briefing - monetary authority of singapore (mas)/media/resource/publications/macro... · c contents...

TRANSCRIPT

briefing27 October 2017

C

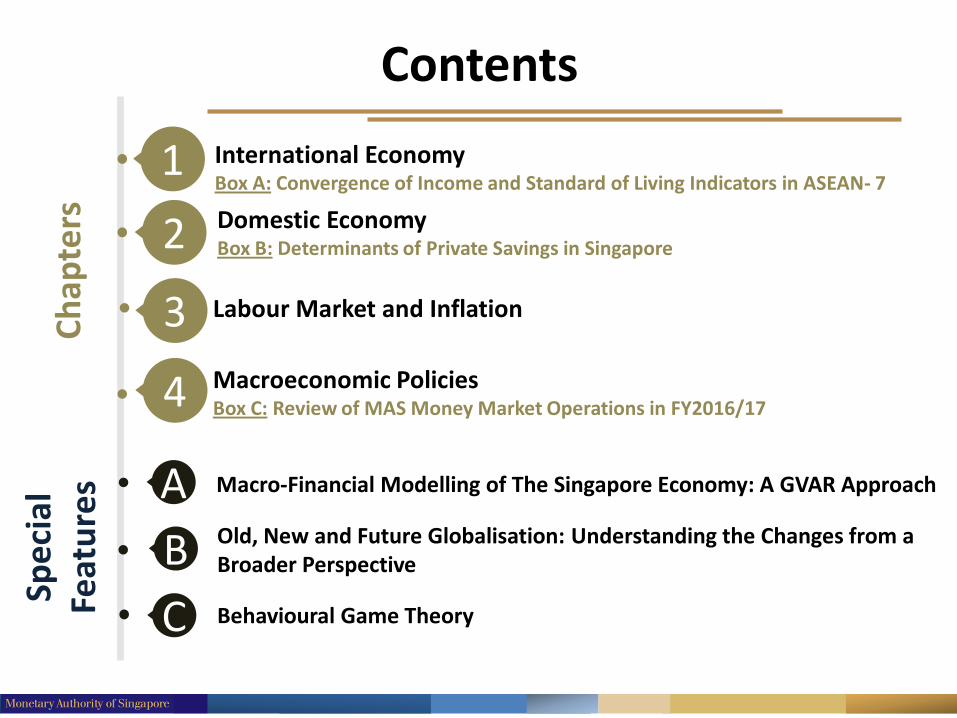

Contents

Domestic EconomyBox B: Determinants of Private Savings in Singapore

Labour Market and Inflation

International EconomyBox A: Convergence of Income and Standard of Living Indicators in ASEAN- 7

Macroeconomic PoliciesBox C: Review of MAS Money Market Operations in FY2016/17

B

Ch

apte

rs

1

2

Macro-Financial Modelling of The Singapore Economy: A GVAR ApproachAOld, New and Future Globalisation: Understanding the Changes from a Broader Perspective

Behavioural Game Theory

Spe

cial

Feat

ure

s

3

4

RESTRICTED

International Economy

Global Activity Gathers Pace Amid Low Inflation

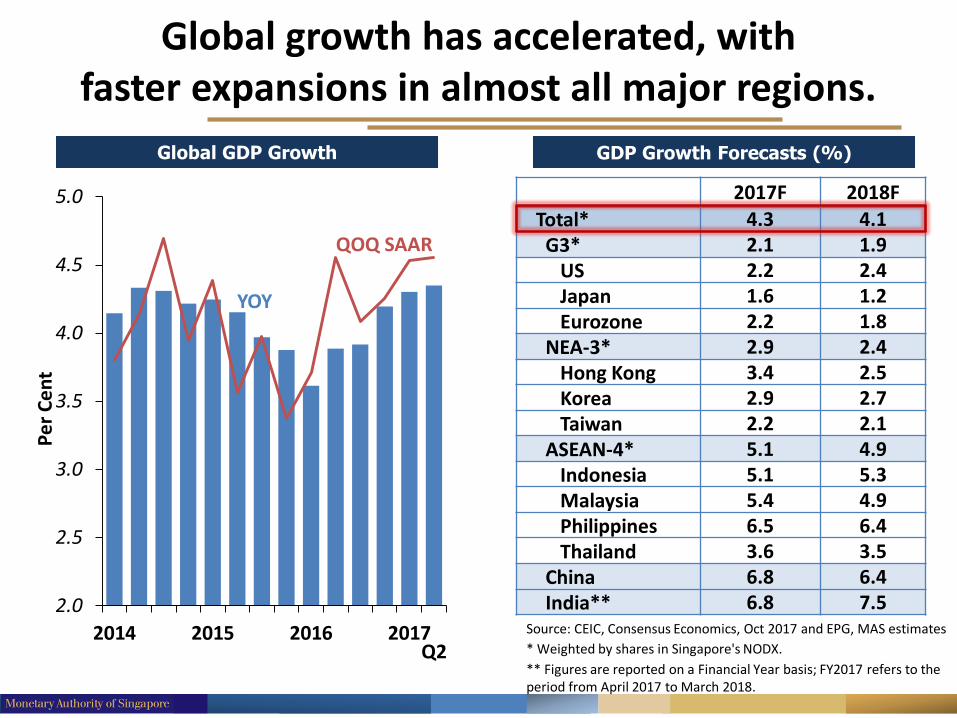

Global GDP Growth

2017F 2018F

Total* 4.3 4.1G3* 2.1 1.9

US 2.2 2.4Japan 1.6 1.2Eurozone 2.2 1.8

NEA-3* 2.9 2.4Hong Kong 3.4 2.5Korea 2.9 2.7Taiwan 2.2 2.1

ASEAN-4* 5.1 4.9Indonesia 5.1 5.3Malaysia 5.4 4.9Philippines 6.5 6.4Thailand 3.6 3.5

China 6.8 6.4India** 6.8 7.5

GDP Growth Forecasts (%)

Global growth has accelerated, with faster expansions in almost all major regions.

Source: CEIC, Consensus Economics, Oct 2017 and EPG, MAS estimates

* Weighted by shares in Singapore's NODX.

** Figures are reported on a Financial Year basis; FY2017 refers to the period from April 2017 to March 2018.

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2014 2015 2016 2017

Pe

r C

en

t

YOY

QOQ SAAR

Q2

2008 2010 2012 2014 2016

-1.5

-1.0

-0.5

0.0

0.5

1.0

% P

oin

t C

on

trib

uti

on

to

YO

Y G

row

th

Changes in Share of Part-timers etc.Changes in Pay of Part-timersChanges in Pay of Full-timersGrowth in Base Pay

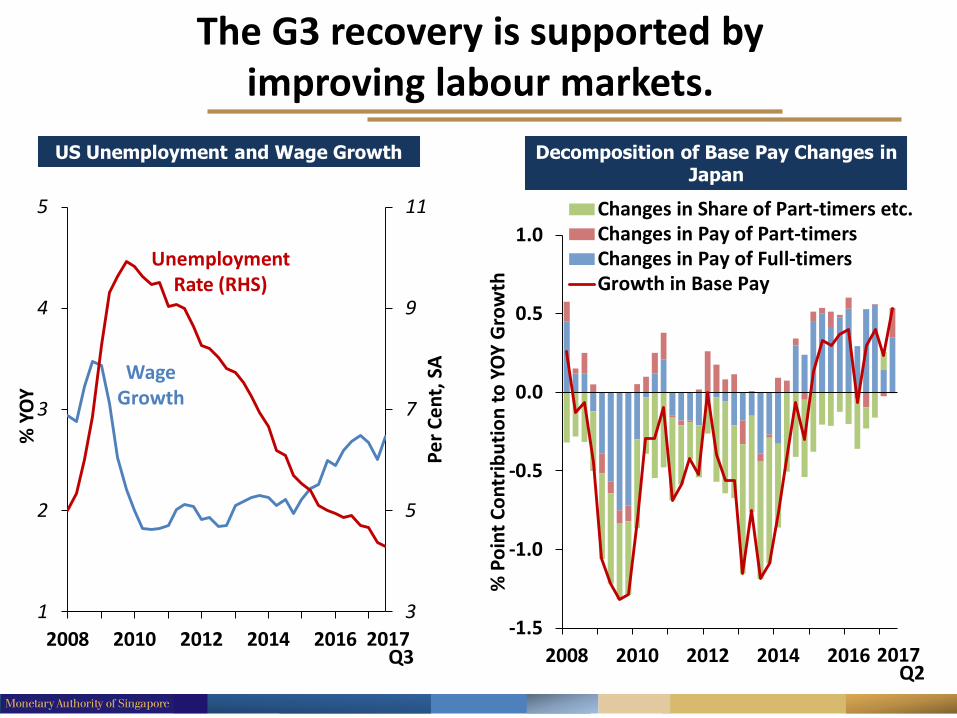

The G3 recovery is supported by improving labour markets.

Decomposition of Base Pay Changes in Japan

US Unemployment and Wage Growth

3

5

7

9

11

1

2

3

4

5

2008 2010 2012 2014 2016

Pe

r C

en

t, S

A

% Y

OY

2017Q3

Wage Growth

UnemploymentRate (RHS)

2017Q2

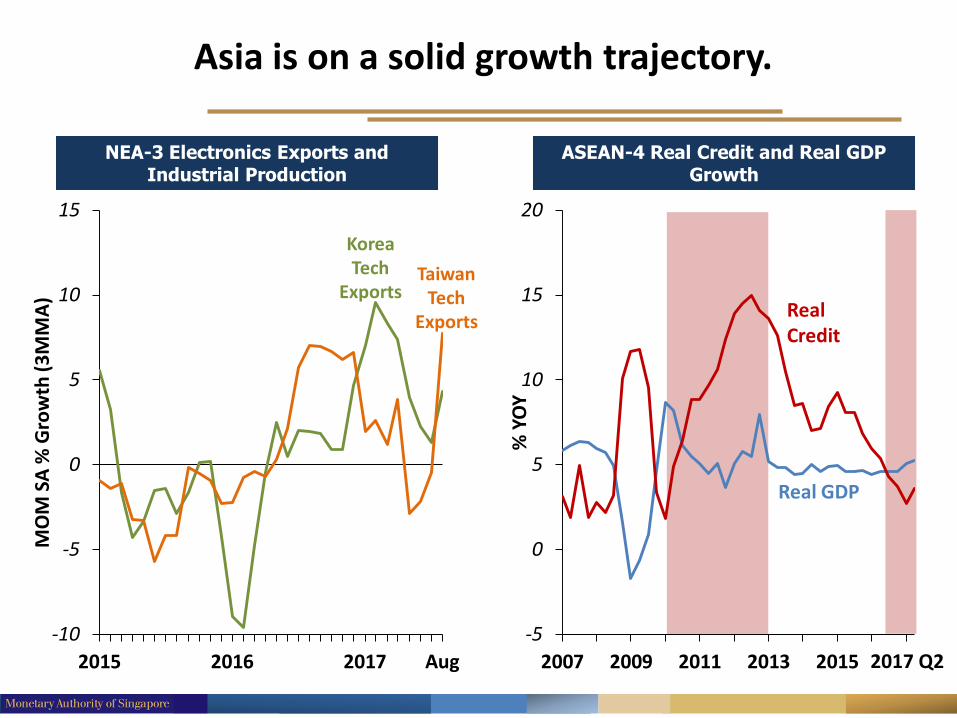

Asia is on a solid growth trajectory.

ASEAN-4 Real Credit and Real GDP Growth

NEA-3 Electronics Exports and Industrial Production

2015 2016 2017 Aug

-10

-5

0

5

10

15

MO

M S

A %

Gro

wth

(3

MM

A)

-5

0

5

10

15

20

2007 2009 2011 2013 2015 2017

% Y

OY

2017 Q2

KoreaTech

ExportsTaiwan

Tech Exports

Real Credit

Real GDP

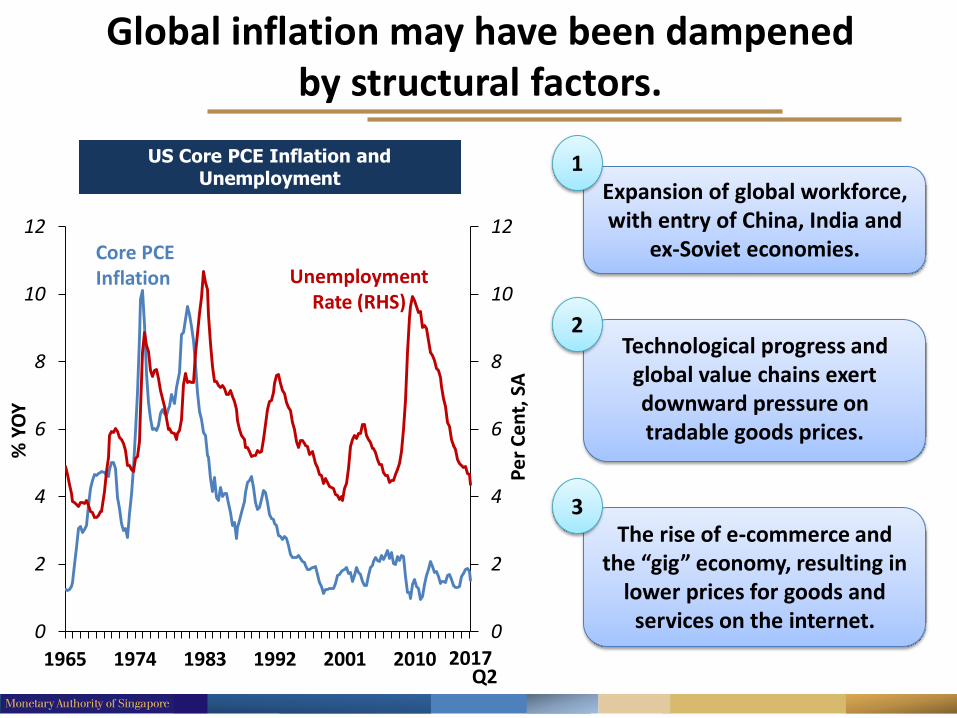

Global inflation may have been dampened by structural factors.

US Core PCE Inflation and Unemployment

0

2

4

6

8

10

12

0

2

4

6

8

10

12

1965 1974 1983 1992 2001 2010

Pe

r C

en

t, S

A

% Y

OY

2017Q2

Core PCE Inflation Unemployment

Rate (RHS)

Expansion of global workforce, with entry of China, India and

ex-Soviet economies.

1

Technological progress and global value chains exert downward pressure on tradable goods prices.

2

The rise of e-commerce and the “gig” economy, resulting in

lower prices for goods and services on the internet.

3

RESTRICTED

Domestic Economy

Some Upsides to Growth

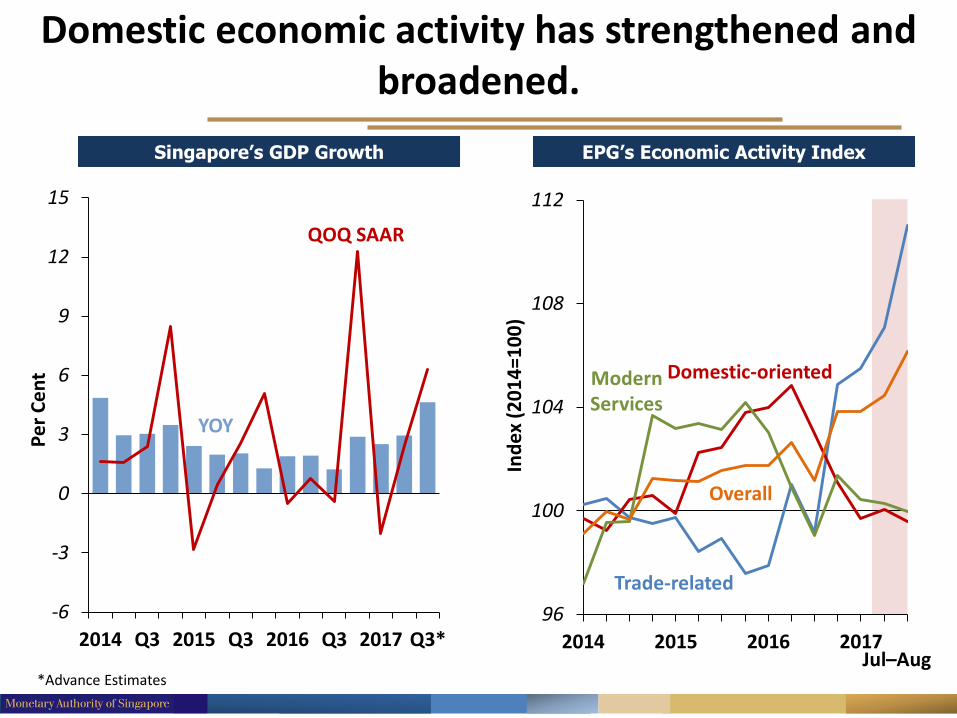

Domestic economic activity has strengthened and broadened.

2014 Q3 2015 Q3 2016 Q3 2017 Q3*

-6

-3

0

3

6

9

12

15

Pe

r C

en

t

Singapore’s GDP Growth

YOY

QOQ SAAR

*Advance Estimates

EPG’s Economic Activity Index

2014 2015 2016 2017

96

100

104

108

112

Ind

ex (

20

14

=10

0)

Jul–Aug

Trade-related

Domestic-oriented

Overall

ModernServices

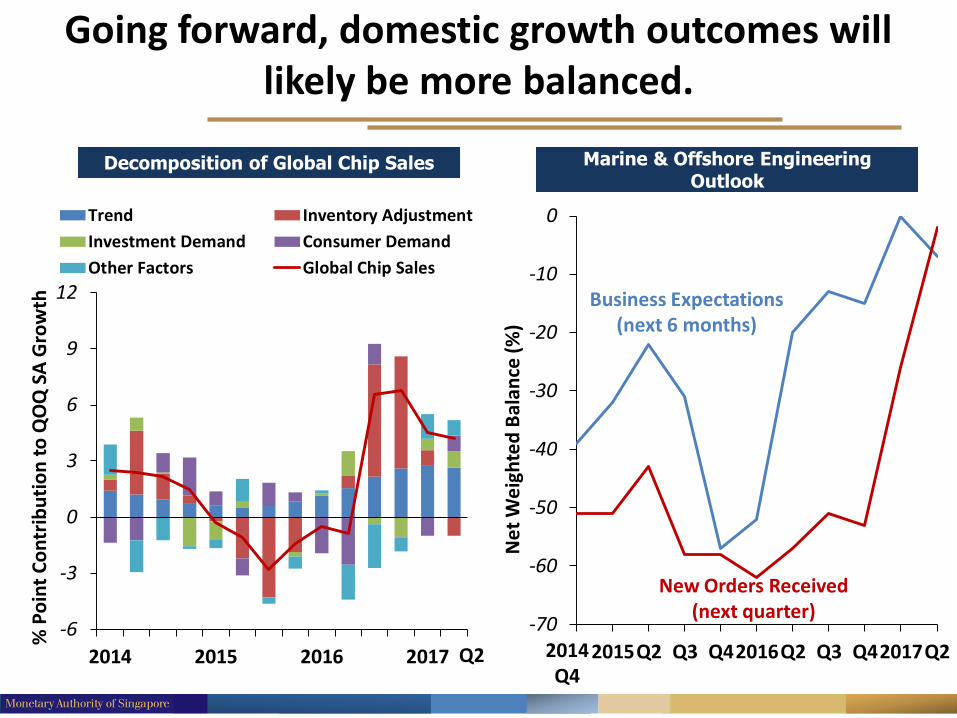

Going forward, domestic growth outcomes will likely be more balanced.

Decomposition of Global Chip Sales

2014 2015 2016 2017

-6

-3

0

3

6

9

12

% P

oin

t C

on

trib

uti

on

to

QO

Q S

A G

row

th

Trend Inventory Adjustment

Investment Demand Consumer Demand

Other Factors Global Chip Sales

Q2

-70

-60

-50

-40

-30

-20

-10

0

2015Q2 Q3 Q42016Q2 Q3 Q42017Q2

Ne

t W

eig

hte

d B

alan

ce (

%)

Business Expectations(next 6 months)

2014Q4

Marine & Offshore Engineering Outlook

New Orders Received(next quarter)

RESTRICTED

Labour Market and Inflation

Inflation is Contained and Stable

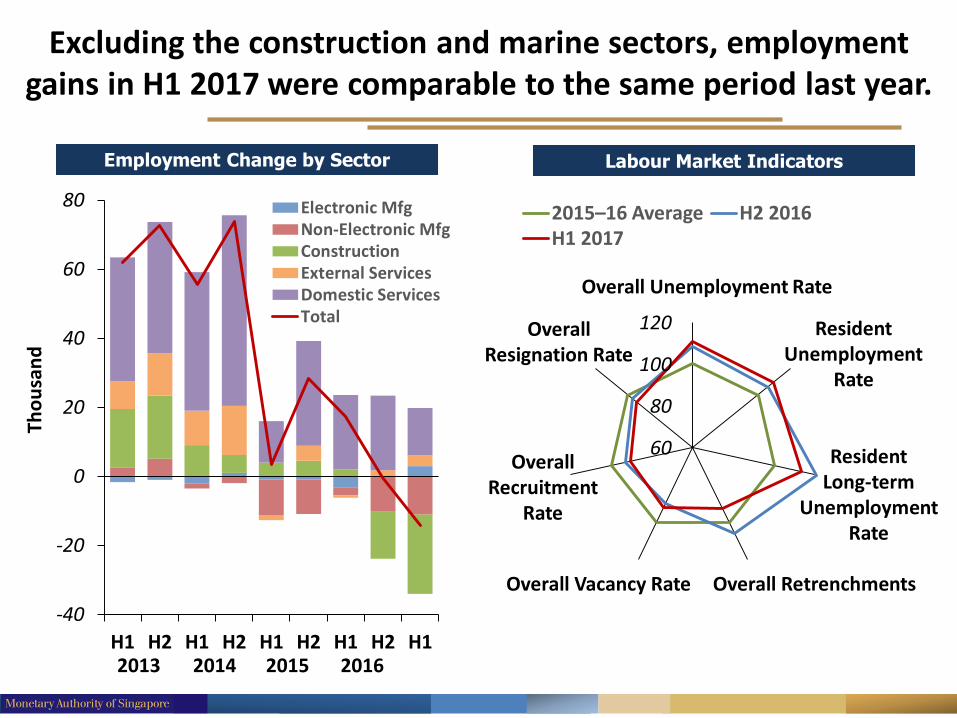

Excluding the construction and marine sectors, employment gains in H1 2017 were comparable to the same period last year.

Employment Change by Sector

H1 H2 H1 H2 H1 H2 H1 H2 H1

-40

-20

0

20

40

60

80

Tho

usa

nd

Electronic MfgNon-Electronic MfgConstructionExternal ServicesDomestic ServicesTotal

2013 2014 2015 2016

Labour Market Indicators

60

80

100

120

2015–16 Average H2 2016H1 2017

Overall Retrenchments

Overall Unemployment Rate

Resident Unemployment

Rate

Resident Long-term

Unemployment Rate

Overall Vacancy Rate

Overall Resignation Rate

Overall Recruitment

Rate

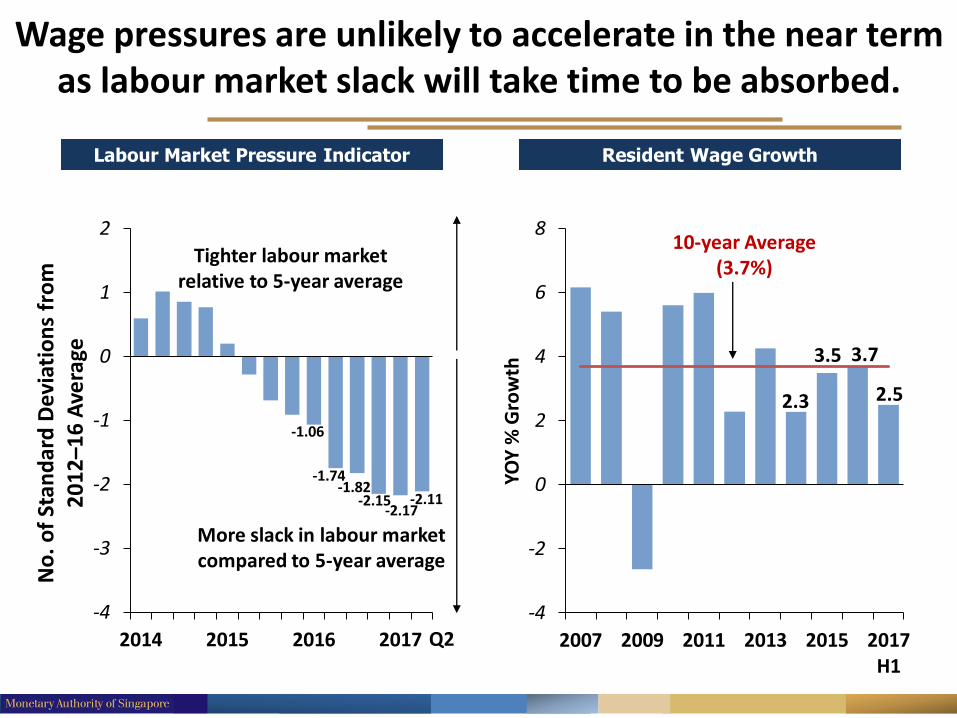

Wage pressures are unlikely to accelerate in the near term as labour market slack will take time to be absorbed.

Resident Wage Growth

2007 2009 2011 2013 2015 2017H1

-4

-2

0

2

4

6

8

YOY

% G

row

th

10-year Average(3.7%)

2.3

3.5 3.7

2.5

Labour Market Pressure Indicator

2014 2015 2016 2017

-4

-3

-2

-1

0

1

2

No

. o

f St

and

ard

De

viat

ion

s fr

om

2

01

2–1

6 A

vera

ge

Tighter labour market relative to 5-year average

More slack in labour market compared to 5-year average

-1.06

-1.74

-2.17-2.11

-1.82-2.15

Q2

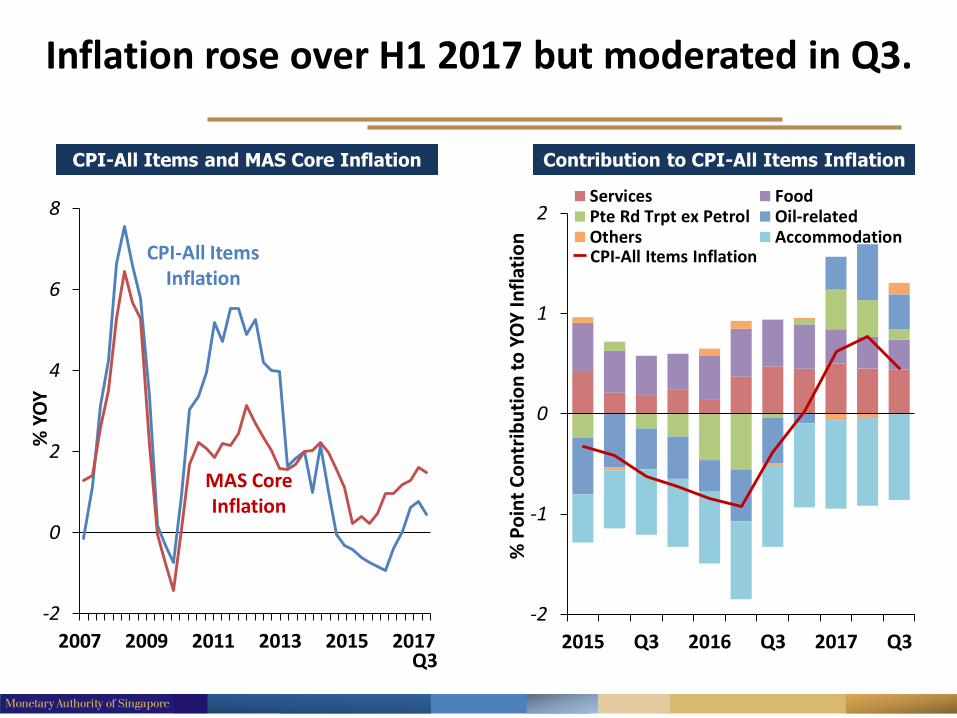

Inflation rose over H1 2017 but moderated in Q3.

Contribution to CPI-All Items Inflation

2015 Q3 2016 Q3 2017 Q3

-2

-1

0

1

2

% P

oin

t C

on

trib

uti

on

to

YO

Y In

flat

ion

Services FoodPte Rd Trpt ex Petrol Oil-relatedOthers AccommodationCPI-All Items Inflation

CPI-All Items and MAS Core Inflation

2007 2009 2011 2013 2015 2017

-2

0

2

4

6

8

% Y

OY

CPI-All Items Inflation

MAS Core Inflation

Q3

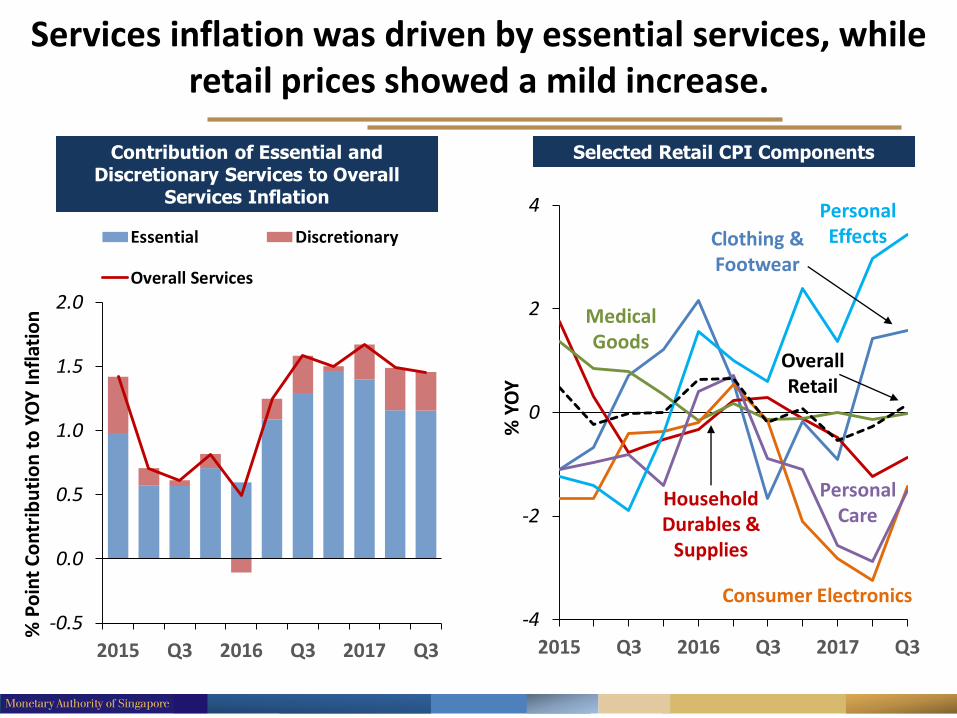

Services inflation was driven by essential services, while retail prices showed a mild increase.

Contribution of Essential and Discretionary Services to Overall

Services Inflation

2015 Q3 2016 Q3 2017 Q3

-0.5

0.0

0.5

1.0

1.5

2.0

Essential Discretionary

Overall Services

% P

oin

t C

on

trib

uti

on

to

YO

Y I

nfl

atio

n

Selected Retail CPI Components

2015 Q3 2016 Q3 2017 Q3

-4

-2

0

2

4

% Y

OY

Clothing & Footwear

Household Durables &

Supplies

Medical Goods

Consumer Electronics

Personal Care

Personal Effects

Overall Retail

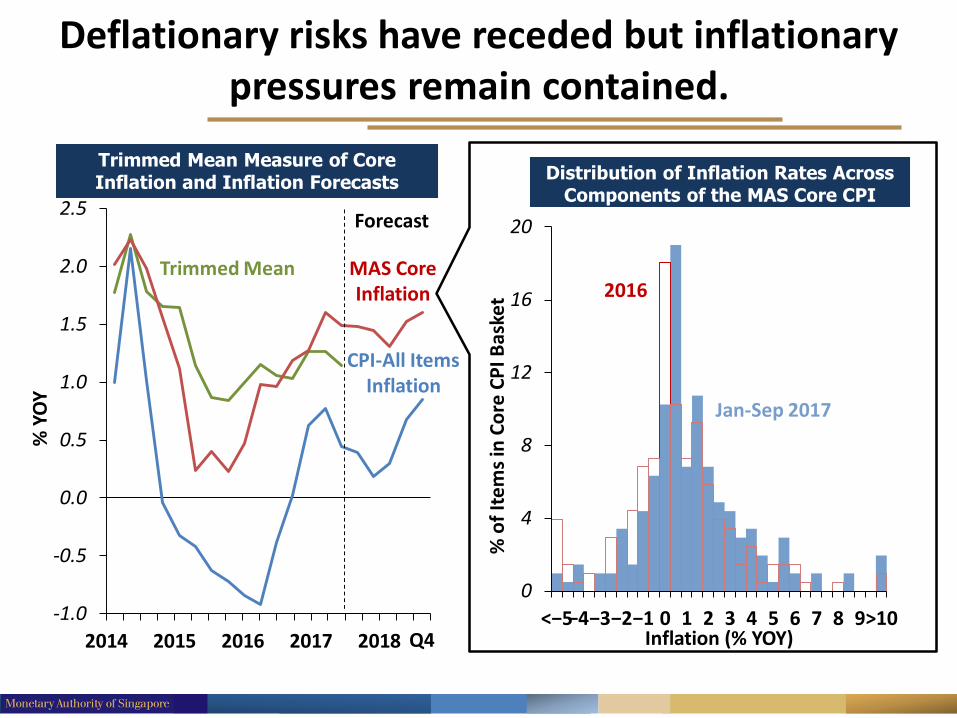

Distribution of Inflation Rates Across Components of the MAS Core CPI

Basket

0

4

8

12

16

20

<−5−4−3−2−1 0 1 2 3 4 5 6 7 8 9>10

% o

f It

em

s in

Co

re C

PI B

aske

t

Inflation (% YOY)

2016

Jan-Sep 2017

Deflationary risks have receded but inflationary pressures remain contained.

2014 2015 2016 2017 2018

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

% Y

OY

CPI-All Items Inflation

MAS Core Inflation

Q4

Trimmed Mean

Trimmed Mean Measure of Core Inflation and Inflation Forecasts

Forecast

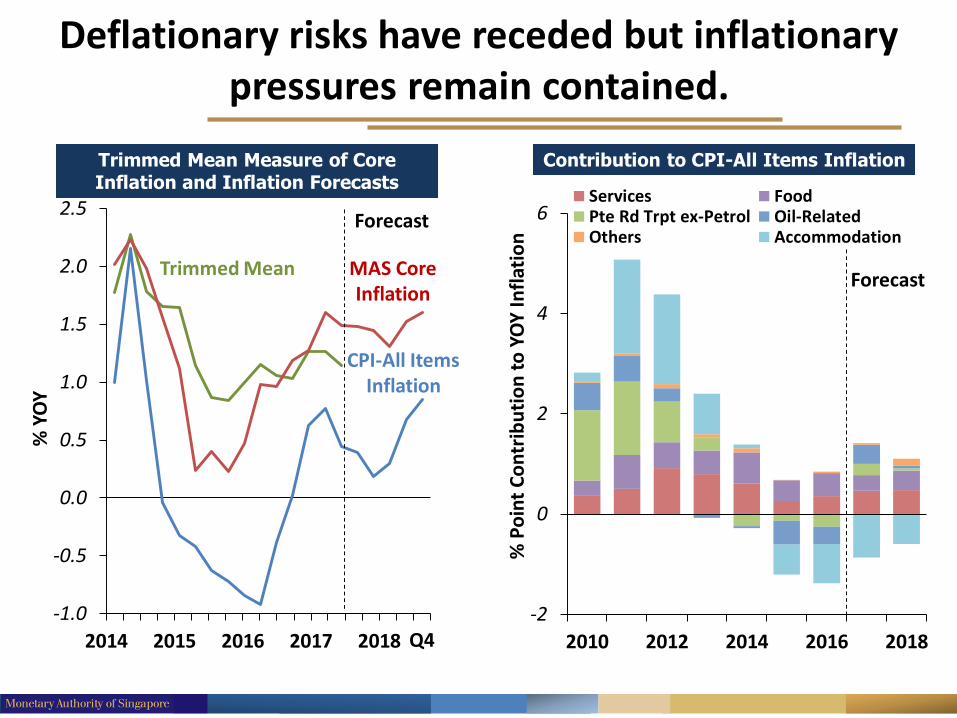

Deflationary risks have receded but inflationary pressures remain contained.

2014 2015 2016 2017 2018

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

% Y

OY

CPI-All Items Inflation

MAS Core Inflation

Q4

Trimmed Mean

Trimmed Mean Measure of Core Inflation and Inflation Forecasts

Forecast

Contribution to CPI-All Items Inflation

2010 2012 2014 2016 2018

-2

0

2

4

6

% P

oin

t C

on

trib

uti

on

to

YO

Y In

flat

ion

Services FoodPte Rd Trpt ex-Petrol Oil-RelatedOthers Accommodation

Forecast

RESTRICTED

Macroeconomic Policy

Maintaining Price Stability As Growth Picks Up

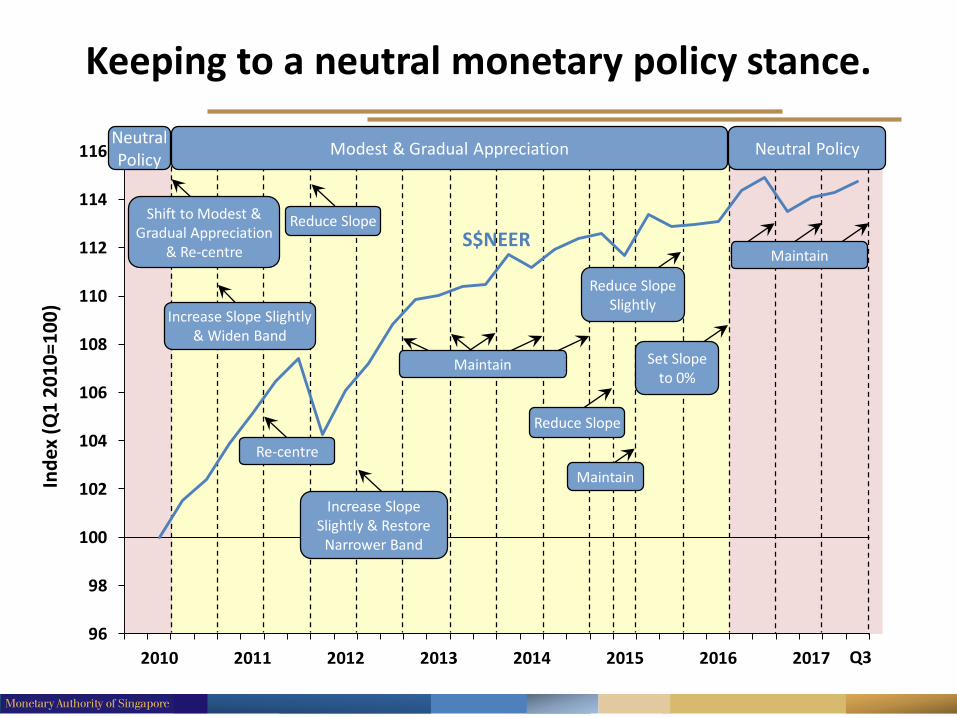

Keeping to a neutral monetary policy stance.

2010 2011 2012 2013 2014 2015 2016 2017

96

98

100

102

104

106

108

110

112

114

116

Ind

ex (

Q1

20

10

=10

0)

Q3

S$NEER

Neutral Policy

Shift to Modest & Gradual Appreciation

& Re-centre

Reduce Slope

Modest & Gradual Appreciation

Reduce Slope Slightly

Neutral Policy

Maintain

Increase Slope Slightly & Widen Band

Re-centre

Increase Slope Slightly & Restore

Narrower Band

Maintain

Reduce Slope

Maintain

Set Slope to 0%

Q&A

27 October 2017