brazil: technological innovation &...

TRANSCRIPT

BRAZIL: TECHNOLOGICAL INNOVATION & INVESTMENT OPPORTUNITIES

Telecommunication Brazilian Market

IT Brazilian Market

Segment of SW for Telecom in Brazil

Opportunities for investment in the segment

Example: VÍSENT Case

R Market Share (%)145Owner Telecom Group

Gross

Revenue

Fixed

Cellular

Broadband

PayTV

Telefónica/Portugal Telecom Telefónica/Vivo 30% 30 31 26 7

Accesses (in Million)October 2008

Telmex/America Movil Claro/Embratel/ Net 23% 11 25 21 48

Brazilian Group Oi/Way TV 18% 35 15 21 1

Italy Telecom TIM 11% 0 25 - -s

41

106

39

Brazilian Group Brasil Telecom 11% 20 4 19 -

Various Others (GVT, BT, Nextel, Sky,Intelig, VoIP Operators, etc.) 7% 4 0 13 44

Brazilian Group (M&A Proccess) Brasil Telecom/Oi 29% 55 19 40 1

Cel

lula

r

Fixe

dTe

leph

one s

Bro

adba

nd

Inte

rnet

Pay

TV

Inte

rnet

Use

rs

sues 3G

• 2 millions cellular in operation (2008/Oct)

ll ( / )

WiMax - broadband access to distances of 6 to 9 Km

• 2.6 GHz (shared with MMDS); 3.5 GHz (in licitation); 5 GHz (no need license)

ain

Iss • Basically 100% UMTS (WCDMA/HSDPA)

Ericsson and Nokia technologies

• Main application: broadband connection PC/Laptop in to Internet

• Some Operators (Embratel, BrT, Neovia)

• Boom will be in 2009 after 3.5 GHz licitation

• Government will try to reserve some space to small business

Ma small business

Video and TV

• IPTV (VoD and Live): implantation by Operators

Source: http://www.teleco.com.br/en

• DTV: SBTVD developed - MPEG-4 (H.264):

• Japanese standard to transport system

• Brazilian middleware GINGA for interactivity

Software and Services Global Market – 2007 (US$ Billion) 12th position in the world ranking with

50

100 315

( $ ) • 12th position in the world ranking with domestic market (0.9 % of BR-GDP)

• Forecast of more than12% annual average growth rate by 2010

• Local development represents 34% of the

0

SA an UK ny ce da aly ds ia in na zil

en nd ea ld

Local development represents 34% of the market

• ~ 8,000 companies (94% are SMB)11

S f

US

Japa U

Ger

man

Fran

c

Cana

d

Ita

Net

herla

nd

Aust

ral

Spa

Chi n

Braz

Swed

e

Switz

erla

n

Kore

Rest

of W

or

Software RevenueMarket by Class

(US$ Million)

995

571 Parameterizable Software

Custom Developed Software

2,623Standard Software

Total : US$ 4.2 Billion

Source: http://www.abes.org.br/UserFiles/Image/PDFs/Mercado_BR2008.pdf

Telecom CRM and BusinessIT

Top 5 – Players

Telecom Infra-structure

ProvidersTop 5 – Players

CRM and Business Analytics Software

Top 5 – Players

ITInfra-structure

Providers

ERICSSON

Alcatel-Lucent

Siemens Nokia

SAS

ORACLE

SAP

Cisco

Juniper

Alcatel LucentSiemens-Nokia

Motorola

Nortel

Microsoft

Salesforce.com

Alcatel-Lucent

Huawei

NEC

Billing & Mediation

T 5 Pl

NMS

PSV T l

OSS/BSS ISV

Top 5 – Players

ERICSSON

Comptel

Top 5 – Players

IBM

HP

PSV-Telecom

VÍSENT

LivewareComptel

Convergys

Orga

Harrys

ERICSSON

ORACLE

Suntech

Objective

I lAmdocs ORACLE

Source: TIinside and IDG

Iclass

Macro economic i

Technologyscenario

• Uncertainties• TelCos/CelCos -reducing overall

• IP Consolidation• Convergence• NGN and IN• WiMaxg

investment, specially in infrastructure

• 3G• Digital TV and IPTV

1.Investment based strictly on ROI

(exception: meet demand)DemandDemand RegulatoryRegulatory

(exception: meet demand)

2.Prioritization of services in relation to

the infrastructure

3 S li di ifi i ( i ll f

• Competition

• Network’s Expansion

• Mobility

• Opened Market

• Rules Changed (LGT)

• New Licenses Licitation3.Suppliers diversification (specially for

services providers)

4.Network utilization by Content

• Broadband Applications

• Video and Images

• New Rules for: WiMax

and Digital TV

Providers

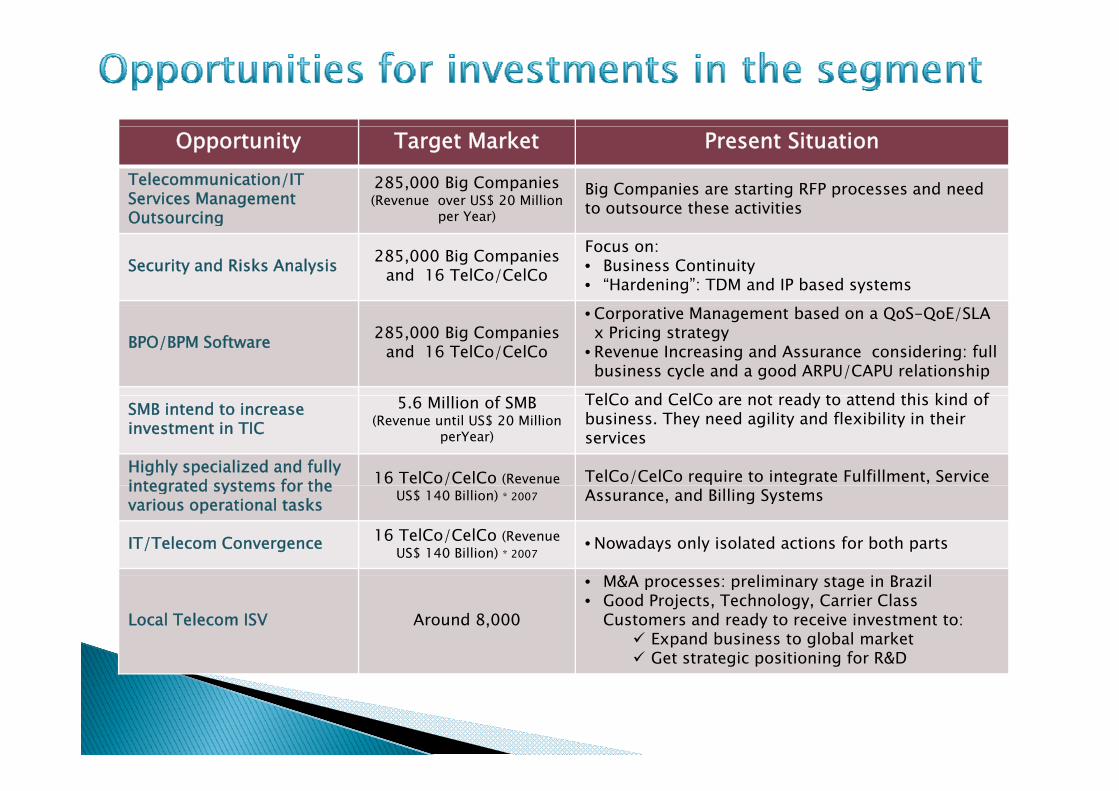

Opportunity Target Market Present SituationTelecommunication/IT Services Management Outsourcing

285,000 Big Companies(Revenue over US$ 20 Million

per Year)

Big Companies are starting RFP processes and need to outsource these activitiesOutsourcing per Year)

Security and Risks Analysis 285,000 Big Companies and 16 TelCo/CelCo

Focus on:• Business Continuity• “Hardening”: TDM and IP based systems

BPO/BPM Software 285,000 Big Companies and 16 TelCo/CelCo

• Corporative Management based on a QoS-QoE/SLAx Pricing strategy

• Revenue Increasing and Assurance considering: full business cycle and a good ARPU/CAPU relationship

T lC d C lC t d t tt d thi ki d fSMB intend to increase investment in TIC

5.6 Million of SMB (Revenue until US$ 20 Million

perYear)

TelCo and CelCo are not ready to attend this kind of business. They need agility and flexibility in their services

Highly specialized and fully integrated systems for the 16 TelCo/CelCo (Revenue TelCo/CelCo require to integrate Fulfillment, Service integrated systems for the various operational tasks

/US$ 140 Billion) * 2007 Assurance, and Billing Systems

IT/Telecom Convergence 16 TelCo/CelCo (RevenueUS$ 140 Billion) * 2007

• Nowadays only isolated actions for both parts

& l l

Local Telecom ISV Around 8,000

• M&A processes: preliminary stage in Brazil• Good Projects, Technology, Carrier Class

Customers and ready to receive investment to:Expand business to global marketGet strategic positioning for R&Dg p g

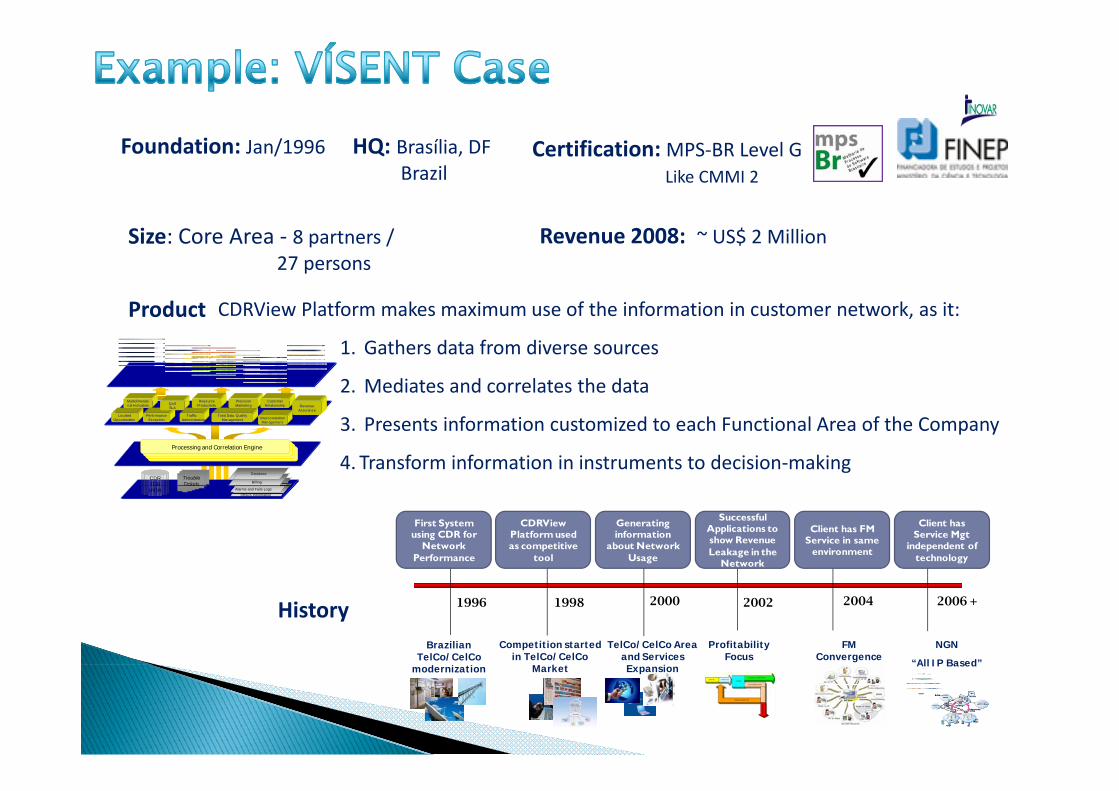

Foundation: Jan/1996 HQ: Brasília, DFBrazil

Certification: MPS‐BR Level GLike CMMI 2

Product CDRVie Platform makes ma im m se of the information in c stomer net ork as it

Size: Core Area ‐ 8 partners / 27 persons

Revenue 2008: ~ US$ 2 Million

Product CDRView Platform makes maximum use of the information in customer network, as it:

1. Gathers data from diverse sources

2. Mediates and correlates the data

3. Presents information customized to each Functional Area of the Company

4. Transform information in instruments to decision‐making

LocatedOpportunities

Multidimensional Indicators

PerformanceException

QoSSLA

Traffic Administration

ResourceProductivity

Processing Correlation Engine

Total Data QualityManagement

PrecisionMarketing

InterconnectionManagement

CustomerRelationship Revenue

Assurance

CDRTDR

TroubleTickets

Database

Billing

Processing and Correlation Engine

TDRIPDR

Tickets

Others InformationAlarms and Fails Logs

Utilizing Counters

Client has Service Mgt

independent of technology

First System using CDR for

Network Performance

CDRView Platform used as competitive

tool

Generating information

about Network Usage

Successful Applications to show Revenue Leakage in the

Network

Client has FM Service in same

environment

HistoryBrazilian

TelCo/CelCod i i

1996 1998

Profitability Focus

20022000

TelCo/CelCo Area and Services E i

FM Convergence

2004

Competition started in TelCo/CelCo

M k t

2006 +

NGN

“All IP Based”modernization ExpansionMarket All IP Based

Present Clients Area: Service Usage, Precision Marketing, Network Performance,

Revenue Assurance, CRM Back Office, and Quality of Service

for TelCo/CelCo: Voice, Data, Messages, and Video based Services

1,000

CDR/day(Million)

900

500

450

350

100

350

200

96 97 98 99 00 01 02 03 04 05 06 07 08 YearsIn production since ...