balance of payments forecasting thorvaldur gylfason

Post on 19-Dec-2015

225 views

TRANSCRIPT

Balance of Balance of

Payments Payments

ForecastingForecasting

Thorvaldur Gylfason

Three partsThree parts1)1) Introduce financial Introduce financial

programming framework and programming framework and role of forecastingrole of forecasting

2)2) Apply framework and Apply framework and forecasting to a particular case forecasting to a particular case

3)3) Explore methods of forecasting Explore methods of forecasting individual components of the individual components of the balance of paymentsbalance of payments

OutlineOutline

Task at handTask at hand Develop financial program for Develop financial program for

19981998 Use information available up 1997Use information available up 1997

Two stepsTwo steps Prepare Prepare baseline scenariobaseline scenario

assumingassuming unchanged economic unchanged economic policypolicy

If baseline scenario is If baseline scenario is unsatisfactory, then design unsatisfactory, then design financial financial programprogram with better policies and with better policies and better resultsbetter results

Financial programming Financial programming frameworkframework1 The baseline scenario is

a financial program,

based on policies

already in place

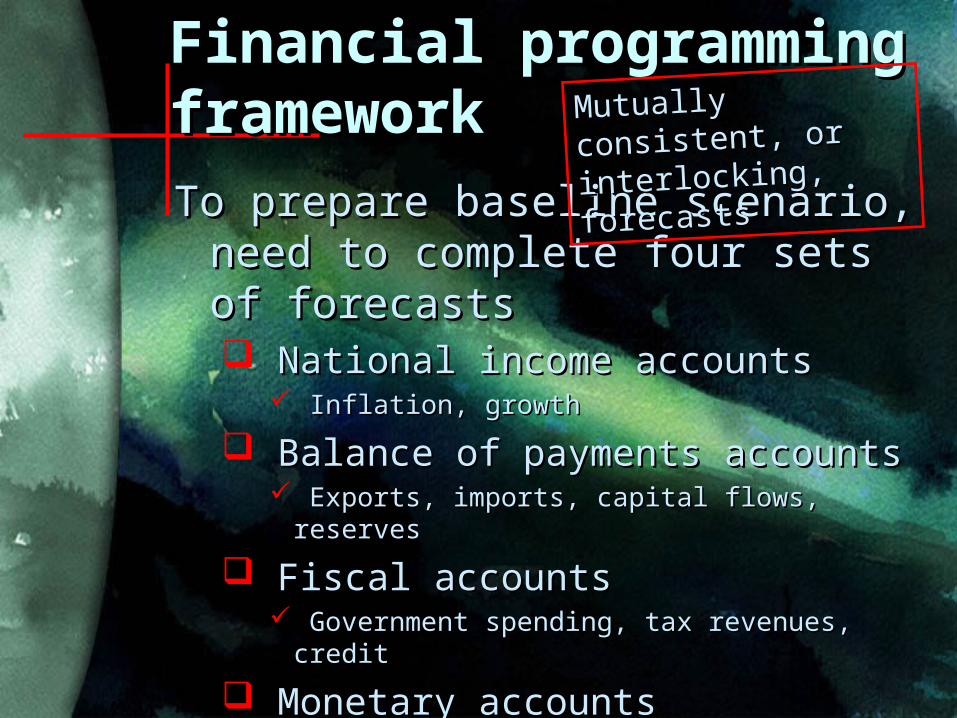

To prepare baseline scenario, need To prepare baseline scenario, need to complete four sets of forecaststo complete four sets of forecasts National income accountsNational income accounts

Inflation, growthInflation, growth

Balance of payments accountsBalance of payments accounts Exports, imports, capital flows, reservesExports, imports, capital flows, reserves

Fiscal accountsFiscal accounts Government spending, tax revenues, creditGovernment spending, tax revenues, credit

Monetary accountsMonetary accounts Money, credit, foreign reservesMoney, credit, foreign reserves

Financial programming Financial programming frameworkframework Mutually consistent, Mutually consistent,

or interlocking, or interlocking,

forecastsforecasts

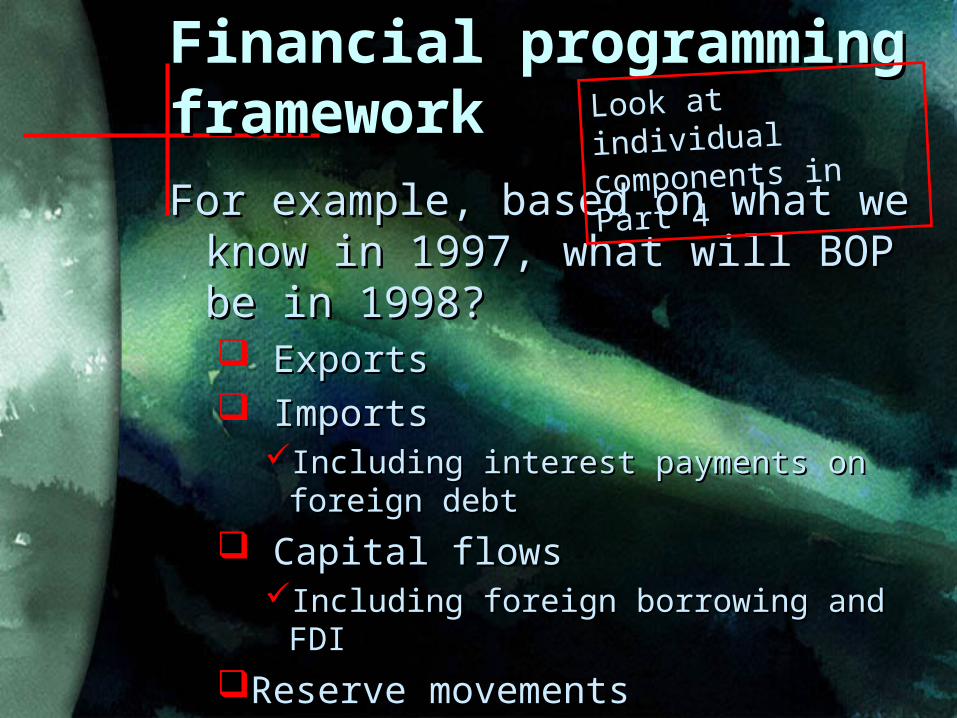

For example, based on what we For example, based on what we know in 1997, what will BOP be know in 1997, what will BOP be in 1998? in 1998? ExportsExports ImportsImports

Including interest payments on foreign Including interest payments on foreign debtdebt

Capital flowsCapital flowsIncluding foreign borrowing and FDI Including foreign borrowing and FDI

Reserve movementsReserve movementsIncluding target for reservesIncluding target for reserves

Financial programming Financial programming frameworkframework Look at individual

components in Part

4

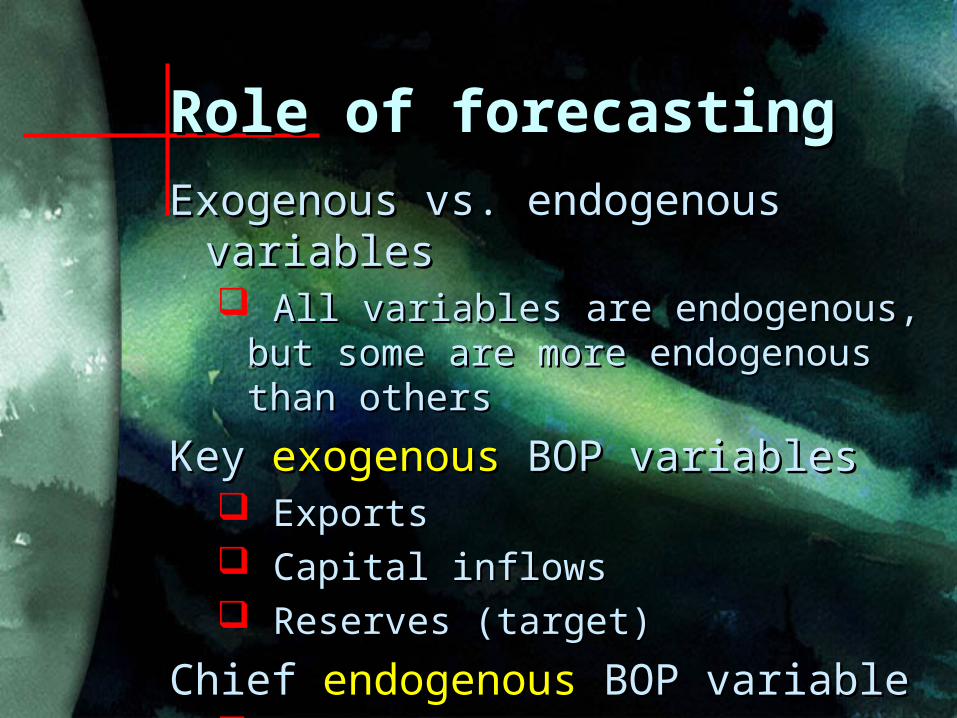

Exogenous vs. endogenous Exogenous vs. endogenous variablesvariables All variables are endogenous, but All variables are endogenous, but

some are more endogenous than some are more endogenous than othersothers

Key Key exogenousexogenous BOP variables BOP variables ExportsExports Capital inflowsCapital inflows Reserves (target)Reserves (target)

Chief Chief endogenousendogenous BOP variable BOP variable ImportsImports

Role of forecastingRole of forecasting

Forecasts of exogenous variables Forecasts of exogenous variables enable us to forecast enable us to forecast endogenous variablesendogenous variables

For example, once we have For example, once we have forecast X, F, and forecast X, F, and R, we can R, we can derive the forecast of Z as a derive the forecast of Z as a residual: Z = X + F – residual: Z = X + F – RR

Forecast of Z needs to be Forecast of Z needs to be consistent with forecasts of consistent with forecasts of inflation and growthinflation and growth

Role of forecastingRole of forecasting

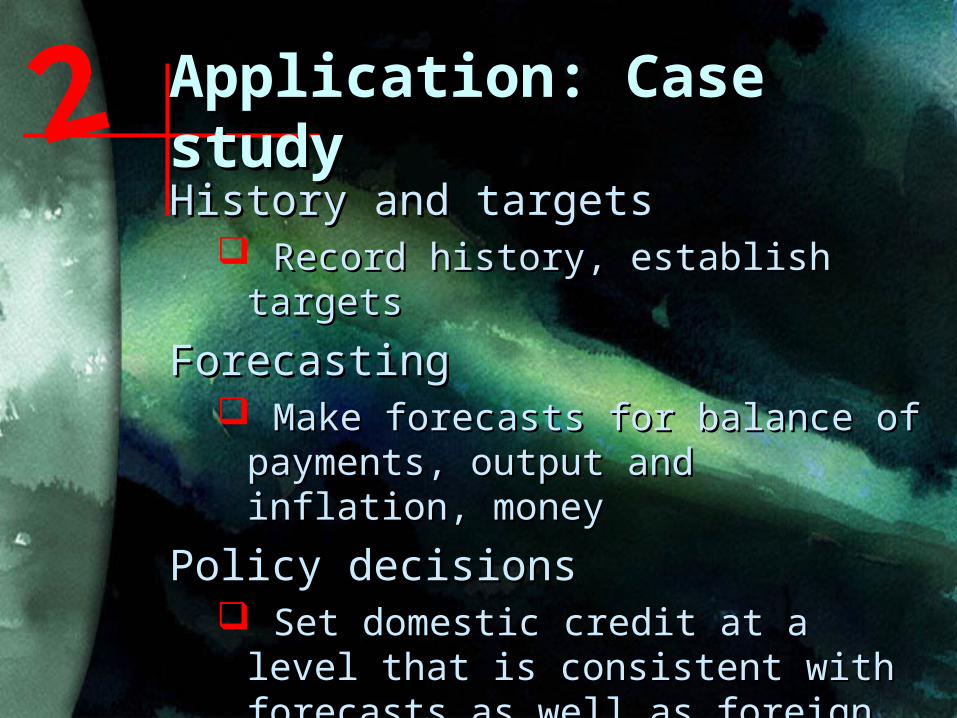

History and targetsHistory and targets Record history, establish targetsRecord history, establish targets

ForecastingForecasting Make forecasts for balance of Make forecasts for balance of

payments, output and inflation, payments, output and inflation, moneymoney

Policy decisionsPolicy decisions Set domestic credit at a level that Set domestic credit at a level that

is consistent with forecasts as well is consistent with forecasts as well as foreign reserve targetas foreign reserve target

Application: Case Application: Case studystudy2

1)1)Make forecasts, set reserve Make forecasts, set reserve target Rtarget R**

– E.g., reserves at 3 months of importsE.g., reserves at 3 months of imports

2)2) Compute permissible imports from Compute permissible imports from BOPBOP– More imports will jeopardize reserve More imports will jeopardize reserve

targettarget

3)3) Infer permissible increase in nominal Infer permissible increase in nominal income from import equationincome from import equation

4)4) Infer monetary expansion consistent Infer monetary expansion consistent with increase in nominal incomewith increase in nominal income

5)5) Derive domestic credit as a residualDerive domestic credit as a residual

D = M – RD = M – R**

Financial programming Financial programming step by stepstep by stepDo this in the right order

Known at beginning of program Known at beginning of program period:period:MM-1-1 = 800, D = 800, D-1-1 = 650, R = 650, R-1-1 = 150 = 150

Recall: Recall: M = D + RM = D + R

XX-1-1 = 700, Z = 700, Z-1-1 = 800, F = 800, F-1-1 = 150 = 150

Recall: Recall: R = X – Z + FR = X – Z + FSo,So,RR-1-1 = 700 – 800 + 150 = 50 = 700 – 800 + 150 = 50Current account deficit, overall surplusCurrent account deficit, overall surplus

RR-1-1/Z/Z-1-1 = 150/800 = 0.1875 = 150/800 = 0.1875Equivalent to 2.25 months of importsEquivalent to 2.25 months of importsWeak reserve positionWeak reserve position

HistoryHistory2.25 months = 9 2.25 months = 9

weeksweeks

X grows by 10%, so X = 770X grows by 10%, so X = 770

F increases by 20%, so F = 180F increases by 20%, so F = 180

Suppose RSuppose R** is set at 220, up from is set at 220, up from 150150

Level of imports is consistent with Level of imports is consistent with RR** is isZ = X + F + RZ = X + F + R-1-1 – R – R**

= 770 + 180 + 150 – 220 = 880= 770 + 180 + 150 – 220 = 880

Reserve target is equivalent to 3 Reserve target is equivalent to 3 months of importsmonths of importsRR**/Z = 220/880 = 0.25/Z = 220/880 = 0.25

Forecast for balance Forecast for balance of paymentsof payments

BOP BOP fore-fore-castcastss

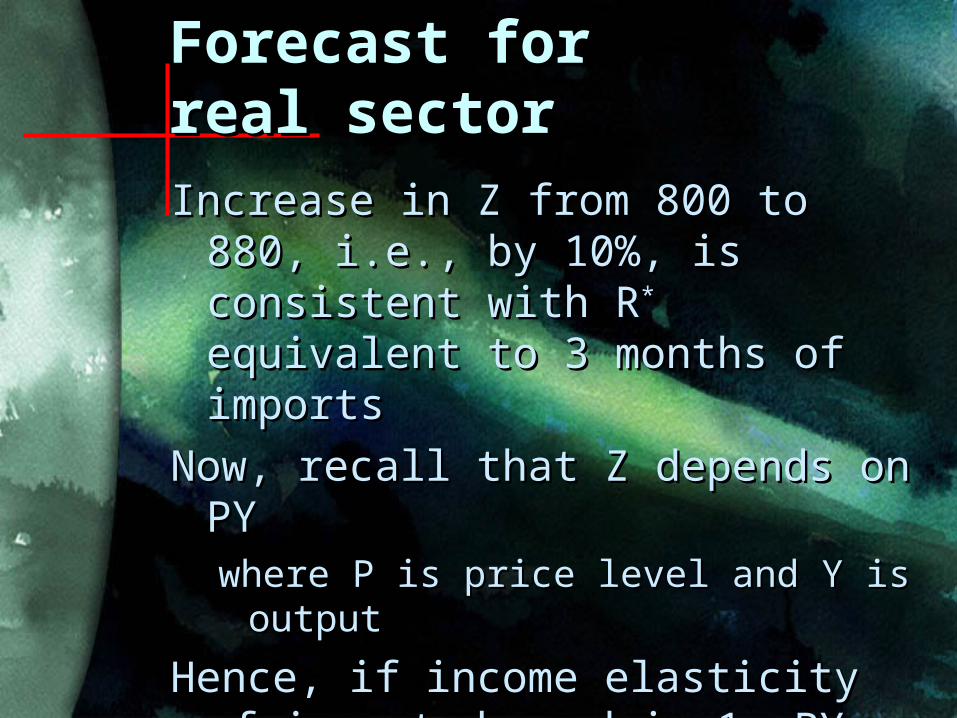

Increase in Z from 800 to 880, i.e., Increase in Z from 800 to 880, i.e., by 10%, is consistent with Rby 10%, is consistent with R** equivalent to 3 months of equivalent to 3 months of importsimports

Now, recall that Z depends on PY Now, recall that Z depends on PY where P is price level and Y is outputwhere P is price level and Y is output

Hence, if income elasticity of Hence, if income elasticity of import demand is 1, PY can import demand is 1, PY can increase by 10% increase by 10% E.g., 3% growth and 7% inflationE.g., 3% growth and 7% inflation

Depends on aggregate supply scheduleDepends on aggregate supply schedule

Forecast for Forecast for real sectorreal sector

If PY can increase by 10%, then, if If PY can increase by 10%, then, if income elasticity of money income elasticity of money demand is 1, M can also increase demand is 1, M can also increase by 10% by 10%

Recall quantity theory of moneyRecall quantity theory of moneyMV = PYMV = PY

Constant velocity means that Constant velocity means that

%%M = %M = %PY = %PY = %P + %P + %YY

Hence, M can expand from 800 to Hence, M can expand from 800 to 880880

Forecast for Forecast for moneymoney

˜

Recall M = D + M = D +

RR

Having set reserve target at RHaving set reserve target at R** = = 220 and forecast M at 880, we 220 and forecast M at 880, we can now compute level of credit can now compute level of credit that is consistent with our that is consistent with our reserve targetreserve target

So, D = 880 – 220 = 660, up from So, D = 880 – 220 = 660, up from 650650D/DD/D-1-1 = 10/650 = 1.5% = 10/650 = 1.5%Restrictive: implies decline in real Restrictive: implies decline in real

termstermsNeed to divide permissible credit Need to divide permissible credit

expansion between public sector expansion between public sector and private sectorand private sector

Determination of creditDetermination of credit

Financial programming Financial programming step by step: Recapstep by step: Recap

Sequence of stepsSequence of steps

RR** ZZ YY MM DD

Z = X + F + RZ = X + F + R-1-1 – R – R**

Z = mPYZ = mPY

MV = PYMV = PY

D = M – RD = M – R**

Notice that Z now means

nominal imports, not real

imports as in Lecture 1 on

Macroeconomic Adjustment

and Structural Reform

Forecasts of X and

F play a key role:

Lower forecasts

mean lower D for

given R*

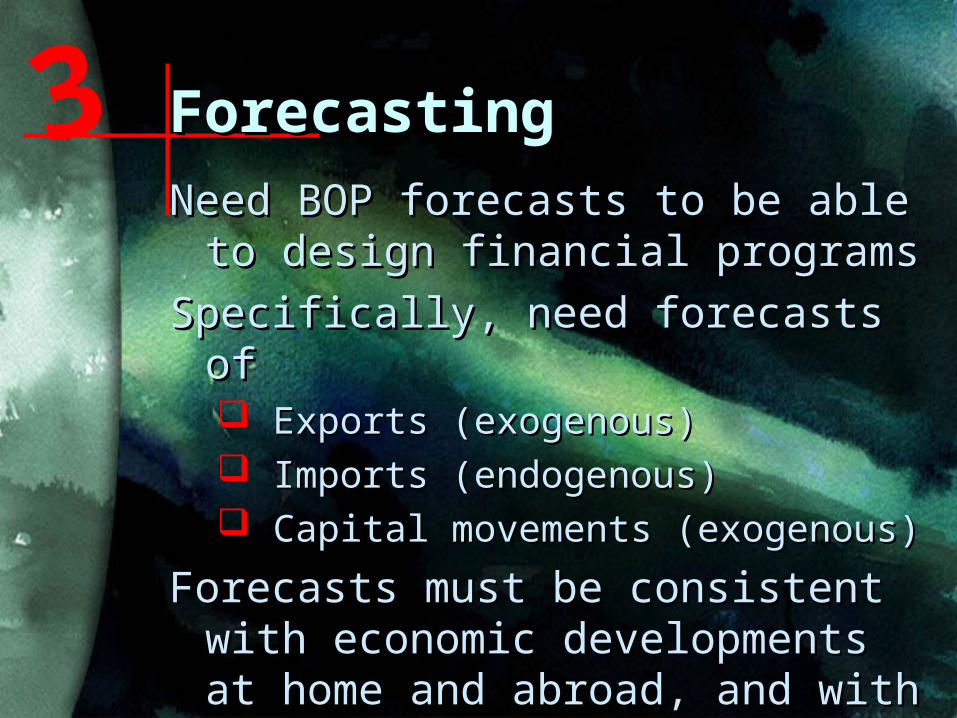

Need BOP forecasts to be able to Need BOP forecasts to be able to design financial programsdesign financial programs

Specifically, need forecasts ofSpecifically, need forecasts of Exports (exogenous)Exports (exogenous) Imports (endogenous)Imports (endogenous) Capital movements (exogenous)Capital movements (exogenous)

Forecasts must be consistent with Forecasts must be consistent with economic developments at home economic developments at home and abroad, and with one and abroad, and with one anotheranother

ForecastingForecasting3

From From supply sidesupply side, disaggregate , disaggregate View main categories of exports View main categories of exports

separatelyseparatelyObtain price forecasts from international Obtain price forecasts from international

organizations, industry groupsorganizations, industry groups

Obtain volume forecasts by surveying Obtain volume forecasts by surveying domestic producers. Recall that domestic producers. Recall that supply supply depends on pricedepends on price

Exports of coffee: PExports of coffee: PccXXcc

Exports of tea: PExports of tea: PttXXtt

Exports of rice: PExports of rice: PrrXXrr

Total exports: Total exports: PX = PPX = PccXXc c ++ PPttXXt t ++

PPrrXXrr

Forecasting exports 1Forecasting exports 1

Small country Small country

assumption: Export assumption: Export

prices are exogenousprices are exogenous

Divide through export equation by Divide through export equation by X to get expression for export X to get expression for export price P price P

P = (XP = (Xcc/X)P/X)Pc c ++ (X(Xtt/X)/X) PPt t ++ (X(Xrr/X)/X) PPrr

Hence, aggregate export price Hence, aggregate export price index is a weighted average of index is a weighted average of export prices for individual export prices for individual commodities, with weights commodities, with weights reflecting their relative reflecting their relative importance to total exportsimportance to total exports

Forecasting exports 1Forecasting exports 1

From From supply sidesupply side, another method , another method without disaggregation without disaggregation

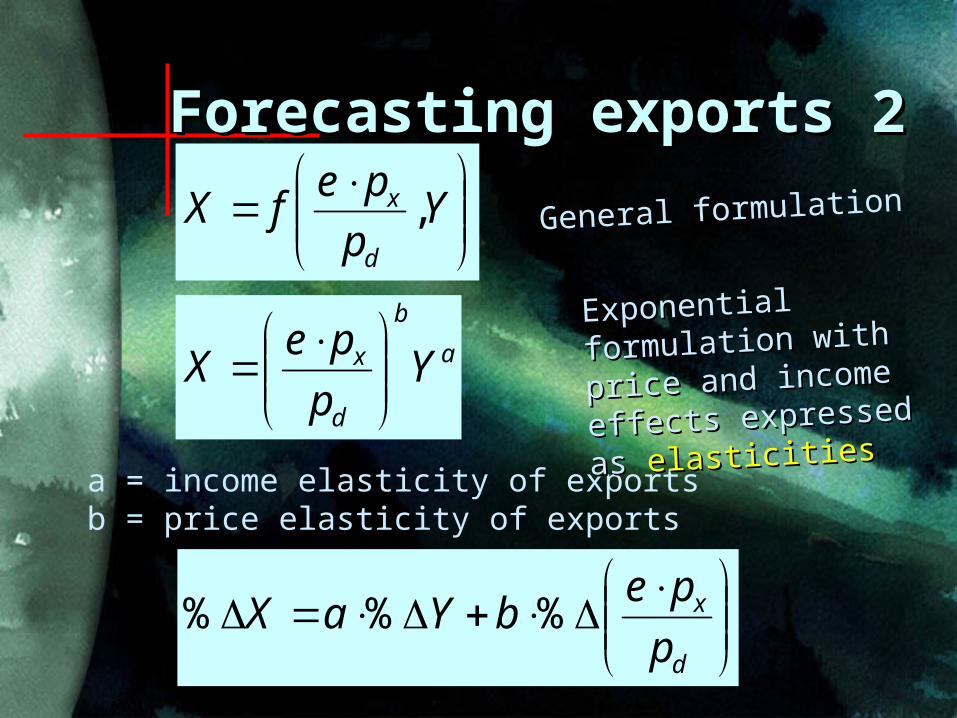

Forecasting exports 2Forecasting exports 2

Standard supply Standard supply

equation: equation:

Supply depends on Supply depends on

relative pricerelative price as well as as well as

output capacityoutput capacity

Y

p

pefX

d

x ,

X = export volume (real exports)e = nominal exchange rate (hr/$)px = price of exports in $pd = price of domestically produced goods in hrY = output capacity at home

+ +

Forecasting exports 2Forecasting exports 2

Y

p

pefX

d

x ,

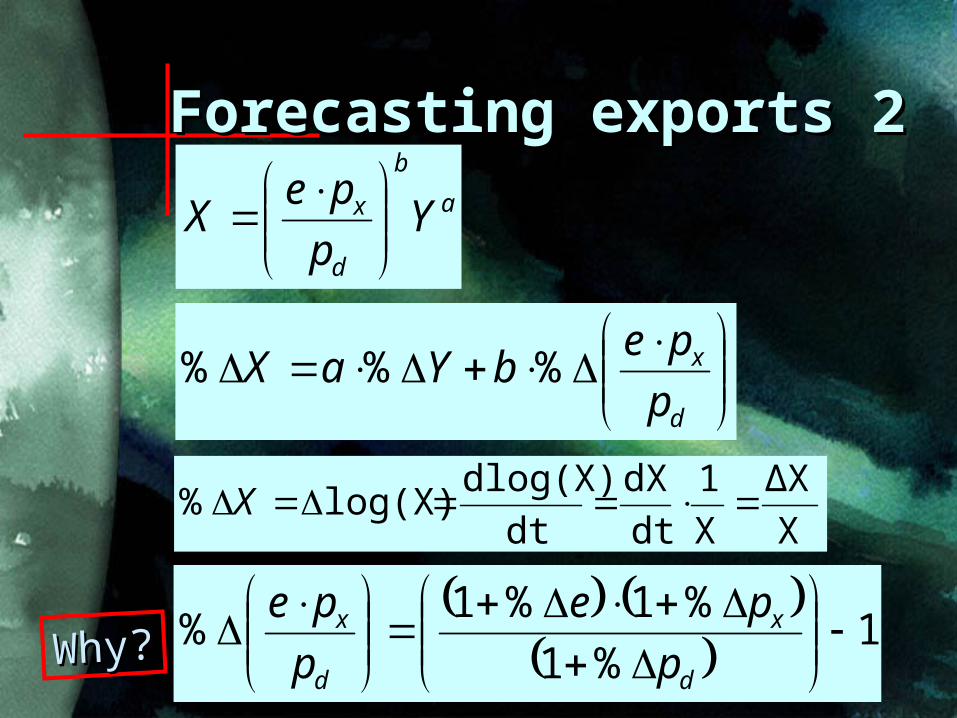

a = income elasticity of exports b = price elasticity of exports

a

b

d

x Yp

peX

d

x

p

pebYaX %%%

General formulation

Exponential Exponential

formulation with formulation with

price and income price and income

effects expressed as effects expressed as

elasticitieselasticities

Forecasting exports 2Forecasting exports 2

Y

p

pefX

d

x ,

a = income elasticity of exports b = price elasticity of exports

a

b

d

x Yp

peX

d

x

p

pebYaX logloglog

General formulation

Exponential Exponential

formulation with formulation with

price and income price and income

effects expressed as effects expressed as

elasticitieselasticities

Forecasting exports 2Forecasting exports 2a

b

d

x Yp

peX

d

x

p

pebYaX %%%

X

ΔX

X

1

dt

dX

dt

dlog(X)log(X)% X

1%1

%1%1%

d

x

d

x

p

pe

p

peWhy?Why?

Forecasting exports 2Forecasting exports 2

w

zxy

1%1

%1%1%

d

x

d

x

p

pe

p

pe

100

100100y

105

110115y

So, if x rises by 15%, z rises by 10%, and w rises by 5%, then y rises not by 20% but by 20.5% because (115*110/105) = 120.476 wzxy %%%%

Simpler formula works only for small changes

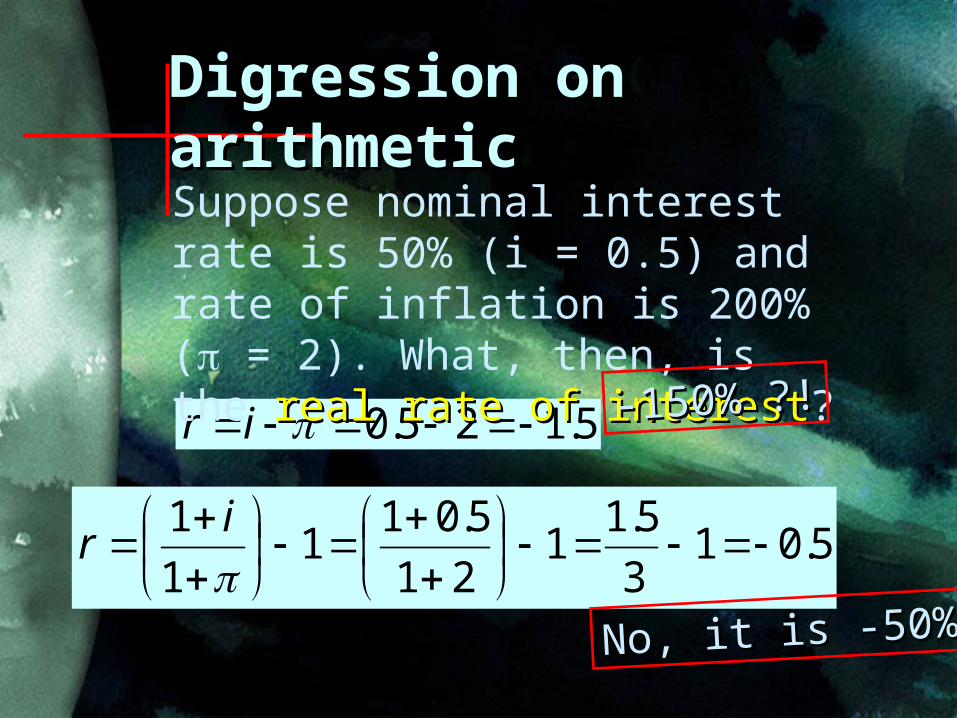

Digression on Digression on arithmeticarithmetic

5.125.0 ir

Suppose nominal interest rate is 50% (i = 0.5) and rate of inflation is 200% ( = 2). What, then, is the real rate of real rate of interestinterest?

5.013

5.11

21

5.011

1

1

i

r

No, it is -50%No, it is -50%

-150% ?!-150% ?!

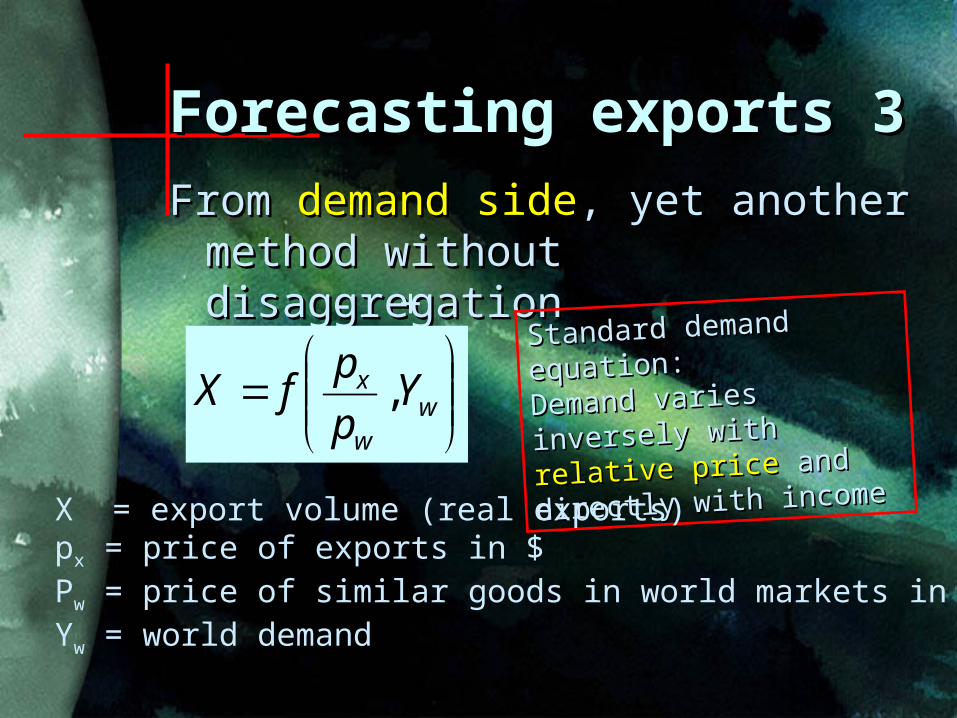

From From demand sidedemand side, yet another , yet another method without disaggregation method without disaggregation

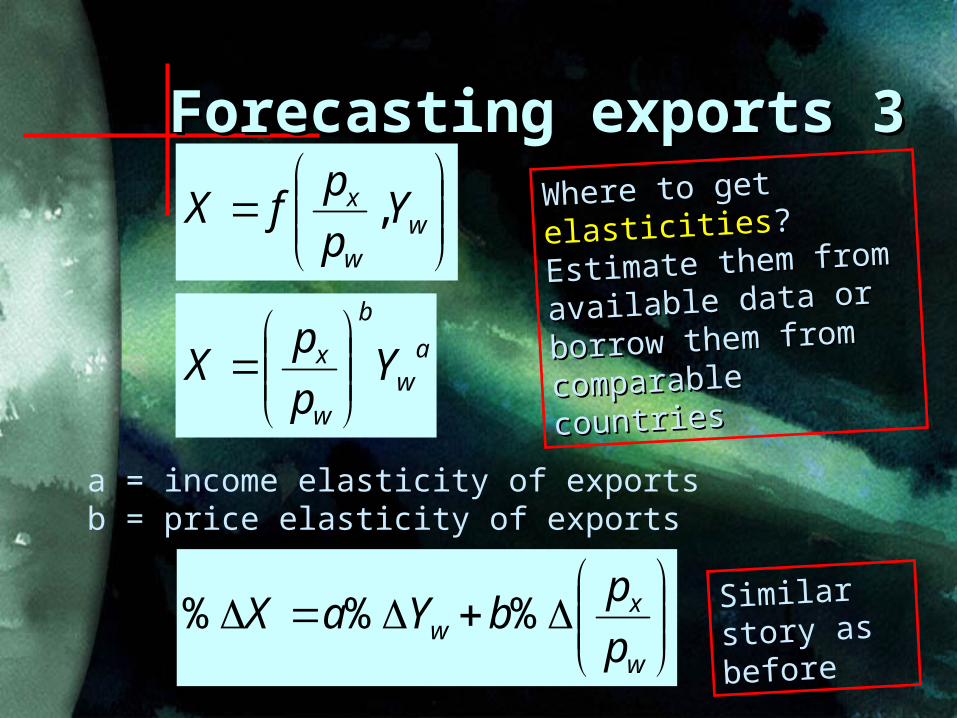

Forecasting exports 3Forecasting exports 3

Standard demand Standard demand

equation: equation:

Demand varies inversely Demand varies inversely

with with relative pricerelative price and and

directly with incomedirectly with income

w

w

x Yp

pfX ,

X = export volume (real exports)px = price of exports in $Pw = price of similar goods in world markets in $Yw = world demand

- +

Forecasting exports 3Forecasting exports 3

w

w

x Yp

pfX ,

a = income elasticity of exports b = price elasticity of exports

aw

b

w

x Yp

pX

w

xw p

pbYaX %%% Similar

story as before

Where to get Where to get

elasticitieselasticities??

Estimate them from Estimate them from

available data or available data or

borrow them from borrow them from

comparable countriescomparable countries

From From demand sidedemand side, without , without disaggregation disaggregation

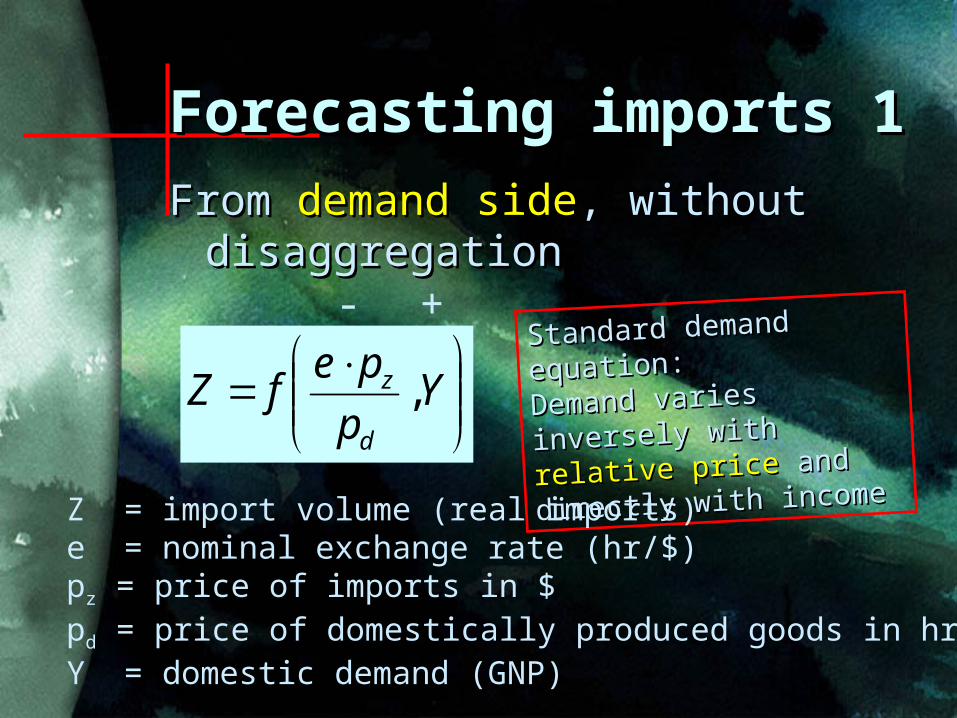

Forecasting imports 1Forecasting imports 1

Standard demand Standard demand

equation: equation:

Demand varies inversely Demand varies inversely

with with relative pricerelative price and and

directly with incomedirectly with income

Y

p

pefZ

d

z ,

Z = import volume (real imports)e = nominal exchange rate (hr/$)pz = price of imports in $pd = price of domestically produced goods in hrY = domestic demand (GNP)

- +

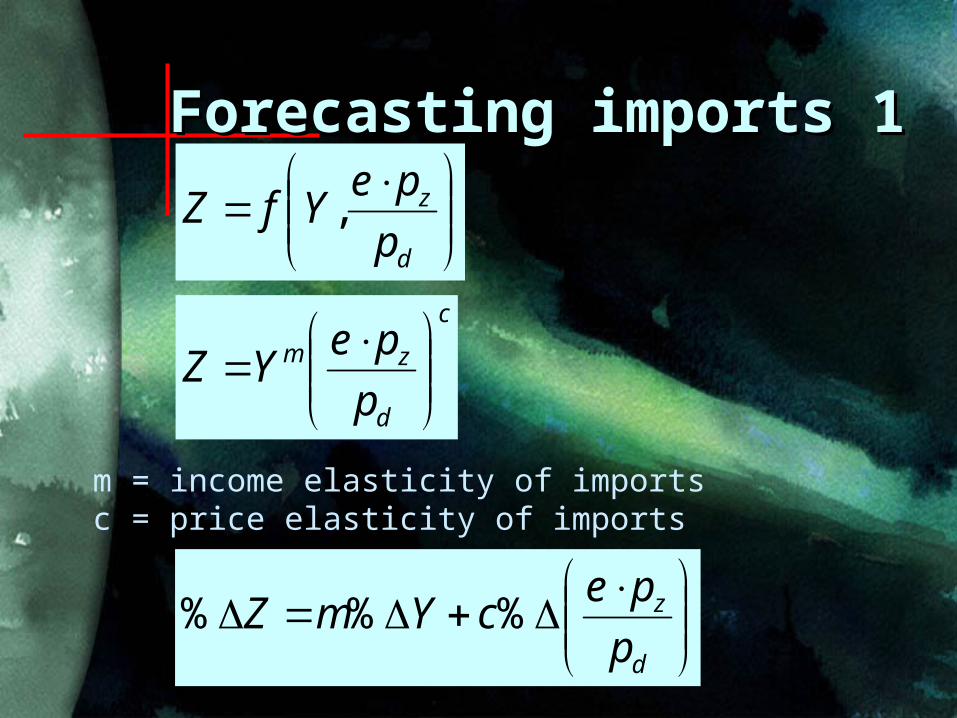

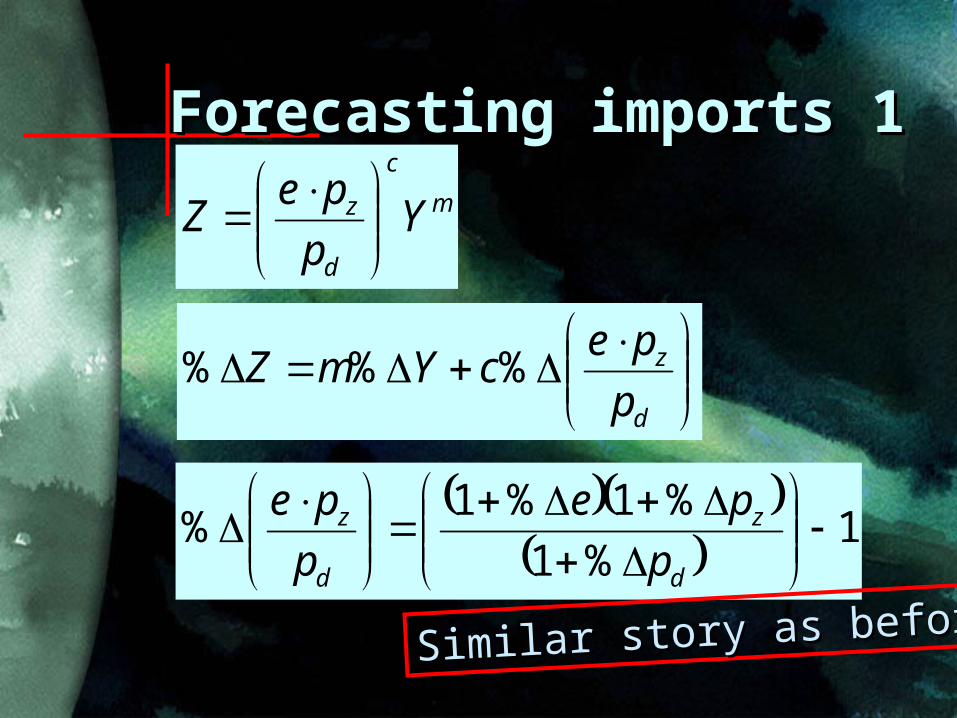

Forecasting imports 1Forecasting imports 1

d

z

p

peYfZ ,

m = income elasticity of imports c = price elasticity of imports

c

d

zm

p

peYZ

d

z

p

pecYmZ %%%

Forecasting imports 1Forecasting imports 1m

c

d

z Yp

peZ

d

z

p

pecYmZ %%%

1%1

%1%1%

d

z

d

z

p

pe

p

pe

Similar story as beforeSimilar story as before

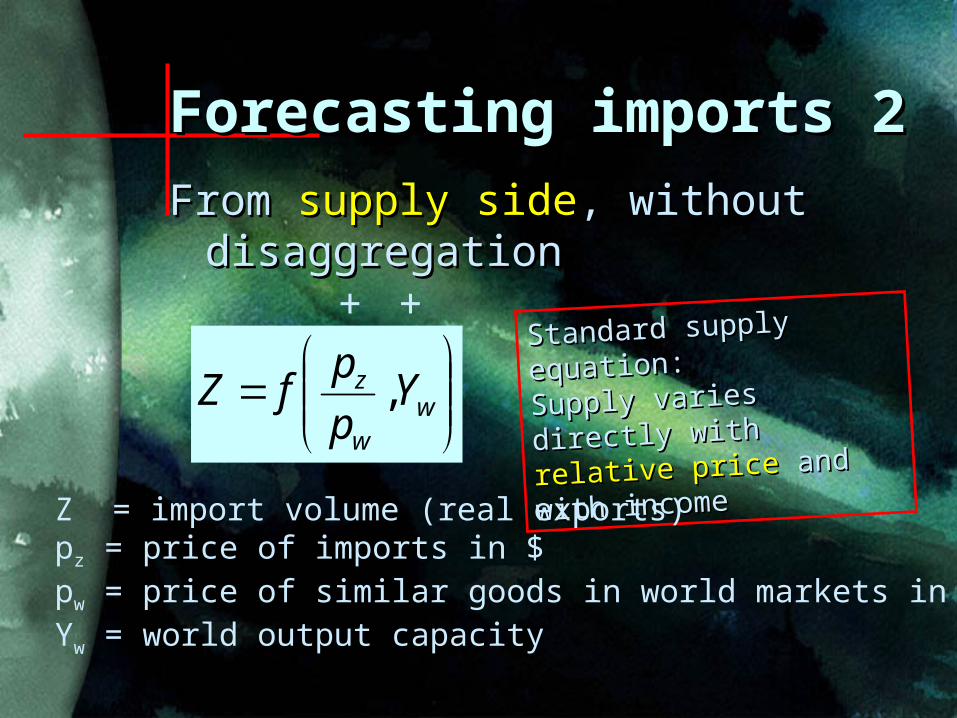

From From supply sidesupply side, without , without disaggregation disaggregation

Forecasting imports 2Forecasting imports 2

Standard supply Standard supply

equation: equation:

Supply varies directly Supply varies directly

with with relative pricerelative price and and

with incomewith income

w

w

z Yp

pfZ ,

Z = import volume (real exports)pz = price of imports in $pw = price of similar goods in world markets in $Yw = world output capacity

+ +

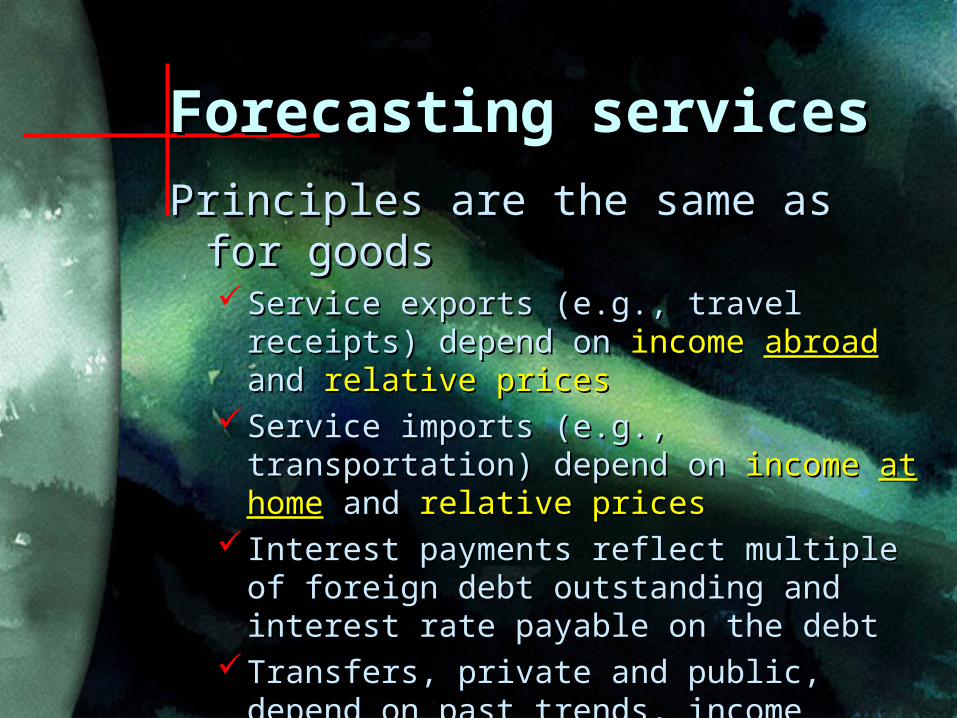

Principles are the same as for Principles are the same as for goodsgoodsService exports (e.g., travel receipts) Service exports (e.g., travel receipts)

depend on depend on income income abroadabroad and and relative relative pricesprices

Service imports (e.g., transportation) Service imports (e.g., transportation) depend on depend on income income at homeat home and and relative relative pricesprices

Interest payments reflect multiple of Interest payments reflect multiple of foreign debt outstanding and interest rate foreign debt outstanding and interest rate payable on the debtpayable on the debt

Transfers, private and public, depend on Transfers, private and public, depend on past trends, income abroad, official past trends, income abroad, official commitments, special relationships (e.g., commitments, special relationships (e.g., EU) EU)

Forecasting servicesForecasting services

This is more difficultThis is more difficultForeign borrowingForeign borrowing: depends on plans of : depends on plans of

domestic authorities, commitments of domestic authorities, commitments of foreign lenders, interest rates at home foreign lenders, interest rates at home and abroadand abroad

Foreign direct investmentForeign direct investment: depends on : depends on domestic market size, labor skills, domestic market size, labor skills, investment and export opportunities, investment and export opportunities, macroeconomic stability, track record, macroeconomic stability, track record, growth prospects, stability and growth prospects, stability and transparency of regulationstransparency of regulations

Errors and omissionsErrors and omissions: depends on trends, : depends on trends, political and economic eventspolitical and economic events

Forecasting capital Forecasting capital flowsflows

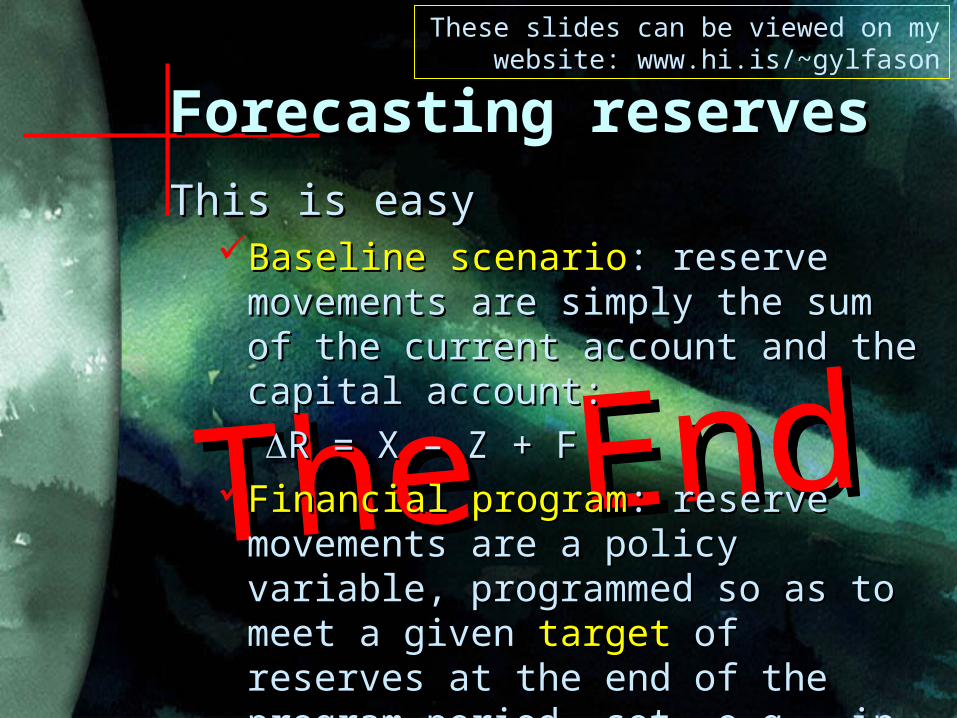

Forecasting reservesForecasting reserves

The EndThe End

This is easyThis is easyBaseline scenarioBaseline scenario: reserve : reserve

movements are simply the sum of movements are simply the sum of the current account and the capital the current account and the capital account: account:

R = X – Z + FR = X – Z + FFinancial programFinancial program: reserve : reserve

movements are a policy variable, movements are a policy variable, programmed so as to meet a given programmed so as to meet a given targettarget of reserves at the end of the of reserves at the end of the program period, set, e.g., in terms program period, set, e.g., in terms of months of import coverageof months of import coverage

These slides can be viewed on my website: www.hi.is/~gylfason

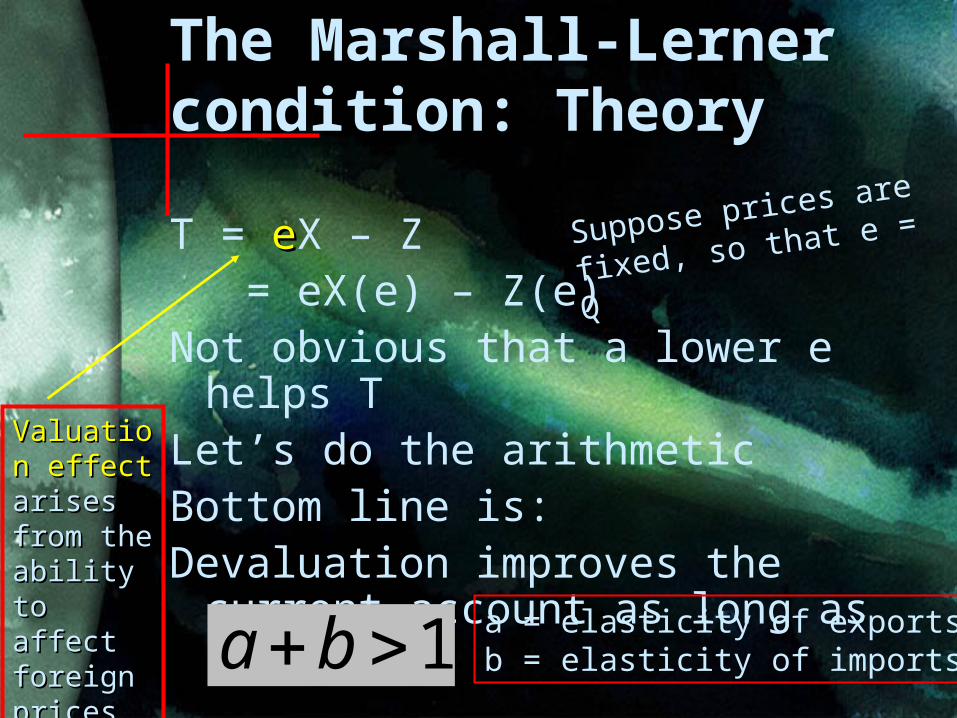

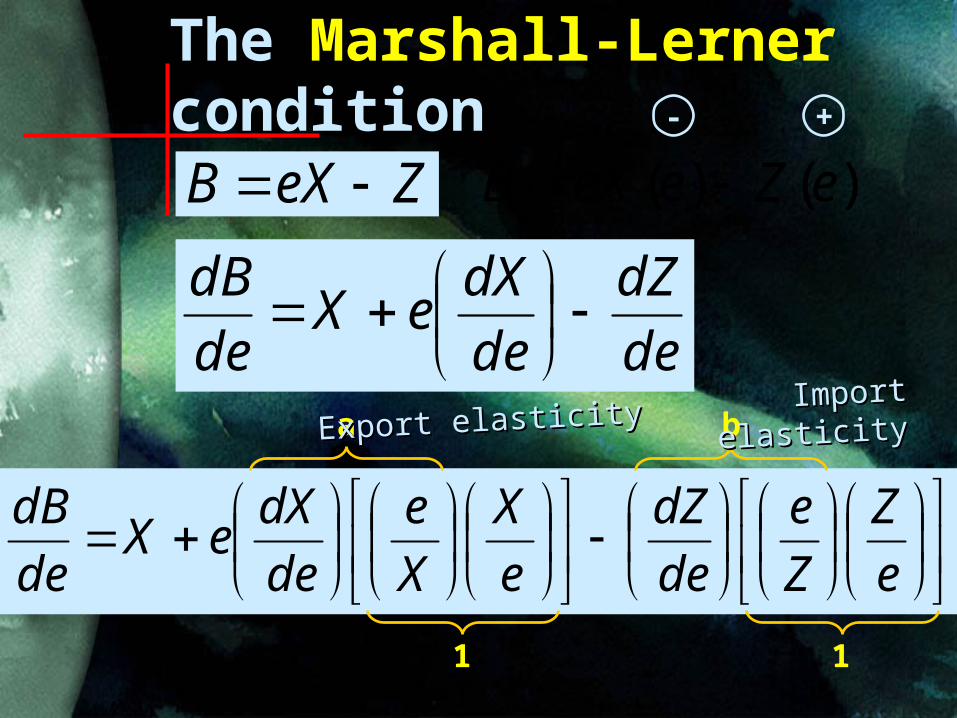

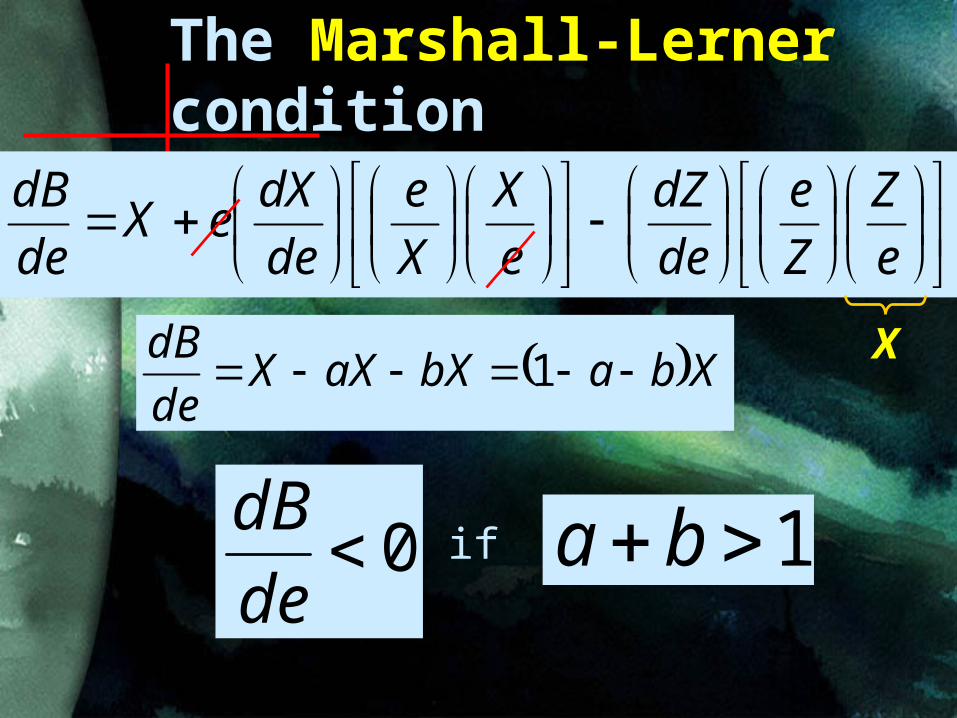

The Marshall-Lerner condition: Theory

T = eeX – Z = eX(e) – Z(e)Not obvious that a lower e helps TLet’s do the arithmeticBottom line is:Devaluation improves the current

account as long as

1ba

Suppose prices are

fixed, so that e = Q

a = elasticity of exportsb = elasticity of imports

Valuation Valuation effecteffect arises arises from the from the ability to ability to affect affect foreign foreign pricesprices

The Marshall-Lerner condition

ZeXB )()( eZeeXB

de

dZ

de

dXeX

de

dB

e

Z

Z

e

de

dZ

e

X

X

e

de

dXeX

de

dB

1 1

a b

- +

Export elasticityExport elasticity ImportImportelasticityelasticity

The Marshall-Lerner condition

e

Z

Z

e

de

dZ

e

X

X

e

de

dXeX

de

dB

XbabXaXXde

dB 1

0de

dB 1baif

X

The Marshall-Lerner condition: Evidence

Econometric studies indicate that the Marshall-Lerner condition is almost invariably satisfied

Industrial countries: a = 1, b = 1Developing countries: a = 1, b =

1.5Hence,

1ba Devaluation

improves the

current account

Empirical evidence from developing countries

Elasticity of Elasticity ofexports imports

Argentina 0.6 0.9Brazil 0.4 1.7India 0.5 2.2Kenya 1.0 0.8Korea 2.5 0.8Morocco 0.7 1.0Pakistan 1.8 0.8Philippines 0.9 2.7Turkey 1.4 2.7Average 1.1 1.5

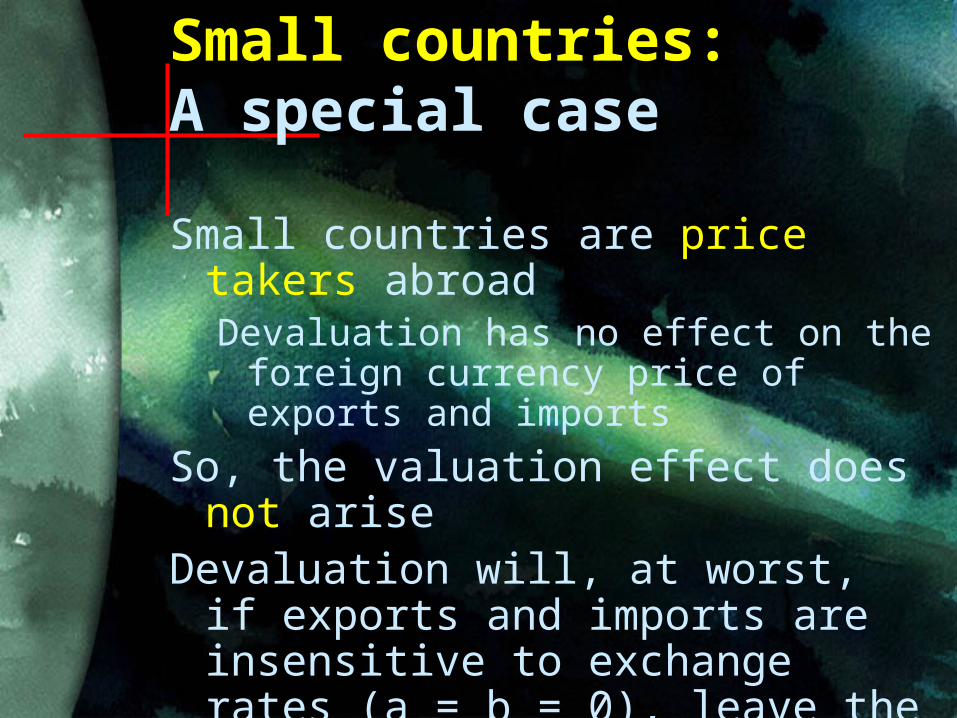

Small countries: A special case

Small countries are price takers abroadDevaluation has no effect on the

foreign currency price of exports and imports

So, the valuation effect does not arise

Devaluation will, at worst, if exports and imports are insensitive to exchange rates (a = b = 0), leave the current account unchanged

Hence, if a > 0 or b > 0, devaluation improves the current account