ballarpur international graphic paper holdings b.v

TRANSCRIPT

CONFIDENTIAL

Ballarpur International Graphic Paper Holdings B.V.(A private company with limited liability organized under the laws of the Netherlands)

US$200,000,000 Subordinated Perpetual Capital SecuritiesThe US$200,000,000 subordinated perpetual capital securities (the “Securities”) will be unsecured subordinated obligations of BallarpurInternational Graphic Paper Holdings B.V. (the “Issuer”). The Securities confer a right to receive interest (“Interest”) at the applicablerate described below for the period from and including August 11, 2011 or from and including the most recent Interest Payment Date(defined below) to (but excluding) the next Interest Payment Date or any redemption date. Subject to the provisions of the Securitiesrelating to deferral of Interest (see “Description of the Perpetual Capital Securities — Deferral of Interest”), Interest accrues (i) from(and including) August 11, 2011 (the “Issue Date”) to (but excluding) August 11, 2016 (the “First Call Date”) at a rate of 9.75% perannum, payable semi-annually on February 11 and August 11 in each year commencing on February 11, 2012; (ii) from (and including)the First Call Date to (but excluding) August 11, 2021 (the “Second Call Date”), unless previously redeemed, at a rate equal to 8.57%per annum above the then current 5-year US Treasury rate, payable semi-annually on February 11 and August 11 in each year up to (andincluding) the Second Call Date; (iii) from (and including) the Second Call Date, unless previously redeemed, to (but excluding) thefollowing Reset Date (as defined herein) at a rate equal to 8.57% per annum above the then current 5-year US Treasury rate plus 100basis points, payable semi-annually on February 11 and August 11 in each year up to (and including) the Reset Date falling immediatelyafter the Second Call Date; and (iv) from (and including) each Reset Date falling after the Second Call Date, unless previouslyredeemed, to (but excluding) the immediately following Reset Date at a rate equal to 8.57% per annum above the then current 5-year USTreasury rate plus 100 basis points, payable semi-annually on February 11 and August 11 each year.The Issuer may, at its sole discretion, elect to defer (in whole or in part) payment of Interest which would otherwise have become dueand payable on an Interest Payment Date by giving notice (which notice shall be irrevocable) to the holders of the Securities and theTrustee not more than 10 nor less than five New York Business Days prior to a scheduled Interest Payment Date. Any Interest deferredpursuant to the terms of the Securities shall constitute “Arrears of Interest”. The Issuer may, at its sole discretion, elect to defer furtherany Arrears of Interest by complying with the foregoing notice requirement applicable to any deferral of any accrued Interest. The Issueris not subject to any limit as to the number of times Interest and Arrears of Interest can or shall be deferred pursuant to the terms of theSecurities, except that the provisions described under “Description of the Perpetual Capital Securities — Restrictions in the case ofDeferral” shall be complied with until all outstanding Arrears of Interest have been paid in full. Each amount of arrears of Interest shallaccrue Interest as if it constituted the principal of the Securities at the applicable rate described above and the amount of such accruedInterest with respect to arrears of Interest shall be due and payable on the following Interest Payment Date, unless further deferred inaccordance with the terms of the Securities. See “Description of the Perpetual Capital Securities — Deferral of Interest” for details.The Securities are perpetual securities and have no fixed final redemption date. The Issuer may elect to redeem the Securities (in wholebut not in part) at par plus accrued Interest, Arrears of Interest and Additional Interest Amounts, if any, on the First Call Date, theSecond Call Date or on any Interest Payment Date thereafter (each such redemption an “Optional Redemption”). In addition, upon theoccurrence of an Accounting Event, Capital Event or Tax Deduction Event (each as defined herein), the Issuer may elect to redeem theSecurities at (1) their Early Redemption Amount (as defined herein), if such redemption occurs before (but excluding) August 11, 2021or (2) if such redemption occurs after (or on) August 11, 2021, at their principal amount, in each case together with Interest accrued,including any Arrears of Interest and any Additional Interest Amounts, up to (but excluding) the redemption date. Upon the occurrenceof a Withholding Tax Event or Squeeze Out Event (as defined herein), the Issuer may elect to redeem the Securities at par plus accruedInterest and Arrears of Interest, if any. Upon the occurrence of a Change of Control (as defined herein), the Issuer may elect to redeemthe Securities at their principal amount plus accrued Interest and Arrears of Interest, if any, or suffer a 5% step-up to the prevailingInterest rate of the Securities. For a more detailed description of the Securities, see “Description of the Perpetual Capital Securities”beginning on page 179.

Offering Price for the Securities: 100% plus accrued Interest, if any, from August 11, 2011

Investing in the Securities involves certain risks. You should read “Risk Factors” beginning on page 31 before investing in theSecurities.

Approval in-principle has been received for the listing and quotation of the Securities on the Official List of the Singapore ExchangeSecurities Trading Limited (the “SGX-ST”). Approval to list the Securities will be granted when the Securities have been admitted to theOfficial List of the SGX-ST. The SGX-ST assumes no responsibility for the correctness of any statements made, opinions expressed orreports contained in this Offering Circular. Admission for the listing and quotation of the Securities on the SGX-ST is not to be taken asan indication of the merits of the Securities or of the Issuer or its respective subsidiaries or associated companies (if any). The Securitieswill be traded on the SGX-ST in a minimum board lot size of US$200,000 for so long as the Securities are listed on the SGX-ST.

The Securities have not been, and will not be, registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”),or any U.S. state securities laws. Accordingly, the Securities being offered and sold only (i) in the United States to qualifiedinstitutional buyers (“QIBs”) (as defined in Rule 144A under the Securities Act (“Rule 144A”)) in reliance on the exemption fromthe registration requirements of the Securities Act provided by Rule 144A and (ii) to persons outside the United States incompliance with Regulation S. Prospective purchasers are hereby notified that the sellers of the Securities may be relying on theexemption from the provisions of Section 5 of the Securities Act provided by Rule 144A. For a description of certain restrictionson resales and transfers, see “Transfer Restrictions”, beginning on page 222.

Joint Lead Managers and Joint Bookrunners

HSBC The Royal Bank of ScotlandThe date of this Offering Circular is August 4, 2011.

NOTICE TO INVESTORS

The Issuer, as well as The Hongkong and Shanghai Banking Corporation Limited (“HSBC”) and TheRoyal Bank of Scotland plc (“RBS”) (together, the “Initial Purchasers”), reserve the right to withdrawthe offering of the Securities at any time or to reject any offer to purchase, in whole or in part, for anyreason, or to sell less than all of the Securities offered hereby.

This Offering Circular is personal to the prospective investor to whom it has been delivered by theInitial Purchasers and does not constitute an offer to any other person or to the public in general tosubscribe for or otherwise acquire the Securities. Distribution of this Offering Circular to any personother than the prospective investor and those persons, if any, retained to advise that prospectiveinvestor with respect thereto is unauthorized, and any disclosure of its contents without the Issuer’sprior written consent is prohibited. The prospective investor, by accepting delivery of this OfferingCircular, agrees to the foregoing and agrees not to make any photocopies of this Offering Circular.

This Offering Circular is intended solely for the purpose of soliciting indications of interest in theSecurities from qualified investors and does not purport to summarize all of the terms, conditions,covenants and other provisions contained in any transaction documents described herein. Theinformation provided is not all-inclusive. The market information in this Offering Circular has beenobtained by the Issuer from publicly available sources deemed by it to be reliable. Notwithstanding anyinvestigation that the Initial Purchasers may have conducted with respect to the information containedherein, the Initial Purchasers do not accept any liability in relation to the information contained in thisOffering Circular or its distribution or with regard to any other information supplied by or on theIssuer’s behalf.

The Issuer confirms that, after having made all reasonable inquiries, this Offering Circular contains allinformation with regard to the Issuer and the Securities which is material to the offering and sale of theSecurities, that the information contained in this Offering Circular is true and accurate in all materialrespects and is not misleading in any material respect and that there are no omissions of any other factsfrom this Offering Circular which, by their absence herefrom, make this Offering Circular misleadingin any material respect. The Issuer accepts responsibility accordingly.

Prospective investors in the Securities should rely only on the information contained in this OfferingCircular. None of the Issuer or the Initial Purchasers have authorized the provision of informationdifferent from that contained in this Offering Circular. The information contained in this OfferingCircular is accurate in all material respects only as of the date of this Offering Circular, regardless ofthe time of delivery of this Offering Circular or of any sale of the Securities. Neither the delivery ofthis Offering Circular nor any sale made hereunder shall under any circumstances imply that there hasbeen no change in the Issuer’s affairs and those of each of its respective subsidiaries or that theinformation set forth herein is correct in all material respects as of any date subsequent to the datehereof.

Prospective investors hereby acknowledge that (i) they have not relied on the Initial Purchasers or anyperson affiliated with the Initial Purchasers in connection with any investigation of the accuracy ofsuch information or their investment decision, and (ii) no person has been authorized to give anyinformation or to make any representation concerning the Issuer or the Securities (other than ascontained herein and information given by the Issuer’s duly authorized officers and employees, as

— i —

applicable, in connection with investors’ examination of the Issuer, and the terms of this offering) and,if given or made, any such other information or representation should not be relied upon as havingbeen authorized by the Issuer or the Initial Purchasers.

The Securities have not been approved or recommended by the United States Securities andExchange Commission (“SEC”) or any other federal or state regulatory authority in the UnitedStates. Furthermore, the foregoing authorities have not passed upon or endorsed the merits of theoffering or confirmed the accuracy or determined the adequacy of this Offering Circular. Anyrepresentation to the contrary is a criminal offense in the United States.

The Hongkong and Shanghai Banking Corporation Limited (the “Stabilizing Manager”) or any of itsaffiliates (or any person acting on behalf of any of them) may, to the extent permitted by applicablelaws and regulations, over-allot or effect transactions with a view to supporting the market price of theSecurities at a level higher than that which might otherwise prevail for a limited period after the issuedate. In doing so, the Stabilizing Manager acts as principal and not as agent of the Issuer and any lossresulting from over-allotment or stabilization will be borne, and any profit arising from them shall beretained, by the Initial Purchasers, as applicable, in equal proportion. However, there is no assurancethat the Stabilizing Manager or any of its affiliates (or persons acting on behalf of any StabilizingManager) will undertake any stabilizing action. Any stabilizing action may begin on or after the dateon which adequate public disclosure of the terms of the offer of the Securities is made and, if begun,may be ended at any time, but will end no later than 30 days after the issue date of the Securities and60 days after the date of the allotment of the Securities, whichever is the earlier. The Issuer authorizeseach Initial Purchaser to make such public disclosure of information relating to stabilization of theSecurities as is required by applicable law, regulation and guidance.

None of the Initial Purchasers, the Issuer or their respective affiliates or representatives ismaking any representation to any offeree or purchaser of the Securities offered hereby regardingthe legality of any investment by such offeree or purchaser under applicable legal investment orsimilar laws. The Initial Purchasers have not separately verified the information contained in thisOffering Circular. None of the Initial Purchasers makes any representation, warranty orundertaking, express or implied, or accepts any responsibility, with respect to the accuracy orcompleteness of any of the information in this Offering Circular. To the fullest extent permittedby law, none of the Initial Purchasers accepts any responsibility for the contents of this OfferingCircular or for any other statement made or purported to be made by the Initial Purchasers or ontheir behalf in connection with the Issuer or the issue and offering of the Securities. Each of theInitial Purchasers accordingly disclaims all and any liability whether arising in tort or contractor otherwise which it might otherwise have in respect of this Offering Circular or any suchstatement.

Each prospective investor contemplating purchasing any Securities should make its ownindependent investigation of the financial condition and affairs, and its own appraisal of thecreditworthiness of the Issuer, and the terms of the Securities being offered, including the meritsand risks involved and its purchase of the Securities should be based upon such investigationswith its own tax, legal and business advisers as it deems necessary. See section, “Risk Factors” for

— ii —

a discussion of certain factors to be considered. Any prospective investor in the Securities shouldbe able to bear the economic risk of an investment in the Securities for an indefinite period oftime.

This Offering Circular does not constitute an offer to sell, or a solicitation of an offer to buy, anySecurities offered hereby by any person in any jurisdiction in which it is unlawful for such person tomake an offer or solicitation in such jurisdiction.

The distribution of this Offering Circular and the offer and sale of the Securities may, in certainjurisdictions, be restricted by law. Neither the Issuer nor the Initial Purchasers represent that thisOffering Circular may be lawfully distributed, or that any Securities may be lawfully offered, incompliance with any applicable registration or other requirements in any such jurisdiction, or pursuantto an exemption available thereunder, or assume any responsibility for facilitating any suchdistribution or offering. In particular, no action has been taken by any of the Issuer or the InitialPurchasers which would permit a public offering of any Securities or distribution of this OfferingCircular in any jurisdiction where action for that purpose is required. Accordingly, no Securities maybe offered or sold, directly or indirectly, and neither this Offering Circular nor any advertisement orother offering material may be distributed or published in any jurisdiction, except under circumstancesthat will result in compliance with any applicable laws and regulations.

Each purchaser of the Securities must comply with all applicable laws and regulations in force in eachjurisdiction in which it purchases, offers or sells the Securities or possesses or distributes this OfferingCircular, and must obtain any consent, approval or permission required for the purchase, offer or saleby it of the Securities under the laws and regulations in force in any jurisdiction to which it is subjector in which it makes purchases, offers or sales. Persons into whose possession this Offering Circular orany Securities may come must inform themselves about, and observe, any such restrictions on thedistribution of this Offering Circular and the offering and sale of Securities. In particular, there arerestrictions on the offer and sale of the Securities, and the circulation of documents relating thereto, incertain jurisdictions including the United States and the European Economic Area and to personsconnected therewith. See “Plan of Distribution”.

U.S. INFORMATION

This Offering Circular is being submitted on a confidential basis in the United States to a limitednumber of QIBs for informational use solely in connection with the consideration of the purchase ofthe Securities. Its use for any other purpose in the United States is not authorized. It may not be copiedor reproduced in whole or in part nor may it be distributed or any of its contents disclosed to anyoneother than the prospective investors to whom it is originally submitted.

For this offering, the Issuer and the Initial Purchasers are relying upon exemptions from registrationunder the Securities Act for offers and sales of securities which do not involve a public offering,including Rule 144A under the Securities Act. Prospective investors are hereby notified that sellersof the Securities may be relying on the exemption from the provision of Section 5 of the Securities

— iii —

Act provided by Rule 144A. The Securities are subject to restrictions on transferability and resale.Purchasers of the Securities may not transfer or resell the Securities except as permitted under theSecurities Act and applicable state securities laws. See “Transfer Restrictions”.

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR ALICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIRE REVISEDSTATUTES WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT A SECURITYIS EFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OF NEWHAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OF STATE OF NEWHAMPSHIRE THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE, COMPLETE ANDNOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT AN EXEMPTIONOR EXCEPTION IS AVAILABLE FOR A SECURITY OR A TRANSACTION MEANS THATTHE SECRETARY OF STATE HAS PASSED IN ANY WAY UPON THE MERITS ORQUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON,SECURITY, OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE,TO ANY PROSPECTIVE PURCHASER, CUSTOMER, OR CLIENT ANY REPRESENTATIONINCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

NOTICE TO PROSPECTIVE INVESTORS IN INDIA

Each of the Initial Purchasers acknowledges that (a) this Offering Circular has not been and will not beregistered, produced or published as an offer document (whether a prospectus in respect of a publicoffer or information memorandum or other offering material in respect of any private placement underthe Companies Act, 1956 or any other applicable Indian laws) with the Registrar of Companies or theSecurities and Exchange Board of India or any other statutory or regulatory body of like nature inIndia, (b) the Securities will not be offered or sold, and have not been offered or sold to any person inIndia by means of any document, other than to persons permitted to acquire the Securities under Indianlaw, whether as a principal or agent, and (c) this Offering Circular or any other offering document ormaterial relating to the Securities will not be circulated or distributed and have not been circulated ordistributed, directly or indirectly, to any person or the public or any member of the public in India orotherwise generally distributed or circulated in India. The Securities have not been offered or sold andwill not be offered or sold in India in circumstances which would constitute an offer of securities(whether to the public or by way of placement) within the meaning of the Companies Act, 1956, or anyother applicable Indian law for the time being in force.

AVAILABLE INFORMATION

To permit compliance with Rule 144A in connection with any resales or other transfers of Securities thatare “restricted securities” within the meaning of the Securities Act, the Issuer has undertaken to furnish,upon the request of a holder of such Securities or any beneficial interest therein, to such holder or to aprospective purchaser designated by him, the information required to be delivered under Rule 144A(d)(4)under the Securities Act if, at the time of the request, any of the Securities remain outstanding as“restricted securities” within the meaning of Rule 144(a)(3) of the Securities Act and the Issuer is neithera reporting company under Section 13 or 15(d) of the U.S. Securities Exchange Act of 1934, as amended,(the “Exchange Act”) nor exempt from reporting pursuant to Rule 12g3-2(b) thereunder.

— iv —

ENFORCEMENT OF CIVIL LIABILITIES

The Issuer is incorporated as a private company with limited liability under the laws of theNetherlands. The agreements entered into with respect to the issue of the Securities are governed bythe laws of the State of New York, except for certain provisions of the Indenture, which are governedby Dutch law. As the United States and The Netherlands currently do not have a treaty providing forthe reciprocal recognition and enforcement of judgments (other than arbitral awards) in civil andcommercial matters, a final judgment for the payment of money rendered by any federal or state courtin the United States which is enforceable in the United States, whether or not predicated solely uponU.S. federal securities laws would not be recognized and enforced by the Dutch courts. However, if aperson has obtained a final and conclusive judgment for the payment of money rendered by a court inthe State of New York which is enforceable in the State of New York and files his claim with thecompetent Dutch court, the Dutch court will generally give binding effect to the judgment of the courtin the State of New York insofar as it finds that the jurisdiction of the court in the State of New Yorkhas been based on grounds which are internationally acceptable and that proper legal procedures havebeen observed and unless the foreign judgment contravenes Dutch public policy.

Subject to the foregoing and service of process in accordance with applicable treaties, investors may beable to enforce in The Netherlands, judgments in civil and commercial matters obtained fromU.S. federal or state courts. However, no assurance can be given that such judgments will beenforceable. In addition, it is doubtful whether a Dutch court would accept jurisdiction and imposecivil liability in an original action commenced in The Netherlands and predicated solely upon U.S.federal securities laws.

BILT and BGPPL are incorporated with limited liability under the laws of India, many of the Group’sDirectors are residents of India and the assets of the Group are substantially located in India. Most ofthe senior management employed by the Group are residents of India. As a result, it may not bepossible for investors to effect service of process upon the Issuer or the Group or such persons outsideIndia, or to enforce judgments obtained against such parties outside India predicated upon the laws ofjurisdictions other than India, including the civil liability provisions of the United States federal orstate securities laws.

In India, recognition and enforcement of foreign judgments is provided for under Section 13 andSection 44A of the Civil Code on a statutory basis. Section 13 of the Civil Code provides that foreignjudgments shall be conclusive regarding any matter directly adjudicated upon, except:

Š where the judgment has not been pronounced by a court of competent jurisdiction;

Š where the judgment has not been given on the merits of the case;

Š where it appears on the face of the proceedings that the judgment is founded on an incorrectview of international law or a refusal to recognize the law of India in cases to which such lawis applicable;

Š where the proceedings in which the judgment was obtained were opposed to natural justice;

— v —

Š where the judgment has been obtained by fraud; or

Š where the judgment sustains a claim founded on a breach of any law then in force in India.

Under the Civil Code, a court in India shall, upon the production of any document purporting to be acertified copy of a foreign judgment, presume that the judgment was pronounced by a court ofcompetent jurisdiction, unless the contrary appears on record.

India is not a signatory to the “Convention on the recognition and enforcement of foreign judgments incivil and commercial matters” or any other international treaty in relation to the recognition orenforcement of foreign judgments. Section 44A of the Civil Code provides that where a foreignjudgment has been rendered by a superior court, within the meaning of such section, in any country orterritory outside India which the Government has by notification declared to be a reciprocatingterritory, it may be enforced in India by proceedings in execution as if the judgment had been renderedby the relevant court in India. However, Section 44A of the Civil Code is applicable only to monetarydecrees not being of the same nature as amounts payable in respect of taxes, other charges of a likenature or of a fine or other penalties and does not include arbitration awards. Furthermore, theexecution of the foreign decree under Section 44A of the Civil Code is also subject to the exceptionsunder Section 13 of the Civil Code, as discussed above.

The United Kingdom, Singapore and Hong Kong have been declared by the Government of India to bereciprocating territories for the purposes of Section 44A of the Civil Code, but the United States hasnot been so declared. A judgment of a court of a country which is not a reciprocating territory may beenforced only by a new proceeding suit instituted in a court of India and not by proceedings inexecution. Such a suit has to be filed in India within three years from the date of the judgment in thesame manner as any other suit filed to enforce a civil liability in India. It is unlikely that a court inIndia would award damages on the same basis as a foreign court if an action was brought in India.Furthermore, it is unlikely that an Indian court would enforce foreign judgments if that court were ofthe view that the amount of damages awarded was excessive or inconsistent with Indian public policy.A party seeking to enforce a foreign judgment in India is required to obtain approval from the ReserveBank of India (the “RBI”) to repatriate outside India any amount recovered pursuant to the executionof such a judgment and such amount may be subject to income tax in accordance with applicable laws.In addition, any judgment in a foreign currency would be converted into Indian Rupees on the date ofthe judgment and not on the date of payment.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Financial Data

All historical financial information in this Offering Circular is that of the Issuer, its consolidatedsubsidiaries (including the Issuer) and subsidiary undertakings (together, the “Group”). In this OfferingCircular, unless otherwise specified, all financial information is of the Group.

— vi —

The audited consolidated financial information of the Issuer, as at and for the fiscal years endedJune 30, 2008, 2009 and 2010 (the “Historical Consolidated Financial Information”) has been preparedin accordance with International Financial Reporting Standards as adopted by the European Union(“IFRS-EU”).

The Historical Consolidated Financial Information has been prepared for the proposed offering of theSecurities by the Issuer. This financial information is different from the historical statutory financialstatements of the Issuer because it does not include certain disclosures relating to the Dutch civil code,including a director’s report and other information and because it applies predecessor basis ofaccounting for the year ended June 30, 2008.

The unaudited consolidated interim financial information of the Issuer for the nine months endedMarch 31, 2010 and 2011 (the “Unaudited Consolidated Interim Financial Information”), includedelsewhere in this Offering Circular, has been prepared in accordance with IAS 34 Interim FinancialReporting, as adopted by the European Union (“IAS 34”).

Independent Third Party Report

This Offering Circular includes information from a report dated February 10, 2011 prepared by Pöyry,an independent third party. The report is included as an annexure to this Offering Circular. Pöyry hasprovided written consent to this report being included in the Offering Circular.

Non-GAAP Financial Measures

As used in this Offering Circular, a non-GAAP financial measure is one that purports to measurehistorical or future financial performance, financial position or cash flows, but excludes or includesamounts that would not be so adjusted in the most comparable IFRS-EU measures. From time to time,reference is made in this Offering Circular to such “non-GAAP financial measures”, primarilyEBITDA, which comprises operating profit adjusted for depreciation charges. Information regardingEBITDA or similar measures is sometimes used by investors to evaluate the efficiency of a company’soperations and its ability to employ its earnings toward repayment of debt, capital expenditures andworking capital requirements. There are no generally accepted principles governing the calculation ofEBITDA or similar measures and the criteria upon which EBITDA or similar measures are based canvary from company to company. EBITDA, by itself, does not provide a sufficient basis to compare theGroup’s performance with that of other companies and should not be considered in isolation or as asubstitute for operating profit or any other measure as an indicator of operating performance, or as analternative to cash generated from operating activities as a measure of liquidity.

— vii —

The reconciliation of Group results from operating activities to EBITDA is as follows:

For the year ended June 30Nine months ended

March 31

2008 2009 2010 2010 2011

(unaudited)US$

millionUS$

millionUS$

millionUS$

millionUS$

million

Operating profit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69.06 51.50 95.33 66.06 65.04Add back depreciation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32.07 31.74 39.38 28.68 33.58

EBITDA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 101.13 83.23 134.71 94.74 98.62

The Issuer uses EBITDA in the management reporting of its segments and in assessing the Group’sgrowth and operational efficiencies. The Issuer’s management believes that EBITDA and othernon-GAAP financial measures provide investors with additional information about the Group’sperformance, as well as ability to incur and service debt and make capital expenditures, and aremeasures commonly used by investors. The non-GAAP financial measures described herein are not asubstitute for IFRS-EU measures of earnings and may not be comparable to similarly titled measuresreported by other companies due to differences in the way these measures are calculated.

Rounding

Certain data in this document, including financial, statistical, and operating information has beenrounded. As a result of the rounding, the totals of data presented in this document may vary slightlyfrom the actual arithmetic totals of such data. Percentages in tables have been rounded and accordinglymay not add up to 100%.

Currency presentation

Unless otherwise indicated, all references to “US dollars” or “US$” are to the lawful currency of theUnited States. All references to the “rupee” or “INR” are to the lawful currency of India. All referencesto the “euro”, “EUR” or “€” are to the currency introduced at the start of the third stage of Europeaneconomic and monetary union pursuant to the Treaty establishing the European Community, asamended. All references to “ringgits” or “MYR” are to the lawful currency of Malaysia.

— viii —

Exchange rate information

The average exchange rates of the Group’s main trading currencies, other than US dollars, are shownrelative to US dollars below. The average rates in the table below are daily weighted averages, but theyare not necessarily the rates used to translate the Group’s results due to the seasonality of its earnings.These exchange rates should not be construed as representations that the relevant currency could beconverted into US dollars at the rate indicated or at any other rate:

Average rate against US dollars on rupee euro ringgit

June 30, 2008 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43.0051 0.6336 3.2659June 30, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47.9450 0.7102 3.5216June 30, 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46.5425 0.8173 3.2519January 31, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45.9556 0.7323 3.0600February 28, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45.2400 0.7255 3.0520March 31, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44.6287 0.7055 3.0256April 30, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44.3450 0.6738 2.9697May 31, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45.0325 0.6970 3.0093June 30, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44.7197 0.6905 3.0218

Average rate against US dollars for the year ended rupee euro ringgit

June 30, 2008 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40.3653 0.6814 3.3158June 30, 2009 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47.6558 0.7310 3.5156June 30, 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46.6745 0.7215 3.3842

Average rate against US dollars for the nine months ended rupee euro ringgit

March 31, 2010 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47.0109 0.6997 3.4313March 31, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45.5388 0.7472 3.1058

Average rate against US dollars for the month ended rupee euro ringgit

January 31, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45.4095 0.7480 3.0610February 28, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45.4390 0.7320 3.0445March 31, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44.9783 0.7133 3.0355April 30, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44.3649 0.6910 3.0110May 31, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44.9289 0.6982 3.0148June 30, 2011 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44.8441 0.6944 3.0287

Source: Bloomberg

As at June 30, 2011 the exchange rate of the rupee per US dollar was 44.7197 and the euro per USdollar was 0.6905 and the Ringgit per US dollar was 3.0218.

Weight presentation

Unless otherwise indicated, all references in this document to “Mt” or “tonnes” are to metric tonnes(approximately 2,204.6 pounds or 1.1 short tons). All references to “tpa” are to metric tonnesper annum.

— ix —

Definitions and Glossary

Certain terms used in this document, including all capitalized terms and certain technical and otherterms, are defined and explained in the section entitled “Definitions and Glossary”.

Information regarding forward-looking statements

Certain statements in this Offering Circular are not historical facts and are “forward-lookingstatements” within the meaning of Section 27A of the Securities Act and Section 21E of the ExchangeAct. This Offering Circular may contain words such as “believe”, “could”, “may”, “will”, “target”,“estimate”, “project”, “predict”, “forecast”, “guideline”, “should”, “plan”, “expect” and “anticipate”and similar expressions that are intended to identify forward-looking statements, but are not theexclusive means of identifying these statements. All statements regarding the Issuer’s or the Group’sexpected financial condition and results of operations and business plans and prospects are forward-looking statements. In particular, “Summary”, “Management’s Discussion and Analysis of FinancialCondition and Results of Operations” and “Business” contain forward-looking statements, includingrelating to market trends, capital expenditure and other factors affecting the Group that are nothistorical facts.

Forward-looking statements are subject to certain risks and uncertainties, including, but not limited to:

Š changes in global economic, political and social conditions;

Š changes in economic and political conditions and increases in regulatory burdens in India andother countries in which the Group operates, transacts business or has interests;

Š accidents and natural disasters in India, Malaysia or in other countries in which the Groupoperates or globally, including specifically India’s neighboring countries;

Š increased competition in the Indian paper industry;

Š effects of a decrease in the level of tariffs imposed on paper imported into India;

Š effects of fluctuations in interest rates and changes in credit ratings upon the cost of borrowing;

Š changes in customer preferences;

Š effects of insufficient insurance;

Š high compliance or clean-up costs under environmental and health and safety laws andregulations;

Š increased labor costs and/or labor disruptions.

Š the Group’s business and operating strategies and its ability to implement such strategies;

— x —

Š the Group’s ability to successfully implement its growth and expansion plans, technologicalchanges, exposure to market risks and foreign exchange risks that have an impact on itsbusiness activities;

Š the Group’s ability to ensure continuity of senior management and ability to attract and retainkey personnel;

Š the availability and terms of external financing;

Š cost overruns or delays in commencement of production from the Group’s new projects;

Š changes in the Group’s relationship with the governments of the countries in which the Groupoperates;

Š changes in exchange controls, import controls or import duties, levies or taxes in the countriesin which the Group operates;

Š changes in laws, regulations, taxation or accounting standards or practices that affect theGroup;

Š changes in prices or demand for the goods and services provided by the Group;

Š the risks of increased costs in technologies related to the Group’s operations and theuncertainty of such technologies producing expected results;

Š changes in the value of the Indian Rupee or Malaysian Ringgit against the US dollar and othermajor global currencies and other currency changes;

Š the ability of third parties to perform in accordance with contractual terms and specifications;

Š acquisitions and divestitures which the Group may undertake; and

Š other factors, including those discussed in “Risk Factors”.

Forward-looking statements involve inherent risks and uncertainties. If one or more of these or otheruncertainties or risks materialize, actual results may vary materially from those estimated, anticipatedor projected. Specifically, but without limitation, capital costs could increase, projects could bedelayed, and anticipated improvements in capacity, performance or profit levels might not be fullyrealized. Although the Issuer believes that the expectations of its management as reflected by suchforward-looking statements are reasonable based on information currently available to it, no assurancescan be given that such expectations will prove to have been correct. Accordingly, you are cautioned notto place undue reliance on the forward-looking statements, which speak only as of the date they aremade. The Issuer does not undertake any obligation to update or revise any of them, whether as a resultof new information, future developments or otherwise.

— xi —

CONTENTS

Section Page

NOTICE TO INVESTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . i

U.S. INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iii

NOTICE TO NEW HAMPSHIRE RESIDENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iv

NOTICE TO PROSPECTIVE INVESTORS IN INDIA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iv

AVAILABLE INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . iv

ENFORCEMENT OF CIVIL LIABILITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . v

PRESENTATION OF FINANCIAL AND OTHER INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vii

DEFINITIONS AND GLOSSARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

SUMMARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

SUMMARY CONSOLIDATED FINANCIAL DATA OF THE GROUP . . . . . . . . . . . . . . . . . . . . . . . . . . 20

THE OFFER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23

RISK FACTORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

USE OF PROCEEDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 57

CAPITALIZATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

SELECTED CONSOLIDATED FINANCIAL DATA OF THE GROUP . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTSOF OPERATIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

BUSINESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 94

INDUSTRY AND MARKET OVERVIEW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

RELATIONSHIP WITH THE BALLARPUR GROUP AND THE AVANTHA GROUP . . . . . . . . . . . . . . 162

MANAGEMENT AND CORPORATE GOVERNANCE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 165

DESCRIPTION OF INDEBTEDNESS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 170

DESCRIPTION OF THE PERPETUAL CAPITAL SECURITIES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

TAXATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 205

PLAN OF DISTRIBUTION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 215

TRANSFER RESTRICTIONS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 222

LEGAL MATTERS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 225

INDEPENDENT AUDITORS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 225

GENERAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 226

INDEX TO CONSOLIDATED FINANCIAL INFORMATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . F-1

PÖYRY REPORT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . A-1

— 1 —

DEFINITIONS AND GLOSSARY

Definitions

The following definitions apply throughout this document unless the context requires otherwise:

“AIA” . . . . . . . . . . . . . . . . . . . . . . . . . . . Avantha International Asset BV

“Avantha” . . . . . . . . . . . . . . . . . . . . . . . . Avantha Holdings Limited

“Avantha Group” . . . . . . . . . . . . . . . . . . . Avantha Holdings Limited and its subsidiaries and subsidiaryundertakings, excluding for these purposes the Ballarpur Group

“Avantha Power” . . . . . . . . . . . . . . . . . . . Avantha Power & Infrastructure Limited and its subsidiaries andsubsidiary undertakings, a part of the Avantha Group

“Ballarpur Group” . . . . . . . . . . . . . . . . . . BILT and its subsidiaries and subsidiary undertakings, excluding forthese purposes the Group

“Ballarpur unit” . . . . . . . . . . . . . . . . . . . . the manufacturing unit located in Ballarpur in District Chandrapur,Maharashtra in Central India

“BGPPL” . . . . . . . . . . . . . . . . . . . . . . . . . BILT Graphic Paper Products Limited

“Bhigwan unit” . . . . . . . . . . . . . . . . . . . . the manufacturing unit located in Bhadalwadi, Maharashtra inWestern India

“BIGPH” . . . . . . . . . . . . . . . . . . . . . . . . . Ballarpur International Graphic Paper Holdings B.V., the Issuer

“BIH” . . . . . . . . . . . . . . . . . . . . . . . . . . . Ballarpur International Holdings B.V., the direct parent company ofthe Issuer

“BILT” . . . . . . . . . . . . . . . . . . . . . . . . . . Ballarpur Industries Limited, the indirect majority shareholder of theIssuer

“BIPH” . . . . . . . . . . . . . . . . . . . . . . . . . . Ballarpur International Paper Holdings B.V., formerly a direct 100%owned subsidiary of BPH. On June 30, 2011, BIPH was merged intoBPH and ceased to exist.

“Board” . . . . . . . . . . . . . . . . . . . . . . . . . . the board of directors of the Issuer

“Bombay Stock Exchange” . . . . . . . . . . . Bombay Stock Exchange Limited

— 2 —

“BPH” . . . . . . . . . . . . . . . . . . . . . . . . . . . Ballarpur Paper Holdings B.V., a directly owned 100% subsidiary ofthe Issuer

“BTTL” . . . . . . . . . . . . . . . . . . . . . . . . . . BILT Tree Tech Limited

“CAGR” . . . . . . . . . . . . . . . . . . . . . . . . . compound annual growth rate

“Civil Code” . . . . . . . . . . . . . . . . . . . . . . The Code of Civil Procedure of India, 1908 as amended

“Code” . . . . . . . . . . . . . . . . . . . . . . . . . . . The U.S. Internal Revenue Code of 1986, as amended

“CCDs” . . . . . . . . . . . . . . . . . . . . . . . . . . compulsory convertible debentures

“EU” . . . . . . . . . . . . . . . . . . . . . . . . . . . . the European Union

“FSC-COC” . . . . . . . . . . . . . . . . . . . . . . . Forest Stewardship Council — Chain of Custody

“Group” . . . . . . . . . . . . . . . . . . . . . . . . . . The Issuer and its consolidated subsidiaries and subsidiaryundertakings

“IAS 34” . . . . . . . . . . . . . . . . . . . . . . . . . International Accounting Standard 34 Interim Financial Reporting asadopted by the European Union

“IFRS-EU” . . . . . . . . . . . . . . . . . . . . . . . International Financial Reporting Standards, as adopted by theEuropean Union

“India” . . . . . . . . . . . . . . . . . . . . . . . . . . . Republic of India

“Indian Stock Exchanges” . . . . . . . . . . . . Bombay Stock Exchange and National Stock Exchange

“Issuer” . . . . . . . . . . . . . . . . . . . . . . . . . . Ballarpur International Graphic Paper Holdings B.V.

“ITC” . . . . . . . . . . . . . . . . . . . . . . . . . . . . Integrated Timber Complex

“J.P. Morgan Mauritius” . . . . . . . . . . . . . J.P. Morgan Mauritius Holdings VII Ltd

“Joint Bookrunners” . . . . . . . . . . . . . . . . HSBC and RBS

“Joint Lead Managers” . . . . . . . . . . . . . . HSBC and RBS

“Kamalapuram unit” . . . . . . . . . . . . . . . . the manufacturing unit located in District Warangal, Andhra Pradeshin Southern India

— 3 —

“Lathe Investment” . . . . . . . . . . . . . . . . . Lathe Investment Pte Ltd

“Managing Directors” . . . . . . . . . . . . . . . the managing directors of the Issuer identified in “Management andCorporate Governance” of this document

“National Stock Exchange” . . . . . . . . . . . National Stock Exchange of India Limited

“Offer” . . . . . . . . . . . . . . . . . . . . . . . . . . . the offer of Securities by the Issuer as described in “The Offer”

“Offering Price” . . . . . . . . . . . . . . . . . . . the price at which each Security is to be issued or sold under the Offer

“Official List” . . . . . . . . . . . . . . . . . . . . . the Official List of the Singapore Stock Exchange

“PwC” . . . . . . . . . . . . . . . . . . . . . . . . . . . PricewaterhouseCoopers Accountants N.V.

“qualified institutional buyers” or“QIBs” . . . . . . . . . . . . . . . . . . . . . . . . . has the meaning given by Rule 144A

“Regulation S” . . . . . . . . . . . . . . . . . . . . . Regulation S under the US Securities Act

“Rule 144A” . . . . . . . . . . . . . . . . . . . . . . Rule 144A under the US Securities Act

“Securities” . . . . . . . . . . . . . . . . . . . . . . . the Issuer’s US$200,000,000 Subordinated Perpetual CapitalSecurities

“Securities Holders” . . . . . . . . . . . . . . . . the holders of Securities

“Senior Managers” . . . . . . . . . . . . . . . . . the Senior Managers identified in “Management and CorporateGovernance” of this document

“SFI” . . . . . . . . . . . . . . . . . . . . . . . . . . . . Sabah Forest Industries Sdn. Bhd., an indirect 97.8% ownedsubsidiary of the Issuer

“SFI unit” . . . . . . . . . . . . . . . . . . . . . . . . the SFI manufacturing unit located in the Malaysian State of Sabah

“Singapore Stock Exchange” . . . . . . . . . Singapore Exchange Securities Trading Limited

“SMI” . . . . . . . . . . . . . . . . . . . . . . . . . . . SMI NewQuest (India) Private Limited

“UK” . . . . . . . . . . . . . . . . . . . . . . . . . . . . the United Kingdom of Great Britain, Northern Ireland, Guernsey,Jersey and the Isle of Man

“Underwriting Agreement” . . . . . . . . . . . the underwriting agreement expected to be entered into between theIssuer, the Directors and the Joint Lead Managers.

— 4 —

“United States” or “US” . . . . . . . . . . . . . the United States of America, its territories and possessions, any Stateof the United States of America, and the District of Columbia

“units” . . . . . . . . . . . . . . . . . . . . . . . . . . . the Group’s manufacturing facilities consisting of the Ballarpur unit,the Bhigwan unit, the Kamalapuram unit and the SFI unit

“US Exchange Act” . . . . . . . . . . . . . . . . . United States Securities Exchange Act of 1934, as amended

“US Securities Act” . . . . . . . . . . . . . . . . . United States Securities Act of 1933, as amended

Glossary

BCB . . . . . . . . . . . . . . . . . . . . . . . . . . . . . black centered board

BCTMP . . . . . . . . . . . . . . . . . . . . . . . . . . bleached chemi-thermomechanical pulp

coated paper board . . . . . . . . . . . . . . . . . thick paper-based material with a coating to improve whiteness,smoothness or gloss

Creamwove . . . . . . . . . . . . . . . . . . . . . . . uncoated wood-free paper that has been made on a woven wire mesh

Depot . . . . . . . . . . . . . . . . . . . . . . . . . . . . a transportation hub for the distribution of goods

GDP . . . . . . . . . . . . . . . . . . . . . . . . . . . . . gross domestic product, the total value of goods and servicesproduced by a country

Gsm . . . . . . . . . . . . . . . . . . . . . . . . . . . . . grams per square meter

Hi-bright . . . . . . . . . . . . . . . . . . . . . . . . . paper with an ISO brightness above 88%

low bright . . . . . . . . . . . . . . . . . . . . . . . . paper with an ISO brightness below 88%

m3/tonne . . . . . . . . . . . . . . . . . . . . . . . . . cubic meters per tonne

Mt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . metric tonnes (approximately 2,204.6 pounds or 1.1 short tons)

MW . . . . . . . . . . . . . . . . . . . . . . . . . . . . . megawatts

non surface sized . . . . . . . . . . . . . . . . . . . paper that has not been treated with starch or other sizing material atthe size process of the paper machine

paper grade pulp . . . . . . . . . . . . . . . . . . . pulp of quality suitable for the production of paper

PBS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . premium business stationery

— 5 —

pulp . . . . . . . . . . . . . . . . . . . . . . . . . . . . . the principal raw material used for the manufacture of paper. Thesuitability of specific types of pulp for the required end use dependsboth on the type of wood used to make the pulp and on the woodpulping process. Hardwood trees are used to produce hardwood pulpwhich has short fibers and is generally better suited to manufacturingcoated packaging boards, coated and uncoated wood-free paper andtissues

rayon grade pulp . . . . . . . . . . . . . . . . . . . pulp chemically treated in order to regenerate pure cellulose fiber

surface sized . . . . . . . . . . . . . . . . . . . . . . paper that has been treated with starch or other sizing material at thesize press of the paper machine

tonnes . . . . . . . . . . . . . . . . . . . . . . . . . . . metric tonnes (approximately 2,204.6 pounds or 1.1 short tons)

tpa . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . metric tonnes per annum

virgin grade packaging board . . . . . . . . . paperboard for folding cartons and other packaging produced fromnon-recycled sources

wood-free paper . . . . . . . . . . . . . . . . . . . . paper that is based on chemical pulp rather than mechanical pulp.Chemical pulp is normally made from pulpwood, which is timbergrown with the principal purpose of making wood pulp for paperproduction. Pulpwood is not considered wood as most of the lignin isremoved and separated from the cellulose fibers in the processing

— 6 —

SUMMARY

This overview highlights certain information contained in this Offering Circular. This overview doesnot contain all the information you should consider before investing in the Securities. You should readthis entire Offering Circular carefully, including the sections entitled “Information RegardingForward-Looking Statements”, “Risk Factors”, “Management’s Discussion and Analysis of FinancialCondition and Results of Operations” and “Business” included elsewhere in this Offering Circular andthe financial information and the Issuer’s US$200,000,000 Subordinated Perpetual Capital Securities(the “Securities”) thereto set forth herein. To understand the terms of the Securities, you shouldcarefully read the section of this Offering Circular entitled “Description of the Perpetual CapitalSecurities”.

Information on the Group

The Group is India’s largest producer of writing and printing paper and Malaysia’s largest producer ofuncoated wood-free paper products, as measured by volume of paper produced. The Group has a66 year history in India, and SFI, which was acquired by the Group in March 2007, has a 29 yearhistory in Malaysia. The Group is a part of the Avantha Group, which is a diversified business groupwith a portfolio spanning paper and pulp, power equipment and services, energy and infrastructure,food processing, chemicals and information technology and services. The Group is also the leadingproducer and seller of market rayon grade pulp in India. The Group’s paper, hardwood pulp and rayongrade pulp manufacturing operations span across four production units: the Ballarpur unit, the Bhigwanunit and the Kamalapuram unit in India and the SFI unit in Malaysia.

As of the year ended December 31, 2009, the Group had a 24% market share in the Hi-bright uncoatedwood-free paper segment in India (as compared to a market share of 13% for the Issuer’s parentcompany, BILT, and a market share of 12% for Tamil Nadu Newsprint and Papers Limited (“TNPL”), acompetitor of the Group) and a 51% market share in the blade coated wood-free paper segment in India(as compared to a market share of 11% for its next closest Indian competitor, JK Paper), as reported byPöyry.

The Group’s business model is based on vertical integration where it seeks to achieve control over thecost of key inputs and operating flexibility to maximize value across the entire value chain. The Groupmaintains its own forest plantations, power facilities, facilities for the production of chemicals requiredfor the paper and hardwood pulp production and extensive hardwood pulp production capacity, all ofwhich provides a high degree of vertical integration.

The Group’s operations have grown significantly since 2008. Since June 30, 2008, the Group’s annualpaper production capacity has increased by 88%, from 403,710 tpa to 758,710 tpa as at March 31,2011. The Group is also currently expanding its hardwood pulp production capacity at both the SFIunit and the Ballarpur unit. The SFI expansion is intended to create a total net increase in hardwoodpulp capacity of 120,000 tpa and the Ballarpur expansion is expected to create a total net increase of170,000 tpa (with new capacity at the Ballarpur unit totalling 300,000 tpa, replacing existing capacityof 130,000 which is being retired). The Issuer expects its total hardwood pulp production capacity tobe 540,000 tpa by the end of 2012 (excluding capacity of 98,550 tpa at the Kamalapuram unit which is

— 7 —

intended to produce rayon grade pulp). The increased hardwood pulp production will reduce theGroup’s cost of hardwood pulp for paper production, secure a source for the Group’s key raw materialinput and reduce exposure to the volatility in market prices for hardwood pulp.

The Group’s production capacity with respect to paper, hardwood pulp and rayon grade pulp as atMarch 31, 2011 is shown below:

At March 31, 2011

Unit (tpa) PaperHardwood

Pulp

RayonGradePulp

Ballarpur . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 299,500 130,000 —Bhigwan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 315,000 — —Kamalapuram . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . — — 98,550SFI . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 144,210 120,000

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 758,710 250,000 98,550

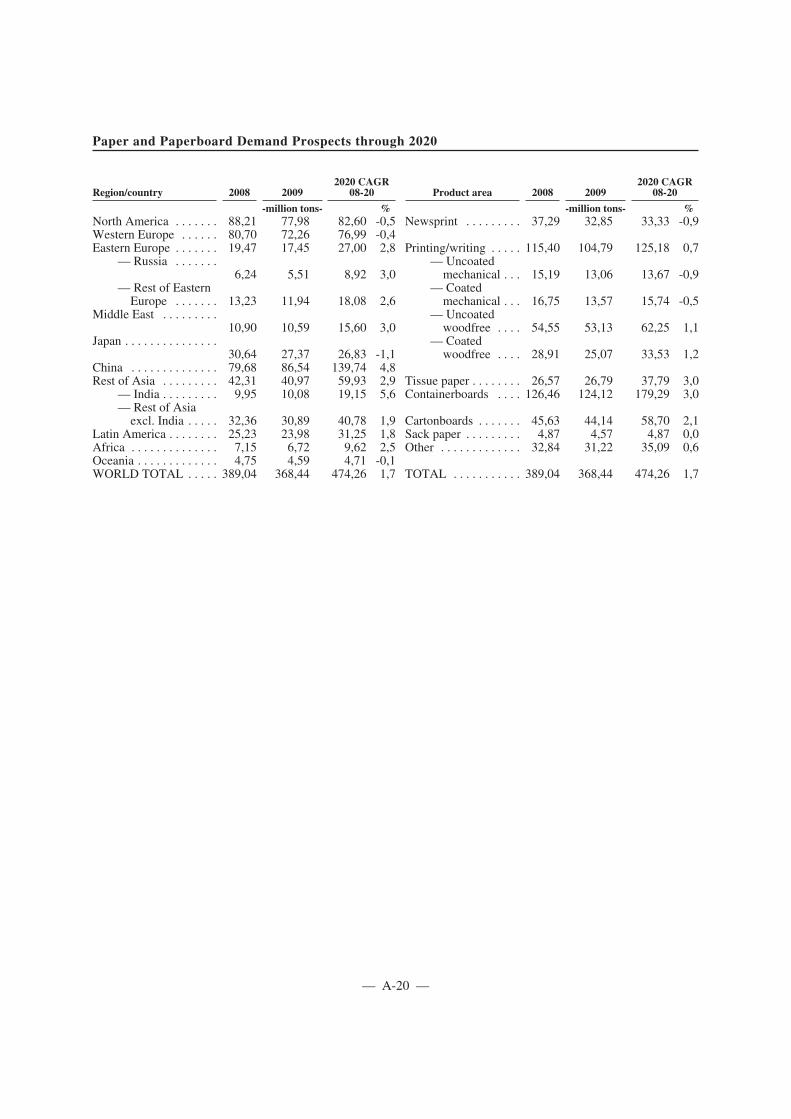

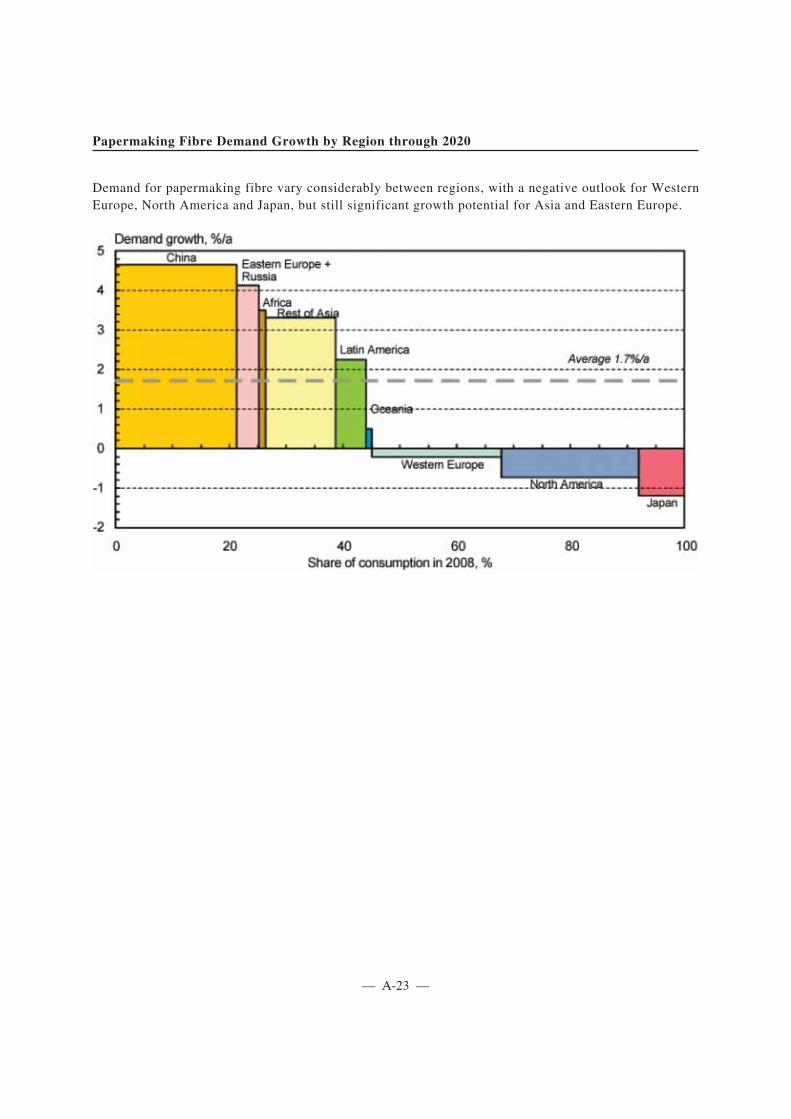

Due to the low level of per capita paper consumption in India, the Issuer believes that there issignificant room for growth in demand and, according to Pöyry, the average per capita consumption ofpaper in India is expected to grow from 8.4 kg in 2009 to 13.9 kg by 2020. Pöyry estimates that thesize of the Indian paper market will rise from 10.1 million tonnes in 2009 to 19.2 million tonnes by2020. Consequently, Pöyry anticipates that the compound annual growth rate of paper demand in Indiafrom 2009 to 2020 will be 6.0%, which is higher than China (4.5%), the rest of Asia (excluding Chinaand India) (2.6%) and significantly higher than Western Europe (0.6%), North America (0.5%) andJapan (-0.2%). Indian demand for coated and uncoated wood free paper products is expected to grow9.3% and 6.4%, respectively, per year between 2009 and 2020. Furthermore, with respect to theGroup’s primary products, blade coated wood free paper and Hi bright uncoated wood free paper,demand is expected to grow 10.2% and 8.1%, respectively, per year between 2009 and 2020 (Source:Pöyry).

Competitive strengths

The Issuer believes its competitive strengths include the following:

Operations in high growth markets

The primary drivers of demand for wood-free paper are GDP growth and increased per capita income.These factors, in turn, provide a foundation for other drivers of demand for wood-free paper, includingincreased spending in the marketing industry, disposable income, government spending on educationand literacy rates. India’s GDP is projected to grow at an annual growth rate of approximately 8% until2020 and is projected to be the 3rd largest global economy by 2050 moving up from its current positionof 5th. India’s share of global GDP is expected to rise to 13% by 2050, from the current share of 2%.This growth is expected to have significant positive effects on increased per capita income, disposableincome and customer purchasing power in India. A shift in discretionary spending in India is projected

— 8 —

to rise from 52% of total private spending to 70% between 2005 and 2025 and a substantial increase inIndia’s middle class are key drivers of increases in per capita disposable income. India’s middle classis expected to increase by approximately 60 million households by 2020, with an increase in the urbanpopulation from 29% in 2005 to 37% in 2025 while India’s population of a working age is projected tobe the largest by 2050. Further, government spending on education was estimated to total US$10.7billion from 2002 through the end of 2011 of which US$6 billion is on paper related products. TheGroup believes that this increased expenditure, along with other social and demographic trends, willimpact literacy rates significantly and the demand for paper products such as books and notebooksduring the next decade.

As a result, per capita consumption of paper and paperboard (including coated and uncoated wood-freepaper) from 2009 to 2020 is expected to increase by approximately 66% from approximately 8.4 kg peryear to approximately 13.9 kg per year. Pöyry estimates that total consumption will increase from10.1 million tonnes in 2009 to 19.2 million tonnes in 2020, representing a compound annual growthrate of 6.0%, as compared to 4.5% in China, 0.5% in North America. The projection for demand inIndia is based primarily on the projection of sustained economic growth at approximately 8%, as wellas population growth of 1.3% per year through 2020.

According to Pöyry, as the Indian middle class and paper consumption grows, there is likely to be ashift to higher quality, such as coated paper. Consumption of coated wood-free paper as a percentageof writing and printing wood-free paper globally was 32% in 2009, similar consumption in India was13%. In addition, according to Pöyry, consumption of blade coated wood-free paper (generallyconsidered higher quality coated paper) has grown by 14% from 2009 through 2010, whileconsumption of knife coated and other coated wood-free paper has declined as a percentage of totalconsumption during this period. As such, demand for coated and uncoated wood-free paper in India isexpected to grow by 9.3% and 6.4%, respectively per year from 2009 through 2020, while the growthrates for the Group’s primary products, blade coated wood-free paper and Hi-bright uncoated wood-free paper are expected to reach 10.2% and 8.1% during this period, respectively (source: Pöyry).

Market leadership

For over 50 years, the Group (together with its predecessors) has been a leading writing and printingpaper producer in India. The Group holds a dominant position in the blade coated wood-free papersegment in India with a 51% market share for the year ended December 31, 2009, as compared to amarket share of 11% for the year ended December 31, 2009 for its closest domestic competitor (source:Pöyry). The Group holds a leading share of the high quality Hi-bright uncoated wood-free papermarket with a share of 24%, as compared to a market share of 13% held by the Issuer’s parentcompany, BILT, and a market share of 12% for TNPL, a competitor of the Group, for the year endedDecember 31, 2009. The Issuer believes that the Group’s ability to service customers with bothuncoated and coated wood-free products results in a distinct advantage as the Group is able to bundleits products, resulting in pricing flexibility and benefits for its customers with respect to product rangeand product size.

— 9 —

In addition, the Group is the largest producer of market rayon grade pulp in India, with total productionof 85,345 tonnes and total capacity of 98,550 tonnes for the year ended June 30, 2010 at theKamalapuram unit.

The Group is also the largest domestic producer of surface sized and non-surfaced size uncoated wood-free paper in Malaysia. It held a market share of 22% in the surface sized uncoated wood-free papermarket for 2009 and a 73% market share in the non-surfaced sized uncoated wood-free paper segment.The majority of the remaining demand in Malaysia is met by imports from Indonesia, Thailand andChina.

In addition, as a result of the Group’s high quality products, market recognition of the BILT brand andits market leading customer service, BILT (including the Group) has been recognized as a“Superbrand” by the Superbrand Organization each year since 2004. This market leadership and brandawareness provides the opportunity for the Group to charge a premium for its products as compared toits principal competitors.

Vertical integration

The Group’s business model is based on vertical integration where it seeks to achieve control over thecost of key inputs and flexibility to maximize value across the entire value chain. The Group maintainsits own forest plantations, power facilities (two of which are wholly owned and two of which areowned by Avantha Power & Infrastructure Limited (“Avantha Power”) from which the Group procuresa part of its requirements for power), facilities for the production of chemicals (through arrangementswith related parties such as Imerys Newquest (India) Private Limited (“Imerys”) and SMI Newquest(India) Private Limited (“SMI”) and third parties such as Specialty Minerals Malaysia Sdn. Bhd.(“SMM”) required for the paper and hardwood pulp production and extensive hardwood pulpproduction capacity, all of which provide a high degree of vertical integration.

The Group remains focused on improving each component of its vertical integration business model inorder to take advantage of the anticipated market growth in the coated and uncoated wood-free papermarkets and has almost doubled its paper production capacity from 403,710 tpa at June 30, 2008 to758,710 tpa at March 31, 2011.

The Group expects that the paper production capacity at the Ballarpur unit, Bhigwan unit and SFI unitis expected to be increased, with a total additional paper production capacity of 685,000 tpa by the yearended June 30, 2014. Of this additional 685,000 tpa, the Group expects 75,000 tpa to be the result ofsmall improvement investments at the Ballarpur unit and Bhigwan unit (with capacity expansion of40,000 tpa and 35,000 tpa, respectively) to be completed by September 2012. The Group expects60,000 tpa to be the result of small improvement investments at the SFI unit to be completed by June2014. The Group expects the remaining 550,000 tpa to be the result of the introduction of a newuncoated paper machine at the Ballarpur unit and a new paper board machine at the Bhigwan unit withproduction commencing in July 2014, which will broaden the Group’s product portfolio to includecoated paper board. The new machine at the Ballarpur unit is expected to have a capacity of

— 10 —

250,000 tpa and the machine at the Bhigwan unit is expected to have capacity of 300,000 tpa. Theadditional 685,000 tpa in capacity will result in total paper production capacity across all units beingincreased to approximately 1,443,710 tpa by June 30, 2014.

In addition to the forest and plantation at the SFI unit during the nine months ended March 31, 2011,the Group procured a portion of its total hardwood fiber requirements from farmers under the farmforestry programs supported by BILT Tree Tech Limited (“BTTL”) and located near the Group’sBallarpur and Kamalapuram units in India. BTTL is an affiliated company of the Group but is not amember of the Group. Although the farmers may sell the wood to other purchasers, the quantitypurchased by the Group and the proximity to the Group’s units results in a consistent source ofhardwood fiber.

In 2004, BILT and the regional government in Maharashtra entered into a contract whereby theGovernment of Maharashtra agreed to provide bamboo from the government forests to the Ballarpurunit for the production of pulp, paper, paper board and other pulp products. The Ballarpur unit wassubsequently transferred to BGPPL, and the Group now benefits from this contract between BILT andthe government in Maharashtra. The Ballarpur unit currently extracts bamboo and BGPPL pays aroyalty and other dues in relation to this extraction. This contract runs until 2014. During the yearended June 30, 2010, the Group purchased 55% of its total hardwood fiber requirements from thirdparties. Increased harvesting at the SFI unit will help the Group maintain a significant level of woodintegration.

The Group meets most of the SFI unit’s wood requirement through its own plantations, and part of thewood requirements for the Ballarpur unit and Kamalapuram unit is purchased through the farm forestryprogram supported by BTTL. This reduces the Group’s exposure to hardwood fiber price volatility andtransportation costs. Additionally, the Group intends to increase planting and harvesting within theplantation at the SFI unit, which is intended to increase the wood supplied by the plantation to theGroup’s hardwood pulp production capacity, thereby increasing the Group’s vertical integration. TheGroup procured approximately 42% of its hardwood fiber requirements from its own sources during thenine months ended March 31, 2011 and intends to increase this to 52% by the year ending June 30,2013 through this planned increase in planting and harvesting.

In order to maximize the benefit of its access to hardwood fiber and the expansion of paper productioncapacity which has already been completed, the Group is focusing on expanding its hardwood pulpproduction and paper production capacity further. The Group believes that the ongoing expansion ofhardwood pulp production at both the SFI unit and the Ballarpur unit will reduce the Group’s exposureto volatile market prices for hardwood pulp and reduce the Group’s cost of hardwood pulp purchases asthe production cost of pulp is substantially lower than the prevailing market price for hardwood pulp.

With respect to the Ballarpur unit, net production capacity of pulp is intended to be expanded to300,000 tpa by March 2012. Of this capacity, 300,000 tpa will be new capacity provided by a newlyacquired hardwood pulpmill which is currently being installed using equipment acquired from anexisting pulpmill in Finland, while the existing facility with capacity of 130,000 tpa will be retired.This increased net capacity of 170,000 tpa, along with the additional capacity discussed below at the

— 11 —

SFI unit, is intended to satisfy the increased pulp requirements resulting from the increased paperproduction capacity expected at the Ballarpur unit and the Bhigwan unit (excluding the 300,000 tpapaper board machine to be installed at the Bhigwan unit the 250,000 tpa uncoated paper machine to beinstalled at the Ballarpur unit and the 60,000 tpa at the SFI unit).

The hardwood pulp production expansion project at the SFI unit is intended to increase hardwood pulpproduction by over 120,000 tpa by September 2011, with wood sourced from the Group’s own forestsand plantations in Malaysia. The Group has leasehold rights to approximately 288,138 hectares offorest and plantation land. The wood fiber available from these forest and plantation lands is expectedto be sufficient to meet the hardwood fiber requirements of the increased hardwood pulp productioncapacity at the SFI unit. This additional hardwood pulp production capacity is intended to be used forthe expanded paper capacities in India.

For the nine months ended March 31, 2011, the Group produced approximately 50% and 56% of itstotal pulp and hardwood pulp requirements, respectively, from its own units and intends to produce90% of its total pulp and 100% of its hardwood pulp by the year ending June 30, 2013.

With this additional hardwood pulp production capacity, the Issuer believes the Group will be fullyintegrated with respect to the hardwood pulp required to maximize its paper production capacity by theend of 2012-2013 (excluding the 300,000 tpa paper board machine to be installed at the Bhigwan unit,the 250,000 tpa uncoated paper machine at the Ballarpur unit and the 60,000 tpa at the SFI unit). TheGroup will continue to purchase its softwood pulp and bleached chemi-thermomechanical pulp(“BCTMP”) from the market. Hardwood pulp made up approximately 88% of the Group’s total pulprequirements during the nine months ended March 31, 2011.

Further, the Group’s units contain captive energy production with on-site facilities at each unit,including two that are owned by Avantha Power. Three of the facilities produce approximately 96% ofthe relevant unit’s energy requirements, while the Kamalapuram unit produces 83% of that unit’srequirements during the year ended June 30, 2010. Historically, Avantha Power has increased powergeneration capacity in parallel with growing paper/pulp operations and the Issuer believes that AvanthaPower will continue this approach for the foreseeable future. The Ballarpur unit’s chemical plantcomplex produces caustic soda (total capacity of 14,400 tpa), chlorine (total capacity of 12,775 tpa),chlorine dioxide (total capacity of 1,095 tpa) and sulphur dioxide (total capacity of 444 tpa), all ofwhich are vital chemicals for the paper process. The Ballarpur unit sells any excess caustic sodaproduced at the Plant on the market. The Group’s other units purchase all chemical requirements fromthe market.

The Group has previously furthered its vertical integration through acquisitions (such as through theacquisition of the Bhigwan unit, previously known as Sinar Mas Pulp and Paper (India) Ltd (“SinarMas India”), in May 2001, and the SFI unit in March 2007). In addition to its pursuit of organic growthas described above, the Group intends to focus future vertical integration upon the pursuit of bothorganic growth and further acquisitions. The Issuer believes that, in line with its previous successfulpaper and hardwood pulp production projects, the current projects will significantly increase theGroup’s ability to capitalize upon the expected growth in the Indian market along with the growing

— 12 —

demand for coated and uncoated wood-free paper products. Further, given the 88% expansion of theGroup’s paper production from July 2008 to March 2011 (from 403,710 tpa to 758,710 tpa) and theintegration of the SFI unit in 2007, the Group has extensive experience in expanding the verticalintegration across the entire value chain. The Issuer believes increased vertical integration willcontinue to improve the Group’s profitability.

Among the most extensive Indian and Malaysian distribution networks

The Indian paper market is characterized by customer fragmentation with respect to the number ofcustomers, average order size and geographic distribution. The Issuer believes that being able to fulfilla large number of client orders of specific size and paper quality is a key differentiator of the Group.The location of certain of the Group’s manufacturing facilities in proximity to major consumer markets(such as Mumbai), as well as to sources of raw materials (such as the plantations at the SFI unit and thehardwood fiber farms near certain Indian units) gives the Group a significant advantage in terms ofmanufacturing, sales and distribution logistics and access to its customers. With what the Issuerbelieves is the largest paper distribution network in India, including distributors which workexclusively for the Group, through which the Group distributed approximated 54% of its sales in theyear ended June 30, 2010, it maintains extensive sales, customer service and distribution coverageacross India. This network allows the Group to reach the approximately 15,000 customers in Indiaserved by the Group, with an order to delivery time of under 30 days.