breaking down the barriers to hedging speaker | calum mackenzie

TRANSCRIPT

Breaking Down the Barriers

to HedgingSpeaker | Calum Mackenzie

Agenda

• Understanding your risks

• Why is it important to hedge interest rates and inflation?

• Overcome the barriers to hedging

• scheme size

• complexity of the investment tools;

• affordability and the need to invest in return seeking assets; and

• market conditions

2

Understanding your biggest risks

?

Focus trustee governance on the biggest risks

Equity market Manager Interest rate Inflation Longevity Covenant

We believe schemes should be hedging at least 70% of interest rate and even more inflation risk

But on average pension funds hedge around 30%

Small changes can change liabilities by £, millions

3

Why is it important to hedge interest rates and inflation?

What happens when interest rates

fall by 1.0%?

A

0

50

100

150

200

250

300

350

Starting position

£m

Funding level: 95%

LA

Consider a scheme invested 50% equities and 50% bonds…

0

50

100

150

200

250

300

350

Without hedging

£m

Funding level: 79%

LA

£m

Funding level: 95%

0

50

100

150

200

250

300

350

With hedging

LA

Small changes can have a major impact on funding!

4

The barriers to hedging

Aon Hewitt 2013 Global Pension Risk Survey:

“51% of small and 35% of medium sized pension funds have no hedging policy”

Barrier Can it be overcome?

Size

Complexity

Cost

Affordability

Yields are too low

There should be no barrier so significant that pension funds cannot manage their biggest risk

5

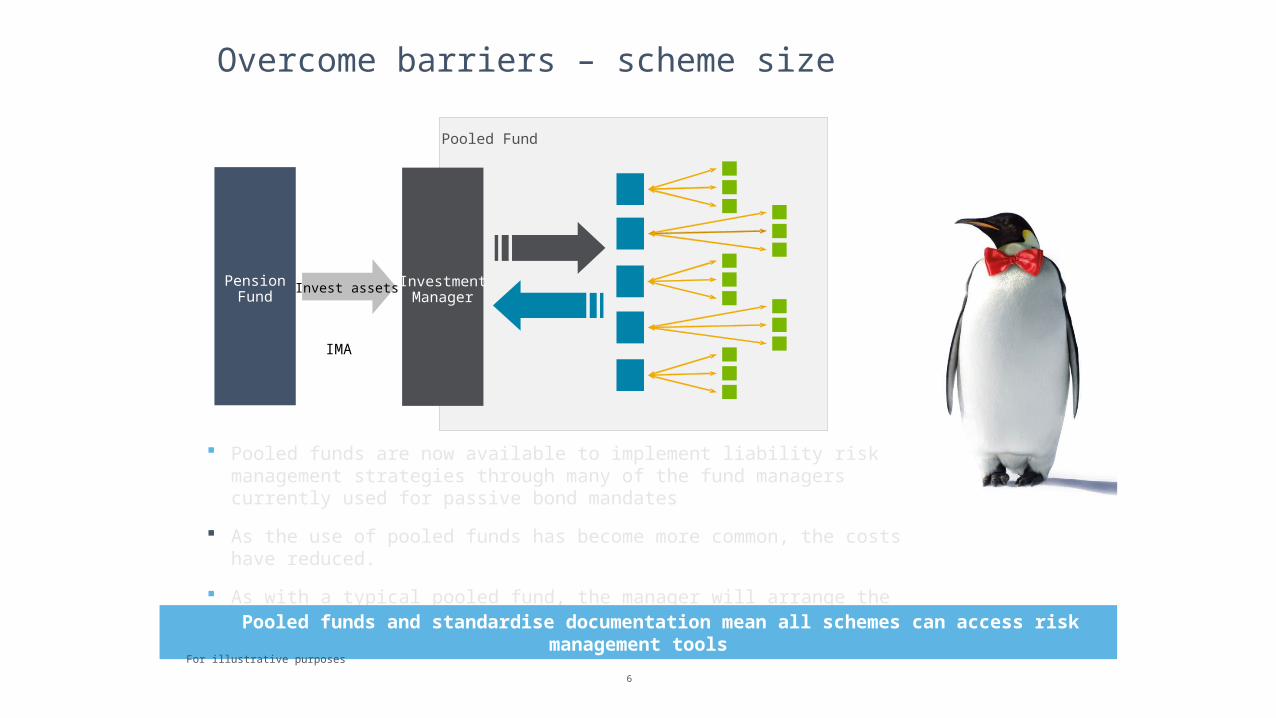

Overcome barriers – scheme size

Pooled funds are now available to implement liability risk management strategies through many of the fund managers currently used for passive bond mandates

As the use of pooled funds has become more common, the costs have reduced.

As with a typical pooled fund, the manager will arrange the purchase of the necessary contract(s) in line with your investment requirements.

Generate LIBOR

PensionFund

IMA

InvestmentManager

Invest assets

Pooled Fund

Pooled funds and standardise documentation mean all schemes can access risk management tools

For illustrative purposes

6

Overcome barriers – complexity

Hedging will become the most important component of pension scheme portfolios

Such strategies don't have to be complex and confusing

Focus on big issues – why hedge, what tools work and what could go wrong?

The risks of not hedging are much greater than risks associated with LDI strategies

There are other governance options to implementing solutions such as delegation

Complexity can be overcome by trustees with the right support

“LDI now covers £446bn of liabilities, an 11 percent increase over 2012 with 686 UK pension scheme

mandates now employing LDI”

KPMG 2013 LDI Survey

7

Looking pricey, even if profit margins were maintained

8

The hedge level can be addressed without altering return seeking assets

Inflation Hedge

Rates Hedge

Deficit

Inflation Hedge

Rates Hedge

, Diversified Portfolio ofGrowth Assets

Deficit

,

Liability DrivenInvestment

Diversified Portfolio ofGrowth Assets

Bonds

8

Overcome barriers – affordability

9

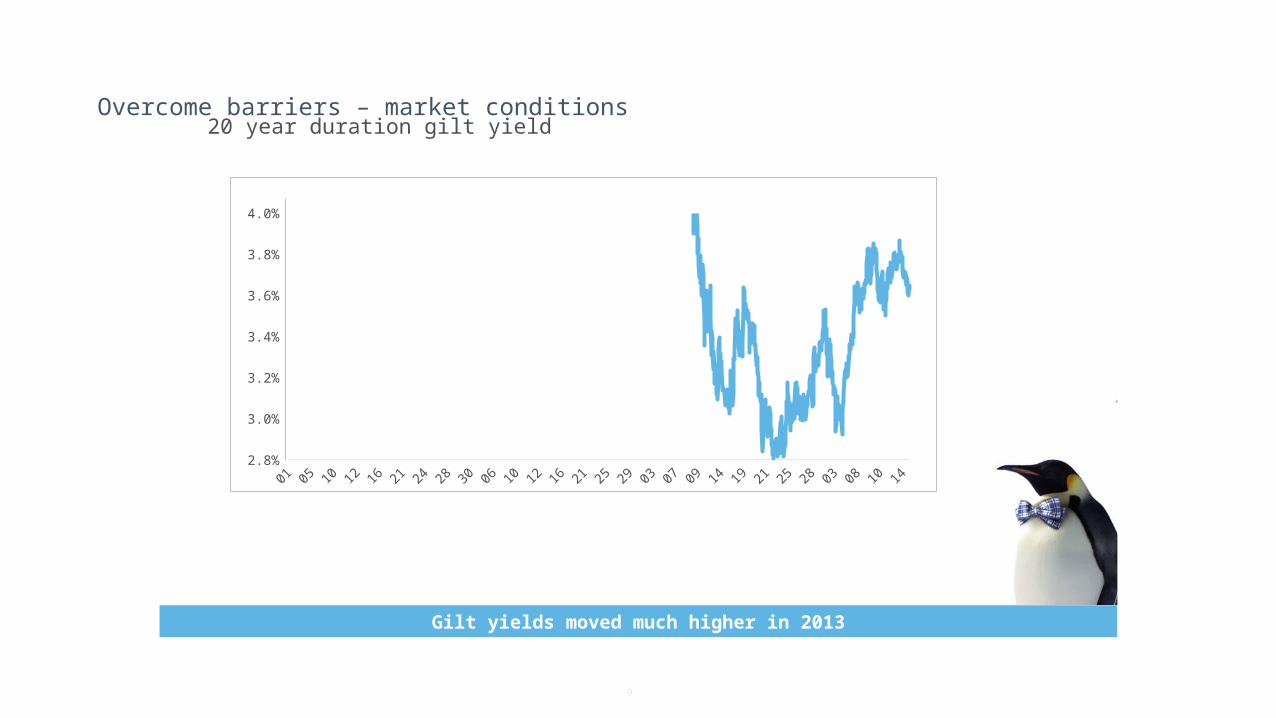

20 year duration gilt yieldOvercome barriers – market conditions

Gilt yields moved much higher in 2013

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14 Feb-142.8%

3.0%

3.2%

3.4%

3.6%

3.8%

4.0%

Market Inflation Prices Versus Us

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2008 2009 2010 2011 2012 2013

Source: Aon Hewitt, Bank of England

BOE 20 Year Duration Break-Even Inflation

Consensus 20 Year Inflation Expectations

Overcome barriers – market conditions

Gilt yields are projected to go beyond 4% in the next 3 years.. this no longer looks too

low…

Inflation pricing has improved relative to long-term expectations (blue line v orange line), so looks a reasonable time to hedge

inflation risk too…

These yield levels are over 4%, which is a much better level

than a year ago!

Market Inflation Prices Versus Us

Now is an appropriate time to consider increasing interest rate and inflation protection

10

How High Will Gilt Yields Go?(20 year duration gilt yields expected in the market)

3.40%

3.50%

3.60%

3.70%

3.80%

3.90%

4.00%

4.10%

4.20%

4.30%

Current In 1 Year In 3 years In 5 years

These yield levels are over 4%, which is a much better level

than a year ago!

Next steps

• Understand and quantify the risks your scheme is exposed to.

• Understand the impact further interest rate and inflation hedging can have on your scheme.

• Training on liability risk management tools

• Get hedging!

11

Disclaimer

Nothing in this document should be treated as an authoritative statement of the law on any particular aspect or in any specific case. It should not be taken as financial advice and action should not be taken as a result of this document alone.

Unless we provide express prior written consent, no part of this document should be reproduced, distributed or communicated. This document is based upon information available to us at the date of this document and takes no account of subsequent developments. In preparing this document we may have relied upon data supplied to us by third parties and therefore no warranty or guarantee of accuracy or completeness is provided. We cannot be held accountable for any error, omission or misrepresentation of any data provided to us by any third party.

This document is not intended by us to form a basis of any decision by any third party to do or omit to do anything. Any opinion or assumption in this document is not intended to imply, nor should be interpreted as conveying, any form of guarantee or assurance by us of any future performance or compliance with legal, regulatory, administrative or accounting procedures or regulations and accordingly we make no warranty and accept no responsibility for consequences arising from relying on this document.

Copyright © 2014 Aon Hewitt Limited

Aon Hewitt Limited is authorised and regulated by

the Financial Conduct Authority.

Registered in England & Wales. Registered No:

4396810.Registered Office:

8 Devonshire Square, London EC2M 4PL