briefing uk-spain cross-border estate planning · briefing . uk-spain cross-border ... uk-spain...

TRANSCRIPT

BRIEFING

UK-Spain Cross-Border Estate Planning ON Wednesday 6 November 2013, 12.00pm – 2.00pm AT 20 Cursitor Street, London, EC4A 1LT, United Kingdom HOSTED BY

UK-Spain Cross-Border Estate Planning – 6 November 2013 ________________________________________________________________________________

These Notes are intended to do no more than refresh the memories of those attending the conference of the salient points made. Whilst every care has been taken in preparing the Notes to ensure their accuracy, they cannot be exhaustive and are no substitute for detailed examination of the relevant statutes, cases and other materials when advising clients on particular matters. No responsibility can be accepted by the Society of Trust and Estate Practitioners or the speakers for any loss occasioned to any person acting or refraining from action in reliance on anything contained in these Notes. No part of the Notes may be reproduced in any form without the prior permission of the speakers.

© STEP Conferences 2013

UK-Spain Cross-Border Estate Planning – 6 November 2013 ______________________________________________________________________________

Notes for delegates claiming points under CPD/CPE schemes

Attendance at today’s conference will assist delegates in meeting their structured training commitments as follows:

Society of Trust and Estate Practitioners

The event qualifies for 1.5 hours towards meeting STEP members’ structured training commitment under the Society’s own Continuing Professional Development Scheme.

The Solicitors Regulation Authority (formerly the Law Society)

The event is accredited with 1.5 hours under the Solicitors Regulation Authority continuing professional development scheme. Please note, however, that to claim the hours, solicitors must sign the attendance register on the conference registration desk at the end of the conference (in order to confirm their attendance for the whole of the event under the Solicitor Regulation Authorities guidelines). Please quote your roll number, as well as your name and firm. The reference allocated by the Solicitors Regulation Authority to courses run by STEP, which must be quoted on your claim form, is AKZ/STCL.

NB In all cases, points/credits are subject to the appropriate claim being made

UK-Spain Cross-Border Estate Planning – 6 November 2013 ______________________________________________________________________________

PROGRAMME

12.00pm Arrival, Registration and Sandwich Lunch

12.30pm Chairman’s Welcome Address Edward Reed, Partner-Private Client, Macfarlanes LLP

12.35am UK-Spain Cross-Border Estate Planning Sonia Velasco, Partner-Tax, Cuatrecasas, Gonçalves Pereira S.L.P.

1.35pm Questions and Answers: Part 1

1.50pm Chairman’s Closing Remarks Edward Reed, Partner-Private Client, Macfarlanes LLP

2.00pm Conference Close

UK-Spain Cross-Border Estate Planning – 6 November 2013 ______________________________________________________________________________

DELEGATE LIST

Luis Aguilera Barclays

Monica Alvarez Barclays

Steve Atkinson Lombard Intermediation Services

Alvaro Aznar Alberto Pérez Cedillo Spanish Lawyers and Solicitors

Karen Bayley Barlow Robbins LLP

Nigel Beadsworth Stonehage Law Limited

Stewart Bond SBCA Chartered Accountants

Helen Bryant Farrer & Co

Julie Burling Ingenhaag LLP

Susan Cambridge Charles Stanley & Co Ltd

Emma Carey Calvert Smith & Sutcliffe

Samuel Cater PKF Littlejohn LLP

Sangna Chauhan Speechly Bircham LLP

Edward Chivers Farrer & Co.

Paul Davidoff Bircham Dyson Bell

Christophe Daviron Citibank

Seema Dodhia BDO LLP

Amanda Edwards Boodle Hatfield LLP

Barbara Gardener Technical Connection ltd

Ceris Gardner Maurice Turnor Gardner LLP

Michael Goldstein Goodman Jones LLP

Adam Hampton Pothecary Witham Weld

Dan Harris Stone King LLP

David Hickmott Mishcon de Reya

Sarah Ibbotson HSBC Trust Co (UK) Ltd

DELEGATE LIST CONTINUED

Catherine Izzard Tees Law

James Johnston Bircham Dyson Bell

Andrew Jones Mackrell Turner Garrett

Sevyn Kalsi New Quadrant Partners LLP

Yasmina Kreaa Menzies LLP

David Lane Vestra Wealth LLP

Margaret Lang WGS Solicitors

Esther Lee Farrer & Co.

Julian Melling NPGWM

Tony Millson Royds LLP

Luke Mowbray Wilsons Solicitors LLP

Eleanor O'Brien Frank Hirth

Ruth O'Neill Piper Smith Watton LLP

Alberto Perez Cedillo Alberto Perez Cedillo Spanish lawyers and Solicitors

Jason Porter Credit Suisse (UK) Limited

Jennie Pratt AshtonKCJ

Graeme Privett Rawlinson & Hunter

Beatrice Puoti Burges Salmon LLP

Michael Soul Michael Soul & Asociados

Richard Stait Magna Carta Wills

Ruth Thompson BDO

Hannah Wailoo Piper Smith Watton LLP

Martin Ward Corinthian Asset Protection

STAFF LIST

Kelly Wu Society of Trust and Estate Practitioners (STEP)

Emma Yeats Society of Trust and Estate Practitioners (STEP)

UK-Spain Cross-Border Estate Planning – 6 November 2013 _____________________________________________________________________________

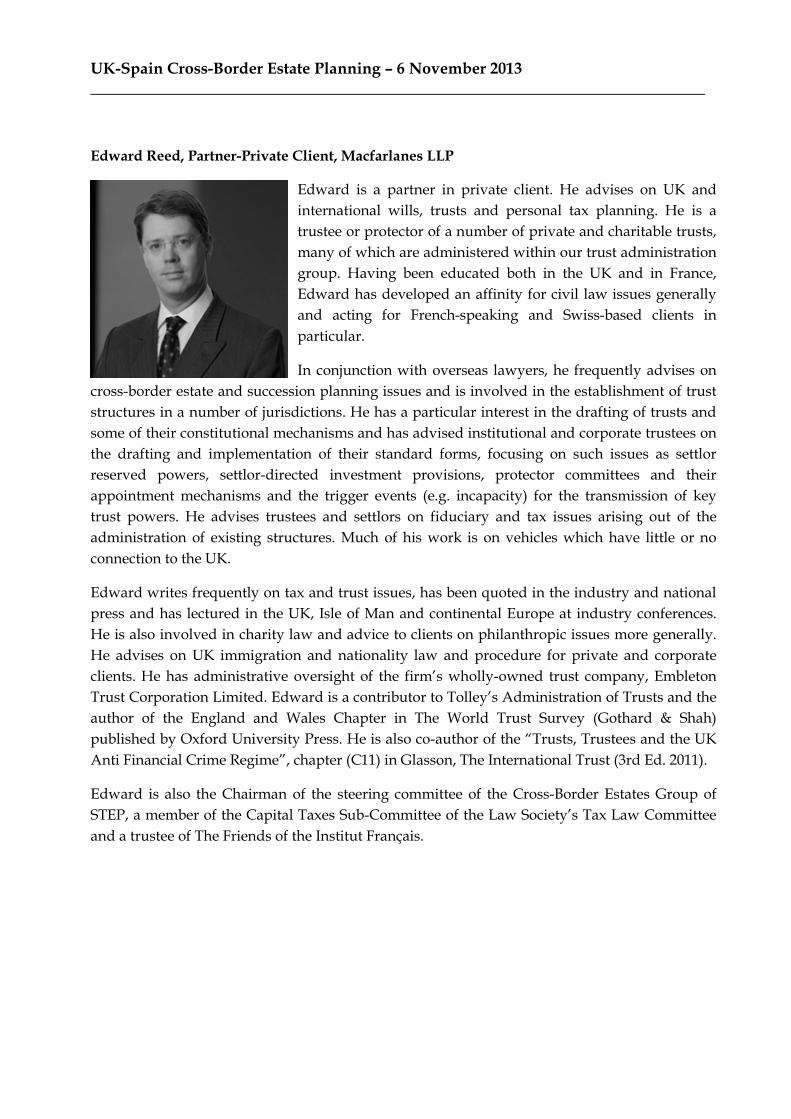

Edward Reed, Partner-Private Client, Macfarlanes LLP

Edward is a partner in private client. He advises on UK and international wills, trusts and personal tax planning. He is a trustee or protector of a number of private and charitable trusts, many of which are administered within our trust administration group. Having been educated both in the UK and in France, Edward has developed an affinity for civil law issues generally and acting for French-speaking and Swiss-based clients in particular.

In conjunction with overseas lawyers, he frequently advises on cross-border estate and succession planning issues and is involved in the establishment of trust structures in a number of jurisdictions. He has a particular interest in the drafting of trusts and some of their constitutional mechanisms and has advised institutional and corporate trustees on the drafting and implementation of their standard forms, focusing on such issues as settlor reserved powers, settlor-directed investment provisions, protector committees and their appointment mechanisms and the trigger events (e.g. incapacity) for the transmission of key trust powers. He advises trustees and settlors on fiduciary and tax issues arising out of the administration of existing structures. Much of his work is on vehicles which have little or no connection to the UK.

Edward writes frequently on tax and trust issues, has been quoted in the industry and national press and has lectured in the UK, Isle of Man and continental Europe at industry conferences. He is also involved in charity law and advice to clients on philanthropic issues more generally. He advises on UK immigration and nationality law and procedure for private and corporate clients. He has administrative oversight of the firm’s wholly-owned trust company, Embleton Trust Corporation Limited. Edward is a contributor to Tolley’s Administration of Trusts and the author of the England and Wales Chapter in The World Trust Survey (Gothard & Shah) published by Oxford University Press. He is also co-author of the “Trusts, Trustees and the UK Anti Financial Crime Regime”, chapter (C11) in Glasson, The International Trust (3rd Ed. 2011).

Edward is also the Chairman of the steering committee of the Cross-Border Estates Group of STEP, a member of the Capital Taxes Sub-Committee of the Law Society’s Tax Law Committee and a trustee of The Friends of the Institut Français.

UK-Spain Cross-Border Estate Planning – 6 November 2013 _____________________________________________________________________________

Sonia Velasco, Partner-Tax, Cuatrecasas, Gonçalves Pereira S.L.P.

A partner in the firm's tax practice, Sonia Velasco advises international clients (multinationals, venture-capital and private-equity entities) on acquisitions, disinvestments and restructurings. From 2006 to 2009, Sonia was based in Cuatrecasas, Gonçalves Pereira's New York office, working closely with United States (US) and Canadian multinationals, and venture capital companies with investments in Spain and Latin America.

Sonia also advises private clients in their wealth planning and succession planning. Her experience in the US has provided her with in-depth knowledge of US legal forms such as trusts that do not have precise counterparts in Spanish law.

Sonia’s specialty areas are:

> Family Business

> Foundations and Non-profit Organizations

> Hotels, Tourism and Leisure

> Private Equity

> Tax

> Technology, Media and Telecommunications (TMT)

UK-SPAIN CROSS BORDER TAX AND

ESTATE PLANNING

SONIA VELASCO

STEP, NOVEMBER 2013

SUMMARY

1. Personal income tax

2. Real estate ownership by foreign individuals

3. ETVE as personal holding company

4. Wealth tax

5. Spanish Tax regime

6. Spanish inheritance and gift tax

7. Trusts

8. New disclosure obligations: Form 720

2

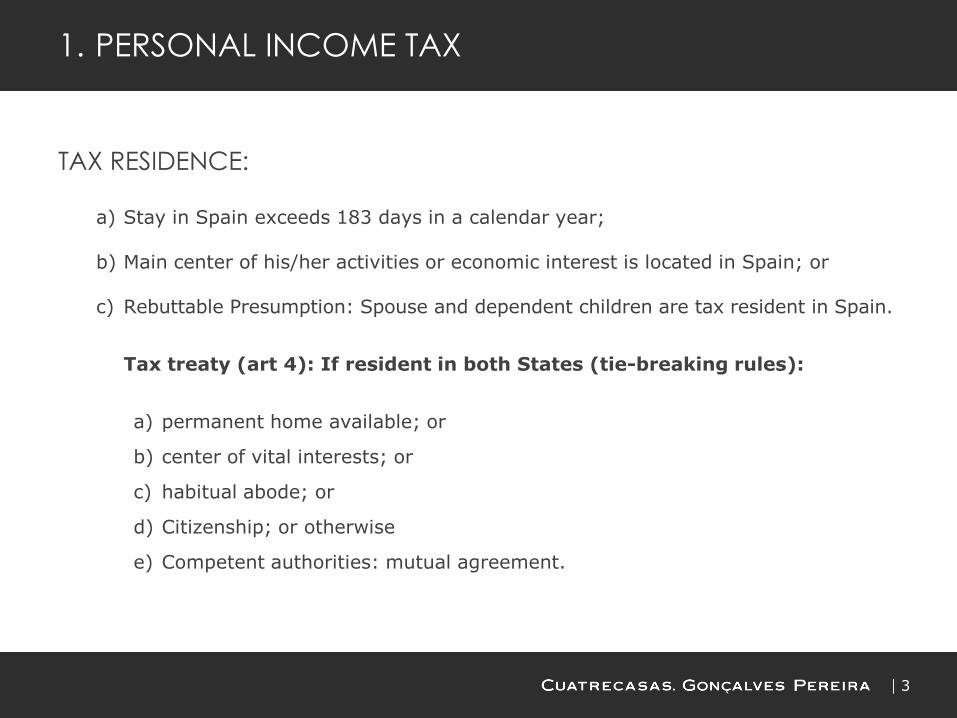

1. PERSONAL INCOME TAX

TAX RESIDENCE:

a) Stay in Spain exceeds 183 days in a calendar year;

b) Main center of his/her activities or economic interest is located in Spain; or

c) Rebuttable Presumption: Spouse and dependent children are tax resident in Spain.

Tax treaty (art 4): If resident in both States (tie-breaking rules):

a) permanent home available; or

b) center of vital interests; or

c) habitual abode; or

d) Citizenship; or otherwise

e) Competent authorities: mutual agreement.

3

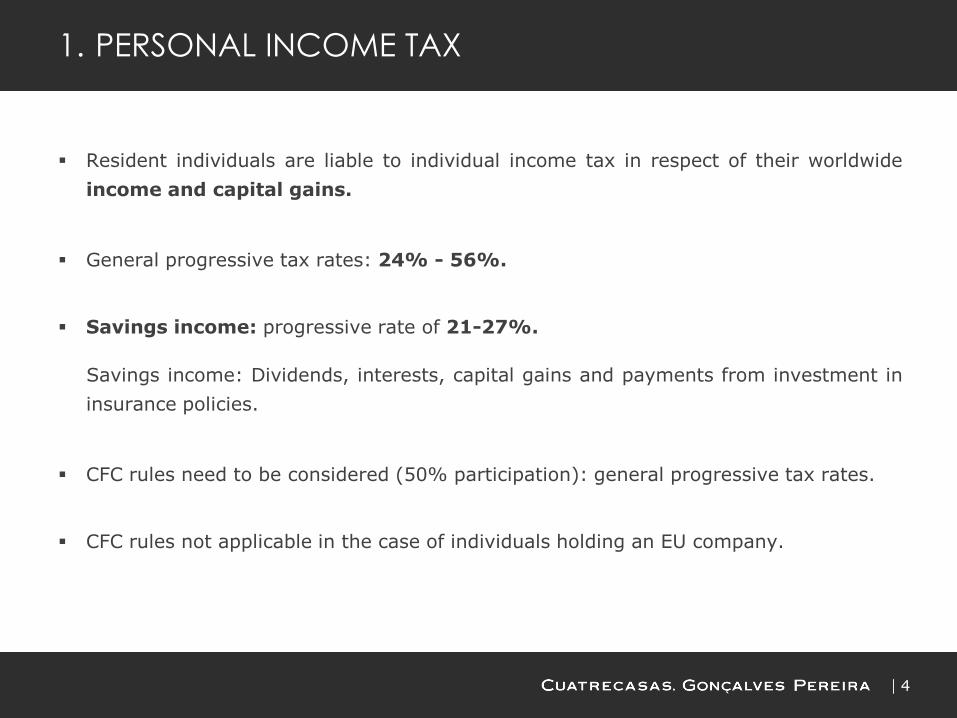

1. PERSONAL INCOME TAX

Resident individuals are liable to individual income tax in respect of their worldwide

income and capital gains.

General progressive tax rates: 24% - 56%.

Savings income: progressive rate of 21-27%.

Savings income: Dividends, interests, capital gains and payments from investment in

insurance policies.

CFC rules need to be considered (50% participation): general progressive tax rates.

CFC rules not applicable in the case of individuals holding an EU company.

4

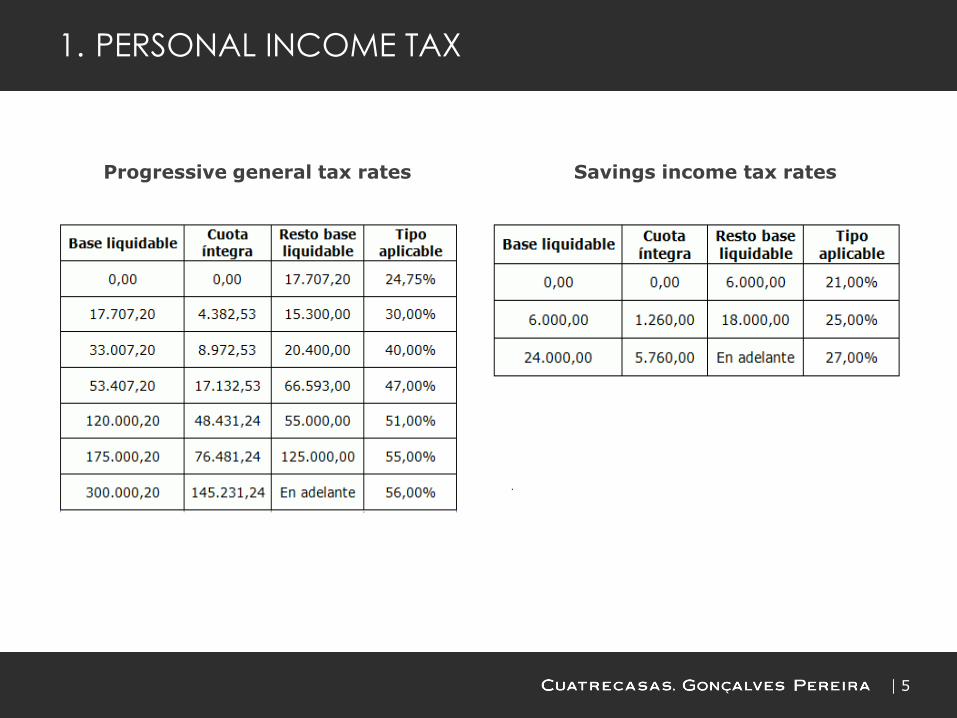

Progressive general tax rates

.

Savings income tax rates

5

1. PERSONAL INCOME TAX

1. PERSONAL INCOME TAX

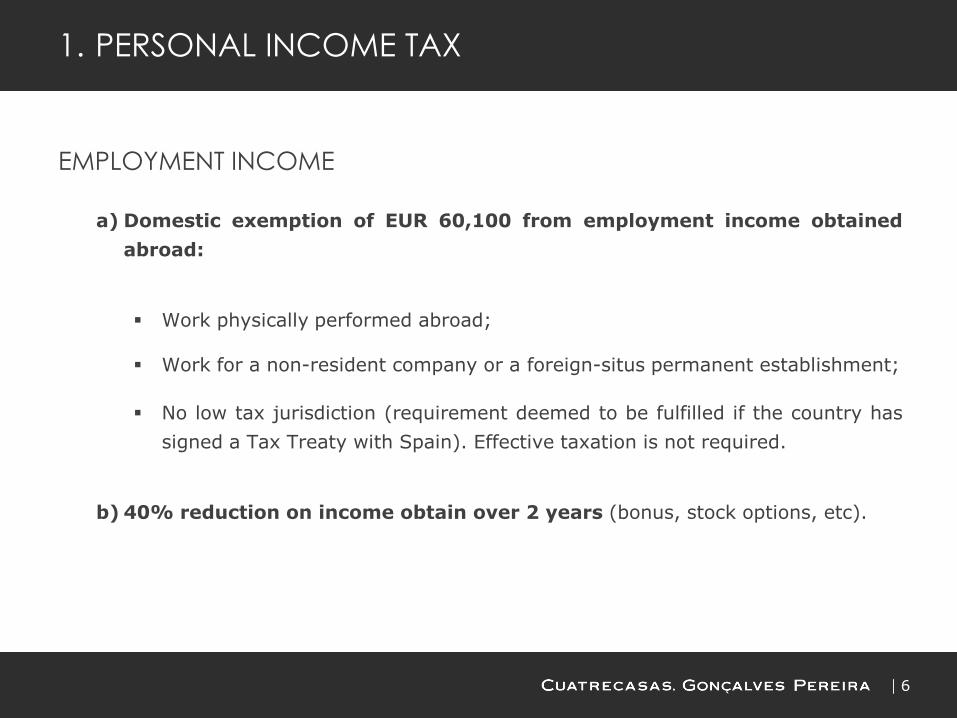

EMPLOYMENT INCOME

a) Domestic exemption of EUR 60,100 from employment income obtained

abroad:

Work physically performed abroad;

Work for a non-resident company or a foreign-situs permanent establishment;

No low tax jurisdiction (requirement deemed to be fulfilled if the country has

signed a Tax Treaty with Spain). Effective taxation is not required.

b) 40% reduction on income obtain over 2 years (bonus, stock options, etc).

6

1. PERSONAL INCOME TAX

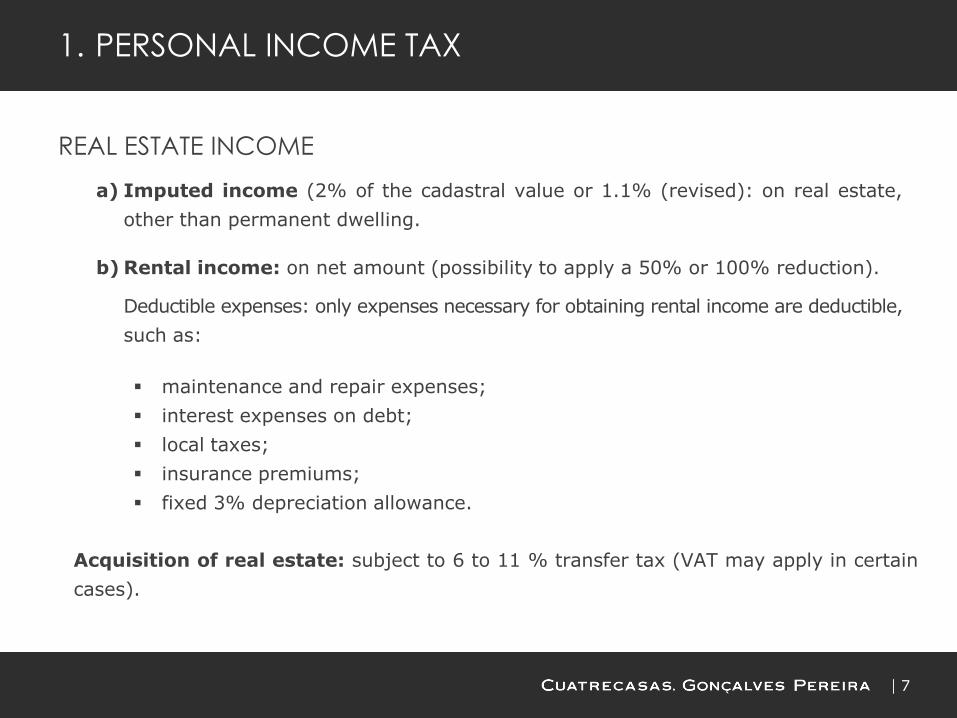

REAL ESTATE INCOME

a) Imputed income (2% of the cadastral value or 1.1% (revised): on real estate,

other than permanent dwelling.

b) Rental income: on net amount (possibility to apply a 50% or 100% reduction).

Deductible expenses: only expenses necessary for obtaining rental income are deductible,

such as:

maintenance and repair expenses;

interest expenses on debt;

local taxes;

insurance premiums;

fixed 3% depreciation allowance.

Acquisition of real estate: subject to 6 to 11 % transfer tax (VAT may apply in certain

cases).

7

1. PERSONAL INCOME TAX

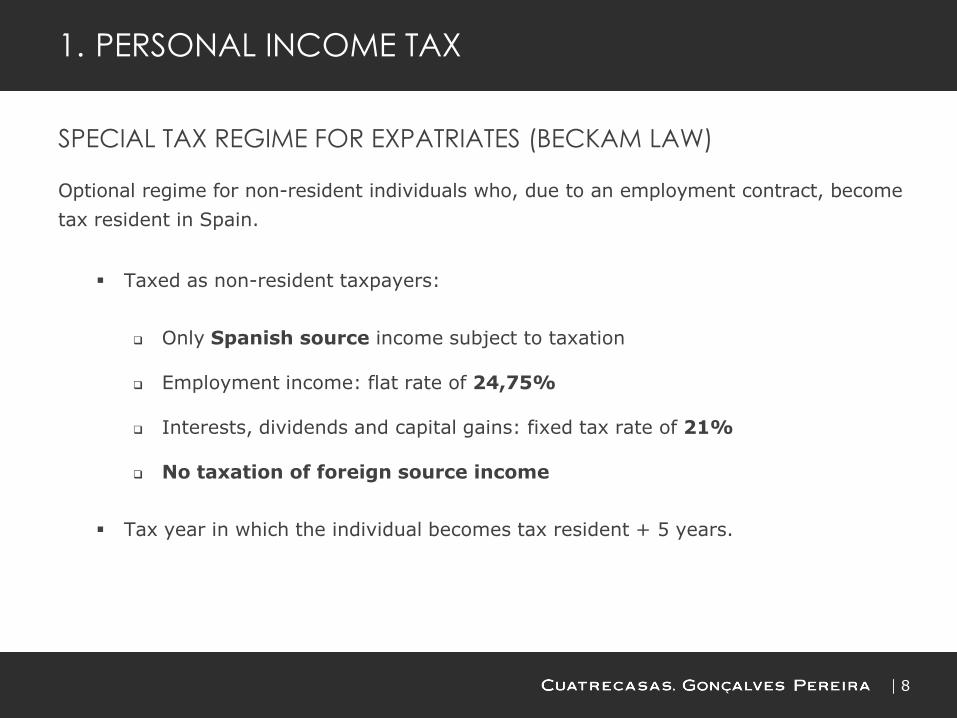

SPECIAL TAX REGIME FOR EXPATRIATES (BECKAM LAW)

Optional regime for non-resident individuals who, due to an employment contract, become

tax resident in Spain.

Taxed as non-resident taxpayers:

Only Spanish source income subject to taxation

Employment income: flat rate of 24,75%

Interests, dividends and capital gains: fixed tax rate of 21%

No taxation of foreign source income

Tax year in which the individual becomes tax resident + 5 years.

8

1. PERSONAL INCOME TAX

SPECIAL TAX REGIME FOR EXPATRIATES

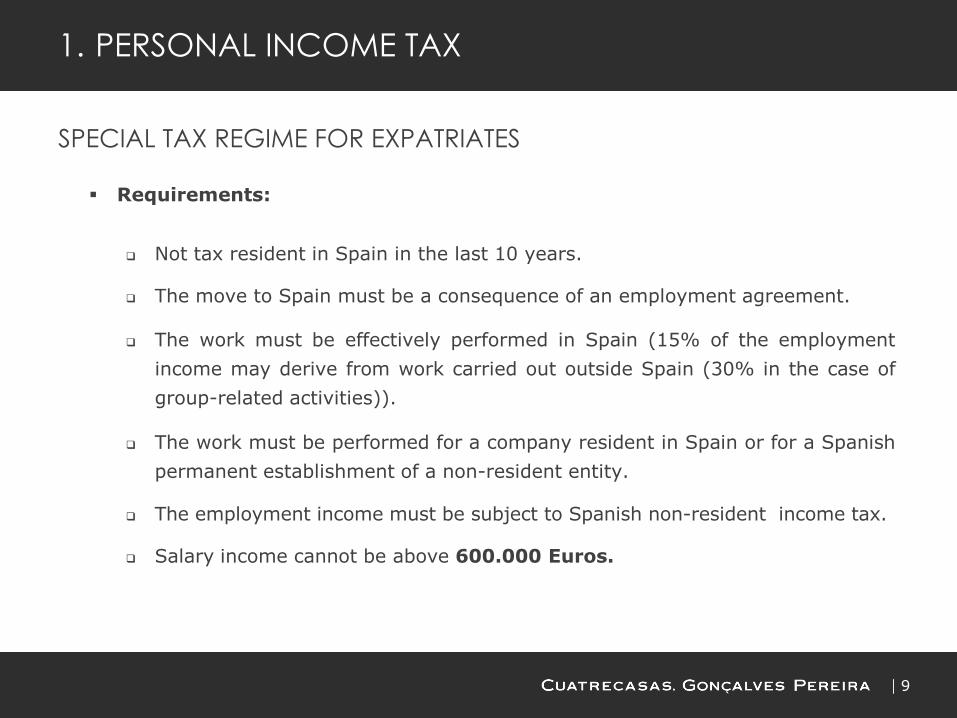

Requirements:

Not tax resident in Spain in the last 10 years.

The move to Spain must be a consequence of an employment agreement.

The work must be effectively performed in Spain (15% of the employment

income may derive from work carried out outside Spain (30% in the case of

group-related activities)).

The work must be performed for a company resident in Spain or for a Spanish

permanent establishment of a non-resident entity.

The employment income must be subject to Spanish non-resident income tax.

Salary income cannot be above 600.000 Euros.

9

10

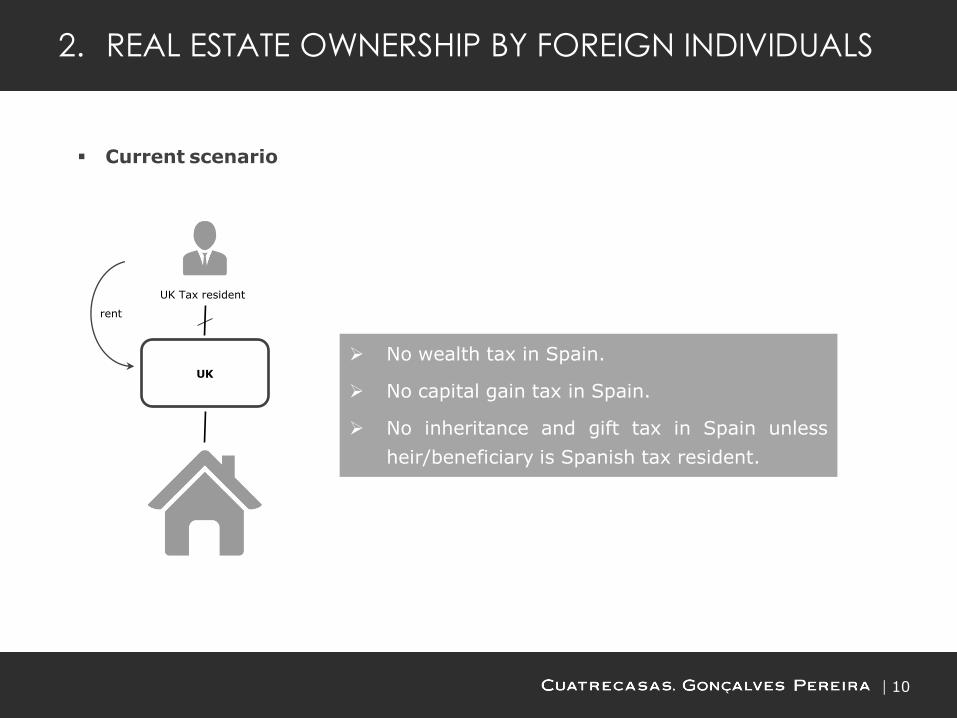

2. REAL ESTATE OWNERSHIP BY FOREIGN INDIVIDUALS

Current scenario

No wealth tax in Spain.

No capital gain tax in Spain.

No inheritance and gift tax in Spain unless

heir/beneficiary is Spanish tax resident.

UK

UK Tax resident

rent

11

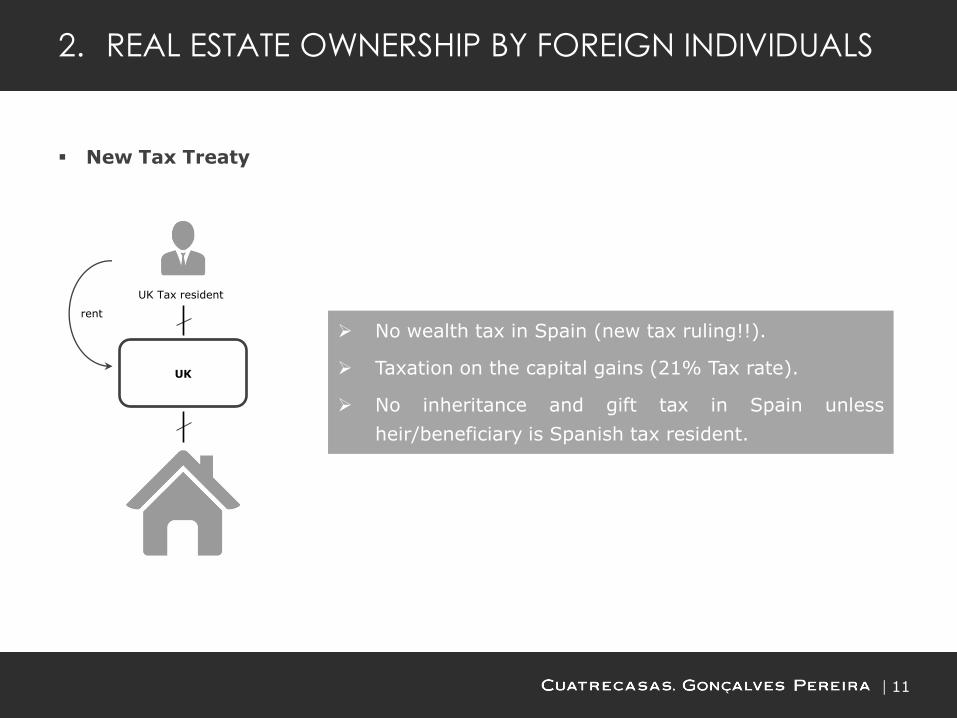

2. REAL ESTATE OWNERSHIP BY FOREIGN INDIVIDUALS

New Tax Treaty

No wealth tax in Spain (new tax ruling!!).

Taxation on the capital gains (21% Tax rate).

No inheritance and gift tax in Spain unless

heir/beneficiary is Spanish tax resident.

UK

UK Tax resident

rent

12

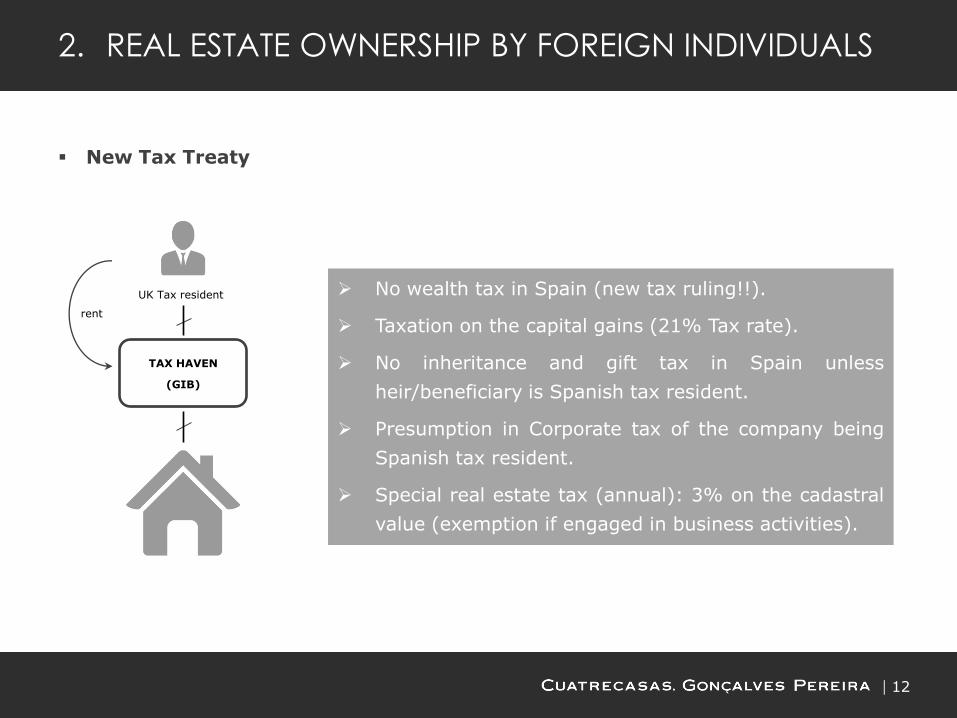

2. REAL ESTATE OWNERSHIP BY FOREIGN INDIVIDUALS

New Tax Treaty

No wealth tax in Spain (new tax ruling!!).

Taxation on the capital gains (21% Tax rate).

No inheritance and gift tax in Spain unless

heir/beneficiary is Spanish tax resident.

Presumption in Corporate tax of the company being

Spanish tax resident.

Special real estate tax (annual): 3% on the cadastral

value (exemption if engaged in business activities).

TAX HAVEN

(GIB)

UK Tax resident

rent

3. ETVE AS PERSONAL HOLDING COMPANY

ETVE: No taxation on dividends and capital gains derived from non-resident qualifying shareholdings.

SHAREHOLDERS: Dividends paid by ETVE out from qualifying shareholdings: 0% withholding tax for both non-resident: (i) corporations and (ii) individuals

21% withholding tax on dividends to resident individuals or a tax haven jurisdictions

0% taxation for Spanish corporations

SHAREHOLDERS: Transfer and winding up of the ETVE: 0% taxation for non residents qualifying shareholders (not tax havens)

0% taxation for Spanish corporations

21% taxation for Spanish resident individuals

13

SIGNED AND IN

FORCE:

Argentina

Bolivia

Brazil

Chile

Cuba

Ecuador

Mexico

Venezuela

Colombia

Costa Rica

Uruguay

Panama

IN PROCESS OF

NEGOTIATION:

Dominican Republic

Honduras

Guatemala

SIGNED BUT NOT YET

IN FORCE:

Peru

El Salvador

Trinidad Tobago

Jamaica

4. WIDEST LATAM TREATY NETWORK

14

Act 4/2008, 25 December 2008: “Abolishment of Wealth Tax”: 100% tax allowance

over the total tax due for both resident and non-resident individuals. No obligation of

filing tax returns below a taxable base of 2 million Euros.

Act RDL 13/2011: “temporary reintroduction of wealth tax for 2012-2013”. Possibly,

wealth tax will be maintained for 2014.

Applicable to resident and non resident except tax residents in Madrid.

5. WEALTH TAX

15

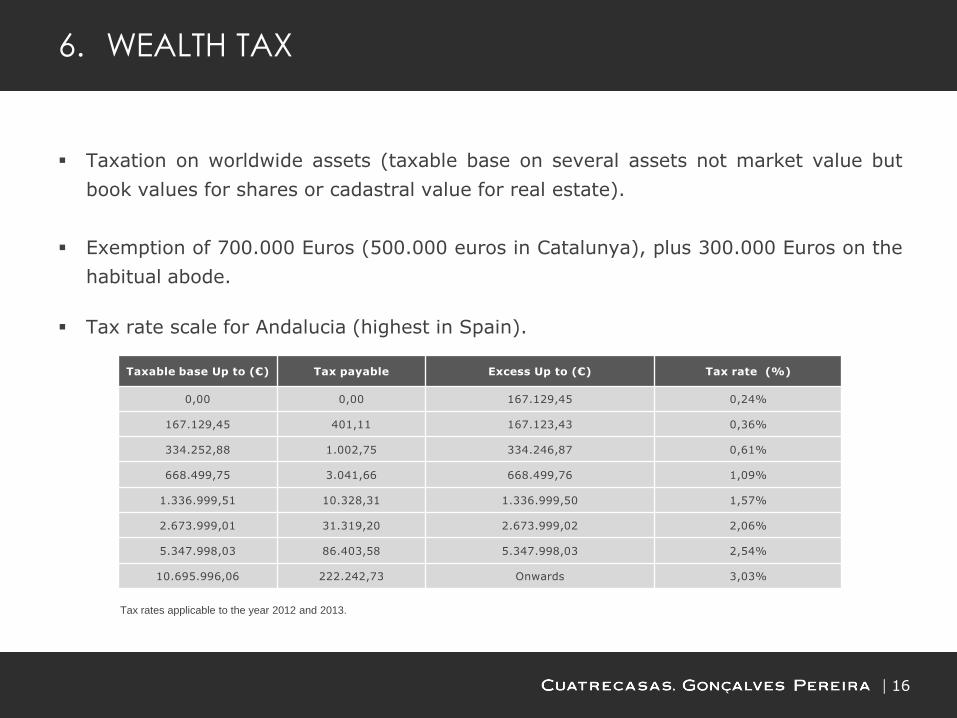

6. WEALTH TAX

Taxation on worldwide assets (taxable base on several assets not market value but

book values for shares or cadastral value for real estate).

Exemption of 700.000 Euros (500.000 euros in Catalunya), plus 300.000 Euros on the

habitual abode.

Tax rate scale for Andalucia (highest in Spain).

Taxable base Up to (€) Tax payable Excess Up to (€) Tax rate (%)

0,00 0,00 167.129,45 0,24%

167.129,45 401,11 167.123,43 0,36%

334.252,88 1.002,75 334.246,87 0,61%

668.499,75 3.041,66 668.499,76 1,09%

1.336.999,51 10.328,31 1.336.999,50 1,57%

2.673.999,01 31.319,20 2.673.999,02 2,06%

5.347.998,03 86.403,58 5.347.998,03 2,54%

10.695.996,06 222.242,73 Onwards 3,03%

Tax rates applicable to the year 2012 and 2013.

16

6. WEALTH TAX

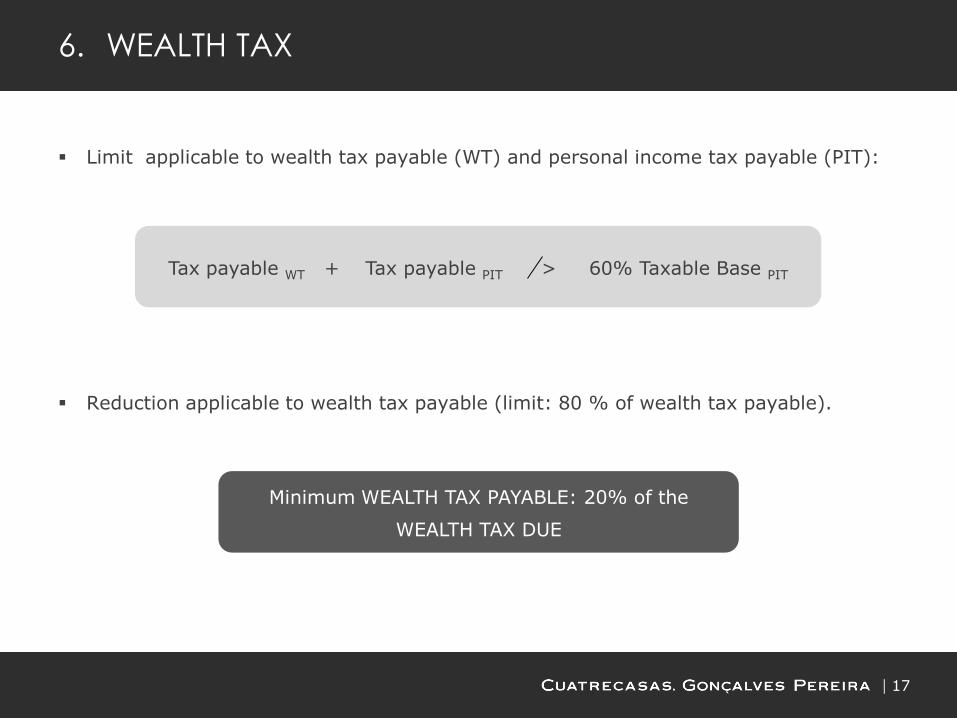

Limit applicable to wealth tax payable (WT) and personal income tax payable (PIT):

Reduction applicable to wealth tax payable (limit: 80 % of wealth tax payable).

Tax payable WT + Tax payable PIT > 60% Taxable Base PIT

Minimum WEALTH TAX PAYABLE: 20% of the

WEALTH TAX DUE

17

7. SPANISH INHERITANCE AND GIFT TAX

SPANISH SOURCE:

The decisive factor is the Spanish tax residence of the recipient and, in some

cases, the location of the assets transferred.

Resident taxpayers: liable to tax on worldwide assets and rights acquired.

Non -resident taxpayers are liable to tax on:

- Assets located in Spain.

- Rights which may be exercised in Spain.

- Proceeds under a life insurance policy taken with a Spanish insurance company

or with Spanish branch of a foreign entity.

18

7. SPANISH INHERITANCE AND GIFT TAX

Taxpayers: the heir or legatee,

the donee/beneficiary,

the beneficiary of a life insurance policy.

*Legal entities are not subject to Inheritance and Gift Tax.

Taxable event: Mortis causa or intervivos acquisition of assets and rights.

Proceeds of a life insurance policy where the beneficiary and the policy holder are

not the same person.

19

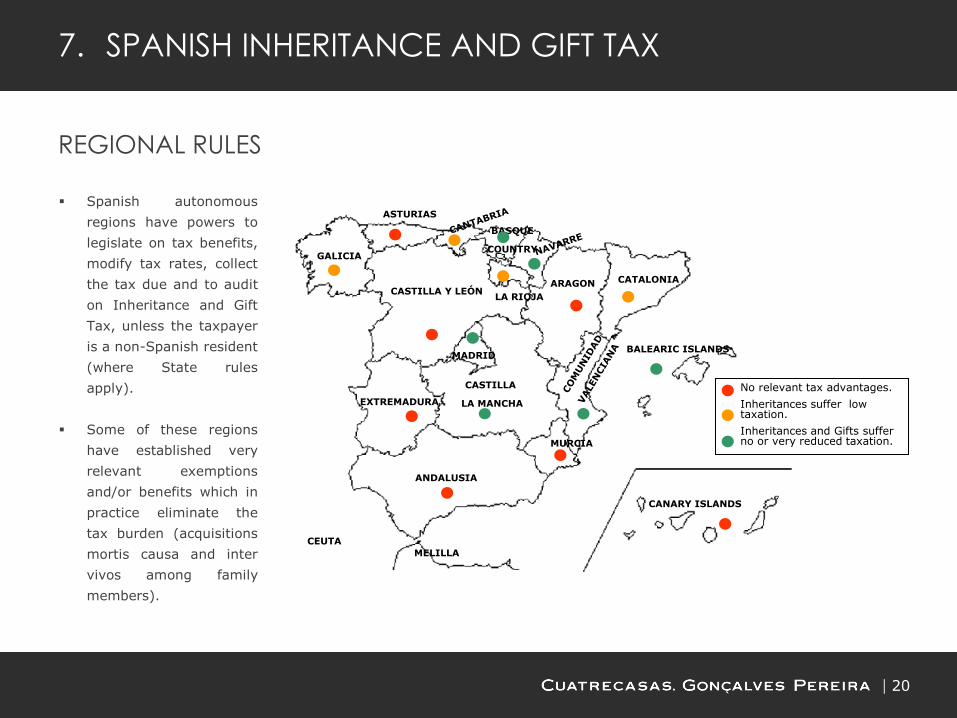

GALICIA

BASQUE

COUNTRY

ASTURIAS

LA RIOJA

ARAGON CATALONIA

MADRID

CASTILLA

LA MANCHA

MURCIA

ANDALUSIA

EXTREMADURA

BALEARIC ISLANDS

CANARY ISLANDS

CEUTA

MELILLA

CASTILLA Y LEÓN

No relevant tax advantages.

Inheritances suffer low taxation.

Inheritances and Gifts suffer no or very reduced taxation.

7. SPANISH INHERITANCE AND GIFT TAX

REGIONAL RULES

Spanish autonomous

regions have powers to

legislate on tax benefits,

modify tax rates, collect

the tax due and to audit

on Inheritance and Gift

Tax, unless the taxpayer

is a non-Spanish resident

(where State rules

apply).

Some of these regions

have established very

relevant exemptions

and/or benefits which in

practice eliminate the

tax burden (acquisitions

mortis causa and inter

vivos among family

members).

20

Mortis causa transfers:

Gifts of real estate:

Gifts other than of real estate:

Resident deceased Non-resident deceased

Non-resident taxpayer STATE RULES STATE RULES

Resident taxpayer REGIONAL RULES (5 years

residency)1 STATE RULES

Spanish real estate Foreign real estate

Non-resident taxpayer STATE RULES N/A

Resident taxpayer REGIONAL RULES (Rule where the real estate is located apply)

STATE RULES

Resident donor Non-resident donor

Non-resident taxpayer STATE RULES STATE RULES

Resident taxpayer REGIONAL RULES (5 years

residency)1

REGIONAL RULES (5 years residency)

1 Regional rules apply when the deceased or the recipient have remained the majority of days for the last 5 years in a concrete Region of Spain. This rule does not apply in gifts in the form of real estate.

7. SPANISH INHERITANCE AND GIFT TAX

21

7. SPANISH INHERITANCE AND GIFT TAX

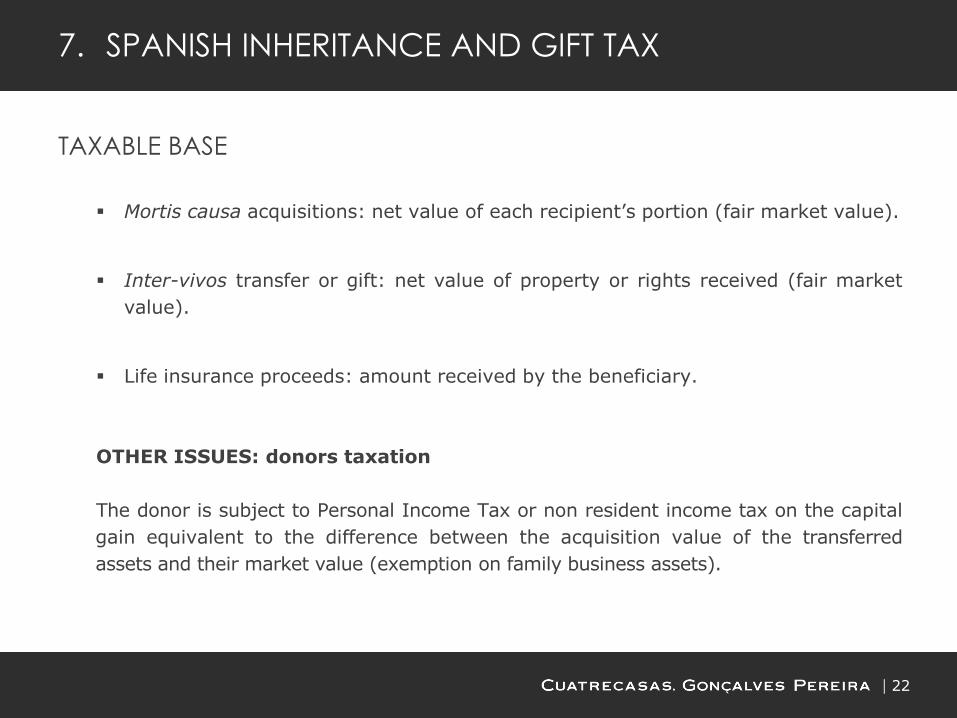

TAXABLE BASE

Mortis causa acquisitions: net value of each recipient’s portion (fair market value).

Inter-vivos transfer or gift: net value of property or rights received (fair market

value).

Life insurance proceeds: amount received by the beneficiary.

OTHER ISSUES: donors taxation

The donor is subject to Personal Income Tax or non resident income tax on the capital

gain equivalent to the difference between the acquisition value of the transferred

assets and their market value (exemption on family business assets).

22

7. SPANISH INHERITANCE AND GIFT TAX

TAX RATES

Progressive rates: 7.65% to 34% (for amounts exceeding 797,555.08 euros).

Multiplying factors apply that range from 1 to 1,5.

Exemptions or lower taxation in some regions: gifts and mortis causa transfers to

descendants, spouse, parents.

The tax liability is adjusted by reference to the recipients net wealth before receiving

the inheritance and the familiar relationship with the deceased or donor. This may

increase the effective tax burden of the taxpayer up to 81.6% (worst-case scenario).

23

CIVIL LAW ASPECTS

Spanish Law is applicable when the deceased has Spanish nationality (if

nationality undetermined, the Law of the habitual residence is applicable).

Two main kinds of succession:

Testamentary succession: disposal upon death by will.

Intestacy.

General principle of non freedom of testamentary disposition (forced heir ship).

Testamentary executors / Heirs of confidence: institutions whereby a person or a

group of persons (board) are appointed to manage the deceased estate and to

subsequently appoint an inheritor.

24

7. SPANISH INHERITANCE AND GIFT TAX

INTESTACY

In accordance to Spanish Civil Law in case of an intestate succession the following

familiar members would be heirs:

1. Children descendants

2. Parents

3. Spouse

4. Collaterals

Spouse is entitled to receive an usufruct ranging from 1/3, 1/2 or 2/3 of the

assets (depending on (i) the regional laws applicable and (ii) the existence of

other inheritors or not).

25

7. SPANISH INHERITANCE AND GIFT TAX

FORCED HEIRSHIP

General principle: no freedom of testamentary disposition.

Children are entitled to receive a portion of the deceased’s assets (excluding life

insurances) which are as follows:

General rule 2/3

Catalonia 1/4

Basque Country 4/5

Navarre 0

Aragon 1/2

Balearic Islands 1/3-1/2

Spouse usufruct/life interest.

26

7. SPANISH INHERITANCE AND GIFT TAX

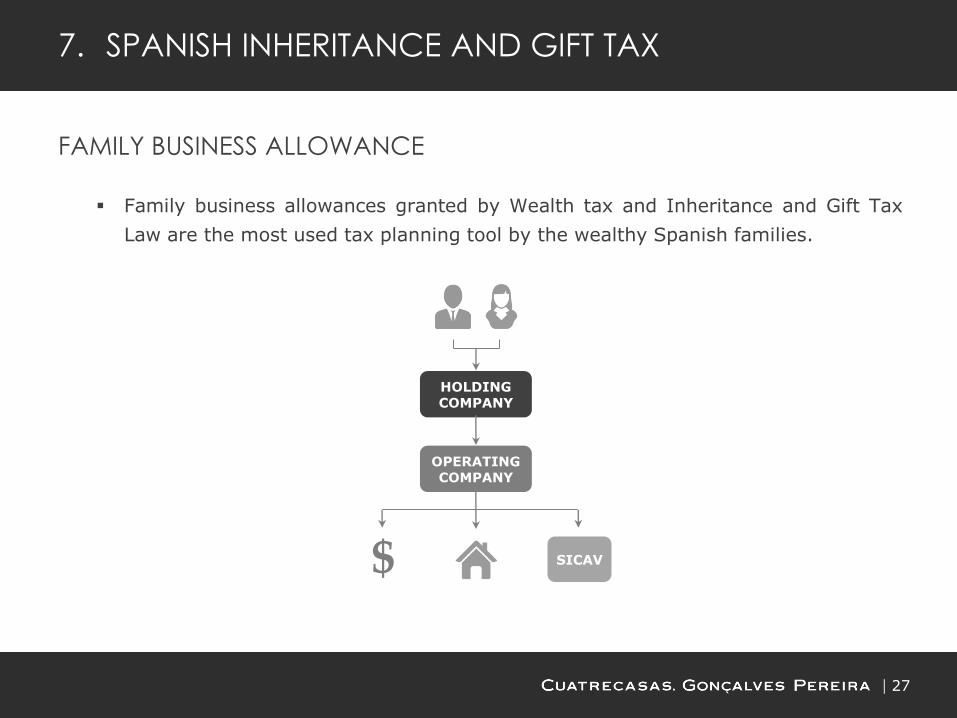

FAMILY BUSINESS ALLOWANCE

Family business allowances granted by Wealth tax and Inheritance and Gift Tax

Law are the most used tax planning tool by the wealthy Spanish families.

HOLDING COMPANY

OPERATING COMPANY

SICAV $

27

7. SPANISH INHERITANCE AND GIFT TAX

FAMILY BUSINESS ALLOWANCE

95% allowance in the assessable base for family businesses (or shares in a

company) provided the following requirements are met.

Inheritance tax:

A relevant business must be effectively carried out.

The deceased must have held more than 5% of the capital of the relevant

entity (or 20% jointly with family members).

More than 50% of the business, professional or dependent employment

income of any of the family members must derive from the management

activities in the company.

Both cases, the family business or the shares or participations must be held

by the heir or legatee during the 10-year period following the death, unless

the recipient dies within the same period.

In this case, a step up in basis is achieved.

28

7. SPANISH INHERITANCE AND GIFT TAX

FAMILY BUSINESS ALLOWANCE

Gift tax (in addition to the prior requirements): The donor must be 65 or older.

If the donor has been acting as director of the company, the donor must leave

the company and cease to receive a remuneration.

The donee must continue the business or hold the participations during the

10-year period.

No step up in basis would be achieved.

Wealth tax

If the mentioned requirements apply, the relief is of 100%.

29

7. SPANISH INHERITANCE AND GIFT TAX

8. TRUSTS

TAXATION OF TRUSTS IN SPAIN

Trusts are civil law institutions not recognized by the Spanish Law.

The Spanish legislation does not provide for any tax treatment for trusts incorporated

abroad.

Tax treatment of foreign trusts is based on legal doctrine and few tax rulings.

Complex and unclear tax treatment.

Trusts holding assets located in Spain are disregarded from a Spanish tax law

perspective.

30

8. TRUSTS

CIVIL LAW COMMENTS ON TRUSTS

The Spanish legislation does recognize the existence of foreign institution validly

created (article 11.1 Civil Code).

Supreme Court of 30 of April 2008 (SS 1832/2001): the Supreme Court does

not recognize a trust but the reason was that it was not proven that the trust

had been validly incorporated.

Limitation: public order (article 12.3 Civil Code).

Private Foundations are prohibited by the Spanish Constitution. (article 34).

Resolution from the Registry and Notaries of 24 of January 2008. Denial of

the possibility that a foundation registers a Spanish real estate property in the

Spanish Registry.

31

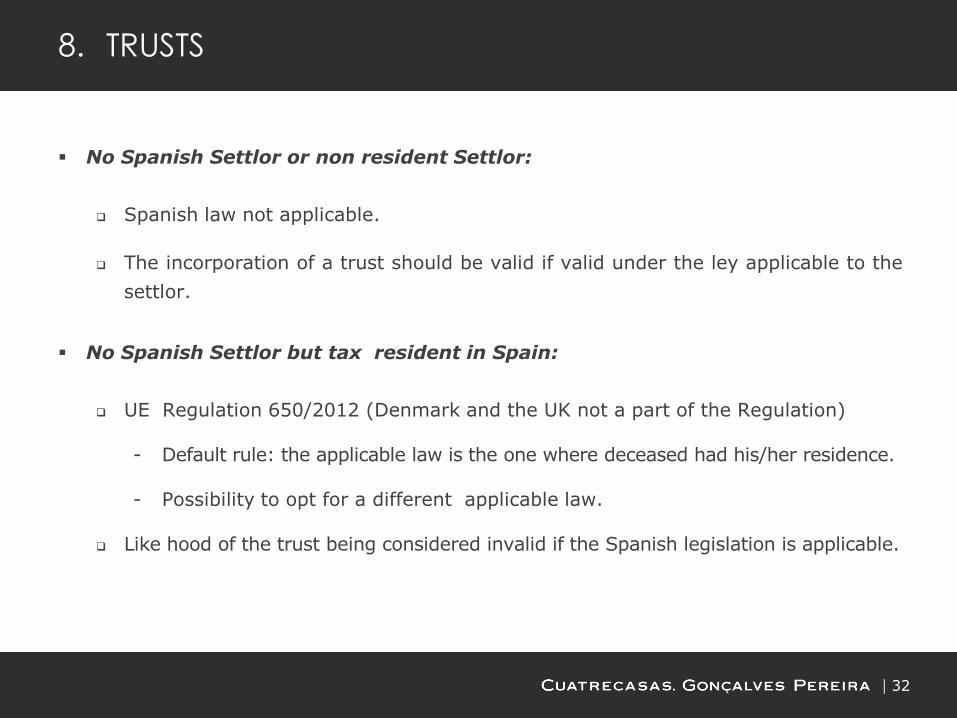

8. TRUSTS

No Spanish Settlor or non resident Settlor:

Spanish law not applicable.

The incorporation of a trust should be valid if valid under the ley applicable to the

settlor.

No Spanish Settlor but tax resident in Spain:

UE Regulation 650/2012 (Denmark and the UK not a part of the Regulation) - Default rule: the applicable law is the one where deceased had his/her residence.

- Possibility to opt for a different applicable law.

Like hood of the trust being considered invalid if the Spanish legislation is applicable.

32

8. TRUSTS

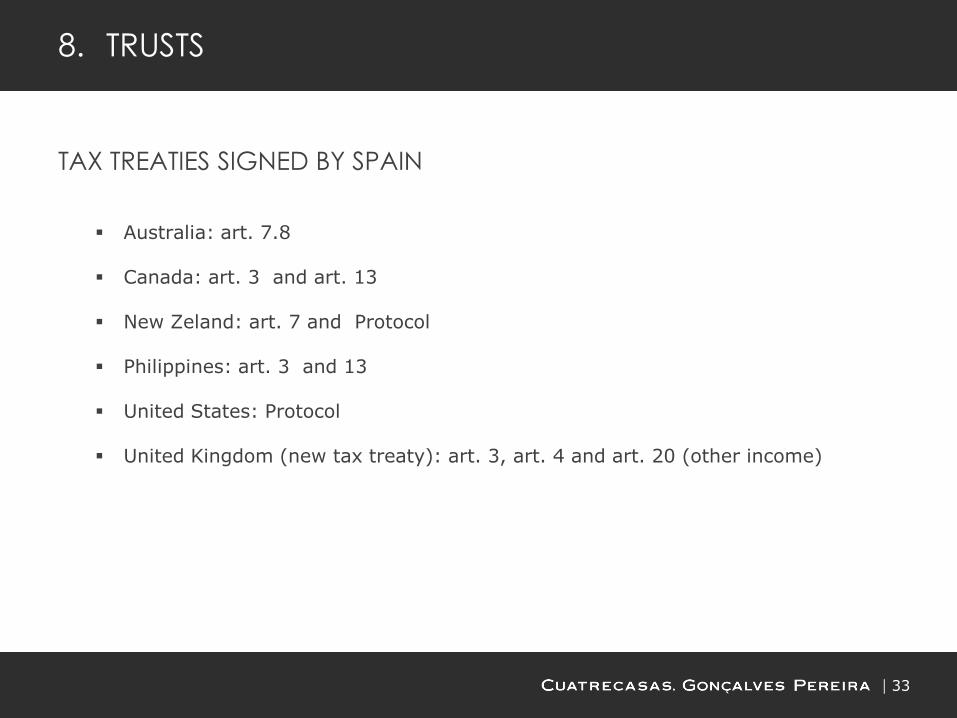

TAX TREATIES SIGNED BY SPAIN

Australia: art. 7.8

Canada: art. 3 and art. 13

New Zeland: art. 7 and Protocol

Philippines: art. 3 and 13

United States: Protocol

United Kingdom (new tax treaty): art. 3, art. 4 and art. 20 (other income)

33

8. TRUSTS

TAXATION OF TRUSTS IN SPAIN (TAX AUTHORITIES RESOLUTIONS)

The Spanish legislation does not provide for any tax treatment for trusts

incorporated abroad.

Tax treatment of foreign trusts is based on legal doctrine and few tax rulings.

Complex and unclear tax treatment.

Trusts holding assets located in Spain are disregarded from a Spanish tax law

perspective.

34

8. TRUSTS

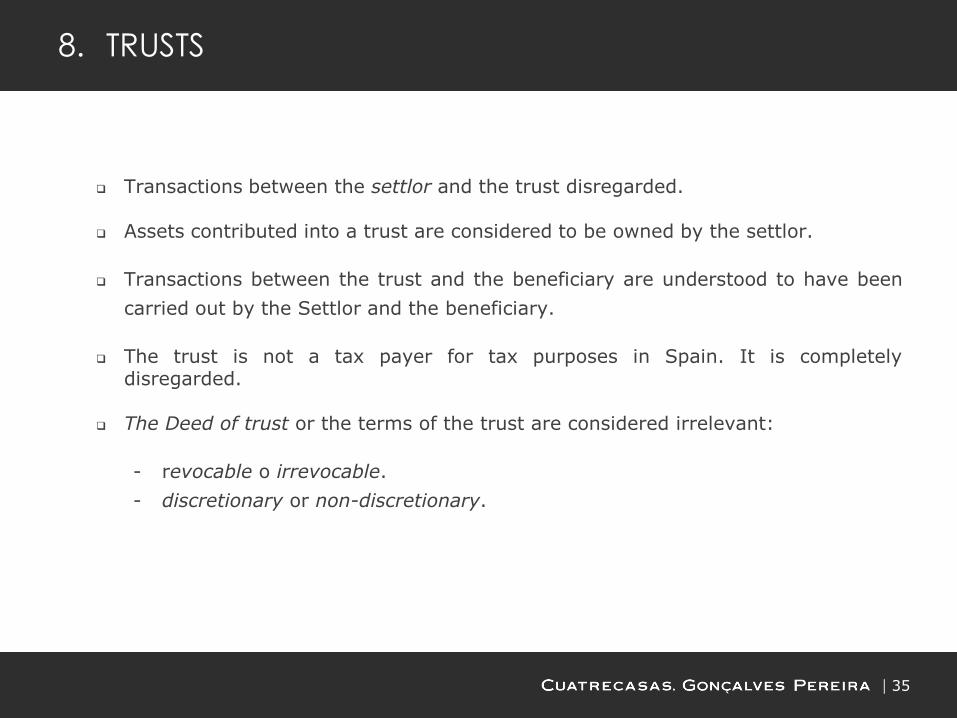

Transactions between the settlor and the trust disregarded. Assets contributed into a trust are considered to be owned by the settlor.

Transactions between the trust and the beneficiary are understood to have been

carried out by the Settlor and the beneficiary.

The trust is not a tax payer for tax purposes in Spain. It is completely

disregarded.

The Deed of trust or the terms of the trust are considered irrelevant:

- revocable o irrevocable.

- discretionary or non-discretionary.

35

8. TRUSTS

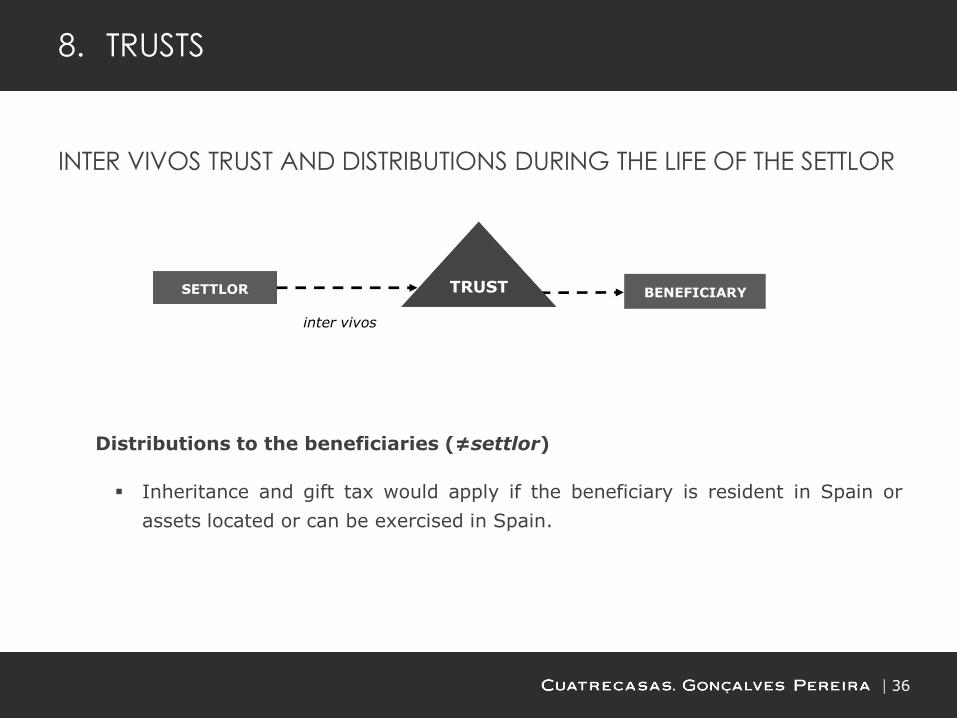

INTER VIVOS TRUST AND DISTRIBUTIONS DURING THE LIFE OF THE SETTLOR

Distributions to the beneficiaries (≠settlor)

Inheritance and gift tax would apply if the beneficiary is resident in Spain or

assets located or can be exercised in Spain.

SETTLOR

inter vivos

BENEFICIARY TRUST

36

8. TRUSTS

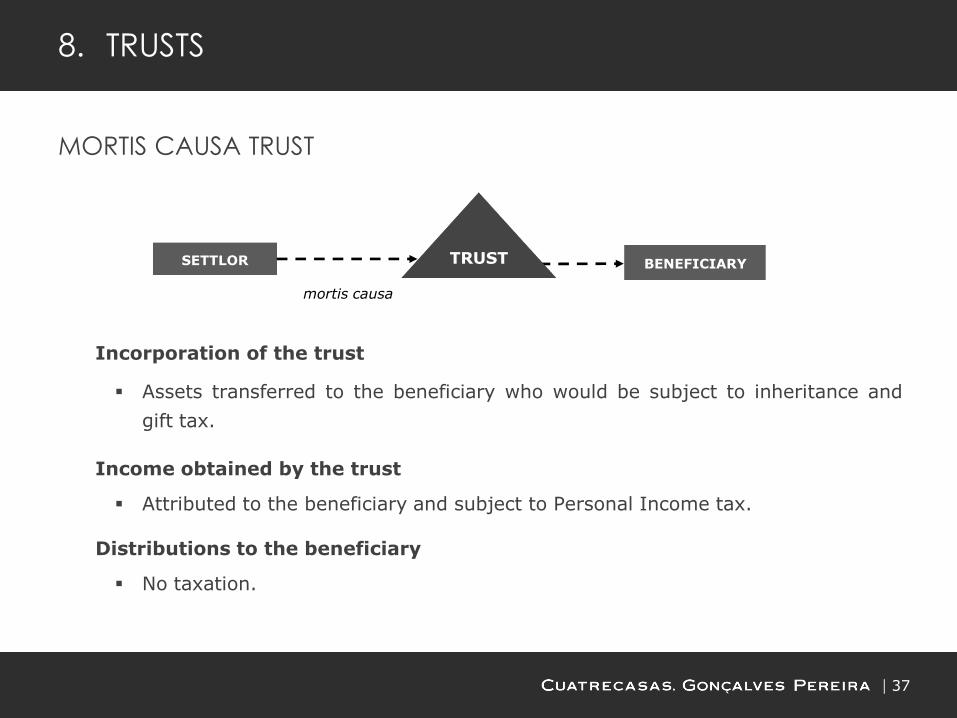

MORTIS CAUSA TRUST

Incorporation of the trust

Assets transferred to the beneficiary who would be subject to inheritance and

gift tax.

Income obtained by the trust

Attributed to the beneficiary and subject to Personal Income tax. Distributions to the beneficiary

No taxation.

SETTLOR

mortis causa

BENEFICIARY TRUST

37

8. TRUSTS

SOME CRITICS

Settlor, subject to personal income tax and wealth tax on assets which may have

been contributed into an irrevocable trust.

Beneficiary: anticipation of taxation since inheritance and gift tax is due even if

the beneficiaries right is contingent.

Simplistic approach of the Spanish tax authorities.

38

9. NEW DISCLOSURE OBLIGATIONS: FORM 720

39

Disclosure obligation of assets abroad (basically, real estate, bank accounts,

financial products, life insurances) with a value above 50.000 Euros per category

of assets.

Annual obligation to file Form 720 (30 March).

Penalties between 1.000 and 10.000 Euros per category of assets may apply.

No statute of limitations if form 720 not filed (unless it could be proved that

income obtained when the tax payer was not resident in Spain or income obtained

paid taxes in Spain). Does it apply to assets inherited?

Obligation to inform the title holder/owner but also beneficiaries and

signatories/trustees if tax resident in Spain.

The STEP Cross-Border Estates Group (C-BEG) was founded in 2004 at the instigation of Richard Frimston of Russell-Cooke LLP. Its area of reference is the domain of estate planning and the administration of estates/successions across national borders. It focuses on reconciling divergent inheritance rules between

civil code jurisdictions, between a civil code approach and a common law approach and between such systems and others such as Shari'a.

This Special Interest Group has to date focused on providing seminars on both

tax and 'civil' topics surrounding such conflicts of law issues, touching on marriage, death, divorce and property law questions. C-BEG continues to follow the Brussels legislation process and the passage of the proposed Brussels III and

Brussels IV Regulations. Visit the Cross-Border Estates Special Interest Group web-pages: www.step.org/cross-border-estates www.step.org/SIGs Join the LinkedIn group: Cross Border Estates Planning Special Interest Group www.linkedin.com/groups/Cross-Border-Estates-Planning-Special-4039028 Become a Member: Membership of STEP’s Special Interest Groups is open to STEP members and non-members alike and there is currently no fee to join. If you wish to become a member of the Cross-Border Estates group and receive updates about their news, events and activities, please visit www.step.org/SIGs. Alternatively you can complete a joining form at the today’s briefing registration desk.

Cross-Border Estates Special Interest Group

Society of Trust and Estate Practitioners (STEP) Artillery House (South)

11-19 Artillery Row London, SW1P 1RT

United Kingdom

Tel: +44 (0)20 7340 0537 Fax: +44 (0)20 7340 0501

Email: [email protected]