brazil depaulagermano ism2011

TRANSCRIPT

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 1/30

Brazilian Steel Industry:market structure,

strategies, andperspectives

Dr. Germano Mendes De PaulaFederal University of Uberlândia

March 2011

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 2/30

2

1. Market structure: a supply side outlook

2. Competitive and corporate strategies

3. Medium-term perspectives: a demand side outlook

Agenda

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 3/30

3

Market structure:

a supply side outlook

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 4/30

4

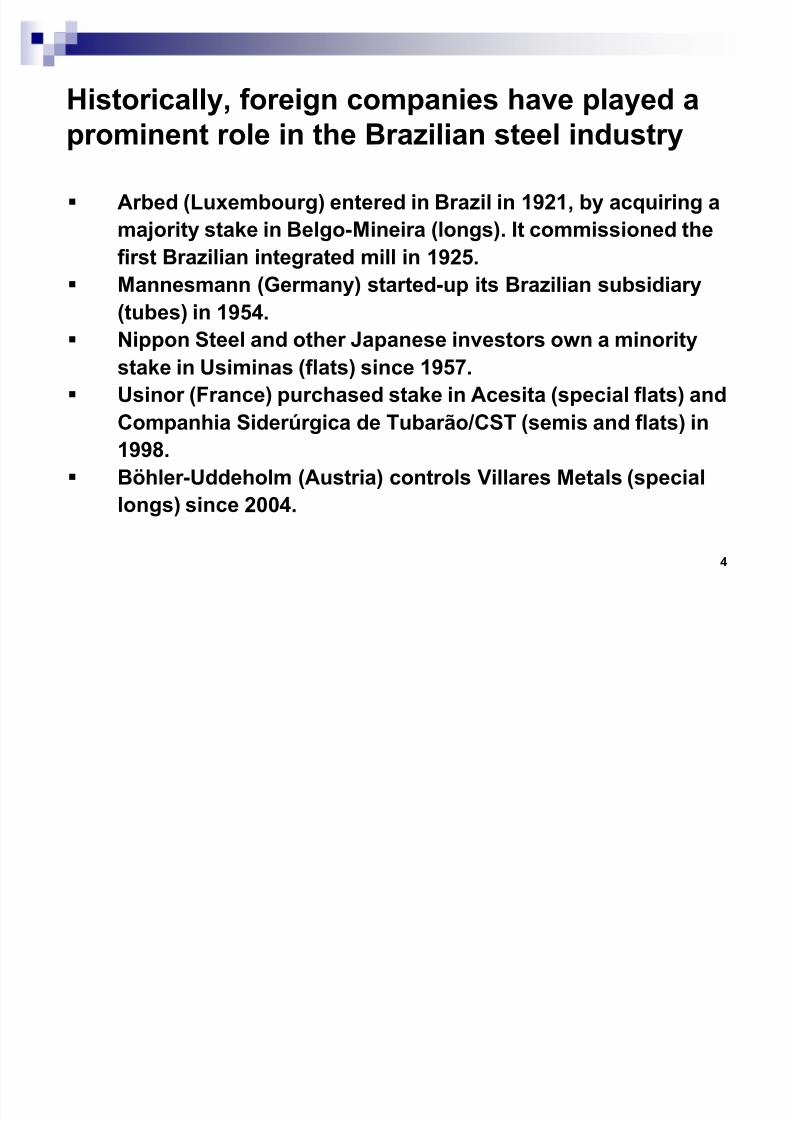

Historically, foreign companies have played a

prominent role in the Brazilian steel industry

Arbed (Luxembourg) entered in Brazil in 1921, by acquiring a

majority stake in Belgo-Mineira (longs). It commissioned the

first Brazilian integrated mill in 1925.

Mannesmann (Germany) started-up its Brazilian subsidiary

(tubes) in 1954.

Nippon Steel and other Japanese investors own a minority

stake in Usiminas (flats) since 1957.

Usinor (France) purchased stake in Acesita (special flats) and

Companhia Siderúrgica de Tubarão/CST (semis and flats) in

1998.

Böhler-Uddeholm (Austria) controls Villares Metals (special

longs) since 2004.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 5/30

5

Others foreigner steelmakers used to take part

in the Brazilian steel industry

Korf (Germany) controlled Fi-El (longs) during 1973-1976 as

well as Pains (longs) along 1976-1994.

Thyssen (Germany) had a minority stake in Gerdau Cosigua

(longs) in the period 1975-1979 and in GalvaSud (galvanizing

line) in 1998-2004.

In CST, Finsider (Italy) was shareholder along the period

1976-1996 and Kawasaki Steel (Japan) from 1976 to 2004.

NatSteel (Singapore) owned shares in Açominas (semis)

during 1998-2002.

Sidenor (Spain) was the largest shareholder of Aços Villares

(special longs) from 2000 to 2006.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 6/30

6

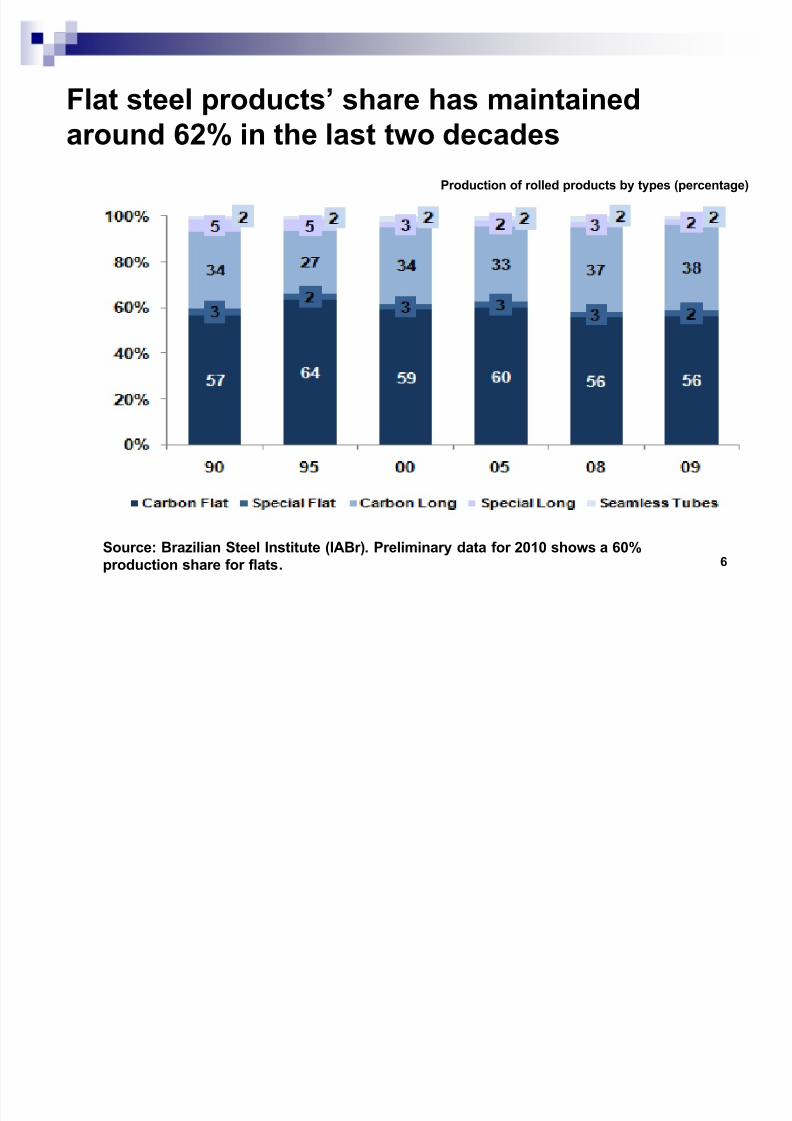

Flat steel products¶ share has maintained

around 62% in the last two decades

Source: Brazilian Steel Institute (IABr).

Preliminary data for 2010

shows a60%

production share for flats.

Production of rolled products by types (percentage)

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 7/30

7

High degree of product specialization, except for

Arcelor Mittal

Source:O

wn elaboration.Votorantim has a relevant stake in Usiminas

.Aperam wasdemerged from Arcelor Mittal in January 2011.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 8/30

8

New battles in the competitive arena, mainly due

to vertical integration and product diversification

Sinobras and Cisam entered into long steel market in 2008.

The first one belongs to the largest Brazilian independent

distributor (Aços Cearense). The owner of the second (Ciafal)

was a pig iron producer and re-roller .

Gusa Nordeste (controlled by Ferroeste, an independent pig

iron producer) is moving into billets and carbon longs in

2011-2012.

CSN is going to jump into carbon long steel market in 2012-

2013. It used to fabricate rails from 1947 to 1996.

Gerdau will become a carbon flat steel producer by 2012-

2013.

Arcelor Mittal had considered to engage into special longs

before the global financial crisis. It is already a SBQ producer

in Argentina.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 9/30

9

Excellent iron ore and tight scrap market explain

the predominance of BOF process

Source: IABr .

Preliminary data for 2010

shows a24%

production share for EAF.

Production of crude steel by process (percentage)

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 10/30

10

Brazil has a long tradition in producing pig iron

by using charcoal

The first Brazilian integrated mills were based on charcoal(Belgo-Mineira Sabará and Belgo-Mineira João Monlevade).

Charcoal integrated mills, mostly in Minas Gerais State:

Aperam Timóteo: 700 ktpy, full operation based oncharcoal from 2012 on;

Arcelor Mittal Juiz de Fora: 360 kpty; Cisam Pará de Minas: 180 ktpy; Gerdau Barão de Cocais: 330 ktpy; Gerdau Divinópolis: 430 kpty; Gusa Nordeste Açailândia: 360 ktpy, forward vertical

integration; Sinobras Marabá: 310 ktpy; Vallourec & Mannesmann Barreiro: 650 kpty; Vallourec & Sumitomo Jeceaba: 600 ktpy, start-up in 2011-

2012.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 11/30

11

Independent pig iron producers showed quite

instable output and export levels

Source: IABr .

163 mini blast furnace owned by independent pig iron producers, with a jointly nominal capacity of 15.6 Mtpy. One two of them (Usipar) are based on coke.

Production and export of pig iron (million tons)

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 12/30

12

Differently from India, the direct reduction has

been not very successful in Brazil

Aços Finos Piratini, a SOE, was the sixth steelworks in theworld to install a direct reduction module. The SL/RN utilizedthermal coal and was in operation from 1973 to 1990.

Usiba commissioned a HyL module in 1974, aiming toconsume natural gas. It was privatized in 1989, being acquiredby Gerdau. It is temporarily shut down since mid 2009.

Purofer module (developed by Thyssen Krupp) was installedin 1977 at Gerdau Cosigua, but faced many problems and itwas shut down in 1979.

Companhia Siderúrgica do Ceará, a project analyzed by Vale,Dongkuk and Danieli, would be based on direct reduction. Theventure was renamed Companhia Siderúrgica do Pecém. Now,the partners are Vale, Dongkuk and Posco; it will be based oncoke blast furnaces.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 13/30

13

Greenfield projects are mainly focus on

exporting semis (slabs, in particular)

Source:O

wn elaboration.Selected projects, of which there is recent publicly availableinformation. Not necessarily all the projects will be implemented, even with delays.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 14/30

14

Brazilian capacity will increase at least 11 Mtpy

until 2015

Source: IABr,C

iti, UBS, BancoN

acional de Desenvolvimento Econômico e Social(BNDES).

Installed crude steel capacity (million tons)

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 15/30

15

C ompetitive and corporate strategies

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 16/30

16

Installed capacities by major players

It is expected that Arcelor M

ittal will announced large investments for flat steel productsalong this year .

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 17/30

17

Steel companies in Brazil have a high degree of

backward vertical integration

*C

SN

controls20%

of Riversdale, with coal assets in South Africa andM

ozambique,while Gerdau owns Cleary Holdings, a Colombian producer of coal and coke.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 18/30

18

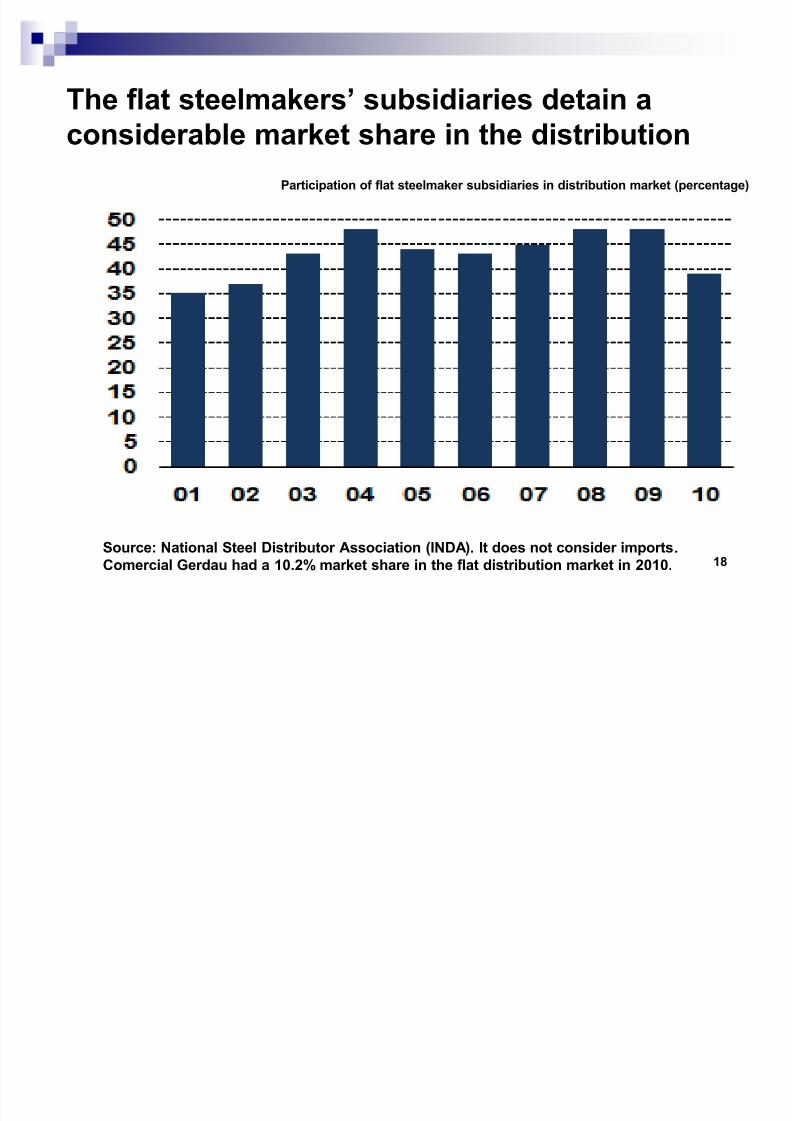

The flat steelmakers¶ subsidiaries detain a

considerable market share in the distribution

Source:N

ational Steel Distributor Association (IN

DA).

It does not consider imports. Comercial Gerdau had a 10.2% market share in the flat distribution market in 2010.

Participation of flat steelmaker subsidiaries in distribution market (percentage)

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 19/30

19

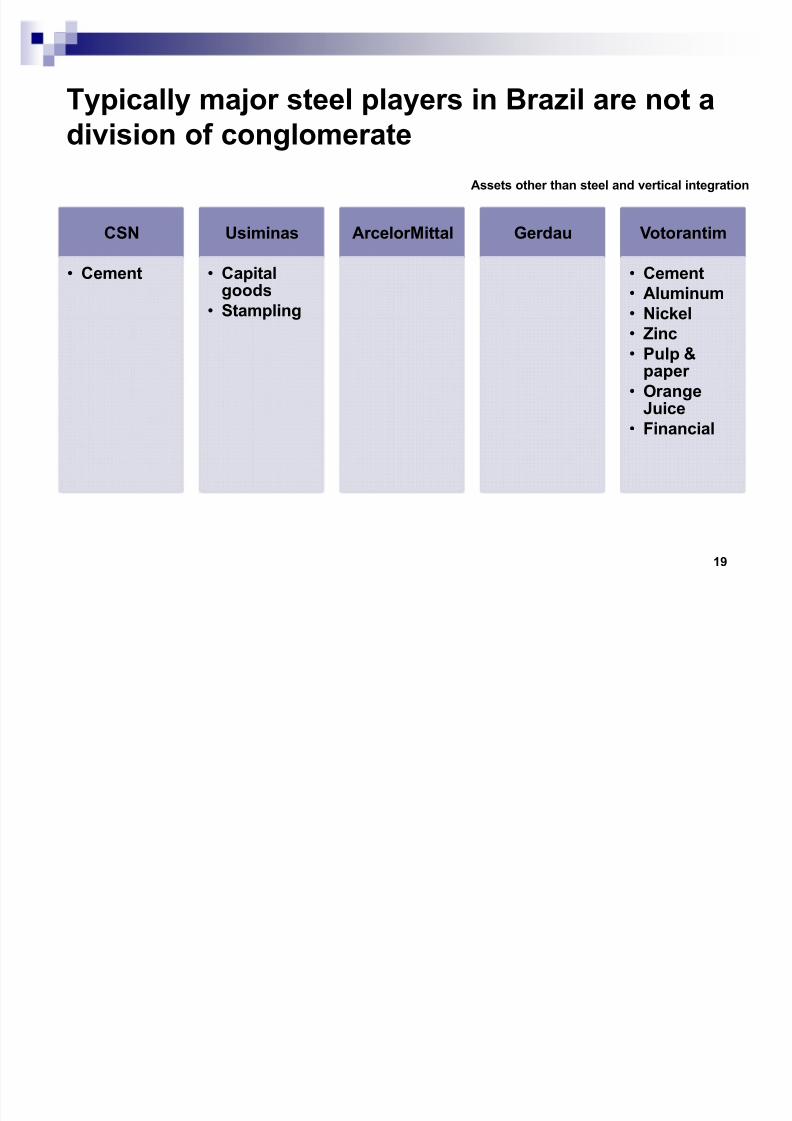

Typically major steel players in Brazil are not a

division of conglomerate

CSN

Cement

Usiminas

Capitalgoods Stampling

Arcelor Mittal Gerdau Votorantim

Cement Aluminum Nickel Zinc Pulp &

paper Orange

Juice Financial

Assets other than steel and vertical integration

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 20/30

20

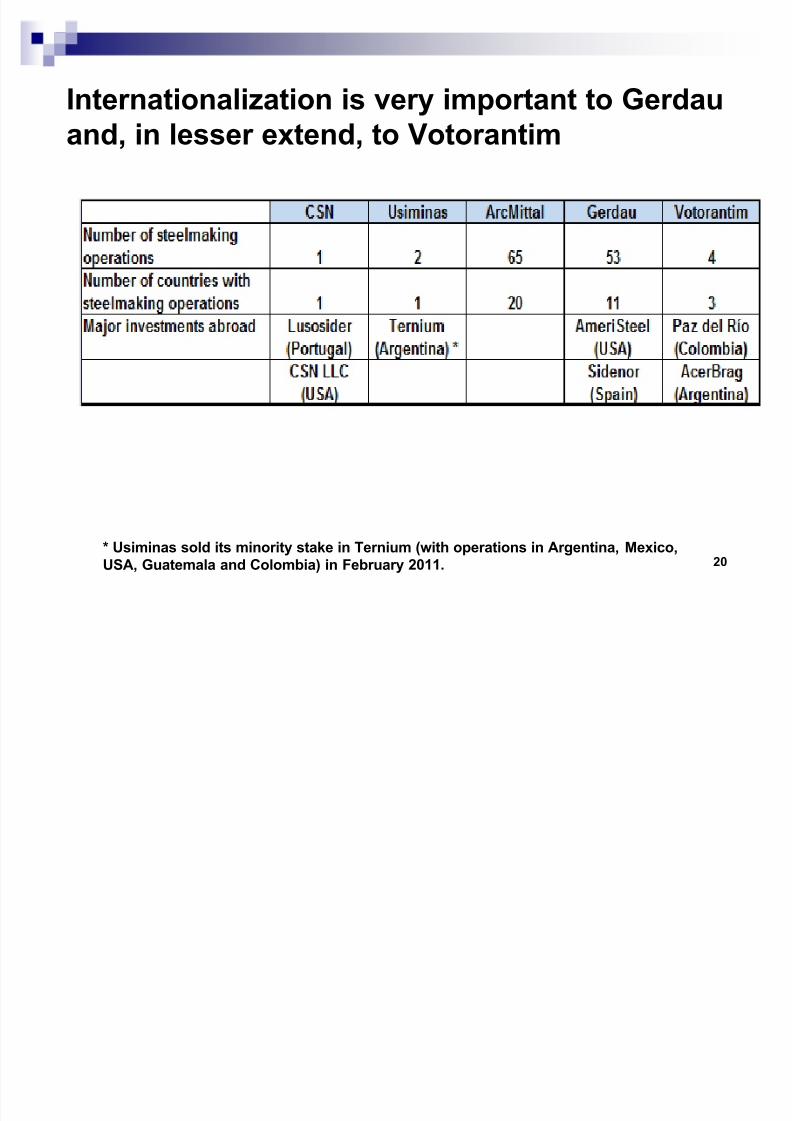

Internationalization is very important to Gerdau

and, in lesser extend, to Votorantim

* Usiminas sold its minority stake in Ternium (with operations in Argentina,M

exico,USA, Guatemala and Colombia) in February 2011.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 21/30

21

Medium-term perspectives

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 22/30

22

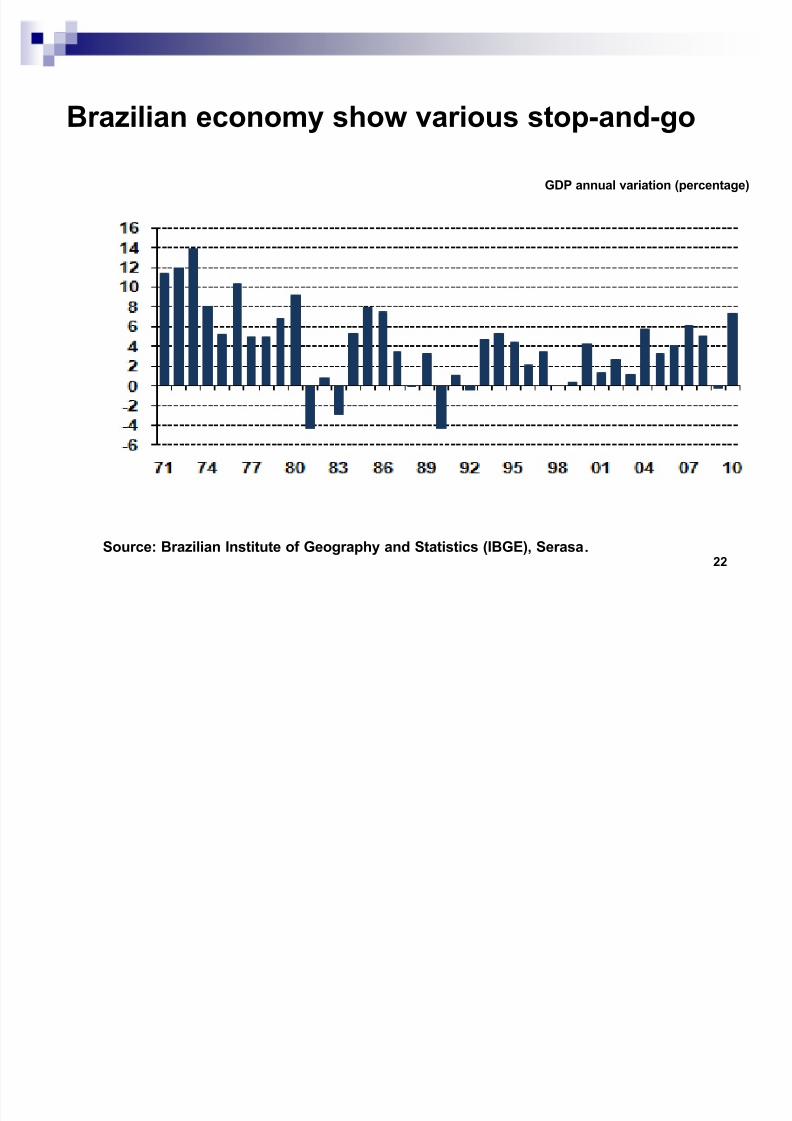

Brazilian economy show various stop-and-go

Source: Brazilian Institute of Geography and Statistics (IBGE), Serasa.

GDP annual variation (percentage)

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 23/30

23

Brazilian steel apparent consumption isextremely instable«nerves of steel are

essential!

Source: IGBE, Serasa, IABr .

GDP and steel apparent consumption annual variation (percentage)

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 24/30

24

Positive factors for steel consumption in Brazil

GDP is expect to grow 4.5% per year in 2011-2020.

Credit as a proportion of GDP has increased from 28% in 2005

to 47% in 2010, fostering the automotive and construction

industries.

The emergence of the ³new middle class´. From 2010 to 2020,

it is expected that families share in the GDP will enlarge from

63% to 67%. The upper classes (higher than US$ 320 per

month) will maintain its 35%. The other ones will raise from

28% to 32%.

Petrobras (oil & gas) has announced investments of US$ 224

billion for period 2010-2014.

The need to develop infrastructure, including for World

Football Cup 2014 and Olympic Games 2016.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 25/30

25

Negative factors for steel consumption in Brazil

Brazil has a large urbanization ratio: 86%.

Low level of investments: Gross Fixed Capital Formation

(GFCF) varied between 15% and 19% during 2002-2010 period.

High interest rates. Today, the nominal basic interest rate is

11.75%.

Appreciated exchange rate, reducing the competitiveness of

industrial sector and stimulating the indirect steel imports.

High bureaucratic governmental procedures, in particular for

environmental permits.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 26/30

26

Flat steel products¶ share has maintained

around 59% in the last two decades

Source: IABr . Preliminary data for 2010 shows a 60% market share for flats. There was amethodological change in 1996.

Apparent consumption of rolled products by types (percentage)

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 27/30

27

Construction and automotive have improved

their relevance

Source: IABr .

Apparent consumption of rolled products by consuming sectors (percentage)

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 28/30

28

Brazilian demand will amplify at least 7 Mtpy

until 2015

Source: IABr, Citi, UBS, BNDES.

Apparent consumption of rolled products (million tons)

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 29/30

29

Final considerations

Greenfield projects, led by foreign companies, are focused

on semis, whereas the incumbents prefer to amplify its rolled

capacity.

There will be a increasing competition in each marketsegment, mainly because of the investments carried out by

current players and, in lesser extend, by vertical integration

of related producers.

Due to the higher input prices, the steelmakers were engaged

into enlarging its backward vertical integration degree.

Domestic vertical integration is the name of the game now.

However, internationalization is a top priority for Gerdau.

Rolled products continue to be a domestic market oriented

business.

8/3/2019 Brazil DePaulaGermano ISM2011

http://slidepdf.com/reader/full/brazil-depaulagermano-ism2011 30/30

Thank you!

30