board of directors the state of the monadnock...

TRANSCRIPT

“…to raise new ideas and improve policy debates throu gh quality information and analysis on issues shaping New Hamp shire’s future.”

The State of the Monadnock Region

Dennis Delay toGreater Keene Chamber of Commerce

Tuesday, September 15, 2015

Board of DirectorsJames Putnam, Chair

David Alukonis

Eric Herr

Dianne Mercier

Catherine A. Provencher

Todd I. Selig

Michael Whitney

Daniel Wolf

Martin L. Gross, Chair Emeritus

Directors Emeritus

William H. Dunlap

Sheila T. Francoeur

Stuart V. Smith, Jr.

Donna Sytek

Brian F. Walsh

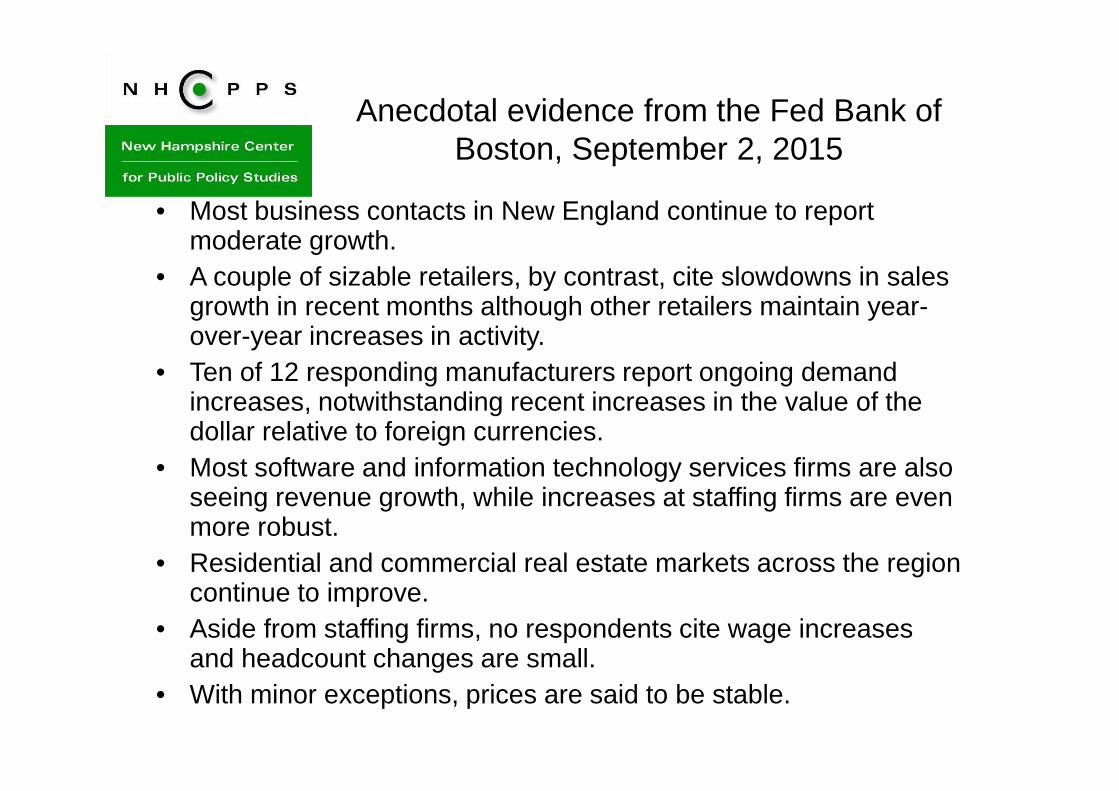

Anecdotal evidence from the Fed Bank of Boston, September 2, 2015

• Most business contacts in New England continue to report moderate growth.

• A couple of sizable retailers, by contrast, cite slowdowns in sales growth in recent months although other retailers maintain year-over-year increases in activity.

• Ten of 12 responding manufacturers report ongoing demand increases, notwithstanding recent increases in the value of the dollar relative to foreign currencies.

• Most software and information technology services firms are also seeing revenue growth, while increases at staffing firms are even more robust.

• Residential and commercial real estate markets across the region continue to improve.

• Aside from staffing firms, no respondents cite wage increases and headcount changes are small.

• With minor exceptions, prices are said to be stable.

NH

–Less of a decline than U

S,

but a slower recovery

92.0

94.0

96.0

98.0

100.0

102.0

104.0

106.0

Jan-07May-07Sep-07Jan-08May-08Sep-08Jan-09May-09Sep-09Jan-10May-10Sep-10Jan-11May-11Sep-11Jan-12May-12Sep-12Jan-13May-13Sep-13Jan-14May-14Sep-14Jan-15May-15

Dec 2007 =100Index of Total N

onFarm

Em

ployment

US

NH

MA

New

Ham

pshire

United S

tates

Massachusetts

Manufacturing, construction and financial activities have not

recovered, government shrinks

Source: NH Economic and Labor Market Information Bureau

-7,400

-2,100 -2,700-3,500

3,100 3,700

1,200

-4,600

6001,500

3,900

1,500

5,700

3,100 2,600

-1,500

-10,000

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

Change in New Hampshire Jobs

Dec 08 to Dec 11

Dec 11 to Dec 14

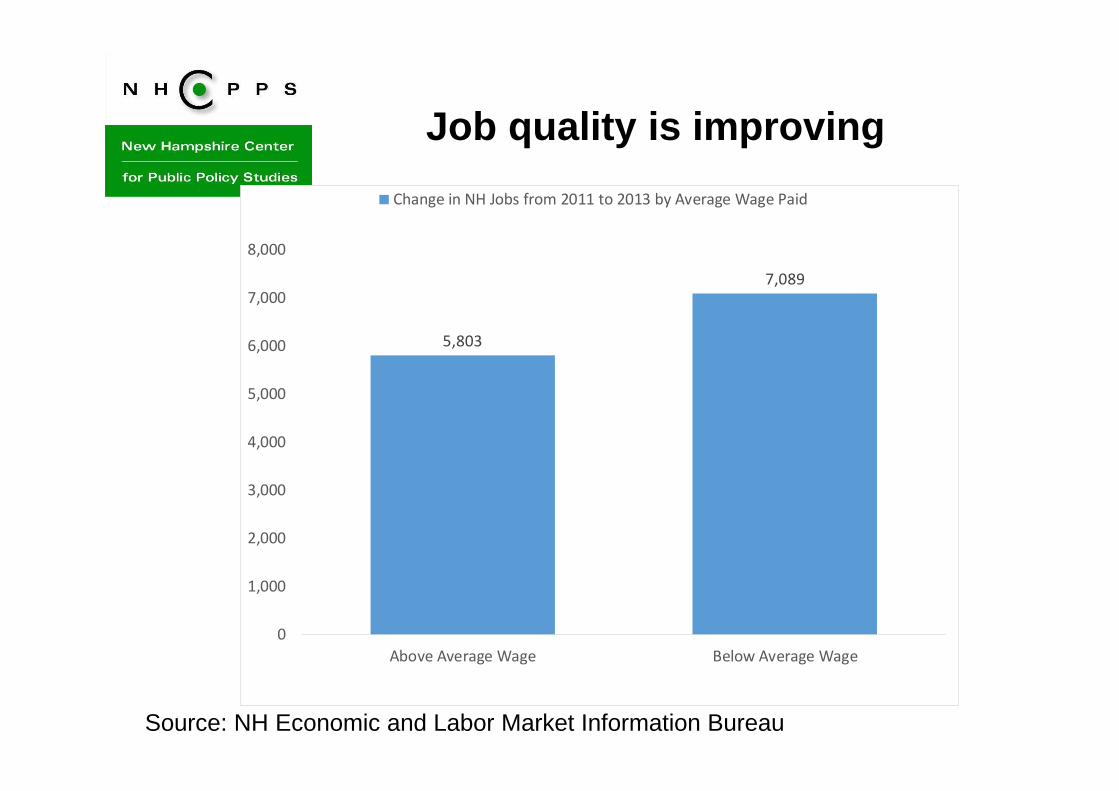

Job quality is improving

Source: NH Economic and Labor Market Information Bureau

5,803

7,089

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Above Average Wage Below Average Wage

Change in NH Jobs from 2011 to 2013 by Average Wage Paid

Unemployment Rate Declining

Source: NH Economic and Labor Market Information Bureau

Monadnock Job Profile

Source: NH Economic and Labor Market Information Bureau

Where people work in Cheshire County

Source: On the Map, US Census Bureau

Where people live in Cheshire County

Source: On the Map, US Census Bureau

NH Residential Real Estate Sales Up

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

0

5,000

10,000

15,000

20,000

25,000

19981999 2000 2001 2002 200320042005 2006 2007 2008 200920102011 2012 2013 2014 2015

NH Single-Family Residential Home Sales and Price (MLS)Source: NH Association of REALTORS

Units sold Median Price

Median Home Price

Number of Units Sold

Decline from the Peak:Sales -40% from 2004Price -25% from 2005

2015 YTD thru May.

Recovery in Cheshire County mirrors state real estate recovery

New

Ham

pshire Hom

e Building

0

5,000

10,000

15,000

20,000

25,00001/6901/7001/7101/7201/7301/7401/7501/7601/7701/7801/7901/8001/8101/8201/8301/8401/8501/8601/8701/8801/8901/9001/9101/9201/9301/9401/9501/9601/9701/9801/9901/0001/0101/0201/0301/0401/0501/0601/0701/0801/0901/1001/1101/1201/1301/1401/15

Twelve Month Average At Annual RatesM

onthly Housing P

ermits in N

ew H

ampshire January 19

70 to July 2015G

rey boxes represent recessionary periods

NH Foreclosures – Worst is Over?

0

100

200

300

400

500

600

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Source: Real Data Corp. compiled by NH Housing

NH Monthly Foreclosure Deeds

Actual Trend

1414

Rental Prices Have Continued to Rise

New Hampshire Rents – NHHFA Surveys

Declines in Prices and Interest Rates Affect Affordability

But…….

• NH’s Young households are burdened by highest level of student debt in the Nation;

• Lending standards are more rigorous—Qualifying Mortgage, 43% debt to income limit, etc.;

• With rents rising and mediocre job quality, more difficult to save and qualify;

• Nearly 20,000 foreclosed units in past several years in the state—some will not qualify;

• Lack of liquidity is keeping boomers in larger houses than they need;

• Prices and interest rates are rising in past several months, blunting recent affordability improvements.

As Elder population rises

17

178,166

144,472

179,178

225,961

178,243

96,762

56,745

24,761

160,495 160,633177,249

159,044

201,565

184,617

102,676

35,808

0

50,000

100,000

150,000

200,000

250,000

15 to 24 25 to 34 35 to 44 45 to 54 55 to 64 65 to 74 75 to 84 85 & older

Population by Age GroupHistory 2010 Base Year

2025New Hampshire

First Time Home Buyers EldersFamilies

1818

Will mean an increase in older home owners

Owner Households

21,243

7,457

19,582

11,888

0

5,000

10,000

15,000

20,000

25,000

Under Age 65 65 & Older

History 2010 Base Year2025

Southwest Region Planning Commission

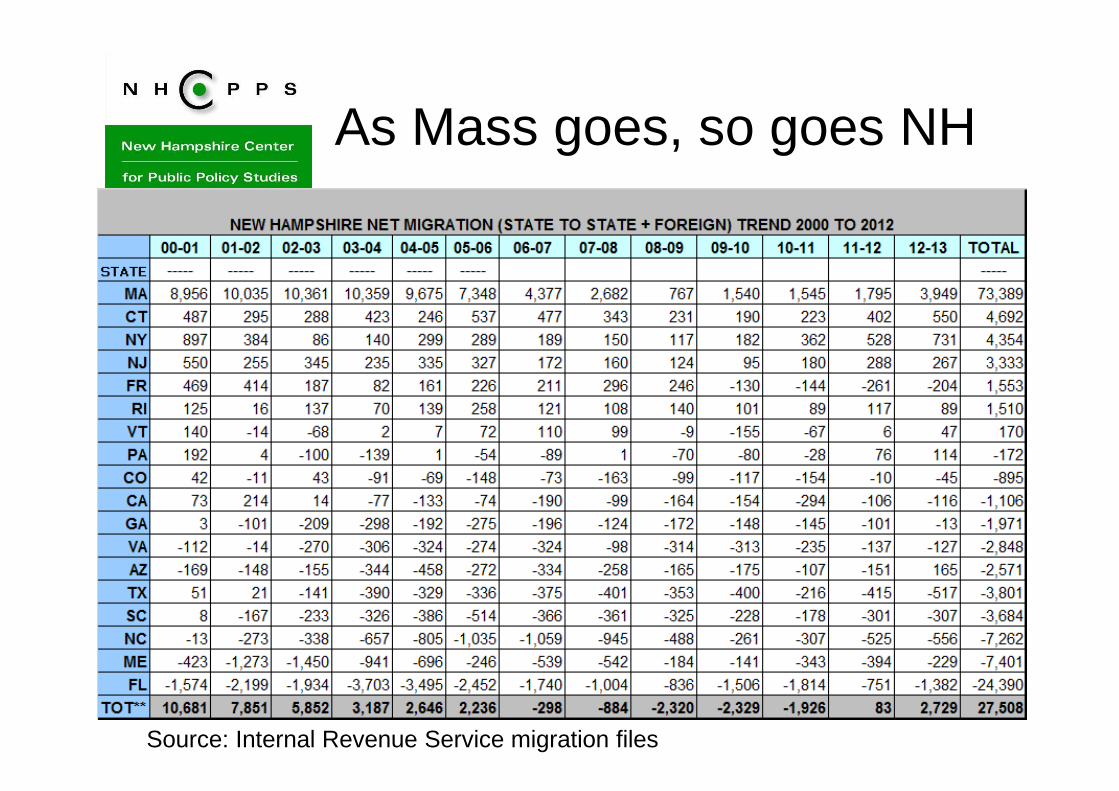

Migration stopped in last decade

Source: Internal Revenue Service migration files

As Mass goes, so goes NH

Source: Internal Revenue Service migration files

Same trends in Cheshire County

121 49 74

(111) (116) (98)(40)

(182) (154)

46

67

(81)

(79)

(232)(189)

(215)

(29) (110)

(400)

(300)

(200)

(100)

-

100

200

2005 2006 2007 2008 2009 2010 2011 2012 2013

Net

Num

ber

of E

xem

ptio

ns

From Previous Year

Net Migration Cheshire County (IRS)

Cheshire County Tot Mig-Diff St

Cheshire County Tot Mig-Same St

NH Population growth anticipated to be slower

Ten Year Percent Change in New Hampshire Population by Decade End

8.5%

13.8%

21.5%

24.8%

20.5%

11.4%

6.5%

3.3% 3.8%

1.1%

1950 1960 1970 1980 1990 2000 2010 2020 2030 2040

ActualForecast

2323

While NH Dept of Employment expects increasing jobs

2012 to 2022

Change in Employment (ELMI Projection) PctChange

Central NH Planning Commission 9.2%

Lakes Region Planning Commission 6.3%

Nashua Regional Planning Commission 9.5%

North Country Council 4.8%

Rockingham Planning Commission 14.7%

Southern NH Planning Commission 14.1%

Southwest Region Planning Commission 4.8%

Strafford Regional Planning Commission 9.5%

Upper Valley / Lake Sunapee Regional Planning 10.2%

New Hampshire 10.5%

2424

Working Age Population Will Decline in Every Region

2010 to 2025

Working Age Population (age 25 to 64) PctChange

Central NH Planning Commission -6.8%Lakes Region Planning Commission -9.2%Nashua Regional Planning Commission -3.0%North Country Council -12.9%Rockingham Planning Commission -1.2%Southern NH Planning Commission -1.5%Southwest Region Planning Commission -4.1%Strafford Regional Planning Commission -0.5%Upper Valley / Lake Sunapee Regional Planning -6.8%New Hampshire -4.0%

Combined with labor force participation reality (declines by age)

25

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

Ra

tio

Em

plo

ym

en

t to

Po

pu

lati

on

New Hampshire Employment to Population by Age Group

16 to 19 years

20 to 24 years

25 to 34 years

35 to 44 years

45 to 54 years

55 to 64 years

65 years and over

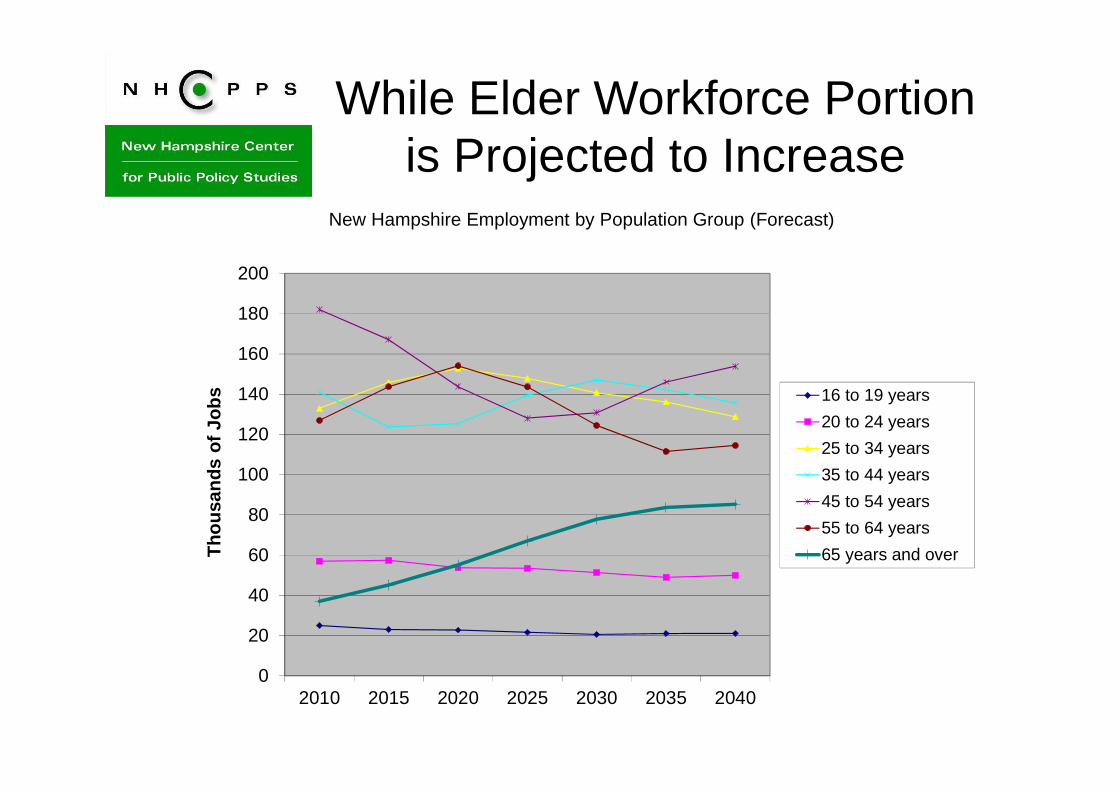

While Elder Workforce Portion is Projected to Increase

0

20

40

60

80

100

120

140

160

180

200

2010 2015 2020 2025 2030 2035 2040

Tho

usan

ds o

f Job

sNew Hampshire Employment by Population Group (Forecast)

16 to 19 years

20 to 24 years

25 to 34 years

35 to 44 years

45 to 54 years

55 to 64 years

65 years and over

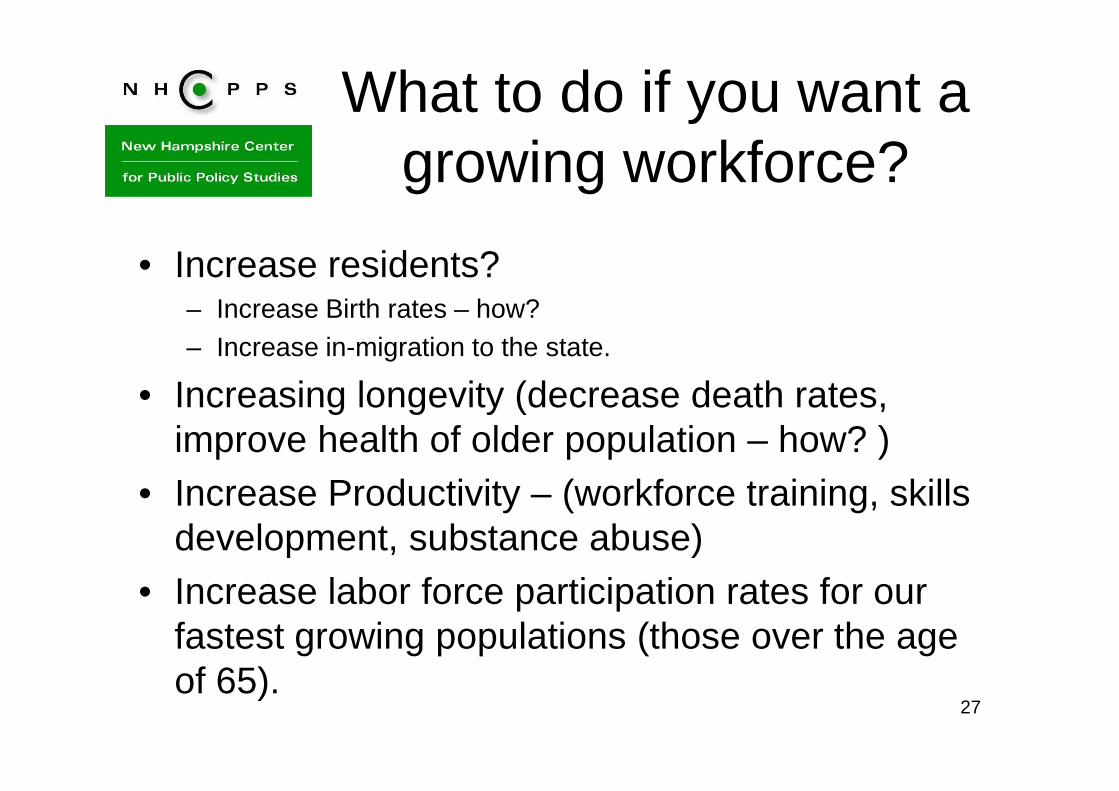

What to do if you want a growing workforce?

• Increase residents?– Increase Birth rates – how? – Increase in-migration to the state.

• Increasing longevity (decrease death rates, improve health of older population – how? )

• Increase Productivity – (workforce training, skills development, substance abuse)

• Increase labor force participation rates for our fastest growing populations (those over the age of 65).

27

Workforce quality by region

Cheshire County Largest Employers

29

30

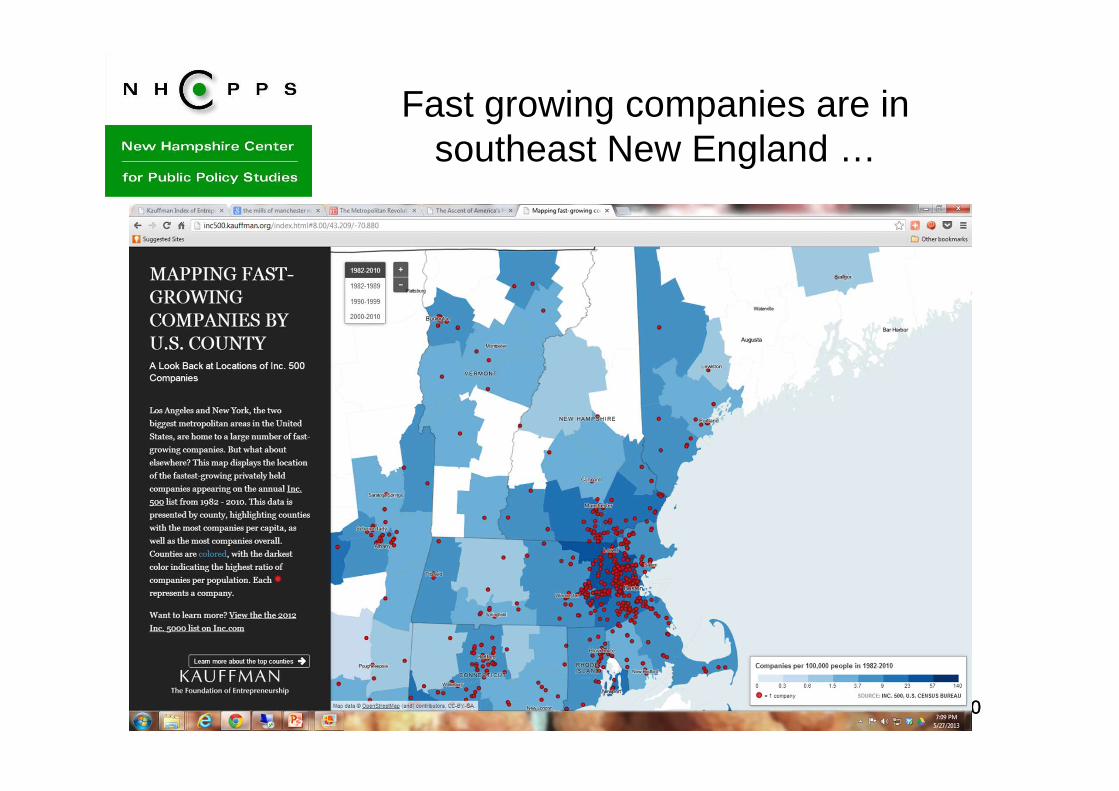

Fast growing companies are in southeast New England …

30

Broadband availability in NH

Property Value by Region

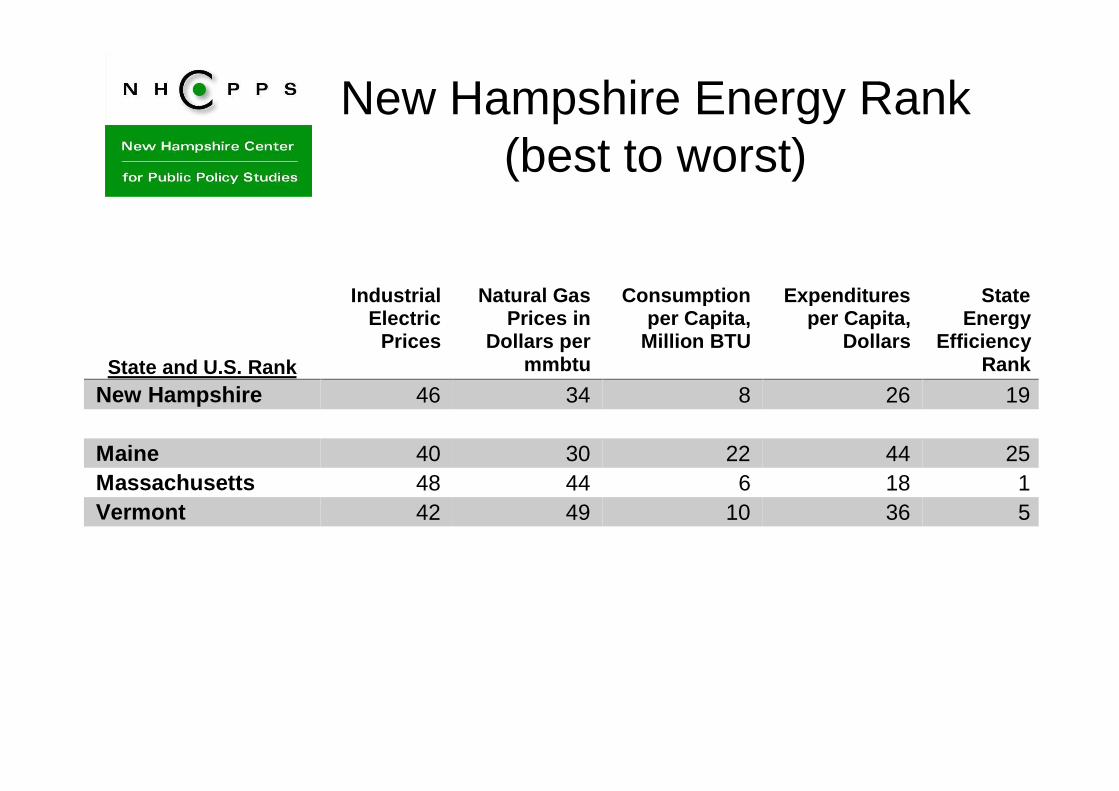

New Hampshire Energy Rank (best to worst)

State and U.S. Rank

Industrial Electric

Prices

Natural Gas Prices in

Dollars per mmbtu

Consumption per Capita,

Million BTU

Expenditures per Capita,

Dollars

State Energy

Efficiency Rank

New Hampshire 46 34 8 26 19 Maine 40 30 22 44 25 Massachusetts 48 44 6 18 1 Vermont 42 49 10 36 5

34

What policies would encourage our energy ‘competitiveness’

• Expanding natural gas capacity?• Northern Pass?• Divestiture of PSNH’s generation capacity?• Encouraging Energy Efficiency?• Encouraging renewables?• Use RGGI funds to solve energy problems?• Understanding the system’s reliability?

NH excels on “current climate” indicators

Area Indicator NH RankWFHousing Homeownership rates 2Regulatory Pollution Abatement / $ Value Added 3EdWorkFrc High School grad rate 4Cultural Voter turnout rate 4EdWorkFrc Pct of pop in Science & Engineering workforce 5EdWorkFrc Pct w/Associates+ 6EdWorkFrc Percent of children aged 3-4 in preschool 6Fiscal State Business Tax Climate Index 7Fiscal Public health/welfare spending per person in poverty 7GrowthReten Manufacturing Supercluster Concentration (LQ) 7

But NH lags on “future climate” indicators

Area Indicator NH RankFiscal Top marginal corporate tax rate 38Infrastructure Percent of bridges deficient or obsolete 39WFHousing Owner costs more than 30% of Income 43Health Health Care Expenditures per Capita by State of Residence, 2009 43Fiscal State debt per $ Personal Income 45Energy Industrial Electric Prices 46GrowthReten Capital Investment Projects per 100,000 pop 46Regulatory Land Use Restriction 47EdWorkFrc Change in 35-44 y.o share of population, 2000 to 2010 48EdWorkFrc Average student debt 50

37

Looking forward: The ecology of

a successful economy

There’s this …• Human Capital• Financial Capital• Economic Creativity• Business Base• Costs of Business• Infrastructure

• Quality of Life

And then … Brad Feld

� A Strong Pool of Tech Founders� Local Capital� Killer Events� Access to Great Universities� Motivated ‘Champions’� Local Press, Organizational Tools� Alumni Outreach� Wins� Recycled Capital� Second-Time Entrepreneurs� Attractive to Engineers� Tent-pole local tech companies 37

NEEP Forecast for New Hampshire October 2014

• The Granite State will add only a few hundred manufacturing jobs over the next five years. However, it is expected that Granite State manufacturing output will continue to increase in the forecast period as it has in the past five years.

• In the private services sector employment will increase by about 2.0 percent annually in the forecast period. The fastest rate of growth will occur in Professional and Business Services, followed by Leisure & Hospitality, and Education and Health Services employment.

• The New Hampshire real estate market has finally seen a return to normal (pre housing bubble) price appreciation and sales growth, according to state realtors. Foreclosure recordings declined steadily over the past year. The state rental market remains strong with rental costs leveling and vacancies remaining below 5 percent in most areas.

Look to an Improving National Economy, Pushed by Housing

and Low Energy Prices

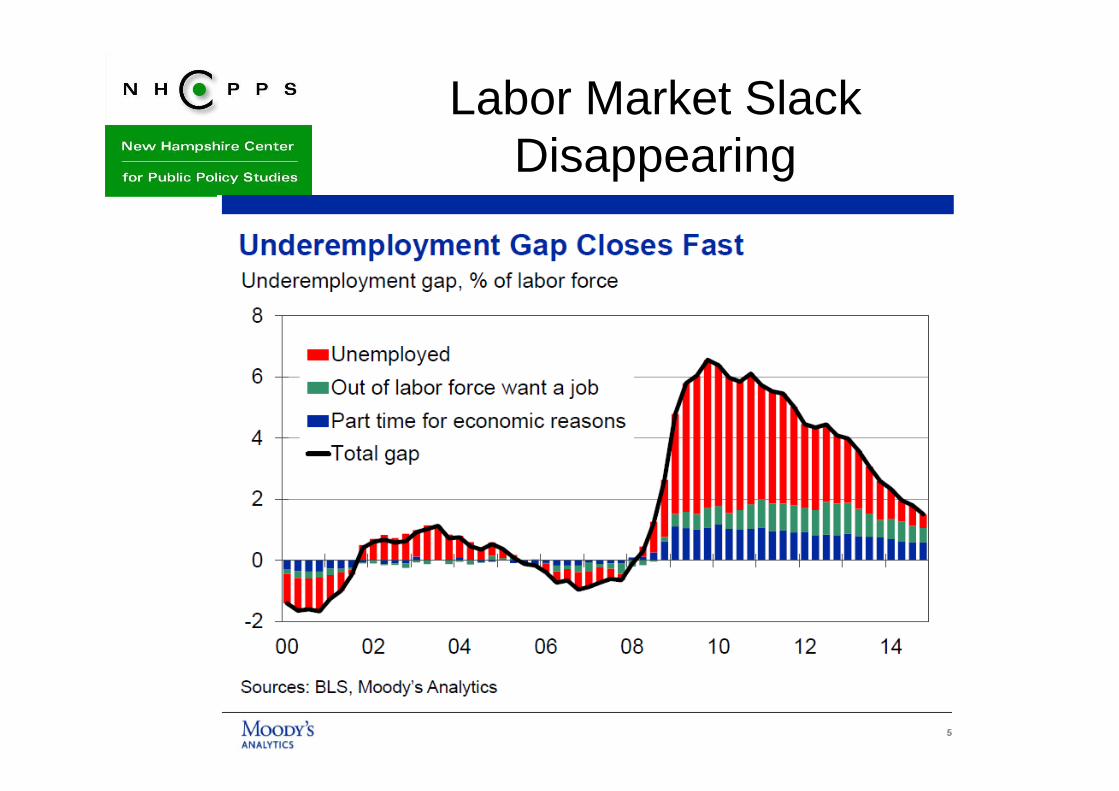

Labor Market Slack Disappearing

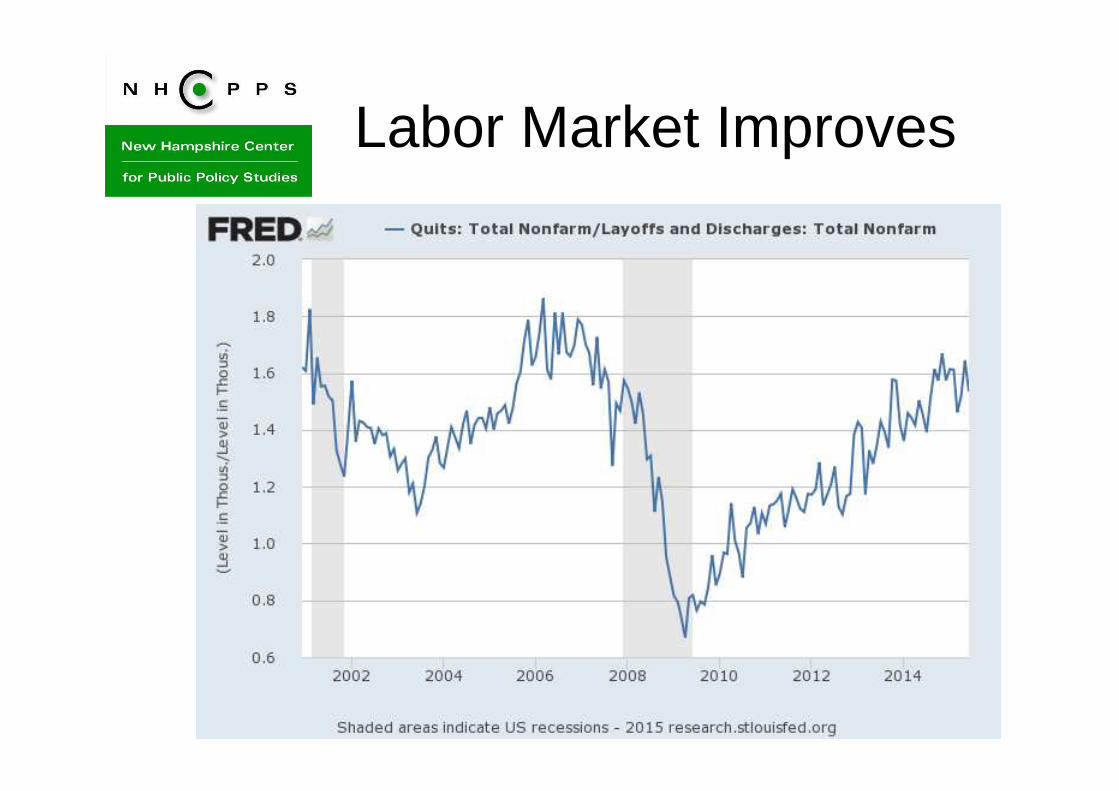

Labor Market Improves

Employers Facing Increasing Labor Cost

Economic Consequence of the Market Turmoil

• Negative consequences– Lower stock prices impacts consumer spending through

wealth effect and businesses’ cost of capital.– Stronger value of the $ weakens the trade balance.– Emerging market economies struggle to adjust to lower

commodity prices.

• Positive consequences– Lower oil prices is a net positive as stronger consumer

spending more than offsets the hit to the energy industry.– Lower mortgage rates supports housing and refinancing

activity.– Reduces over-valuation in asset markets and chances that a

bubble will form. Allows Fed to raise rates more slowly.

Source: Moody’s Analytics, September 1, 2015

Economic cross currents net out

Source: Moody’s Analytics

Overall Risk IndexWealth Effect 40%, trade 40%,

energy 20%

Sources: BLS, Moody’s Analytics

New Hampshire Center for Public Policy Studies

Want to learn more?• Online: nhpolicy.org• Facebook: facebook.com/nhpolicy• Twitter: @nhpublicpolicy• Our blog: policyblognh.org• (603) 226-2500

“…to raise new ideas and improve policy debates throu gh quality information and analysis on issues shaping New Hamp shire’s future.”

46

Board of DirectorsJames Putnam, Chair

David Alukonis

Eric Herr

Dianne Mercier

Catherine A. Provencher

Todd I. Selig

Michael Whitney

Daniel Wolf

Martin L. Gross, Chair Emeritus

Directors Emeritus

William H. Dunlap

Sheila T. Francoeur

Stuart V. Smith, Jr.

Donna Sytek

Brian F. Walsh

47

The Aging Bubble …

48

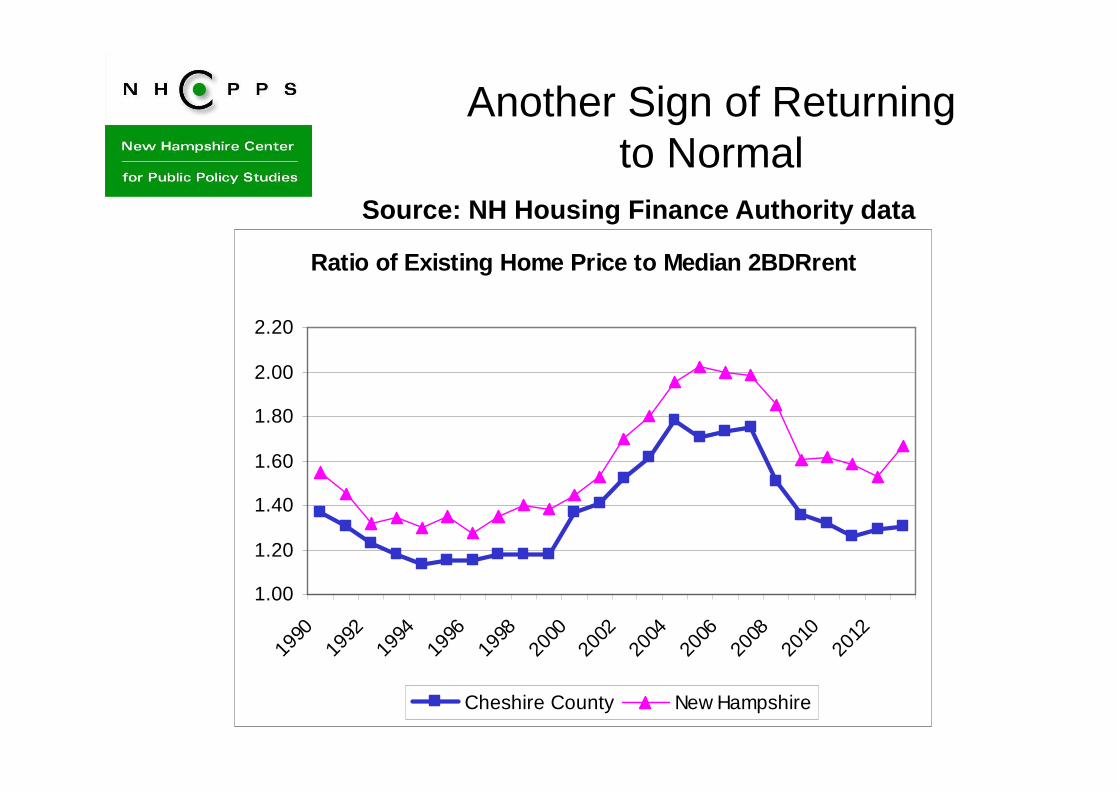

Another Sign of Returning to Normal

Source: NH Housing Finance Authority data

Ratio of Existing Home Price to Median 2BDRrent

1.00

1.20

1.40

1.60

1.80

2.00

2.20

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

Cheshire County New Hampshire

Assisted Living Demand Increases with Age

50Source: Centers for Medicare and Medicaid Services, Medicare Beneficiary Survey, 2007. Cited in ULI, Housing In America: The Baby Boomers Turn 65. 2012. Page 38

Living Arrangements of US Medicare

Recipients, 2007

98%

93%

78%

1%3%

7%

1%4%

15%

0%

20%

40%

60%

80%

100%

120%

65-74 75-84 85+

Traditional Communities

Assisted Living

Long Term Care

Assisted Living Demand is years away

510

50,000

100,000

150,000

200,000

250,000

2000 2010 2015 2020 2025 2030 2035 2040

New Hampshire Elder Population

65 to 74

75 to 84

85 and Older