basic_on_stock_market.pptx 26th may 2014 (1)

DESCRIPTION

basics of stock marketTRANSCRIPT

COMPERHENSIVE OUTLOOK OF INDIAN FINANCIAL MARKET

i

Investment :Investment is putting your money in a Financial Instrument with the view of earning a desired return out of that Investment

Basics of Investment

OBJECTIVE OF INVESTMENT Objective of investment can vary according

to the needs and requirement of the individual.

1) Retirement Planning: A person having a view to build up a

retirement Corpus could invest in a financial Asset. Generally these investment are of a longer term in a nature and Mutual Fund is the most popular instrument to invest for the retirement planning

o) Children Future Planning: Every parent has a dream that their children must live a happy and successful life. So either for

the child’s marriage,education,or Business an individual takes up an

Investment Route

o) Tax Planning: Now a days when many investment are allowed in the tax free

Section of Income tax Act in India. Almost every tax paying person wishes to invest

somewhere for the dual purpose of Investment and tax planning . Generally

Insurance and Mutual funds are the most common investment instrument here

o) Speculation/ Trading:Speculation and Trading means to

invest with a purpose of Short term Earning and speculating on a

particular Asset. Equity and commodity Markets are the most common place

where the trader can found.

o) Business Needs: Mutual fund ,Insurance Companies ,

Banks , Financial Institutions, Corporate who have a professional

reason for investing in the Financial Markets as this is their primary

business. They generally invest in large corpus.

6) Additional Earnings:Sometimes the investors do not have any fixed reason for investing they invest only

because they have some additional Income with them. In India , they generally invest in

Fixed Deposits.

Understanding The Indian Financial

market

WHAT IS FINANCIAL MARKET?

Financial Market like any other market is a System where Trading in Financial Instrument takes place. This System is now completely Automated through Electronic Interfaces and consists of many Buyers and Sellers with their individual objectives of entering in Financial Markets. This system of trading is a Government Recognized System.

FUNCTIONS OF FINANCIAL MARKETS

1. Price Discovery2. Liquidity to financial assets3. Reduce cost of transacting

F i na nc ia l M a rk ets

De bt M ark et

Eq ui ty M a rk e t

M on ey M ark et

Ca pi ta l M ark et

P rim ary M ark et

Se c o nd ary M ark e t

F o rward M ark et

F u tu res M ark et

OT C M a rk et

Classification of Financial Markets

EQUITY

It is a High Risk-High Return Asset Class Preferred for Longer term investment with high Volatility in short

term cycles which makes it preferred for Traders. Returns are linked to the Performance of the Company. The returns are not Fixed and depend on the Industry’s

performance, Economic, Political & other Macro Environment features.

Can be issued by Government, Private or an MNC Company.

COMMODITY

Trading in Physical Commodities like Gold, Silver, Crude Oil, Agri Products like Wheat, Sugar, etc takes place.

The Dynamics of the trading system is identical to the physical trading system in the Domestic & International Markets.

These are shorter period investments and find a place in a trader or speculators portfolio.

DEBT & FIXED INTEREST BEARING INSTRUMENTS

It has a Low Risk- Low Return. Comprise of Govt. Bonds, Debenture of Companies, Fixed

Deposits, Commercial Papers, etc whose returns are fixed and are known at the time of Investments.

Most common place of investments in developing countries as they have a very low chance of losing Principal Amount and are generally with the Banks.

PARTICIPANTS IN FINANCIAL MARKETS

1. Regulators2. Exchanges3. Brokers/Intermediaries4. Clients

REGULATORS

Regulator is a body which regulates and overlook the smooth functioning of Financial market Systems, they do recognize, allow, disallow other Financial intermediaries for working in financial markets, redressal for the Investors, creates/modifies rules and regulations in the financial markets.

TYPES OF REGULATORS

1. Ministry of Finance – Top most office in the country as far as financial matters are concerned. Headed by Mr. Arun Jately.

2. SEBI – Big Boss of the Financial Market and the main regulator in the Capital Markets. Headed by Mr. UK Sinha.

3. RBI – Controls the Banking and monetary systems in the country. Headed by Mr. Raghuram Rajan.

TYPES OF REGULATORS4. AMFI(association of mutual funds in

india) – Organization regulates, licenses and works for the up liftment of the Mutual Fund Industry in India. Headed by Mr. Sandeep Sikka.

5. IRDA(insurance reglatory & development authority) – It regulates and looks after the licensing and development of all the Insurance Companies in India. Headed by Mr T.S Vijayan.

MAJOR INDIAN EXCHANGES

Exchange provides the facility of trading in financial products in India, these are two exchanges for equity Trading and two exchanges for Commodity Trading.

Exchange

Equity

NSE

Commodity

BROKERS/ INTERMEDIARIES

They are the bodies which act as an interface between the Client and the Financial System and facilitate the proper trading in Financial Products.

Eg.- Swastika Investmart, JM Financial, ICICI Prudential, Bajaj Capital, etc.

CLIENTS

It includes all the Investors and Traders like All the Indian Retail Investors, HNIs, Institutional Investors, FIIs.

FINANCIAL PRODUCTS

1. Equity & Direct Equity Related Products – Equity Shares of Private, Public and MNCs trading in Indian Security Markets.

2. Mutual Funds – A collective fund that is distributed by the different investors & managed by an organization on behalf of the investors.

3. PMS – It is the Portfolio Management Services where a Portfolio trades on account of an investor on the name and behalf of Investor.

FINANCIAL PRODUCTS

4. Commodity – Electronic trading in Agricultural and Metal Commodities through recognized Stock Exchanges in India.

5. Insurance – An organization which insures lives and/or goods of a particular Individual or an Organization by charging a calculated Premium on it.

PRIMARY MARKET

WHAT IS PRIMARY MARKET??

CAPITAL MARKET

PRIMARY MARKET SECONDARY MARKET

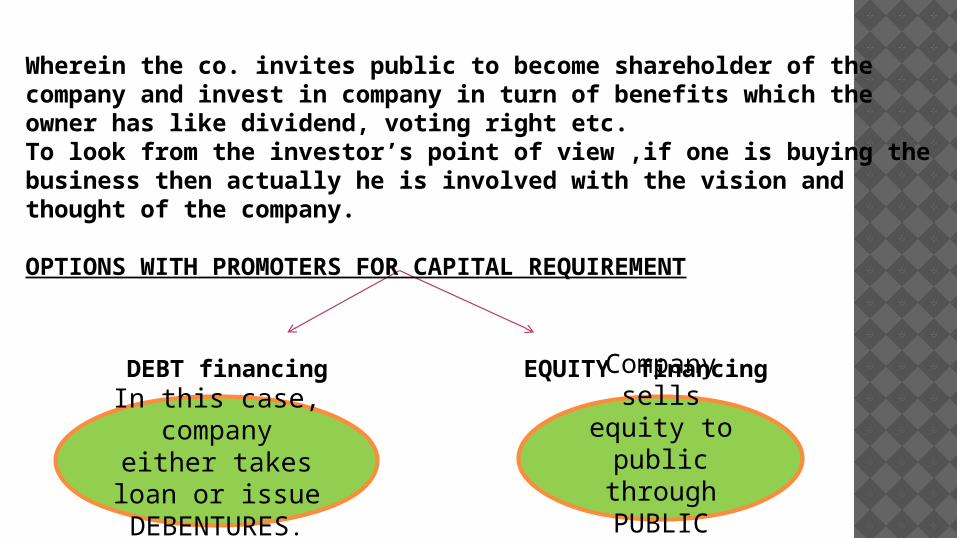

Primary market refers to the part of the capital market in which promoter group offers shares to public or public groups for the purpose of rising fund for the company.When capital requirement for expansion and working capital becomes necessary, equity raising option called primary mkt

In this case, company

either takes loan or issue

DEBENTURES.

Company sells equity

to public through

PUBLIC ISSUE

Wherein the co. invites public to become shareholder of the company and invest in company in turn of benefits which the owner has like dividend, voting right etc.To look from the investor’s point of view ,if one is buying the business then actually he is involved with the vision and thought of the company.

OPTIONS WITH PROMOTERS FOR CAPITAL REQUIREMENT

DEBT financing EQUITY financing

• This is the market for new long term equity capital. The primary market is the market where the securities are sold for the first time. Therefore it is also called the new issue market (NIM).

• In a primary issue, the securities are issued by the company directly to investors.

• The company receives the money and issues new security certificates to the investors.

• Primary issues are used by companies for the purpose of setting up new business or for expanding or modernizing the existing business.

Features of primary markets

The primary market performs the crucial function of facilitating capital formation in the economy.The new issue market does not include certain other sources of new long term external finance, such as loans from financial institutions. Borrowers in the new issue market may be raising capital for converting private capital into public capital; this isknown as "going public."The financialassets sold can only be redeemed by The original holder.

ADVANTAGES & DISADVANTAGES OF IPOAdvantages: Disadvantages

• No cost of capital• Huge amt can be

raised• Brand value• Correction

valuation

• Disclosure of information

• Decisions takes time

• Cost of IPO

PARTIES TO IPO Registrar Lead manager Underwriter Merchant Banker Promoter

ROLE OF REGISTRAR Typically the Registrar of Companies is responsible for

keeping records of filings that corporations tend to make. This would include annual reports, applications for incorporation, and company changes that may be made.

It is the most important piece of legislation that empowers the Central Government to regulate the formation, financing, functioning and winding up of companies. The Act contains the mechanism regarding organisational, financial, managerial and all the relevant aspects of a company. It provides for the powers and responsibilities of the directors and managers, raising of capital, holding of company meetings, maintenance and audit of company accounts, powers of inspection, etc.

ROLE OF LEAD MANAGERS Lead managers are independent financial institution

appointed by the company going public. Companies appoint more then one lead manager to manage big IPO's. They are known as Book Running Lead Manager and Co Book Running Lead Managers.

Their main responsibilities are to initiate the IPO processing, help company in road shows, creating draft offer document and get it approve by SEBI and stock exchanges and helping company to list shares at stock market & dispatch of refunds of bidders.

ROLE OF UNDERWRITERS Underwriters are those persons who, in a public issue, agree to

take up shares or debentures which are not fully subscribed. They make a commitment to get the issue subscribed either by others or by themselves. When a company decides to go public, it needs an assurance that if its securities are not fully subscribed by the public, there would be someone to subscribe to those securities. And the underwriter does this job very effectively. He enters into an agreement with the issuer company that in the occurrence of such an event, it would subscribe to, by itself or by others, the securities that remain unsubscribed. For performing this job, he receives a certain amount from the issuer company, known as the ‘underwriting commission’. Apart from this amount, he can also earn profits by selling these securities in the market.

An underwriter can be any person, whether a body corporate or otherwise. Even an individual can be an underwriter. The only requirement for an underwriter is that he needs to have adequate financial resources, which enables him to perform his job in an efficient and effective manner.

ROLE OF MERCHANT BANKER Instrument designing Pricing the issue Registration of offer document Underwriting support Marketing of the issue Allotment & refund Listing on stock exchanges

ROLE OF PROMOTERS Promoters are the people, who, for themselves

or on behalf of others, organize a corporation. They issue a prospectus, obtain stock subscriptions, and secure a charter. Promoters stand in a fiduciary relationship to the proposed company and must act in Good Faith in all their dealings for the proposed corporation.

Discovery of a business idea Detailed investigation Assembling the factors of production Entering into preliminary contracts

EQUITY CAPITAL & ITS CLASSIFICATION

AUTHORISED

CAPITAL

ISSUED CAPITAL

EQUITY CAPITAL

SUBSCRIBED CAPITAL

PAID UP CAPITAL

Equity capital is ownership capital. Equity shareholders are the final owners of the company.

CLASSIFICATION OF EQUITY SHARES

• BLUE CHIP SHARES : Shares of large, well-established, and financially strong companies with an impressive record of earnings and dividends.

• GROWTH SHARES : Shares of companies that have a fairly entrenched position in a growing market and which enjoy an above average rate of growth as well as profitability.

• INCOME SHARES: Shares of companies that have fairly stable operations, relatively limited growth opportunities, and high dividend payout ratios.

• CYCLICAL SHARES: Shares of companies that have a pronounced cyclicality in their operations.

• DEFENSIVE SHARES: Shares of companies that are relatively unaffected by the ups and downs in general business conditions.• SPECULATIVE SHARES: Shares that tend to fluctuate widely because there is a lot of speculative trading in them. EQUITY SHARES CAN BE ISSUED BY A COMPANY AT ANY OF THE FOLLOWING PRICES : At par, At premium or At discount.

DIFFERENT TYPES OF ISSUES……

• INITIAL PUBLIC OFFER (IPO) : It is referred to simply as an "offering" or "flotation", when a company (called the issuer) issues common stock or shares to the public for the first time.

• FOLLOW ON PUBLIC OFFER (FURTHER ISSUE) : The basic difference between Initial Public Offer (IPO) and Follow on Public Offer (FPO) is as the names suggest as FPO is for the companies which have already listed on exchange but want to raise funds by issuing some more equity shares.

• RIGHTS ISSUE : With the issued rights, existing shareholders have the privilege to buy a specified number of new shares from the firm at a specified price within a specified time

PREFERENTIAL ISSUE :

The preferential issue of equity shares/ Fully Convertible Debentures (FCDs) / Partly Convertible Debentures (PCDs) or any other financial instruments which would be converted into or exchanged with equity shares at a later date, by listed companies whose equity share capital is listed on any stock exchange, to any select group of persons under section 81(1A) of the Companies Act 1956 on private placement basis.

INITIALPUBLIC OFFER (IPO)

• Book running lead managers• Bankers to the issue• Registrars to the issue• Underwriters . TYPES OF PRIMARY ISSUES :

Fixed price : An issuer company is allowed to freely price the issue. The basis of issue price is disclosed in the offer document where the issuer discloses in detail about the qualitative and quantitative factors justifying the issue price.

VARIOUS INTERMEDIARIES….

Book building is a process of price discovery. Hence, the Red Herring prospectus does not contain a price. Instead, the red herring prospectus contains either the floor price of the securities offered through it or a price band along with the range within which the bids can move. The applicants bid for the shares quoting the price and the quantity that they would like to bid at. Only the retail investors have the option of bidding at ‘cut-off’. After the bidding process is complete, the ‘cut-off’ price is arrived at on the lines of auction. The basis of Allotment is then finalized and letters allotment/refund is undertaken.

BOOK BUILDING

What is a Red Herring Prospectus?

Red Herring Prospectus is a prospectus, which does not have details of either price or number of shares being offered, or the amount of issue. This means that in case price is not disclosed, the number of shares and the upper and lower price bands are disclosed. On the other hand, an issuer can state the issue size and the number of shares are determined later.

What is a price band?

The red herring prospectus may contain either the floor price for the securities or a price band within which the investors can bid. The spread between the floor and the cap of the price band shall not be more than 20%. In other words, it means that the cap should not be more than 120% of the floor price.

CATEGORY OF INVESTORS

• QUALIFIED INTITUTIONAL INVESTORS banks, mutual funds, insurance companies, FIIs etc. maximum reserve kept for them is 50% (out of which 5% for mutual funds).

• NON INSTITUTIONAL INVESTORS HUFs, HNIs, companies, corporate bodies, NRIs, societies etc. reserve kept for them is 15%. (application size > 1 lakh).

• RETAIL INVESTORS Individuals , HUF’s. reserve kept for them is 35%. (application size < 1 lakh).

BIDDING PROCESS

• DURING THE IPO Distributing forms to investors by brokers. Investors fill up the form and submit along with cheque and a copy of pan card to broker.

• Bidding of shares through a specialized software i.e. NEAT software .The IPO market timings are 10 am to 5 pm.

• POST THE IPO : applications cheques are sent to banker for clearing of cheques & application forms are sent to registrar for final checking of forms and allotment.

FOR INVESTORS……

• INDUSTRY ANALYSIS : overall performance of particular industry/sector in which the company lies. Last performance of 3 to 5 yrs can be seen.

• COMPANY ANALYSIS : it includes the promoters of the company , their background in case of IPO and if it is FPO then see to performance of co. preceding last 3 yrs.

• PEER GROUP COMPARISON : performance of peer group companies of that sector.

• ECONOMY ANALYSIS : depends on the economy of the country and political situations. Global situation is also considered.

INTRODUCTION – Secondary Market

• Place where the trading of stocks of the company takes place second time.

• Buyer and sellers are the investors.• Here ownership is in public’s domain.• Secondary market is a synonym to stock exchanges.

• A mutual organization which provides facilities for stock brokers to trade stocks and securities.

• Also provides facilities for the issue and redemption of securities.

• Capital events like payment of income and dividend take place .

STOCK EXCHANGES

Functions Of A Stock Exchange

Providing trading mechanism online.

Collection ,display and distribution of data and information.

To provide listing facilities.

To provide protection to the investors and regulate broker and participant.

Effective and efficient settlement of transaction.

Simple mechanism

Return Pass back to Investor

Pool their money

Fund Manager

Invests inSecurities

Generates

Investment cycle

Systems used by Exchanges

BOLT: System provided by BSE only for trading on Bombay stock exchange.

NEAT: National Exchange for Automated Trading System is provided by NSE only for trading on NSE.

ODIN: Open Dealer integrated Network, developed by Financial Technologies. Mutually used for all the exchanges.

Market timings

Both in NSE and BSE timings are following:

Pre –opening session: 9-9:15am Normal market session: 9:15am to 3:30pm Post closing session: 3:40 to 4pm

Circuit Breakers

Circuit breakers are important because:

Sometimes the movement of stock prices can beat all logic and move tremendously in any direction.Circuit Breaker is a system to sustain sanity of the stock market in such situations. For example, the BSE Sensex moved up by 2110.79 points on May 18, 2009 after the Parliament election results were announced.

Movement Time Close period

10 % Before 1.00 pm 1 hour

1.00pm to 2.30pm ½ hour

After 2.30pm Does not close

15% Before 1.00 pm 2 hour

1.00pm to 2.30pm 1 hour

After 2.30pm Close for the rest of the day

20% Any time Close for the rest of the day

For index:

Kinds of circuit breakers

Continued….

For stocks: Daily price band of 2%( either way)Daily price band of 5%( either way)Daily price band of 10%( either way)No price band : Scripts on derivative products are availablePrice band of 20%( either way) on all remaining scripts

Rolling settlement

• Intraday trading allowed

Trade to trade segment

• Intraday trading not allowed

Settlements in market

SECONDARY MARKET

OVERVIEW

STOCK INDICES

A stock market index is a method of measuring a section of the Stock Market . Many indices are cited by news or financial services firms and are used as benchmarks, to measure the performance of portfolios such as mutual funds.

India Index Services & Products Ltd. (IISL) is a joint venture between the National Stock Exchange of India Ltd. (NSE) and CRISIL Ltd. (formerly the Credit Rating Information Services of India Limited). IISL has been formed with the objective of providing a variety of indices and index related services and products for the capital markets.

IISL has a consulting and licensing agreement with Standard & Poor's (S&P), for co-branding IISL's equity indices.

IISL

TYPES OF INDIAN INDICES

Market indices Sectoral IndicesBSE 200 BSE FMCG BSE Auto

BSE 500 BSE CD BSE MCX.

BSE TECK BSE Metal BSE REALTY

BSE IT BSE PSU BSE Pharma

BSE small cap BSE mid-cap

S&P CNX Nifty BSE Sensex Nifty Jr.

GLOBAL INDICES

USA EUROPEANINDICES

ASIAN MARKET INDICES

Dow Jones FTSE (London) NIKKEI (Japan)

NASDAQ DAX (Germany) HANG SENG (Hong Kong)

S&P 500 CAC (France) KOSPI (South Korea)

PARTICIPANTS IN MARKET

This are known to be active players of secondary market and having prevalent influence over market movements.

Trader Hedger/speculator Jobber Day trader Investor Domestic financial institution (DII)

FII Arbitrageur Depositories Broker Mutual fund

TRANSACTION CYCLES

Placing Order

Trade Execution

Clearing Trades

Settlement Of Trades

Funds/ Securities

Decision to Trade

SETTLEMENT PROCESS Determination of obligations- NSCCL determine what counter party owe, and

what counter party are due to recieve on the settlement date. Pay-in of funds and securities – The members bring in their funds/securities to

the NSCCL. They make available required securities in designated account with depositories by the prescribed pay-in time. Then depositories moves the securities available in the accounts of member to the account of NSCCL.

Pay out of funds and securities- after processing for shortages of funds/securities and arranging for movement of funds from surplus banks to deficit bank through RBI clearing, the NSCCL sends electronic instructions to the depositories/clearing banks to release payout of securities/funds.

Risk Management- A sound risk management system is integral to an efficient settlement system. NSCCL has put in place a comprehensive risk management system, which is constantly monitored and upgraded to preempt market failure.

SETTLEMENT AGENCIES NSCCL- it clears all trades determines

obligations of members, arranges for pay-in of funds/securities, receive funds/securities, processes for shortages in funds/securities, arranges for pay-out of funds/securities to members, guarantees settlements, and collects and maintains margins

SETTLEMENT AGENCIES

Clearing Members- They are responsible for settling their obligation as determined by the NSCCL. They have to make available funds and/or securities in the designated accounts with clearing banks/depository participant as the case may be.

Custodians- It’s a person who holds for safekeeping the documentary evidence of the title to the property belonging like share certificates, etc.

Clearing Banks- They are a key link between the clearing members and NSCCL for funds settlement. Every clearing member is required to open a dedicated settlement account with one of the clearing banks.

Depositories- its an entity where the securities of an investor are held in electronic form. The person who holds a Demat account is a beneficiary owner.

Professional clearing member- NSCCL admits special category of members namely ,professional clearing member. PCM may clear and settle trades executed for their clients (individuals, institutions etc.). In such an event, the functions and responsibilities of the PCM would be similar to custodians. PCMs may also undertake clearing and settlement responsibilities for trading members.

SETTLEMENT PROCESS IN CM SEGMENT OF NSE

NSE

Clearing Banks

Custodians / CMs

Depositories NSCCL

8

6

9

5

10

4

2 3

1

11

7

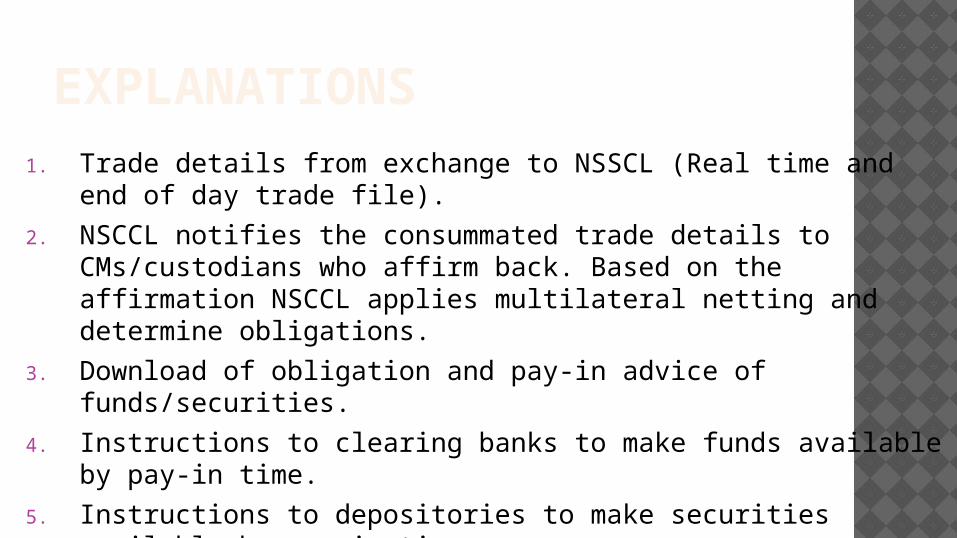

EXPLANATIONS1. Trade details from exchange to NSSCL (Real time and end of day trade file).

2. NSCCL notifies the consummated trade details to CMs/custodians who affirm back. Based on the affirmation NSCCL applies multilateral netting and determine obligations.

3. Download of obligation and pay-in advice of funds/securities.

4. Instructions to clearing banks to make funds available by pay-in time.

5. Instructions to depositories to make securities available by pay–in time.

6. Pay- in of securities (NSCCL advices depositories to debit pool account of custodians/CMs and credit its account and depository does it).

7- Pay-in of funds (NSCCL advices clearing banks to debit account of custodians/CMs and credit its account an clearing bank does it).

8- Pay-out of securities(NSCCL advices depository to credit pool account of custodians/CMs and debit its account and depository does it).

9- Pay-out of funds (NSCCL advises clearing Banks to credit account of custodians/CMs and debit it’s account a clearing bank does it).

10- Depository informs custodians/CMs through DPs.

11- Clearing Banks inform custodians/CMs.

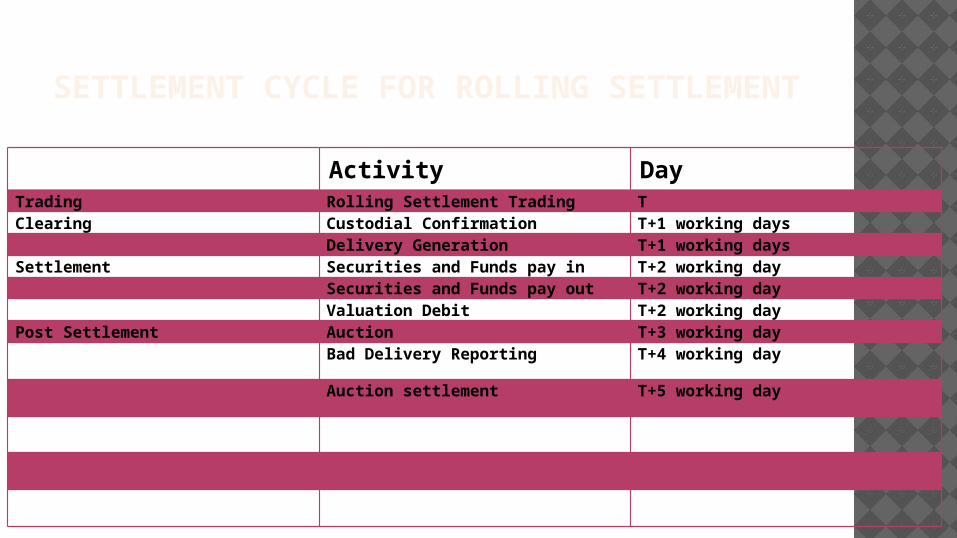

SETTLEMENT CYCLE FOR ROLLING SETTLEMENT

Activity DayTrading Rolling Settlement Trading TClearing Custodial Confirmation T+1 working days

Delivery Generation T+1 working daysSettlement Securities and Funds pay in T+2 working day

Securities and Funds pay out T+2 working dayValuation Debit T+2 working day

Post Settlement Auction T+3 working dayBad Delivery Reporting T+4 working day

Auction settlement T+5 working day

AN INTRODUCTION TO

FINANCIAL DERIVATIVES

MEANING AND DEFINITION OF DERIVATIVES

MEANING : Derivative is a financial instrument whereby two parties come in to a contract and transfer there risk, value of which is derived from the value of underlying asset.

DEFINITION : Derivative is a bilateral contract whereby parties agrees to transfer their risk, and value of the contract is derived from the value of underlying asset. The underlying asset includes stocks, commodities, interest rates, currencies, bonds etc.

TYPES OF DERIVATIVES PRODUCTS

FORWARDS FUTURES OPTIONS SWAPS WARRANTS LEAPS

FORWARDS

In a forward contracts, one party agrees to buy, and the counterparty to sell, a physical asset or a security at a specific price on a specific date in the future. Thus a forward contract is a customized contract.

FUTURES

A future contract is a forward contract that is standardized and exchange traded. The main difference with forwards are that futures are traded in an active secondary market, are regulated, backed by the clearing house, and require a daily settlement of gains and losses.

OPTIONS

An option contract gives its owner the right, but not the legal obligation, to conduct a transaction involving an underlying asset at a predetermined future date and at a predetermined price (exercise price).

Options are of two types A) Call option B) Put option

CALL AND PUT OPTIONS

CALL OPTION : Call option gives the owner the right , but not the obligation to buy an underlying asset at predefine price in any future date.

PUT OPTION : Put option gives the owner the right, but not obligation to sell an underlying asset at predefine price in any future date.

SWAPS

A swap is a series of forward contracts. In the simplest swap, one party agrees to pay the short term (floating) rate of interest on some principal amount, the counterparty agrees to pay a certain (fixed) rate of interest in return.

WARRANTS

Options generally have lives of up to one year, the majority of options traded on exchanges having a maximum maturity of nine months. Longer dated options are called warrants and are generally traded over the counter.

LEAPS

The acronym LEAPS means Long-Term Equity Anticipated Securities. These are options having a maturity of up to three years.

DIFFERENCE BETWEEN FORWARDS AND FUTURES

FORWARDS FUTURESA) Customized StandardizedB) Traded OTC On exchangeC) No margin req. Margin req.D) Settlement on On daily basis last date

CONCLUSION

Hence, it can be concluded that derivatives are risk management instrument which minimizes the risk, or some time eliminate the risk associated with securities, bonds, commodities, interest rates, currencies etc.. And are largely traded contracts, thus provide high liquidity to market floor.

MUTUAL FUNDS AND OTHER INVESTMENT COMPANIES

MUTUAL FUNDS

MFs are financial intermediaries that collect funds from individual investors

Pooling of assets is the key idea.

ADVANTAGES OF MUTUAL FUNDS

Diversification benefits.

Low Transaction costs.

Availability of various

schemes.

Professional management.

Liquidity.

Returns.

Flexibility.

DISADVANTAGES OF MUTUAL FUND

No choice of securities.

Problem of fund managers not

performing well.

Management fees.

NET ASSET VALUE

Value of each share is called the net asset value.

• Selling new shares• Redeeming existing shares

Used as a basis for valuation of investment company shares

NET ASSET VALUE

Calculation

• Market Value of Assets - Liabilities

• Shares Outstanding

TYPES OF INVESTMENT COMPANIES

Managed Investment Companies

Open-End

Closed-End

CLASSIFICATION OF MUTUAL FUNDS On the basis of structure

– Open ended close ended

On the basis of Investment Objective Growth funds Income funds Balanced funds Money market funds

OPEN ENDED VS. CLOSE ENDED

Close ended

A close-ended Mutual fund has a stipulated maturity period e.g. 5-7 years. The fund is open for subscription only during a specified period at the time of launch of the scheme

An open-ended Mutual fund is one that is available for subscription and repurchase on a continuous basis. These Funds do not have a fixed maturity period. Investors can conveniently buy and sell units at Net Asset Value (NAV). The key feature of open-end schemes is liquidity.

OPEN ENDED VS. CLOSE ENDEDBASIS OPEN ENDED CLOSE ENDED

Buying of shares Directly through fund Stock exchanges

Sales Price NAV Market Price

Shares outstanding Variable Fixed

Investment option Highly marketable sec Less marketable sec

Redemption Any time the investor wants At the time of maturity

COMMINGLED FUNDA normally illegal practice in

which a broker mingles his own funds with those of his/her client, making it difficult to distinguish

to whom to give returns.

A mutual fund that includes assets from several accounts, pooled together, to reduce management and administration costs; here also called pooled fund. Eg :money market fund .

INVESTMENT POLICIES

Money market funds

Debt funds International funds

Balanced & income funds

Asset allocation & flexible funds

Index funds

COSTS OF INVESTING IN MUTUAL FUNDS

Front end load

Back end or exit load

Operating expenses

EXCHANGE TRADED FUNDS

A security that tracks an index, a commodity or a basket of assets like an index fund, but trades like a stock on an exchange.

One of the most widely known ETFs is called the Spider (SPDR), which tracks the S&P 500 index and trades under the symbol SPY.

ETF

Potential advantages

• Lower taxes • Trade continuously • Lower costs

Potential disadvantages

• Prices can depart by small amounts from NAV

INFORMATION ON MUTUAL FUNDS

Morningstar (www.morningstar.com)

Yahoo (biz.yahoo.com/funds)

Investment Company Institute (www.ici.org)

Directory of Mutual Funds

Queries are invited…….

MUTUAL FUNDS

Mutual Funs is a pool of money in which the investor invest their money to generate returns out of them.In India the mutual fund launched in the year 1963 with the setting of UTI. Public sector Bank and financial Institutions were allowed to establish mutual fund in the year 1987. Since 1993 private sector and foreign institution were permitted to set up Mutual fund.

AMFI: Association of Mutual fund Industry take care about the rules and regulations of MF industry & also work For the investors Protection

Types of Mutual fund by entry and Exit options:1)Open ended Funds:2)An open end fund is one that is available

for subscription always. They do not have fixed maturity. Investors can conveniently buy and sell units at NAV related price. The key feature of open end scheme is its any time liquidity.

3)Close Ended Fund: A close end fund has a stipulated maturity period which generally ranging from 3 to 15 years . The fund is open for subscription only during a specific period . Investor can invest in the scheme at the time of NFO ( New fund offer) they can be liquidate at the time of maturity or after lock in period.

3) Interval Scheme: Interval scheme are those scheme ,which combines the features of open ended and closed ended schemes. The units may be traded on the stock exchange or may be open for sale or redemption during pre detemined interval at NAV related prices.

NAV: Net Asset Value is the value of a unit of a mutual fund. It is the value of a scheme’s asset less the value of its liabilities.

NAV=(Asset- Liabilities)-------------------

No. of out standing units

BY Nature:

1)Equity Fund: These fund invest a maximum part of their corpus into equity holdings. The structure of the fund may vary different for different scheme and the fund manager outlook on different schemes.

a)Diversified equity Fundsb)Sector specific fundc) Tax Saving Funds(ELSS)d)Mid cap Funds

Debt Fund:The objective of this fund to invest in debt instruments of Govt. authorities , Private Companies and Banks By investing in debt instrument these fund ensures low risk and provide stable income to the investors.

Balanced Fund:

As the name suggest they are a mix of both equity and debt funds. They invest in both equities and debt instruments. Equity part provide growth and debt part provide stablity in returns.

Advantages of Mutual Funds:

1)Professional Management:

You avail the services of experienced and skilled professionals who are backed by a dedicated research team. Which analyses the performance and prospects of the companies and acheive the objective of the scheme.

Low cost:

Mutual funds are relatively less expensive way to invest comparing to invest in directly in the capital Markets because the benifits of scale in brokerage and other fees translate into lower cost for investors

Liquidity and transparency:

Just like an individual stock ,mutual fund also allows investors to liquidate their holding as and when they want. You get regular information on the value of your investment and the portfolio of your mutual fund scheme.

Flexibility:

Through feature such as Systematic Investment Plan , you can systematically invest or withdraw fund according to your needs and convenience.

Net asset Value:

Net Asset Value ( NAV) is the value of a unit of a mutual fund. It is the value of a scheme’s asset value less the value of liabilities:

(Asset- Liabilities)NAV=-------------------------------------------

No. of outstanding Units