bankruptcy implementation presentation

TRANSCRIPT

Retiree Informational Meeting

Presented By:Michael VanOverbekeGRS General Counsel

June 10, 2015

Disclaimers

The Board of Trustees of the General Retirement System of the City of Detroit makes today’s presentation for informational purposes only. Nothing stated orally or in writing in this presentation is intended to be legal advice to you.

If there are any inconsistencies between the information in this presentation and the Retirement Plan provisions, the terms of the Plan shall control.

Benefit Adjustments

Presentation Outline The Retirement Plan provisions include:

• ASF Recoupment (GRS Only)• Income Stabilization Program (GRS & PFRS)•Pension Restoration Program (GRS & PFRS)•Establishment of Investment Committee (GRS & PFRS)

ASF RecoupmentINTEREST CREDITS to the ASF

The GRS Board has historically credited ASF Accounts with the actuarially assumed rate of investment return irrespective of Plan performance.

Since the late 70’s additional interest credits were credited dependent, in part, on investment performance.

In 2011, City Council adopted an Ordinance limiting ASF interest credits to the Plan’s net investment return, with a cap of 7.9% and a floor of 0%.

The Bankruptcy Plan of Adjustment’s calculation of “excess interest” applied the 2011 interest formula to the July 1, 2003 – June 30, 2013 Recoupment Period with a 20% Cap on the highest balance in this period.

ASF RecoupmentINTEREST CREDITS to the ASF

ASF Recoupment applied to individuals that participated in the ASF between July 1, 2003 – June 31, 2013.

Initially the City mandated that ASF Recoupment be repaid by all ASF Distribution Recipients on a monthly basis over respective lifetimes at 6.75% interest. Now recoupment is over a fixed period and a limited lump sum repayment option was provided.

ASF Recoupment

Recoupment for Active or Terminated Employees with an Open ASF Account

• The “Excess Interest” which was subject to recoupment (subject to the 20% Cap) was deducted from the ASF Account and credited to the GRS “Legacy” Pension Plan.

• Effective January 2, 2015, GRSD effected 5,278 transactions with a direct recoupment of approximately $55.46 million from active ASF Accounts (25 remaining manual calcs.).

• For members/retirees with $0 or insufficient balance: monthly reduction in pension or lump sum cash option.

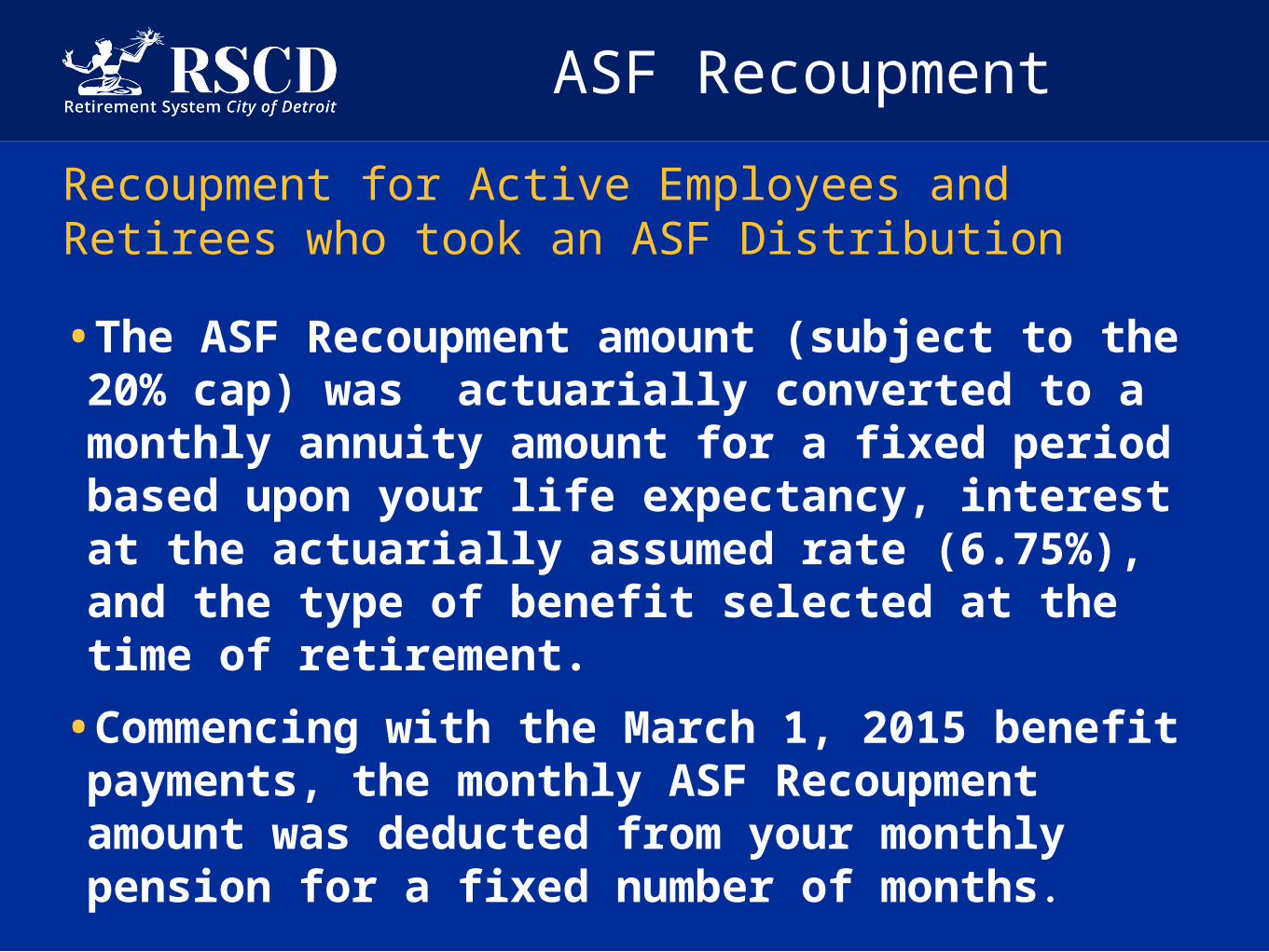

ASF RecoupmentRecoupment for Active Employees and Retirees who took an ASF Distribution•The ASF Recoupment amount (subject to the 20%

cap) was actuarially converted to a monthly annuity amount for a fixed period based upon your life expectancy, interest at the actuarially assumed rate (6.75%), and the type of benefit selected at the time of retirement.

•Commencing with the March 1, 2015 benefit payments, the monthly ASF Recoupment amount was deducted from your monthly pension for a fixed number of months.

ASF RecoupmentLump Sum Cash Option for Active Employees and Retirees who took an ASF Distribution

• In lieu of having a monthly amount deducted from pension, the Cash Option allowed for the ASF Recoupment amount to be paid in a single lump sum.

• Lump Sum election forms were mailed with a due dates for the election and the payment based upon a detailed timeline in the POA.

• Must have timely made the election (January 21, 2015) and met the payment requirements (March 24, 2015).

• Total ASF Cash Option is capped at $30M. If more than $30M elected Cash Option, participants would have gotten a pro rata share.

ASF RecoupmentLump Sum Cash Option

• 816 members timely elected the lump sum option totaling $26.47 Million (of which only 613 paid $21.49 Million).

• Late Elections –• The election due date was stated as Monday, January 19th, the Martin Luther King Jr. Holiday. • Due to the Holiday, this date was extended to Wednesday, January 21st.• On January 22nd & 23rd, KCC received an additional 39 lump sum election forms ($1.01M) timely

postmarked but received late. City is in agreement and GRS is filing a motion in Bankruptcy Court to include them.

• In lieu of having a monthly amount deducted from pension, the Cash Option allowed for the ASF Recoupment amount to be paid in a single lump sum.

• Lump Sum election forms were mailed with a due date for the election and the payment based upon a detailed timeline in the POA.

• Must have timely made the election (January, 2015) and met the payment requirements (March 24, 2015).

• Total ASF Cash Option is capped at $30M. If more than $30M elected Cash Option, participants would have gotten a pro rata share.

ASF Recoupment

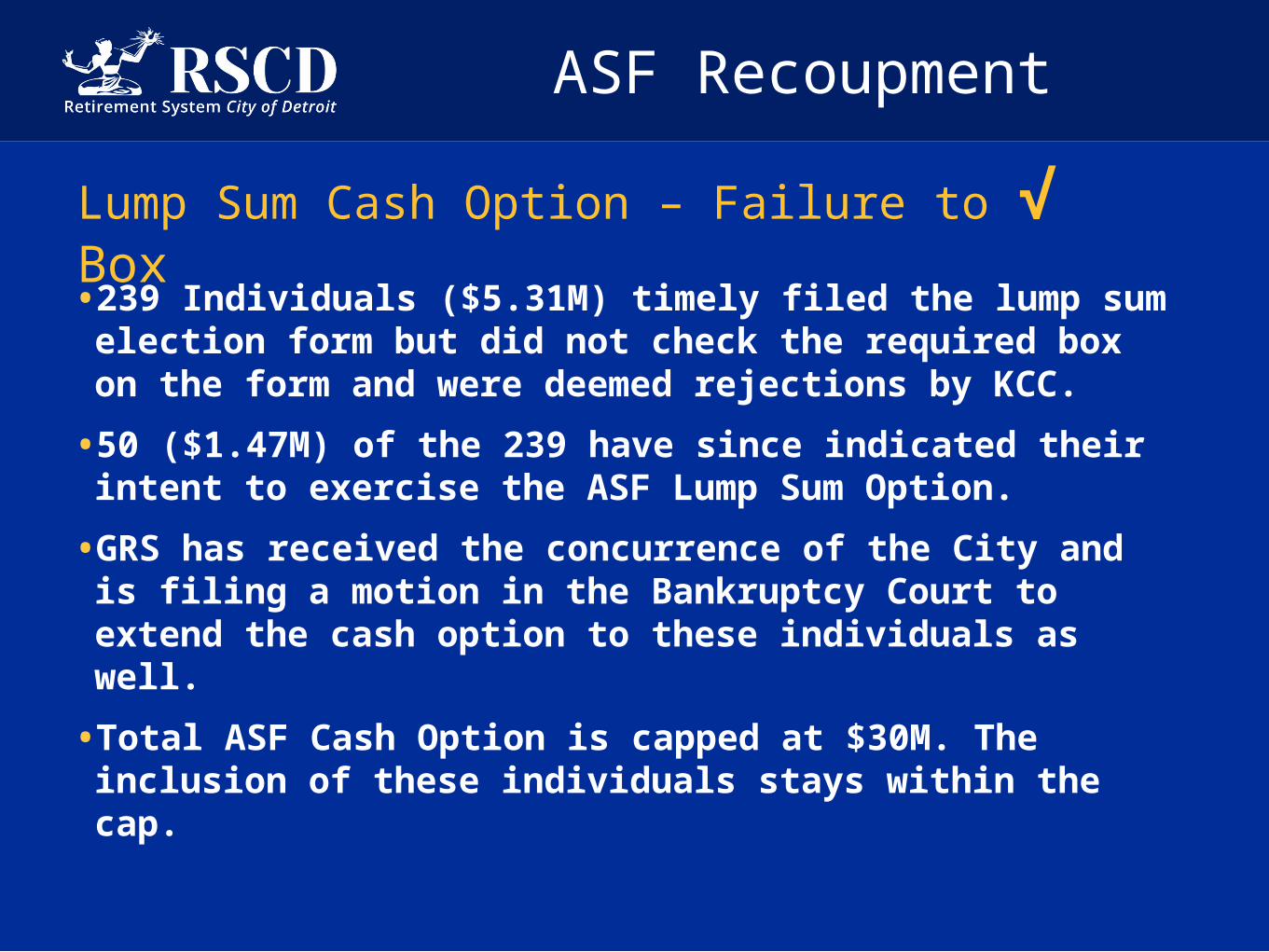

Lump Sum Cash Option – Failure to √ Box• 239 Individuals ($5.31M) timely filed the lump sum

election form but did not check the required box on the form and were deemed rejections by KCC.

• 50 ($1.47M) of the 239 have since indicated their intent to exercise the ASF Lump Sum Option.

• GRS has received the concurrence of the City and is filing a motion in the Bankruptcy Court to extend the cash option to these individuals as well.

• Total ASF Cash Option is capped at $30M. The inclusion of these individuals stays within the cap.

Income Stabilization

Program

Income Stabilization BenefitProgram Guidelines• Income Stabilization Fund - $20M over 14 years to GRS & PFRS

from UTGO Bond settlement (approx. $14M to GRS and $5M to PFRS).

•Applications were due before December 31, 2014.• Eligibility and initial benefit amounts determined by MI

Dept. of Treasury.• One-time opportunity to apply.• Amount of benefits included in monthly retirement benefit

payment.

• ISF Program was implemented commencing with March 1, 2015 retirement benefit payment.

Income Stabilization BenefitEligibility• Age 60 or older (or under the age of 18) on December 10, 2014.

• Total household income equal to, or less than, 140% of Federal Poverty Line in 2013

Income Stabilization Benefit

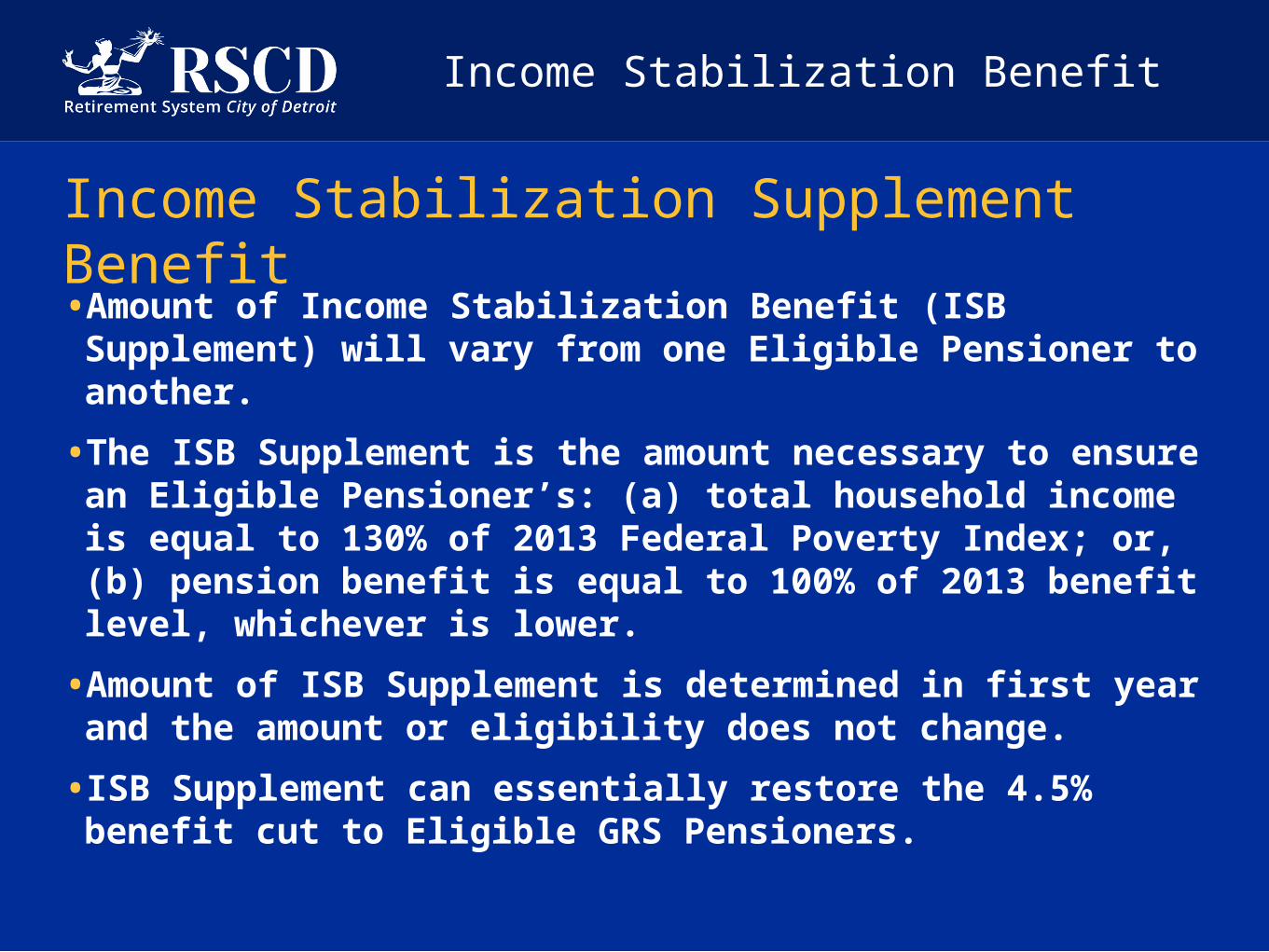

Income Stabilization Supplement Benefit • Amount of Income Stabilization Benefit (ISB Supplement)

will vary from one Eligible Pensioner to another.• The ISB Supplement is the amount necessary to ensure an

Eligible Pensioner’s: (a) total household income is equal to 130% of 2013 Federal Poverty Index; or, (b) pension benefit is equal to 100% of 2013 benefit level, whichever is lower.

• Amount of ISB Supplement is determined in first year and the amount or eligibility does not change.

• ISB Supplement can essentially restore the 4.5% benefit cut to Eligible GRS Pensioners.

Income Stabilization BenefitIncome Stabilization Benefit Plus – GRS & PFRS• ISB Plus Benefit determined as of 2015 and annually

thereafter.• Eligibility is based upon Eligible Pensioner’s 2013 household

income indexed for inflation being less than 105% of Federal Poverty Level.

• ISB Plus Benefit amount is the supplement necessary to restore an Eligible Pensioners monthly benefit to the lesser of: (a) 100% of total accrued pension benefit plus COLAs; or (b) 105% of Federal Poverty Level in that year.

• ISB Plus Benefit can essentially restore the cumulative COLAs lost as a result of the City’s bankruptcy to Eligible Pensioners.

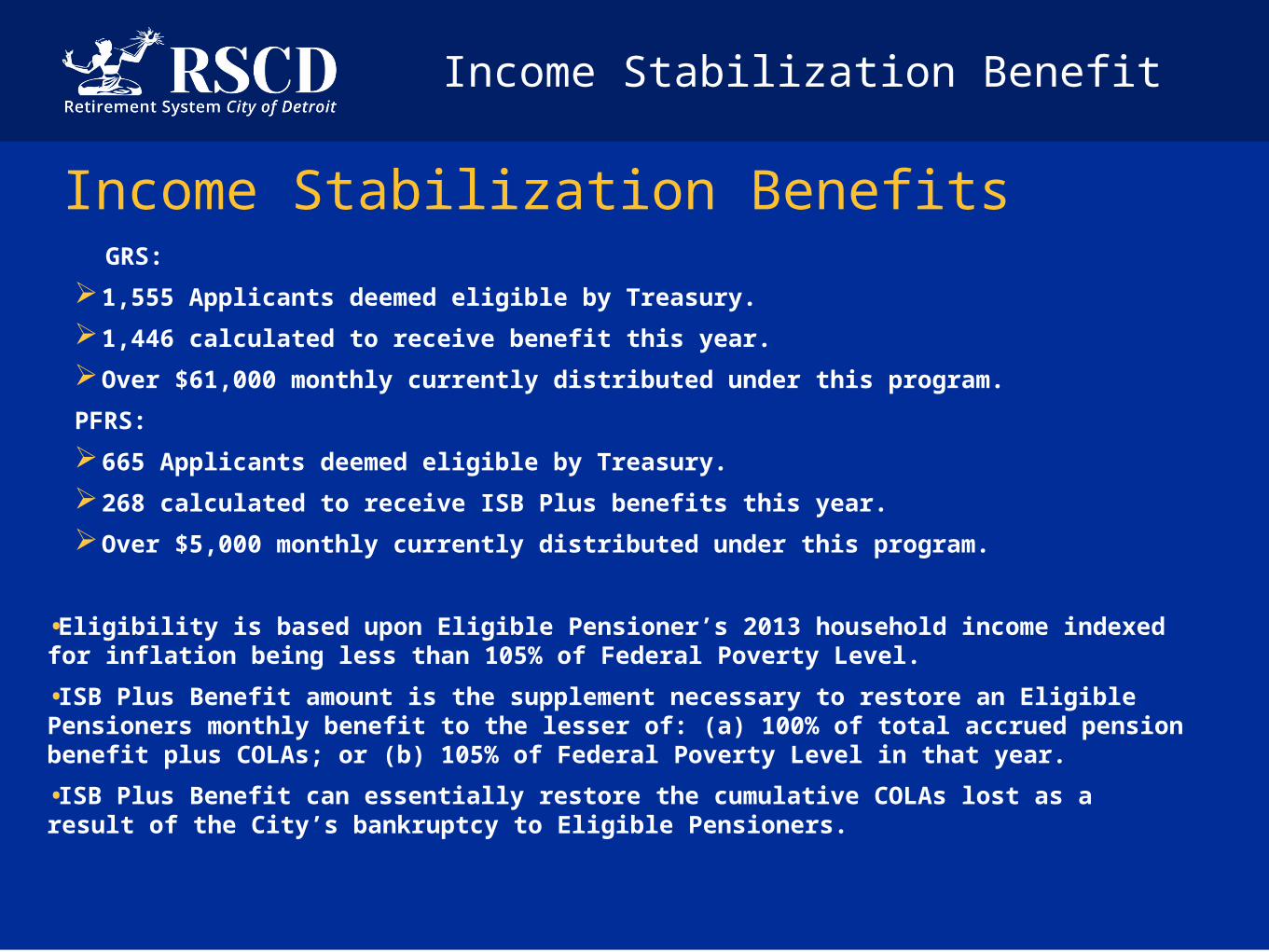

Income Stabilization BenefitIncome Stabilization Benefits

GRS:1,555 Applicants deemed eligible by Treasury.1,446 calculated to receive benefit this year.Over $61,000 monthly currently distributed under this program.PFRS: 665 Applicants deemed eligible by Treasury.268 calculated to receive ISB Plus benefits this year.Over $5,000 monthly currently distributed under this program.

•Eligibility is based upon Eligible Pensioner’s 2013 household income indexed for inflation being less than 105% of Federal Poverty Level.•ISB Plus Benefit amount is the supplement necessary to restore an Eligible Pensioners monthly benefit to the lesser of: (a) 100% of total accrued pension benefit plus COLAs; or (b) 105% of Federal Poverty Level in that year.•ISB Plus Benefit can essentially restore the cumulative COLAs lost as a result of the City’s bankruptcy to Eligible Pensioners.

Pension Restoration

Program

Pension Restoration

• Program to allow for the potential restoration of accrued benefits, including COLA and ASF Recoupment, that were reduced as part of the POA.

• Driven by improvement in the GRS & PFRS Funded Level (investment returns, actuarial experience, outside contributions).

• Supervised and administered by the respective Boards and the new Investment Committees.

• Restoration flows through 3 Waterfall Classes of participants.

GRS Pension Restoration

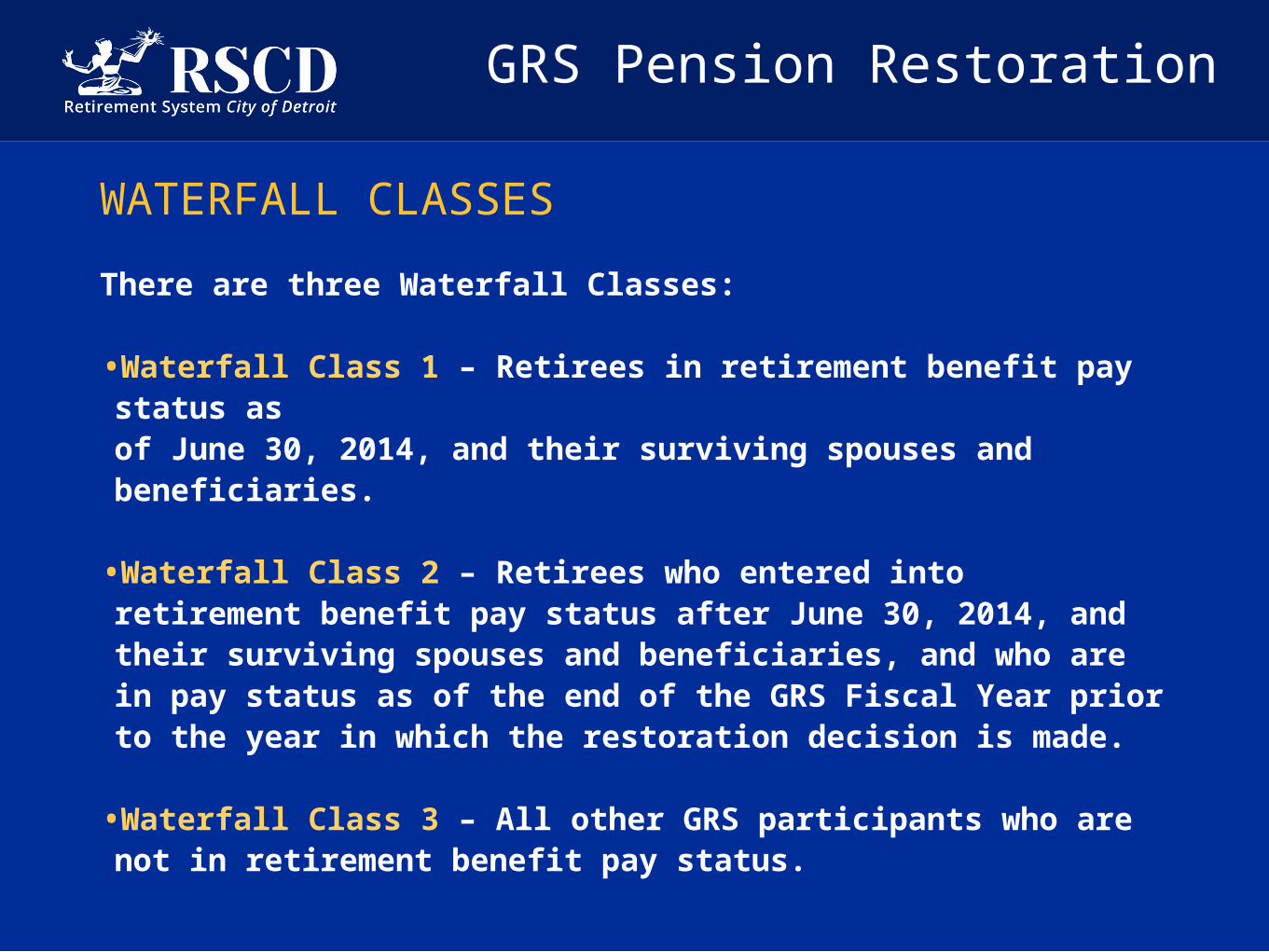

WATERFALL CLASSESThere are three Waterfall Classes:

•Waterfall Class 1 – Retirees in retirement benefit pay status as of June 30, 2014, and their surviving spouses and beneficiaries.

•Waterfall Class 2 – Retirees who entered into retirement benefit pay status after June 30, 2014, and their surviving spouses and beneficiaries, and who are in pay status as of the end of the GRS Fiscal Year prior to the year in which the restoration decision is made.

•Waterfall Class 3 – All other GRS participants who are not in retirement benefit pay status.

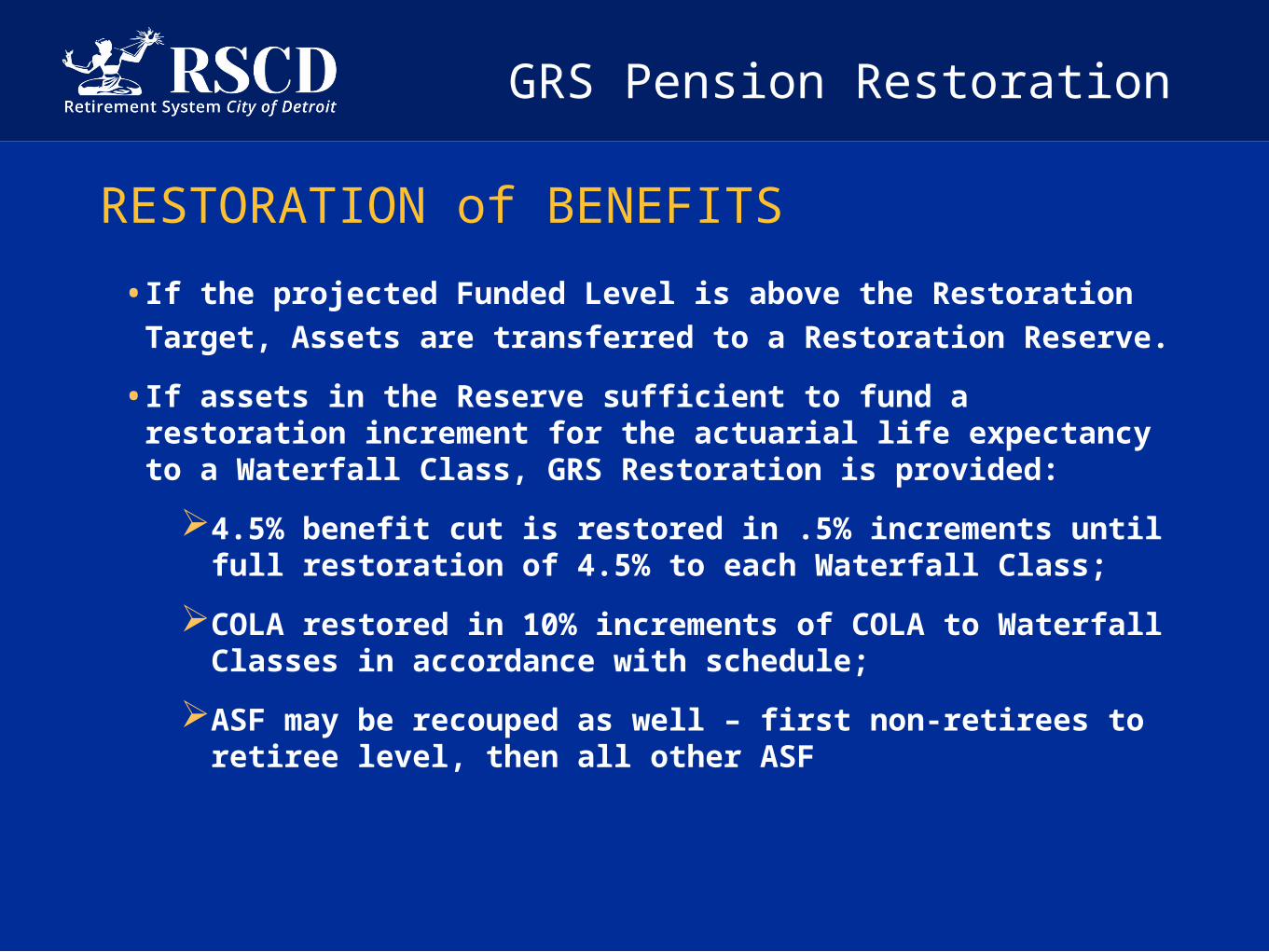

GRS Pension Restoration

RESTORATION of BENEFITS• If the projected Funded Level is above the Restoration Target,

Assets are transferred to a Restoration Reserve.

• If assets in the Reserve sufficient to fund a restoration increment for the actuarial life expectancy to a Waterfall Class, GRS Restoration is provided:

4.5% benefit cut is restored in .5% increments until full restoration of 4.5% to each Waterfall Class;

COLA restored in 10% increments of COLA to Waterfall Classes in accordance with schedule;

ASF may be recouped as well – first non-retirees to retiree level, then all other ASF

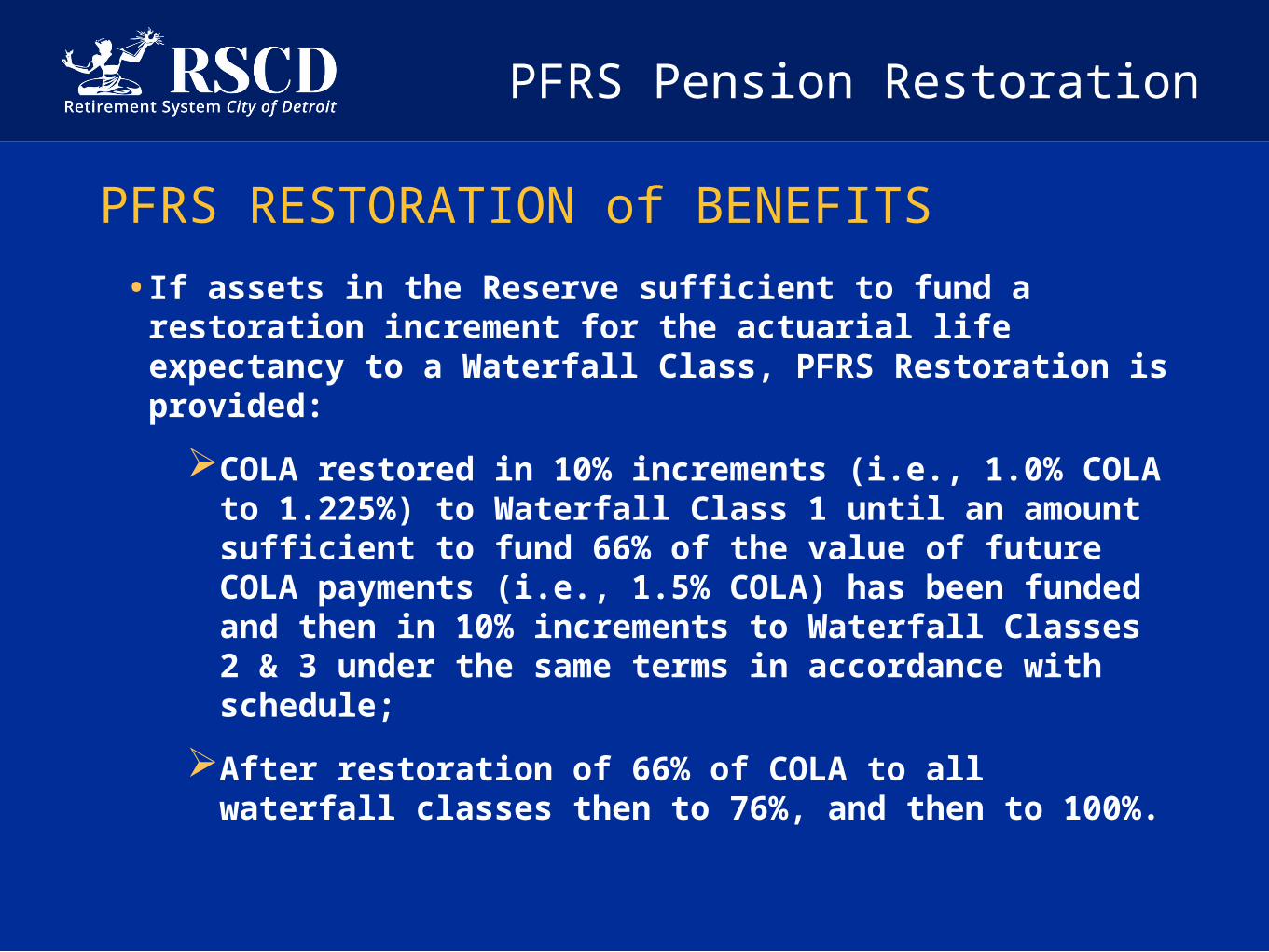

PFRS Pension Restoration

PFRS RESTORATION of BENEFITS• If assets in the Reserve sufficient to fund a restoration

increment for the actuarial life expectancy to a Waterfall Class, PFRS Restoration is provided:

COLA restored in 10% increments (i.e., 1.0% COLA to 1.225%) to Waterfall Class 1 until an amount sufficient to fund 66% of the value of future COLA payments (i.e., 1.5% COLA) has been funded and then in 10% increments to Waterfall Classes 2 & 3 under the same terms in accordance with schedule;

After restoration of 66% of COLA to all waterfall classes then to 76%, and then to 100%.

GRS Pension Restoration

GRS Restoration Program Guidelines

Period Funding Target

Restoration Target

Reserve Suspension

Restoration Reduction

Until 6/30/23 70% 75% Below 71% Below 70%

7/1/23 – 6/30/33 Actual 2023 Funded Level

Funding Target +3%;

Min. 73%

Below Funding Target + 1%

Below Funding Target

7/1/33 – 6/30/43 Actual 2023 Funded Level

Funding Target + 3%;

Min 73%

Below Funding Target +1%

Below Funding Target

GRS Pension Restoration

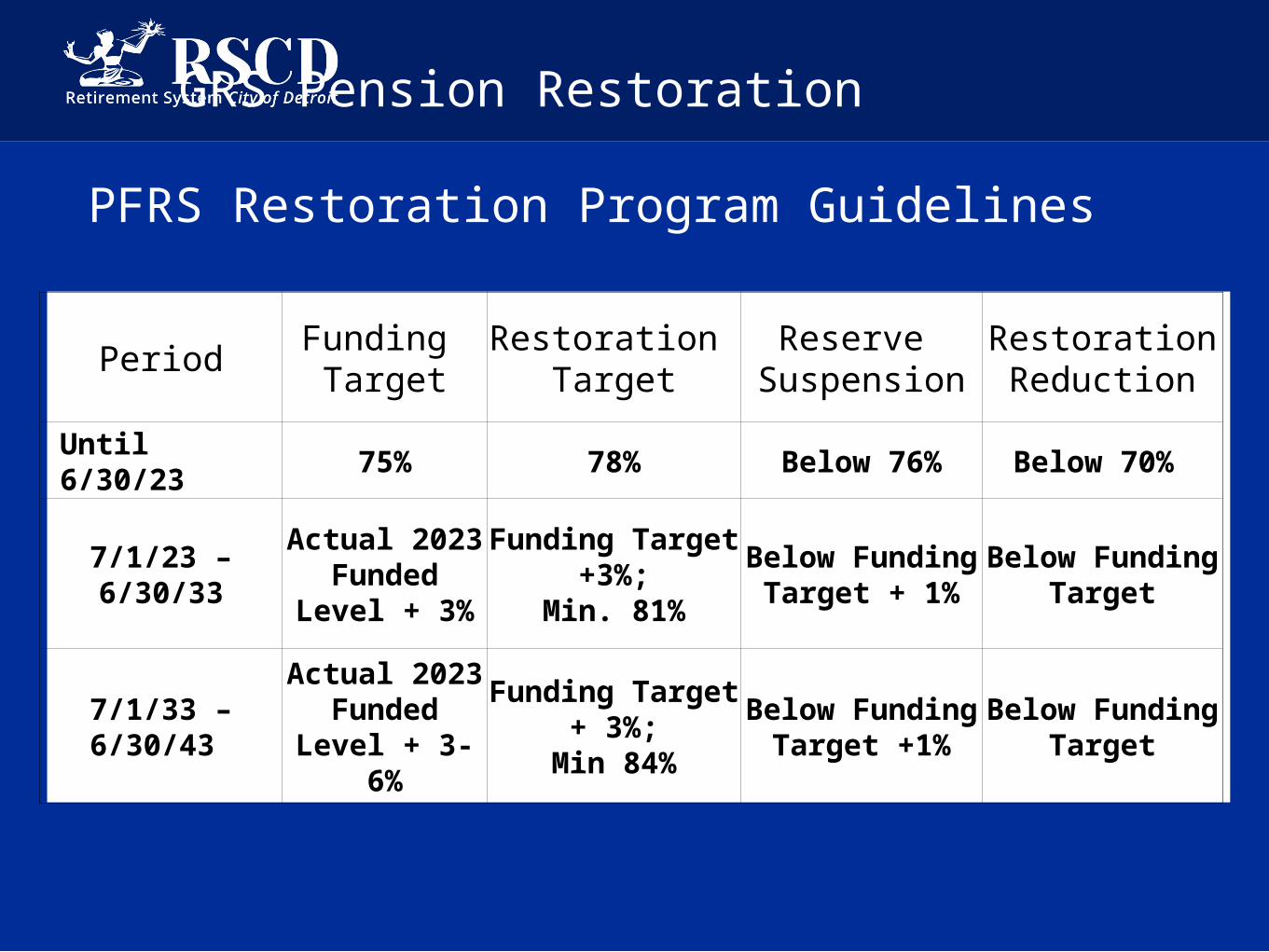

PFRS Restoration Program Guidelines

Period Funding Target

Restoration Target

Reserve Suspension

Restoration Reduction

Until 6/30/23 75% 78% Below 76% Below 70%

7/1/23 – 6/30/33Actual 2023

Funded Level + 3%

Funding Target +3%;

Min. 81%

Below Funding Target + 1%

Below Funding Target

7/1/33 – 6/30/43 Actual 2023

Funded Level + 3-6%

Funding Target + 3%;

Min 84%

Below Funding Target +1%

Below Funding Target

GRS Pension Restoration

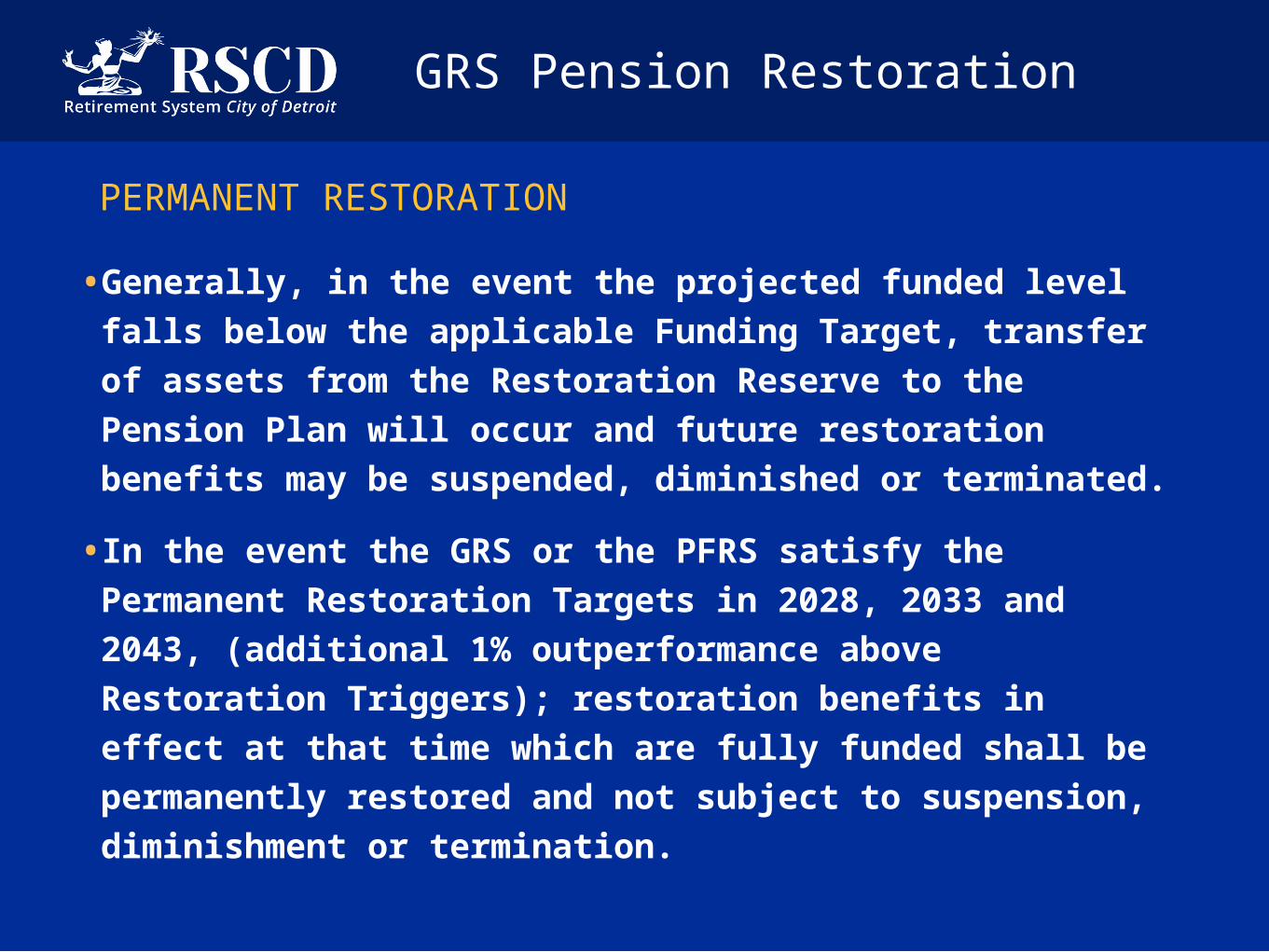

PERMANENT RESTORATION

• Generally, in the event the projected funded level falls below the applicable Funding Target, transfer of assets from the Restoration Reserve to the Pension Plan will occur and future restoration benefits may be suspended, diminished or terminated.

• In the event the GRS or the PFRS satisfy the Permanent Restoration Targets in 2028, 2033 and 2043, (additional 1% outperformance above Restoration Triggers); restoration benefits in effect at that time which are fully funded shall be permanently restored and not subject to suspension, diminishment or termination.

Investment Committee

Pension Governance under the POA

• Generally, all “investment management decisions” made by the Retirement Boards require a recommendation by the Investment Committees created by the POA.

• “Investment management decisions” is broadly defined in the POA and Retirement Plan Document (e.g., in addition to investment matters, also includes approval of actuarial, reporting and audit matters, restoration of benefits, etc.).

• The GRS Investment Committee consists of 7 members and the PFRS Investment Committee consists of 9 members.