bank of america corporation legislative & regulatory retirement update tony ranallo, cfp®,...

TRANSCRIPT

Bank of America Corporation

Legislative & Regulatory Retirement Update

Tony Ranallo, CFP®, CIMA®, CPWA®Senior Vice President – Wealth ManagementPortfolio Manager

Ranallo GroupMerrill Lynch Wealth Management400 Locust, Ste 600Des Moines, IA 50309515.245.8045

2

Bank of America Corporation

Tony Ranallo, CFP®, CIMA®, CPWA® - Senior Vice President – Wealth Management, Portfolio Manager

Since he started in the financial services industry in 2002, Tony has specialized in working with corporate retirement plans and qualified individuals, focusing on retirement asset accumulation and distribution strategies. He now oversees The Ranallo Group at Merrill Lynch, one of the largest wealth advisory teams in the state managing more than $300 million in assets for individual and corporate clients.

Tony graduated Cum Laude from Arizona State University with a Bachelor of Science in Finance and later completed his Masters of Science in Financial in Denver, Colorado.

Continuing to place an emphasis on education, Tony was one of the youngest professionals in the country to attain the CERTIFIED FINANCIAL PLANNERTM (CFP®) certification, and later completed the Retirement Plans Associate (RPA) designation in 2007.

He has also completed the CIMA® designation and recently completed the CPWA® program.

The Certified Investment Management AnalystTM (CIMA®) designation program is recognized as the standard for advanced investment consulting. This credential communicates to clients and peers that the consultant has completed a rigorous process reflecting a high level of competency, professionalism, and investment expertise. The program is dually sponsored by the Wharton School of Business, University of Pennsylvania and the Investment Management Consultants Association (IMCA).

The Certified Private Wealth AdvisorSM (CPWA®) designation program is an advanced credential created specifically for wealth advisors who work with high-net-worth clients on the life cycle of wealth: accumulation, preservation, and distribution. The program is dually sponsored by the Booth School of Business, University of Chicago and the Investment Management Consultants Association (IMCA).

Locally, Tony is active with numerous non-profit organizations. He is on the board of the Des Moines Community Playhouse and works closely with several other local charities such as Amanda the Panda. Tony was a Business Record Forty under 40 selection in 2014.

Tony resides in Waukee, Iowa with his wife Kimberly, their sons A.J. and Frankie, and daughter Peyton .

3

Bank of America Corporation

Frank the tank

4

Bank of America Corporation

Trends in the retirement plan market

Continued movement toward defined contribution plans Government plans last to adopt 401(k) style plans– Tennessee moving to hybrid 401(k) pension plan

More emphasis on participant readiness Shift focus to participant outcomes, not just limiting liability to

fiduciaries

Consolidation of investment menus Limit choices to reduce complexity to participants Reduce investment overlap Move to core asset classes vs. stylized asset classes (Midcap Blend

vs. Midcap Value and Midcap Growth)

5

Bank of America Corporation

Trends in the retirement plan market

Adding asset classes to allow for more diversification Real Estate, Inflation Protected Bonds, Short Duration Bond Liquid Alternatives

Move from actively managed funds to passive index funds Lower cost and reduce tracking error to underlying benchmarks Less liability for Fiduciaries from a monitoring standpoint

Guaranteed lifetime income offerings Annuity like living benefits that guarantee income Reduces risk of market volatility reducing retirement income, outliving

ones assets Can be issues with portability when trustees move platforms

6

Bank of America Corporation

Proposed Fiduciary Rule

Brokers and financial professionals must act in fiduciary capacity when working with retirement accounts

Must provide advice that’s in the best interest of the client

Current non-advisory accounts are held to a ‘suitability’ standard, not a ‘fiduciary’ standard like fee based advisory accounts Advisors are not liable for investment selection in non-advisory,

brokerage accounts

Requires more extensive client profiling by the advisor, annual client reviews, etc.

7

Bank of America Corporation

Proposed Fiduciary Rule

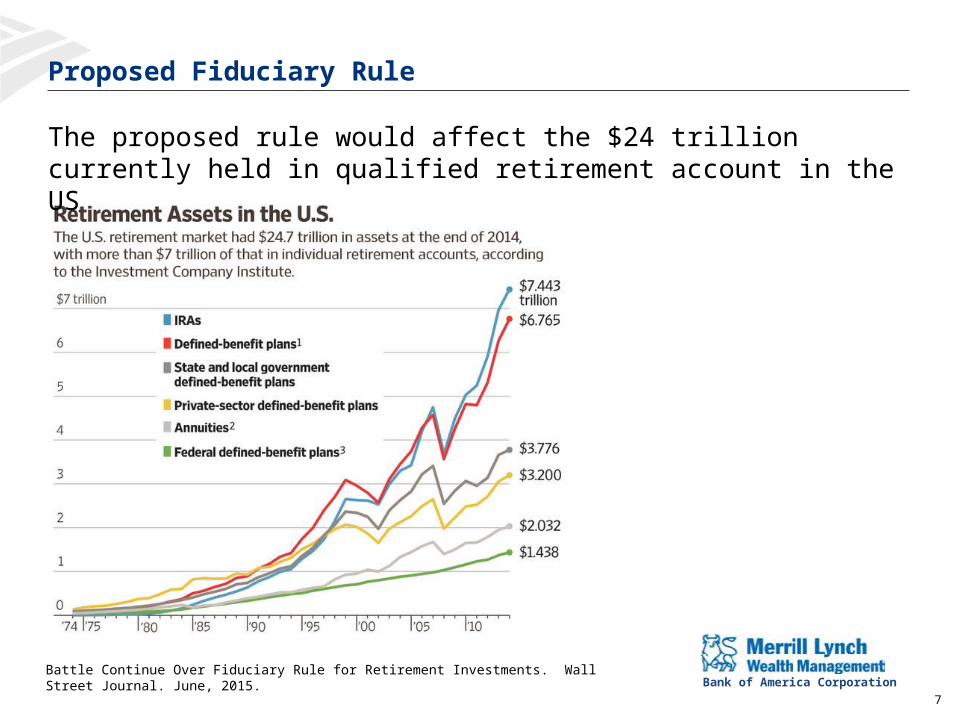

The proposed rule would affect the $24 trillion currently held in qualified retirement account in the US

Battle Continue Over Fiduciary Rule for Retirement Investments. Wall Street Journal. June, 2015.

8

Bank of America Corporation

Proposed Fiduciary Rule

Complaints revolve around additional costs and liability

Compliance monitoring and administrative costs would increase Internal systems and controls would need to be upgraded Additional compliance specialists added, especially for smaller broker

dealers

Legal departments would have to be expanded Qualified account holdings could be challenged by clients who feel

their investments ‘are not in their best interest’ Disclosures created to defend proprietary investment offering vs.

lower cost third party investments Difficulties recommending insurance based products with high

expenses and long surrender periods

9

Bank of America Corporation

Proposed Fiduciary Rule

Summary

The rule would provide for a uniform fiduciary-duty rule across retirement accounts, whether in a brokerage or fee based advisory account

Proposed rule will have the largest affect on companies offering brokerage and insurance solutions for qualified assets

Expected to reduce a firm’s ability to push proprietary firm sponsored investments

Promote ongoing, active relationships between advisors and clients with qualified assets

10

Bank of America Corporation

State Run Retirement Plans

The President’s 2016 fiscal budget would allot $6.5 million to support several two-year pilot programs for states to experiment with ways to expand private sector retirement options. Those include 401(k) plans and individual retirement accounts, particularly for people whose employers do not currently offer a plan.

State’s would create retirement plans, similar to health exchanges, for employees that are not offered, or do not qualify for their company’s retirement plan

Currently, 80% of workers have access to an employer sponsored retirement plan Of that, 80% are participating

11

Bank of America Corporation

Self Directed Brokerage Accounts

What are they?

Self-direct brokerage accounts remain part of plan assets, and as such are subject to the same rules and regulations as the 401(k) plan. The self-direct brokerage service is designed to give participants more flexibility with their retirement planning by offering a brokerage experience, while also allowing plan sponsors the ability to maintain control. 30% of retirement plans offer a self directed feature Usually found in large employer plans (greater than 5,000

employees)

12

Bank of America Corporation

Self Directed Brokerage Accounts

Plan Sponsors can:

Restrict the types of investments participants can choose from Full investment capabilities Mutual funds only Equity/Fixed Income Investments only

Establish a minimum participant core account balance required prior to opening a self-direct brokerage account

Establish maximum percentage of overall participant account balance permitted in self directed brokerage account

13

Bank of America Corporation

Self Directed Brokerage Accounts

Department of Labor is considering requiring additional oversight for self directed brokerage accounts by plan Fiduciaries

Many participants are not equipped with the financial knowledge to select suitable investments

Some plans only allow self direction as a way to sidestep fiduciary duties and not provide a core menu of investments

Most brokerage windows offer participants little to no guidance and access to an almost unrestricted universe of investments

14

Bank of America Corporation

Self Directed Brokerage Accounts

Summary

Currently only a Request for Information by the Department of Labor

Expect more serious discussions if proposed Fiduciary Rule is passed

Many times, a self directed brokerage account is not in the best interest of the participant Universe of securities overwhelming Portfolios tend to hold concentrated positions that are not in line with

a participant’s risk tolerance Advisor replicates strategy in self directed brokerage account that

could be implemented in core plan for less cost– Institutional vs. retail funds– No trading cost in core plan, funds purchased at net asset value

Bank of America Corporation

Regulatory Update – Lifetime Retirement Income

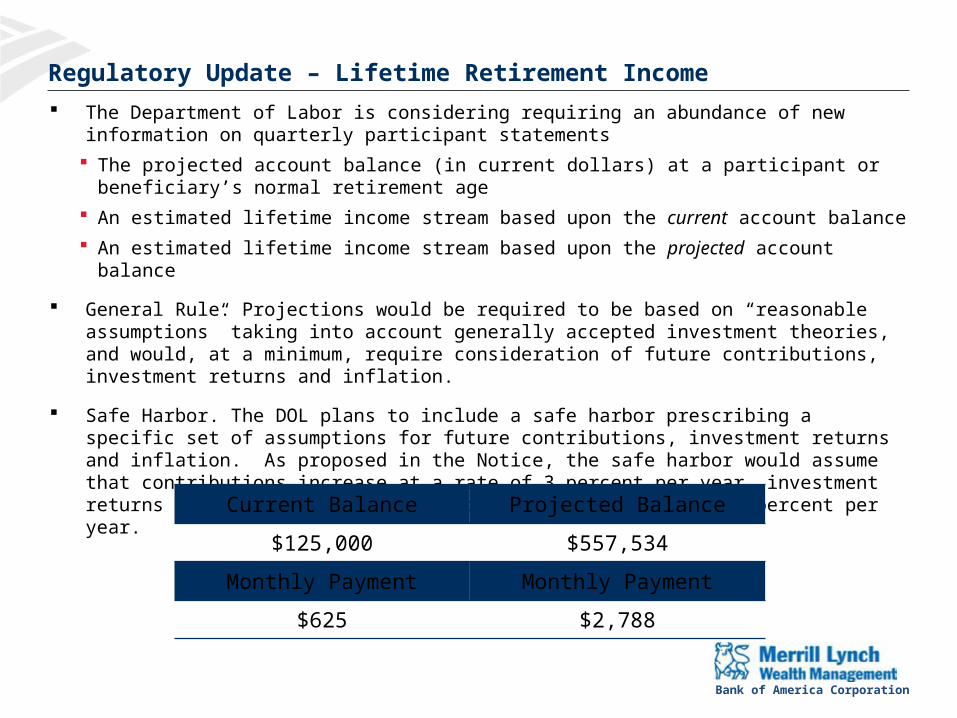

The Department of Labor is considering requiring an abundance of new information on quarterly participant statements

The projected account balance (in current dollars) at a participant or beneficiary’s normal retirement age

An estimated lifetime income stream based upon the current account balance

An estimated lifetime income stream based upon the projected account balance

General Rule. Projections would be required to be based on “reasonable assumptions” taking into account generally accepted investment theories, and would, at a minimum, require consideration of future contributions, investment returns and inflation.

Safe Harbor. The DOL plans to include a safe harbor prescribing a specific set of assumptions for future contributions, investment returns and inflation. As proposed in the Notice, the safe harbor would assume that contributions increase at a rate of 3 percent per year, investment returns are 7 percent per year, and the inflation rate is 3 percent per year.

Current Balance Projected Balance

$125,000 $557,534

Monthly Payment Monthly Payment

$625 $2,788

Bank of America Corporation

Regulatory Update – Service Provider and Participant Disclosures

On February 3, 2012, the Department of Labor published final regulations on fee disclosure for retirement plans that ultimately became effective July 1, 2012.

Plan fiduciaries must ensure plan investment expense and compensation to service providers are “reasonable”

Plan Service Providers must disclose via the 408(b)(2) disclosure the fees they receive and the services they provide

Plan fiduciaries must disclose certain plan, fee, and investment related information to participants via the 404(a) fee disclosures Disclosures can be delivered electronically Pending legislation to require a ‘guide’ to assist plan fiduciaries if fee

disclosure is contained in multiple or ‘lengthy’ documents–Awaiting definition of ‘lengthy’

Bank of America Corporation

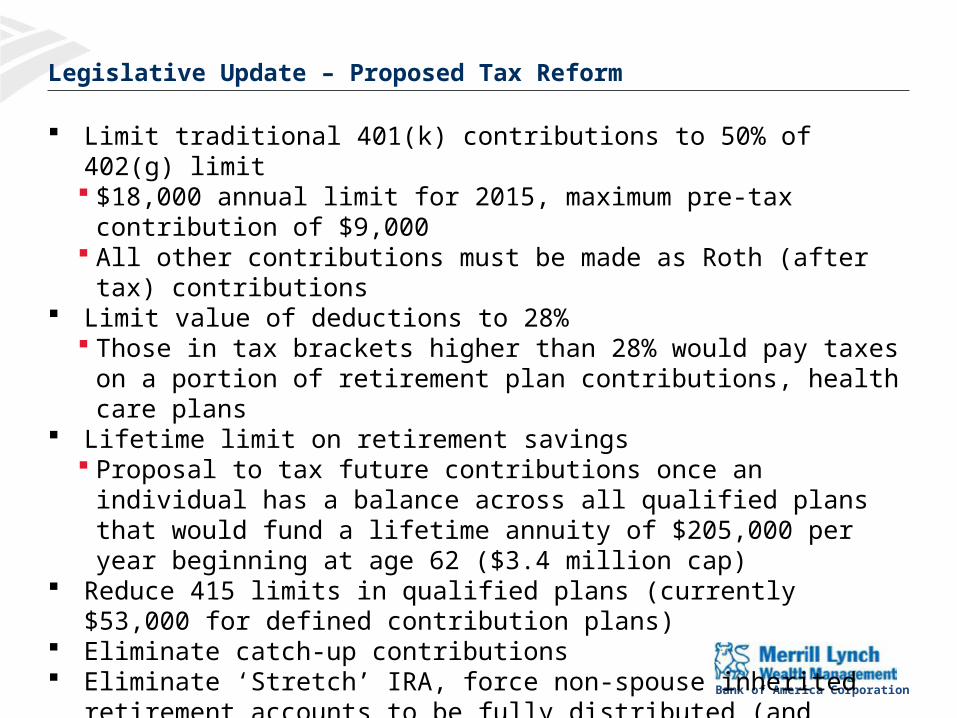

Legislative Update – Proposed Tax Reform

Limit traditional 401(k) contributions to 50% of 402(g) limit $18,000 annual limit for 2015, maximum pre-tax contribution of $9,000 All other contributions must be made as Roth (after tax) contributions

Limit value of deductions to 28% Those in tax brackets higher than 28% would pay taxes on a portion of

retirement plan contributions, health care plans Lifetime limit on retirement savings

Proposal to tax future contributions once an individual has a balance across all qualified plans that would fund a lifetime annuity of $205,000 per year beginning at age 62 ($3.4 million cap)

Reduce 415 limits in qualified plans (currently $53,000 for defined contribution plans)

Eliminate catch-up contributions Eliminate ‘Stretch’ IRA, force non-spouse inherited retirement accounts to

be fully distributed (and taxed) within 5 years Required minimum distributions for Roth IRAs

Bank of America Corporation

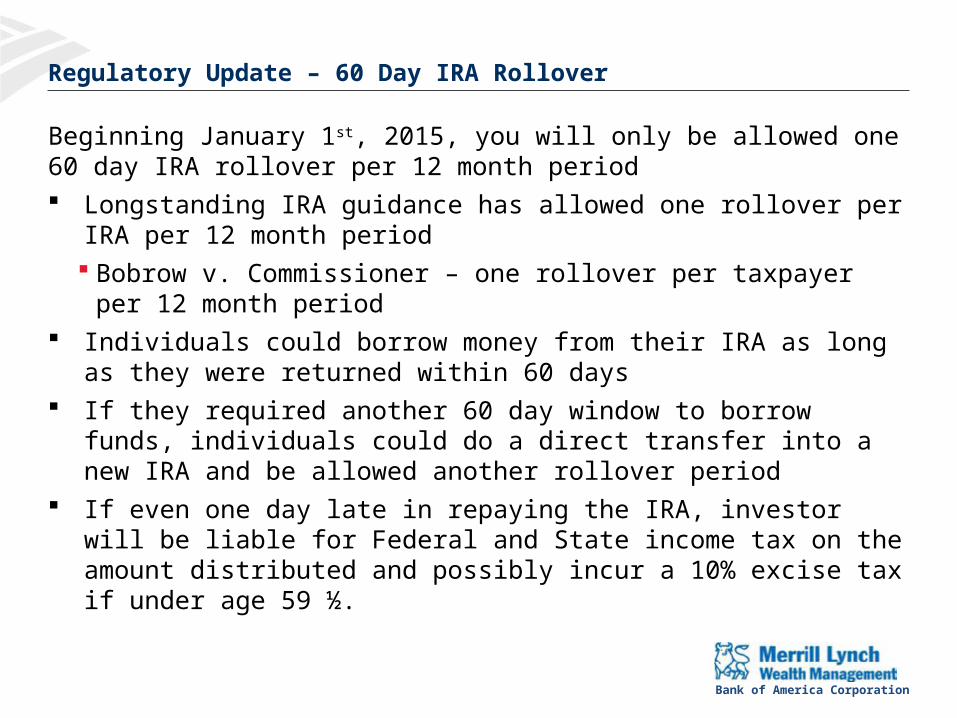

Regulatory Update – 60 Day IRA Rollover

Beginning January 1st, 2015, you will only be allowed one 60 day IRA rollover per 12 month period Longstanding IRA guidance has allowed one rollover per IRA per 12

month period Bobrow v. Commissioner – one rollover per taxpayer per 12 month

period Individuals could borrow money from their IRA as long as they were

returned within 60 days If they required another 60 day window to borrow funds, individuals could

do a direct transfer into a new IRA and be allowed another rollover period If even one day late in repaying the IRA, investor will be liable for Federal

and State income tax on the amount distributed and possibly incur a 10% excise tax if under age 59 ½.

19

Bank of America Corporation

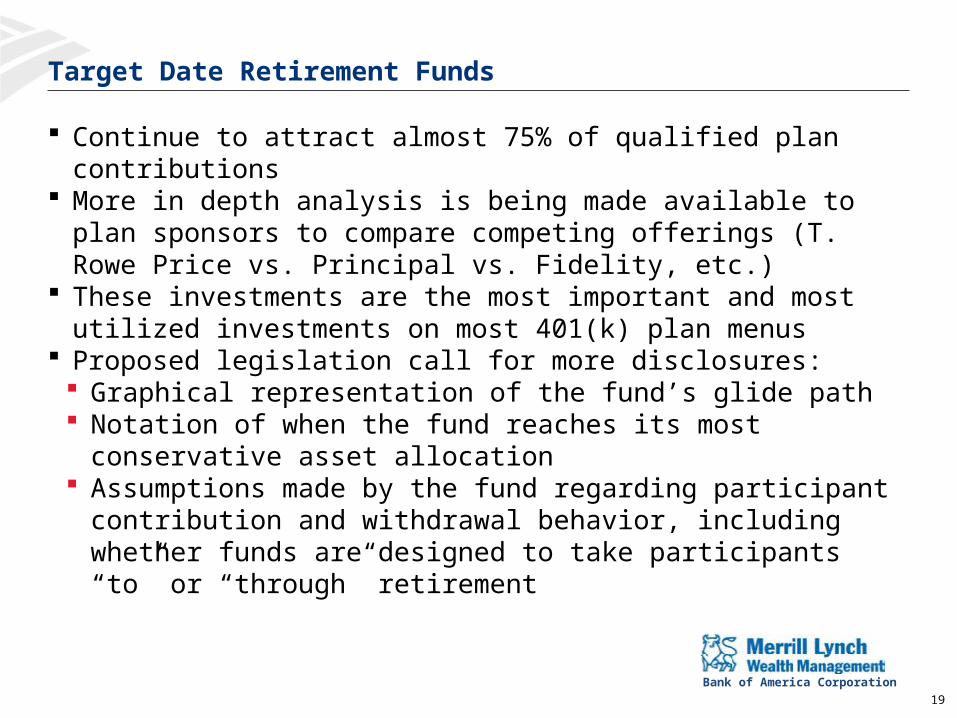

Target Date Retirement Funds

Continue to attract almost 75% of qualified plan contributions More in depth analysis is being made available to plan sponsors to

compare competing offerings (T. Rowe Price vs. Principal vs. Fidelity, etc.)

These investments are the most important and most utilized investments on most 401(k) plan menus

Proposed legislation call for more disclosures: Graphical representation of the fund’s glide path Notation of when the fund reaches its most conservative asset

allocation Assumptions made by the fund regarding participant contribution and

withdrawal behavior, including whether funds are designed to take participants “to” or “through” retirement

20

Bank of America Corporation

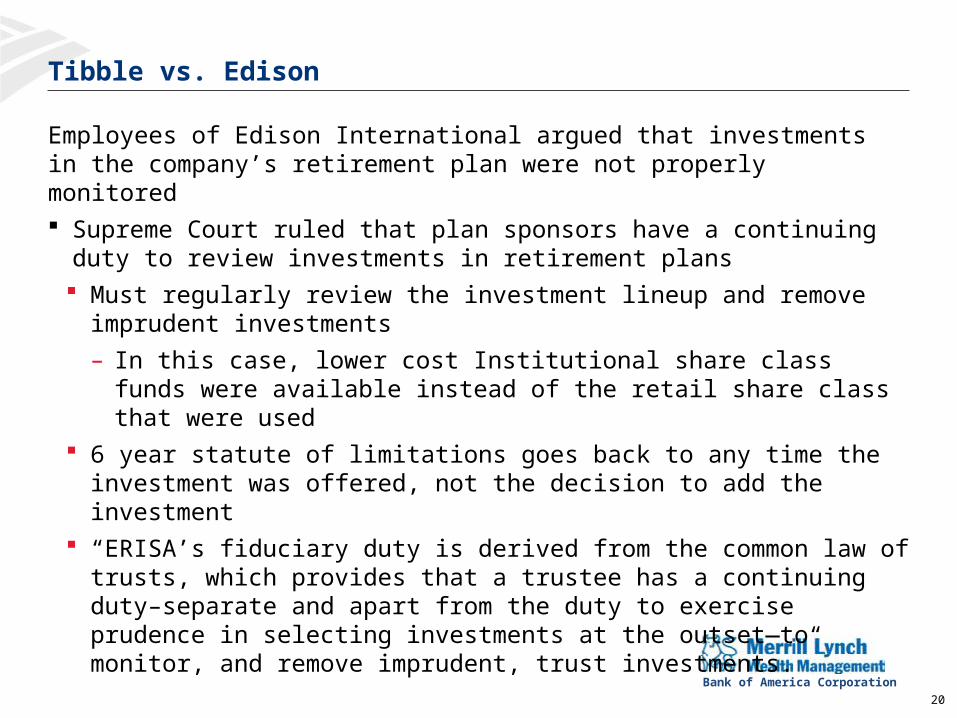

Tibble vs. Edison

Employees of Edison International argued that investments in the company’s retirement plan were not properly monitored Supreme Court ruled that plan sponsors have a continuing duty to review

investments in retirement plans Must regularly review the investment lineup and remove imprudent

investments

– In this case, lower cost Institutional share class funds were available instead of the retail share class that were used

6 year statute of limitations goes back to any time the investment was offered, not the decision to add the investment

“ERISA’s fiduciary duty is derived from the common law of trusts, which provides that a trustee has a continuing duty–separate and apart from the duty to exercise prudence in selecting investments at the outset—to monitor, and remove imprudent, trust investments.”

21

Bank of America Corporation

Active vs. Passive

Indexing (passive management) is an investment strategy that attempts to track a specific market index as closely as possible after accounting for all expenses incurred to implement the strategy. This objective differs substantially from that of active investment managers, whose objective is to outperform their targeted benchmark even after accounting for all expenses. When utilizing active funds, Fiduciaries take the risk of underperformance and

tracking error to respective benchmarks Actively managed mutual funds are more expensive Difficult to consistently outperform benchmarks to make up for cost differential Nearly impossible to consistently pick funds that will stay in the top quartile of

their peer groups

The case for index-fund investing. Vanguard. March, 2015.

22

Bank of America Corporation

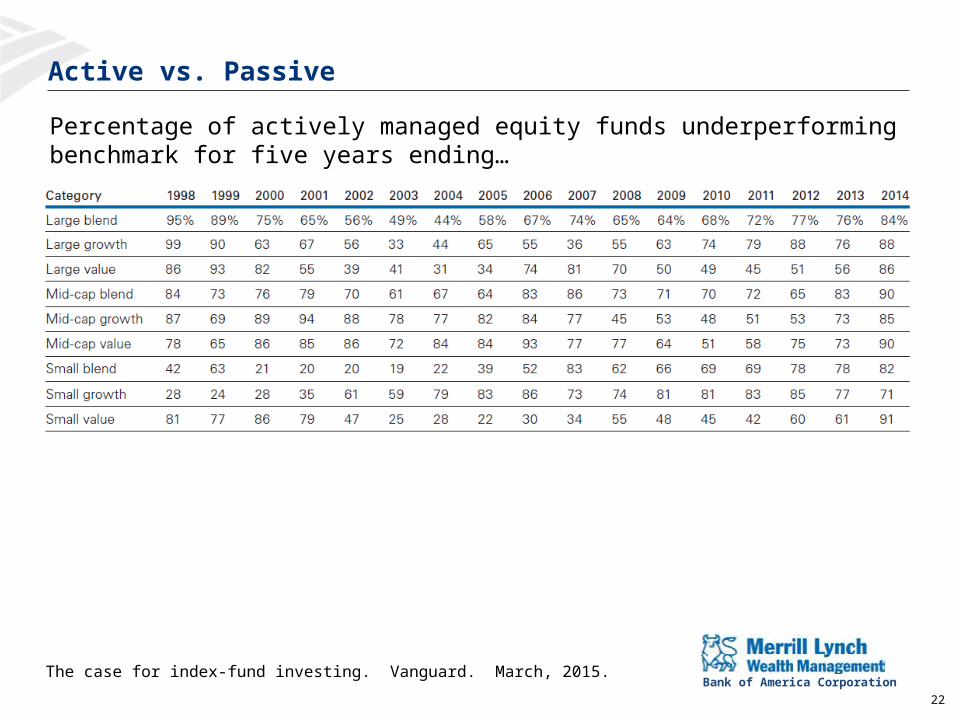

Active vs. Passive

Percentage of actively managed equity funds underperforming benchmark for five years ending…

The case for index-fund investing. Vanguard. March, 2015.

23

Bank of America Corporation

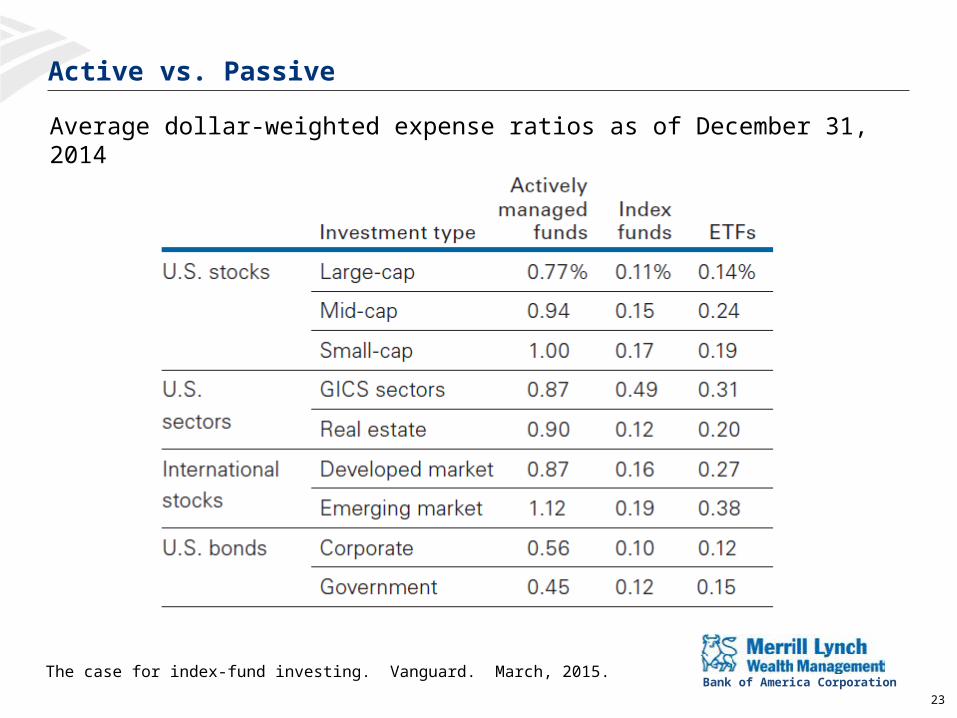

Active vs. Passive

Average dollar-weighted expense ratios as of December 31, 2014

The case for index-fund investing. Vanguard. March, 2015.

24

Bank of America Corporation

Questions?

Bank of America Corporation

Disclosures

Bank of America Merrill Lynch is a marketing name for the Institutional Retirement, Philanthropy & Investments businesses of Bank of America Corporation. Banking and fiduciary activities are performed globally by banking affiliates of Bank of America Corporation, including Bank of America, N.A., Member FDIC. Brokerage activities are performed globally by brokerage affiliates of Bank of America Corporation, including Merrill Lynch, Pierce, Fenner & Smith Incorporated (MLPFS). MLPFS is a registered broker-dealer, Member SIPC and wholly owned subsidiary of Bank of America Corporation.

Investment products:

Certain associates are registered representatives with Merrill Lynch, Pierce, Fenner & Smith Incorporated and may assist you with investment products and services.

Bank of America Merrill Lynch makes available investment products sponsored, managed, distributed or provided by companies that are affiliates of Bank of America Corporation or in which Bank of America Corporation has a substantial economic interest, including Columbia Management, BlackRock and Nuveen Investments.

© 2009 Bank of America Corporation. All rights reserved.

Are Not FDIC Insured Are Not Bank Guaranteed May Lose Value

The policy issues, status and views expressed are subject to change without notice at any time. This brief is provided for informational purposes only and should not be used or construed as advice or a recommendation of any product, service, security or sector.