automotive industry turkey - turkofamerica.com · otomotiv sanayii derne ği / osd automotive...

TRANSCRIPT

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

1Logo speaker’s institution Logo local institution

The Automotive Industry in Turkey

Hülya Özbudun / OSD Technical Coordinator

14 June 2010

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

2Logo speaker’s institution Logo local institution

Founded in 1974Main Objectives Are:

���� To Represent MV Sector In Public Authorities, Local and International Organisations

���� To Gather and Publish Various Information on MVI of Turkey

���� To Organize & Conduct Joint Actions in Different FieldsIs an Active Member of:

� OICA � ACEA Liaison Committee

� ODETTE� ENX

OSD is a Partner of ACEA / EUCAR, EU ERTRAC and EU Motor Vehicle Technical Committee UN / WP 29

All Relevant Information is Found in OSD Web-Site: www.osd.org.tr

Otomotiv Sanayii Derneği / OSDAutomotive Manufacturers Association

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

3Logo speaker’s institution Logo local institution

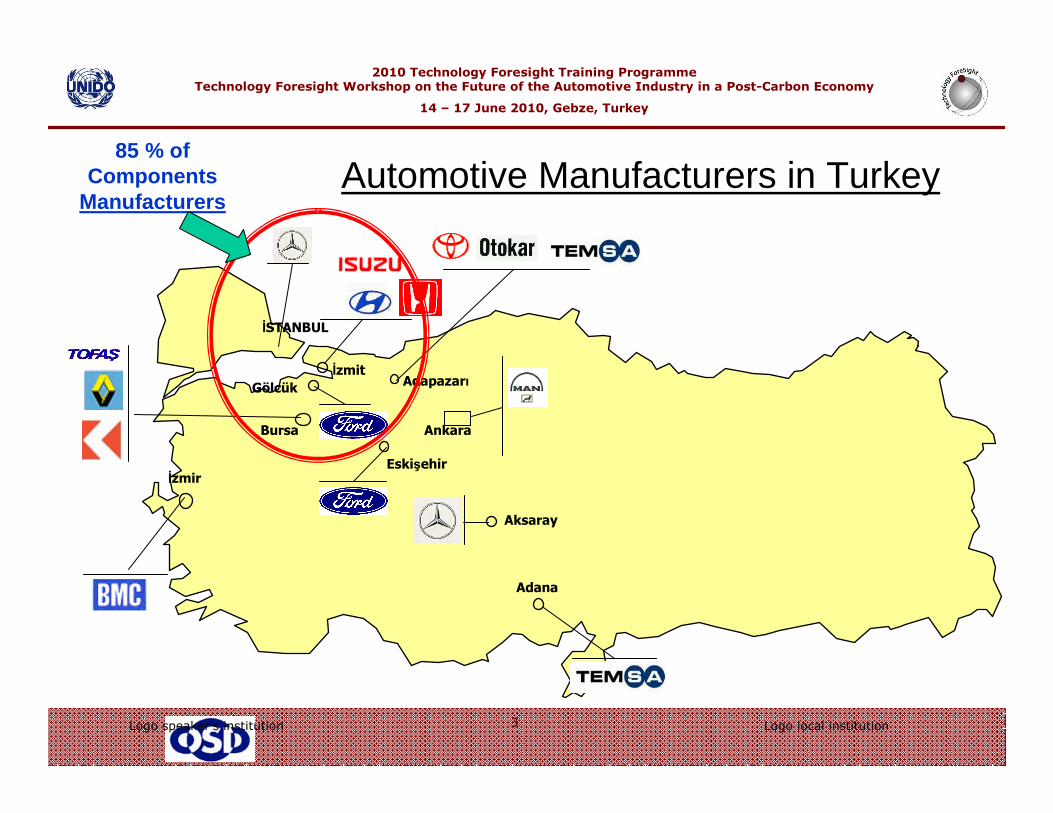

Đzmir

Adapazarı

Ankara

ĐSTANBUL

Gölcük

Aksaray

Đzmit

Bursa

Eskişehir

Adana

85 % of Components

ManufacturersAutomotive Manufacturers in Turkey

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

4Logo speaker’s institution Logo local institution

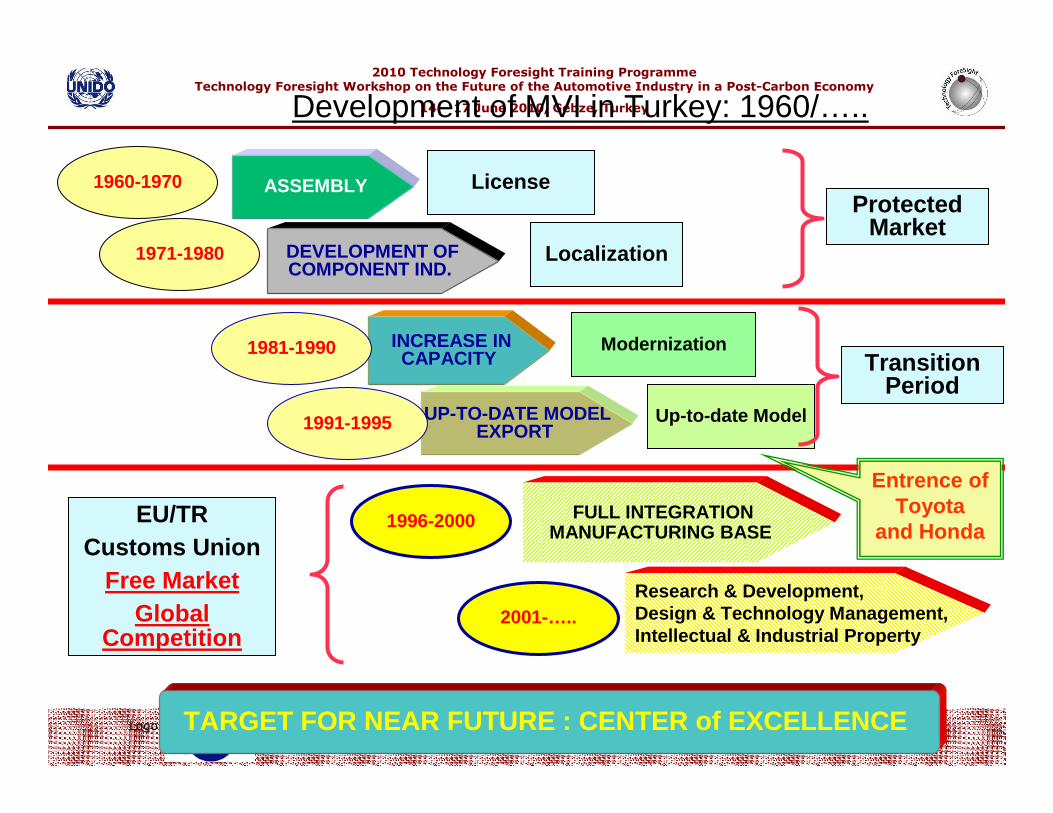

ASSEMBLY

DEVELOPMENT OFCOMPONENT IND.

INCREASE INCAPACITY

UP-TO-DATE MODELEXPORT

FULL INTEGRATIONMANUFACTURING BASE

Research & Development, Design & Technology Management,Intellectual & Industrial Property

1960-1970

1971-1980

1981-1990

1991-1995

1996-2000

2001-…..

TARGET FOR NEAR FUTURE : CENTER of EXCELLENCE

License

Localization

Modernization

Up-to-date Model

Transition Period

EU/TRCustoms Union

Free MarketGlobal

Competition

Protected Market

Development of MVI in Turkey: 1960/…..

Entrence ofToyota

and Honda

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

5Logo speaker’s institution Logo local institution

0

200

400

600

800

1.000

1.200

1963

1964

1965

1966

1967

1968

1969

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

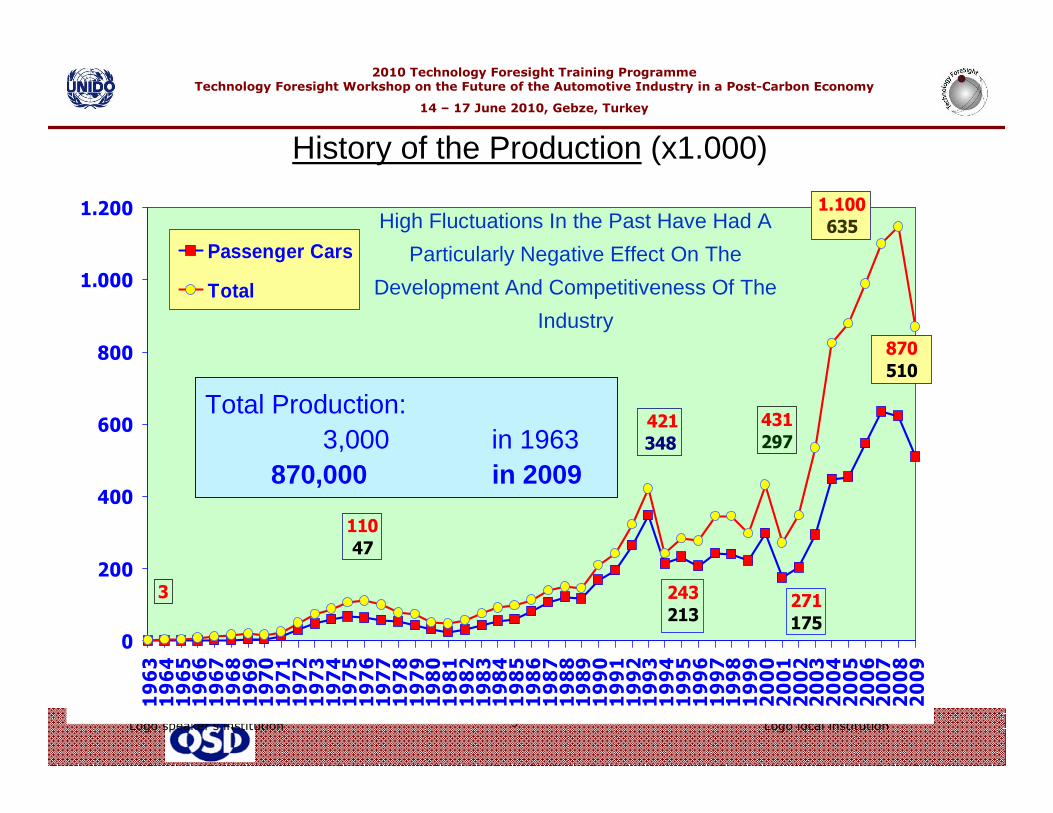

Passenger Cars

Total

110

47

421

348

431

297

1.100

635

3 243

213 271

175

870

510

Total Production:3,000 in 1963

870,000 in 2009

History of the Production (x1.000)

High Fluctuations In the Past Have Had A

Particularly Negative Effect On The

Development And Competitiveness Of The

Industry

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

6Logo speaker’s institution Logo local institution

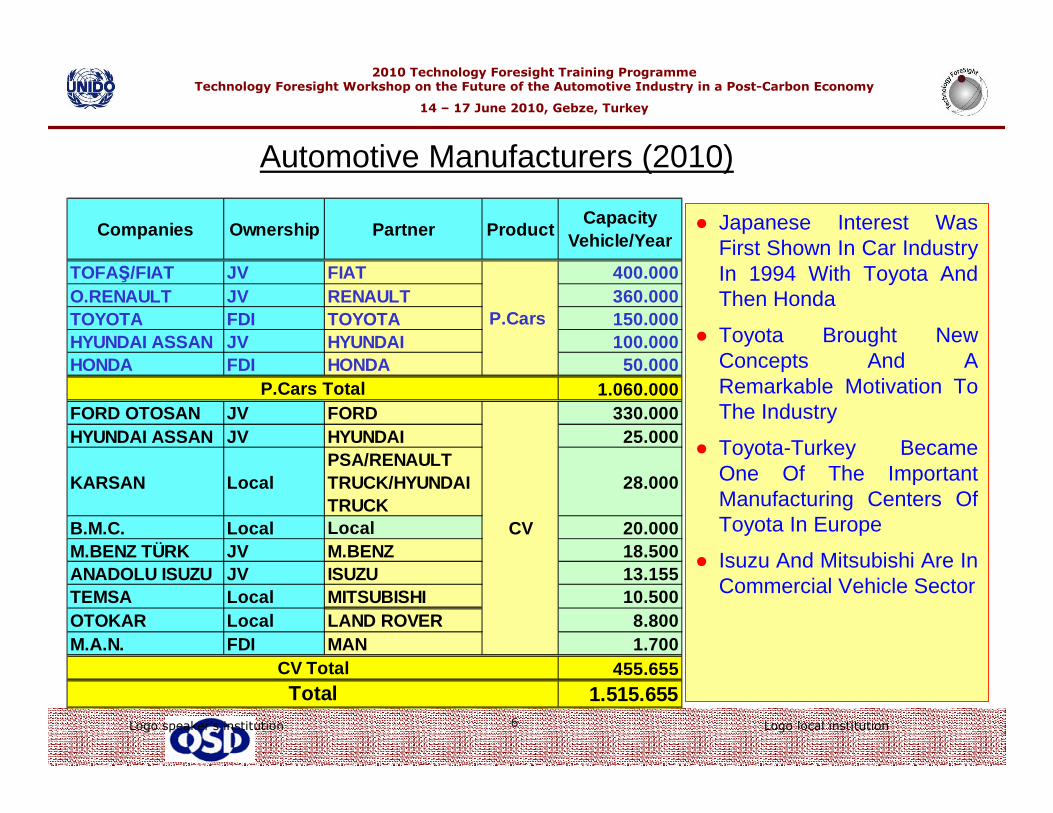

TOFAŞ/FIAT JV FIAT 400.000O.RENAULT JV RENAULT 360.000TOYOTA FDI TOYOTA 150.000HYUNDAI ASSAN JV HYUNDAI 100.000HONDA FDI HONDA 50.000

1.060.000FORD OTOSAN JV FORD 330.000HYUNDAI ASSAN JV HYUNDAI 25.000

KARSAN LocalPSA/RENAULT TRUCK/HYUNDAI TRUCK

28.000

B.M.C. Local Local 20.000M.BENZ TÜRK JV M.BENZ 18.500ANADOLU ISUZU JV ISUZU 13.155TEMSA Local MITSUBISHI 10.500OTOKAR Local LAND ROVER 8.800M.A.N. FDI MAN 1.700

455.6551.515.655

Capacity Vehicle/Year

CV

Ownership

TotalCV Total

P.Cars

Companies Partner

P.Cars Total

Product ● Japanese Interest Was First Shown In Car Industry In 1994 With Toyota And Then Honda

● Toyota Brought New Concepts And A Remarkable Motivation To The Industry

● Toyota-Turkey Became One Of The Important Manufacturing Centers Of Toyota In Europe

● Isuzu And Mitsubishi Are In Commercial Vehicle Sector

Automotive Manufacturers (2010)

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

7Logo speaker’s institution Logo local institution

Number of Manufacturers 13Link With Non-EU 5 (% 17 of 2009 production)

* JV/FDI 4 * License 1

Link With EU 7 (% 82 of 2009 production)

* JV/FDI 5 * License 2

Local 1 (% 1 of 2008 production)

Link With EU Manufacturers� FIAT GROUP JV� FORD JV� MAN FDI� M.BENZ JV� RENAULT JV� JAGUAR LAND ROVER L� PSA L

Link With Non-EU Manufacturers

� ISUZU JV� TOYOTA FDI� MITSUBISHI L� HONDA FDI� HYUNDAI JV

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

8Logo speaker’s institution Logo local institution

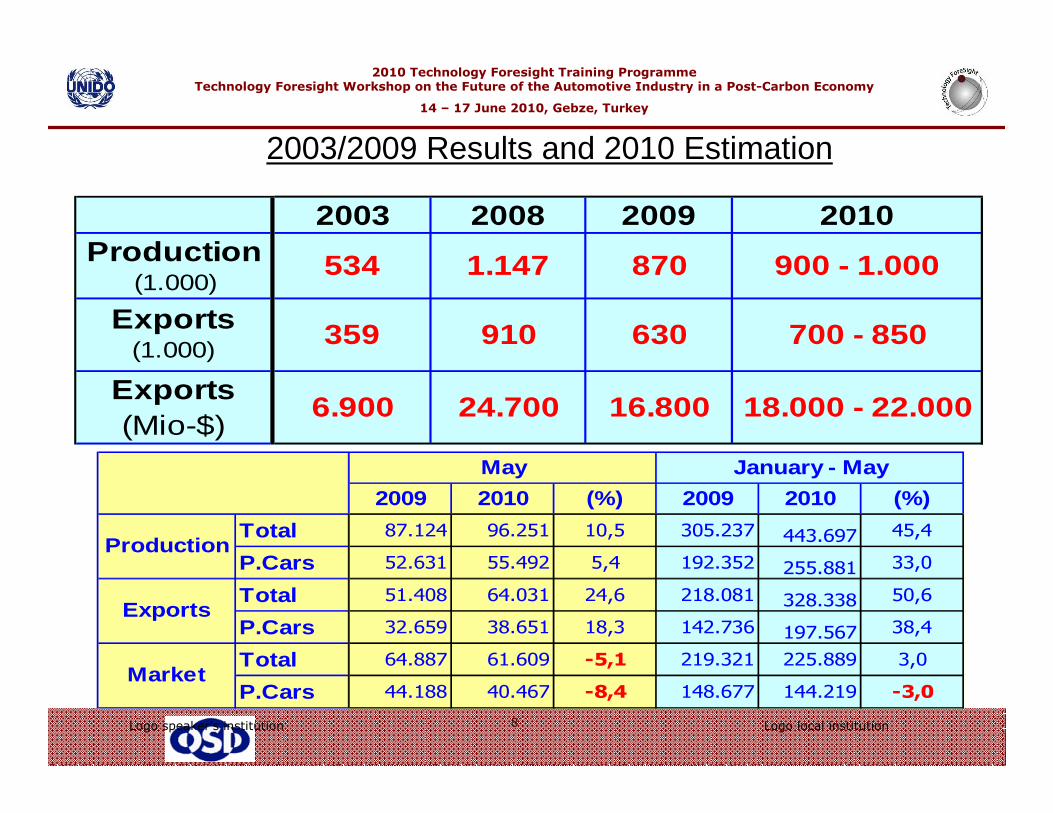

2003 2008 2009 2010Production

(1.000)534 1.147 870 900 - 1.000

18.000 - 22.000

700 - 850910

24.700

Exports (1.000)

Exports (Mio-$)

359 630

6.900 16.800

2009 2010 (%) 2009 2010 (%)

Total 87.124 96.251 10,5 305.237 443.697 45,4

P.Cars 52.631 55.492 5,4 192.352 255.881 33,0

Total 51.408 64.031 24,6 218.081 328.338 50,6

P.Cars 32.659 38.651 18,3 142.736 197.567 38,4

Total 64.887 61.609 -5,1 219.321 225.889 3,0

P.Cars 44.188 40.467 -8,4 148.677 144.219 -3,0Market

May January - May

Production

Exports

2003/2009 Results and 2010 Estimation

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

9Logo speaker’s institution Logo local institution

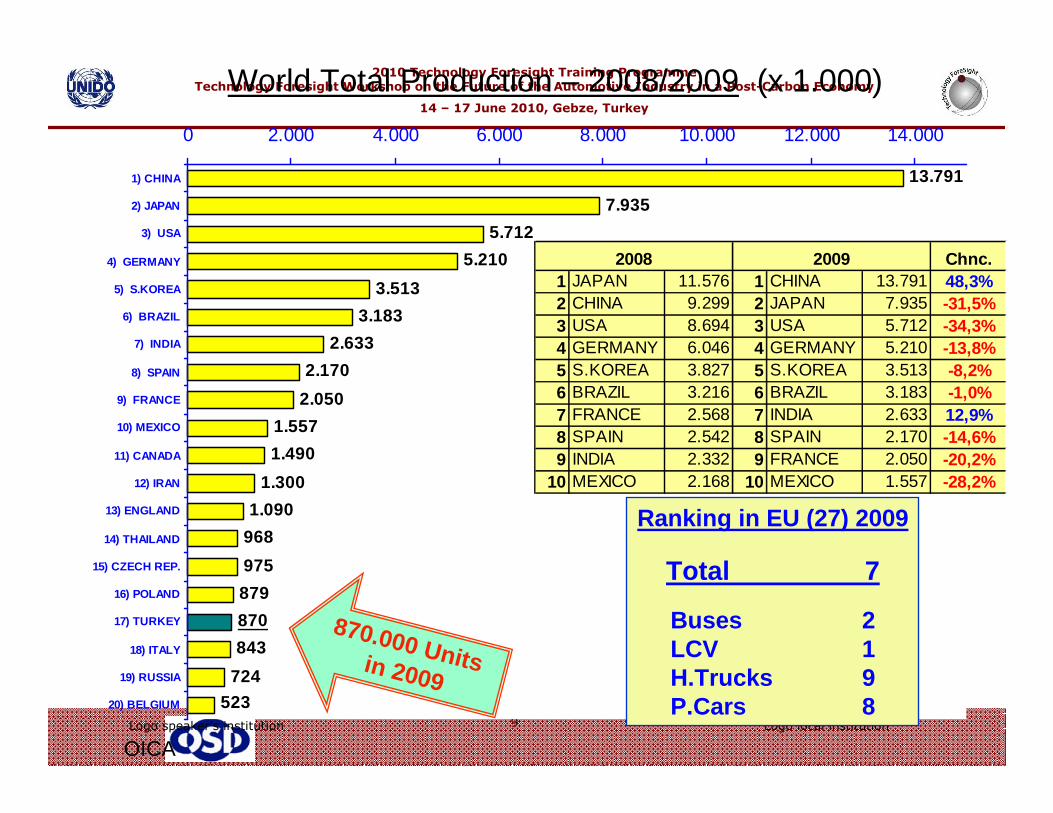

13.791

7.935

5.712

5.210

3.513

3.183

2.633

2.170

2.050

1.557

1.490

1.300

1.090

968

975

879

843

724

523

870

0 2.000 4.000 6.000 8.000 10.000 12.000 14.000

1) CHINA

2) JAPAN

3) USA

4) GERMANY

5) S.KOREA

6) BRAZIL

7) INDIA

8) SPAIN

9) FRANCE

10) MEXICO

11) CANADA

12) IRAN

13) ENGLAND

14) THAILAND

15) CZECH REP.

16) POLAND

17) TURKEY

18) ITALY

19) RUSSIA

20) BELGIUM

Ranking in EU (27) 2009

Total 7

Buses 2LCV 1H.Trucks 9P.Cars 8

870.000 Units in 2009

World Total Production – 2008/2009 (x 1.000)

Chnc.1 JAPAN 11.576 1 CHINA 13.791 48,3%2 CHINA 9.299 2 JAPAN 7.935 -31,5%3 USA 8.694 3 USA 5.712 -34,3%4 GERMANY 6.046 4 GERMANY 5.210 -13,8%5 S.KOREA 3.827 5 S.KOREA 3.513 -8,2%6 BRAZIL 3.216 6 BRAZIL 3.183 -1,0%7 FRANCE 2.568 7 INDIA 2.633 12,9%8 SPAIN 2.542 8 SPAIN 2.170 -14,6%9 INDIA 2.332 9 FRANCE 2.050 -20,2%

10 MEXICO 2.168 10 MEXICO 1.557 -28,2%

2008 2009

OICA

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

10Logo speaker’s institution Logo local institution

� 2009 Population 72.561.312

� % GNP per capita (2006) 5477 $

� # of Employees in MVI (2009)

» # of Workers 31 191» Total 39.584

� # of Supplying Companies (2009) 1300

� Vehicle ownership rate (2009)98 pcars/1.000 Inhabitants 147 vehicles/1.000 Inhabitants

Statistics on Automotive Production

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

11Logo speaker’s institution Logo local institution

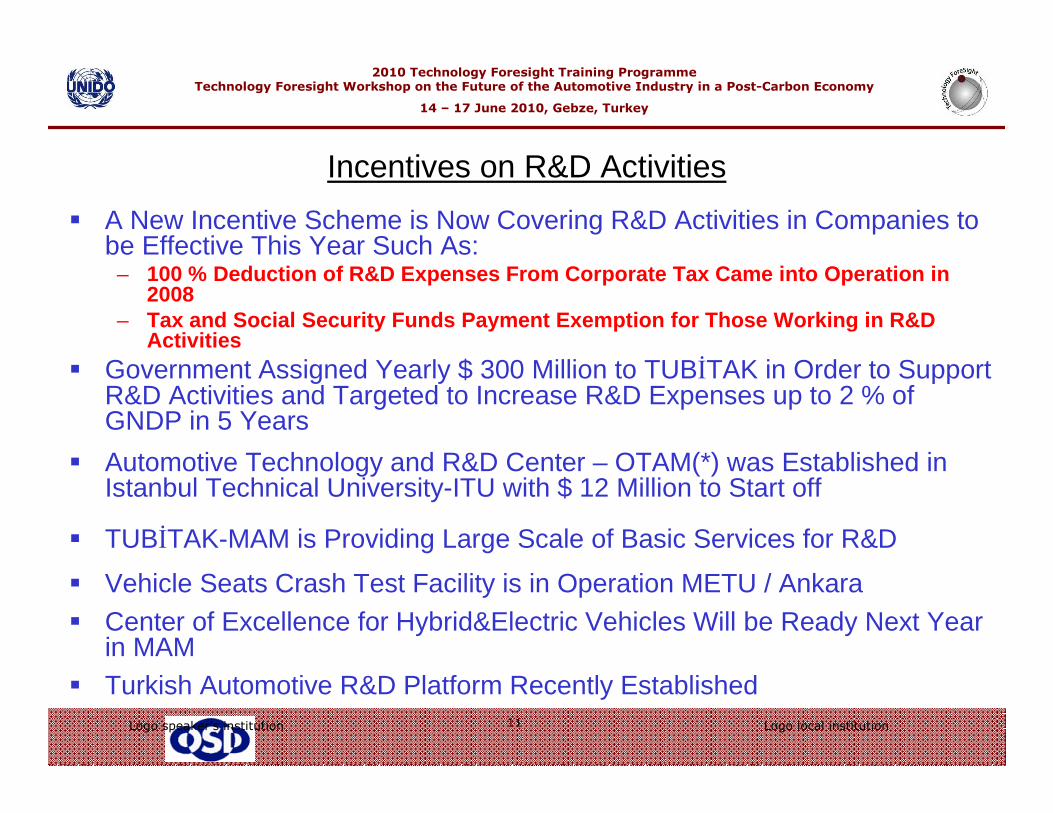

� A New Incentive Scheme is Now Covering R&D Activities in Companies to be Effective This Year Such As:

– 100 % Deduction of R&D Expenses From Corporate Tax Came into Operation in 2008

– Tax and Social Security Funds Payment Exemption for Those Working in R&D Activities

� Government Assigned Yearly $ 300 Million to TUBĐTAK in Order to Support R&D Activities and Targeted to Increase R&D Expenses up to 2 % of GNDP in 5 Years

� Automotive Technology and R&D Center – OTAM(*) was Established in Istanbul Technical University-ITU with $ 12 Million to Start off

� TUBĐTAK-MAM is Providing Large Scale of Basic Services for R&D

� Vehicle Seats Crash Test Facility is in Operation METU / Ankara� Center of Excellence for Hybrid&Electric Vehicles Will be Ready Next Year

in MAM� Turkish Automotive R&D Platform Recently Established

Incentives on R&D Activities

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

12Logo speaker’s institution Logo local institution

� Motor Vehicle Technical Committee (MARTEK) was Established by 10 Chosen Members From Public and Industry.

Ministry of Industry and Trade 2Ministry of Transport 1Ministry of Interior 1Undersecretaries of Foreign Trade 1General Directorate For Highways 1Turkish Statistics Institute 1Automotive Industry (OSD) 1Automotive Supply Industry (TAYSAD)1Technical Services Representative 1

For Technical Legislation Adaptation and Implementation, connected with MARTEK & parallel to international and national regulations, 10 + 2 working parties were formed respectively.

Main Stakeholders - I

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

13Logo speaker’s institution Logo local institution

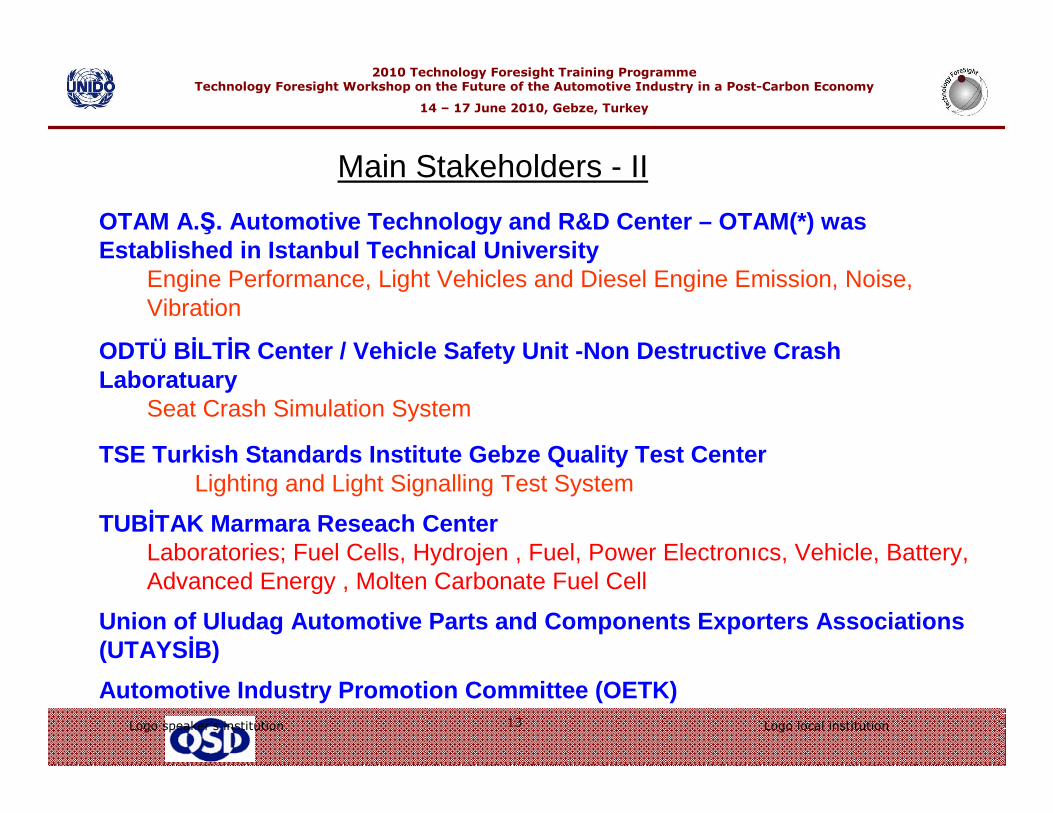

OTAM A.Ş. Automotive Technology and R&D Center – OTAM(*) was Established in Istanbul Technical University

Engine Performance, Light Vehicles and Diesel Engine Emission, Noise, Vibration

ODTÜ BĐLTĐR Center / Vehicle Safety Unit -Non Destructive Cra sh Laboratuary

Seat Crash Simulation System

TSE Turkish Standards Institute Gebze Quality Test CenterLighting and Light Signalling Test System

TUBĐTAK Marmara Reseach CenterLaboratories; Fuel Cells, Hydrojen , Fuel, Power Electronıcs, Vehicle, Battery, Advanced Energy , Molten Carbonate Fuel Cell

Union of Uludag Automotive Parts and Components Exp orters Associations (UTAYSĐB)

Automotive Industry Promotion Committee (OETK)

Main Stakeholders - II

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

14Logo speaker’s institution Logo local institution

� Climate Change Is An Important Issue For Significant And Sustainable CO2 Reductions In Our Industry

� Especially Intended For Reducing Energy Costs To A Competitive Level

� Energy Efficiency Not Only For Products But Also Production Processes As Well

� Benchmarking Processes And Some Applications Are Used To See The Best Practices and Sharing Them With Our Members

Productive Chain

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

15Logo speaker’s institution Logo local institution

● New Programs And Investments Are Performed To Protect The Environment And Improve The Energy Efficiency Of The Plants

● “Energy Management With Targets” Approach Is Used. Total Target Is Formed By:

� Managerial Targets, � Department Targets� Plant Targets

● According To This Formation, There Has Been Achievable And Measurable Targets For Short , Medium And Long Term

● The Outcome �� Cutting Pollution / Less CO 2 Emissions

� Reducing Energy Expenses � Improving Efficiency� Higher Product Quality

Energy Efficiency Activities In Our Plants

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

16Logo speaker’s institution Logo local institution

� Installing Indoor And Outdoor Efficient Lighting,

� Applying Skylight To Roofs

� Using Air Curtains

� Modernizing Boilers And Cooling Towers

� Replacing Pneumatic Tools With Electrical Ones

� Modernizing Paint Shops

� Recycling Waste Water

Energy Efficiency Activities In Our Plants

Actions Already Realized

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

17Logo speaker’s institution Logo local institution

Short Term

� Building Up Competition System About Energy Saving Project

� Actualizing “Building Automation System” For Lighting And Heating & Cooling System

� Recycling Waste Heat And Air

� Fighting With Steam And Air Leakages

Medium Term

� Increasing The Usage Of Inverters

� Replacing Magnetic Ballast With Electronic Ballast For Improving Extra Electrical Losses

� Using Frequency Converters For Pumps And Ventilation Motors

� Replacing Eff-3 And Eff-3 Motors With Eff-1 On Motors, Pumps And Fans

Long Term

� Using Renewable Energy Sources

Energy Efficiency Targets In Our Plants

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

18Logo speaker’s institution Logo local institution

� In Terms Of Motor Vehicle Production, Turkey Is The 17th BiggestProducer Of The World And The 7th Largest Manufacturer In Europe

� Export Its Products Mostly To Europe Which Is Highly Competive Market

� The Fact That Turkey Has Achieved Compliance With The EU In Terms Of The Environmental And Technical Legislations, As Well As Other International Legislations, And The Production Capability Which Meets The Customer Expectations Are Some Of The Strengths Of Turkey In This Sector.

� Our Global Partners Share The Innovations By Our Industry.

Global Productive Chain

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

19Logo speaker’s institution Logo local institution

YearsP.Car Truck Pick-Up Minibus Bus Total

2000 4.422.180 557.295 794.459 235.885 118.454 6.128.273

2001 4.534.803 562.063 833.175 239.381 119.306 6.288.728

2002 4.600.140 567.152 875.381 241.700 120.097 6.404.470

2003 4.700.343 579.010 973.457 245.394 123.500 6.621.704

2004 5.400.440 647.420 1.259.867 318.954 152.712 7.779.393

2005 5.772.745 676.929 1.475.057 338.539 163.390 8.426.660

2006 6.140.992 709.535 1.695.624 357.523 175.949 9.079.623

2007 6.472.156 729.202 1.890.459 372.601 189.128 9.653.546

2008 6.796.629 744.217 2.066.007 383.548 199.934 10.190.335

2009 7.093.964 727.302 2.204.951 384.053 201.033 10.611.303

Automotive Vehicles Park In Turkey

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

20Logo speaker’s institution Logo local institution

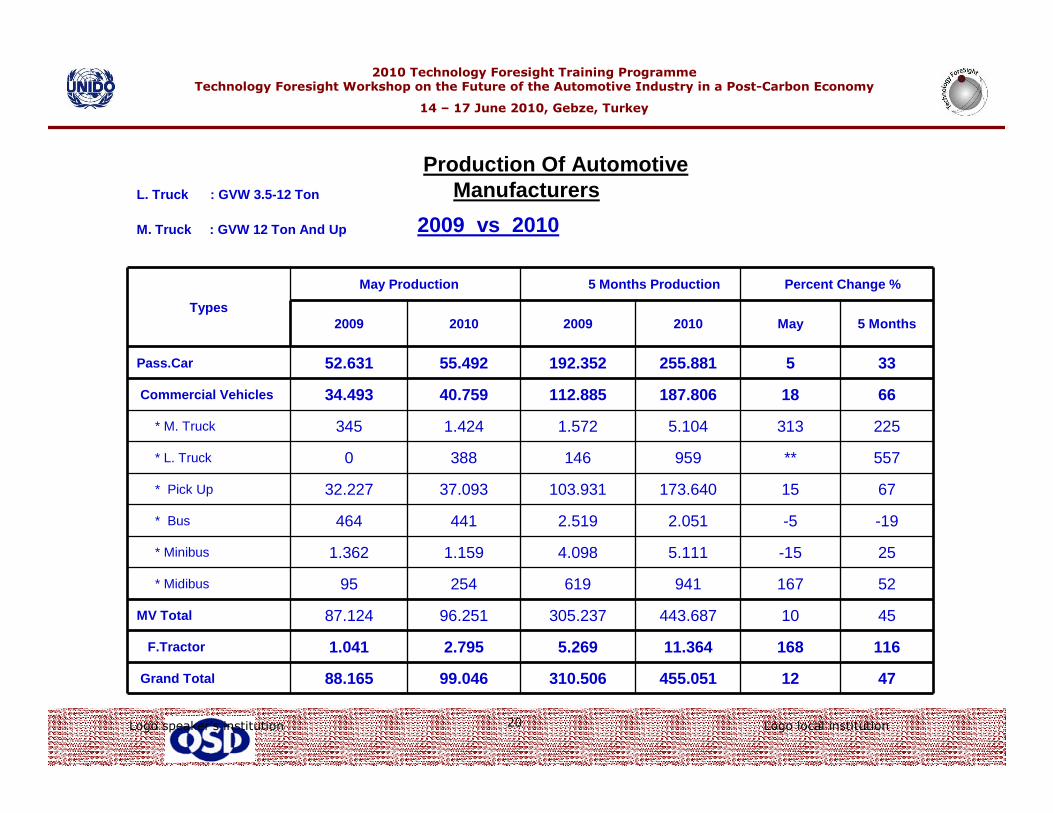

L. Truck : GVW 3.5-12 Ton

Production Of Automotive Manufacturers

M. Truck : GVW 12 Ton And Up 2009 vs 2010

Types

May Production 5 Months Production Percent Change %

2009 2010 2009 2010 May 5 Months

Pass.Car 52.631 55.492 192.352 255.881 5 33

Commercial Vehicles 34.493 40.759 112.885 187.806 18 66

* M. Truck 345 1.424 1.572 5.104 313 225

* L. Truck 0 388 146 959 ** 557

* Pick Up 32.227 37.093 103.931 173.640 15 67

* Bus 464 441 2.519 2.051 -5 -19

* Minibus 1.362 1.159 4.098 5.111 -15 25

* Midibus 95 254 619 941 167 52

MV Total 87.124 96.251 305.237 443.687 10 45

F.Tractor 1.041 2.795 5.269 11.364 168 116

Grand Total 88.165 99.046 310.506 455.051 12 47

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

21Logo speaker’s institution Logo local institution

34

1719

14

63

6

0

8

16

24

32

40

0-05 06-10 11-15 16-20 21-25 26-30 > 31

Age Frequency in 2008

Sha

re

%

Vehicles Over 16 Years Age3.025.945 vehicles in 20083.684.050 vehicles in 2012

The Share in the Park -2008

> 11 Years of Age 49%

> 16 Years of Age 30%

Older Vehicles Emitting Higher GHG Emissions

Age Frequency OfThe Vehicle Fleet

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

22Logo speaker’s institution Logo local institution

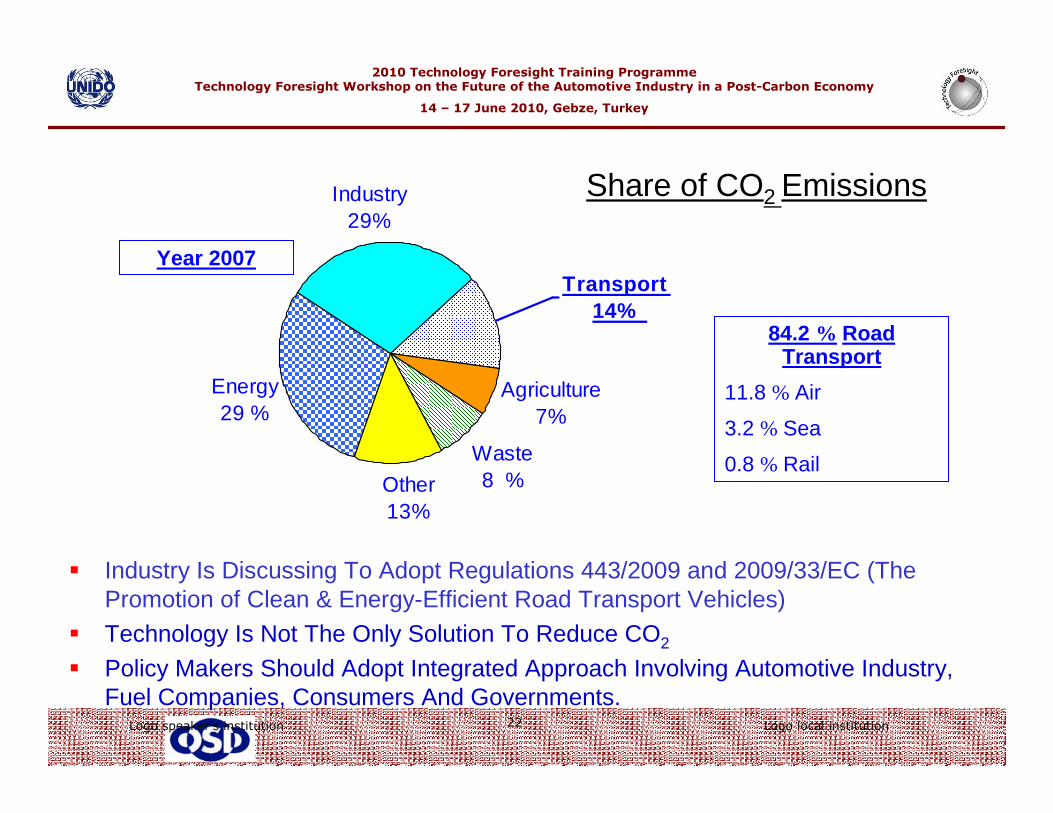

� Industry Is Discussing To Adopt Regulations 443/2009 and 2009/33/EC (The Promotion of Clean & Energy-Efficient Road Transport Vehicles)

� Technology Is Not The Only Solution To Reduce CO2

� Policy Makers Should Adopt Integrated Approach Involving Automotive Industry,Fuel Companies, Consumers And Governments.

Agriculture7%

Other13%

Industry29%

Waste8 %

Energy29 %

Transport 14%

84.2 % Road Transport

11.8 % Air

3.2 % Sea

0.8 % Rail

Year 2007

Share of CO2 Emissions

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

23Logo speaker’s institution Logo local institution

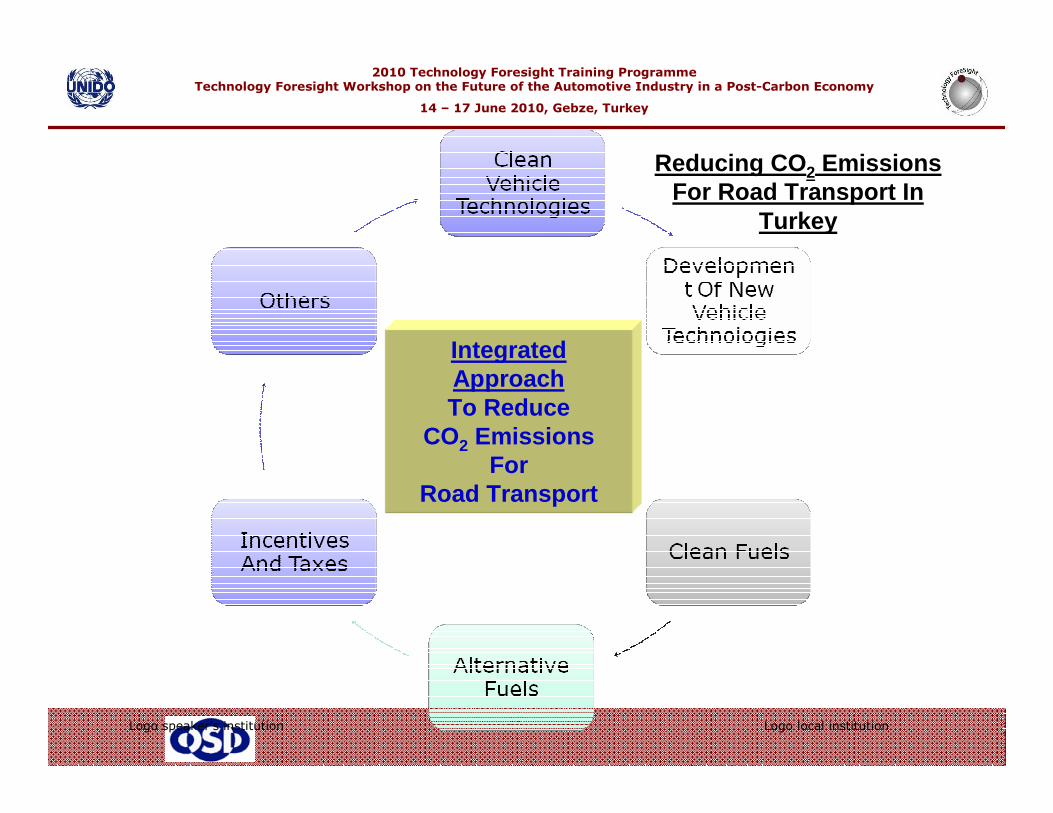

Integrated ApproachTo Reduce

CO2 Emissions For

Road Transport

Reducing CO 2 Emissions For Road Transport In

Turkey

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

24Logo speaker’s institution Logo local institution

● Clean Vehicle Technologies

� Gasoline And Diesel Direct Injection

� Multi Fuel Vehicles

� Hybrid Vehicles

� Usage Of Alternative Fuels And Hydrogen

� Electric Vehicles● Development Of New Vehicle Technologies

� Usage Of Light Material

� Improving Aerodynamic Features

� Improving Tyre Performance

� Designing Special City Bus And Logistic Vehicles

Reducing CO2 Emissions in MVI

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

25Logo speaker’s institution Logo local institution

● Clean Fuels

� Marketing High Quality Of Fuel For New Engine Technologies

� Marketing Fuels With Less Carbon Content To Become Widespread

� Monitoring Fuel Market for Sustainable Fuel Quality

● Alternative Fuels

� Producing Biofuels Utilizing Vacant Agricultural Areas Without Any Detrimental Effect On Food Production

� Producing 2nd Generation Biofuels From Waste Products

Additional Means to Reduce CO2 Emissions-I

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

26Logo speaker’s institution Logo local institution

● Incentives And Taxes

� Scrapping Incentives For Older Vehicles

� Inciting R&D For Emission Reduction, New Technologies And New Investment

� Tax Incentives For Fuels Needed For New Technologies To Become Widespread

� Tax Incentives For Biofuels R&D Production And Usage

� Road Taxation Of The Vehicles Independent Of Age

� Banning The Importation Of Used Vehicles Continuously

● Others

� Changing The Driver Behavior by Eco-driving

� Developing Infrastructure

� Balancing Modes In Transportation

Additional Means to Reduce CO2 Emissions-II

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

27Logo speaker’s institution Logo local institution

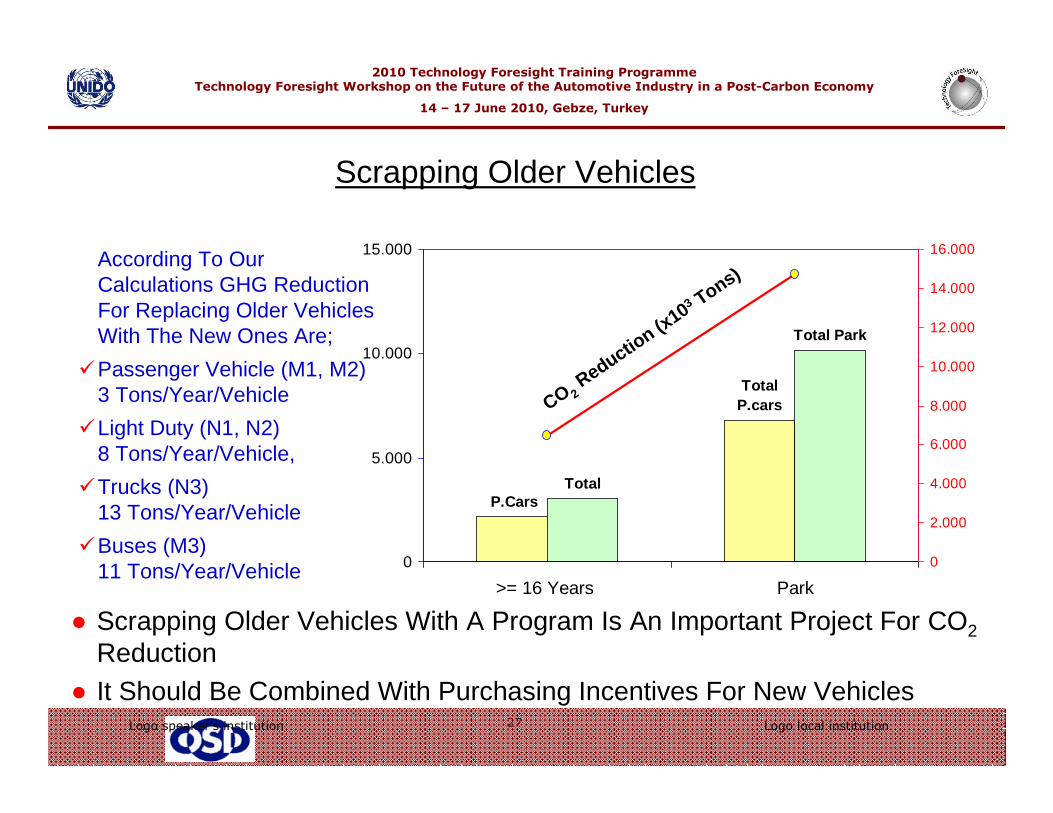

● Scrapping Older Vehicles With A Program Is An Important Project For CO2

Reduction ● It Should Be Combined With Purchasing Incentives For New Vehicles

Total P.cars

P.Cars

Total Park

Total

0

5.000

10.000

15.000

>= 16 Years Park

0

2.000

4.000

6.000

8.000

10.000

12.000

14.000

16.000According To Our Calculations GHG Reduction For Replacing Older Vehicles With The New Ones Are;

�Passenger Vehicle (M1, M2) 3 Tons/Year/Vehicle

�Light Duty (N1, N2) 8 Tons/Year/Vehicle,

�Trucks (N3) 13 Tons/Year/Vehicle

�Buses (M3) 11 Tons/Year/Vehicle

CO 2Reductio

n (x103 Tons)

Scrapping Older Vehicles

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

28Logo speaker’s institution Logo local institution

Ministry of Environment and Forestry (MEF)� Turkey’s Climate Change National Action Plan Is Being Developed To

Formulate Turkey’s National Strategies And Policies On Climate Change. On The Other Hand, National Energy Efficiency Law Is In Force Including Transport Sector.

Ministry Of Industry And Trade (MIT)� There Is A Strategy Document Of MIT� Strategy Document Together With Action Plan Adopting Our

Production Process And Products In Line With Climate Change

CO2 Policies

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

29Logo speaker’s institution Logo local institution

� Automotive Culture 50 years of production tradition� High Sense of Quality TQM, Lean Production, 6 Sigma� Labour Peace unionized work force / collective bargaining

since 1963� Qualified, Well-Trained, Motivated Labour Force at Competitive Cost� Flexible Working Hours 7.5 hours/shift - 3 shifts / day-6 days/week

Rate of Absenteeism < 1.5 %

� Entrepreneurship $ 10 billion worth of Investment� Partnership With World-Leading Manufacturers� Experienced Local Component Industry / Supplier Bas e� Unsaturated Domestic Market With High Potential of Demand� Geographic proximity to Europe and Asia� Developed Infrastructure & Services in the Region� Logistics, Energy, Transport, Banking,

Communication� Manufacturing Facilities With State-of-the-Art Tech nology� Tax treaty with the EU reduces tariffs on exports

The Assets & Opportunities

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

30Logo speaker’s institution Logo local institution

Weaknesses� Special Consumption Tax And VAT Raise The Domestic Purchase

Price Of A Vehicle To 60% - 100%+ Above The Pre-tax Price.

� Tax on Fuel is Also Very High; The Total Tax Burden Of On The Pre-tax Value Of The Fuel Price Is 195 % For The Gasoline And For The Diesel Fuel Is 134 % In 2009.

Threats� Preparations To Join The EU And Bring Industry In Line With Other

Members Could Erode Turkey’s Competitiveness

� Dependence On EU Markets

� Rapid Growth In China And India

Weaknesses & Threats

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

31Logo speaker’s institution Logo local institution

VisionTo Form A Developed And Competitive “Automotive Base" Where All Value-added Activities Are Globally Carried Out

– In The Short Term Production: Over 1,0 MillionExports: Over 0,8 Million Already Realized

– In The Medium Term Production: 2,0 MillionExports: 1,5 Million Can be Achieved

Direct Employment Of 600,000 Total Exports Of $ 50 Billion

By Means of Additional Investment At Least $ 5 Bil lion

Objectives of the Turkish Automotive Industry

2010 Technology Foresight Training ProgrammeTechnology Foresight Workshop on the Future of the Automotive Industry in a Post-Carbon Economy

14 – 17 June 2010, Gebze, Turkey

32Logo speaker’s institution Logo local institution

Thank you for your interest

Otomotiv Sanayii Derneğ[email protected]