bankasurans 2016 zirvesi - challenges & opportunities for bancassurance in the middle east...

TRANSCRIPT

Challenges & Opportunities for Bancassurance in the Middle East region

Sohail Jaffer | Deputy CEO, FWU Global Takaful Solutions | 4 October2016

Digital Bancassurance Turkey and Global 2016 Summit

Contents

1

Overview of Bancassurance: Middle East region

Challenges for Bancassurance: Middle East region

Opportunities for Bancassurance: Middle East region

Takeaways

GCC Market Overview

1. OVERVIEW: BANCASSURANCE IN THE MIDDLE EAST

Focus on 6 Middle Eastern countries within the regional intergovernmental union know as theGCC

or Gulf Cooperation Council

Oman

Country Population (mn) % expat

UAE 9.2 90%

Saudi Arabia 27.8 30%

Oman 3.3 40%

Bahrain 1.4 50%

Kuwait 2.8 70%

Qatar 2.2 85%

Total 46.7 48%

UAE Saudi Arabia

High expatriate population

Country GDP per capita

(PPP) 2015 est.

2014 Insurance

penetration rate

UAE $ 67,600 2.3%

Saudi Arabia $ 53,600 1.1%

Oman $ 44,600 1.3%

Bahrain $ 50,100 1.4%

Kuwait $70,200 0.6%

Qatar $ 132,100 1.0%

Bahrain Kuwait Qatar

High income & low insurance penetration rate

Source: CIA World Factbook,UN data (2016), Alpen Capital 2015 report 2

Insurance Market Size

1. OVERVIEW: BANCASSURANCE IN THE MIDDLE EAST

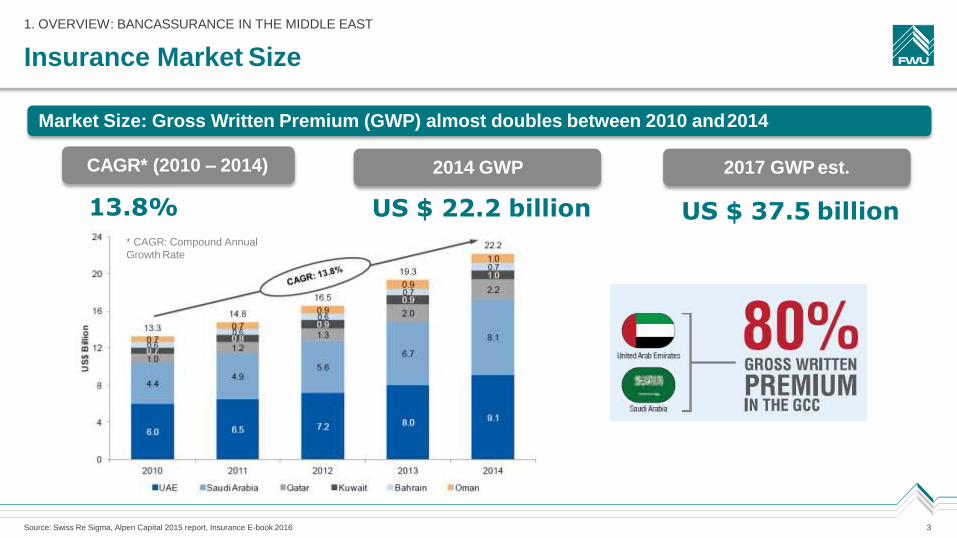

Market Size: Gross Written Premium (GWP) almost doubles between 2010 and2014

CAGR* (2010 – 2014)

13.8%

* CAGR: Compound Annual

Growth Rate

2014 GWP 2017 GWP est.

US $ 22.2 billion US $ 37.5 billion

Source: Swiss Re Sigma, Alpen Capital 2015 report, Insurance E-book 2016 3

Insurance Products Distributed

1. OVERVIEW: BANCASSURANCE IN THE MIDDLE EAST

Non-life insurance accounts for the majority of GWPs in

the GCC

Main product lines distributed in the GCC include:

Life:

Term life, Credit Life &

Savings products are in their

infancy, but growing

Non-Life:

Motor

Building / Household

Corporate Savings Plans

Health insurance

Several international providers are present, however the

market is dominated by national / regional playersMajor Re-insurers that have established a

GCC presence

Source: Insurance E-book 2016 4

Insurance Distribution Channels

1. OVERVIEW: BANCASSURANCE IN THE MIDDLE EAST

Banks

Direct marketing

Insurance Agency salesforce

In some cases serving bank customers based on referrals

Internet

Agents

Independent Financial Advisors (*IFAs) / Brokers

Retail / Corporate segment

Neutral

comparison

websites

Comparison websites are gaining traction in the GCC, e.g.: www.souqalmal.com

www.compareit4me.com

www.bayzat.com (Health insurance only)

Brokers / *IFAs

Important distribution channel, as the customer already hasa

relationship with the bank

More attractive pricing, as distribution costs often lower

Out-bound call centre

5

What makes bancassurance an attractive distribution channel

1. OVERVIEW: BANCASSURANCE IN THE MIDDLE EAST

Customer Benefits Benefits for Banks

Benefits for Insurance companies

Sources: Bancassurance in Practice, Munich Re; The global bancassurance market (June 2014), Sidley Austin LLP 6

retain bank

New product line (Insurance)

Additional fee based income

Cross-selling opportunities help

customers

Increase share of customer’swallet

Increase productivity of sales teams

Opens a new distribution channel

Annuity based fee income / EmbeddedValue

Access to bank’s existing customer base at an

effective cost

Economies of scale as critical mass is achieved

relatively faster

Customers already have existing relationship

with bank

Easy access to insurance products through

trusted bank brand

Bancassurance products are usually simple

and easy to understand

Bank staff well placed to advise on insurance

products that complement other consumer

finance products (e.g. homemortgage)

More attractive pricing of bancassurance

products, as distribution cost are often lower

Bank Distribution Models

1. OVERVIEW: BANCASSURANCE IN THE MIDDLE EAST

Direct Sales Team (DST)

Bank employs a dedicated Direct Sales Team

to distribute insuranceproducts

The DST is usually very mobile, often visiting

clients off-site

Mobile digital technology performing contract

issuance has boosted this distributionmodel

Implant Model

Insurance company sales staff usually have a

physical presence in Bank branches

Bank employees source referrals

Successful case studies include: AXA / Bank

Mandiri in Indonesia

(RMs)

customer

Bank Branch Distribution

Bank branch relationship managers

distribute selected insuranceproducts

CFPs support branch clusters

RMs able to optimise on existing

relationships

Referral Model

Bank branch employees refer customer leads

7

to either insurance company sales staff or

dedicated bank insurance sales team

Call centre / branch RMs facilitate sales

An efficient system for managing referrals of

warm leads is vital

Challenges for Bancassurance in the Middle East

8

2. CHALLENGES FOR BANCASSURANCE IN THE MIDDLE EAST

Bank Branch Distribution

As the GCC does not represent a single market (unlike the European Union), no cross border distribution is

possible

Insurance providers are required to establish a legal presence in each of the 6 countries that they wish to

distribute products

This limits the potential for economies of scale, as insurance providers are required to deal with 6 different

regulatory regimes and different currencies, in addition to requiring full regulatory capital in eachmarket

As a result, offering customers attractive solutions / pricing becomeschallenging

Referral Model

As the GCC economies are still growing, the breadth and depth of local capital markets is low, particularly

within equity markets

As a result, many investors focus on the local Fixed Income, Money Markets and RealEstate

However, this means that delivering attractive investment returns remains a challenge – with several

providers offering risk calibrated strategies for their long term savingsplans

Challenges for Bancassurance in the Middle East

2. CHALLENGES FOR BANCASSURANCE IN THE MIDDLE EAST

Low customer awareness about benefits of insurance

The low customer awareness about the benefits of insurance is reflected by the low insurance penetration

rate in the GCC region of 1.4% (Swiss Re Sigma, 2014)

As a result, insurance that is required by law accounts for a large portion of annual Gross Written Premiums

(GWPs).

In most GCC countries motor and health insurance aremandatory

Customer risk profiling and fact finds vary from one provider to another

No regulatory requirement for insurance sales staff certification

Within the GCC, few regulators require insurance sales staff to be certified, as is the case in most developed

markets

Certified Financial Planners (insurance sales staff) can benefit the bancassurance channel

9

improved customer service

Price competition is rife

Particularly within motor and health insurance, insurers use price competition as a way to win newbusiness

This practice is tantamount to paying for new business, and as both motor and health insurance are sold in

yearly policies, instead insurers would be better served by differentiating their offeringwith:

Challenges for Bancassurance in the Middle East

2. CHALLENGES FOR BANCASSURANCE IN THE MIDDLE EAST

Few regional banks with cross border presence

Fragmented banking industry means that economies of scale are difficult toachieve

Multiple providers in mid sized banks create shelf space managementchallenges

Necessary investment in employee training, digital applications and programs to enhance customer

satisfaction are difficult to achieve for many banks

Certain insurers have entered into multi-year preferred distribution agreements with banks

In terms of these preferred distribution agreements, the insurer often needs to pay an exclusive marketing

fee to the relevant bank, in addition to productcommission

Due to the additional marketing fee incurred, the insurer’s margins are compressed

10

tailored or bundledproducts

Opportunities for Bancassurance in the Middle East

3. OPPORTUNITIES FOR BANCASSURANCE IN THE MIDDLE EAST

Understanding that different distribution channels are neededto

reach different customer segmentsCustomer segmentation

Different bank customer segments have different savings&

protection needs

Contact needed with experienced

CFPs

Affluent customers

Mass-Affluent customers

Retail customers

Customer Segments

Pure

Protection

•PA

•Travel

•Credit

Life

•Funeral

Policy

Product types

Single

premium

Long term

savings

Regular

premium

Long term

savings

Product mix & customer segments will

determine

the

distribution channel selected

Products requiring higher levels of long term financial commitment need distribution

channels with experienced Certified Financial Planners(CFP)

11

Mobile phones

Opportunities for Bancassurance in the Middle East

3. OPPORTUNITIES FOR BANCASSURANCE IN THE MIDDLE EAST

Mobile direct sales team is becoming increasingly important to grow and service a customer

orientated bancassurance business franchise

Direct Sales Team (DST) importance is growing, especially in enhancing customerexperience

Digital applications / tablets facilitate transactions when and where it is convenient for thecustomer

Use of Technology is important to deliver suitable customer solutions in a seamless way

Some banks have deployed DSTs equipped with digital applications / iPads to facilitate distributionof

bancassurance products, however the development of these solutions still has some way togo

Digital technology is changing the way customer want to interact and purchase products (including

bancassurance)

80%

2/3

Technology can be used to:

TwitterProfile customers

Deliver suitable customersolutions in a seamless way

Opportunity to

engage

Estimated global population access by 2020:

12

Smart phones +

tablets

Opportunities for Bancassurance in the Middle East

3. OPPORTUNITIES FOR BANCASSURANCE IN THE MIDDLE EAST

Quality Assurance is an after-sales activity

that contributes to service excellence

Quality Assurance is aboutensuring

the quality of business sold,

optimising customer satisfaction,

leading to lower lapsation

Increase Customer Satisfaction

Improve Quality of Business

Reduce mis-sellingMitigants:

Customer suitability / profiling

Certification

Call back procedures

Key Service Enhancements:

Call back procedures ensure that customers

understand the product they havepurchased

Enhances the sales process by collecting

customer feedback

Increase efficiency by reducing mis-selling

and thereby reducing future contract lapsation

Customer complaint resolution procedures

enhance customer experience

13

Opportunities for Bancassurance in the Middle East

3. OPPORTUNITIES FOR BANCASSURANCE IN THE MIDDLE EAST

Customer needs surveys leading to understanding the real needs of customers

Banks are in a unique position to be able to conduct customer surveys to better understand needs of

specific customer segments

By understanding the real customer needs, rather than perceived needs, banks are able to develop suitable

customer solutions together with insuranceproviders

Certified Financial Planners (CFPs)

Few regulators have a requirement for insurance sales staff to attain certification viaexams

Certification of the bancassurance sales team is about elevating the level of customer service onoffer

Certification enhances professional sales skills, benefiting banca distribution channels within several areas:

1.Improve CFP skills in: 2. Benefits of well informed BancaCFPs:

14

Customer Service

Product Knowledge

Application of Selling techniques

Conflict handling

Distinguish channel fromcompetitors

Improve image among customers

Retain existing customers

Attract new customers

Opportunities for Bancassurance in the Middle East

Sources: Towers Watson 15

3. OPPORTUNITIES FOR BANCASSURANCE IN THE MIDDLE EAST

Unfunded End of Service Gratuity liability of $25 billion +

For most non-GCC nationals (expatriates) in the GCC, occupational retirement schemes do not exist

Instead, employers are required by law to provide expatriates with a lump-sum payment, known as theEnd

of Service Gratuity, at the end of their service to the employer

There is no legal requirement for employers to fund the End of Service Gratuity liability; and employers use

accrued End of Service Gratuity money as part of their workingcapital

As a result there is an opportunity to provide solutions that meet the needs of employers and expatriatestaff

The combined End of Service Gratuity liability of employers in the GCC is expected to increase to over$75

billion by 2020, according to Towers Watsonresearch

Retirement Savings Plans

Across the GCC, EY estimates that public pension funds (for GCC nationals) amounts to $ 397 billion or $

15,000 per GCC national

While, within the GCC, there is no retirement savings mechanism for foreigners (non-GCC nationals),who

make up 48% of the population. As a result this segment represents a significant opportunity for

bancassurance growth

Opportunities and Challenges

Source: E&Y: The Bancassurance Bulletin: January – May 2013 16

4. TAKEAWAYS

Challenges need to be overcome to unlock opportunity of Bancassurance partnerships

Challenges to Bancassurance Partnerships

Inequitable allocation of costs betweenpartners

Uneven recognition of the value that insurance sales add to the bank’s core products and services

Differing views of best product, best channel and customer segmentation of needs andwants

Resistance to share data / information

Attempts to dominate the relationship by eitherparty

Bancassurance is an important & growing distribution channel for the GCCregion

Implant and Direct Sales Team models are proving very successful

Bancassurance offers Insurers access to large receptive customersegments:

Provides platform for customer awareness of insurance

Can contribute to rapid growth in new business

Thank you…

Subtitle | Presenter | Date 17

Sohail Jaffer

International Business

Development, Partner

FWU Global Takaful Solutions

Al Fattan Currency House Bldg., Level16

Dubai International Financial Centre

Dubai, UAE

Phone: +971 44175 422

Fax: +971 44175 555

Email: [email protected]

The information in this presentation does not constitute a sales offer, investment advice or an offer for the acquisition of financial products, and shall not in

this regard imply obligations for the FWU Group or anybody else towards the readers of the presentation.

This presentation is solely intended to provide information on matters of interest for the readers and as such information is not meant to replace the

knowledge and the judgment of the readers who should make all appropriate inquiries.