bob economics - market outlook cytd20 21dec20

TRANSCRIPT

INDIA ECONOMICS

@2020 Bank of Baroda. All rights reserved

Important disclosures are provided at the end of this report.

MARKET OUTLOOK 21 December 2020

Year of rollercoaster ride

2020 was one of the worst years for global economy but one of the best years

for NASDAQ (5th highest since inception). Even in India, technology stocks

outperformed. Global yields fell and commodity prices increased. US$ too

fell. 2021 should see the trend continuing as pivot of growth shifts to Asia.

Higher commodity prices will drive inflation up. India’s retail inflation will

remain above 4% and yields will inch up as RBI starts to withdraw liquidity

support gradually (CRR cut upto Mar’21) and credit growth revives.

Sameer Narang +91 22 6698 5713 [email protected] Sonal Badhan

Aditi Gupta

Dipanwita Mazumdar [email protected]

Jahnavi

KEY HIGHLIGHTS

Global growth plunged, technology stocks

outperformed

Commodity prices inching up, US$ weak

Yields fall globally, central banks to remain

accommodative

India and global growth to revive, PLI scheme

and digitisation to benefit India

What a year: The 2020 pandemic, 9th since 1700, brought down global growth

from 2.8% in 2019 to a contraction of 4.4%. Fiscal deficits expanded globally

led by US at 19% and Europe at 10%. Central Banks stepped up stimulus by

bringing rates to record lows and undertaking balance sheet expansion. US Fed

increased its asset size by 14.8% of GDP in a year, and India by 6.7% (till

Dec’20).

Financial assets re-priced: Portfolio allocations moved away from debt into

equities in the US by more than US$ 200bn. US equity markets are higher in the

year led by 40% return on the tech heavy NASDAQ index. Even in India, tech

stocks have given a 39% return during the year. FPI inflows into Indian equity

markets during CY20 are at US$ 21.5bn while debt outflows are US$ 13.8bn.

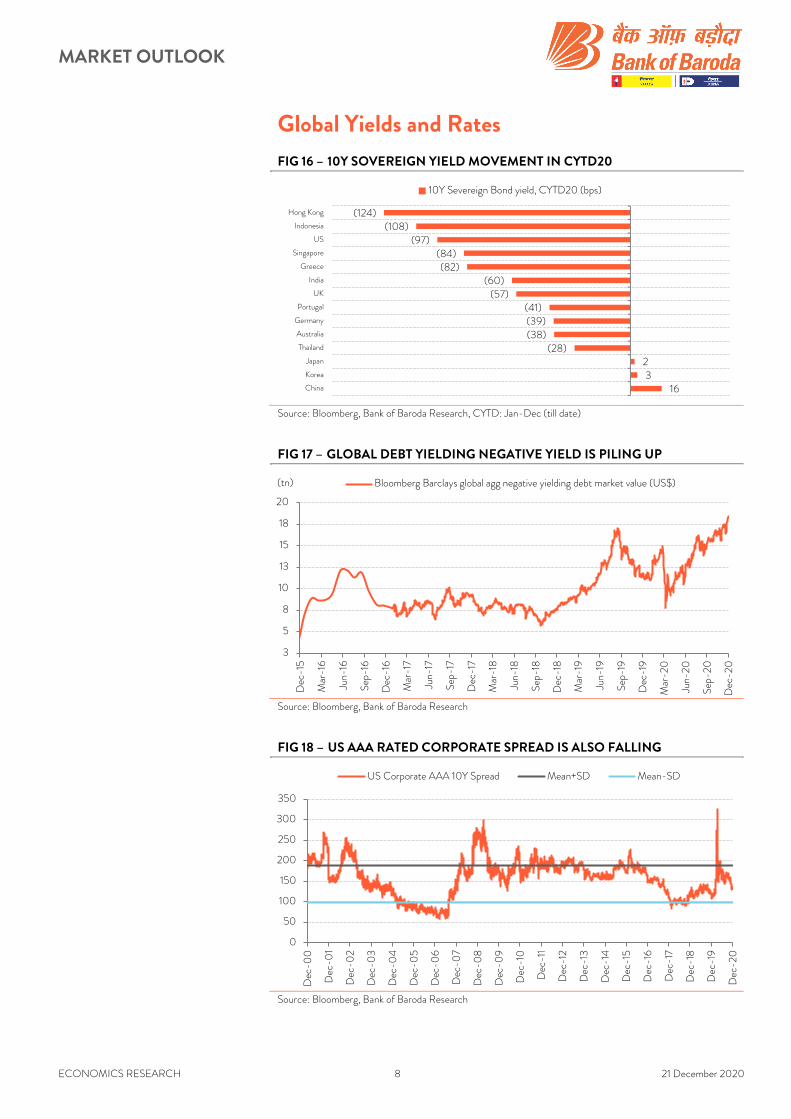

Global yields at rock bottom: As much as US$ 18tn of global debt are yielding a

negative return. Junk bond yields in the US have fallen to lowest level since

Feb’20. Even in India, RBI’s liquidity support has worked wonders with spread of

corporate bond yields over Gsec for prime borrowers falling to levels not seen

since 2010. For AAA borrowers (3yr) spread over Gsec is now less than 20bps.

What will change in 2021: Global liquidity conditions are likely to remain

accommodative, but yields may start to inch up as global growth revives. DXY

index will continue to under-perform. Commodity prices will remain firm as Asia

will continue to drive growth. Inflation will gradually inch up. Services inflation will

pick up gradually. Equity markets will continue to inch up as growth revives.

India’s growth at 8.8% in FY22: Led by revival in domestic consumption, India’s

growth will revive to 8.8% in FY22. Government’s PLI scheme is positive for

exports. So is flow of work to Indian IT firms. Inflation will remain a teething issue

(4.5% in FY22 versus 6.5% in FY21) because of higher global commodity prices.

Yields have bottomed out and will steadily inch upwards as credit growth revives.

MARKET OUTLOOK

ECONOMICS RESEARCH 2 21 December 2020

Contents

Macro Scenario ............................................................................................ 3

Policy Table .................................................................................................. 5

Global Equity Indices: .................................................................................. 6

India Scenario ............................................................................................... 7

Global Yields and Rates ............................................................................... 8

Indian Rates ............................................................................................... 10

Global Currencies and Commodities ..........................................................11

MARKET OUTLOOK

ECONOMICS RESEARCH 3 21 December 2020

Macro Scenario

FIG 1 – IMF PROJECTION SHOWS GDP OF MAJOR

ECONOMIES TO CONTRACT SHARPLY IN CY20 FIG 2 – BALANCE SHEET OF MAJOR ECONOMIES ARE

SKYROCKETING

Source: IMF, Bank of Baroda Research Note: US growth estimates are

FOMC’s projection, FY21 estimates of India are RBI’s projection and FY22

estimates are author’s own calculation

Source: Bloomberg, Bank of Baroda Research

FIG 3 – MANUFACTURING PMI FIG 4 – SERVICES PMI

Source: CEIC, Bank of Baroda Research Source: CEIC, Bank of Baroda Research

FIG 5 – EXPORTS GROWTH COUNTRYWISE FIG 6 – IMPORTS GROWTH COUNTRYWISE

Source: CEIC, Bloomberg, Bank of Baroda Research Source: CEIC, Bloomberg, Bank of Baroda Research

(2.4%)

(8.3%)(9.8%)

(5.3%)

1.9%

(7.5%)

4.2% 5.2% 5.9%

2.3%

8.2% 8.8%

(15%)

(10%)

(5%)

0%

5%

10%

US Euro Area UK Japan China India

CY20 CY21

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

0

100

200

300

400

500

600

700

800

Dec-03

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Dec-15

Dec-16

Dec-17

Dec-18

Dec-19

Dec-20

BoJ balance sheet (JPY tn)

Fed balance sheet (US$ bn) (R)

27

3642

3338

5652

58 5650

0

10

20

30

40

50

60

70

India China US ISM Eurozone Japan

Min Current* Manufacturing PMI

5

30

42

12

36

5456 56

47 47

0

10

20

30

40

50

60

India China US Eurozone Japan

Min Current* Services PMI

14.8%

(5.9%)

(7.9%)

(13.3%)

(15.4%)

(16.4%)

(17.1%)

(22.6%)

(25%) (15%) (5%) 5% 15%

China

Indonesia

Brazil

Japan

US

UK

India

Russia

Exports, CYTD20

(2%)

(7%)

(10%)

(13%)

(14%)

(15%)

(18%)(28%)

(30%) (20%) (10%) 0%

China

Russia

US

Japan

UK

Brazil

Indonesia

India

Imports, CYTD20

MARKET OUTLOOK

ECONOMICS RESEARCH 4 21 December 2020

FIG 7 – INFLATION PROJECTION COUNTRYWISE

SHOWS INDIA AN OUTLIER FIG 8 – FISCAL DEFICIT AS % OF GDP COUNTRYWISE

Source: IMF, Bank of Baroda Research, Note: US CPI are projections of

FOMC, India print is author’s own calculation Source: IMF, Bank of Baroda Research

1.2%

0.4%0.9% 0.2%

3.0%

6.5%

1.8%

0.9%0.2% 0.3%

2.7%

4.5%

0%

1%

2%

3%

4%

5%

6%

7%

US Euro Area UK Japan China India

CYTD20 CY21

1.9

(0.6)

(6.3)

(8.2)

(3.3)

(2.2)

(6.0)

(6.3)

(5.3)

(10.1)

(11.9)

(13.1)

(14.2)

(16.5)

(16.8)

(18.7)

(22) (17) (12) (7) (2) 3

Russia

Euro Area

China

India

Japan

UK

Brazil

US

(%)

2020 2019

MARKET OUTLOOK

ECONOMICS RESEARCH 5 21 December 2020

Policy Table

FIG 9 – GLOBAL CENTRAL BANKS ARE ON MONETARY EASING CYCLE

Country Current inflation rate

(%)

Current policy rate

(%)

CY19

(change in bps)

CYTD20

(change in bps)

Direction of policy rate

in CYTD20

Turkey 14.03 15.00 (1,200) 300 �

Germany (0.30) 0 0 0 -

Japan (0.90) (0.10) 0 0 -

China (0.50) 4.35 0 0 -

UK 0.30 0.10 0 (65) �

Australia 0.70 0.1 (75) (65) �

Korea 0.60 0.5 (50) (75) �

Thailand (0.41) 0.5 (50) (75) �

India 6.93 4 (135) (115) �

Indonesia 1.59 3.75 (100) (125) �

Malaysia (1.50) 1.75 (25) (125) �

US 1.20 0.25 (75) (150) �

Russia 4.40 4.25 (150) (200) �

Phillipines 3.30 2.00 (75) (200) �

Brazil 4.31 2.00 (200) (250) �

Mexico 3.33 4.25 (100) (300) �

Source: Bloomberg, Bank of Baroda Research

MARKET OUTLOOK

ECONOMICS RESEARCH 6 21 December 2020

Global Equity Indices:

FIG 10 – CYTD20 CHANGE OF MAJOR EQUITY INDICES

Source: Bloomberg, Bank of Baroda Research, CYTD: Jan-Dec (till date)

FIG 11 – PERFORMANCE OF MAJOR STOCKS OF NASDAQ

Source: Bloomberg, Bank of Baroda Research, CYTD: Jan-Dec (till date)

FIG 12 – VOLATILITY IN EQUITY INDICES IS PACIFYING

Source: Bloomberg, Bank of Baroda Research

33%18%18%

12%8%8%

7%6%

(1%)(7%)(7%)(7%)(7%)

(10%)(11%)

(13%)

Korea

Japan

China

MSCI EM Equity

India

Germany

Australia

US

Portugal

Hong Kong

Thailand

Greece

Indonesia

Russia

Singapore

UK

Equity Indices, % change CYTD20

731%126%

119%

73%

73%

65%

52%

39%

35%

29%

13%

(30%) 20% 70% 120% 170%

Tesla

NVIDIA Corp

Paypal

Amazon

Apple

Netflix

Adobe

Microsoft

Comcast

NASDAQ-Top 10 Stocks, YTD

5

25

45

65

85

10

30

50

70

90

Dec-19

Feb-20

Mar-20

May-20

Jun-20

Aug-20

Sep-20

Oct-20

Dec-20

NSE volatility index Chicago board options exchange volatility index (R)

MARKET OUTLOOK

ECONOMICS RESEARCH 7 21 December 2020

India Scenario

FIG 13 – SECTORWISE STOCKS PERFORMANCE FIG 14 – SMALL CAP ROSE THE MOST

Source: Bloomberg, Bank of Baroda Research, CYTD: Jan-Dec (till date) Source: Bloomberg, Bank of Baroda Research, CYTD: Jan-Dec (till date)

FIG 15 – PERFORMANCE OF MAJOR STOCKS IN THE DOMESTIC MARKET

Source: Bloomberg, Bank of Baroda Research, CYTD: Jan-Dec (till date)

39.1%

18.6%

12.2%

9.8%

9.0%

7.9%

5.0%

(2.4%)

(4.0%)

(20%) (10%) 0% 10% 20% 30% 40% 50%

Teck

Cons durables

Auto

Cap goods

Metal

Power

Realty

Oil & Gas

BANKEX

Performance of majore sectors in BSE, CYTD20

29.7%

18.9%

13.8%

12.8%

BSE SmallCap

BSE MidCap

BSE

BSE LargeCap

Performances according to mcap, CYTD20

63%57%

46%38%

34%33%33%32%

28%27%

24%24%22%21%

16%12%11%

5%3%3%2%

(1%)(2%)(4%)

(10%)(13%)

(19%)(19%)

(23%)(40%)

Infosys Ltd

HCL Technologies Ltd

Asian Paints Ltd

Mahindra & Mahindra LTD

Tata Steel Ltd

Sun Pharma Ltd

Reliance Industries Ltd

TCS

Titan Co Ltd

Ultra tech Cement Ltd

Nestle India Ltd

Bajaj Finance Ltd

Tech Mahindra Ltd

HUL

Kotak Mahindra Bank Ltd

Bharti Airtel Ltd

HDFC Bank Ltd

Bajaj Auto Ltd

HDFC

Maruti Suzuki India Ltd

Powere Grid Corp of India, LTD

L&T

Bajaj Finserv ltd

ICICI Bank Ltd

ITC Ltd

NTPC Ltd

State Bank of India

Axis Bank Ltd

ONGC

IndusInd Bank Ltd

Performance of major stocks of Sensex, CYTD20

MARKET OUTLOOK

ECONOMICS RESEARCH 8 21 December 2020

Global Yields and Rates

FIG 16 – 10Y SOVEREIGN YIELD MOVEMENT IN CYTD20

Source: Bloomberg, Bank of Baroda Research, CYTD: Jan-Dec (till date)

FIG 17 – GLOBAL DEBT YIELDING NEGATIVE YIELD IS PILING UP

Source: Bloomberg, Bank of Baroda Research

FIG 18 – US AAA RATED CORPORATE SPREAD IS ALSO FALLING

Source: Bloomberg, Bank of Baroda Research

1632

(28)(38)(39)(41)

(57)(60)

(82)(84)

(97)(108)

(124)

China

Korea

Japan

Thailand

Australia

Germany

Portugal

UK

India

Greece

Singapore

US

Indonesia

Hong Kong

10Y Severeign Bond yield, CYTD20 (bps)

3

5

8

10

13

15

18

20

Dec-15

Mar-16

Jun-16

Sep-16

Dec-16

Mar-17

Jun-17

Sep-17

Dec-17

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

Jun-19

Sep-19

Dec-19

Mar-20

Jun-20

Sep-20

Dec-20

(tn) Bloomberg Barclays global agg negative yielding debt market value (US$)

0

50

100

150

200

250

300

350

Dec-00

Dec-01

Dec-02

Dec-03

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Dec-15

Dec-16

Dec-17

Dec-18

Dec-19

Dec-20

US Corporate AAA 10Y Spread Mean+SD Mean-SD

MARKET OUTLOOK

ECONOMICS RESEARCH 9 21 December 2020

FIG 19 – US JUNK BOND YIELD

Source: Bloomberg, Bank of Baroda Research

FIG 20 – US MORTGAGE RATE

Source: Bloomberg, Bank of Baroda Research

0

5

10

15

20

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Dec-15

Dec-16

Dec-17

Dec-18

Dec-19

Dec-20

Bloomberg Barclays US Corporate High Yield Average OAS

1%

2%

3%

4%

5%

6%

Dec-10

Jun-11

Dec-11

Jun-12

Dec-12

Jun-13

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Jun-18

Dec-18

Jun-19

Dec-19

Jun-20

Dec-20

US 30Y Mortgage rates US 30Y Sovereign bond yield

MARKET OUTLOOK

ECONOMICS RESEARCH 10 21 December 2020

Indian Rates

FIG 21 – CORP SPREAD FOR 3Y AAA RATED PAPERS

BELOW ITS MEAN REVERSION LEVEL FIG 22 – FOR 10Y AAA RATED CORPORATE PAPERS AS

WELL IT IS APPROACHING ITS LOWS

Source: Bloomberg, Bank of Baroda Research Source: Bloomberg, Bank of Baroda Research

FIG 23 – SPREAD OF NBFC AAA RATED IS ALSO

BELOW ITS MEAN REVERSION LEVEL

FIG 24 – FOR 10Y AAA RATED NBFC PAPER, THE

SPREAD IS ALSO SIGNIFICANTLY LOWER

Source: Bloomberg, Bank of Baroda Research Source: Bloomberg, Bank of Baroda Research

FIG 25 – INR SWAP 3-YR FIG 26 – INR SWAP 10-YR

Source: Bloomberg, Bank of Baroda Research Source: Bloomberg, Bank of Baroda Research

0

50

100

150

200

250

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Jun-18

Dec-18

Jun-19

Dec-19

Jun-20

Dec-20

Average traded spreads of corporates for 3Y AAA

Mean+SD

Mean-SD

0

30

60

90

120

150

180

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Jun-18

Dec-18

Jun-19

Dec-19

Jun-20

Dec-20

Average traded spreads of corporates for 10Y AAA

Mean+SD

Mean-SD

0

50

100

150

200

250

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Jun-18

Dec-18

Jun-19

Dec-19

Jun-20

Dec-20

Average traded spreads of NBFCs for 3Y AAA

Mean+SD

Mean-SD

0

50

100

150

200

Dec-13

Jun-14

Dec-14

Jun-15

Dec-15

Jun-16

Dec-16

Jun-17

Dec-17

Jun-18

Dec-18

Jun-19

Dec-19

Jun-20

Dec-20

Average traded spreads of NBFCs for 10Y AAA

Mean+SD

Mean-SD

3

5

7

9

11

Dec-00

Dec-02

Dec-04

Dec-06

Dec-08

Dec-10

Dec-12

Dec-14

Dec-16

Dec-18

Dec-20

INR Swap 3Y Mean+SD Mean-SD

3

5

7

9

11

Dec-04

Dec-05

Dec-06

Dec-07

Dec-08

Dec-09

Dec-10

Dec-11

Dec-12

Dec-13

Dec-14

Dec-15

Dec-16

Dec-17

Dec-18

Dec-19

Dec-20

INR Swap 10Y Mean+SD Mean-SD

MARKET OUTLOOK

ECONOMICS RESEARCH 11 21 December 2020

Global Currencies and Commodities

FIG 27 – MOVEMENT OF MAJOR CURRENCIES, CYTD20

Source: Bloomberg, Bank of Baroda Research

FIG 28 – FX RESERVES ACCRETION, CYTD20

Source: Bloomberg, Bank of Baroda Research

FIG 29 – EQUITY IN CYTD20 FIG 30 – DEBT IN CYTD20

Source: Bloomberg, Bank of Baroda Research Source: Bloomberg, Bank of Baroda Research

9.3

8.6

6.5

5.9

5.3

5.2 5.1

2.0

1.6 1.4

1.3

0.5 (1.7)

(3.0)

(6.6)

(15.5)

EUR

AUD

CNY

NZD

PHP

KRW

JPY

GBP

CAD

SGD

MYR

THB

IDR

INR

DXY

RUB

CYTD20 change (%)

121

71

51

33

20

17

3

2

2

1

(3)

(3)

(20) 0 20 40 60 80 100 120 140

India

China

Japan

Hong Kong

Euro Area

Mexico

Indonesia

U.K

US

Germany

South Africa

Brazil

(bn)

Forex Reserves accretion, YTD

228.1110.1104.0

21.517.312.3

(3.1)(4.6)(8.1)

(11.8)(16.1)

(19.2)

US

Euro Area

China

India

UK

Russia

Indonesia

Turkey

South Africa

Italy

Germany

Taiwan

Net FII Equity, YTD

(US$ bn) 310.5119.3

49.620.29.63.72.7

(3.9)(6.9)

(13.8)(15.2)

(307.7)

Euro Area

China

Germany

UK

Russia

Philippines

Malaysia

Brazil

Turkey

India

Italy

USNet FII Debt

(US$ bn)

MARKET OUTLOOK

ECONOMICS RESEARCH 12 21 December 2020

FIG 31 – MOVEMENT OF MAJOR ASSET CLASSES

Source: Bloomberg, Bank of Baroda Research

17.6%

9.8%

(5.3%)

(1.0%)

(8.9%)

(6.0%)

(10.5%)

50.4%

26.8%

1.3%

(0.6%)

(1.9%)

(3.9%)

(33.2%)

(40%) (20%) 0% 20% 40% 60%

Precious metal index

Gold

MSCI EM equity

MSCI EM currency

Roger Agri index

CRB index

Brent

CYTD20 CY19

MARKET OUTLOOK

ECONOMICS RESEARCH 13 21 December 2020

Disclaimer

The views expressed in this research note are personal views of the author(s) and do not necessarily reflect the views of Bank of Baroda. Nothing contained in this

publication shall constitute or be deemed to constitute an offer to sell/ purchase or as an invitation or solicitation to do so for any securities of any entity. Bank of Baroda

and/ or its Affiliates and its subsidiaries make no representation as to the accuracy; completeness or reliability of any information contained herein or otherwise provided

and hereby disclaim any liability with regard to the same. Bank of Baroda Group or its officers, employees, personnel, directors may be associated in a commercial or

personal capacity or may have a commercial interest including as proprietary traders in or with the securities and/ or companies or issues or matters as contained in this

publication and such commercial capacity or interest whether or not differing with or conflicting with this publication, shall not make or render Bank of Baroda Group

liable in any manner whatsoever & Bank of Baroda Group or any of its officers, employees, personnel, directors shall not be liable for any loss, damage, liability whatsoever

for any direct or indirect loss arising from the use or access of any information that may be displayed in this publication from time to time.

Visit us at www.bankofbaroda.in

For further details about this publication, please contact:

Economics Research Department

Bank of Baroda

+91 22 6698 5713