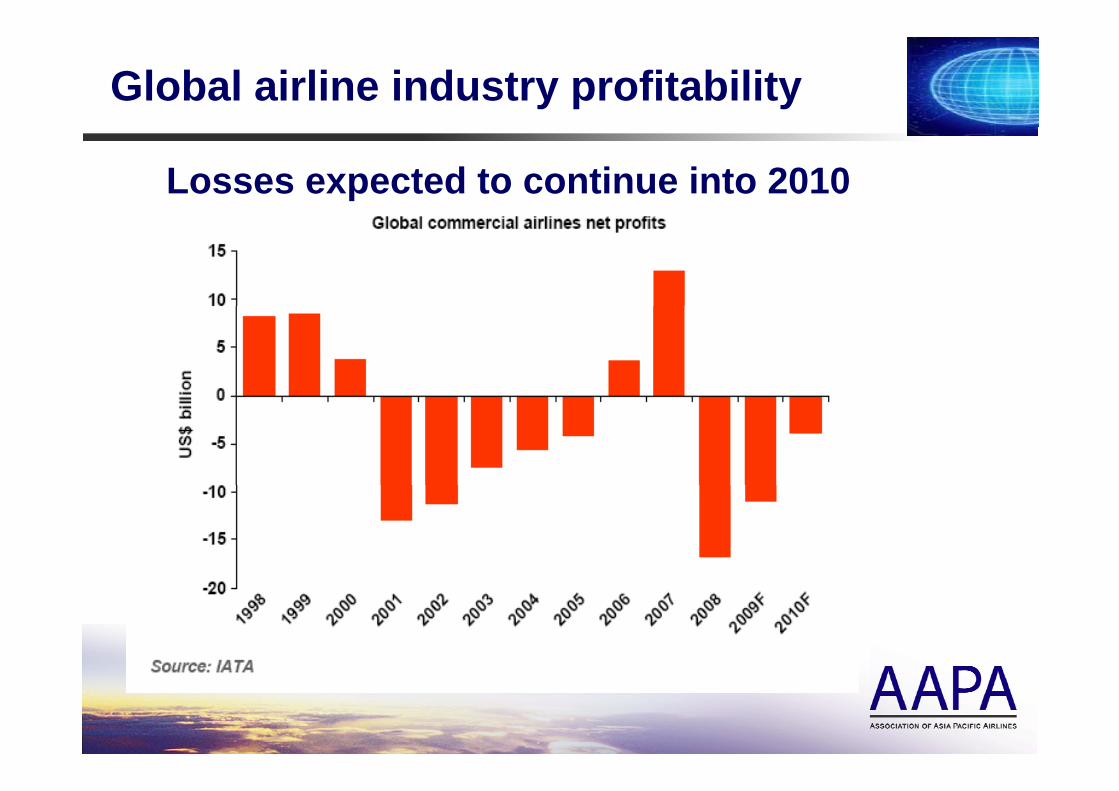

Global airline industry profitability

Losses expected to continue into 2010

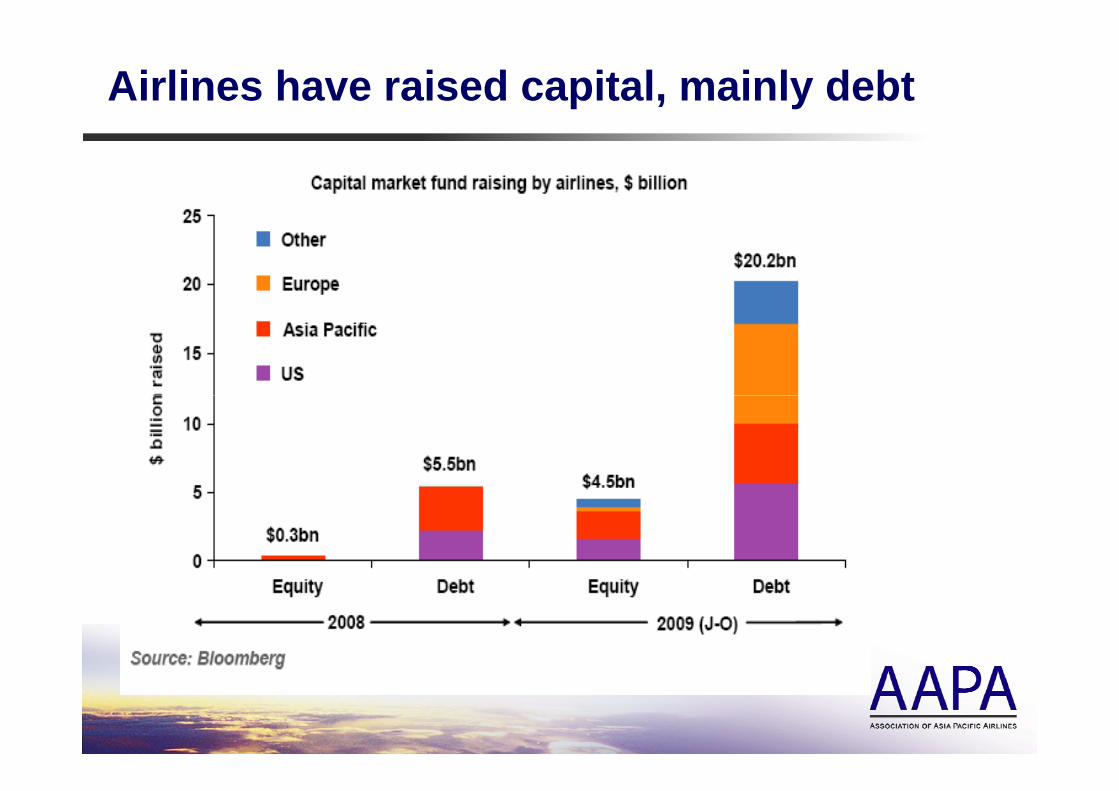

Airlines have raised capital, mainly debt

Airlines managed through the downturn

• Trimmed route networks and capacity in response to lower demandlower demand

• Reduced utilisation, grounded surplus aircraft, deferred g psome new deliveries

• Implemented wide range of measures to reduce staff• Implemented wide range of measures to reduce staff costs, retrenchment as a last resort

C d h h d b l h t• Conserved cash, shored up balance sheets

• Worked with industry partners to reduce unnecessaryWorked with industry partners to reduce unnecessary costsAirlines focused on survival whilstAirlines focused on survival whilst preserving ability to respond to any upturn

Regulatory Issuesg y• Regional perspectivesg• Safety

S it & F ilit ti• Security & Facilitation• Structural reformStructural reform• Environment

Global regulatory influences

AsiaAsia Pacific

Wider impact of US and EU regulations

Asia Pacific: regulatory perspectives

• Diverse region: multiple governments and regulators

• Institutional framework remains fragmented, although APEC and ASEAN do touch on aviation policy issues

• Need for multilateral cooperation

• Positive bias towards consensus, but sometimes slows the process

• Harmonisation is more about sharing best practices b f l i l ti t b t l i diff ftbefore legislating, not about resolving differences after unilaterally imposed regulations

• Global regulatory agenda still dominated by US and EU• Global regulatory agenda still dominated by US and EU

Asia Pacific lacks single voice and gunified negotiating power

Safety

• Asia Pacific aviation maintains a very good safety record• Still need to strengthen regional safety oversight and

make better use of available regulatory resources• Support ICAO recommendations and efforts to enhance

regional safety• Strong reservations about unilateral imposition of

operational bans on airlines, and effects of category downgrading of national authorities

• Need to harmonise ICAO/US/EU standards

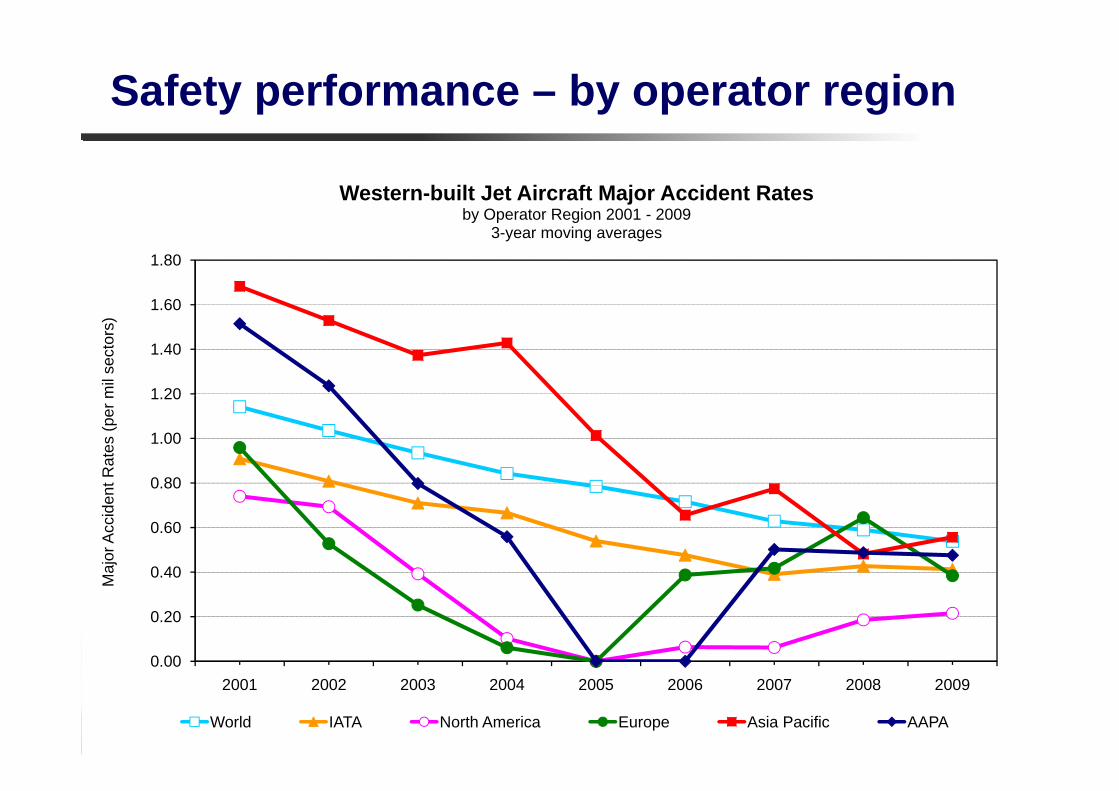

Safety performance – by operator region

Western-built Jet Aircraft Major Accident Rates by Operator Region 2001 - 2009

1 60

1.80

by Operator Region 2001 - 20093-year moving averages

1 20

1.40

1.60

mil

sect

ors)

0 80

1.00

1.20

t Rat

es (p

er m

0 40

0.60

0.80

Maj

or A

ccid

ent

0 00

0.20

0.40M

0.002001 2002 2003 2004 2005 2006 2007 2008 2009

World IATA North America Europe Asia Pacific AAPA

Security & Facilitation

• Air travel is both highly safe and secure

• Security procedures must balance risks against costs and inconvenience to the public

• Instead of kneejerk reactions, we need greater consistency and less duplicationy p

• Governments need to work with industry for the benefit of the travelling publicg p

• New technologies, including biometric identification and electronic information exchange, are an and electronic information exchange, are an opportunity to enhance security whilst streamlining travel

Structural reform

• Progressive liberalisation of traffic rights has supported growth but led to highly fragmented industry structuregrowth but led to highly fragmented industry structure

• Restrictive national ownership and control rules stand in the way of necessary restructuring and internationalthe way of necessary restructuring and international consolidation

D ti k t i l d t f i i t t d• Domestic markets remain closed to foreign investment and competition

• Airlines unable to fully access international capital markets

• Also need to reform quasi-monopoly aviation serviceAlso need to reform quasi monopoly aviation service providers, including airports and air navigation

Alliances and codeshares try to workAlliances and codeshares try to work around these constraints

Brighter Skies Beyond

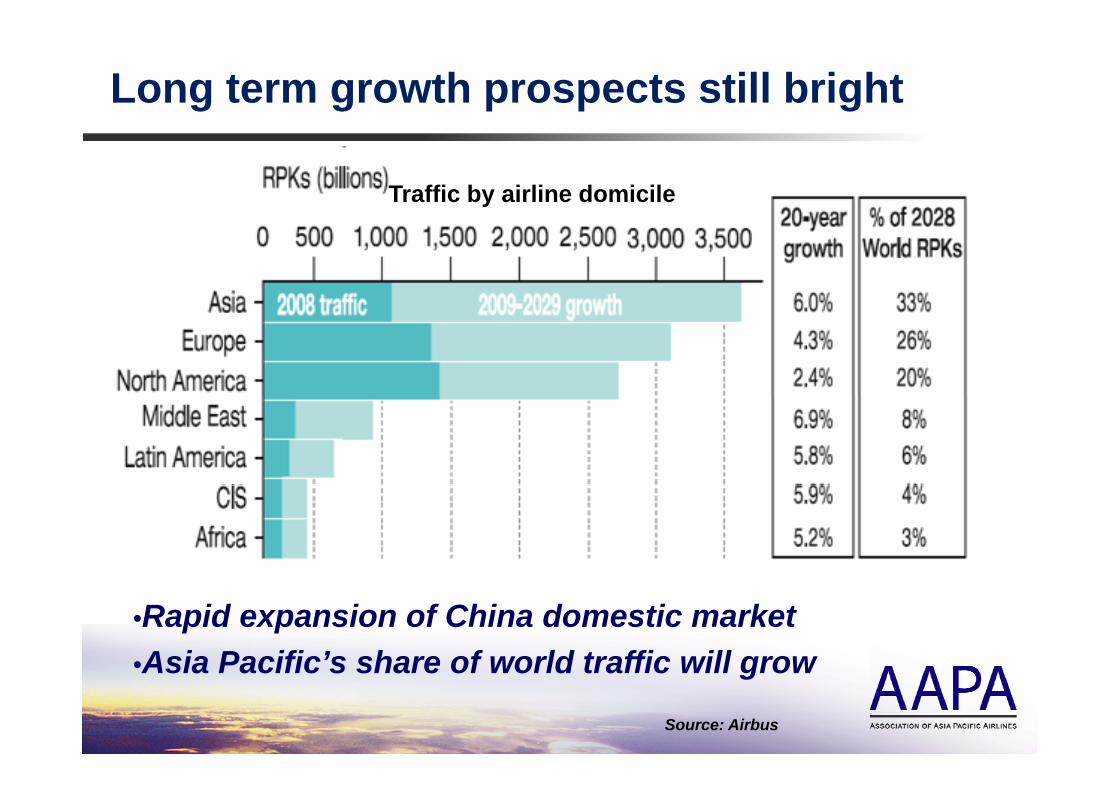

Long term growth prospects still bright

Traffic by airline domicile

•Rapid expansion of China domestic market•Asia Pacific’s share of world traffic will grow

Source: Airbus

•Asia Pacific s share of world traffic will grow

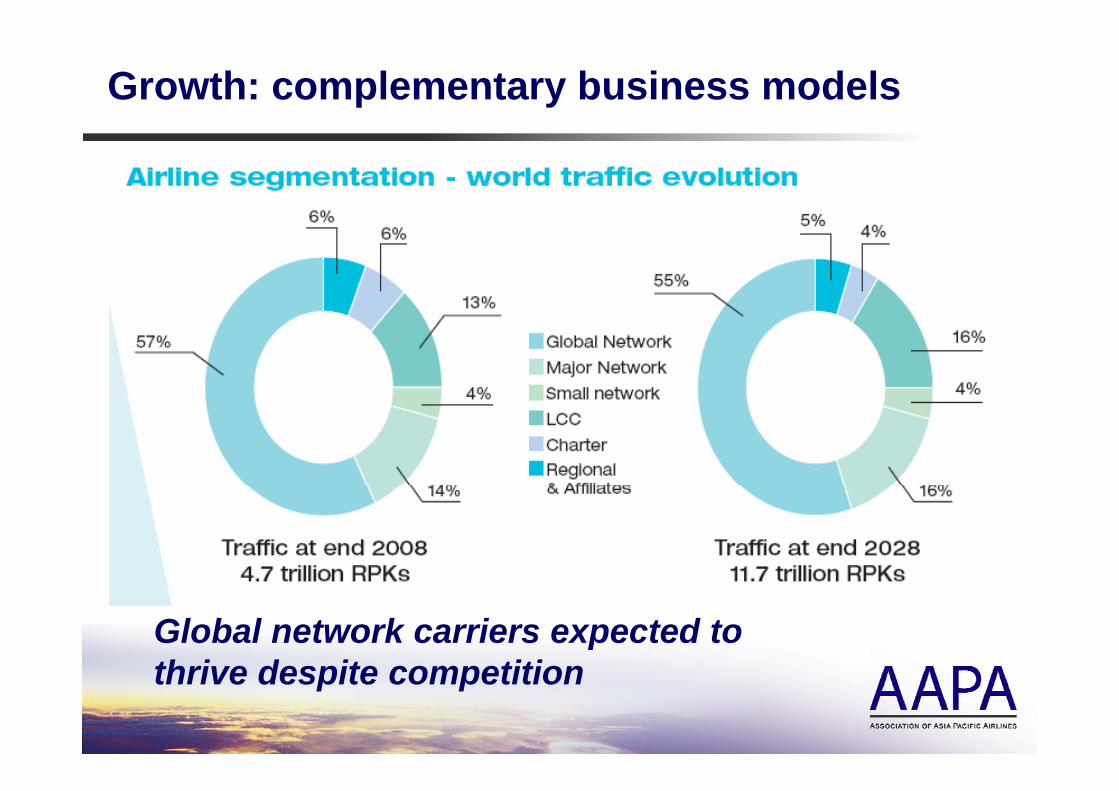

Growth: complementary business models

Global network carriers expected to th i d it titithrive despite competition

Sustainable Aviation

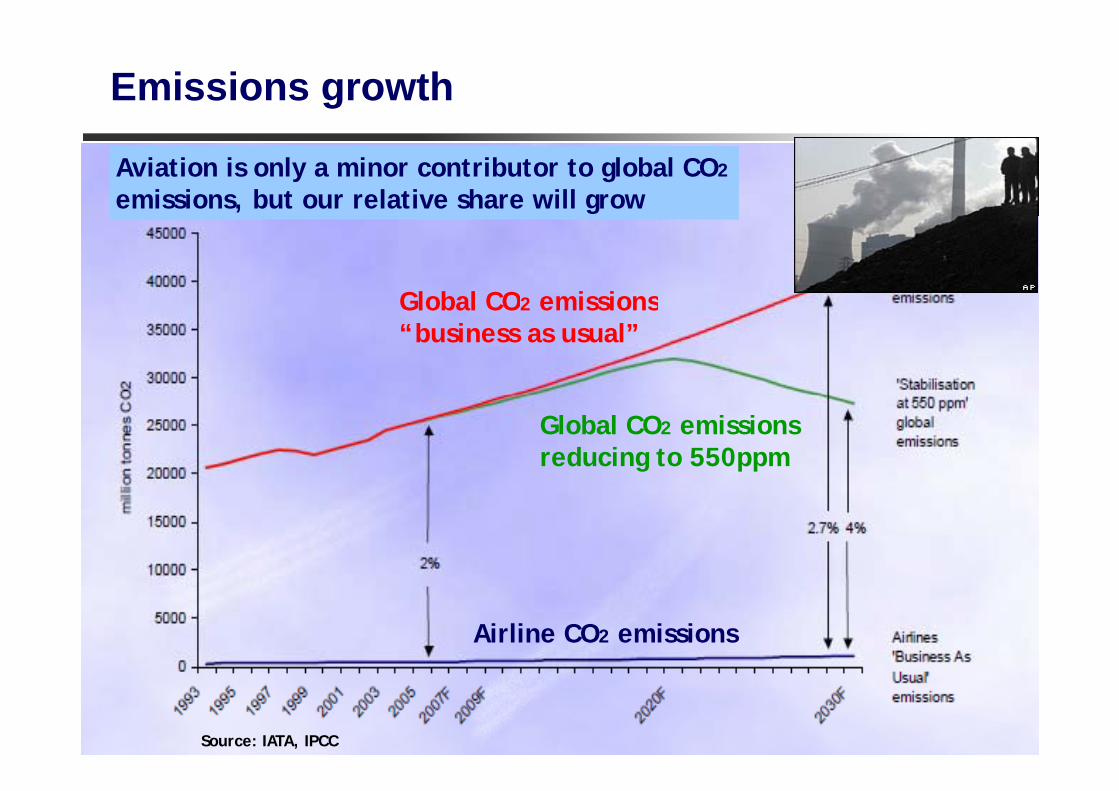

Emissions growth

Aviation is only a minor contributor to global CO2

emissions, but our relative share will grow

Global CO2 emissionsGlobal CO2 emissions“business as usual”

Global CO2 emissionsreducing to 550ppm

Airline CO2 emissions

Source: IATA, IPCC

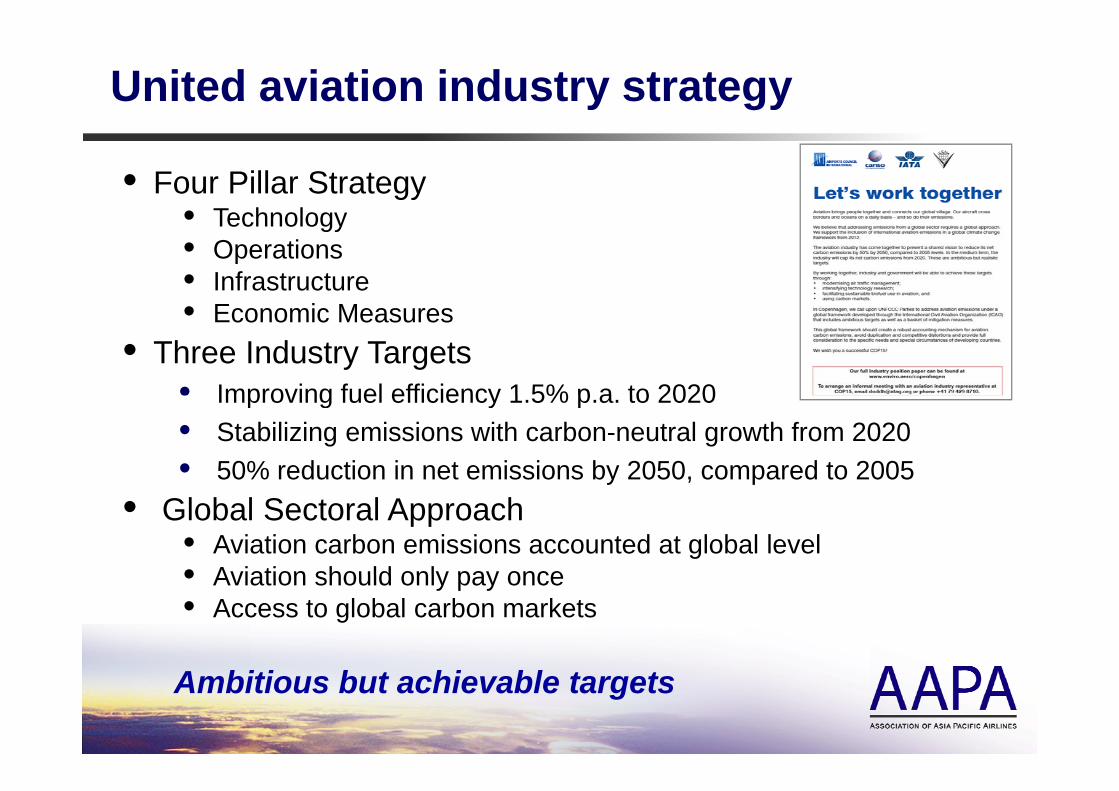

United aviation industry strategy

• Four Pillar Strategy• Technology• Technology• Operations• Infrastructure

E i M• Economic Measures• Three Industry Targets

• Improving fuel efficiency 1 5% p a to 2020Improving fuel efficiency 1.5% p.a. to 2020 • Stabilizing emissions with carbon-neutral growth from 2020 • 50% reduction in net emissions by 2050, compared to 2005

• Global Sectoral Approach• Aviation carbon emissions accounted at global level• Aviation should only pay once• Aviation should only pay once• Access to global carbon markets

Ambitious but achievable targets

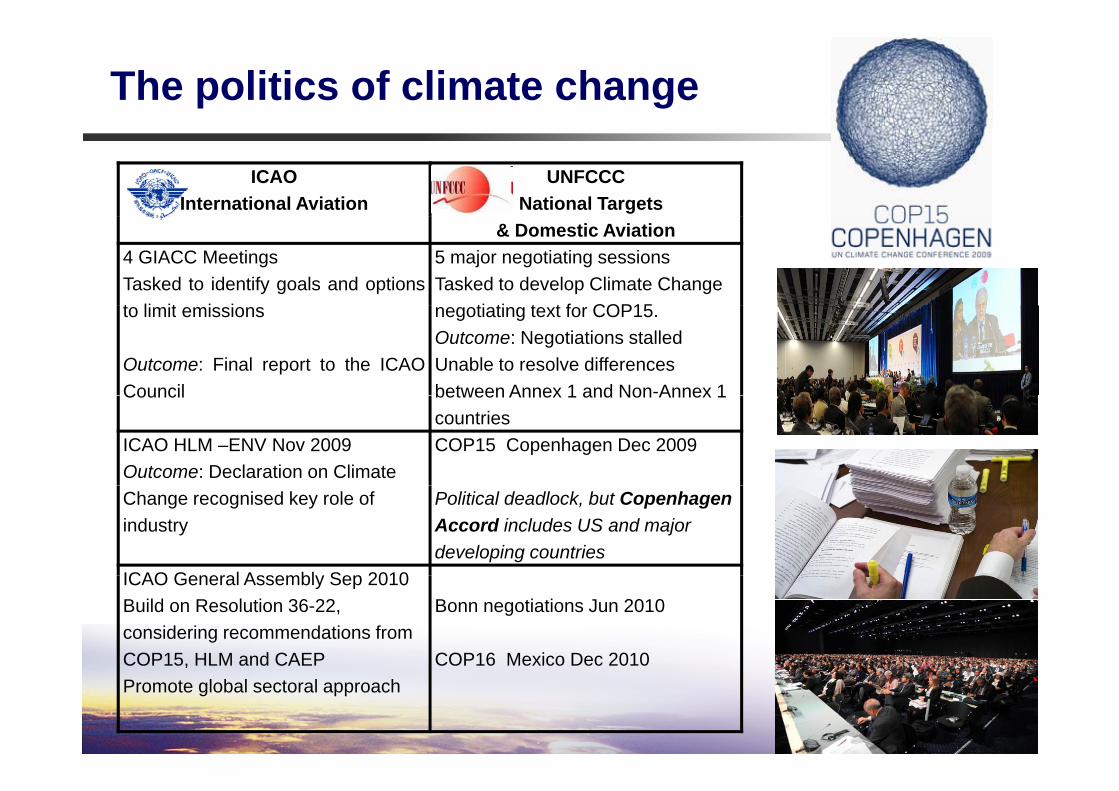

The politics of climate change

ICAOInternational Aviation

UNFCCCNational Targets

& Domestic Aviation4 GIACC MeetingsTasked to identify goals and optionst li it i i

5 major negotiating sessionsTasked to develop Climate Change

ti ti t t f COP15to limit emissions

Outcome: Final report to the ICAOCouncil

negotiating text for COP15.Outcome: Negotiations stalled Unable to resolve differences between Annex 1 and Non-Annex 1Council between Annex 1 and Non Annex 1 countries

ICAO HLM –ENV Nov 2009Outcome: Declaration on Climate

COP15 Copenhagen Dec 2009

Change recognised key role of industry

Political deadlock, but Copenhagen Accord includes US and major developing countries

ICAO G l A bl S 2010ICAO General Assembly Sep 2010Build on Resolution 36-22, considering recommendations from COP15, HLM and CAEP

Bonn negotiations Jun 2010

COP16 Mexico Dec 2010COP15, HLM and CAEPPromote global sectoral approach

COP16 Mexico Dec 2010

Conclusions

• Aviation is at the heart of global economic development

• The industry has weathered the storm of global recession

• But recovery remains uneven, and airlines are still struggling to restore profitability

• Growing economic influence of Asia Pacific needs to be matched by stronger engagement on key international policy issues

• Further steps needed to truly liberalise this most global

Prospects for long term growth remain good

of industries

Prospects for long term growth remain good

www.aapairlines.orgAssociation of Asia Pacific Airlines9/F Kompleks AntarabangsaJalan Sultan IsmailKuala Lumpur 50250MALAYSIAMALAYSIA

Tel: +60 3 2145 5600Fax: +60 3 2145 2500