bitcoin financing: ucc, regulatory and hedging...

TRANSCRIPT

Bitcoin Financing:

UCC, Regulatory and Hedging Concerns

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's speakers. Please refer to the instructions emailed to registrants for additional information. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 1.

TUESDAY, APRIL 10, 2018

Presenting a live 90-minute webinar with interactive Q&A

Matthew Frankle, Shareholder, Greenberg Traurig, New York

Alexander T. Grishman, Partner, Haynes and Boone, New York

Andrew C. Helman, Attorney, Marcus Clegg, Portland, Maine

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-873-1442 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 2.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Financing Cryptocurrencies: UCC and Lender Issues

haynesboone.com | gtlaw.com | marcusclegg.com

WHAT WE WILL COVER TODAY

INTRODUCTIONS

OVERVIEW AND REGULATORY FRAMEWORK

CRYPTOCURRENCY AS COLLATERAL UNDER ARTICLE 9

RETAIL COMMODITY FINANCING

SECURITIES FINANCING

6Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

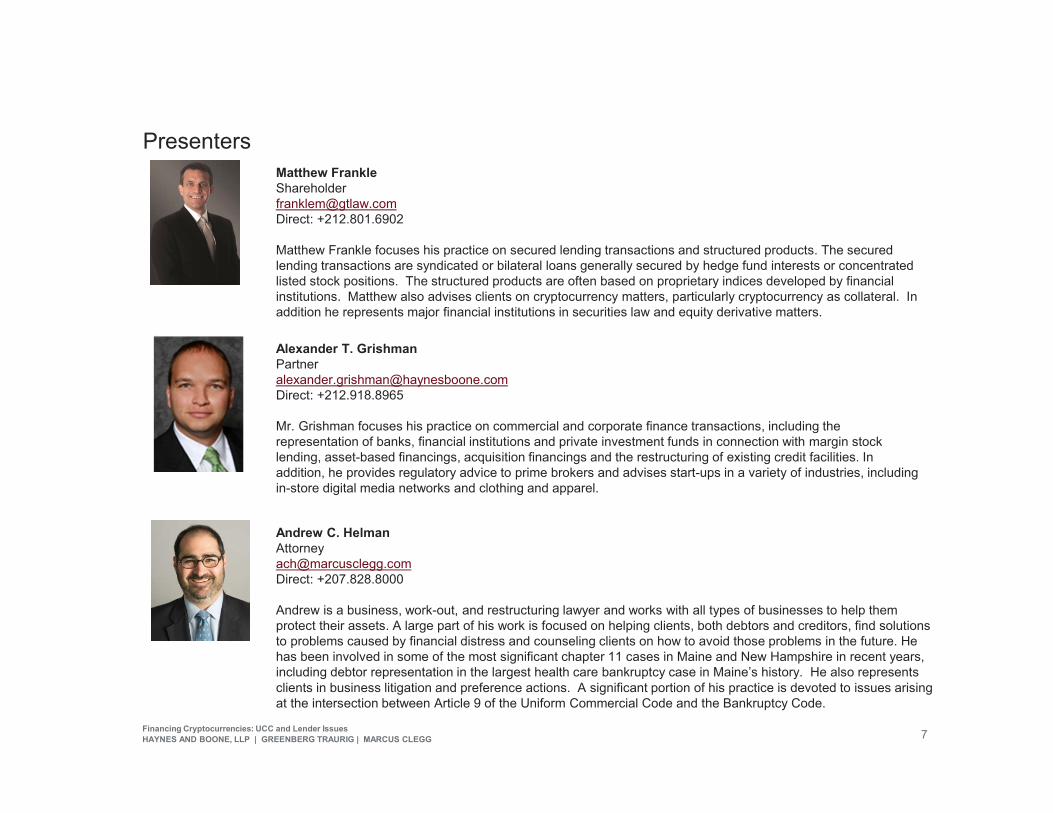

Presenters

7Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Matthew [email protected]: +212.801.6902

Matthew Frankle focuses his practice on secured lending transactions and structured products. The secured lending transactions are syndicated or bilateral loans generally secured by hedge fund interests or concentrated listed stock positions. The structured products are often based on proprietary indices developed by financial institutions. Matthew also advises clients on cryptocurrency matters, particularly cryptocurrency as collateral. In addition he represents major financial institutions in securities law and equity derivative matters.

Alexander T. [email protected]: +212.918.8965

Mr. Grishman focuses his practice on commercial and corporate finance transactions, including the representation of banks, financial institutions and private investment funds in connection with margin stock lending, asset-based financings, acquisition financings and the restructuring of existing credit facilities. In addition, he provides regulatory advice to prime brokers and advises start-ups in a variety of industries, including in-store digital media networks and clothing and apparel.

Andrew C. [email protected]: +207.828.8000

Andrew is a business, work-out, and restructuring lawyer and works with all types of businesses to help them protect their assets. A large part of his work is focused on helping clients, both debtors and creditors, find solutions to problems caused by financial distress and counseling clients on how to avoid those problems in the future. He has been involved in some of the most significant chapter 11 cases in Maine and New Hampshire in recent years, including debtor representation in the largest health care bankruptcy case in Maine’s history. He also represents clients in business litigation and preference actions. A significant portion of his practice is devoted to issues arising at the intersection between Article 9 of the Uniform Commercial Code and the Bankruptcy Code.

OVERVIEW AND REGULATORY FRAMEWORK

WHAT IS CRYPTOCURRENCY AND HOW IS IT REGULATED?

8Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies - Overview

• Cryptocurrencies

o Often called “virtual currencies” or “digital currencies”

– Digital assets used as a medium of exchange

– Exchanged over the internet peer-to-peer

– Transactions are publicly recorded on decentralized ledgers, or blockchains

» Bitcoin is the most well-know and analogizes well with gold or hand to hand physical money

Spawned many variations

» Others, like ether, provide a use case beyond a store of value, and analogizes well to oil

» Other digital assets, usually called “tokens”, like DAO Token, are designed as “smart contracts” that can self execute and often are involved in capital raises, or ICOs

9Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies - Overview

• What is it?

o Nakamoto described Bitcoin as a chain of digital signatures

– Two related cryptographic keys

» “Public key” is essentially the user’s identity

» The related “private key” allows the user to speak for the public key

– Whoever has the private key can spend or transfer the cryptocurrency

o Blockchain keeps the order and record of transactions

– Miners compete to solve a puzzle

» Using computing power, miners enhance their chances

» The randomness of which miner wins, prevents control by one group

10Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies – Regulatory Framework

• Cryptocurrencies as Commodities

o CFTC v. McDonnell

– Virtual currencies are “goods” exchanged in the market for a uniform quality and value

– Falls within CEA’s definition of “commodities” as “all other goods and articles . . . in which contracts for future delivery arepresently or in the future dealt in”

– In re Coinflip

» Bitcoin and other virtual currencies are encompassed in the definition and property defined as commodities

• Cryptocurrencies as Securities

o The jurisdictional authority of CFTC to regulate virtual currencies as commodities does not preclude other agencies from exercising regulatory power

o The SEC has pursued organizations as issuers of unregulated securities

– The DAO Investigation: applied traditional “Howey Test” to determine DAO Tokens were securities

o Some unofficial SEC statements seem to cede jurisdiction to CFTC for certain cryptocurrencies: “While there are cryptocurrencies that, at least as currently designed, promoted and used, do not appear to be securities, simply calling something a “currency” or a currency-based product does not mean that it is not a security”

11Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies – Regulatory Framework

• Coins / Tokens / Cryptocurrencies as a Security

o “…when a security is being offered, [U.S.] securities laws must be followed”

o A token offering that represents an investment of money in a common enterprise with a reasonable expectation of profits derived from the efforts of others is a security

o SEC 21(a) Report – an ICO Offering is pitched on the basis that coins will increase in value, ability to lock in profits through trades on the secondary market and otherwise profit based on the work of others

12Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

CRYPTOCURRENCY AS COLLATERAL

WHAT HAPPENS WHEN BITCOIN MEETS ARTICLE 9 OF THEUNIFORM COMMERCIAL CODE?

13Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrency as Collateral

• Cryptocurrencies are steadily working their way into the traditional economy as payment systems and investment vehicles

o As 2017 ended, 11 percent of Americans said they currently or previously owned virtual currency

o Major financial institutions are offering cryptocurrency trading and investment products

o More than 100,000 businesses are accepting cryptocurrency as payment

o Cryptocurrency-backed loans are developing

• How will commercial law interact with this new digital asset?

o Security interests will likely remain attached to and enforceable against most types of cryptocurrency even after dispositions

o The specific and identifiable nature of each unit of cryptocurrency will aid secured parties and bankruptcy trustees seeking to identify particular units of cryptocurrency after disposition

• Are financial markets adequately recognizing these risks and benefits in pricing of cryptocurrency?

14Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies - Collateral

• How does one perfect a security interest in cryptocurrency?

• It depends on what type of asset it is

• Article 9 contains many specifically enumerated classes of collateral, and several are easily ruled out:

o Cryptocurrency will not be “instruments” because, by definition, “instruments” only exist in a written form and involve the payment of money. UCC § 9-102(47)

o Cryptocurrency are not “inventory” because “inventory” (a sub-type of goods) is limited to tangible, physical property. UCC § 9-102(48)

o Cryptocurrency will not be a “deposit account” because those are accounts at banks or other financial institutions accepting funds for deposit. UCC § 9-102(29)

o Cryptocurrency will not be an “account” because it is not a right to payment for services or property. UCC § 9-102(2)

15Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies - Collateral

• Possible asset classes include:

o Investment property “means a security, whether certificated or uncertificated, security entitlement, securities account, commodity contract, or commodity account” UCC § 9-102(49)

o Money is a “medium of exchange currently authorized or adopted by a domestic or foreign government[.]” UCC § 1-201(b)(24)

o General Intangible is a catch-all for “any personal property, including things in action,” that is not another form of property. UCC § 9-102(42). Investment property, securities, and money, for example, are not general intangibles

o Security (see following slide)

16Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies - Collateral

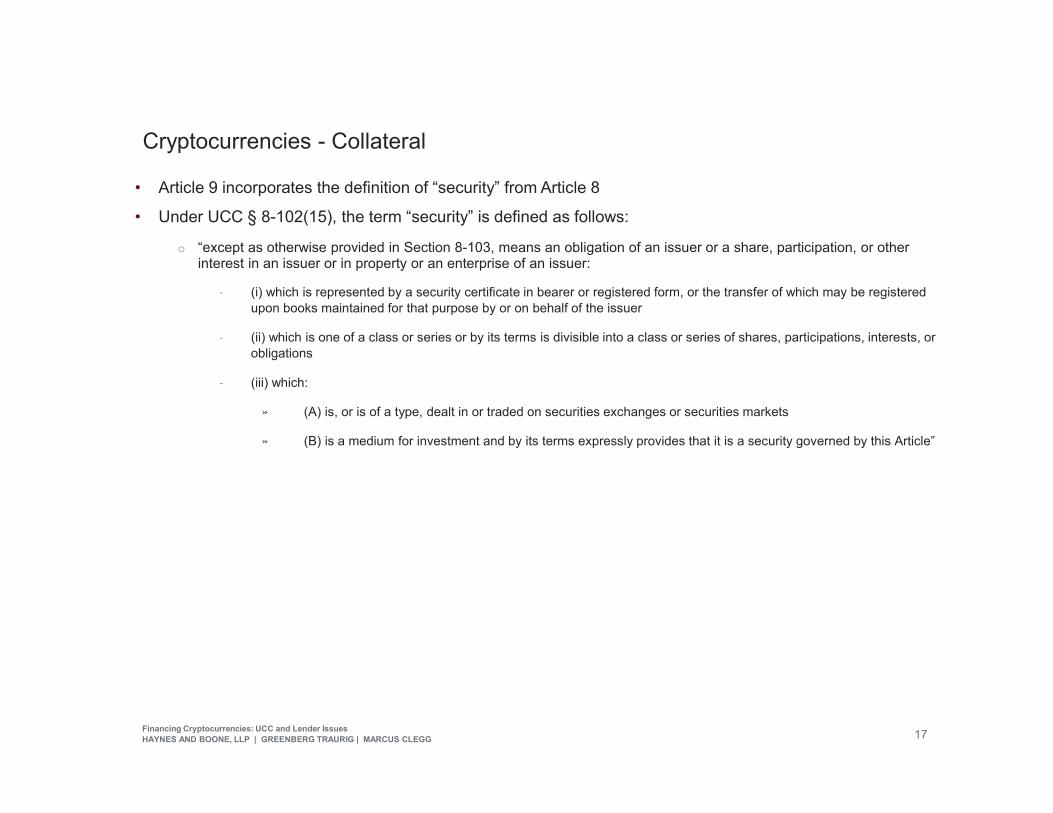

• Article 9 incorporates the definition of “security” from Article 8

• Under UCC § 8-102(15), the term “security” is defined as follows:

o “except as otherwise provided in Section 8-103, means an obligation of an issuer or a share, participation, or other interest in an issuer or in property or an enterprise of an issuer:

– (i) which is represented by a security certificate in bearer or registered form, or the transfer of which may be registered upon books maintained for that purpose by or on behalf of the issuer

– (ii) which is one of a class or series or by its terms is divisible into a class or series of shares, participations, interests, or obligations

– (iii) which:

» (A) is, or is of a type, dealt in or traded on securities exchanges or securities markets

» (B) is a medium for investment and by its terms expressly provides that it is a security governed by this Article”

17Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies - Collateral

• So what type of asset is cryptocurrency?

• Most cryptocurrency will not be “money” because it is not official currency established by a government

o The exception to this could be cryptocurrency established by a foreign government, such as Venezuela, Switzerland, or the Marshall Islands—all of which are reportedly considering establishing such currencies.

• Cryptocurrency will most likely only be “investment property” if it qualifies as a “security.” Based on available information, there appear to be several impediments to this:

o It is not an “obligation of an issuer or a share, participation, or other interest in an issuer or in property of an issuer”

– No “obligation”

– Assuming an exchange is an “issuer,” is it a “share, participation or other interest” in the “issuer or in property or an enterprise of an issuer”?

– Is an exchange even an “issuer” in the first place?

o There is no paper certificate nor registration books maintained identifying the specific owner of a unit of cryptocurrency

o Exchanges do not appear to “create” bitcoin or act as guarantors, ruling out UCC § 8-201(b)

o Bitcoin is not fungible, ruling out sub(ii) of the definition

• General Intangible is the only definition that seems to clearly apply

18Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies - Collateral

• There are several reasons why classifying cryptocurrency as a general intangible (or even a security) matters compared to “money”

o A security interest in a general intangible (or a security) can be perfected simply by filing a financing statement in the jurisdiction where the debtor is located

– Neither control nor possession is required, unlike money or a deposit account

o Once perfected, the security interest “continues in collateral notwithstanding sale, lease, license, exchange or other disposition unless the secured party authorized the disposition free of the security interest[.]” UCC § 9-315(a)(1)

– A security interest will remain attached to and perfected in cryptocurrency even after a vendor accepts it as payment, as long as the secured party did not consent to the disposition free and clear of the security interest

– In contrast, money transfers free of a security interest. UCC § 9-332

o A security interest in one form of collateral will attach to and be perfected in “proceeds” for at least 20 days, and perhaps longer. UCC §§ 9-102(64), 9-315(e)

– The security interest will be perfected in proceeds even if the proceeds are held by a third party

19Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies - Collateral

• Horrible Hypos:

o Assume a company has pledged its general intangibles to secure a loan and then uses bitcoin to buy tickets to an NBA game from a team accepting cryptocurrency as a perk for management or business entertainment

o Assume a corporate traveler pays for a meal at an airport accepting cryptocurrency (which is owned by the employer)

– In both examples, the vendor takes the cryptocurrency subject to any security interest

– The debtor will have no recognizable “proceeds” for these types of experiential purchases

– The vendor could become a litigation target of the secured party

– In litigation, the secured party may benefit from the identifiable nature of cryptocurrency and likely would not have to engage in tracing for commingled proceeds of cash

o Assume the vendor has a secured party with a lien on all assets, including general intangibles, with an “after acquired” clause in its security agreement

– Even if the vendor takes the cryptocurrency free of a security interest (because there was none or the disposition was authorized), a further disposition of the cryptocurrency would likely be subject to the security interest of the vendor’s lender

20Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

RETAIL COMMODITY FINANCING

LIMITATIONS ON FINANCING CRYPTOCURRENCIES CLASSIFIEDAS COMMODITIES

21Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies – Secured Loans to Retail Customers

• CFTC has jurisdiction over contracts for future delivery as well as fraud in the spot market

• Additionally, though, CFTC has jurisdiction over financed retail commodity transactions

o Any agreement, contract or transaction in any commodity that is

– Entered into with . . .a person that is not an eligible contract participant; and

– Entered into . . . on a leveraged or margined basis . . .

o Background

– CFTC v. Zelener

» Involved foreign exchange contracts that purportedly we spot transactions

Contract called for settlement within two days; but instead, the parties “rolled forward” the transaction

CFTC asserted this was, in substance, a futures contract

– Congress created the Retail Foreign Exchange and then Retail Commodity provisions as a separate class of transactions to be regulated under the CEA

22Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies – Secured Loans to Retail Customers

• Actual Delivery Exception

o Retail Commodity Provision does not apply for “contract of sale that results in actual delivery . . . within 28 days

– Actual delivery has been interpreted strictly

» Book entry is not enough

– Retail Commodity Transactions Involving Virtual Currency

» CFTC proposal on “actual delivery” for virtual currencies

Customer must be able to take possession and control of entire commodity

Use it freely in commerce

Offeror or counterparty must not retain any interest or control

Must take physical delivery; no cash settlement

» Example specifically cites depository must be purchaser’s agent

» Example cited includes no liens

23Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Cryptocurrencies – Secured Loans to Retail Customers

• Bitfinex

o Offered leveraged for Bitcoin margin purchases

o Retained private keys; or multi-sig

o CFTC found no actual delivery

• What if the leverage was offered, but not the sale

o Does the exception even apply?

– On its face, the actual delivery exception only applies to “contracts of sale”

o Does granting a lien result in giving up possession?

– Borrower transfers cryptocurrency to lender or lender’s agent

– Can the loan remain for over 28 days?

24Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

SECURITIES FINANCING

ISSUES FOR LENDERS WHEN FINANCING DIGITAL ASSETS THAT ARE CLASSIFIED AS SECURITIES

25Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

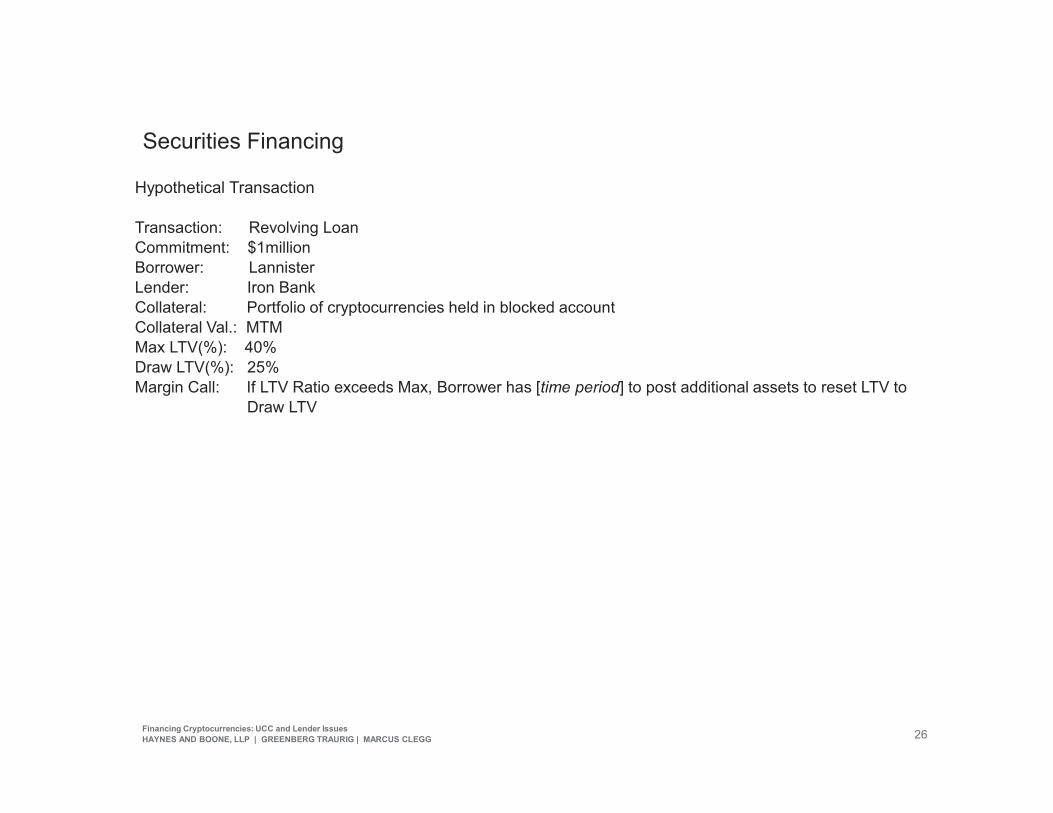

Securities Financing

Hypothetical Transaction

Transaction: Revolving LoanCommitment: $1millionBorrower: LannisterLender: Iron BankCollateral: Portfolio of cryptocurrencies held in blocked accountCollateral Val.: MTMMax LTV(%): 40%Draw LTV(%): 25%Margin Call: If LTV Ratio exceeds Max, Borrower has [time period] to post additional assets to reset LTV to

Draw LTV

26Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Securities Financing

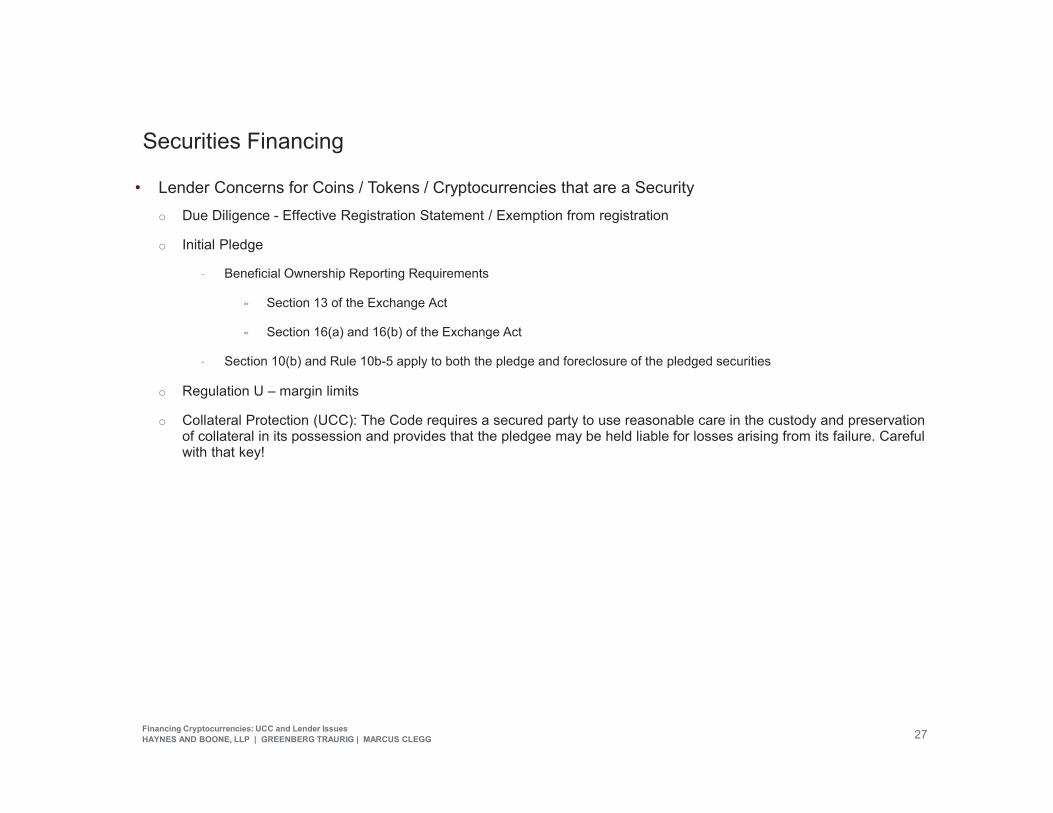

• Lender Concerns for Coins / Tokens / Cryptocurrencies that are a Security

o Due Diligence - Effective Registration Statement / Exemption from registration

o Initial Pledge

– Beneficial Ownership Reporting Requirements

» Section 13 of the Exchange Act

» Section 16(a) and 16(b) of the Exchange Act

– Section 10(b) and Rule 10b-5 apply to both the pledge and foreclosure of the pledged securities

o Regulation U – margin limits

o Collateral Protection (UCC): The Code requires a secured party to use reasonable care in the custody and preservation of collateral in its possession and provides that the pledgee may be held liable for losses arising from its failure. Carefulwith that key!

27Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Securities Financing

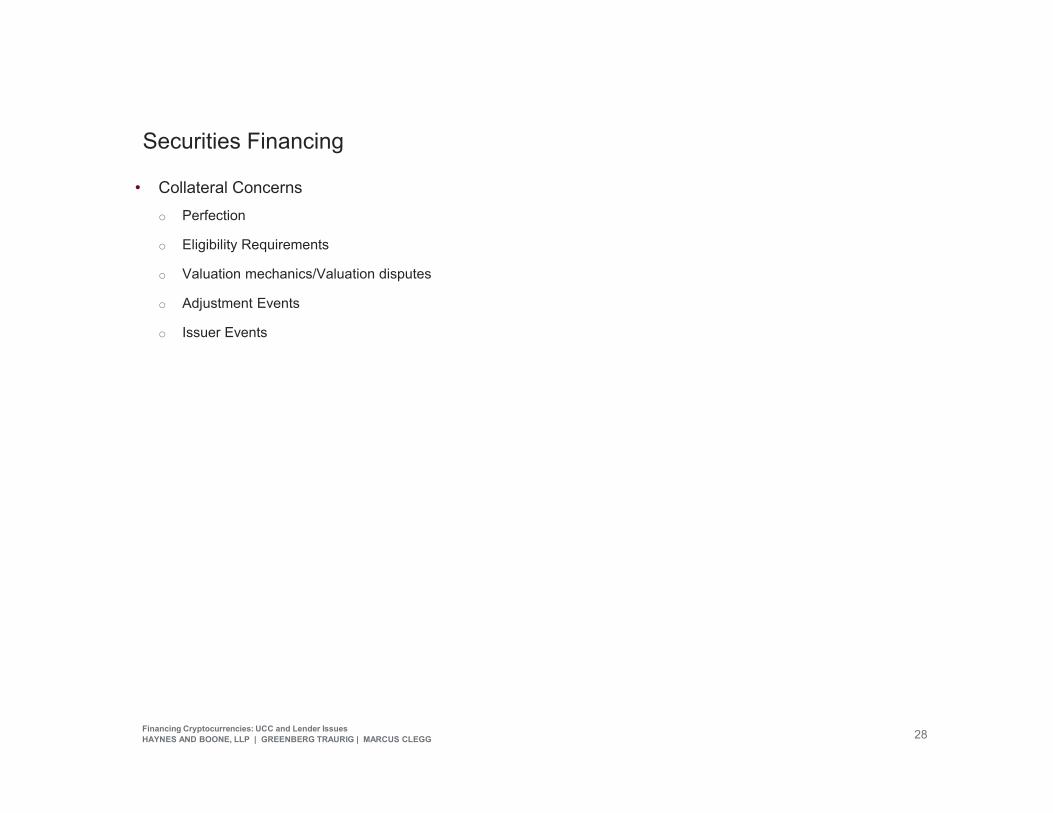

• Collateral Concerns

o Perfection

o Eligibility Requirements

o Valuation mechanics/Valuation disputes

o Adjustment Events

o Issuer Events

28Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Securities Financing

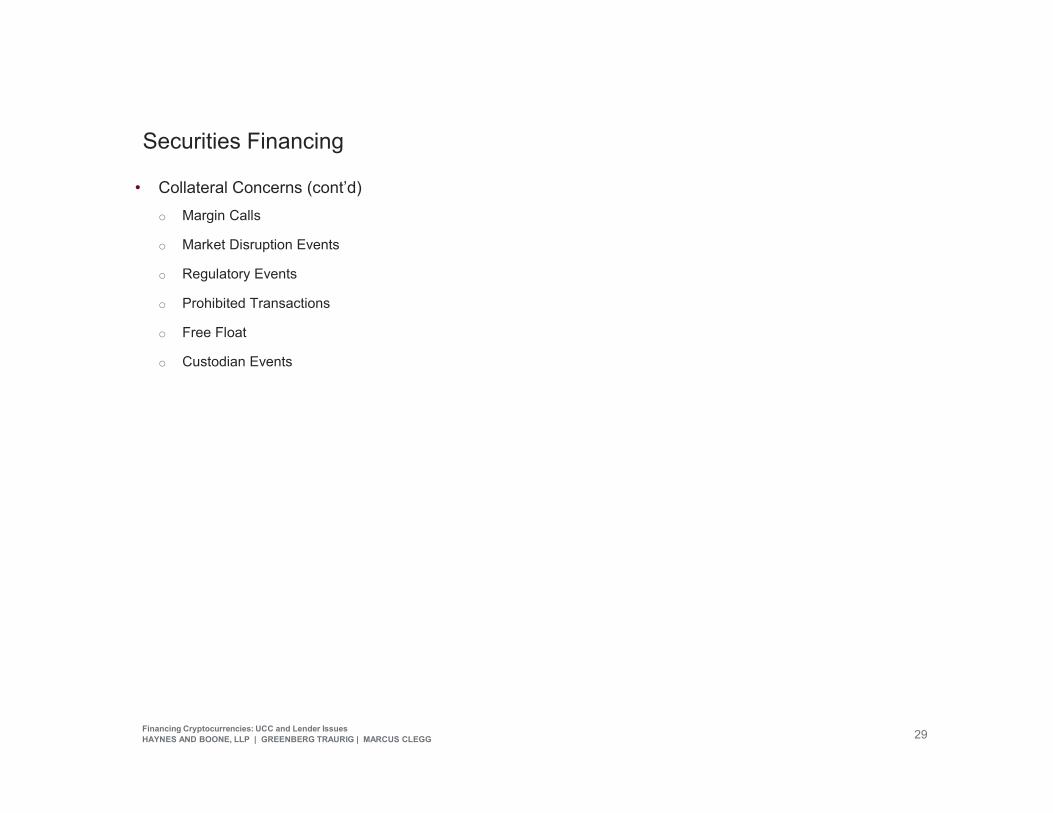

• Collateral Concerns (cont’d)

o Margin Calls

o Market Disruption Events

o Regulatory Events

o Prohibited Transactions

o Free Float

o Custodian Events

29Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Securities Financing

• Perfection

o Securities Account

o Financial Asset

o SACA

o Private Key

30Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Securities Financing

• Foreclosure

o Registration or exemption for sale

– 4(1)

– 4(1)(1/2)

– 144 – requirements and volume limits

• UCC Issues

o Recognized market

o Public Sale

o Private Sale

o Commercially reasonable

• Bankruptcy Stay/Safe Harbors

31Financing Cryptocurrencies: UCC and Lender Issues

HAYNES AND BOONE, LLP | GREENBERG TRAURIG | MARCUS CLEGG

Thank You