breaking the silence on environmental risk

TRANSCRIPT

Breaking the silence on environmental risk

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES i

The Hong Kong Institute of Chartered Secretaries

(Incorporated in Hong Kong and limited by guarantee)

GOOD GOVERNANCE COMES WITH MEMBERSHIP

The Hong Kong Institute of Chartered Secretaries is an independent professional body with approximately 4,900 members

and 2,600 students. It is dedicated to the promotion of its members’ role in the formulation and effective implementation of

good corporate governance policies in Hong Kong and throughout China as well as the development of the profession of

Chartered Secretary.

The Institute was first established in 1949 as an association of Hong Kong members of the Institute of Chartered Secretaries

and Administrators (ICSA) of London. It became a branch of ICSA in 1990 before gaining local status in 1994.

HKICS issues two sets of post nominals to its Members who qualify locally. One set on behalf of HKICS: FCS for Fellows and

ACS for Associates, and one set on behalf of the international body ICSA: FCIS for Fellows and ACIS for Associates.

The Hong Kong Institute of Chartered Secretaries

3rd Floor

Hong Kong Diamond Exchange Building

8 Duddell Street

Central

Hong Kong

Tel: (852) 2881 6177

Fax: (852) 2881 5050

Email: [email protected]

Website: www.hkics.org.hk

Beijing Representative Office

Room 1710,

U-SPACE Building

Block A

No.8 Guangqumenwai Street

Chaoyang District

Beijing

China 100022

Tel: (8610) 5861 2050

Fax: (8610) 5861 2051

Email: [email protected]

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIESii

There are few who would argue that the state of Hong Kong’s environment is now a source of disquiet for its residents. Theair that we breathe, the water we drink and very earth on which we walk seems to be deteriorating on a daily basis if somereports are to be believed. And so it is timely that The Hong Kong Institute of Chartered Secretaries (Institute) publishes thisresearch paper on Environmental Reporting.

The world of business has not traditionally been held in high regard by environmentalists in terms of the concern it showsfor Mother Nature. This research paper shows that while every company has an impact on the environment regardless ofsector and type, few senior managers and directors have an idea of why Environmental Reporting is necessary or whatfunctions or benefits such reporting can bring. This is despite the fact that 80% of those surveyed as part of the Institute’sresearch into the subject acknowledge that pollution is a serious matter for Hong Kong.

The Institute believes that Environmental Reporting can help stakeholders make informed decisions as to the relationshipthey want with a company. That might be as an investor, customer, supplier, and employee or perhaps even a regulator. Bybeing open on their policies on recycling, waste disposal, travel and so on companies can give a positive message that theycare about the environment. This can be a very attractive position to take in today’s competitive business environment.Environmental Reporting also forces companies to face the reality that they have a real and measurable impact on theenvironment and, hopefully, will also force senior management’s hand on how best to minimise the negative impact andmaximise the positive through creative solutions and risk management - an often overlooked benefit of environmentalreporting.

As President of the Institute I would like to urge all companies to adopt environmentally friendly practices whereverpossible and include Environmental Reporting in your statutory reports. We also urge the government to take a similarstance in encouraging particularly the listed companies to take a proactive approach to Environmental Reporting. Thecorporation is an ‘artificial person’ created by law and so bears a social responsibility to the environment no different from anatural person. If the business world does not take the initiative to pay attention to environmental issues and voluntarilyinclude certain Environmental Reports in their statutory reports such as Annual Reports, in future they might find themselvesin a situation where the government forces their hand by making the reporting of such matters mandatory.

The environment matters. The business world should take a lead and prove that it cares. A first good step would be theinclusion of an Environmental Report in the next tranche of Annual Reports. We are at a critical stage in terms of decidingwhat to do about the high levels of pollution in Hong Kong, consequently this timely research paper makes for interestingand sometimes worrying reading.

All research reports are a collaborative effort but ultimately there is one person who leads. In this case it was Loretta Chanthe Institute’s Director, Technical and Research. On behalf of Council and indeed all members I offer my sincere thanks toLoretta and the rest of the team at the secretariat which included part time research assistants Mandy Lee, Iris Fung andElton Ma.

I would also like to thank fellow Council member Dr Brian Lo who, together with Professor Vanessa Stott of The Hong KongPolytechnic University, School of Accounting and Finance, took the role of outside consultants. Your contributions wereinvaluable. Special thanks should go to Kieran Colvert, Editor of CSJ, the Institute’s official journal, who stepped in at thelast moment to add a final polish and edit to the research paper. To all those who helped but are not mentioned this is dueto space constraints, your contributions are appreciated and valued and on behalf of the Institute I thank you all.

Richard LeungPresident,HKICS 2005-6

F O R E W O R D

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES iii

Concerns have been rising recently over the quality of our air. The environment we live in, pollution and the depletion of

the world’s natural resources not only affect us but also the generations to come. Needless to say, they also have an impact

on our attractiveness as an international financial centre.

At Hong Kong Exchanges and Clearing (HKEx), we recognise our duty to minimise the environmental impact arising from

our operations and seek opportunities to reduce and recycle the resources we consume. Our environmental management

procedures include the eIPO system, where applications for shares in an IPO can be made online, recycling paper waste

and IT equipment, and using energy saving office equipment. We also hope to work to reduce the size of prospectuses and

hence decrease the use of paper. This follows our earlier efforts to encourage listed companies and their shareholders to opt

for electronic copies of company reports.

We are committed to environmental improvement and pollution prevention and call on companies to do the same. Indeed,

this Environmental Reporting Research Report is a timely reminder to us all of our responsibility to sustainable development

and of the increasing relevance of social, environmental and governance factors in a firm’s financial performance.

This report contains valuable information from our listed companies and their views on environmental issues and whether

environmental reporting should be made mandatory. I believe the report contributes meaningfully to informed discussion

and debate about our environment and the role companies should play, and I commend it to you. Greater awareness is the

first step on any journey of improvement.

I thank The Hong Kong Institute of Chartered Secretaries for their work in preparing the report and also for their

recommendations on the way forward for us all to consider. HKEx believes there is value for companies to strive to enhance

their social accountability and improve their corporate governance practices, and we will continue to carefully monitor

market views on this and other matters.

Ronald Arculli

Chairman

Hong Kong Exchanges and Clearing Limited

P R E F A C E

1. Introduction 1The HKICS view 2

The survey 3Summary of the findings 3

Summary of the recommendations 4

2. Background 4What is environmental reporting? 4

What are the functions and benefits of environmental reporting? 5Recent developments in other jurisdictions 14

Should environmental reporting be made mandatory in Hong Kong? 18How to get started? 19

What distinguishes a good environmental report from a mediocre one? 20

3. Survey Findings 23Response rate and profile of the respondents 23

Key findings 24General opinions of the respondents 34

Respondents’ comments on environmental reporting issues 40Additional observations 42

4. The Way Forward for Hong Kong — Recommendations 43Regulatory incentives 43

Market Indices 44

5. Conclusions 46Annex 1 Questionnaire 47

Annex 2 Extracts of the Interviews 53Annex 3 Drivers for Change 62

Bibliography 66

Acknowledgements 68

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 01

ENVIRONMENTAL REPORTING1. INTRODUCTION

In April and May 2006, The Hong Kong Institute of Chartered Secretaries (“HKICS”) carried out a survey of all 961

companies listed on the Main Board of The Stock Exchange of Hong Kong Limited (“Exchange”) to find out the extent

of environmental reporting (“ER”) in Hong Kong. There has been an increasing trend overseas for mandatory reporting

on companies’ environmental risks and impacts (see “Recent developments in other jurisdictions” below). Since

1999 it has been mandatory for all government bureaux and departments and government-owned organisations in

Hong Kong to publish yearly environmental reports. The government hopes that this mandatory adoption of ER in the

public sector will encourage the private sector to follow suit. However, over the past six years, though the number of

corporations engaging in ER is growing, ER is still at a nascent stage in Hong Kong when compared with countries

such the UK, Australia and Japan.

This HKICS survey confirms the view that very few Hong Kong companies are engaged in ER. The survey comprised

two parts. The primary data came from a questionnaire sent in May this year to all 961 Main Board listed companies

soliciting information on, among other things, whether they are currently reporting on their environmental risks and

impacts, and, if not, whether they have the intention to do so in the coming three years. This questionnaire-based

survey found that 16 out of the 48 respondent companies (or 33.3%) are engaged in ER. This does not, of course,

reflect the actual percentage of Main Board listed companies engaged in ER since only 5% of the companies

approached responded to the questionnaire. This disappointing response rate per se is evidence of the lack of interest

in, and knowledge of, ER. A survey conducted by the Hong Kong Environmental Protection Department (“EPD”) in

2005 found that 10% of Main Board listed companies were engaged in ER in some form.

Supplementing the data from the questionnaire-based survey, publicly available information (such as annual reports,

sustainability reports, corporate social responsibility reports and corporate websites) of the 201 Main Board listed

companies which were the constituent stocks of the Hang Seng Composite Index (“HSCI”) were analysed in April this

year. This HSCI survey found that 10 of the 201 companies surveyed had published standalone environmental

reports, or corporate social responsibility (“CSR”) or sustainability reports of which environmental reports form a

part, while 42 had disclosed to a certain extent their environmental performance through other channels, such as

their annual reports or corporate websites. In other words, it showed that about 26% of HSCI constituent stocks were

engaged in ER.

ER is clearly a low priority for most listed companies in Hong Kong. The questionnaire also asked questions probing

attitudes to ER among respondents, and the dominant attitude seems to be that ER has little to do with their business.

This perception is probably rather deep-rooted since about 87.5% of those surveyed companies which are not

currently engaging in ER indicated that they have no plan to do so in the coming three years. This shows that they do

not believe that they can gain much out of this exercise. It is unlikely, therefore, that there will be a sharp increase in

the uptake of ER by listed companies in Hong Kong in the next few years.

The companies engaged in ER tend to have relatively large market capitalisations, or have a potentially great

environmental impact, such as power and aviation companies. Many respondents sought to explain the absence of

environmental data in their reports by suggesting that since their businesses have nothing to do with the environment

ER is irrelevant to them. Such an opinion reflects a lack of understanding of the fact that every company, by its

operations, services or products, has an impact on the environment.

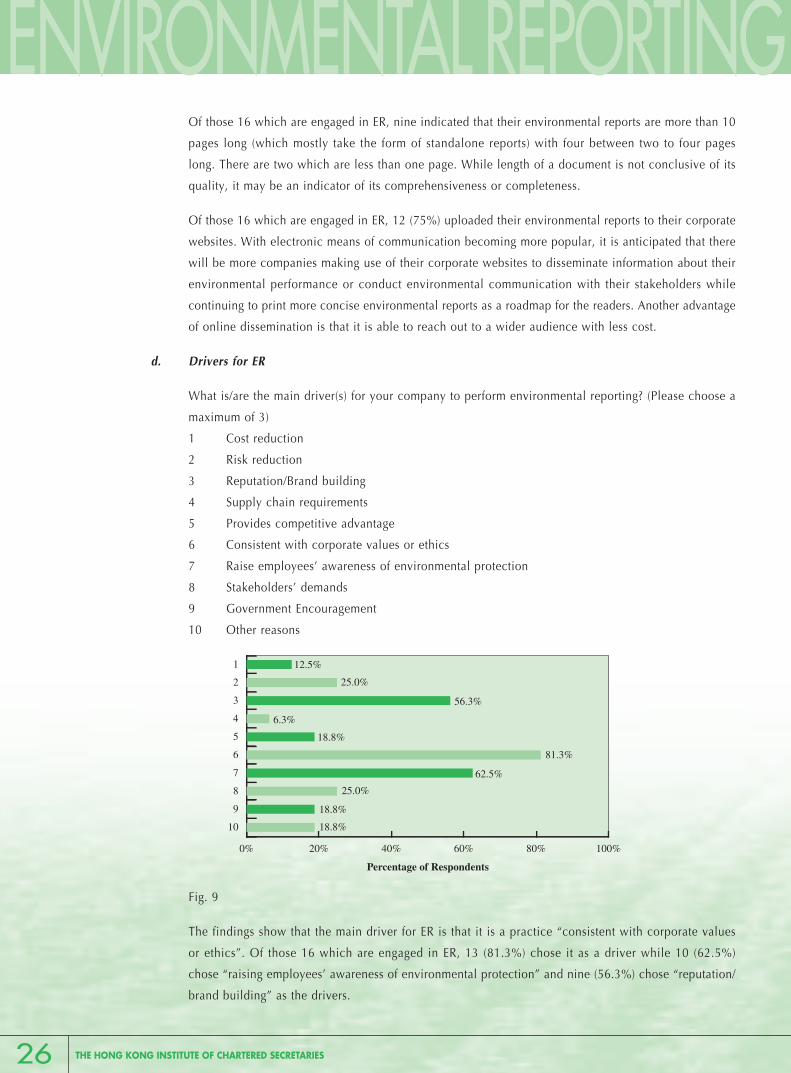

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES02

ENVIRONMENTAL REPORTINGSimilarly, few of the surveyed companies appear to include environmental risks as part of their risk management

systems. Even for those companies engaged in ER, the three main drivers cited were: “consistency with corporate

values or ethics”, “reputation/brand building” and “promotion of the employees’ awareness of environmental

protection”. Few chose “risk reduction” as a driver. It seems that the effectiveness of ER as a tool to identify and

control potential risks faced by a company is not fully understood or accepted by the business community in Hong

Kong.

It also seems that few companies have made the association between environmental risk and the financial performance

or the competitiveness of a company. Improvement of financial performance and the competitiveness of a company

can be achieved through increasing its efficiency and reducing operational costs, which in most cases can be

facilitated by efficient use of raw materials, energy saving and the reduction of waste. Of those 16 surveyed

companies which have been engaged in ER, only two chose “cost reduction” as a driver.

The HKICS view

The HKICS believes that a wider uptake of ER in Hong Kong will bring substantial benefits, not only to the companies

involved, but also to the reputation of the Hong Kong market. Since international standards in this area have risen

dramatically in the last decade as the dire potential consequences of climate change, pollution and resource depletion

have started to be taken more seriously, Hong Kong needs to consider the damage that is being done to Hong Kong’s

reputation in the investment community on account of its low environmental reporting standards (see “Drivers for

Change” in Annex 3).

This research paper analyses the benefits of ER (see “What are the functions and benefits of ER?” below). It argues

that, apart from being a communication tool between a company and its various groups of stakeholders, it is also an

effective tool for managing environmental and operational risks. In addition, it can enhance the competitiveness and

the shareholder value of the company in the long run. The HKICS survey indicates that the lack of understanding of

ER and its benefits within the Hong Kong business community has generated the prevailing misconception that it is

irrelevant to them and is a burden on companies rather than a potential benefit. The HKICS intends this research

paper to argue the case for the benefits of ER, and also to provide practical guidance for companies on how to start

reporting on their environmental risks and impacts (see “How to get started” below).

The HKICS survey also shows that a majority of respondents consider that there is insufficient regulatory incentive for

listed companies to engage in ER, with 62.5% of those which are not engaging in ER citing the fact that it is not a

legal requirement as the main reason for not reporting. When asked what would encourage them to take up ER,

65.6% cited “regulatory incentive”. Moreover, 68.1% of all respondents agreed (6.4% of them strongly agreed) that

there are currently not enough regulatory incentives for listed companies to engage in ER in Hong Kong. However,

51.1% of the respondents agreed (with 6.4% strongly agreeing) that ER should remain voluntary. When the question

was put the other way around, that is, when respondents were asked if they agreed that it should be made mandatory,

only 29.8% of them agreed.

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 03

ENVIRONMENTAL REPORTINGThe HKICS does not support the view that ER should be a mandatory requirement. Given the lack of understanding of

ER in Hong Kong, making it a mandatory requirement runs the risk of a high rate of non-compliance, and the

encouragement of a “checklist mentality” towards environmental disclosure. There are, however, a number of ways

to motivate the less committed companies to take up ER as soon as practicable. This research paper therefore

recommends that the Exchange should introduce ER as a Recommended Best Practice in the Code on Corporate

Governance Practices (“CG Code”) as soon as practicable, and issue guidelines to listed companies to help them start

engaging in ER. The establishment of a Hang Seng Environment Index, and a CSR Index or Sustainability Index, in the

long run is also recommended as a way to promote ER and CSR in Hong Kong.

The survey

A questionnaire (see Annex 1) was sent to all 961 companies (as at 12 May 2006) listed on the Main Board of the

Exchange. Respondents were asked, among other things, to indicate if they undertake ER, what are their main drivers

and barriers for ER, and for those which are not engaged in ER, whether they have the intention to do so in the

coming three years. Their comments were also solicited on various issues including whether ER should be a mandatory

practice in Hong Kong. The findings of this questionnaire-based survey will be discussed later in this research paper.

Apart from the questionnaire-based survey, all 201 Main Board listed companies which were the constituent stocks

of the Hang Seng Composite Index as at 10 April 2006 have been taken as samples for another survey (“HSCI

Survey”). Information was obtained from publicly available sources such as their latest annual reports, sustainability

reports, CSR reports and corporate websites. The main purpose of this exercise was to find out how many of the

surveyed companies were engaged in ER in any form.

Face to face interviews were also conducted with seven individuals involved in relevant areas, such as environmental

protection, social responsibility investment, research in corporate environmental management and the preparation of

environmental reports (see Annex 2 for the identities of the interviewees and extracts from the interviews). The

interviewees were asked to comment on various issues relating to ER and environmental protection.

Summary of the findings

Sample Size:

Questionnaire respondents: 48

HSCI companies surveyed: 201

• 16 (33.3%) of the questionnaire respondents are engaged in ER.

• 52 (26%) of the HSCI companies surveyed are engaged in ER.

• 10 (5%) of the HSCI companies surveyed publish standalone environmental reports.

• 25 (52.1%) of the questionnaire respondents indicated that they have an environmental policy.

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES04

ENVIRONMENTAL REPORTING• 20 (62.5%) of the questionnaire respondents which are not engaged in ER cited the fact that it is not a legal

requirement as the reason for not doing it.

• 28 (87.5%) of the questionnaire respondents which are not engaged in ER indicated that they have no plan to

do so in the coming three years.

• 21 (65.6%) of the questionnaire respondents which are not engaged in ER cited “regulatory incentive” as the

primary driver which would influence their future adoption of ER.

• 24 (51.1%) of 47 questionnaire respondents believe that ER should remain voluntary in Hong Kong.

Summary of the recommendations

• The Exchange should introduce ER as a Recommended Best Practice in the CG Code.

• The Exchange should issue guidelines to listed companies detailing what it expects of them as regards ER.

• Seminars or workshops relating to ER should be organised by regulators jointly with the EPD.

• The environmental reports, CSR or sustainability reports published by listed companies should be made

accessible on the websites of the Exchange and the EPD (subject to the consent of the relevant companies).

• The establishment of a Hang Seng Environment Index, and a CSR Index or Sustainability Index, should be

considered as a long-term goal.

2. BACKGROUND

What is environmental reporting?

An environmental report is a communication document describing the link between a company and the environment.

It is usually produced with the objective of establishing a dialogue concerning environmental issues with stakeholders

of the reporting company. It relates closely to the wider concept of “sustainable development” which according to

the most widely used definition, known as the Brundtland definition1, means “a form of development that meets the

needs of the present without compromising the ability of future generations to meet their own needs”.

ER is also closely related to the concept of CSR which does not have a fixed meaning but can generally be taken to

mean the integration of social and environmental concerns with business operations and in the interactions with the

stakeholders of a corporation on a voluntary basis2.

1 The Brundtland Report, representing the growing global awareness of the enormous environmental problems facing the planet, is the report made by

the World Commission on Environment and Development in 1987. It is often called the Brundtland Report after the chairperson of the commission, the

then Minister of Norway, Mrs Gro Harlem Brundtland.2 p.6 of European Union Green Paper — “Promoting a European Framework for Corporate Social Responsibility” (2001)

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 05

ENVIRONMENTAL REPORTINGThe interlinking of these three concepts explains why some corporations now report on their environmental impacts3

in sustainability reports, or CSR reports, which also incorporate the social and economic dimensions of a company.

This HKICS research paper will, however, focus on environmental reports, while references will also be made to CSR

reports and sustainability reports from time to time in view of their close connection with ER.

ER is commonly seen as a form of non-financial reporting by the business world. To categorise ER as non-financial

reporting is not necessarily wrong, but it would be a fallacy to assume that the information disclosed in environmental

reports does not have any financial implications for the reporting company. On the contrary, data on a company’s

energy consumption, waste production and any hazardous emissions have obvious financial implications. Environmental

information can be translated into financial terms by the development of environmental accounting techniques

which help assess accurately and consistently how well the environmental costs and liabilities are incorporated into

the financial statements of a company.

Financial reporting, having evolved over a longer period of time, has become well established in terms of its

framework and standards. ER however, is a new concept for most companies, investors and the general public. It

may take some time for people to recognise the fact that the financial performance of a company is affected by many

factors left outside the scope of its financial statements, and ER, sustainability or CSR reports can help close this gap.

The combination of disclosures in the non-financial reports and the financial data disclosed in the traditional

financial reports can provide a fuller picture of the company.

What are the functions and benefits of environmental reporting?

1. Social accountability

With the emergence of CSR, the demand for more transparency and accountability for the environmental and

social impacts of corporate conduct has increased. The principle of “shareholder primacy” which advocates

that directors’ rights should be exercised only for maximising shareholders’ wealth has faced great challenges

and become less and less tenable as the belief that corporations have broader social responsibilities becomes

more prevalent. There has been a lot of debate in this area. An argument advanced to support this broader

view is that since the act of incorporation confers a lot of privileges such as limited liability, society is entitled

to expect that a corporation will act in the interests of the general public and not just for self-interest.

In the UK, the concept of “enlightened shareholder value” was introduced in the Companies Bill 20054. The

Bill requires directors to take a balanced view of the implications of decisions over time and take due account

of both long-term, short-term and wider factors such as the need of the company to maintain an effective

relationship with its employees, customers and suppliers. While the primary duty of directors is to “promote

the success of the company for the benefit of its members as a whole”, they must in fulfilling such duty, have

regard to various things including “the impact of the company’s operations on the community and the

environment”5.

3 According to the Sustainability Reporting Guidelines of the Global Reporting Initiative, “environmental impacts” mean an organisation’s impact on

living and non-living natural systems, including eco-systems, land, air and water.4 The Bill was introduced to the House of Lords on 1 November 2005. The title of the Bill was changed from “Company Law Reform Bill” to “Companies

Bill” during the committee stage in the House of Commons in July 2006.5 Clause173(1) of the Companies Bill.

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES06

ENVIRONMENTAL REPORTINGBusiness operations can generate considerable impacts on the environment. The public, being co-owners of

the environment, is getting more conscious of its right to know more about the social and environmental

impact created by a company in its business operations. ER is an effective channel for a company to disclose

to the public its environmental performance and impact.

2. Communication with stakeholders

The notion of “stakeholders” reflects the idea that the conduct of corporations can affect a broader range of

people other than shareholders. The term does not refer to a homogeneous group and does not have a precise

definition, but it can be interpreted as “groups vital to the success and survival of a corporation”6. According

to the Corporate Social Responsibility Discussion Paper issued by Corporations and Markets Advisory Committee

of the Australian Government, published in November 2005 (“Australian CSR Discussion Paper”), the term

can include:

• shareholders, who unlike other stakeholders, have a direct equity interest in the company;

• other persons with a financial interest in the company such as financiers, suppliers, creditors or

business partners;

• persons who are involved in the wealth creation of the company, e.g. employees and consumers;

• anyone otherwise directly affected by a company’s conduct e.g. the local community; and

• pressure groups or NGOs usually defined as public interest bodies that espouse social goals relevant to

the activities of a company.

It is in the best interest of a company to take into account the views, legitimate needs and expectations of its

stakeholders. The long-term shareholder value and profitability of a company always depends on meeting the

fair expectations of its stakeholders. The OECD Principles of Corporate Governance (2004) states that:

“The governance framework should recognise that the interests of the corporation are served by recognising

the interests of the shareholders [including employees and creditors] and their contribution to the long-term

success of the corporation”.

Effective communication with its stakeholders is therefore crucial for the success of a corporation. Traditionally,

financial reports used to be the only communication document issued by companies and financial information

was the only important information which the company had to disclose to its stakeholders. Nowadays, there is

growing acceptance that the way a corporation discloses and deals with its environmental, social and other

non-financial risks does have a bearing on its financial viability. The importance of ER has therefore been

growing rapidly.

6 p.27 of Corporate Social Responsibility Discussion Paper published in November 2005 by Corporations and Markets Advisory Committee of the

Australian Government.

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 07

ENVIRONMENTAL REPORTINGBelow we look at companies’ potential stakeholders and their interests in ER.

a. Shareholders

Shareholders are a major group of stakeholders to whom the directors of a corporation are directly

accountable. Unlike the other groups of stakeholders, shareholders can exert influence on the corporate

decisions through the exercise of voting rights in the shareholders’ meetings. In recent years, shareholders

worldwide are generally more conscious of their rights to information. The increase in the awareness

of shareholders’ rights has generated greater demand for transparency and accountability from

corporations. ER is an effective tool for the communication of environmental policies and efforts of the

corporations with their shareholders.

b. Customers and employees

Customers may make their choices about products or services based on the production method or

environmental impact of a corporation. Eco-labelling nowadays plays an important role in the marketing

of goods and services in some countries such as Japan and the European Union (“EU”). The EU eco-

label “flower” can be found in some 300 products and services from all EU countries which have

reached certain criteria in respect of the raw material extraction, manufacture, distribution and final

disposal. Customers have more confidence in products or services with eco-labels which will be of

particular importance to those customers who are more environmentally conscious. The commitment

of a corporation to social and environmental values may also enhance its reputation and motivate

talented people to work for it. It can also increase the environmental awareness of the staff of the

corporation and boost their morale.

c. Lenders

The growing importance of environmental management to the financial community is also evident.

Lenders, investors and insurers are paying more attention to the environmental risks and performance

of corporations when they evaluate their financial risks.

The Equator Principles, a voluntary set of guidelines initially developed by a small group of banks

together with the World Bank Group’s International Finance Corporation in 2003 for managing social

and environmental issues relating to financing of projects, have been adopted by over 40 financial

institutions7 around the world as an important step in promoting responsible project financing. Through

the Equator Principles, financial institutions undertake to provide loans only to those projects which

can be developed in a socially responsible manner and reflect sound environmental management

practices. The Principles were revised in July 20068 and the revision “underscores how far the financial

sector has progressed in embedding in the project finance arena a common set of best practices to

manage social and environmental risks related to project financing”. The threshold for application of

the Equator Principles has been lowered from US$50 million to US$10 million and they now also

apply to project finance advisory activities.

7 As of June 2006, there were 41 financial institutions which have adopted the Equator Principles and it is estimated that they cover approximately 80%

of global project lending.8 See the press release issued by the Equator Principles Financial Institutions on 6 July 2006.

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES08

ENVIRONMENTAL REPORTINGThe Hong Kong and Shanghai Banking Corporation Limited (“HSBC”) adopted the Equator Principles in

2003 as a “wider approach to managing sustainability risks in lending and investment”. According to

the HSBC Corporate Social Responsibility Report 2005, the Equator Principles have been implemented

across the group and training has been extended beyond its project finance teams to include staff

responsible for managing relationships in industries with potentially high environmental and social

risks. Decision support tool is also being developed for assessing environmental and social risks in a

consistent and structured manner. The Standard Chartered Bank also adopted the Equator Principles in

2003. In its publication, Sustainable Lending and the Equator Principles 2005, it is stated that it is the

bank’s policy “for all lending proposals to consider environmental and social issues, taking into

account all recognised standards or local laws” and “there is no monetary threshold to the policy,

which covers all transactions where there is a clear link between the purpose of the funding and an

environmental or social consideration”. Sustainable lending training is also given as part of its overall

risk training programme.

Banks and financial institutions play a key role in bringing natural resources to the market. Adoption of

the Equator Principles will increasingly be recognised as a good governance and risk management

practice on the part of the lenders. ER by the borrowing companies is hence an effective way to help

lenders understand their environmental performance and management. Further, it can facilitate the

grant of loans.

d. Investors

In making investment decisions, investors may consider whether the target corporations have met

certain environmental, social and ethical standards. This approach is usually referred to as “Socially

Responsible Investment” or “Sustainable and Responsible Investment” (“SRI”). The development of SRI

worldwide has been facilitated by the establishment of various corporate responsibility market indices

such as the Dow Jones Sustainability Index in the US, the FTSE4Good in the UK, the SRI Index in South

Africa and the RepuTex SRI Index in Australia. These indices have been designed for measuring the

performance of companies which meet globally recognised corporate responsibility standards and

facilitating investment in these companies.

The concept of SRI is still new to Hong Kong and there is no local SRI Index. However, in some

countries, SRI has been developing rapidly. In Australia, product issuers which offer a financial product

with an investment component are required to disclose in their product disclosure statements the

extent to which they take into account environmental, social or ethical considerations in their selection

of investment. They should expressly state that they do not take these considerations into account if

that is the case9.

9 Section 1013DA, Disclosure Guidelines, Australian Securities and Investments Commission.

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 09

ENVIRONMENTAL REPORTINGIn the UK, starting from July 2000, pension fund trustees have to disclose the extent to which social,

environmental and ethical considerations enter into their investments10. In the light of such requirement,

major fund managers in the UK in turn also require companies to publish comprehensive environmental

reports. Thus, identifying environmental risks and opportunities is becoming increasingly important for

institutional investors11. Likewise, in other European countries, such as France, Germany, Sweden and

Belgium, there are similar disclosure requirements for the pension fund managers.

e. Business partners

Many large corporations are greatly concerned about green procurement and have implemented CSR

strategies in their supply chain and management of supplier risk. Suppliers of these corporations are

required to set out their environmental or social practices in the tenders or to comply with the code of

conduct compiled by the corporations. To incorporate environmental concerns into the supply chain is

an effective way to transfer best practice and achieve environmental targets through collaboration. In

view of globalisation, supply chain management has become more and more critical. Hence, ER of the

suppliers which communicate their environmental performance to the purchasers is getting more

important.

f. Other stakeholders

The above groups are the major stakeholders that corporations have to engage in the course of their

business. Other stakeholders such as credit rating agencies and other interest groups may also require

information about the environmental practices and performance of corporations for compiling the

rating or benchmarking tools. Such tools are useful for providing peer comparisons and measurement

of the progress of environmental performance of corporations.

ER is a form of stakeholder engagement which in simple terms means “the various mechanisms that

have been used by organisations to listen to, and account for, the views of stakeholders as well as

involving them in the provision of solutions” to the corporations12. As it has been pointed out in the

Global Reporting Initiative’s Sustainability Reporting Guidelines13, “a primary goal of reporting is to

contribute to an ongoing stakeholder dialogue. Reports alone provide little value if they fail to inform

stakeholders or support a dialogue that influences the decisions and behaviour of both the reporting

organisation and its stakeholders”. ER is thus the beginning of a dialogue between a corporation and its

stakeholders on environmental issues. It should be kept going by continuous interaction and efforts on

both sides. On another level, ER also assists the stakeholders to make their decisions regarding the

reporting companies, be it an investment decision, purchasing decision or lending decision. In short,

ER being part of the stakeholders engagement process, enables the reporting company to find solutions

with the input of its stakeholders. On the other hand, it helps its stakeholders make informed decisions

regarding the company.

10 Pursuant to an amendment to the UK Pension Act which came into force in July 2000.11 According to a survey released by Just Pensions and the Trades Union Congress in February 2003 on the attitudes of UK pension fund trustees toward

socially responsible investing, 69% of the surveyed pension fund trustees practiced stock selection that took into account social, environmental andethical issues specified in their Statement of Investment Principles.

12 p.34 of Australian CSR Discussion Paper.13 p.9 of 2002 version of the Guidelines.

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES10

ENVIRONMENTAL REPORTING3. Risk management and competitive edge

For the corporations undertaking ER, the collection and disclosure of data and information concerning

environmental issues will yield scope for improved management practices and can therefore lead to increased

competitiveness.

a. Pledge and review

In an environmental report, the reporting company will always state its environmental policy, objectives

and efforts towards strategic management of environmental issues. By disclosing its targets and the

state of its environmental activities, the company is motivated to evaluate its own performance on a

regular basis, an effect known as “pledge and review”. It drives the company to identify its own

shortcomings and methods for improvements.

b. Risk management

A well-managed company should have regard to a wide variety of risk factors including non-financial

risks which are likely to impinge on its operations. Identifying and assessing potential risks facing a

company and taking measures to avoid or manage the risks is therefore extremely important for the

management of a company. Risk management is an integral part of good corporate governance. There

is no requirement in the Rules Governing the Listing of Securities on the Exchange (“Listing Rules”)

that a Main Board listed company should establish a risk management system.

However, in Code Provision C.2.1 of the Code on Corporate Governance Practices (Appendix 14 to the

Listing Rules), it is provided that:

“The Directors should at least annually conduct a review of the effectiveness of the system of internal

control of the issuer and its subsidiaries and report to the shareholders that they have done so in their

Corporate Governance Report. The review should cover all material controls, including financial,

operational and compliance controls and risk management functions”.

Though there is no express reference to social and environmental risks, the management of environmental

risks should clearly come within the scope of the above Code Provision C.2.1. Management of non-

financial risks may not be able to help a company maximise profits in the short term. However, the

failure to do so may result in an increase in its operating costs, an increased risk of litigation, regulatory

intervention, damage to its reputation and brand, and loss of community support. These risks are all

detrimental to the business performance and financial position of a company.

The emergence of the concept of “corporate environmental management” (“CEM”) and “corporate

environmental governance” (“CEG”) is evidence of increasing awareness of the need of companies to

manage their environmental risks.

ENVIRONMENTAL REPORTING

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 11

CEM is defined as “values, norms, processes and institutions through which companies attempt to

ensure that they operate in a safe and environmentally sustainable manner” and it extends beyond

compliance with environmental legislation14. It requires incorporation of environmental systems and

tools in business strategic planning to ensure that environmental issues are integrated into the overall

corporate objectives.

CEG is defined as “the policies, procedures, and practices developed by companies to reduce the risk

of their operations causing damage to the environment, to help them use resources more effectively,

and to demonstrate to stakeholders and the public that they operate in an environmentally friendly

way. More specifically, it involves setting out the responsibilities of directors and establishing the

accountability of the board to the company’s stated environmental objectives, as well as their

effectiveness in meeting those requirements. These may include mechanisms for corporate environmental

reporting, the adoption of in-house environmental management and auditing systems, certification

under the ISO 14000 series of standards, “greening” the supply chain, and product stewardship.”15

From the above definitions, it is clear that the successful implementation of CEM and CEG will require

environmental knowledge, the combined efforts and involvement of the senior management level of a

company. As these are new concepts to most companies in Hong Kong and given the low awareness of

environmental issues within the business community as shown in the questionnaire-based survey

(which will be discussed in detail later), it seems that few companies in Hong Kong have adopted

them. In fact, it is found that most small to medium enterprises (“SMEs”)16 are still in the phase of

compliance with environmental regulations17.

ISO 14001 is an element of CEG as defined above. It is an internationally accepted specification

developed by the International Organization for Standardization (ISO) for an environmental management

system (“EMS”). In effect, it is a set of cohesive elements which an organisation may use to minimise

its impact on the environment. The growing importance of EMS as a practical tool to reduce the

environmental impact and support continuous environmental improvement was stressed in the

“Government Position Statement on EMS” issued by the UK Government in September 2005. In the

statement, the UK government strongly supports the use by corporations of a robust EMS and the use of

international standards such as ISO 14001, EU Eco Management and Audit Scheme (“EMAS”) and BS

8555 which is a recent addition to the EMS family.

14 p.7 of Working Paper “Drivers and Barriers to Engaging Small and Medium-Sized Companies in Voluntary Environmental Initiatives” by Sonja Studer,

Richard Welford and Peter Hills (November 2005).15 p.1 of Project Report 1 “In-house Environmental Knowledge Capital and Corporate Environmental Governance in Hong Kong Business” by Margaret Lo,

Joyce Tsoi, Richard Welford, Peter Hills and Jon Hills (January 2003)16 The Hong Kong government defines SMEs as manufacturing businesses with less than 100 employees, or non-manufacturing businesses with less than

50 employees.17 p.2 of the Project Report 1 “In-house Environmental Knowledge Capital and Corporate Environmental Governance in Hong Kong Business” by Margaret

Lo, Joyce Tsoi, Richard Welford, Peter Hills and Jon Hills (January 2003).

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES12

ENVIRONMENTAL REPORTINGA revision to the ISO 14001 was made in 2004. The revision has shifted the emphasis in the standard

to a clearer focus on transparency of processes, continuous improvement of performance and periodic

evaluation of legal compliance. Some of the perceived benefits of obtaining an ISO 14001 certification

include the improved perception of the key environmental issues by the employees, better public

image of the corporation, increase in the efficiency in energy and raw materials use and improved

ability to meet compliance with environmental regulations.

Though ISO 14001 is recognised as an important tool in achieving CEG, it is not meant to be an

absolute standard or a guarantee of high level of environmental performance. In particular, it is worth

noting that a company does not have to be in compliance with all environmental regulations to be

certified to ISO 14001. It does, however, need to have a system in place which can help them towards

compliance. Besides, the integrity of the ISO 14001 certification depends very much on the credibility

of the certification bodies which are themselves subject to annual audits by the accreditation bodies18.

As of April 2005, there were a total of 88,800 ISO 14001 certifications in the world. In December

2005, there were 396 ISO 14001 certified bodies in Hong Kong which includes government departments

and public bodies19. The growing trend of ISO 14001 certification in Hong Kong is shown in the chart

below. And the attributes of the certified bodies are summarised in the table below.20

0

50

100

150

200

250

300

350

400

450

3/00 6/00 9/00 12/00 3/01 6/01 9/01 12/01 3/02 6/02 9/02 12/02 3/03 6/03 9/03 12/03 3/04 6/04 9/04 12/04 3/05 6/05 9/05 12/05

Certificate by companies = 357

Certificate still valid Certificate withdrawn

Local Trend of ISO 14001 Certificates in HK

74 8091

105118

136146

165175

196206

223

251265 273

288307

328345

355366

383 385396

3 3 3 5 5 6 7 7 10 11 19 22 24 28 31 33 38 40 41 49 51 5364 72

Fig. 1

18 “ISO14001: 2004 What do investors need to know?” published by Association For Sustainable & Responsible Investment in Asia (2005).19 Figures provided by the Hong Kong Environmental Protection Department.20 Chart and table were compiled by the Hong Kong Environmental Protection Department

ENVIRONMENTAL REPORTING

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 13

Fig. 2: Distribution of ISO 14001 Certificates (by Industrial Sectors)

By Industrial Sectors (EAC Code) No.

Construction (28) 86

Electrical & optical equipment (19) 66

Other services (35) 38

Financial intermediation, real estate, 28

rental (32)

Wholesale & retail trade, repairs of 24

motor vehicles, motorcycles &

personal & household goods (29)

Transport, storage & communication (31) 23

Public administration (36) 22

Engineering services (34) 19

Other social services (39) 14

Basic metal & fabricated metal products (17) 11

Machinery & equipment (18) 9

Electricity supply (25) 8

Manufacturing not elsewhere classified (23) 7

Rubber & rubber products (14) 6

Concrete, cement, lime, plaster, etc. (16) 6

By Industrial Sectors (EAC Code) No.

Hotels & restaurants (30) 5

Food products, beverage & tobacco (3) 4

Printing companies (9) 3

Textiles & textile products (4) 3

Recycling (24) 2

Agriculture, fishing (1) 2

Education (37) 2

Mining & quarrying (2) 1

Pulp, paper & paper products (7) 1

Publishing companies (8) 1

Chemicals, chemical products & fibers (12) 1

Pharmaceuticals (13) 1

Gas supply (26) 1

Health & social work (38) 2

Total 396

It should be made clear that an ISO 14001 certified company or a company which has incorporated

the CEM or CEG into its business systems is not necessarily engaged in ER. On the other hand, a

company which is engaged in ER may not be an ISO 14001 certified company though it is likely to be

one which has set up a system which measures the impact of its operations on the environment.

However, the ISO 14001 certification and the engagement in ER do have a correlation as found in the

questionnaire-based survey which shall be discussed in detail later. Nevertheless, ISO 14001 certification,

CEM, CEG, EMS and ER all form an integral part of a risk management system which is instrumental in

the identification and management of the environmental risks faced by a company.

c. Enhancement of competitiveness

ER has often been perceived by the business community as a burden on a company which entails

additional costs and resources. Some even believe that it creates competitive disadvantage. There is no

doubt that ER requires additional resources and in-house knowledge of environmental issues. A company

engaged in ER, however, can through the regular evaluation, early identification and proper management

of environmental risks, enhance its operational efficiency and overall financial performance in the

following ways:

• reduction of operating costs as a result of more efficient use of raw materials, reduction of

waste and energy saving;

• increase of business opportunities and expansion of international markets;

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES14

ENVIRONMENTAL REPORTING• avoidance or reduction of liability resulting from adverse litigation or penalty or fine imposed

on the company for breach of environmental laws and regulations;

• prevention and mitigation of operational and business risks;

• reduction of insurance costs;

• enhancement of corporate reputation as an environmentally responsible corporation and good

corporate citizen; and

• increase in the environmental awareness and morale of the staff.

ER can help increase the business opportunities of a company since green procurement has become a

common corporate policy of many large corporations both locally and worldwide. Suppliers are

frequently required to provide their environmental policies and reports for assessment by the large

corporations. Some corporations also require their suppliers to comply with their ethical or environmental

code of conduct. Some even take the further step of auditing or monitoring their suppliers’ environmental

practices to ensure such compliance21. In a global economy where more companies are relocating part

of their production to the low cost countries, the allocation of responsibilities within the supply chain

has become an important issue and ER by suppliers is increasingly becoming a common supply chain

requirement.

Based on the above benefits, there is growing acceptance of the view that ER is an effective tool for

managing environmental risks as well as improving the overall operational efficiency of a company

which consequentially helps increase its competitiveness. In the long run, the adoption of socially and

environmentally responsible business practices is also conducive to the enhancement of shareholder

value of a company, which to a large extent is built upon the investors’ perception of the business.

Recent developments in other jurisdictions

There has been an increasing trend overseas for tougher requirements on corporate environmental disclosure.

1. European Union

In May 2001, the European Commission issued a recommendation on the recognition, measurement and

disclosure of environmental matters in the annual reports and accounts of the EU companies. It further

commented that the quantity, transparency and comparability of environmental data flowing through the

annual accounts and annual reports of companies must be increased22.

21 p.24 of the HSBC Corporate Social Responsibility Report 2005.22 EU Commission Recommendation 30 May 2001 (2001/453/EC).

ENVIRONMENTAL REPORTING

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 15

This recommendation paved the way for the subsequent EU Accounts Modernisation Directive issued in June

2003 (“EU Accounts Modernisation Directive”) which provided, among other things, that EU corporations

should include in their annual reports “analysis of environmental and social aspects necessary for an

understanding of the company’s development, performance or position”.

2. The UK

In 2000, the UK Prime Minister challenged the FTSE 350 leading companies to report on their environmental

performance. As of January 2006, 140 of the top 250 companies in UK report on their environmental

performance23.

The EU Accounts Modernisation Directive which applies to over 36,000 large and medium companies in UK24

(including over 1,200 quoted companies)25 introduces requirements for companies to include a balanced and

comprehensive analysis of the development and performance of the business in their Directors’ Report. The

analysis should “include both financial and, where appropriate, non-financial key performance indicators

relevant to the particular business, including information relating to environmental and employee matters”

(“Business Review”).

This requirement on the Business Review in the Directors’ Report became effective for financial years beginning

on or after 1 April 200526. Only those non-quoted companies which satisfy the statutory definition of “small

company”27 will be exempted from this requirement.

In January 2006, the UK Department for Environment Food and Rural Affairs (“DEFRA”) issued a set of new

voluntary environmental reporting guidelines titled “Environmental Key Performance Indicators - Reporting

Guidelines for UK Business” to give clear guidance to companies on how to report on their environmental

performance using environmental Key Performance Indicators (“KPI”). The guidelines are relevant to both

mandatory reports such as the Business Review and other voluntary environmental reports. The guidelines set

out 22 environmental KPIs that are significant to UK businesses and describe which KPIs are most significant

to which business sectors. The majority of sectors have five or fewer relevant KPIs and for most companies,

greenhouse gas emission is the most significant KPI28.

23 News release dated 24 January 2006 of UK Department for Environment, Food and Rural Affairs.24 “Medium company” is defined as a company with turnover not more than £22.8 million, balance sheet not more than £11.4 million and employees not

more than 250 employees (p.9 of Environmental Key Performance Indicators-Reporting Guidelines for UK Business published by UK Department forEnvironment, Food and Rural Affairs in January 2006).

25 “Quoted company” is a company whose shares are listed in the UK or the EEA, or admitted to dealing on the New York Stock Exchange or Nasdaq(Guidance on the changes to the Directors’ Report Requirements in the Companies Act 1985-April and December 2005).

26 The requirement to produce a statutory Operating and Financial Review was abolished in January 2006.27 “Small company” is a company which satisfies two of the following criteria: turnover not more than £5.6million, balance sheet total not more than

£2.8million, and not more than 50 employees.28 According to the initial findings of a survey commissioned by the UK Environment Agency in 2006 on FTSE All Shares companies, 96% of the 79 FTSE

All-Share companies that have published their Annual Report and Accounts and have discussed their interaction with the environment and thedisclosures regarding climate change dramatically increased to 51% from 17% in 2004. However, the quantification of environmental impacts remainslow with less than 20% of companies reporting on greenhouse gas emissions. A full study of the survey is due in the autumn of 2007.

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES16

ENVIRONMENTAL REPORTING3. The US

The Securities and Exchange Commission (“SEC”) reporting obligations under Items 101, 103 and 303 of

Regulation S-K include environmental disclosure requirements which are applicable to all companies subject

to SEC rules. However, only information considered as “material” has to be disclosed. In the SEC rules,

“material” is defined as “those matters to which there is a substantial likelihood that a reasonable investor

would attach importance in determining whether to buy or sell the securities registered”.

Item 101 requires filing of a general description of the business which must include information about the

material impact that the environmental regulations will have on the registrant’s capital expenditures, corporate

earnings, and general competitive position. Item 103 requires disclosure of information relating to legal

proceedings (including those relating to environmental regulations) which are material to the business or

financial condition of the registrant. And according to Item 303, disclosure, in the form of a management

discussion and analysis, of any known trends or uncertainties that have or will have a material impact on the

revenue from continuing operation of the registrant, has to be made.

4. France

Since 2001, France has gone beyond the EU Accounts Modernisation Directive by mandating social and

environmental reporting for listed companies which are required to include in their annual reports “information

on how the company takes into account the social and environmental consequences of its activities”.

5. South Africa

In South Africa, companies listed on the Johannesburg Stock Exchange have been required since 2003 to

report annually on their social and environmental performance using Global Reporting Initiatives (“GRI”)29.

6. Australia

The Corporations Act 2001 requires that the director’s report in an annual report of a company which is

“subject to any particular and significant environmental regulation” should give details of the company’s

performance in relation to environmental regulation30. For a listed company, the director’s report should also

include information that members of the company would reasonably require to make an informed assessment

of the operation of the company, its financial position and the company’s business strategies and its prospects

for future financial years31.

29 GRI’s vision is that reporting on economic, environmental, and social performance by all organisations will be as routine and comparable as financial

reporting. Organisations seeking to report using GRI framework should use the Sustainability Reporting Guidelines developed by GRI as the basis for

their reports.30 Section 299(1)(f) of Corporations Act.31 Section 299A of Corporations Act.

ENVIRONMENTAL REPORTING

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 17

Under Rule 4.10.17 of the ASX Listing Rules, a listed company should include a review of operations and

activities for the reporting period. The review does not have to follow any particular format. Reference can,

however, be made to the Group of 100 Inc publication “Guide to the Review of Operations and Financial

Condition” (“Review Guide”) which is reproduced in Guidance Note 10 of the ASX Listing Rules.

The Review Guide makes specific reference to social and environmental factors and states that the review

should include an analysis of key financial and non-financial performance indicators (“KPIs”) used by the

management in their assessment of the company and its performance and where practical, KPIs should

include multiple perspective such as sustainability measures including social and environmental performance

measures.

The Australian government has recently suggested to the ASX Corporate Governance Council that the

sustainability reporting requirement should be incorporated into the “Principles of Good Corporate Governance

and Best Practice Recommendations” which shall be applied to the listed companies on a “comply or explain”

basis32.

7. Japan

In 2004, there were about 700 companies (out of 6,000 organisations which were either listed or employ

more than 500 employees) which were engaged in ER in Japan. Japan and Australia have mainly been

responsible for the increase in the uptake of ER in the Asia Pacific region since late 1990s. The Ministry of

Environment in Japan has published several sets of very comprehensive guidelines which can be adopted by

corporations on a voluntary basis33.

Starting from April 2005, “specified corporations” as defined in the Ministerial Ordinance must prepare and

publish environmental reports for every financial year in accordance with “Law Concerning the Promotion of

Business Activities with Environmental Consideration by Specified Corporations, etc., by Facilitating Access to

Environmental Information, and Other Measures”, failing which a civil fine of up to 200,000 yen shall be

imposed on their executive officers. Large corporations other than “specified corporations” are also encouraged

to publish environmental reports.

8. PRC

Since its accession to the WTO, China has been actively tightening its environmental regulations and trying

hard to combat pollution by businesses. Exporters in China have also been suffering from “green barriers” —

the international trade standards designed to protect the environment, health and safety of the people of the

importing countries34.

32 See Australian CSR Discussion Paper (November 2005)33 Environmental Reporting Guidelines, Environmental Performance Indicators Guidelines, Environmental Accounting Guidelines & Eco-Action 21

Environmental Management Systems Environmental Activities Reports Guidelines.34 p.14 of Project Report 1 “In-house Environmental Knowledge Capital and Corporate Environmental Governance in Hong Kong Business” by Margaret

Lo, Joyce Tsoi, Richard Welford, Peter Hills and Jon Hills (January 2003).

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES18

ENVIRONMENTAL REPORTINGThe Law on the Environmental Impact Assessment (“EIA”) came into operation in September 2003. The EIA

requires the planning activities of central and local governments to be subject to the requirements of the

environmental impact assessment and in some cases, subject to public consultation. In addition, private

sector construction activities are also subject to mandatory environmental impact assessment under the EIA.

In January 2005, the State Environmental Protection Administration (“SEPA”), an organisation directly under

the State Council and responsible for the overall supervision and management of China’s environmental work,

ordered the cessation of 30 major projects (totalling over US$14 billion in investment) on the ground that they

have failed to conduct proper environmental assessments and obtain approvals from environmental authorities

before commencing construction35.

The environmental law has been further strengthened in February 2006 by the promulgation of the

Interim Provisions on Punishment of Acts Violating Laws and Disciplines on Environmental Protection, under

which stringent disciplinary measures will be imposed on the government staff who fail to administer the

environmental law.

On 5 June 2006, a White Paper titled “Environmental Protection in China” was published by the State Council

Information Office. It is a very comprehensive document which summarises the efforts made by China in

environmental protection over the past 10 years. It is indicated in the paper that there will be a change in

China “from mainly employing administrative measures in environmental protection to comprehensive use of

legal, economic, technical and necessary administrative measures to solve environmental problems”.

Despite the commitment of the government, CSR reporting which covers ER is presently almost non-existent

in China36, but a change is expected as China continues to expand its foreign trade, seek overseas listings and

as overseas companies increase their sourcing of products from suppliers in China.

Should environmental reporting be mandatory in Hong Kong?

Pressure for greater transparency and disclosure about environmental and social practices has led many countries to

introduce new disclosure regulations in recent years. As noted above, many countries have introduced environmental

information disclosure requirements. In light of the above international developments, should Hong Kong consider

mandating ER? Before Hong Kong follows the international trend, a careful study of the situation in Hong Kong

looking at the environmental awareness of the general public and the business community has to be conducted.

There is no doubt that mandating ER would at least level the playing field for companies and improve disclosure of

environmental risks, but it could also have certain disadvantages. Making ER a mandatory requirement too early —

when most of the companies are not truly convinced that it is something worth doing, or have very little knowledge

of its functions or benefits, runs the risk of developing a “checklist mentality” in the business community. Companies

may pay lip service to the requirement by including irrelevant performance indicators in their reports but make no

real change to their corporate practices. The reports may also tend to be prescriptive, lacking in depth and diversity

when the reporting companies produce them without conviction and commitment merely in response to the legal

requirement. Further, if ER is made mandatory prematurely before building up a business culture in general support

of the practice, there is likely to be a high percentage of breach of the mandatory requirement.

35 Masons (2006) March Update.36 KPMG International Survey of Corporate Social Reporting 2005.

ENVIRONMENTAL REPORTING

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 19

Most of the interviewees for this research paper (see Annex 2) take the view that Hong Kong is not yet ready to make

ER a mandatory requirement. They argue that most of the companies have not yet acquired a basic level of

understanding of ER, including how to do it, or what benefits they can get out of it. It was suggested by some

interviewees that the more effective way to boost the uptake of ER would be to encourage large and influential

companies to set a good example by taking the lead. As more companies take up ER, the peer group pressure will

become a driving force for the others which will find themselves lagging far behind unless they also adopt the

prevailing practice.

How to get started

ER is relatively new to Hong Kong and most of the companies in Hong Kong have little knowledge and experience of

preparing environmental reports or CSR/sustainability reports. However, it is an emerging trend to which Hong Kong

cannot turn a blind eye if it is going to catch up with the major markets in the world. All the interviewees contacted

for this research paper (see Annex 2) are in support of ER by companies in Hong Kong. They are all positive that ER

can to a certain extent promote environmental awareness and help control the pollution problem in Hong Kong. As

expressed by several of the interviewees, ER is not as complicated as it seems and the most important thing is to get

started.

The GRI Guidelines, published to promote sustainability reporting after a multi-stakeholder consultative process

around the world, have been the most widely adopted guidelines for CSR/sustainability reporting. In view of the

width of its scope, some starters of ER or sustainability reports may find it too complicated, or some parts of it

irrelevant to them. Countries like the UK and Japan which are highly supportive of ER have published comprehensive

guidelines through their respective governmental departments which serve similar functions of EPD.

Back in Hong Kong, the EPD published A Guide to Corporate Environmental Performance Reporting (“EPD Guide”)

in 2001 in the hope that it will “contribute towards a growing acceptance among private sector organisations to

produce good quality environmental performance reports”37. The EPD Guide gives a very concise overview of key

steps of preparing an environmental report by way of a flow chart which is reproduced as follows:

Decide on Your Organizations Objectives of

Reporting

Appoint Responsible

Persons

Identify Your Target Audiences, their Needs and

Expectations

Decide on Report Format

and Style

Decide on the Timing of

Publication

Plan Report Framework and

Contents

Gather Information

and DataWrite Report Obtain Internal

ApprovalObtain Third-Party

Verification

Decide on Distribution

Strategy

Print and Release Report

Invite Feedback

Design Report

Review and Evaluate in Preparation of Next Year’s Cycle

Fig. 3

37 A Guide to Environmental Reporting for Controlling Officers was published by the EPD in February 1999 to assist Controlling Officers within the Hong

Kong Special Administrative Region Government in preparing their environmental reports.

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES20

ENVIRONMENTAL REPORTINGThe EPD Guide has also suggested the following general report framework of an environmental report:

Organization’s Profile

Describes the organization’s main business areas, and the facilities being operated and managed as well as their

locations and activities.

Environmental Goal, Policy, Objectives and Targets/Milestones

Identifies the extents to which environmental issues are being considered and addressed in the operations, services

and products of the organization.

Environmental Management Analysis

Discusses how the organization is to manage its operations and services to achieve its environmental objectives and

targets.

Environmental Performance Analysis

Shows where the organization stands now on its environmental performance in relation to its operations, services

and products by analyzing and presenting the key environmental indicators and measurements against the

corresponding policy, objectives, targets/milestones as benchmarks.

Environmental Actions Requiring Special Attention

Highlights the views of the top management on how their organization has performed during the reporting year and

which areas the management will focus on in the coming year.

Fig. 4

Reference can be made to the EPD Guide for further details and examples. For starters of ER, the guidelines set out

therein should be sufficient. For those who have been doing ER for some time and are planning to switch to CSR or

sustainability reports, the GRI Guidelines are a very good reference and basis for reporting. It should, however, be

noted that the GRI Guidelines are being updated and a third generation of the GRI Guidelines known as G3 is

expected to be released in October 2006.

What distinguishes a good environmental report from a mediocre one?

A good quality environmental report should meet certain essential criteria embodied in a widely adopted benchmarking

system. The EPD engaged Deloitte Touche Tohmatsu in 2001 to develop a benchmarking system called “A Benchmark

for Environmental Performance Reports” (“EPR Benchmark”) which intends to serve as a tool for improving the

quality of ER and a practical guidance for self-assessment of the quality of a report. Though the EPR Benchmark was

developed with the purpose of assisting approximately 80 government bureaux and departments to improve the

quality of their environmental reports which became mandatory since 2000, they are equally applicable to the

private sector.

ENVIRONMENTAL REPORTING

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES 21

According to the EPR Benchmark, there are five essential criteria for a good environmental report which are summarised

as follows:

a. Communicate effectively

• Reports must be readable and understood by the intended readers

b. Show relevance

• Reports must meet the needs and experiences of their readers

c. Demonstrate commitment and management quality

• Readers must believe in the commitment of top management to carry out the organisation’s vision and

strategy

d. Quantify performance

• To see if progress has been achieved, performance must be measured

e. Achieve credibility

• Readers want to be assured that the report is realistic, complete and balanced, and that the information

has been verified

Based on the above criteria, a score card has also been designed for self-assessment of the reporting organisations.

Details of the criteria and score card can be found in the EPR Benchmark.

Competition can always serve as an incentive to promote a worthy cause. Yearly awards have been presented to

companies or organisations for their good ER and sustainability reporting by the ACCA for more than 10 years. The

competition is organised for promoting the transparency in reporting by organisations of the impact of their business

activities on sustainable development. The judging criteria are based on completeness (40%), credibility (35%) and

communication (25%). The following are a few examples of the criteria indicators:

a. Completeness

• Corporate context (including major products/and or services, financial performance, geographical

locations)

• Key economic, social and environmental impacts of business (in the case of sustainability report)

• Rationale behind choice of indicators used in the report

• Reporting and accounting policies

b. Credibility

• Environmental financial statements and full cost accounting

• ISO accreditation/certification

• Adoption of reporting best practice e.g. GRI Guidelines

• Compliance/non-compliance record

• Environmental/sustainability impact data with appropriate cross linkages

• Third party verification statement

THE HONG KONG INSTITUTE OF CHARTERED SECRETARIES22

ENVIRONMENTAL REPORTINGc. Communication

• Understandability, accessibility and appropriate length

• Layout and appearance

• Use of internet

• Comprehensive navigation through report

• Appropriateness of graphs, illustrations and photos

• Integration with financial statements

Reference can be made to the Report of the Judges 2005 for full details of the criteria. The judges of the 2005 Award

have also made some very insightful comments and recommendations (summarised below) for improvement of the

quality of the environmental or sustainability reports:

a. All reports should include elementary components

• Identification of target audience