bestlink college of the philippinesit4106servicemanagementsystem.weebly.com/uploads/3/1/7/3/... ·...

TRANSCRIPT

Bestlink College of the Philippines

Chapter I – Project Charter

1.0 PROJECT BACKGROUND

This chapter introduces the Accounts Payables and Account Receivables with

Treasury Management System (APART MS) under Service Management System. As

we are in a new era of an advanced high-tech environment, the business world is also

entering into an era of fierce competition noticed by takeovers and mergers. This

illuminates the type of dynamic and complex business environment that companies

have to face.

The rapid change in the environment reminds us that, for a business to survive, it

has to focus on its core competencies and discover in order to keep ahead of the

competitors. The field of Service Management system has evolved mainly in

accordance to the fact that financial accounts need to be managed strategically for the

firm to enjoy sustainable competitive advantage over competition. Several scholars

have noted the complex structures of financial account management in the present-day

Industry. Firms that learn how to manage their financial accounts well takes advantage

over others in a long run. The point is, the goal of producing a consistent management

of financial accounts must be attained.

1.1 PROBLEM / OPPORTUNITY PROBLEM

The following will be the problem/s to be resolve:

Time Consuming Task

Present application software being used is not sufficient to execute core

processes.

Needs a definite accounting process that makes the system more reliable.

Needs integration/interconnection with related Information Management

Systems. It must have a unified and secured data management control.

1.2 BENEFITS

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 1

Bestlink College of the Philippines

When the APARTMS has been implemented, chances are, it provides the

following advantages to the client(s):

A user will have an efficient updating and processing of accounts (esp.

AR and AP), with a detailed reports and easy solving-related

processes.

- It displays Accounting processes which are compose of Journal

Entries, T-Accounts or Ledger and Trial Balance.

Daily update of Treasury and funds.

- Income Statement and Financial Report has been displayed.

In addition, the APARTMS are intertwined and interconnected with

other related SMS subsystem, with an effective data cycle. Also, it has

a unified Database management control.

- Import / Exports data with General Ledger and BCMS.

It cut cost and time.

- AP and AR Accounts are managed easily.

It will provide up-to-date account reports.

- any transaction that has been process is automatically added to

the Journal Entries.

Higher data security compared to the existing system.

- Uses MySQL for data management.

1.3 GOALS To achieve the potential progress of their existing IS, while rendering

the foundational aspects of business flows and laws.

To monitor the Assets, Liabilities, Equity, and Expenses of the Clients

and at the same time, provides its report that can be satisfactory valid

and legal.

Easily updates the Clients/users on what has been paid and defines if

the company maintains or loses financial resources.

Income Statement and Balance Sheet has been processed

automatically.

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 2

Bestlink College of the Philippines

To solve some minor Financial Management errors/mishandling.

Unified Database with other related SMS subsystem.

1.4 STAKEHOLDERS AND CLIENTS Marban Security Agency (Client)

Dennis Gonzales (Project Study I Adviser)

JunpyoManayan (Project Manager)

Mac Douglas Goron (System Analyst)

Joefel Langcauon (Programmer)

Jayson Cabigas (Business Analyst)

Mark Christian San Diego (Document Specialist)

2.0 PROJECT SCOPE

APARTMS covers the Information management of financial accounts, especially

Accounts Payables, Receivables, and Treasury fund.

2.1 OBJECTIVES

The main purpose of APARTMS is to manage and provide statement of

account, especially AP/AR and helps the accounting personnel to update assets

and treasury. The goal of APARTMS is:

It provides Financial Statement where a client is being informed how the

Financial Resources are managed.

It defines the Economical status of the client, where it gains or loses

money.

It distinguishes balances, credits, debits, and payables and at the same

time, describes the monetary unit being involved.

APART MS can be accessible in selected personnel whether Admin or

Accountant use.

It also manage the Treasury Information, where a journal entry and check

preparation has been produced, along with Financial statement Reports.

2.2 DELIVERABLES

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 3

Bestlink College of the Philippines

The APART MS will help the company to monitor and manage financial

process, and allows the user to have an update with its core transactions. It also

gives a proficient tasking to the company who will use the proposed MS.

1. Journal Entry Form

2. T-Accounts or Ledger

3. Trial Balance

4. Income Statement Report Form

5. Balance Sheet Report Form

6. Check/Voucher Form

Planning Phase

The APARTMS undergoes SDLC method, along with other

manipulativeways of gathering data.

System Development System Design System Analysis Testing and Integration Implementation Operation and Maintenance

2.3 OUT OF SCOPE Electricity Issues: The APARTMS cannot be used in the midst of power

shortage.

Banking and other bank-related process is yet to be executed due to

the system requirements.

APARTMS is yet to be connected online.

3.0 PROJECT PLAN3.1 Approach and Methodology

Conduct a planning/strategy measures on how to obtain resources or

information.

Mapping or tracing

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 4

Bestlink College of the Philippines

Formal interviews/surveying/actualization

Related Literature (Foreign and Local) review.

Research papers and forms for other information needed.

Simulation of the process flow being generated.

3.2 Project Timeline

ID Task Name Start Finish Duration

1 Conducting of preliminary meeting 12:00 NN 4:30PM 4HRS

2 Information Gathering 5:00PM 9:00PM 4HRS

3

Finalizing the system’s technical

features 9:00 AM 5:00PM 8HRS

4 Identifying System Design Specification 1:00 PM 2:00 PM 1HRS

5 System Coding

9:00AM, Sept.

21, 2014

10:00 PM, Sept.

28,2014 7 Days

6 System Design Prototyping N/A

7 System Modelling N/A

3.3 Success Criteria

The APARTMS must attain the following criteria:

It monitors/manages the financial statement efficiently, provided with a

exact and tallied reports (20%)

It has a fast processing speed (5%)

Functionality (10%)

User-Friendly features (15%)

Import/Export execution (40%)

Zero-Data Redundancy system (10%)

3.4 Issues and Policy Implications

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 5

Bestlink College of the Philippines

For legality issues, al reports being produced by APART MS must be valid

and detailed.

APART MS is not allowed to be duplicated for own purposes. It was

created for business and school use only.

Selected personnel will be allowed to manage and maintain the

application software, with the approval of the stakeholders

Any technicalities being encountered in using APART MS software must

be addressed immediately, with the approval of the stakeholders.

In case of system upgrade, a contract between the stakeholders and the

proponents must be provided and must follow the legal issues of software

by-laws.

3.5 Risk Management

Risk FactorProbability(H-M-L)

Impact(H-M-L) Risk Management Action

Economical Changes H H Proper Budgeting

Competition H H Cheaper Software

User Demands M M User-related

Technical related risks M M Back-ups

3.6 Service Transition

These are the following activities that the company will surely comply

regarding with the system’s software, hardware, system specifications, computer

personnel, system requirements and implementation procedure.

The company must invest new desktop/ Laptop computers.

At least one (1) Printer for each department

One computer administrator per department

Higher Specification of hardware for each computer unit

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 6

Bestlink College of the Philippines

Conducting a proper training for the employees when the system has

been implemented

Regular Maintenance of the system software

Upgrade of the system software (depends on the client)

Implementing the accessibility to the system according to the position

of the company (user, admin, manager etc.)

3.7 Option Analysis4.0 TECHNICAL FEATURES

Login Information, accessed only by the Administrator and User.

Form which includes payables table, with amount, date, and description label.

Treasury and fund viewing, in which the amount is defined in Peso.

Report form, ready to print.

5.0 PROJECT ORGANIZATION AND STAFFING

ROLE NAME AND CONTACT INFORMATION

RESPONSIBILITIES

Project Manager Manayan, Jun • Developing the project plan

• Managing the project stakeholders

• Managing Communication

• Managing the project team

• Managing the project risk

• Managing the project schedule

• Managing the project budget

• Managing the project conflicts

• Managing the project delivery

System Analyst Langcauon, Joefel • Identify, understand and plan for

organizational and human impacts

of planned systems, and ensure

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 7

Bestlink College of the Philippines

that new technical requirements are

properly integrated with existing

processes and skill sets.

• Plan a system flow from the ground

up.

• Interact with internal users and

customers to learn and document

requirements that are then used to

produce business requirements

documents.

• Write technical requirements from a

critical phase.

• Interact with designers to

understand software limitations.

• Help programmers during system

development

• Perform system testing

• Deploy the completed system.

• Document requirements or

contribute to user manuals.

• Whenever a development process

is conducted, the system analyst is

responsible for designing

components and providing that

information to the developer.

Business Analyst Cabigas, Jayson • Business focused

• Domain specific knowledge

• Solve operational problems

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 8

Bestlink College of the Philippines

• Solves business process problems

• Refines the business model

Programmer Goron, Mac Douglas • System Coding

• Handling System Software

• Program Development

• Perform System Analysis

• Train subordinates in

programming

• Develops programming methods

• Correct errors on the system

coding

Document Specialist San Diego, Mark Christian

• Documenting the process

• Craft the right message

• Distil the message into effective

documents

• Release the documentation

• Evaluate the results

6.0 PROJECT BUDGET

Budget Items Description Budget Cost

One – Time Cost

PS1 Payment Php 1,000 *5

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 9

Bestlink College of the Philippines

Payment for the defense of the PS1

documentation of the proponents.

PS1 expenses are compulsory

payment of the proponents.

PS1 Manual / Book This manual is used as a preference

of the proponents in developing the

PS1 documentation. Php 300 *5

Total One – time Cost Php 6,500

Budget Items Description Budget Cost

Ongoing Cost

Food

Food expenses are absolutely

important for the proponents to avail.

This will also included into the

ongoing cost for the project

development. Php 1,500 / month

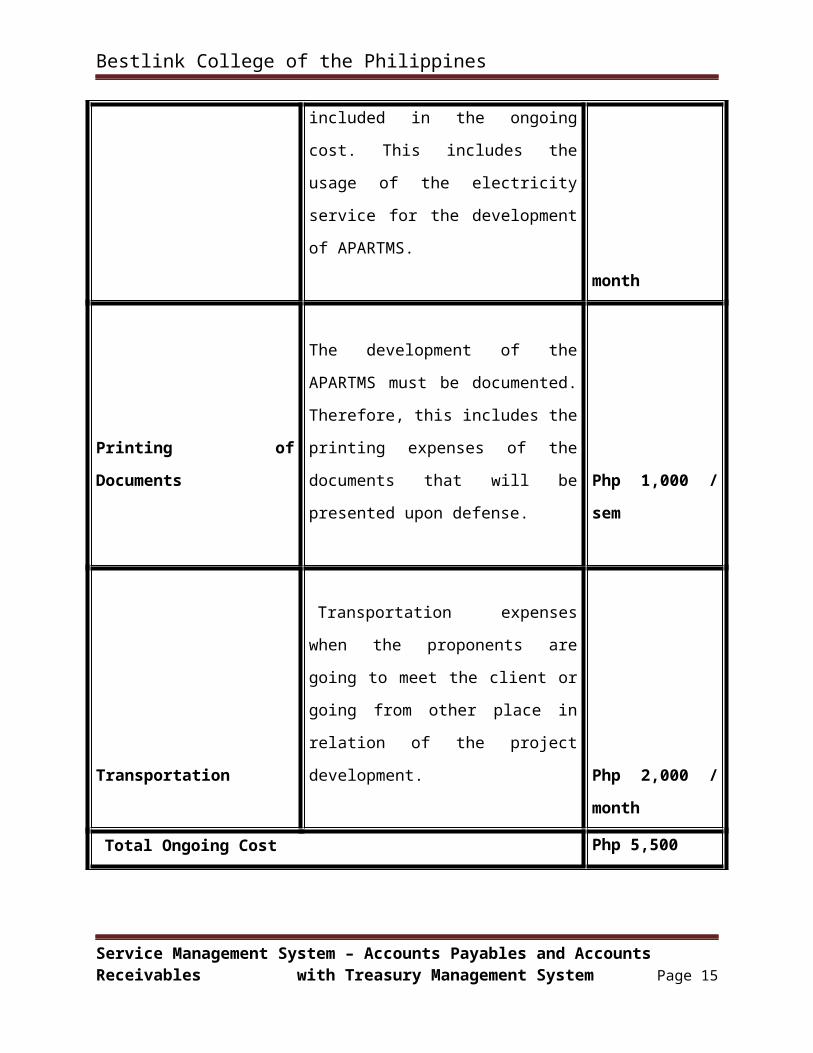

Electricity

Electricity expenses also included in

the ongoing cost. This includes the

usage of the electricity service for the

development of APARTMS. Php 1,000 / month

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 10

Bestlink College of the Philippines

Printing of Documents

The development of the APARTMS

must be documented. Therefore, this

includes the printing expenses of the

documents that will be presented

upon defense. Php 1,000 / sem

Transportation

Transportation expenses when the

proponents are going to meet the

client or going from other place in

relation of the project development. Php 2,000 / month

Total Ongoing Cost Php 5,500

Chapter II – Related Studies and Systems

1.0INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS DETERMINANTS OF ACCOUNTS RECEIVABLE AND ACCOUNTS PAYABLE: A CASE OF PAKISTAN TEXTILE SECTOR

ABSTRACTThe objective of this study is to analyze the determinants of Pakistani listed

companies’ accounts receivable and accounts payable focusing the textile sector. It is

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 11

Bestlink College of the Philippines

evident from the findings that accounts receivable are strongly affected by the firm’s

incentive to use trade credit as a means of price discrimination and level of internal

financing. Additionally, the size of the firm also affects the level of accounts receivable a

firm maintains. Whereas, most significant determinants of accounts payable are size of

the firm, level of purchases and market interest rate.

INTRODUCTIONIn corporate finance trade credit has been supposed to be a nonissue for a long

time, at least in the context of perfect markets (Sartoris and Hill, 1988). Nevertheless, it

is observed that a significant quantity of cash is invested in accounts receivable and an

enormous amount of accounts payable, as a source of financing in nearly all non-

financial firms (Deloof and Jegers, 1999). Significance of trade credit differs among the

countries and it is expected to be higher in the countries which produce more

manufacturing products, although there is substantial difference across them (Marotta,

1998). Rajan and Zingales (1995) compared non-financial companies in the G7

countries and found that relative part of accounts receivable differs between 29% Italy

and 13% Canada, on the other hand, the respective limits for accounts payable were

17% France and 11.5% Germany. Mian and Smith (1992) reported that in 1986 US

manufacturing firms had 21 percent of accounts receivable of their total assets and

about 40% of account payable of their total liabilities. Deloof and Jegers, (1999)

reported that in 1995 Belgian non-financial firms’ accounts receivable were 16% of total

assets, and accounts payable 12% of total liabilities. Several studies have been

conducted to simply analyze the existence of trade credit (see a.o. Schwartz, 1974;

Feriss, 1981; Frank and Maksimovic, 1998; Long, Malitz and Ravid, 1993; Brennan,

Maksimovic and Zechner, 1988; Brick and Fung, 1984; and Emery, 1984 and 1987), but

very few studies have discussed the reason behind the trade credit is offered or which

corporations use it or delivers it most (Petersen and Rajan, 1997). Storey (1994)

analyzed earlier work on the financing patterns of UK small companies and found that

for small firms trade credit is more valuable than for large firms. Whereas Walker (1991)

investigated the US small firms and found that US small firms are also relying on trade

and bank credit and these two financing sources are being used as substitutes.

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 12

Bestlink College of the Philippines

Furthermore, it is always argued that borrowing at rational rates is an issue for

corporate decision makers. Berger and Udell (1998) suggested that when borrowing

outside the firm, small firms face particular restrictions. Borrowing a small amount of

capital from external capital markets becomes their obstacle, which is usually called as

Macmillan gap, and for this reason they are being offered higher interest rates (Storey,

1994). While market imperfections, just as, agency costs and asymmetric information,

are the reasons of these issues as proposed by several economic theorists. Even risky

debt has a preference when information asymmetries are not favorable. Mayers (1984)

pointed out this situation as ‘pecking order’ theory of financing in which a firm first raises

capital internally by reinvesting its net income and selling off its short-term marketable

securities. When that supply of funds is exhausted, the firm will issue debt and perhaps

preferred stock. Only as a last resort will the firm issue common stock. Whereas, it has

also been reported by several studies that close bank-borrower association improves

credit accessibility (Niskanen and Niskanen, 2006). Other studies propose that the

availability of credit is affected positively by bank-borrower relationship (Petersen and

Rajan, 1994).

LITERATURE REVIEWDanielson and Scott (2004) investigated the effect of bank loan availability on

the trade credit and credit card demand of small firms and found that firms increase

their demand for trade credit and credit card debt when facing credit constraints

are imposed by banks. Deloof and Jegers (1999) investigated the role of trade

credit as source of financing for Belgian firms focusing accounts payable and found

that trade credit plays a significant role in the corporate financing policy. They

found that the amount of trade credit a customer takes is determined by the need

for funds and by the internally available funds. Finally they found that trade credit

can act as a vital substitute for short term as well as long term financial debt.

Atanasova (2007) tested for the existence of creditconstraints and their effect on

the corporate financing policies and found that credit constrained firms substitute

trade credit to institutional finance especially during tight money periods.

Huyghebaert (2006) tested hypothesis that why firms use trade credit on business

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 13

Bestlink College of the Philippines

start-ups and find that more trade credit is used when firms face financial

constraints and suppliers have a financing advantage over banks in financing high

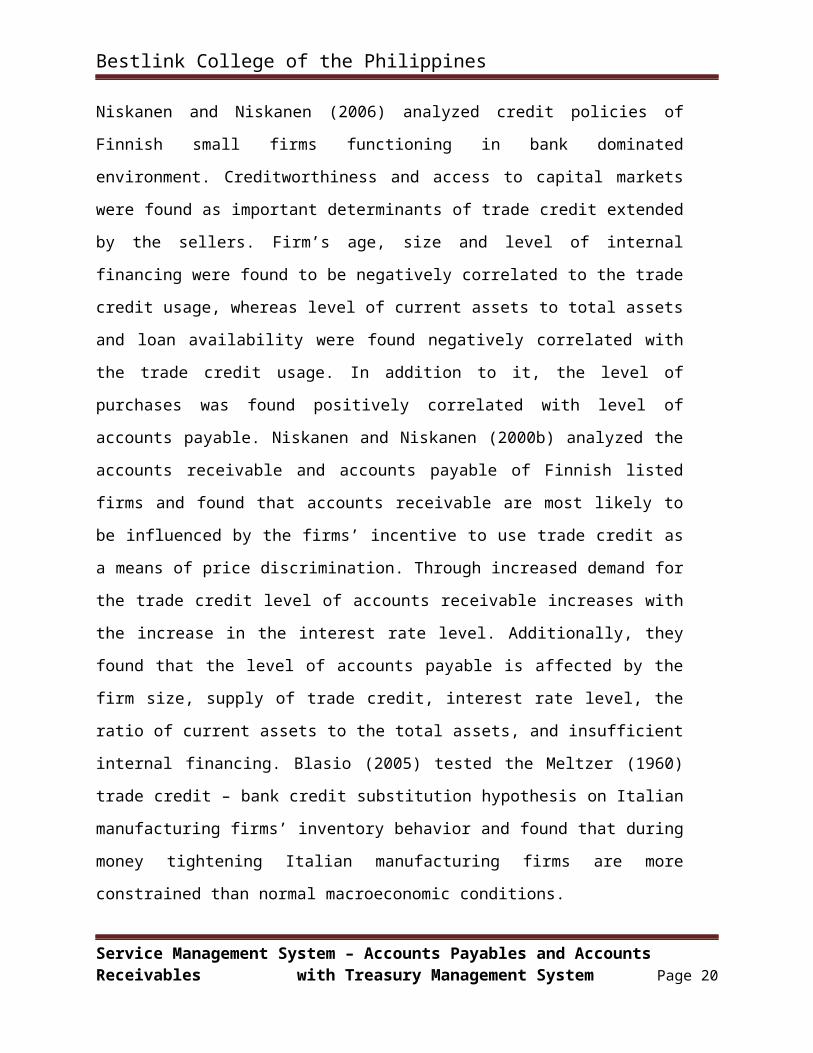

risk firms. Niskanen and Niskanen (2006) analyzed credit policies of Finnish small

firms functioning in bank dominated environment. Creditworthiness and access to

capital markets were found as important determinants of trade credit extended by

the sellers. Firm’s age, size and level of internal financing were found to be

negatively correlated to the trade credit usage, whereas level of current assets to

total assets and loan availability were found negatively correlated with the trade

credit usage. In addition to it, the level of purchases was found positively correlated

with level of accounts payable. Niskanen and Niskanen (2000b) analyzed the

accounts receivable and accounts payable of Finnish listed firms and found that

accounts receivable are most likely to be influenced by the firms’ incentive to use

trade credit as a means of price discrimination. Through increased demand for the

trade credit level of accounts receivable increases with the increase in the interest

rate level. Additionally, they found that the level of accounts payable is affected by

the firm size, supply of trade credit, interest rate level, the ratio of current assets to

the total assets, and insufficient internal financing. Blasio (2005) tested the Meltzer

(1960) trade credit – bank credit substitution hypothesis on Italian manufacturing

firms’ inventory behavior and found that during money tightening Italian

manufacturing firms are more constrained than normal macroeconomic conditions.

THEORIESAND EMPIRICAL EVIDENCES ON TRADE CREDITVarious theoretical studies have tried to investigate the reason of providing

intermediary services by suppliers to their customers and to find out the rationale to

use trade credit as a substitute of less costly bank debt.

Transaction CostTransaction Costs have been declared to be one rationale to sustain

credit sales. Transaction costs theory describes that paying at once for

several shipments collectively saves transaction costs and permits flexibility

in payments (Ferris, 1981).Furthermore, money can be saved by keeping

smaller cash balances.

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 14

Bestlink College of the Philippines

Financial ModelsFinancial models are based on capital market imperfections concerning

information asymmetries. These imperfections lead to the phenomena in

which firms, with lower cost of financing due to their better access to capital

markets, tender trade credit to other financially constrained firms (Schwartz,

1974). Furthermore, trade credit facilitates firms to support the growth of

their clients. It is also believed that trade credit can serve to alleviate credit

rationing problems as trade credit plays as a signal on the buyers’ good

quality to the financially intermediary (Frank and Maksimovic, 1998; Biais

and Gollier, 1997).

Financial theory proposes that the seller has a lead over financial

institutions in information gaining and controlling the consumer. In European

countries, all these gains speak about the nearer and greater relationship

between buyer and seller than between the financial institutions and buyers.

That is supplier have a threatening tool to stop future supplies when

consumer does not pay in time. On the other hand a financial institution may

not have a device like this to have power over consumers, while warning to

depart future lending may not have instant consequence on the consumers’

attitude (Petersen and rajan, 1997).

Price Discrimination

Price discrimination is a possibility of charging dissimilar prices for dissimilar

consumers. This can happen in a situation when credit conditions include

discounts on paying before time. These conditions are mostly presented by

leading firms in the industry (Brennan et al., 1988; Mian and Smith, 1992). These

firms have an advantage to collect extra sales to existing clients without

decreasing price. As a result these firms extend high priced trade credit which is

not acceptable for creditworthy customers. While for low rating companies this

credit may be acceptable as it might be less costly than borrowing from financial

intermediary (Brennan et al., 1988; Petersen and Rajan, 1997). Additionally,

trade credit offers a facility to gauge the quality of products earlier than paying for

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 15

Bestlink College of the Philippines

it so this becomes an inherent guarantee for the seller’s manufactured goods

(Lee and Stowe, 1993). For small and less reputable sellers this facility of trade

credit may have a great importance (Frank and Maksimovic, 1998).

Macroeconomic Conditions

Macroeconomic conditions have also an effect on trade credit usage and

conditions which cannot be ignored and has been highlighted by many

researches. Kashyap et al., (1993) investigated the effect of macroeconomic

factors on trade credit and found that under restrictive monetary policy and

controlled money supply smaller firms are ready to extend trade credit on the

given conditions as increasing borrowing rates create trade credit a

supplementary viable type of short term funding. Petersen and Rajan (1997)

highlighted the same issue and found that firms extend trade credit when loan

from financial intermediaries is not present. They further added that, in this

scenario, the role of financial intermediary will be performed by larger suppliers

as firms having no access to institutionalized financial markets will borrow from

these larger firms.

Data Description and Dependant VariablesThe data sample of this study comprises of financial accounting information of

the firms listed at Karachi Stock Exchange during 2004 to 2009.This accounting data is

extracted from the Balance Sheet Analysis published by the State Bank of Pakistan.

After excluding missing firm year data from analysis 891 observations were analyzed

from 151 firms.

Results:DETERMINANTS OF ACCOUNTS RECEIVABLE

Carrying receivables has both direct and indirect costs but it also has an

important benefit that is increased sales. Receivable management begins with the

credit policy, but a monitoring system is also important. Corrective action is often

needed, and the only way to know whether the situation is getting out of hand is with

a good receivables control system.

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 16

Bestlink College of the Philippines

Demand for Trade CreditA firms’ decision on how much to lend to its customers is determined

from the level of firms’ accounts receivables. Still the quantity of trade credit,

a firm offers, is influenced by a demand component (Petersen and Rajan,

1997). This demand on the whole is not possible to compute directly as

approaches of nearly all firms’ consumers to trade credit varies. This is due

to the reason that, just for example, a retail company can contain thousands

of credit consumers which can be either persons or other firms. Whereas,

the accounts payable of a particular company, can be similar in greater part

as they are payable to the other companies which are comparatively little in

number in any particular industry. As the demand curve for trade credit is

not identified, interpretation of estimated coefficients can help in

understanding this problem.

Petersen and Rajan (1997) found that large firms maintain higher

accounts receivables. One reason for this result can be, the greater access

of larger firms to capital markets which makes them less capital reserved.

Second reason can be the demand component from capital rationed firms

that causes the accounts receivable of larger firms higher than average.

Creditworthiness and Access to Capital MarketsFirm size and age are used to compute the firm’s creditworthiness and

access to capital markets. The natural log of firm age (Ln(1+ firm age)) is used as

proxy for creditworthiness and natural log of total assets (Ln(book value of

assets)) is taken to proxy the suppliers’ access to external capital. The results in

the Table 1 show that size is significant variable with (p = 0.000102129). These

results are consistent with earlier studies like Petersen and Rajan’s(1997).

Internal FinancingThe study uses operating cash flow (earnings before depreciation and interest

minus taxes) divided y assets to gauge the firm’s capability to produce cash from

internal sources to fund the trade credit which it extends to its customers. The

results indicate that internal financing effects positively to the level of accounts

receivables. The variable is positive and significant at (p= 0.00000000) which

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 17

Bestlink College of the Philippines

indicates that the larger the positive cash flow the supplier has, the higher the

trade credit he is ready to offer to its customers. The results are consistent with

findings of Niskanen and Niskanen (2000) and are contradictory to the findings of

Petersen and Rajan (1997).

Model I: AR = β0 + β1CF + β2CM + β3GR + β4KIB + β5SIZETable 1: Dependant Variable:

Accounts Receivable/Assets

β0 β1 β2 β3 β4 β5

Coefficient

-

42.702 1.457* -698.612* 0.0533 0.634 15.291*

S.E 26.690 0.110 123.976 0.179 1.197 3.892

P-Value (0.110) (0.000) (0.000) (0.766) (0.596) (0.000)

R-Square 0.384 F-Value 45.596*

Adjusted-

R2 0.376 (0.000)

DW 1.037

*Significant at

α = 0. 01 **

Significant at

α = 0. 05

Price DiscriminationPrice discrimination is an act of billing the same product to different clients

with different prices, even when the costs of supplying them are same. This

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 18

Bestlink College of the Philippines

practice is mostly observed by monopolists as they exploit their leading power for

discrimination. This study uses ratio of contribution margin (sales minus variable

costs) to assets to proxy for monopoly power to carry out price discrimination. In

our sample of all textile firms existing on Karachi Stock Exchange, it is found that

a significant but a negative relationship exist between price discrimination and

accounts receivable management policies which is validated by a p value of (p=

0.00000004). These results are contradictory to the findings of

Niskanen&Niskanen (2000).

Cost Of Alternative CapitalThe study uses annual average three month KIBOR rate to compute the basic

cost of capital. A positive relationship is expected between accounts receivable

level and level of interest rate. The reason behind this can be the demand for

trade credit which can be expected to be high when the cost of alternative capital

is increased. An insignificant coefficient is found in the results Table 1 with value

of (p= 0.59654834).

GrowthNormally firm’s target growth rates are attached with its trade credit policies.

Generally, credit conditions just as discounts and duration of payments play a role of

competitive instruments. In order to increase sales, firm may select a policy of offering

trade credit with delayed due periods than its competitors are offering. This proposes

that there is a positive relationship between growth and the level of accounts receivable.

Though, trade credit may be used to boost sales of those firms which could not maintain

a smooth rise in their sales. Even in conditions of declining sales a firm may offer more

trade credit than an average company in the industry (Petersen and Rajan, 1997).This

study computes growth by the annual sales growth percentage. Empirically, it is found

that sales growth is insignificant (p= 0.766271766) which can be interpreted as the

sales growth does not affect the level of trade credit offered.

DETERMINANTS OF ACCOUNTS PAYABLE (TRADE CREDIT)Firms generally make purchases from other firms on credit, recording the debt as

an account payable. Accounts payable, or trade credit, is the largest single category of

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 19

Bestlink College of the Philippines

operating current liabilities, representing about 40% of the current liabilities of the

average US nonfinancial corporations. The percentage is somewhat larger for smaller

firms. Because small companies often do not qualify for financing from other sources,

they rely especially heavily on trade credit. Table 2 presents the outcome of proposed

determinants on which the accounts payable is regressed. This model uses the same

variables (including the control variables) used for accounts receivable model. Besides

these variables, two more variables are added in this model. First, to determine the

asset maturity RATIO OF CURRENT ASSETS (INVENTORIES AND FINANCIAL

ASSETS) TO TOTAL ASSETS is used. Second, to assess the supply of trade credit

PURCHASES TO TOTAL ASSETS is used.

Supply of Trade CreditNiskanen and Niskanen (2000) use the annual purchases as a proxy for the

supply of trade credit making an assumption that all purchases are on credit.

They believe that this assumption is not very restrictive, as large companies

normally do not pay their purchases in cash. This study also uses the purchases

as proxy to supply of trade credit and considers the same assumption. The result

relating the supply of trade credit is same as expected: a significant and positive

coefficient is obtained (p= 0.0005) which indicates that an increase in the supply

of trade credit increases the level of its use.

Creditworthiness and Access to Capital MarketsResult concerning asset size is quite significant in explaining the accounts

payable level. The coefficient is positive and significance level is also quite high

(p= 0.0000). This positive sign shows that financing of larger firms is comprised

of more trade credit than smaller firms. This may be due to their greater access

to capital markets. This finding is consistent with Niskanen and Niskanen (2000)

where as Petersen and Rajan (1997) found a weak positive relationship between

the firm size and accounts payable.

Model No II:

AP = β0 + β1GR + β2CA + β3SIZE + β4KIB + β5CF + β6PUR

Table 2: Dependant Variable:

Accounts Payable

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 20

Bestlink College of the Philippines

β0 β1 β2 β3 β4 β5 β6

Coefficien

t

-

1273.16

1

-

0.84828

6

2.22140

9

225.909

2

9.69028

8 0.426306

0.10307

7

S.E

89.4942

1

0.26570

5 0.592596

14.8522

1

2.51317

1 0.156219

0.02944

1

P-Value (0.0000) (0.0015) (0.0002) (0.0000) (0.0001) (0.0066) (0.0005)

R-Square

0.64379

0 F-Value 157.5394*

Adjusted-

R2

0.63970

4

(0.000

)

DW

0.83927

6

*Significant at

α = 0. 01 **

Significant at

α = 0. 05

GrowthTheory suggests that healthier investment opportunities are available to the

firms which are growing and these firms require increased financing for these

new investment opportunities. It is assumed that trade credit may be used as

fractional source of financing for these growing firms. However, opposite is found

from empirical results. Sales growth is found to have a negative but significant

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 21

Bestlink College of the Philippines

coefficient (p= 0. 0015) which implies that faster a firm is growing the less it uses

trade credit in its financing. Hence, firms growing slowly or not growing at all

utilize the trade credit most. Furthermore, these results are consistent with

Niskanen and Niskanen (2000) and contradictory to the findings of Rajan and

Zingales (1997).

Internal FinancingThe results reveal that operating cash flow is a significant variable in

explaining the accounts payable level with p-value of (p= 0066).

Asset MaturityIn explaining the level of accounts payable the asset maturity, measured

by the ratio of current assets to the total assets, is found to have a greater

proportion with a significant positive variable (p= 0002). This finding is

consistent with the view that firm’s assets are financed with funds having

same maturities. This is carried out to plan repayments of the funding to

match with the decline in the value of firm’s assets (Diamond, 1991). As a

result, short-term assets are usually financed with short-term debt just as

accounts payable, while long-term assets are financed with long-term debt

or equity.

Cost of Alternative CapitalMarket interest rate, measured as average 3 month KIBOR rate, is

appeared to be quite significant explanatory variable in explaining accounts

payable (p= 0001). Positive coefficient of market interest rate shows that

higher the interest rates the higher the demand for trade credit will be. As it

is vivid from the results that market interest rate is not significant in accounts

receivable model, this may support the idea that demand side is more

affected by the fluctuations in the market interest rate.

CONCLUSIONThis study empirically analyzed the determinants of Pakistani listed firms

accounts receivable and accounts payable management policies. The results show

that accounts receivable are strongly affected by the firms’ incentive to use trade

credit as a means of price discrimination and level of internal financing.

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 22

Bestlink College of the Philippines

Furthermore, size of the firm also affects the level of accounts receivable a firm

maintains. The results of the accounts payable model show that all the variables,

which were taken to determine the level of accounts payable, were statistically

significant. Additionally, most significant determinants of accounts payable were

size of the firm, level of purchases and market interest rate. Dissimilarity in the

results of this study to earlier studies may greatly be due to the variation among

Pakistani, U.S., UK and Finnish capital markets. As it is evident, that ban-borrower

relationship, when analyzed as financial intermediaries, is supposed to be a

substitute source of capital for trade credit. This relationship can be studied as

further research line in this area. But the unavailability of data on this relationship

makes it bit a difficult task as statistics regarding relationship between banks and

firms are not publicly available.

REFERENCE: www.journal-archieves14.webs.com/240-251.pdf

2.0 IMPACT OF ACCOUNTS RECEIVABLE MANAGEMENT ON THE PROFITABILITY DURING THE FINANCIAL CRISIS: EVIDENCE FROM SERBIA

ABSTRACT:The competitive nature of the business environment requires firms to adjust

their strategies and apply financial policies to survive and enable growth. In most

firms, receivables represent large financial sources invested in asset and involve

significant volume of transactions and decisions. This paper investigates how

public companies listed at the regulated market in the Republic of Serbia manage

their accounts receivables during the recession times. A sample of 108 firms is

used, which are the most successful Serbian firms listed at the Prime and Standard

Listing as well as the Multilateral Trading Platform of the Belgrade Stock

Exchange. The accounts receivables policies are examined in the crisis period of

2008-2011. In order to explore the relation between accounts receivables and

firm’s profitability, the short-term effects are tested. The study shows that between

accounts receivables and two dependent variables on profitability, return on total

asset and operating profit margin, there is a positive but no significant relation. This

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 23

Bestlink College of the Philippines

suggests that the impact of receivables on firm’s profitability is changing in times of

a crisis.

INTRODUCTIONAccounts receivable measures the unpaid claims a firm has over its customers at

a given time, usually comes in the form of operating line of credit and is mainly due

within a relatively short time period (up to one year). The volume of accounts receivable

indicates firm's supply of trade credit while accounts payable shows its demand of trade

credit. The study of accounts receivable and accounts payable during periods of

financial crisis is an important topic, particularly when the global economy is going

through a credit shock. During global financial crisis, characterized by high liquidity risk

faced by the banks, trade credits may increase, operating as a substitute for bank

credits, or decrease - acting as their complement. Bastos and Pindado (2012), for

example, suggest that credit constraints during a financial crisis cause firms holding

high levels of accounts receivable to postpone payments to suppliers, which act in the

same manner with their suppliers. This gives rise to a trade credit contagion in the

supply chain characterized by a cascading effect. The current financial crisis provides

economists a unique opportunity to study the role of alternative financial sources during

periods of breakdown of institutional financing.

Accounts receivables are one of the most important part of working capital.

Receivables often represent large investment in asset and involve significant volume of

transactions and decisions. However, there are considerable differences in the level of

receivables in firms around the world. Demirgüç-Kunt and Maksimovic (2001)present

evidence that in countries such as France, Germany, and Italy accounts receivable

exceeds a quarter of firms' total assets, while Rajan and Zingales (1995) find that 18%

of the total assets of US firms consists of receivables. In different theories, the existence

of receivables is explained by commercial reasons, transaction-cost motivations, and

financial incentives (Bastos&Pindado, 2007; Deloof&Jegers, 1999; Marotta, 2005;

Petersen &Rajan, 1997).Accounts receivable management is a crucial filed of corporate

finance because of its effects on a firm’s profitability and risk, and consequently on the

firm's value. Yet, the main body of the literature of accounts receivables focuses on

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 24

Bestlink College of the Philippines

studying the relation with firm’s profitability at the developed capital markets and during

the non-crisis period.

Understanding the effects of a financial crisis on receivables management is

especially important to Serbia as a transition country. Trade credit is an important

source of finance for Serbian firms and, therefore, it can make a strong contribution to

firms' profitability and the development of the whole economy. In this context, the aim of

this paper is to examine the impact of accounts receivable management on the

profitability of the Serbian companies during the financial crisis, in the period 2008-

2011. The study investigates whether companies have to change their non-crisis

accounts receivables management policies when the economy is into a recession. In

order to test the relation between accounts receivables and a firm’s profitability, the

short-term effects will be tested in times of a crisis.

The contribution of the paper is twofold. Firstly, it extends the existing empirical

literature on relationship between firm's profitability and accounts receivables in

developing and transitional economies in the crisis period, by focusing the analysis on

the Serbian listed firms where, up to now, no research has been conducted. Secondly,

this study verifies some of the previous findings by testing the relationship between

accounts receivables management and the profitability of the sample firms, and thus

broadens the possibilities for cross-country comparisons in the field of profitability

determinants.

The structure of this paper is as follows. In Section 1,a summary of previous

research on the effects of accounts receivable management on firm's profitability is

given. In the next section we describe the sample, define the measures of profitability as

well as the explanatory variables, and finally, test the potential determinants of on

profitability. In Section 3we provide conclusions, emphasize some limitations of the

study and propose the objectives of future research.

LITERATURE REVIEWThe goal of accounts receivables management is to maximize shareholders

wealth. Receivables are large investments in firm's asset, which are, like capital

budgeting projects, measured in terms of their net present values (Emery et al., 2004).

Receivables stimulates sales because it allows customers to assess product quality

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 25

Bestlink College of the Philippines

before paying, but on the other hand, debtors involve funds, which have an opportunity

cost. The three characteristics of receivables – the element of risk, economic value and

futurity explain the basis and the need for efficient management of receivables.

According to Berry and Jarvis (2006) a firm setting up a policy for determining the

optimal amount of account receivables have to take in account the following:

The trade-off between the securing of sales and profits and the amount of

opportunity cost and administrative costs of the increasing account receivables.

The level of risk the firm is prepared to take when extending credit to a

customer, because this customer could default when payment is due.

The investment in debt collection management.

Academicians have studied accounts receivable individually, but mostly as a part

of working capital management, from various points of view. Bougheas et al. (2009), for

example, focuses the research on the response of accounts receivable to changes in

the cost of inventories, profitability, risk and liquidity. The other authors explore the

impact of an optimal receivables management, i.e. the optimal way of managing

accounts receivables that leads to profit maximization. Researches realized by

Deloof(2003), Laziridis and Tryfonidis (2006), Gill et al (2010), Garcia-Teruel and

Martinez-Solano (2007), Samiloglu and Demirgunes (2008) andMathuva (2010) done in

Belgium, Greece, USA, Spain, Turkey, and Kenyarespectively, all point out to a

negative relation between accounts receivables and firm profitability (Table 1). In other

words, having an accounts receivable policy which leads to a low as possible accounts

receivables has as a result the highest profitability. Contradicting evidence is found by

Sharma and Kumar (2011), who find a positive relation between ROA and accounts

receivables.

Table 1: Summary of previous research on the effects of receivables turnover on firm’s profitability

Research Sample, period Type of relation

Deloof (2003) 1009 large Belgian non-financial firms for the Significant negative

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 26

Bestlink College of the Philippines

1992-1996 period relation on

profitability

Lazaridis and 131 companies listed in the Athens Stock Significant negative

Tryfonidis (2006) Exchange (ASE) for the period of 2001-2004 relation on

profitability

Gill et al (2010) 88 American firms listed on New York Stock Significant negative

Exchange for the period 2005 – 2007 relation on

profitability

García-Teruel and 8,872 Spanish SMEs for the period 1996-2002 Significant negative

Martínez- relation on

Solano(2007) profitability

Samiloglu and Istanbul Stock Exchange (ISE) listed Significant negative

Demirgunes (2008) manufacturing firms for the period of 1998-2007 relation on

profitability

Mathuva (2010) 30 firms listed on the Nairobi Stock Exchange Significant negative

(NSE) for the periods 1993 to 2008 relation on

profitability

Sharma and Kumar 263 non-financial BSE 500 firms listed at the Significant positive

(2011) Bombay Stock (BSE) from 2000 to 2008 relation on

profitability

Baveld (2012) 37 large firms in The Netherlands, during the Significant negative

non-crisis period of 2004-2006 and during the relation on

Financial Crisis of 2008 and 2009 profitability

However, the main body of the literature of accounts receivables focuses on studying

in the environment of developed capital markets and during the non-crisis period. The

consequences of a financial crisis on receivables is of enormous relevance, since a

crisis causes trade credit contagion as a consequence of financial contagion between

financial intermediaries (Bastos and Pindado, 2012). Researches on trade credit

during financial crises are done in case on Japan's crisis (Fukuda et al., 2006), for the

Asian crisis (Love et al 2007) and for the recent global financial crisis (Yang, 2001,

Bastos and Pindado, 2012). As to researches that study relationship between

profitability and accounts receivables during current global crisis period, it is worth

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 27

Bestlink College of the Philippines

mentioning the study done by Baveld (2012). It this study that investigates how public

listed firms in The Netherlands manage their working capital, two periods are

compared - the non-crisis period of 2004-2006 and the financial crisis period of 2008 -

2009. Baveld'sstudy indicate a statistically significant negative relation between

accounts receivables and gross operating profit during non-crisis period. On the other

hand, during crisis period, no significant relation between these two variables is

observed. This result may suggest that the relation between accounts receivables

and firm’s profitability is changed in times of a crisis in the way that some firms should

not keep their accounts receivables at minimum in order to maximize profitability

during crisis periods.

Taking into consideration the results of study done by Baveld (2012) and the

others above mention studies, the aim of this research is to examine the impact of

accounts receivable management on the profitability of the Serbian companies during

the financial crisis, in the period 2008-2011.

EMPIRICAL ANALYSISSample and Data Description

We tested the regression model of profitability on the sample consisting of

real-sector publicly traded companies whose shares are quoted on the regulated

market of the Belgrade Stock Exchange. We compiled the basis of financial

statements (source: Serbian Business Registers Agency - SBRA) for those

publicly-listed companies that were quoted in all the segments of regulated stock

exchange market, that met the size criterion in all analyzed years (meaning big or

medium enterprises) and operated in real sector (financial firms are excluded

from the sample). In such an initial stadium of defining the sample, we had 432

firms in total. After the Decision on Stock Exchange Reorganization, brought on

27/04/2012, we excluded from the sample all the companies shifted from OTC

market to be quoted in MTP (Multilateral TradingPlatform) segment, since they

did not belong to Regulated market and were not activein the previous 180 days

regarding share trading of the particular issuer. We also excluded companies

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 28

Bestlink College of the Philippines

with consolidated financial statements in any of the analyzed years, as well as

those companies whose loss was over the amount of capital so that they were

practically financed only from borrowed sources, and accordingly, the value of

financial leverage equals one.

The sample contains the financial data for 4 years in sequence, in period

from 2008 to 2011. The final sample, representing the basis for the empirical

study, comprises a total of 108 big and medium publicly-listed non-financial

companies, whose shares are quoted on the regulated segment of the Belgrade

Stock Exchange. These companies are mostly the result of mass corporatization

in Serbia at the beginning of 21st century, as a part of the process of Serbian

transition to market economy and private property. The most significant share in

the sample structure by the criterion of sector or business belongs to companies

from processing industry (52%), agriculture, forestry and fishing (14,9%),

transportation and storage (10,2%) and construction (8,4%).Financial statements

of these companies are prepared following the International Accounting

Standards (IAS), or International Financial Reporting Standards (IFRS).

Total number of observations for each variable is 432 (108*4). When we

consider the four-year value average or the value for one year only, total number

of observations is 108. We have processed the data from companies’ financial

statements and calculated dependent and independent variables within the

regression model, which is defined in the following text.

Descriptive statisticsThe ratio analysis mainly uses two types of profitability measures –

margins and returns. Margins ratios(Gross profit margin, Operating profit margin,

Net profit margin, Cash-flow margin)describe the firm's ability to translate sales

into profits at various stages of measurement. Ratios that calculate returns

represent the firm's ability to measure the overall efficiency of the firm in

generating returns for its shareholders (Return on asset, Return on equity,

Return on capital, Cash return on assets and so on). Many different

measurements of firm profitability are used by the researchers who studied the

relation between accounts receivable and profitability. The simplest and the most

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 29

Bestlink College of the Philippines

used ratio, that relates the profitability of a company with its assets, is Return on

Assets (ROA). It is calculated as net income divided by total assets.

Two profitability measures are used in this study: Operating Profit Margin

(OPM), calculated as operating profit divided by total assets and Return on Total

Assets (ROTA) calculated as earnings before interest and tax divided by total

assets. ROTA measures the ability of general management to utilize the total

assets of the business in order to generate profits, while Operating Profit Margin

shows the profitability of sales resulting from regular business. Operating income

results from ordinary business operations and excludes other revenue or losses,

extraordinary items, interest on long term liabilities and income taxes.

The descriptive statistics of two profitability measures and explanatory

variables are reported in Table 2, while the correlation matrix is presented in

Table3. The measures of profitability, as well as the explanatory variables

(receivables turnover ratio, accounts receivable to revenue ratio, size and

liquidity), are averaged for the period 2008-2011. Size is the natural logarithm of

net sales. Liquidity is measured by current ratio (current assets/current liabilities).

Receivables turnover ratio measures the average period for which sales revenue

will be held in accounts receivable. This ratio is usually used to describe the

efficiency and effectiveness of receivables collection. The trends in accounts

receivable to revenue ratio highlight tendency in the degree of investment in

accounts receivable.

The results of dependent variables, Return on Total Assets (ROTA) and

OperatingProfit Margin (OPM), exhibit that the mean of ROTA (OPM) of all firms

analyzed is0.047 (0.032). The distribution of ROTA is positively skewed, with

kurtosis of 0.083, which describes that the scores for the ROTAs are clustered

around the mean in the right-hand tail. On the other hand, the distribution of OPM

is negatively skewed, with kurtosis of 17.716, which indicates that the more

peaked distribution is skewed to the left. It can be observed that the profitability

of Serbian companies whose shares are traded on a regulated market is not at a

significant level. But, having in mind the analyzed crisis period, the fact that they

still operate in profit zone is indicative.

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 30

Bestlink College of the Philippines

The average number of days accounts receivables for the Serbian

companies listed at the regulated market is 69,5 days. This is far below the

value of RTR of the whole Serbian economy in 2011, which is, according to

Euro stat data, 128 days. The natural consequence of crisis environment is a

conservative behavior of Serbian companies. The most significant crisis effect

is related to corporate growth and is reflected in the fact that companies

postpone planned investments. All the attention is concentrated on providing

cash, given that the real sector is primarily faced with liquidity risk, and the

need for working capital is increasing in time of crisis. The difficulties in

collection of receivables are becoming serious as the crisis progresses. The

value of receivables turnover ratio continually increases in the analyzed crisis

period, starting from 66, 4 days in 2008, and reaching 73,1 days in 2011. The

increase in input prices and increased exchange rates, together with the

problematic collection of receivables affected the operating result.

Table2 Summary statistics

ROTA OPM ARRR RTR SIZE LIQ

Mean ,044636 ,032373 ,194138 69,50925 5,864046 2,400914

Median ,035425 ,03137716 ,143752 51,50000 5,816000 1,587933

Std. Deviation ,067246 ,13817079 ,136127 48,26746 ,492433 2,478863

Variance ,005 ,019 ,019 ,100 ,242 6,145

Skewness ,369 -2,883 1,120 1,151 ,408 2,850

Std. Error of Skewness ,233 ,233 ,233 ,233 ,233 ,233

Kurtosis ,083 17,716 ,692 ,867 ,016 9,891

Std. Error of Kurtosis ,461 ,461 ,461 ,461 ,461 ,461

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 31

Bestlink College of the Philippines

Minimum -,109028 -,846249 ,027984 10,0000 4,696000 ,233524

Maximum ,220683 ,377185 ,625985 228,000 7,255000 15,843705

The average value of accounts receivable to revenue ratio describes the

accounts receivables management of Serbian companies in the crisis time too.

The value of this ratio for the sample is 19,41%, telling that almost 20% of total

sales revenue is related to the unpaid sales. As the crisis progresses, from 2008

to 2011, the value of ARRR increases (from 18% to 20,4%), indicating that

theamount of cash that is tied up with the slow paying customers is growing. Yet,

this numbers are still below the share of receivables in the net revenue of 25%

evidenced in France, Germany, and Italy by Demirgüç-Kunt and Maksimovic

(2001).

The results on the average collection period for Serbian companies are

higher than the findings of some studies done in non-crisis period. Deloof (2003)

find an average of RTR of 54,64 days in Belgium, Gill et al. (2010) of 53,48 days

in the US. On the other hand, Garcia-Teruel and Martinez-Solano (2007) present

evidence on the average receivables turnover ratio for Spanish firms of 96,82

days, Samiloglu and Demirgunes (2008) and Lazaridis and Tryfonidis (2006) find

average receivables turnover ratio in Turkey and Greece is 139,07 and 148,25

respectively.

Table 3 shows correlation coefficients of all variables. ROTA and OPM are dependent

variables. Concerning the explanatory variables, relatively high correlation coefficients

(higher than 0.5) are observed only in case of ARRR and RTR. The results of the

correlation analysis shows that the number of days accounts receivables as well as

accounts receivable to revenue ratio positively relate to both the dependent variables

- return on total assets and operating profit margin. This indicates that in crisis time, a

higher level of accounts receivables could induce a higher profit in the Serbian case.

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 32

Bestlink College of the Philippines

Contradicting evidence is found with the correlation analysis of Bavald (2009), who

finds a negative relation between the number of days accounts receivables and a

firm’s profitability in the crisis time in the case of the Netherlands. The results of

Bavald's correlation analysis show a negative relation between the number of days

accounts payables and both return on assets and gross operating profit. This

indicates that managers can create value by keeping the levels of accounts

receivables to a minimum.

Table3: The correlation matrix of profitability and independent variables

ROTA OPM ARRR RTR SIZE LIQ

ROTA 1

OPM (,680)** 1

ARRR (,329)** ,142 1

RTR (,293)** ,127* (,959)** 1

SIZE (,385)** (,436)** (,283)** (,253)* 1

LIQ (,298)** (,405)** -,116 -,059 ,086 1

**Correlation is significant at the 0.01 level (2-tailed).

*Correlation is significant at the 0.05 level (2-tailed).

Sales and liquidity show also a positive relation on the dependent variables,

which is consistent with the findings of Deloof (2003), and Baveld (2012). A

shortcoming of Pearson correlations, that they are not able to identify the causes

from consequences(Deloof, 2003), will be overcome by the regression analysis.

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 33

Bestlink College of the Philippines

REGRESSION MODELThe regression analysis used in this study is based on the following equations:

• OPMit = β0 + β1ARRRit + β2RTRit+ β3SIZEit + β4LIQit +εit

• ROTAit = β0 + β1ARRRit + β2RTRit+ β3SIZEit + β4LIQit +εit

where OPM and ROA measures the firm profitability, SIZE, the company size as

measured by natural logarithm of sales, ARRR, the accounts receivable to revenue

ratio, RTR, receivables turnover ratio, LIQ, the current liquidity ratio. The analysis

utilizes fixed effect regression model for the whole sample (Table 4).

The results of regression analysis indicate a positive relation between accounts

receivables and return on total assets, which is not statistically significant. Table 4 also

shows a stronger, but positive relation between accounts receivables and the second

dependent variable – operating profit margin. This finding is not surprising taking into

account that operating profit margin describes the profitability of sales resulting from the

core business, which is highly influenced by the amount of receivables and the

collection effectiveness.

As it is pointed out by Baveld (2012), the absence of any significant relation for

both the dependent variables may indicate that the relation between accounts

receivables and firm’s profitability is changed in times of a crisis. These regression

results could be explained by the fact that Serbia is an transition and emerging market

where most of the firms are seen more profitable if they give their clients more trade

credit. Indeed, these finding are contradicting with the results on the impact on

receivables on firm's profitability in many developed counties (see Table 1), but

consistent with Sharma and Kumar (2011), who also find a positive relation between

ROA and accounts receivables in the case of India. The conclusion can be made that

large and medium listed firms in Serbia use to keep their levels of accounts receivables

to a high level during crisis years.

Table 4 Regression model results for two dependant variables:Return on Total Asset and Operating Profit Margin

Dependent variable: ROTA Dependent variable: OPM

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 34

Bestlink College of the Philippines

Independent Std. t- Std. t-

variable Coeff. Error statistic Sig. Coeff. Error statistic Sig.

(Constant) -,280* ,085 -3,281 ,001 -,908 ,167 -5,445 ,000

ARRR ,056 ,093 ,601 ,549 ,306 ,181 -1,686 ,095

RTR ,041 ,039 1,042 ,300 ,184 ,077 2,397 ,018

SIZE ,038* ,012 3,219 ,002 ,108* ,023 4,659 ,000

LIQ ,008* ,002 3,545 ,001 ,020* ,004 4,525 ,000

Weighted

statistics

R square ,300 ,367

Adjusted R

,273

,343

square

SE of

,057

,112

regression

F-statistic 11,033 14,937

* Significant at 5% level

Table 4 shows that R-squared value is 0.300 (0.367) indicating that 30% (36.7%)

variance in Return on Total Assets (Operating Profit Margin) as dependent variable

can be explained through four independent variables used.

CONCLUSIONThis study explores how large and medium sized companies listed at the

regulated market segment of the Belgrade Stock Exchange manage their accounts

receivables in the most profitable way during a crisis period, from 2008 to 2011.The

analysis of the relation between accounts receivables and two dependent variables on

profitability, return on total asset and operating profit margin, indicates a positive, but

no significant relation. This implies that managers of the most successful Serbian

companies are of the opinion that it’s profitable, and thus beneficial for their firms, to

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 35

Bestlink College of the Philippines

support their financially constraint customers by increasing the level of the receivables.

In this way, companies secure their future sales and survival in crisis times. Companies

take into account the trade-off between extending trade credits and increasing the

default risk involved on the one hand, and the short-term and the long-term benefits of

such a receivables management on the other hand. Profitability and creation value for

shareholders over crisis time is achieved by increasing the accounts receivable levels.

This study is featured at least by three main limitations. In the first place, it is

based on the data of the Serbian non-financial firms listed at the regulated market.

Therefore, a generalization of the results of this research for the whole economy

(financial firms, non-listed firms) is not acceptable. Secondly, the analysis is limited to a

four-year crisis period, not taking into account the impact on receivables on profitability

in a previous, non-crisis period. It this way, a comparative approach could not be

applied and the differences between non-crisis and crisis period could not be

compared and highlighted. Finally, the correlation and regression analysis is conducted

using the Return on Total Assets and Operating Profit Margin as dependent variables,

and four independent variables. In this respect, future research should comprise a

more comprehensive set of explanatory variables and should be based on a larger and

comprehensive database.

REFERENCES: http://www.asecu.gr/files/9th_conf_files/dencic-mihajlov.pdf

3.0 FACTORING OF RECEIVABLES AUDIT TECHNIQUES GUIDE

NOTE: This guide is current through the publication date. Since changes mayhave

occurred after the publication date that would affect the accuracy of this document, no

guarantees are made concerning the technical accuracy after the publication date.

OverviewCompanies generate accounts receivable by selling goods or services to their

customers on credit. Many companies who extend credit to their customers sell their

accounts receivable to a factor. A factor is a specialized financial intermediary who

purchases accounts receivable at a discount. Under a factoring agreement a company

sells or assigns its accounts receivable to a factor in exchange for a cash advance. The

factor typically charges interest on the advance plus a commission. The price paid for

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 36

Bestlink College of the Philippines

the receivables is discounted from their face amount to take into account the likelihood

of un collectability of some of the receivables.

Factoring is a technique used by companies to manage their accounts receivable

and provide financing. Typically companies that have access to sources of

financing that is less expensive than factoring would not use factoring as source of

credit.

A factor may provide any of the following services:

• Investigation of the credit risk of customers of the client;

• Assumption of the credit risk of customers;

• Collection of the client’s accounts receivable from customers;

• Bookkeeping and reporting services related to accounts receivable;

• Provision of expertise related to disputes, returns and adjustments;

• Advancing or financing.

There are numerous types of factoring arrangements. Some of the basic types vary the

treatment of credit risk assumption and customer or debtor notification.

When the factoring agreement involves the purchase of accounts receivable where the

factor bears the risk of a customer or debtor failing to pay the client for reason of

financial inability it is a non-recourse or without-recourse agreement. In the situation

where the client must bear the risk of non-payment due to financial inability, the

agreement is a recourse agreement. In many instances, factoring agreements provide

for accounts to be purchased on both a recourse and non-recourse basis depending on

the credit worthiness of the customers or the debtors.

Compliance FocusA strategy has been identified in which multinational corporations use the

factoring of accounts receivable among related parties. The goal of this strategy is to

avoid U.S. taxation by shifting income offshore and to significantly reduce remaining

U.S. income by deducting expenses related to the same income.

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 37

Bestlink College of the Philippines

Typical Fact Pattern:A U.S. subsidiary (“Taxpayer”) of a foreign parent earns sales income and books

accounts receivable. The Taxpayer then factors (sells at a discount) the accounts

receivable to a brother-sister foreign affiliate. The Taxpayer pays the foreign factor the

following fees: a discount; administration fees; commissions; and interest.

The Taxpayer deducts these fees or may net them against gross receipts.

However, the foreign factor does not perform any of the typical services of a factor,

including collection of the Taxpayer’s accounts receivable. Instead, the

Taxpayer agrees to continue doing all or most of its own collection work on its

accounts receivable. In some cases, factoring arrangements involve the use of a

domestic (U.S. based) factor instead of a factor located offshore. In cases involving a

domestic factor, some audit steps and issues discussed below may not apply. If the

transaction is between two domestic entities it may be structured for state tax purposes

and has no federal tax effect. In addition, insome cases, the Taxpayer and factor may

be engaged in a financing arrangement involving securitizing the accounts receivable.

General Audit Steps

Although U.S. taxpayers are taxed on their worldwide income, the income of foreign

subsidiaries of U.S. taxpayers is generally deferred from taxation in the U.S.

Consequently, the existence of a factoring arrangement may not be readily identified on

the face of a return. Therefore, at a minimum the following audit steps should be

utilized:

• Submit a specific IDR to determine if any accounts receivable were sold if yes,

were they sold to:

• A related entity; and/or

• Any entity located offshore.

• Review the tax return balance sheet to determine if the accounts receivable

reflected thereon are reasonable for the size and type of business.

• Perform a comparative analysis of the balance sheets for the current and atleast

5 prior tax years, noting any significant reduction in accounts receivable.

• Review the tax preparation work papers for large debits to income.

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 38

Bestlink College of the Philippines

Review and analyze Form 5472 and the audited financial statements of both the

domestic entity and the related foreign entity for any footnotes reflecting the sales

and/or securitization of the accounts receivable. Request that theforeign entity provide

this information in English. Note whether this analysis demonstrates income shifting

from the domestic entity to the foreign entity. Also note whether there is evidence that

the foreign entity was conducting a trade or business within the United States.

The following facts should be determined during the audit through IDRs or functional analysis and by requesting documentary substantiation where appropriate.

The Factor• Name and location of the factor;

• Relationship of the factor to the taxpayer;

• The name and location of a common parent of the factor and the taxpayer;

• Whether the taxpayer and the factor are part of a consolidated group;

• Whether the factor is a Controlled Foreign Corporation (CFC);

• The name of any promoter/advisor or accounting firm involved in structuring the

taxpayer’s factoring arrangement.

The Factoring ArrangementThe factoring arrangement is usually set forth in a Factoring Agreement between

the factor and the taxpayer. Obtain a description of the terms of the factoring

arrangement including if applicable the following:

• The names of the parties that entered into the Factoring Agreement;

• The date the Factoring Agreement was signed;

• The services the factor agreed to provide;

• The services the factor contracted back to the taxpayer;

• The fees the taxpayer charged the factor for performing the services

contracted back to the taxpayer;

• The discount and fees charged by the factor for:

Service Management System – Accounts Payables and Accounts Receivables with Treasury Management System Page 39

Bestlink College of the Philippines

• discount on accounts receivable;

• administrative fees;

• commission fees;

• interest charges.

• The date the taxpayer was required to transfer accounts receivable to the

factor;

• The date the factor had until to accept or deny the factored accounts

receivable;

• Whether the sale of the receivables to the factor was recourse or non-

recourse;

• The reasons the taxpayer provided for entering into the factoring

arrangement;

• Whether the taxpayer ever entered a factoring arrangement before;

• Whether it is a common practice in the taxpayer’s industry to factor

receivables;

• If a related entity is utilized to perform factoring, explain the source of the

funding used by this entity to acquire the accounts receivable.