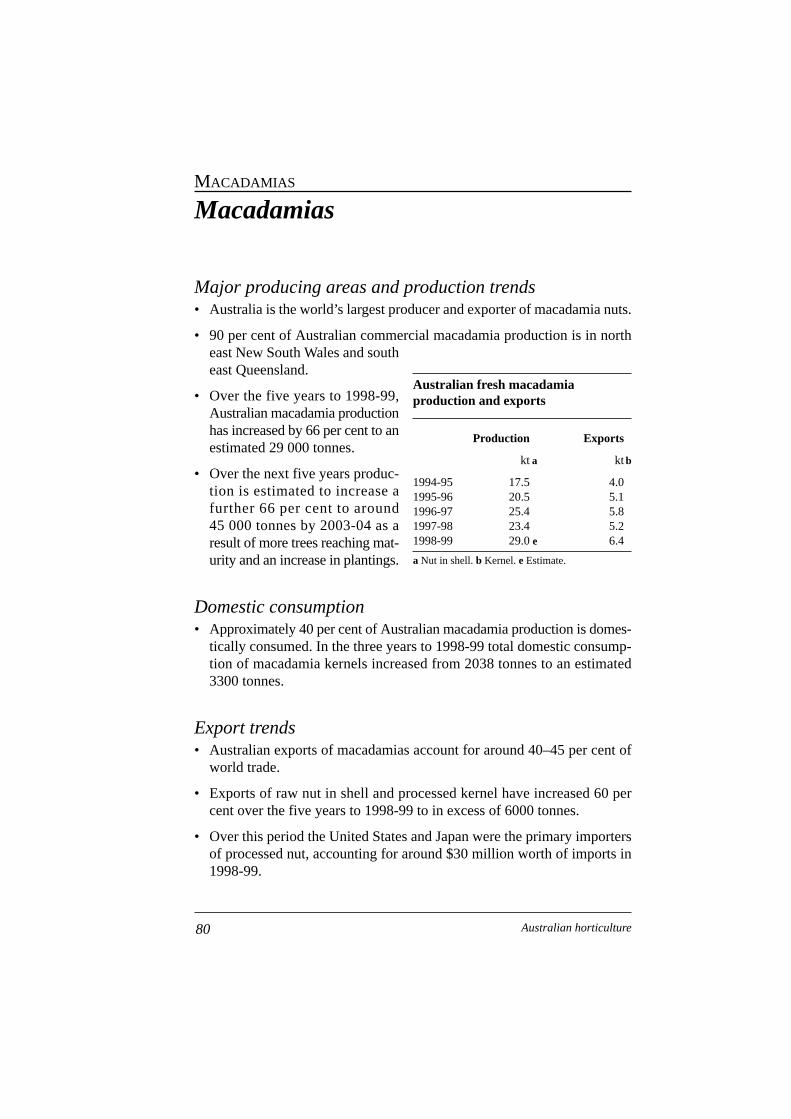

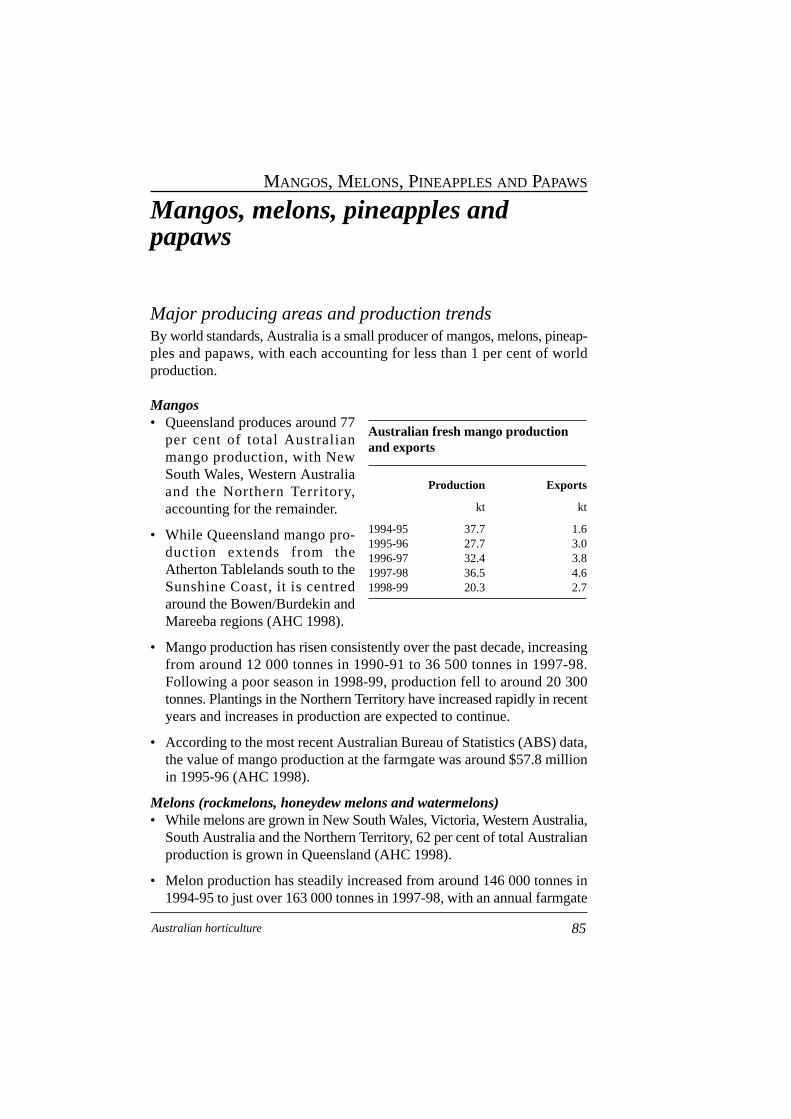

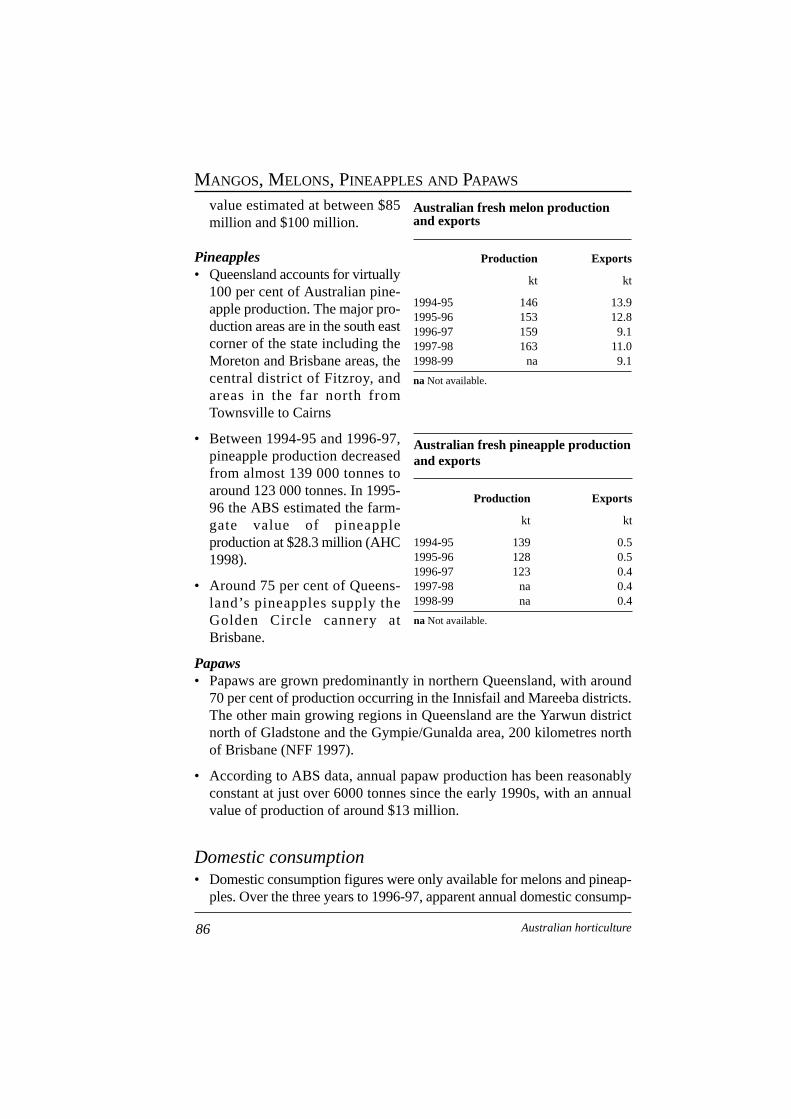

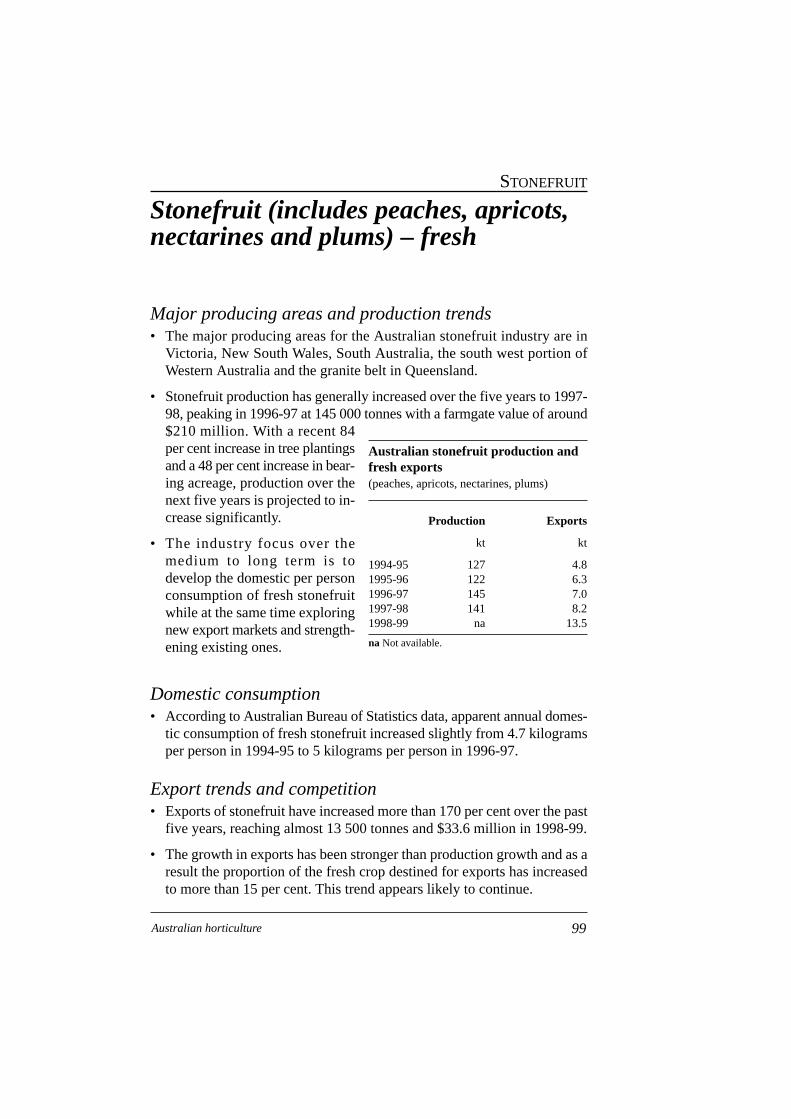

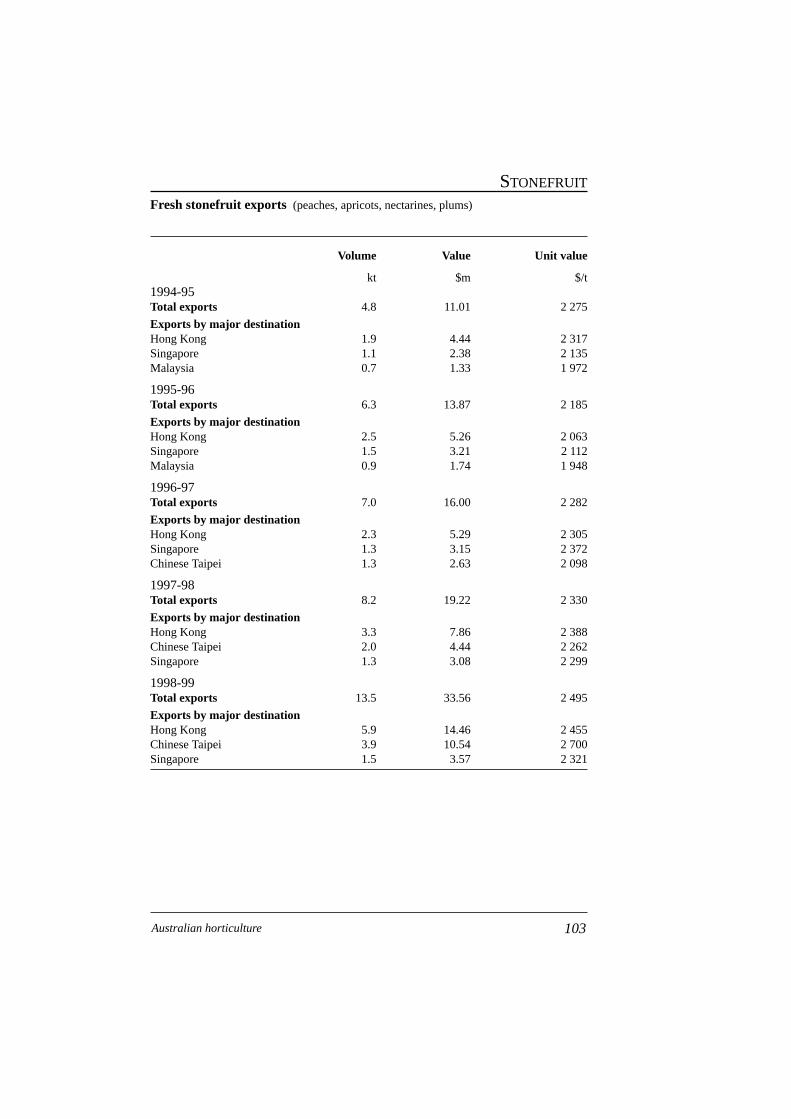

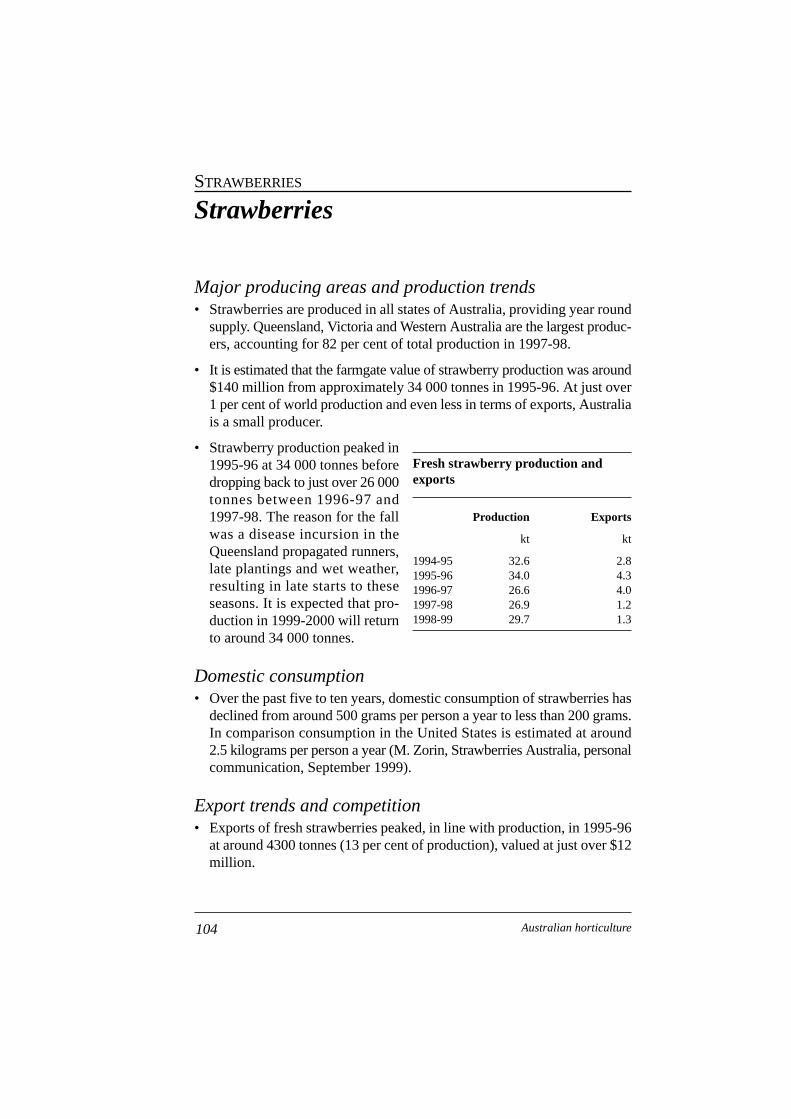

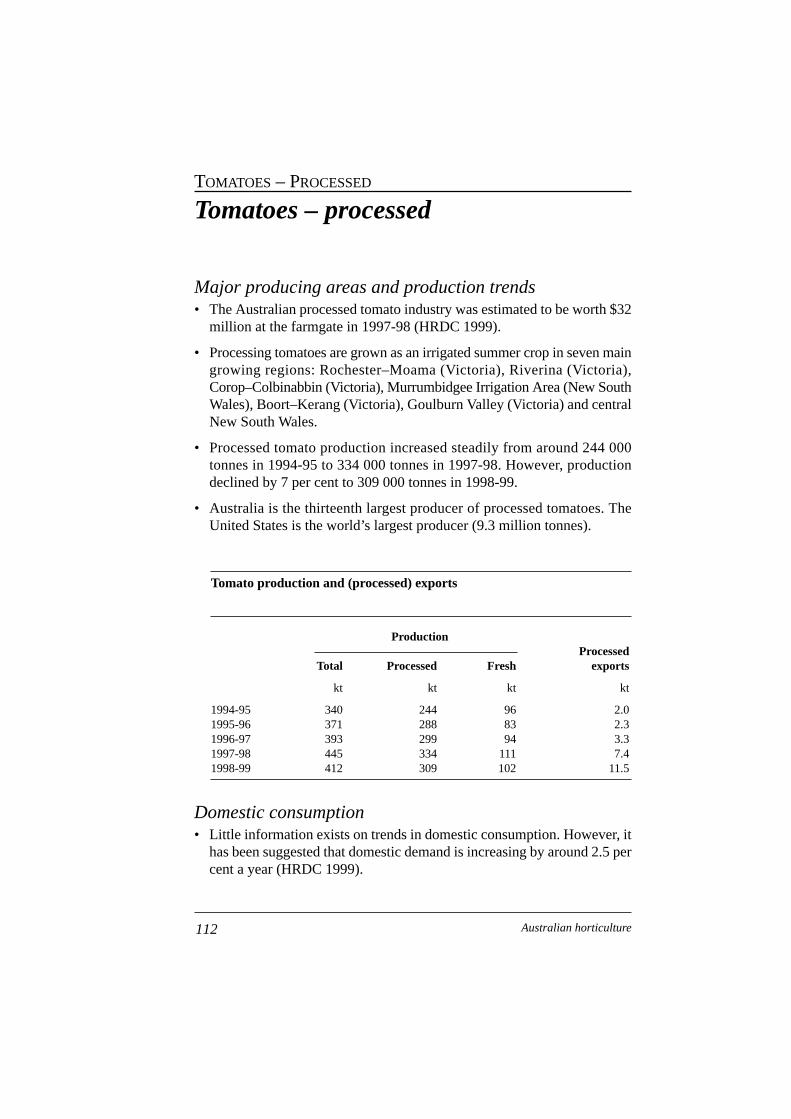

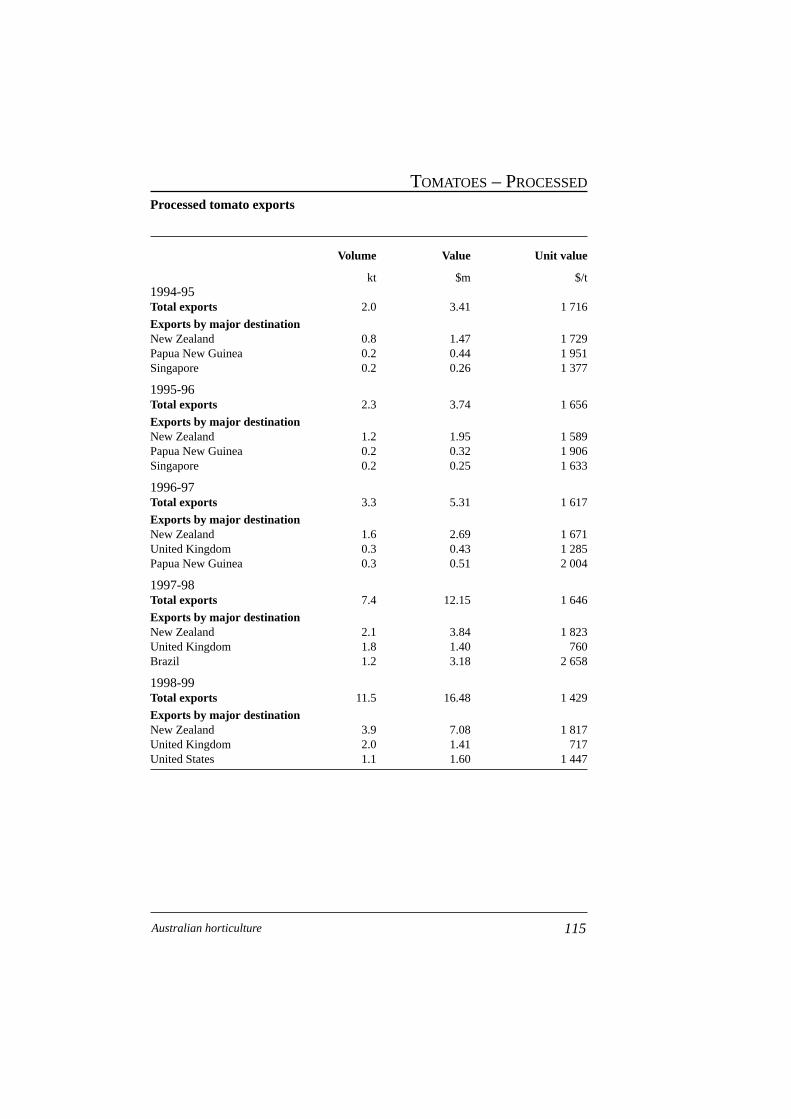

australian horticulture in the global...

TRANSCRIPT

AUSTRALIAN HORTICULTURE

IN THE GLOBAL

ENVIRONMENT

© ABARE, Horticultural Research and Development Corporation andAustralian Horticultural Corporation 2000

This work is copyright. The Copyright Act 1968 permits fair dealing forstudy, research, news reporting, criticism or review. Selected passages, tablesor diagrams may be reproduced for such purposes provided acknowledg-ment of the source is included. Major extracts or the entire document maynot be reproduced by any process without the written permission of theExecutive Director, ABARE, or the Managing Director of the HRDC or AHC.

ISBN 0 642 76406 9

Australian Bureau of Agricultural and Resource EconomicsGPO Box 1563 Canberra 2601

Telephone +61 2 6272 2000 Facsimile +61 2 6272 2001Internet www.abareconomics.com

ABARE is a professionally independent government economic researchagency.

Horticultural Research and Development CorporationLevel 6, 7 Merriwa Street, Gordon 2072

Telephone +61 2 9418 2200 Facsimile +61 2 9418 1352Internet www.horticulture.com.au

HRDC is a national organisation that manages, coordinates and invests inresearch and development which advances Australian horticulture.

Australian Horticultural CorporationLevel 11, 51 Druitt Street, Sydney 2000

Telephone: +61 2 9264 9966 Facsimile +61 2 8267 4199Internet www.horticulture.com.au

AHC provides innovative marketing solutions and support programs to theAustralian horticulture industry.

The views expressed and conclusions reached in this report are those ofABARE. The HRDC or AHC shall not be responsible in any way whatso-ever to any person who relies in whole or in part on the contents of this report.

ABARE project 1749 HRDC project AH99001

Foreword

This report is part of a project titled ‘Australian horticulture in the next WTOround’. An initiative of the Horticultural Market Access Committee andmanaged by the Australian Horticultural Corporation (AHC) and theHorticultural Research and Development Corporation (HRDC), funding forthe project was provided by the AusHort R&D Committee of the HRDC.

The report is divided into three parts. The first part provides an overview ofAustralian horticultural production and summarises the key issues associ-ated with market access for trade negotiation. The second part provides casestudy analysis of trade policy for selected major markets. Part three detailsa number of Australian horticultural industries and provides an effectivereference of over twenty fresh and manufactured fruit and vegetable prod-ucts.

The World Trade Organisation negotiations in Seattle last year provided anopportunity to progress market access and domestic support issues arisingfrom the Uruguay Round in 1994. The results of the analysis reported in thisstudy formed an important part of the briefing provided to Australian nego-tiators in their pursuit of horticultural trade prospects. A range of trade poli-cies restrict access to many important Australian horticultural export markets.Key issues considered in this report are tariffs, sanitary and phytosanitarymeasures and international support arrangements.

This report also provides an effective industry resource, profiling a numberof industries and their related products. It complements the annual AustralianHorticultural Statistics Handbook by providing in-depth commentary ontopics such as major producing areas and production trends; domestic con-sumption; export trends and competition; state/regional export contributions;market access issues; and technical barriers to trade.

BRIAN S. FISHER MARK NAPPER

Executive Director Managing DirectorABARE Australian Horticultural Corporation

February 2000

iiiAustralian horticulture

Acknowledgments

The Agricultural Economics Section of the Industries Branch of ABAREwas commissioned by the project management committee to undertake thisreport. The research was undertaken by Roger Van Hilst, Catherine Rees andCharmayne O’Rourke and has benefited from the input of Vince O’Donnell,Neil Andrews and Ivan Roberts.

Considerable assistance was also provided by the project managementcommittee of Mark Napper and James Kellaway (Australian HorticulturalCorporation), Kim James (Horticultural Research and DevelopmentCorporation), Margaret Milgate (Queensland Fruit and Vegetable Growers),Bob Curren (Australian Citrus Growers) and Jon Durham (Australian Appleand Pears Growers Association).

The authors also acknowledge information provided by the AustralianQuarantine and Inspection Service; Department of Foreign Affairs and Trade;Agriculture, Fisheries and Forestry – Australia; and the many industries asso-ciated with the contents of this report.

iv Australian horticulture

Contents

Part 1: Australian horticulture and market access issues

Introduction 1Australian horticultural production 1Australian export trends and competition 1Australian support arrangements 3

Horticulture and multilateral trade negotiations 4Summary of issues 5Implications for Australian horticulture in the context ofnegotiations 8

Part 2: Trade policy analysis – case studies 10European Union 11United States 18Japan 22South Korea 25Indonesia 28China 30Chinese Taipei 32

Part 3: Industry profiles 35Almonds 36Apples and pears – fresh 40Avocados 48Canning fruit 52Cherries 56Chestnuts 60Citrus (fresh) and citrus juice 63Custard apples 71Cut flowers 74Macadamias 80

vAustralian horticulture

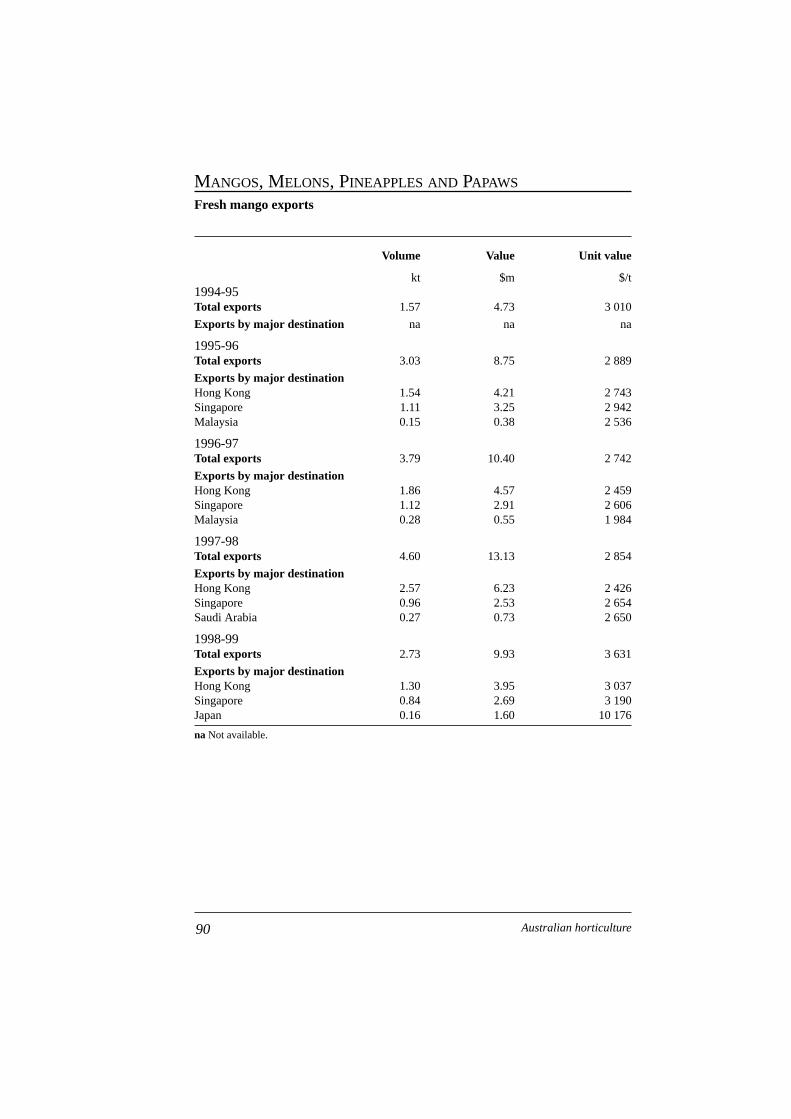

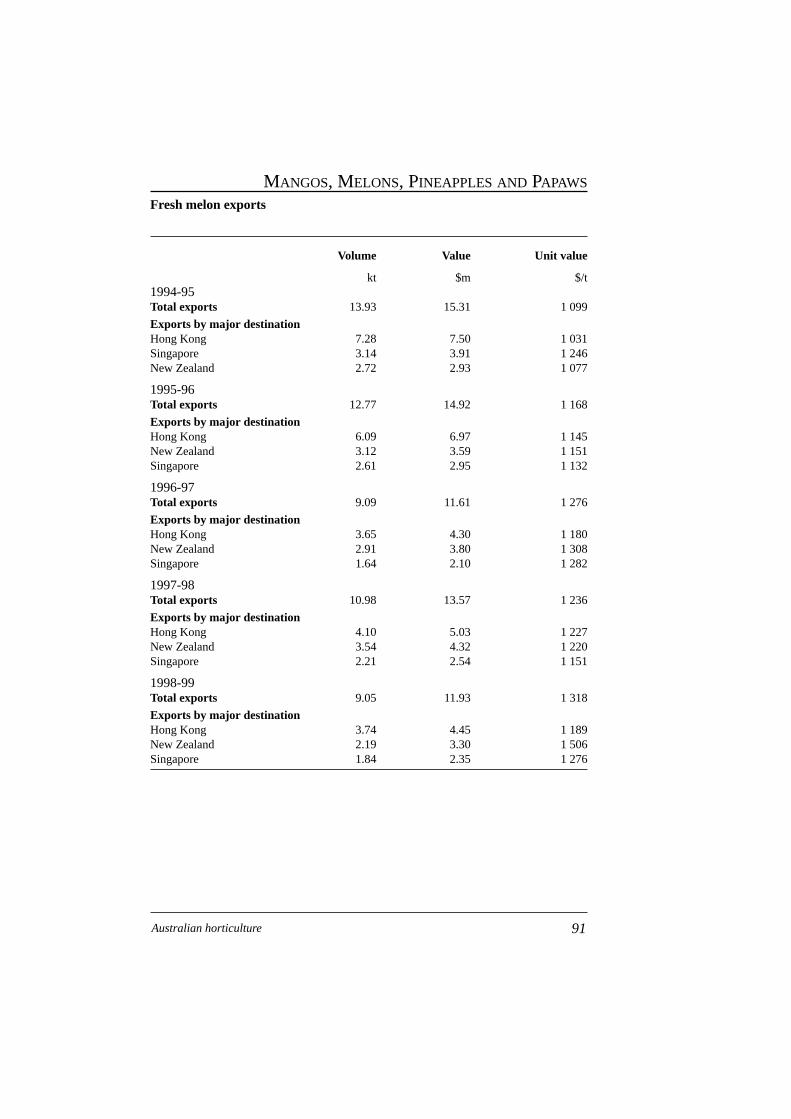

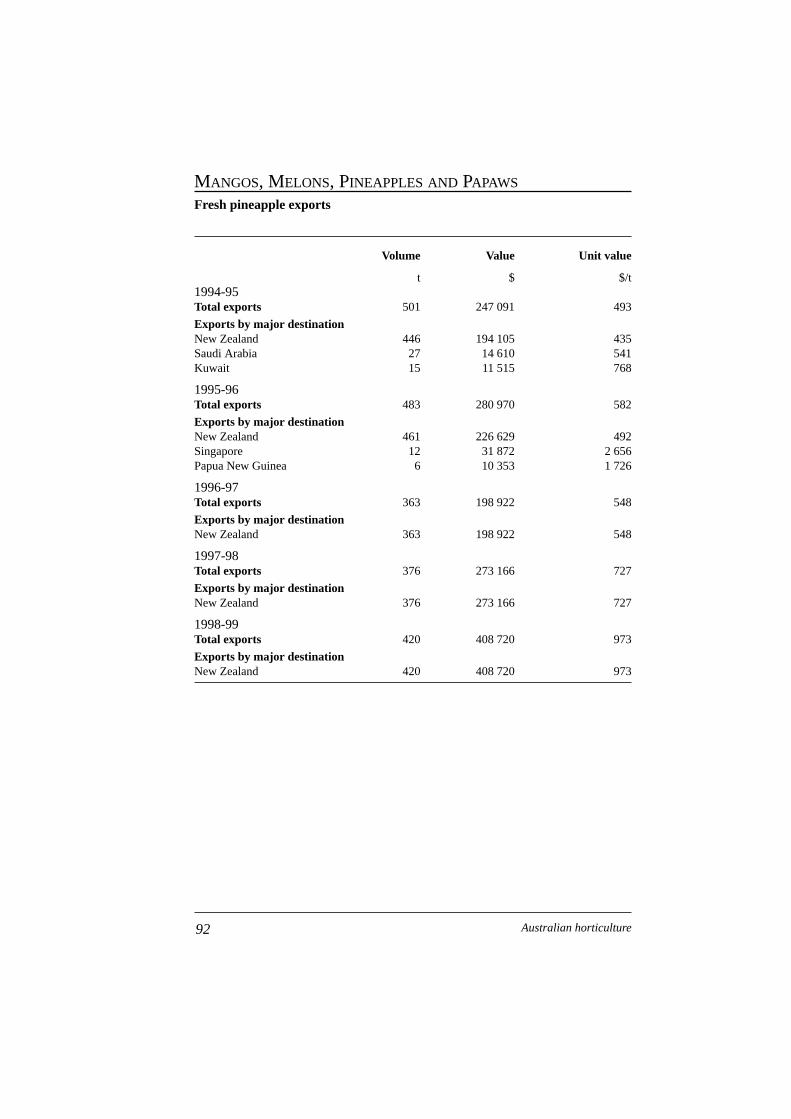

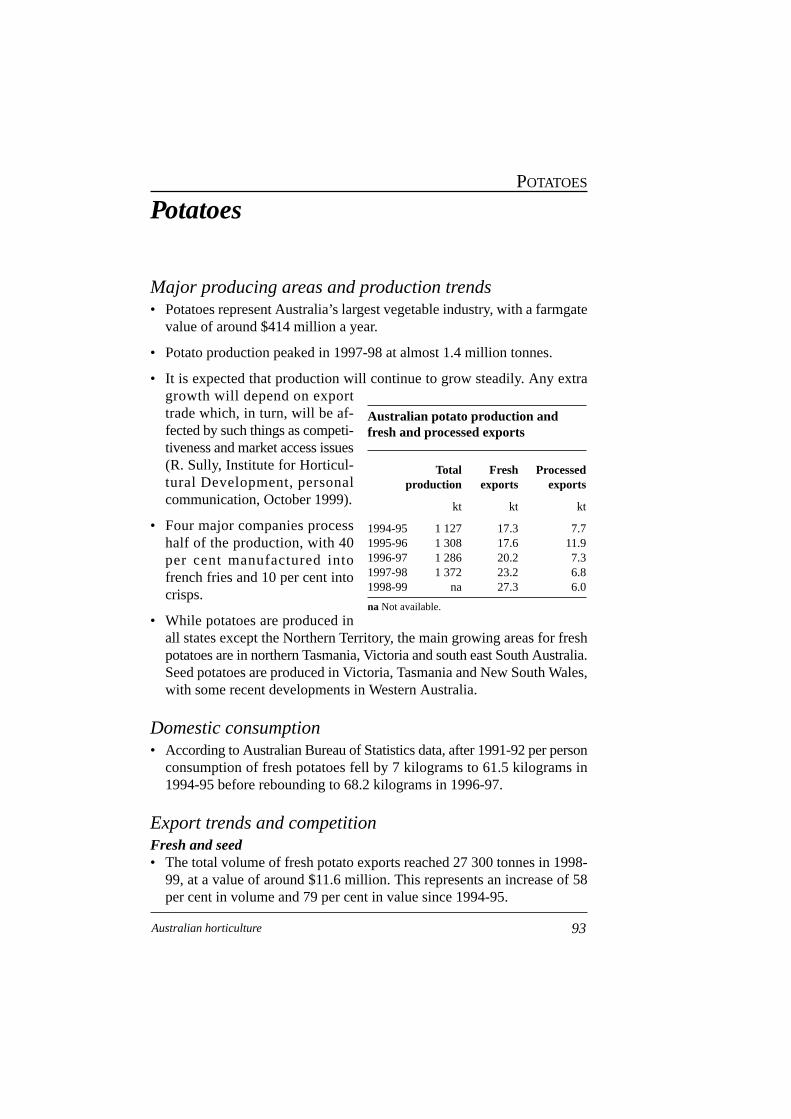

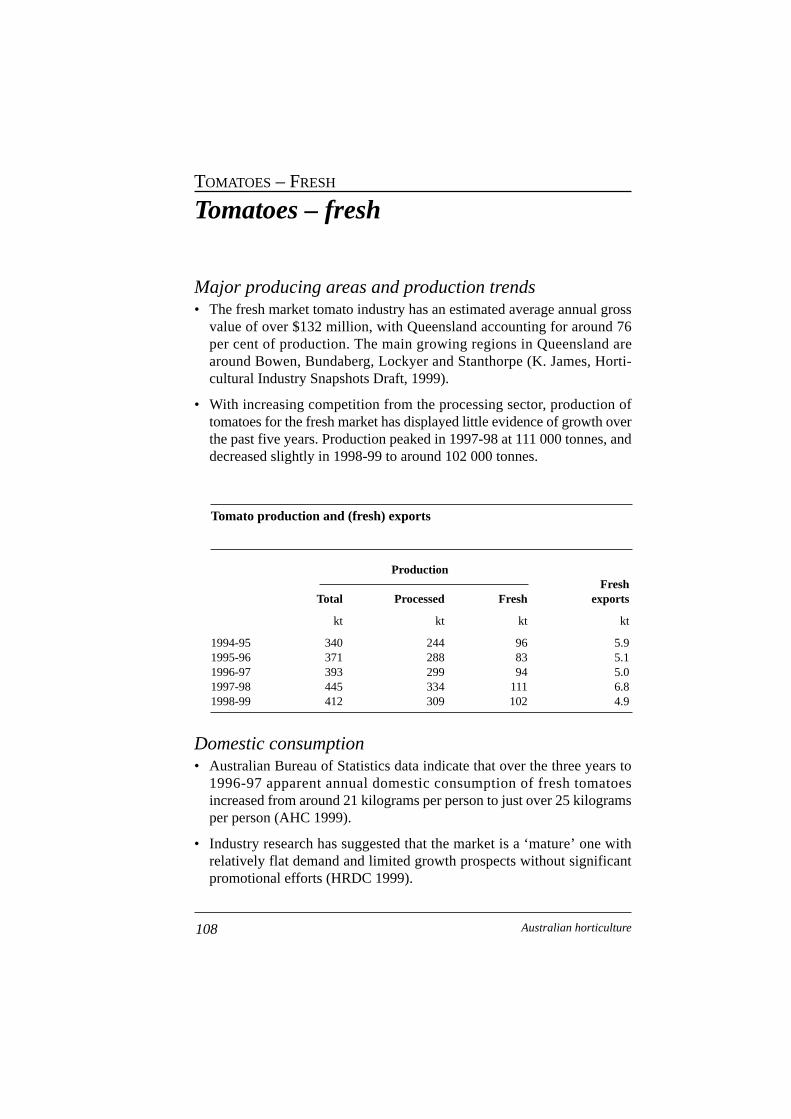

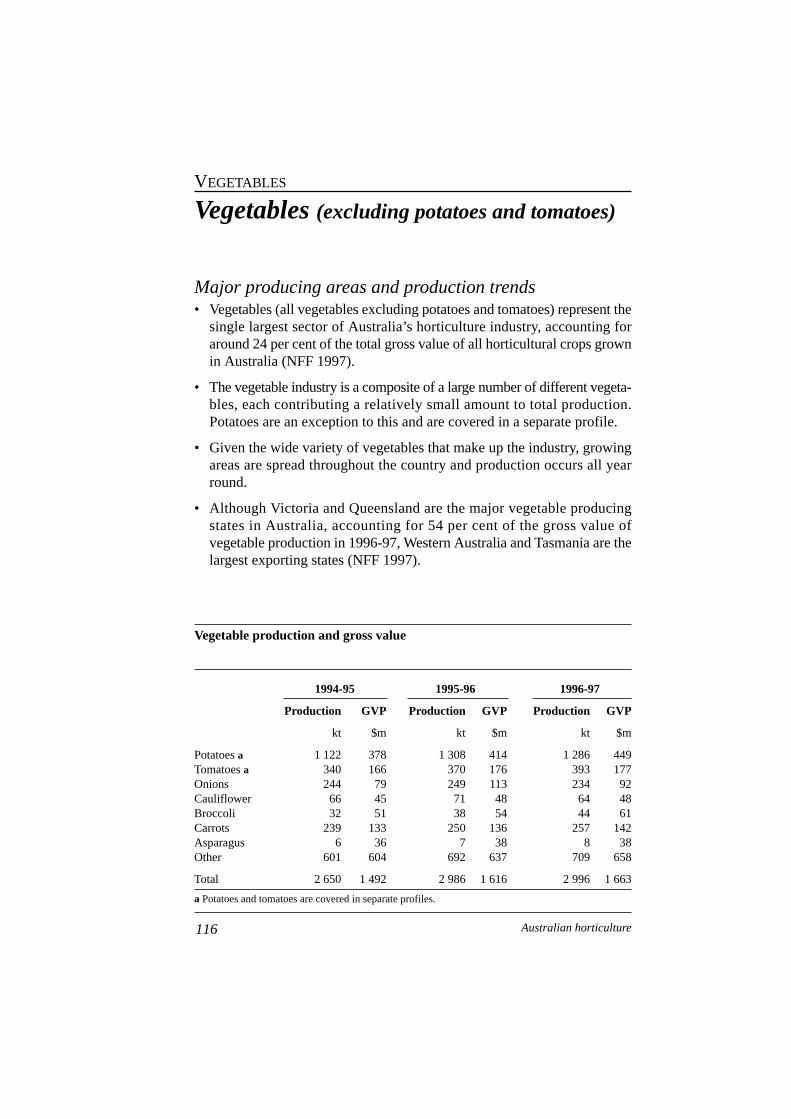

Mangos, melons, pawpaws and pineapples 85Potatoes 93Stonefruit – fresh 99Strawberries 104Tomatoes – fresh 108Tomatoes – processed 112Vegetables (excluding potatoes and tomatoes) 116

References 124

FiguresA Gross value of Australian agriculture 2B Gross value of Australian horticultural production, by sector,

1997-98 2C Gross value of Australian horticultural production, by state,

1997-98 2

vi Australian horticulture

Australian horticulture andmarket access issues

IntroductionHorticultural policy measures in countries that are of strategic importanceto Australian horticultural exporters and the future growth of the industryare discussed in this report. Industry profiles for key Australian horticulturesectors are also presented in part 3.

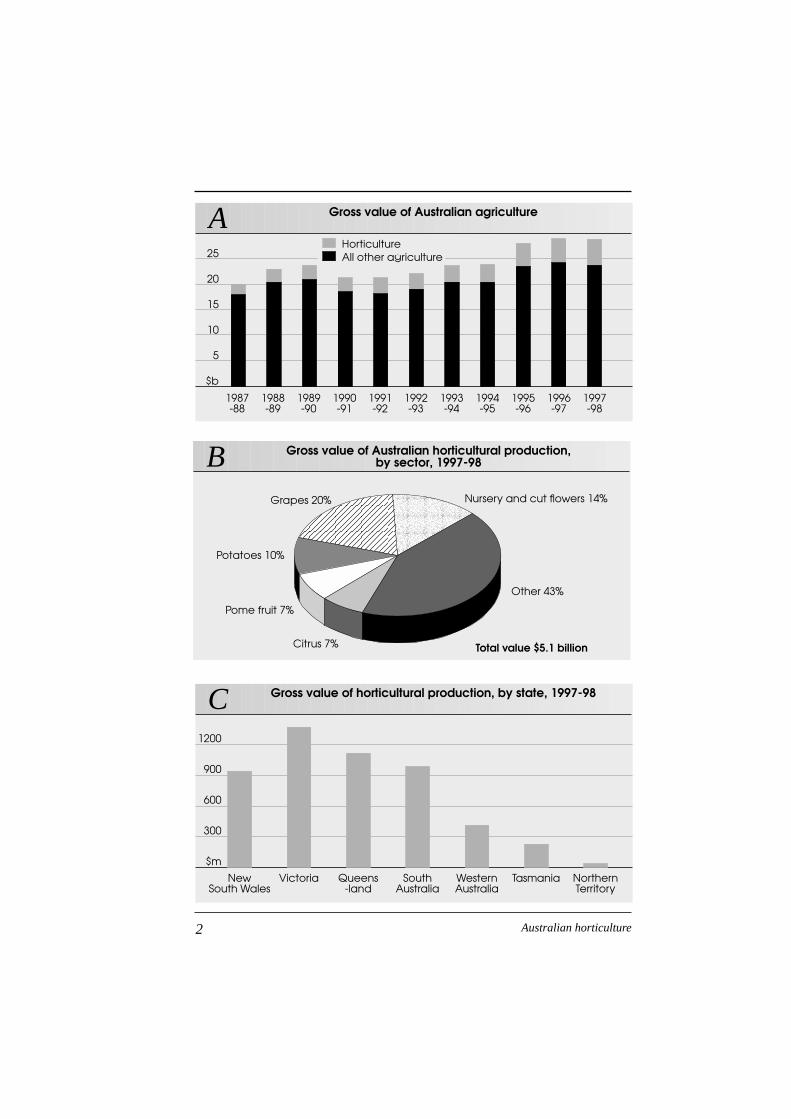

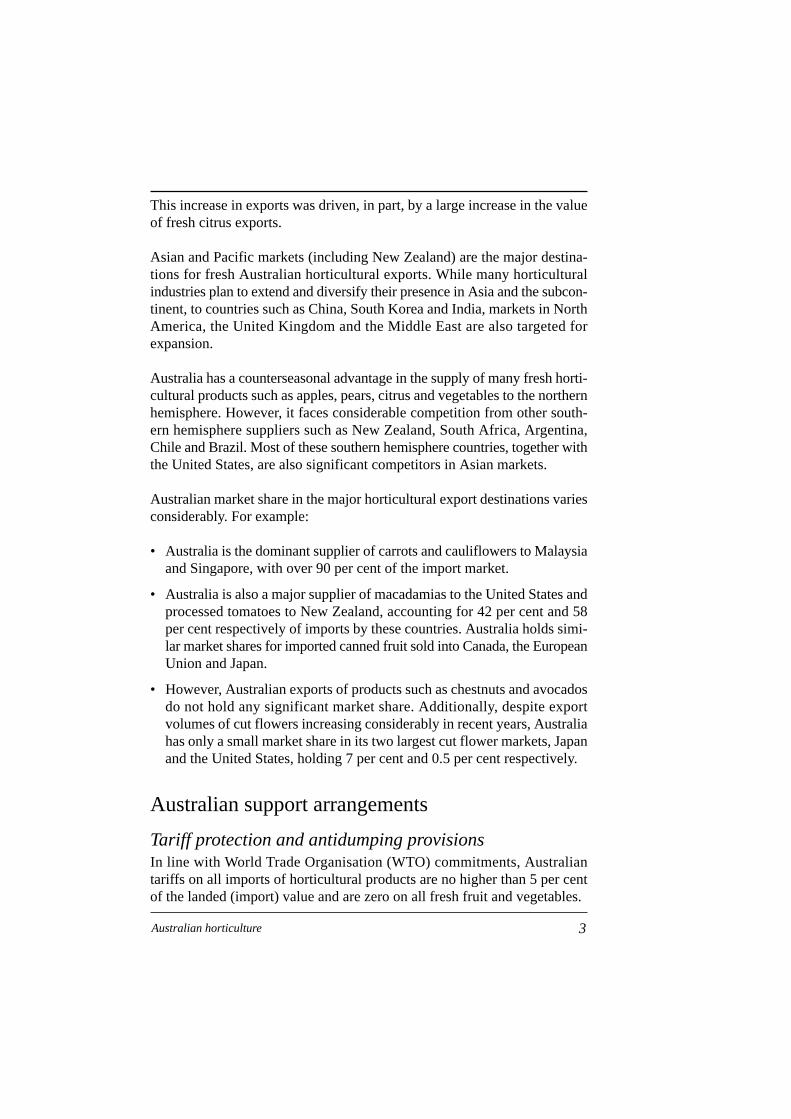

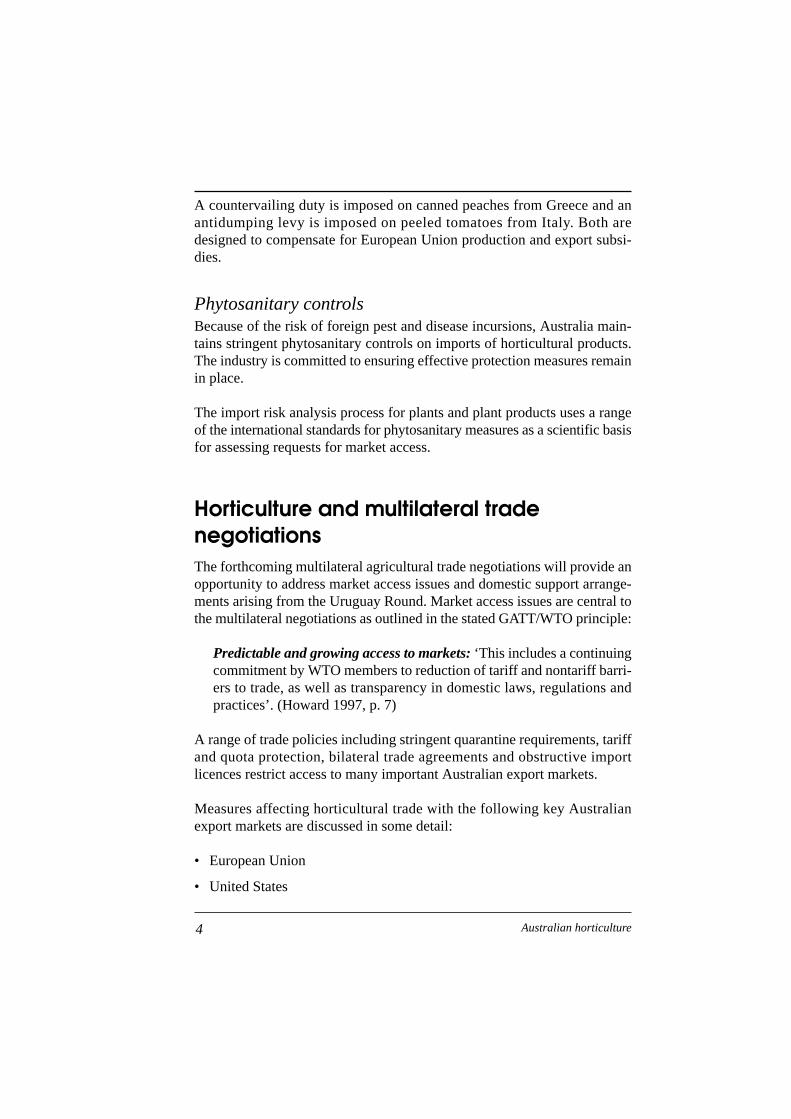

Australian horticultural productionBetween 1987-88 and 1997-98 the gross value of horticulture productionincreased by 142 per cent to around A$5.1 billion (however, this figureincludes nursery production, of A$695 million, which was not available in1987-88). Over the same period, the total value of Australian agricultureproduction increased by just over 40 per cent to around A$28 billion (figureA). Consequently, the gross value of Australian horticultural production asa proportion of total agricultural production increased steadily from around11 per cent to 16 per cent (ABS 1998, 1999).

The major Australian horticulture sectors covered in this report, by value,are nursery and cut flowers, potatoes, pome fruits (apples and pears) andcitrus (figure B), which together accounted for 38 per cent of the value ofall horticultural production in 1997-98 (ABS 1999). While grapes are notincluded in this report, they alone accounted for 20 per cent of the value ofhorticulture production in 1997-98.

Although horticultural crops are grown throughout Australia, the majorityof production occurs in Victoria, South Australia, Queensland and New SouthWales (figure C). Together, these four states accounted for around 87 percent of the value of total fruit and vegetable production in 1997-98 (ABS1999).

Australian export trends and competitionIn the ten years to 1998-99, the value of Australian horticultural exportsincreased by 112 per cent to A$1.2 billion. This reflects a large rise in freshfruit exports, which rose by 270 per cent to A$348 million over that period.

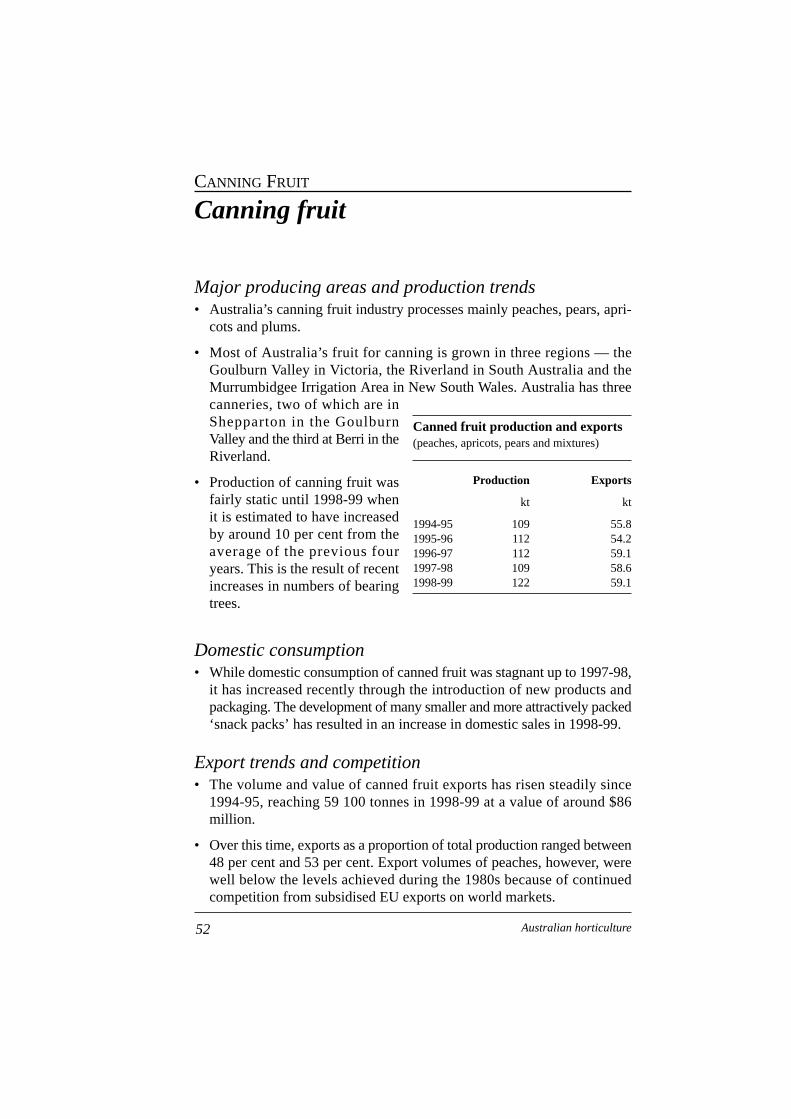

1Australian horticulture

PART 1

2 Australian horticulture

Gross value of Australian agricultureA

1987-88

1988-89

1989-90

1990-91

1991-92

1992-93

1993-94

1994-95

1995-96

1996-97

1997-98

$b

5

10

15

20

25HorticultureAll other agriculture

Gross value of Australian horticultural production,by sector, 1997-98B

Citrus 7%

Pome fruit 7%

Potatoes 10%

Grapes 20% Nursery and cut flowers 14%

Other 43%

Total value $5.1 billion

Gross value of horticultural production, by state, 1997-98C

$m

300

600

900

1200

NorthernTerritory

TasmaniaWesternAustralia

SouthAustralia

Queens-land

VictoriaNewSouth Wales

This increase in exports was driven, in part, by a large increase in the valueof fresh citrus exports.

Asian and Pacific markets (including New Zealand) are the major destina-tions for fresh Australian horticultural exports. While many horticulturalindustries plan to extend and diversify their presence in Asia and the subcon-tinent, to countries such as China, South Korea and India, markets in NorthAmerica, the United Kingdom and the Middle East are also targeted forexpansion.

Australia has a counterseasonal advantage in the supply of many fresh horti-cultural products such as apples, pears, citrus and vegetables to the northernhemisphere. However, it faces considerable competition from other south-ern hemisphere suppliers such as New Zealand, South Africa, Argentina,Chile and Brazil. Most of these southern hemisphere countries, together withthe United States, are also significant competitors in Asian markets.

Australian market share in the major horticultural export destinations variesconsiderably. For example:

• Australia is the dominant supplier of carrots and cauliflowers to Malaysiaand Singapore, with over 90 per cent of the import market.

• Australia is also a major supplier of macadamias to the United States andprocessed tomatoes to New Zealand, accounting for 42 per cent and 58per cent respectively of imports by these countries. Australia holds simi-lar market shares for imported canned fruit sold into Canada, the EuropeanUnion and Japan.

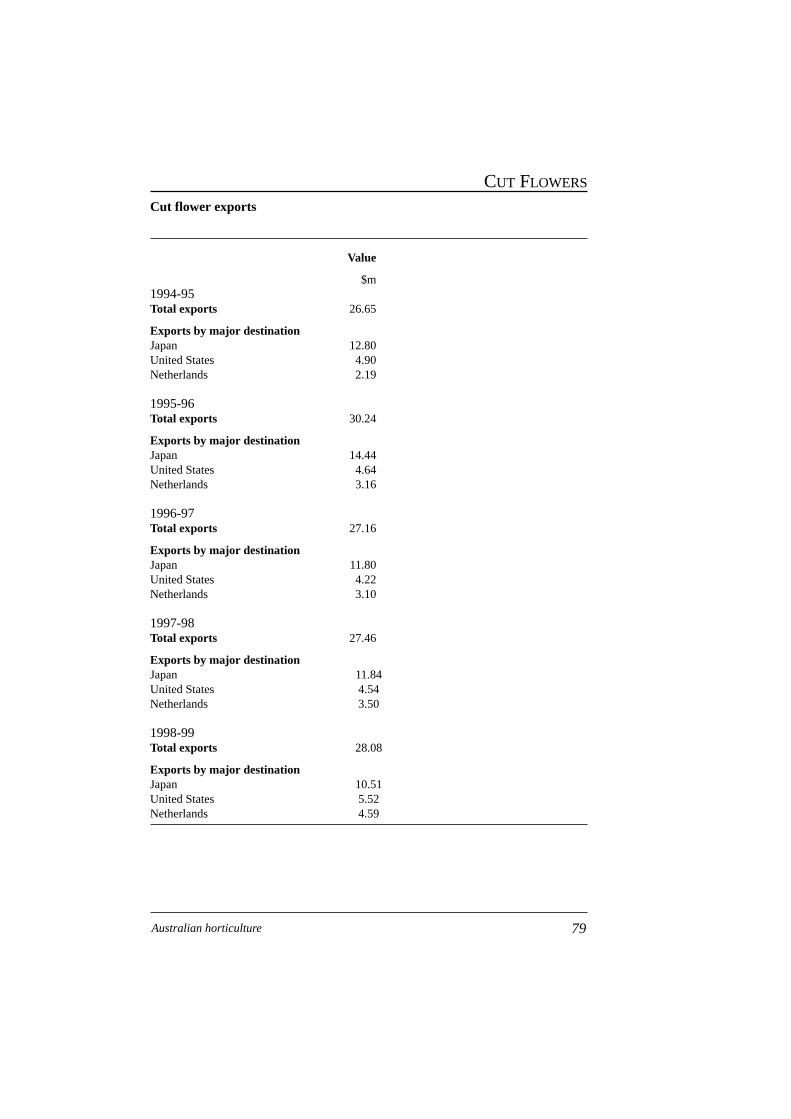

• However, Australian exports of products such as chestnuts and avocadosdo not hold any significant market share. Additionally, despite exportvolumes of cut flowers increasing considerably in recent years, Australiahas only a small market share in its two largest cut flower markets, Japanand the United States, holding 7 per cent and 0.5 per cent respectively.

Australian support arrangements

Tariff protection and antidumping provisionsIn line with World Trade Organisation (WTO) commitments, Australiantariffs on all imports of horticultural products are no higher than 5 per centof the landed (import) value and are zero on all fresh fruit and vegetables.

3Australian horticulture

A countervailing duty is imposed on canned peaches from Greece and anantidumping levy is imposed on peeled tomatoes from Italy. Both aredesigned to compensate for European Union production and export subsi-dies.

Phytosanitary controlsBecause of the risk of foreign pest and disease incursions, Australia main-tains stringent phytosanitary controls on imports of horticultural products.The industry is committed to ensuring effective protection measures remainin place.

The import risk analysis process for plants and plant products uses a rangeof the international standards for phytosanitary measures as a scientific basisfor assessing requests for market access.

Horticulture and multilateral tradenegotiations The forthcoming multilateral agricultural trade negotiations will provide anopportunity to address market access issues and domestic support arrange-ments arising from the Uruguay Round. Market access issues are central tothe multilateral negotiations as outlined in the stated GATT/WTO principle:

Predictable and growing access to markets: ‘This includes a continuingcommitment by WTO members to reduction of tariff and nontariff barri-ers to trade, as well as transparency in domestic laws, regulations andpractices’. (Howard 1997, p. 7)

A range of trade policies including stringent quarantine requirements, tariffand quota protection, bilateral trade agreements and obstructive importlicences restrict access to many important Australian export markets.

Measures affecting horticultural trade with the following key Australianexport markets are discussed in some detail:

• European Union

• United States

4 Australian horticulture

• Japan

• Indonesia

• South Korea

• China and

• Chinese Taipei.

These markets have been selected for case study analysis because they arecharacterised by one or more of the following import protection measures:

• high applied and/or bound tariffs

• stringent sanitary and phytosanitary regulations and

• trade distorting domestic support arrangements.

Other important markets for Australian horticultural produce, such asSingapore and Hong Kong, are not included in the case studies because oftheir relatively open access.

Summary of issues

TariffsProhibitively high tariff rates and large discrepancies between bound andapplied tariff duties are of major concern to Australian horticultural produc-ers. Addressing tariff concerns will be a top priority for Australian negotia-tors. However, not all countries have high tariff barriers in place and not allhorticultural products are subject to exorbitant tariff rates. So while levelsof protection for horticultural exports are high relative to some other indus-tries, this protection is largely uneven across countries and commodities. Inaddition, tariff quotas are in place for some export destinations such as theEuropean Union. However, there is no evidence to suggest that these tariffquotas are restricting Australian horticultural exports at this stage.

A bound tariff is the maximum tariff rate that a WTO member can apply toimported goods. It is a ceiling rate of duty, which a signatory country hasundertaken not to exceed except through negotiations, with compensationfor affected trading partners. The applied tariff rate is the actual rate that isapplied to imports at a particular time. In many cases, bound tariffs exceedby very large amounts the actual tariffs applied by countries. Reductions in

5Australian horticulture

tariff barriers will be illusory if cuts in the bound rates — which are the basisfor both negotiation and commitments — do not reduce the actual tariffapplied (ABARE 1999).

For the purposes of this report, relatively low tariff levels (below 10 per cent)are not identified, as they are not considered to be significant impedimentsto trade given the greater level of trade restraints found in other markets.

Sanitary and phytosanitary regulationsWhile issues relating to sanitary and phytosanitary regulations are outsidethe Uruguay Round Agreement on Agriculture, their existence has an impor-tant bearing on market access. Therefore, any strategy by horticulturalexporters to expand effective market access must take into account the barri-ers posed by quarantine regulations. Thus, sanitary and phytosanitary regu-lations can be expected to influence various countries’ approaches to themultilateral negotiations as well as ongoing bilateral negotiations betweencountries (ABARE 1999).

The most important quarantine issue affecting access for Australian horti-cultural products relates to regulations designed to protect domestic indus-tries from incursions of fruit fly species endemic to Australia. This and otherquarantine related issues are widespread across Australian horticulturalcommodities and extend beyond the range of case study countries consid-ered here. Further bilateral negotiations, combined with cooperative effortsbetween the relevant domestic organisations, will be crucial to reducing quar-antine related trade obstacles in the future.

Domestic support and export subsidiesDomestic support in importing countries can greatly affect market opportu-nities for Australian horticulture, even if there is relatively liberal access tothose markets. Also domestic support in competing exporting countries canresult in the generation of surpluses that compete on world markets withAustralian products. In some instances these exports may be assisted throughdirect export subsidies as well as domestic subsidies.

Domestic support can take many forms including government subsidies toincrease prices to farmers for their products, subsidies for farm inputs suchas water or subsidisation of capital infrastructure. In some instances thesupport can be regionally based within markets to assist farmers to maintain

6 Australian horticulture

regional employment or regional landscapes (such as vineyard or olive grovelandscapes). All of these subsidies tend to increase domestic production,which can impinge on market opportunities for imports.

Export subsidies are among the most distorting of support arrangements, anda reduction in these arrangements would bring significant benefits to theAustralian horticulture industry. However, any negotiated benefits would belimited if there were a reorientation toward other distorting support meth-ods that would further inhibit horticultural exports from Australia.

The following is a summary of the key policy arrangements identified asbeing of potential concern to the Australian horticulture industry in its effortsto expand trade. These are discussed in more detail in the following sections.

• The European Union enforces strict food safety standards and has hightariffs on many commodities. EU farmers receive a range of governmentsupports under the Common Agricultural Policy that include compensa-tion payments for product withdrawal, direct production subsidies, exportsubsidies and rootstock adjustment programs. In addition, Europeanproducers of processed horticultural goods benefit from manufacturingsubsidies.

• The United States has in place a number of arrangements that impedetrade in horticultural products. These include: tariffs that are considerablyhigher than Australian levels; the North American Free Trade Agreementwhich favors imports from Canada and Mexico over other trading nations;and strict quarantine controls for some products that impose fumigationcosts on exporting countries, even when there is no disease or pest risk.The United States has a range of indirect industry support measures, includ-ing a comparatively high specific import duty on orange juice.

• Japan has relatively high tariff rates on some imported horticultural prod-ucts. It also enforces stringent quarantine controls on all horticulturalimports, considering access on the basis of each variety being a separateproduct.

• In Indonesia, there is a large discrepancy in the applied and bound tariffrates on most horticultural imports.

• Only a limited range of horticultural products have been granted accessto South Korea. Once granted, stringent quarantine measures and a hightariff quota system on fruit and vegetables restrict this access. South Koreaadopts a ‘one product at a time per country’ policy for assessing access.

7Australian horticulture

• Official access to markets in China, when achieved, is likely to be impededby sanitary and phytosanitary measures on imports of various fruits andvegetables. Gaining access takes considerable time, as China’s policy isto assess just one product at a time per country. To date Australia has onlybeen granted access to China for Tasmanian apples. China also has veryhigh import duties of around 30 per cent. China’s accession to the WTOin the near future is likely to result in reductions to these trade barriers.

• Chinese Taipei applies high, two-tier seasonal tariffs, import quotas, prohi-bitions and strict quarantine measures on many horticultural imports. Arecently adopted chemical residue testing procedure has also delayed horti-cultural exports because of increased paperwork and an as yet incompletelist of safe chemicals registered with Chinese Taipei officials. It is expectedthat Chinese Taipei will join the WTO following China’s accession. Thisis likely to result in reduced trade barriers and greater transparency intrade procedures.

Implications for Australian horticulture in thecontext of negotiationsThis study identifies a number of impediments to market access facingAustralian exports of horticultural products. The main constraint on tradeappears to be quarantine restrictions imposed by importing countries. ForAustralian product to gain access to markets that have been restricted on thebasis of quarantine it will be necessary for Australian authorities to negoti-ate protocols with the relevant authorities in importing countries. WhereAustralia or even discrete regions within Australia are not affected by thepests or diseases of concern, failure of the importing country to allow importsfrom Australia would appear to be unjustified.

Australian access to many world markets is also restricted by high tariffs forhorticultural products. The main markets of concern to the Australian indus-try include Thailand, South Korea, China and Chinese Taipei. If Australianhorticultural exports are to gain or improve access to these markets it willbe essential that future WTO agriculture negotiations result in significantcuts to tariffs.

One of the main domestic support arrangements affecting horticulture wouldappear to be the European Union’s policies for fresh and processed fruit andvegetables. However, domestic support commitments under the WTOUruguay Round Agreement on Agriculture are for agriculture as a whole

8 Australian horticulture

rather than for individual products or product groupings (such as horticul-ture). This, together with other limitations of the domestic support commit-ments, such as exemptions for decoupled support and production limitingarrangements, mean that domestic support commitments are relatively weak(Roberts et al. 1999).

If the distortions to trade from domestic support policies are to be reduced,it will be necessary for future negotiations to agree to effective disciplineson domestic support. This will include ensuring that only properly decou-pled support measures are excluded from negotiated reductions and havingcommitments on domestic support based on individual products, or at themost, groups of closely related products. These requirements are as relevantto horticultural products as they are to other agricultural commodities.

9Australian horticulture

Trade policy analysis – case studies

Demand for horticultural products is a major determinant of the size andprosperity of the Australian horticulture industry. Demand is in part influ-enced by conditions of access to markets. Many markets have high tariff andnontariff barriers that stifle imports and reduce economic gains from effi-ciency and specialisation. Reducing barriers to trade is critical to exposingproducers and consumers to market prices and to assuring market access forcompetitive and efficient producers. Increasing market access would lead togains for taxpayers and consumers in countries with large trade distortions.It would also benefit efficient producers around the world, resulting in neteconomic gains for the world as a whole.

The discussion in this part provides a case study analysis of countries thathave one or more significant market access issues for the Australian horti-culture industry and are agreed priority markets for the industry.

Following recently signed bilateral agreements between the United Statesand China, it is evident that China (and subsequently Chinese Taipei) willjoin the WTO in 2000. China’s and Chinese Taipei’s accession to the WTOis expected to reduce many of the market access barriers that exist in thesecountries.

10 Australian horticulture

PART 2

European Union

In 1995 the European Union was the third largest producer of fresh fruit andvegetables after China and India (European Commission 1998). The EuropeanUnion protects its domestic horticulture sectors through both tariff and non-tariff barriers. Nevertheless, the European Union is currently a major marketpriority for Australian horticultural exports, especially apples, nuts, onionsand beetroot.

TariffsEU tariffs on imported processed horticultural products are of concern toAustralian exporters. For example, tariffs of 15.6 per cent to 18 per cent arelevied on processed tomatoes, while Australian exports of canned fruit andjuice into the European Union face a tariff rate of 19.8 per cent. These ratesare considerably higher than Australia’s tariff rate on processed tomatoesand canned fruit and juice of 5 per cent. The European Union levies tariffrates of 9.5 per cent and 13.5 per cent on imports of prepared or preservedmacadamias as well as fresh or dried macadamia kernels.

Australian exporters of cut flowers are significantly disadvantaged in theEuropean Union. Australia’s major competitors in this market are the south-ern African nations and Israel that are considered to be developing nations.As such, they receive preferential treatment in the form of low tariff duties,while Australia faces import tariffs of between 11.3 per cent and 20 per cent.

While the European Union levies a relatively high applied tariff rate of 12per cent on imports of fresh strawberries, the bound rate is higher still, at20.8 per cent.

Sanitary and phytosanitary requirementsOther than strict food safety standards applying in the United Kingdom forproducts such as apples and pears, there appear to be few quarantine barri-ers applied by the European Union. This may be due, in part, to membercountries of the European Union not requiring treatment for Mediterraneanfruit fly, which is widespread throughout the European Union.

11Australian horticulture

EUROPEAN UNION

A phytosanitary certificate conforming to the International Plant ProtectionConvention must accompany all imports. Official inspection in the export-ing country (on which the phytosanitary certificate is based) must take placenot more than 14 days prior to shipment.

Domestic support and export subsidiesThe European Union, under the Common Agricultural Policy, provides fora number of domestic support regimes that influence its fruit and vegetableproduction and trade, including a fresh fruit and vegetable regime and aprocessed fruit and vegetable regime. Both of these regimes, however, havebeen subject to reform in recent years in an attempt to bring about a moremarket oriented sector. For fresh fruit and vegetables, intervention is still inplace and export subsidies continue to be paid. For processed fruit and vegeta-bles, the level of production aid is an area for negotiation.

A proposed common potato regime has been developed by a number of inter-ested countries. However, the Agricultural Council of the Commission attheir meeting in November 1996 rejected the proposed regime and as theissue has not reappeared on the Council agenda the proposed potato regimewill not be considered in this section.

Fresh fruit and vegetable regimeThe fresh fruit and vegetable regime was reformed in 1996 with the inten-tion of creating a more market oriented sector. The stated objectives of thereformed regime are to achieve a balance between supply and demand atprices that are fair to producers and to encourage specialisation within theEuropean Union while taking into account third country trade. The reformedregime strengthens the position of producer organisations through a newoperating fund while providing for a reduction in the role of subsidised with-drawals (intervention). All fruit and vegetables are covered by this regimeexcept potatoes, wine grapes, bananas, sweetcorn, beans and peas for fodderand olives.

InterventionThe objective of intervention is to stabilise prices in years of glut but not toprovide an alternative outlet to the market. It provides compensation fromEU funds to producers withdrawing the following products from the market–– apples, clementines, apricots, lemons, melons, nectarines, peaches,aubergines, sweet oranges, pears, cauliflowers, table grapes, tomatoes, watermelons, mandarins (including satsumas, tangerines and other hybrids).

12 Australian horticulture

EUROPEAN UNION

Products withdrawn from the market can be distributed free to approvedcharitable organisations if they do not affect the market. Alternatively, prod-ucts can be used as animal feed or distilled into industrial alcohol. If anyproducts cannot be disposed of in the above way, they must be destroyed insuch a way that takes into account possible environmental impacts. Thisintervention process differs greatly from that of other schemes such as dairy,beef and grains, where the EU intervention agencies accumulate interven-tion stocks of these products. The products are then sold on the domesticmarket, if prices rise sufficiently, or exported with the aid of export subsi-dies, thereby distorting the market. That does not mean, however, that theEU arrangements for horticulture are not market distorting.

Compensation for product withdrawn from the market is only paid forproduce of marketable quality. The levels of compensation are derived fromprices set in the 1995-96 price fixing round. For withdrawal compensationin 1997 (the first year of application) a reduction of 20 per cent was madeto the initial price for all products other than citrus. Between 1997 and 2002compensation will have declined in equal stages till it reaches a rate 40 percent below the initial level. Although citrus produce will have similar reduc-tions in compensation levels over the five year period, it is not calculated ona percentage basis.

Limits on the volume of produce eligible for EU withdrawal compensationhave also been established. These limits were set at 50 per cent of themarketed production of each eligible product in the 1997 marketing year (30per cent for citrus fruits), reducing in equal amounts to 10 per cent in thefifth marketing year (8.5 per cent for apples and pears). During this periodof reduction, the existing ‘stabiliser mechanism’ will continue to operate ifneeded. Under this mechanism, the value of compensation reduces if with-drawal exceeds defined ‘threshold’ volumes. For example, only 3.9 per centof marketed production of apples and 6.1 per cent of pears were withdrawnin 1996-97 (European Commission 1998).

Although the intervention scheme in operation is market distorting, it is diffi-cult to assess the extent of the impact it has on the market for fresh fruit andvegetable produce. The withdrawal of produce by the producer organisa-tions would lead to some price support although the level of compensationappears to be low compared with market prices.

With the reform of the fresh fruit and vegetable regime in 1996, interven-tion has been declining and more emphasis is being placed on product devel-

13Australian horticulture

EUROPEAN UNION

opment and improvement using producer organisations rather than directlysupporting the industry.

Producer organisationsProducer organisations have access to intervention but they can also submitproposals for operational programs aimed at improving production andmarketing.

To gain access to EU funds, producer organisations must draw up an oper-ational program, which is 50 per cent funded by the European Union (up toan overall ceiling), with the remaining costs covered by member contribu-tions. Some of the objectives of the program should include promotion ofcultivation practices and production techniques that ensure production isplanned and adjusts according to demand, reduces costs, stabilises producerprices and improves product quality.

The operational fund of producer organisations may be used to finance marketwithdrawals, either by paying a supplement to the European Union with-drawal compensation, or by paying withdrawal compensation for productsnot eligible for Union withdrawal compensation.

Marketing standardsThe European Union applies marketing standards for fresh horticulturalproduce. These standards apply to all products at all stages of distributionfrom the grower’s packhouse to the retail shop and to imports and exports,but excludes farm gate sales and produce intended for processing. The stan-dards include criteria of quality, size, labeling, packaging and presentation.Produce can be rejected if it does not meet marketing standards and thusstringent application of these may be used to limit the amount of fresh produceimported into the European Union.

Other forms of supportProducers of citrus fruit who have contracts with processors are eligible forthe payment of processing aid to make processing a more attractive alter-native to withdrawal from the market. This aid results in increased pricesfor processing fruit and larger volumes processed.

In the European Union, orchard grubbing grants have been available to grow-ers of apples, pears, peaches and nectarines to reduce surpluses. At presentall schemes are closed.

14 Australian horticulture

EUROPEAN UNION

Export subsidies are available to EU exporters of apples, lemons, oranges,peaches, nectarines, table grapes, tomatoes and certain nuts to third coun-tries to compensate for the difference between EU and world prices. Anexport licence is required to be eligible for the export subsidies.

Under the WTO Agreement on Agriculture, the volume of subsidised exportsmust decline by 21 per cent while expenditure on the export subsidises mustdecline by 36 per cent from their 1986-90 base level, over the period from1995 to the year 2000. In 2000 the European Union’s maximum annual allow-able quantity of subsided fresh fruit and vegetable, including citrus, will be906 900 tonnes, compared with around 1.1 million tonnes in 1995. In 1997,expenditure on EU export subsidies for fresh fruit and vegetables was US$89million.

Processed fruit and vegetablesThe processed fruit and vegetable regime has been developing since 1968and was most recently reformed in 1996. The main objective of this regimeis to provide production aid to the processing industry to make it morecompetitive on world markets. The aim is to compensate local processorsfor the higher cost of raw materials sourced from within the European Union.However, the structure of the scheme results in it institutionalising the highercost of these raw materials.

Production aidProduction aid is paid to processors of dried figs, prunes, peaches, pears andtomato products if they contract before the beginning of the marketing yearto pay producers a specified minimum price for raw material. Both the rawmaterial and the finished products have to meet minimum quality criteria.Canned pineapple also qualifies for production aid under similar but sepa-rate provisions.

The intention of production aid is to take into account the difference betweenthe minimum price and the price of the raw materials on the world market.The minimum price is determined according to the price set in previousmarketing years and movement of prices in the fresh sector. Account is alsotaken of the difference between the minimum price and prices in majorcompeting countries, as well as trends in the volume and value of externaltrade. Because of production aid, trade with third country suppliers of rawproduce for processing is reduced even if these suppliers could supply theproduct at a lower cost than the EU suppliers could. Imports are further disad-vantaged by the changed regime in that processors are only eligible for

15Australian horticulture

EUROPEAN UNION

production aid if they have supply contracts with recognised EU producerorganisations.

As an example, for the 1999-2000 marketing year the minimum price forpeaches intended for the production of peaches in syrup and/or natural fruitjuice will be 28.37 euro per 100 kilogram net. The production aid for thesame product will be 6.10 euro per 100 kilogram net.

Some provisions have been made to reduce market imbalances that occur asa result of production aid. Aid for peaches and pears in syrup or natural juiceswill be reduced in subsequent years if average production in the previousthree marketing years exceeds established thresholds. Aid for the followingyear is then reduced in proportion to the amount by which the threshold wasexceeded. The thresholds are 582 000 tonnes net weight for peaches in syrupand/or natural juices (EU production in 1996-97 was 494 000 tonnes) and102 805 tonnes net weight for Williams and Rocha pears in syrup and/ornatural juices (EU production in 1996-97 was 126 000 tonnes). As 1996-97was the first marketing year where these provisions applied, the first threeyear average will be for the 1996-97, 1997-98 and 1998-99 marketing years.

For processed tomato products, aid is limited by quota to a fixed volume ofproduction. In addition, a system of preliminary contracts between tomatogrowers and processors ensures that adequate area is planted to meet thedemands of the local processing industry.

As the world price used to calculate the level of production aid is the farm-gate price of fresh products in third countries, any pre-farmgate improve-ments in productivity in these countries will not improve the competitivenessof these products in the European Union. Instead it will simply lower theworld price that is used to calculate the level of production aid that wouldcorrespondingly increase. However, productivity improvements post-farm-gate will improve the competitiveness of third country canned products inthe European Union.

As production aid is based on production levels, processors increase produc-tion up to the thresholds to increase total aid payments. There is an incen-tive for producers to at least maintain production at around the thresholdlevels. The production aid would also tend to provide support for the priceof raw products that meet the quality standards. As a result production ofboth processed and unprocessed fruit is distorted by the payment of produc-tion aid.

16 Australian horticulture

EUROPEAN UNION

Specific measuresThe introduction of specific measures to promote and improve the compet-itiveness of products of major regional importance is provided for in the baseregulation if such products are faced with strong international competition.

Export subsidiesExport subsides for some processed products are paid on the basis of thedifference between EU and third country prices to enable products coveredby the regime to be exported competitively to third countries. The productscurrently eligible for subsidies are processed tomatoes, provisionally pre-served cherries, glace cherries, processed hazelnuts and certain pure orangejuices. Additionally, where the products incorporate added sugar, subsidiesmay be fixed on the percentage of added sugar in processed fruit andvegetable products. This is to compensate for the high supported price foradded sugar in the European Union.

To comply with the Uruguay Round agreement, the volume of subsidisedexports must decline by 21 per cent while expenditure on the export subsi-dies must decline by 36 per cent from their 1986–90 base level over the sixyear implementation period from 1995 to 2000. In the year 2000, the Euro-pean Union’s maximum annual allowable quantity of subsidised processedfruit and vegetables will be 158 600 tonnes, compared with around 200 800tonnes in 1995.

17Australian horticulture

EUROPEAN UNION

United States

The United States is a major market for Australian horticulture, especiallyfresh citrus, macadamia nuts and cut flowers. The Australian apple and pearindustry is interested in extending its presence in the United States and thecitrus industry is seeking expanded access (under treatment) for areas thatcannot qualify for fruit fly area freedom.

TariffsThe United States applies high tariff rates on many processed horticulturalgoods. For example, tariff rates of 16.2–18.5 per cent are applied to importsof Australian canned fruit and juice, compared with Australia’s tariff rate of5 per cent. A 23 per cent ad valorem duty is imposed by the United Stateson imported preserved macadamias, while fresh or dried macadamia nuts inshell and fresh or dried macadamia kernels are levied at US1.8c a kilogramand US7c a kilogram respectively. The tariff rate on imported processedtomatoes is 12.3 per cent, which is considerably higher than Australia’s tariffrate of 5 per cent.

In addition Australian exports of fresh citrus and avocados to the UnitedStates face tariffs of US2c a kilogram and US12c a kilogram respectively.

Sanitary and phytosanitary requirements While the United States does not have a comprehensive list of pests anddiseases, it may regard any pest that does not exist or is not widespread inthe United States as a quarantine pest.

Operating on the basis of an open list of unspecified pests is not a scientificapproach and reduces the transparency of pest risk analysis as laid down inthe WTO Agreement on the Application of Sanitary and PhytosanitaryMeasures (European Commission 1999).

Import permits are required for a large range of restricted items includingfruits and vegetables. It is expected that permit applications be submitted tothe relevant authorities at least 30 days before the arrival of the shipment atthe port of entry.

18 Australian horticulture

UNITED STATES

A phytosanitary certificate is also required for many items including fruit,nuts, vegetables, plants and plant products. Certificates must be issued notmore than 15 days before shipment. Certificates are not required for freshcut flowers or processed plant products unless otherwise restricted.

There are a number of SPS issues affecting Australian exports of horticul-tural products to the United States. These apply to apples and pears, cher-ries, cut flowers and chestnuts.

Apple and pear exports to the United States require accompanying docu-mentation including an import permit, phytosanitary certificate and addi-tional declarations covering treatment of light brown apple moth and fruitflies.

Under the restriction applying to apples and pears, exports are permittedentry provided that:

• they have been produced in accordance with the Workplan for ExportCertification of Australian Apples, Pears and Nashi; or

• they are inspected for light brown apple moth on arrival.

The first option is conducted under guidelines established by the Animal andPlant Health Inspection Service (APHIS) of the United States and must besupervised by an APHIS officer at industry expense.

The second option relies on Australian clearance procedures and compul-sory US inspection on arrival. The US inspection authorities adopt a virtu-ally zero tolerance policy of pests. If detected the shipment must be eitherdestroyed or reshipped to an alternative market (Mexico and Canada willnot accept the shipment if it fails US inspection).

While the United States has approved in-transit cold treatment for fruit fly,they do not accept that preclearance inspection procedures by AQIS for lightbrown apple moth are sufficient to remove the optional requirement for USinspection on arrival. This is despite these procedures being approved byother importers of Australian apples and pears such as New Zealand.

While imports of cherries are not currently permitted into the United States,there is a pest risk assessment pending. However, according to the Australian

19Australian horticulture

UNITED STATES

industry, US authorities claim they do not have the resources to completethe assessment and it may be two years before they can address the issue.

As reported by the European Commission (1999), ‘for new non-manufac-tured agricultural products, there are requirements for import permits to theUnited States. The procedures between application and the inclusion in thelist of approved products are excessively long, even several years. This hasbeen experienced even in cases where other products from the same area ofproduction with the same phytosanitary risks were permitted.’

Under article 6 in the Sanitary and Phytosanitary Agreement, provisionsexist for countries to recognise regions within an exporting country as beingdisease or pest free.

As with other fruit susceptible to fruit fly in Australia, there are cherry produc-tion regions that have been recognised domestically as fruit fly free underthe Interstate Certified Assurance program. The industry argues that over-seas markets should acknowledge these areas, as is the case with citrus tothe United States, claiming that fruit would be cleaner from chemicals andcould be exported at less cost.

While exports of cut flowers and ornamentals generally do not require aphytosanitary certificate, the Australian industry claims that US importinspections are overly stringent and are impeding commercial trade.

Another issue is the rules governing cut flowers of the rutaceae family suchas boronia and yellow bells. As citrus belongs to the same family, any plantswithin this family are technically subject to the same protocols as citrus inrelation to citrus canker. While citrus exports are permitted under area free-dom provisions, flowers of the rutaceae family are produced outside of theseareas and are not permitted under those provisions. AQIS states that Australiais free of citrus canker and is seeking recognition of country freedom fromthe United States to expedite the export of these cut flowers (L. Ransom,AQIS, personal communication, September 1999).

The chestnut industry has also raised concerns over the length of time requiredto gain import permits, claiming that potential buyers have been lost as aresult of waiting for permits. They also claim that US protocols for fumiga-tion are for insects that do not exist in Australia.

20 Australian horticulture

UNITED STATES

AQIS is also working with the citrus and tomato industries in efforts toimprove the range of access of these products from Australia.

The United States presently only accepts citrus from areas with fruit fly areafreedom status (Riverland South Australia; Sunraysia New South Wales,Victoria; Murrumbidgee Irrigation Area New South Wales), with cold ster-ilisation only allowed as a fall back treatment in the event of a breach of areafreedom for those areas (not accepted as a frontline treatment for non fruitfly free areas). The United States also adopts a tough stance on citrusblackspot.

Domestic support and export subsidiesDomestic support for horticultural products in the United States appears tobe minimal.

Under the 1996 farm bill, production flexibility contracts are available foreligible producers and these only include those who had participated or hadcertified acreage in the wheat, feed grains, cotton and rice programs in anyone of the past five years (US Department of Agriculture 1996). Horticulturalproducers are not eligible for this assistance. There is some planting flexi-bility on contract acreage where any commodity may be grown except fruitsand vegetables. This would act to prevent areas that might otherwise bediverted to fruit and vegetables being used for horticulture. That provisionwould tend to support internal US prices for fruit and vegetables.

21Australian horticulture

UNITED STATES

Japan

Japan is a major export destination for Australian cut flowers, mangos,macadamias, oranges and mandarins.

TariffsAustralian exports of fresh citrus and citrus juice to Japan are impeded byrelatively high tariff rates. Applied tariffs on oranges range from 17.3 percent between June and November, to 34.7 per cent for the remainder of theyear. Tariffs on mandarins are 18 per cent all year. Japan has an ad valoremtariff on citrus juice imports at applied rates of between 22.5 and 31.5 percent, or at 24.33 yen a kilogram, whichever is greatest. In spite of these tariffrates Japan is Australia’s fifth largest citrus export market. A reduction intariffs would enable Australia to further develop this market.

Access to Japanese markets for Australian exports of apples and pineapplesare impeded by a tariff rate of 20 per cent.

Sanitary and phytosanitary requirementsJapan is relatively free of exotic pests and diseases and effectively pursuesa minimal risk import policy in its quarantine and food safety decisions.

General import prohibitions exist on ‘all plants and plant products whichserve as hosts of injurious insects or pathogens unknown or of restrictedoccurrence in Japan’. Japan’s list of nonquarantine organisms is incompleteand does not include many insects that are common to Japan and manyexporting countries such as aphids and mites. Japan’s system of zero toler-ance means that products which may carry nonharmful insects are requiredto undergo needless fumigation (European Commission 1999).

In addition, a phytosanitary certificate is required for fresh fruit and vegeta-bles. While a phytosanitary certificate is not required for Australian driednative flowers, clearance by the Japanese is reported to be quicker and easierif a certificate is obtained (AQIS 1999). The pests of main concern forAustralian exports to Japan are fruit fly and codling moth.

22 Australian horticulture

JAPAN

The Japanese approval procedures for fresh fruit are very long (up to threeyears), costly and lacking in transparency (European Commission 1999).The quarantine measures applied by Japan result in extensive researchrequirements before import bans are lifted. Even after imports are approved,the procedures for many of the treatments to guarantee no pest or diseaseentry can be very costly, effectively pricing imports out of the domesticmarket (Milgate 1995).

In cases such as stonefruit, apples, pears and mangos, phytosanitary proto-cols may cover only specific limited product varieties, excluding other, almostidentical varieties. Japan requires repeated testing of established quarantinetreatments each time a new variety of an already allowed agriculturalcommodity is approved for import.

In addition to quarantine measures, strict food safety standards apply andchemical residue testing is carried out on imported fruit and vegetables whereimports exceed 100 tonnes a year for a particular product. There are currentlytests for 104 chemicals (Milgate 1995).

Under a list of key sectoral priorities for 1999-2000, the Australian govern-ment has identified recognition of equivalence by the Japanese Health andWelfare Ministry of certification by AQIS and testing by accredited labora-tories. It has also identified the need for the Japanese government to lift itstesting requirement for agricultural chemicals that are not registered for usein Australia or not used in certain products (Department of Foreign Affairsand Trade 1999).

The lack of recognition by Japan of mainland area freedom from fruit fliesand other pests and diseases in Australia is an important issue of concern forAustralia. As of September 1999, AQIS had a submission for fruit fly areafreedom nearing completion. Other horticultural products, including a rangeof vegetables, would similarly benefit from Japanese acceptance of area free-dom provisions.

Other quarantine issues specific to Japan include the granting of import accessfor a further four varieties of mangos. Japanese quarantine authorities recentlydecided to lift import restrictions on the varieties Keitt, Palmer, R2E2 andKent.

There is also an application for the export of mainland tomatoes to Japan,with the development of risk management options pending.

23Australian horticulture

JAPAN

Domestic support and export subsidiesIn Japan there are no export subsidies, credit programs, transport subsidies,and tax and investment incentives (US Department of Agriculture 1998). Agri-cultural support in Japan is largely provided through administered prices,trade measures and supply management regimes, such as the vegetable supplystabilisation fund. In the 1997 fiscal year (April–March), Japan was 86 percent self-sufficient in vegetables and 53 per cent in fruit (MAFF 1998). Asa result, for vegetables in particular, domestic production dominates themarket, although imports of various kinds of fresh vegetables have been onthe increase in recent years.

Domestic food prices in Japan are high and the Japanese food self-suffi-ciency rate is the lowest among the OECD countries. The Japanese tend toassociate food security with high self-sufficiency. Generally, Japan has ahigh level of food security because of its high incomes and ability to competefor supplies on world markets. However, the perception of vulnerabilitythrough low self-sufficiency appears to have been one of the key issues indesigning a new institutional framework for agriculture which is currentlybeing put into place.

Japan has achieved its 20 per cent targeted reduction in domestic support foragriculture as a whole under the Uruguay Round, as measured by the GATTAggregate Measurement of Support. The measurement was 3.7 trillion yenin 1992, which was 26 per cent less than during the base period, 5.0 trillionyen. Japan does not use any export subsidies that are subject to the reduc-tion commitments under the Uruguay Round agreement.

24 Australian horticulture

JAPAN

South Korea

South Korea is a significant market for Australian potatoes. The citrus andstonefruit industries are also interested in entering this market if quarantineand tariff quota impediments can be overcome.

TariffsAustralia is currently denied access to the South Korean citrus market onquarantine grounds. However, even if these restrictions were lifted, accessto this market would potentially be impeded by a high tariff quota system.Within quota tariffs are 50 per cent, while above quota tariffs are bound ashigh as 152 per cent for mandarins.

Similarly, access to the South Korean market for Australian onion produc-ers is impeded by prohibitive tariffs which are 135 per cent or 180 won perkilogram, whichever is greatest. The Australian chestnut export industry isstill in its infancy. However, commercial trade with the South Korean marketwould be prohibited by tariff rates of 219.4 per cent or 1470 won per kilo-gram, whichever is greatest.

With the exception of citrus, applied tariff rates for many horticultural prod-ucts are relatively low. Bound rates, however, are generally very high and itis on these rates that negotiations are held. For example, the bound rate onapples, pears, avocados and stonefruit is 45 per cent, on citrus 50 per cent,and on cauliflower and broccoli 27–40.5 per cent.

Sanitary and phytosanitary requirements While bound tariffs on agricultural products are excessively high, there isalso a wide range of quarantine and customs related impediments, particu-larly on horticulture, that have emerged over recent years.

Under the general restrictions of South Korean import law, all shipments aresubject to inspection and, if harmful organisms or soil are found, they canbe treated, destroyed or refused entry.

25Australian horticulture

SOUTH KOREA

Phytosanitary certificates must accompany all admissible plants, plant prod-ucts, their containers and packing materials. Other food products that do notrequire a phytosanitary certificate must have health certificates.

The most typical trade barriers in South Korea are nontariff barriers thatcommonly result from nontransparent regulatory practices. The lack of regu-latory transparency and consistency can affect licensing, inspections, typeapproval, marking/labeling requirements and other standards. Despite theAdministrative Procedures Act of 1996, the government is still inconsistentin providing public notice, and announcing minimum comment periods andtransitional periods before implementation of new regulations (US Depart-ment of State 1998).

Australian access to the South Korean horticulture market is currently limitedto potatoes, onions, carrots, leafy and flowering type vegetables and cut flow-ers, with access for other horticultural products restricted by quarantinemeasures.

The Australian horticulture industry has identified access for citrus (orangesand lemons) as its highest priority and technical discussions between quar-antine agencies have been under way for several years to obtain acceptanceof Australian fruit (Department of Foreign Affairs and Trade 1999).

Domestic support and export subsidiesLike Japan, agricultural policy development in South Korea has been aimedat maintaining a high degree of self-sufficiency. Farm income has beensupported primarily through strong government intervention, and thus, theagricultural sector is highly dependent on government support (MAF 1999).Specific information on South Korean government intervention is difficultto find, therefore more general comments on support are provided.

Vegetable production is of great importance to South Korean agriculture.Major vegetables grown are Chinese cabbage, radish, red pepper, garlic andonion. Several kinds of fruit including apples, pears, mandarin oranges,grapes and sweet persimmon are produced in South Korea. Fruit productionhas increased steadily with government encouragement.

South Korea had no export subsidies subject to reduction commitments underGATT during the base period and therefore no reduction commitments existunder this element in South Korea’s schedule (MAF 1999).

26 Australian horticulture

SOUTH KOREA

Establishment of a system of fostering professional farm operating units The South Korean Ministry of Agriculture and Forestry (MAF) has a planto enhance competitiveness of full time farmers who display growth poten-tial and enthusiasm. Under the plan, MAF will foster 150 000 full time farm-ers by 2004, of which 30 000 will be involved in horticulture.

Reduction of government subsidies to farm operating units and theirprogressive conversion to loans The excessive government subsidies to farmers limit the farmers’ self-reliance. With the aim of addressing these effects, it was decided that subsi-dies for farmers and corporate farms should be phased out and converted toloans by the year 2001.

Toward a new integrated financial support system for farm operations MAF has decided to move toward a new integrated system of granting finan-cial support for individual farm units in each period when they need financ-ing. Before financial support is granted, an in-depth analysis and evaluationof the longer term farming programs that are submitted by individual farm-ing units will be carried out. The new system is scheduled to be fully imple-mented by 2001 after being practised on a pilot basis during 1999 (MAF1999).

27Australian horticulture

SOUTH KOREA

Indonesia

Indonesia is one of Australia’s most important horticultural export markets,with significant quantities of Australian citrus, apples, pears, stonefruit,melons and potatoes being sold into this market.

TariffsWhile the applied tariff rates on imports of Australian horticultural productsinto Indonesia are very low and as such, are not considered a barrier to trade,Indonesian bound rates are very high. For example, Indonesia imposes anapplied tariff rate of 5 per cent on imports of fresh citrus, but the bound rate,which could be applied, is 40–50 per cent. Bound rates of 40–50 per centapply to many other horticultural goods such as apples, pears, avocados,canned fruit, vegetables and stonefruit.

With bound tariffs being substantially greater than applied tariffs, if govern-ment policy were to become more inward looking, the Indonesian govern-ment could legitimately raise applied tariff rates to very high noncommerciallevels. So while the actual applied rates are relatively low there is scope toincrease these rates to the high ceiling levels set by the bound rates. To limitthe scope for this to occur, significant reductions in bound rates would berequired.

Sanitary and phytosanitary requirementsAustralia has access to Indonesia for a wide range of horticultural products.Products can pass Indonesian quarantine requirements for fruit fly by eitherarea freedom or the adoption of a range of disinfestation methods.

All permitted imports are subject to preshipment inspection by an Australianbased Indonesian inspection organisation. All products valued at US$5000or more must be issued a certificate for goods to be cleared through IndonesiaCustoms.

A phytosanitary certificate is required for all plants and plant products. Pro-cessed food requires a health certificate.

28 Australian horticulture

INDONESIA

Indonesian quarantine is not identified as a significant barrier to entry and thusmay be regarded as a low priority area for negotiations or bilateral discussions.

Domestic support and export subsidiesThere is little detailed information available on domestic support arrange-ments in Indonesia for horticultural products. Credit facilities exist for devel-oping food crops and horticulture, although details of such facilities arelimited. Among others there appear to be credit facilities for farmers and forprimary cooperatives.

The Indonesian Ministry of Agriculture has identified that the support anddevelopment of food crops and horticulture is an important policy issue(Ministry of Agriculture 1999). The aim of this increased focus on food cropsand horticultural development is to increase production and productivity, toimprove post-harvest and product quality. To achieve these objectives, theDirectorate General of Food Crops and Horticulture has developed a numberof programs, such as farming system development, integrated small farm-ers development, and the infrastructures and resources development program.

The Indonesian government also encourages investment in horticulture andfood crops (Ministry of Agriculture 1999). This includes investment in thefarming system, post-harvest procedure, processing, procurement of produc-tion inputs and marketing. In the current policy on investment in this areathe target of food crops and horticulture was 62.8 billion rupiahs or 50 percent of the total investment in the agriculture sector. However, details on thespecific nature of this investment policy in relation to horticulture are notreadily available.

29Australian horticulture

INDONESIA

China

If market access impediments including high tariff barriers can be overcome,China holds great potential as an export market for Australian horticulture.With China to become a member of the WTO in 2000 many of the currentbarriers to access are likely to be reduced.

TariffsWith most favored nation status, Australia faces tariffs of 30 per cent onexports of apples, pears, cherries, macadamias, canned fruit and vegetables.With the exception of apples, other fresh horticultural imports from Australiaare only approved for the hotel trade and not general domestic consumption.

Sanitary and phytosanitary requirementsApples from Tasmania are the only fresh horticultural products that havebeen granted general access to China. This access was achieved largelythrough Tasmania’s pest and disease free status. Further access to China formangos and citrus is a current industry priority.

As established trade protocol with China is very limited, little is known aboutthe specifics of China’s quarantine requirements for horticultural products.Phytosanitary certificates are required for all plants and unprocessed plantproducts, while import permits are only required for imports that are usuallyprohibited.

With China’s likely accession to the WTO most of its trade barriers will haveto be dismantled or substantially reduced as it commits to open its marketsto world exports.

Domestic support and export subsidiesSpecific information on domestic support arrangements in China for horti-cultural products is difficult to obtain; however, some general informationis available. According to the US State Department (1998a), direct subsi-dies for Chinese exports were abolished on 1 January 1991. However, anumber of indirect subsidies to China’s manufactured exporters still exist,

30 Australian horticulture

CHINA

such as guaranteed provision of energy, raw materials or labor supplies andbank loans that need not be repaid or which enjoy lengthy or preferentialpayment terms. Exporters also have access to tax rebates and duty exemp-tions on imported inputs for export production.

As part of its negotiations to join the WTO, China announced in 1997 thatit would not reintroduce export subsidies for agricultural goods followingits accession. As little public information about the central government’s1997 and 1998 budget revenue and expenditures has been released, it is diffi-cult to verify that export subsidies are not used. In 1997, total subsidies fordomestic price support and loss making state owned enterprises representedabout 11 per cent of total revenues.

31Australian horticulture

CHINA

Chinese Taipei

Chinese Taipei is a market in which Australian exports could be furtherexpanded. However, import quotas and tariffs are impeding current marketdevelopment. Nevertheless, Australia has established itself as an importantsupplier of fresh kiwifruit and stonefruit to this market.

It is expected that Chinese Taipei will also join the WTO soon after China’saccession. As a part of this process, the removal of import quotas on apples,citrus, plums and peaches and the reduction in import tariffs remains a keypriority for the Australian horticultural industry.

TariffsAccess for horticultural products to Chinese Taipei is restricted by tariffsand quotas. Australia has a quota allocation of 2400 tonnes for apples and600 tonnes for citrus (excluding mandarins). While the duty on apples is 50per cent, the duty on pears and fresh citrus is 40 per cent. Tariff duties ononions, cauliflower and broccoli range from 32.5 to 40 per cent and on stone-fruit, from 35 to 50 per cent. The tariff on avocados is 28 per cent. Whileimports of fresh cherries attract a lower duty of 12 per cent, it is still highby Australian standards.

Sanitary and phytosanitary requirementsAccess to the Chinese Taipei market is prohibited for some horticulturalproducts on quarantine grounds, while access for most other products isrestricted. Approval for restricted products needs to be sought from theChinese Taipei Board of Foreign Trade and/or the Bureau of CommodityInspection and Quarantine. There are often additional declarations andphytosanitary certificates required for certain pests.

The presence in Australia of burrowing nematode, Mediterranean fruit fly,Queensland fruit fly and codling moth, together with other injurious pestsand diseases, are of major concern to the authorities in Chinese Taipei. Strictdisinfestation procedures are enforced for all allowable fresh product (exceptof Tasmanian origin) imported into Chinese Taipei.

32 Australian horticulture

CHINESE TAIPEI

Where fruit fly host products are exported from mainland Australia to ChineseTaipei by airfreight, the product must undergo fruit fly disinfestation treat-ment of fixed temperature fumigation with methyl bromide followed by adefined period under cold storage prior to export.

The Australian stonefruit industry argues that the fixed temperature systemis detrimental to fruit quality and would prefer to have a sliding scale system(as used for exports to other markets) recognised by Chinese Taipei author-ities. Although a sliding scale treatment is accepted for the same fruit exportedfrom the United States, Chinese Taipei insists on Australia providing compre-hensive scientific data to prove the effectiveness of the sliding scale treat-ment for Australian fruit (P. McFarlane, Australian Fresh Stonefruit GrowersAssociation, personal communication, September 1999).

For seafreight export to Chinese Taipei the product is required to undergo a14 day in-transit cold disinfestation treatment for fruit fly. In the case of cher-ries, this disrupts the timing of the fruit to the market and can result in poorprices. The industry would prefer that the same treatment could be under-taken in Australia under appropriate supervision, thus allowing the fruit tobe airfreighted to the market in a more timely manner (I. Hay, CherryHaven,personal communication, October 1999).

An issue for the horticulture industry in general is to pursue recognition ofmainland area freedom from fruit fly as is provided for under Article 6 ofthe Sanitary and Phytosanitary Agreement.

Domestic support and export subsidiesThe policy objectives governing Chinese Taipei’s national agricultural indus-try include developing the agricultural industry, constructing farming villagesand taking care of farmers. Chinese Taipei recently redesigned their agri-cultural policies (Council of Agriculture 1996). A new program called theCross-Century Agricultural Development Program was implemented in fiscalyear 1998 (from July 1997). The period of implementation for this programis four years.

Although details on this new program are difficult to find it is understoodthat under this program the production and area planted to unpolished rice,raw sugar cane and dryland crops such as corn, sorghum and soybean willbe reduced. Direct payments for acreage set aside and rotation of high valueproducts and horticultural produce such as flowers will be granted for areas

33Australian horticulture

CHINESE TAIPEI

released by the above measures. These direct payments encourage increasedproduction of crops that are eligible for the payments, ultimately increasingthe amount of produce available on the domestic market and for export. Thisincreased domestic production will then compete with imports and also otherproduct on the global market.

In addition, a number of direct and indirect subsidy programs are offered toagricultural producers by the Chinese Taipei government (US State Depart-ment 1998b). These include financial assistance and guaranteed domesticprices higher than those prevailing on the global market. Incentives that mayhave the effect of subsidising exports are also provided to industrial firmsin export processing zones and to firms in identified emerging industries. AsChinese Taipei is currently in the process of WTO accession, it must notifythe WTO of these programs. As a result some of these subsidy programsmay need to be amended or abolished if they are deemed inconsistent withWTO principles.

34 Australian horticulture

CHINESE TAIPEI

Industry profiles

The principal features of key Australian horticultural industries are discussedin detail in the remainder of this report. Aspects of these sectors include:location of production and output trends; export performance by key markets;Australian support arrangements; market access issues in important markets;and assistance to local industries in export markets and in the main compet-ing exporting countries.

The discussion for each industry is not exhaustive. A range of sources wasused. The most important of these were the Australian Bureau of Statistics,the United Nations, US Department of Agriculture, and persons engaged inthe local (Australian) industries.

The following horticultural sectors are covered in this part of the report:

• almonds

• apples and pears – fresh

• avocados

• canning fruit

• cherries

• chestnuts

• citrus (fresh) and citrus juice

• custard apples

• cut flowers

• macadamias

• mangos, melons, pawpaws and pineapples

• potatoes

• stonefruit – fresh

• strawberries

• tomatoes – fresh

• tomatoes – processed

• vegetables (excluding potatoes and tomatoes)

35Australian horticulture

PART 3

Almonds

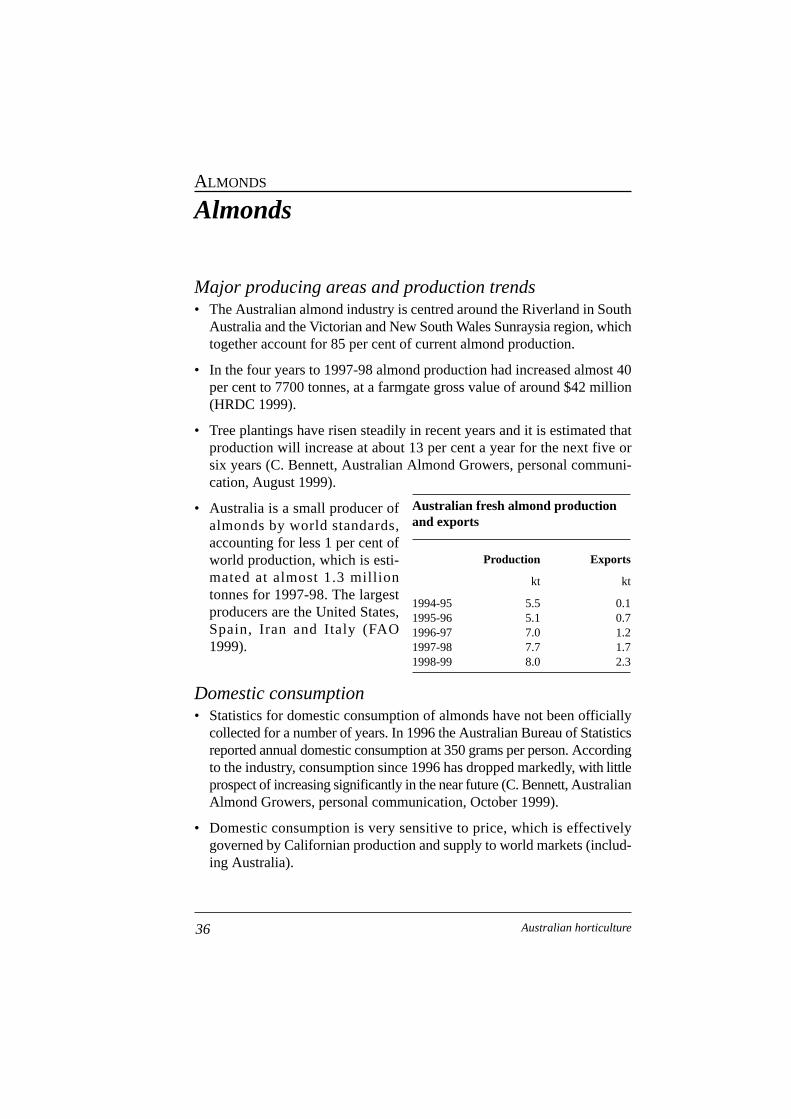

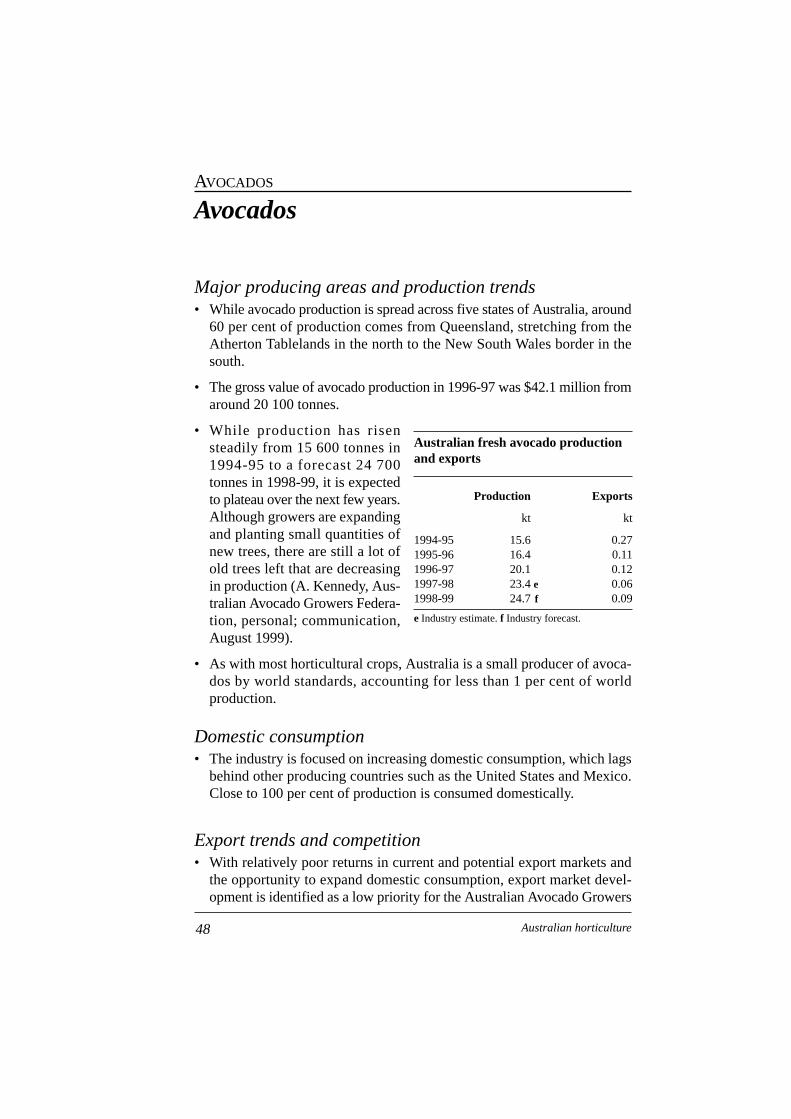

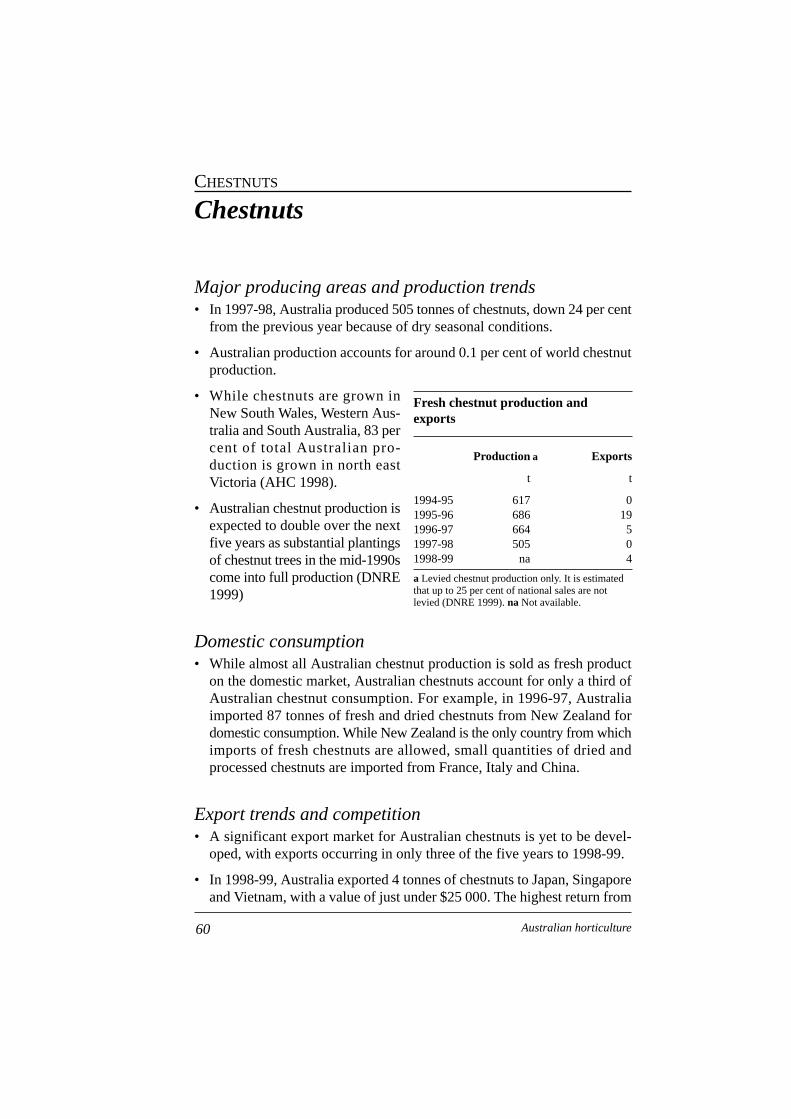

Major producing areas and production trends• The Australian almond industry is centred around the Riverland in South

Australia and the Victorian and New South Wales Sunraysia region, whichtogether account for 85 per cent of current almond production.

• In the four years to 1997-98 almond production had increased almost 40per cent to 7700 tonnes, at a farmgate gross value of around $42 million(HRDC 1999).

• Tree plantings have risen steadily in recent years and it is estimated thatproduction will increase at about 13 per cent a year for the next five orsix years (C. Bennett, Australian Almond Growers, personal communi-cation, August 1999).

• Australia is a small producer ofalmonds by world standards,accounting for less 1 per cent ofworld production, which is esti-mated at almost 1.3 milliontonnes for 1997-98. The largestproducers are the United States,Spain, Iran and Italy (FAO 1999).

Domestic consumption• Statistics for domestic consumption of almonds have not been officially

collected for a number of years. In 1996 the Australian Bureau of Statisticsreported annual domestic consumption at 350 grams per person. Accordingto the industry, consumption since 1996 has dropped markedly, with littleprospect of increasing significantly in the near future (C. Bennett, AustralianAlmond Growers, personal communication, October 1999).

• Domestic consumption is very sensitive to price, which is effectivelygoverned by Californian production and supply to world markets (includ-ing Australia).

36 Australian horticulture

ALMONDS

Australian fresh almond productionand exports

Production Exports

kt kt

1994-95 5.5 0.11995-96 5.1 0.71996-97 7.0 1.21997-98 7.7 1.71998-99 8.0 2.3

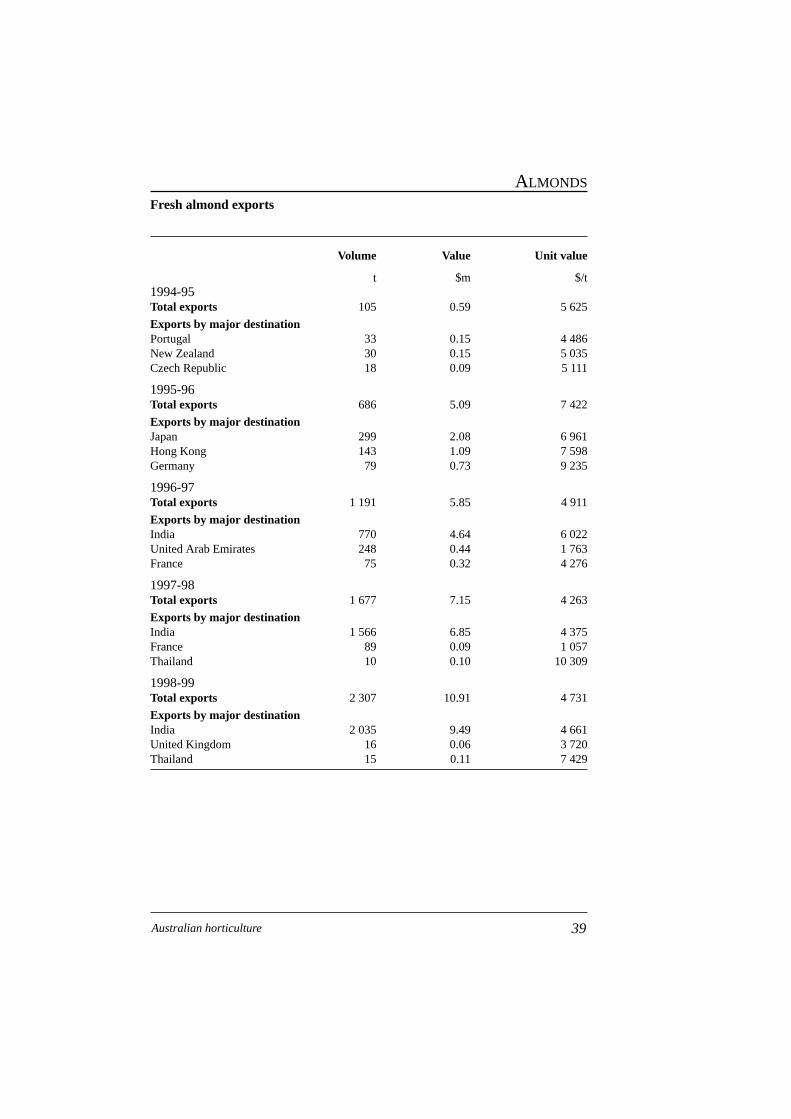

Export trends and competition• Consistent increases in production combined with a decline in domestic

consumption, have resulted in a significant increase in exports over thepast five years, albeit from a low base.

• Exports of almonds increased from 105 tonnes in 1994-95 to over 2300tonnes in 1998-99, with a value of almost $11 million. Australia is consid-ered to be the largest southern hemisphere supplier.

• With an expected growth in production of around 13 per cent a year forthe next five or six years and little prospect of significant increases in dom-estic consumption, the industry will be increasingly reliant on exports.

• Export markets for almonds have traditionally been opportunistic. Forexample, in each of the three years to 1996-97, the top three export desti-nations were different markets (see export table).

• Since then, however, India has become the major importer of Australianalmonds, accounting for around 90 per cent of total Australian exports in1997-98 and 1998-99.

• European countries such as Spain, Germany, France and the UnitedKingdom are regarded as potential markets. While these markets preferlocal, stronger flavored varieties, consumption far exceeds domesticproduction. Consequently, these countries import large quantities ofalmonds. At present, these imports are predominantly being sourced fromthe United States.

• Australia’s main variety is the same as that produced by the United Statesand Australia is a price taker on world markets. One view within theAustralian industry is that a shift to the European preferred varieties wouldestablish a viable long term market niche, thus avoiding much of the directcompetition with the Californian producers (C. Bennett, Australian AlmondGrowers, personal communication, October 1999).

• The United States dominates virtually every export market for almonds.Australia holds negligible shares in the export markets to which it shipsproduct. However, Australia does have a counterseasonal supply advan-tage in exporting to northern hemisphere markets.

State/regional export contributions• South Australia has been the dominant almond exporting state and in 1998-

99 exported 60 per cent (1373 tonnes) of total almond exports (by volume).

37Australian horticulture

ALMONDS

Australian support arrangements• No known domestic support arrangements.

Market access issues• The major market access issue for the almond industry centres on India

which has a very high tariff rate of 40 per cent on almond imports. Thisis much higher than most other importing countries.

• Thailand too has a very high tariff of 60 per cent. While it remains at thislevel it is unlikely that this market will be considered an export opportu-nity.

• Tariffs on almonds shipped into the European Union, at around 6 per cent,are not considered to be a barrier to access.

Industry assistance in major importing and exportingcountries• No known assistance for overseas exporters.

Technical barriers to trade• There are no known technical barriers to trade.

38 Australian horticulture

ALMONDS

Fresh almond exports

Volume Value Unit value

t $m $/t1994-95Total exports 105 0.59 5 625

Exports by major destinationPortugal 33 0.15 4 486New Zealand 30 0.15 5 035Czech Republic 18 0.09 5 111

1995-96Total exports 686 5.09 7 422

Exports by major destinationJapan 299 2.08 6 961Hong Kong 143 1.09 7 598Germany 79 0.73 9 235

1996-97Total exports 1 191 5.85 4 911

Exports by major destinationIndia 770 4.64 6 022United Arab Emirates 248 0.44 1 763France 75 0.32 4 276

1997-98Total exports 1 677 7.15 4 263

Exports by major destinationIndia 1 566 6.85 4 375France 89 0.09 1 057Thailand 10 0.10 10 309

1998-99Total exports 2 307 10.91 4 731

Exports by major destinationIndia 2 035 9.49 4 661United Kingdom 16 0.06 3 720Thailand 15 0.11 7 429

39Australian horticulture

ALMONDS

Apples and pears – fresh

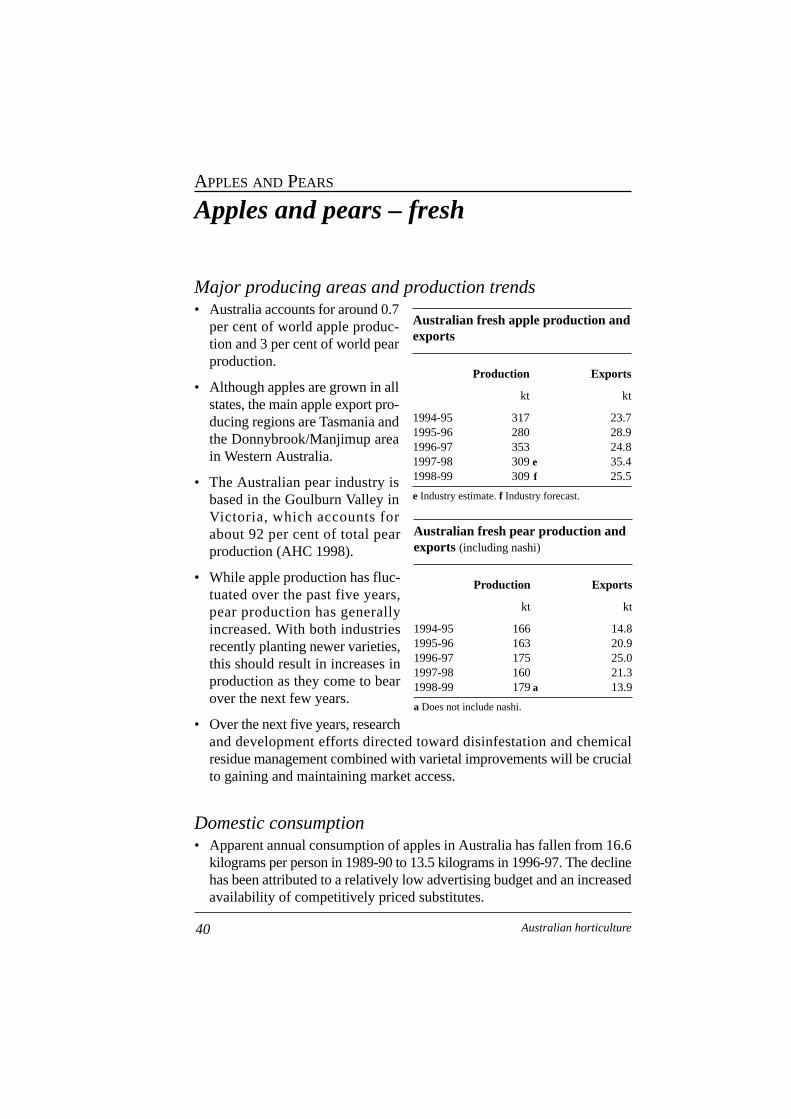

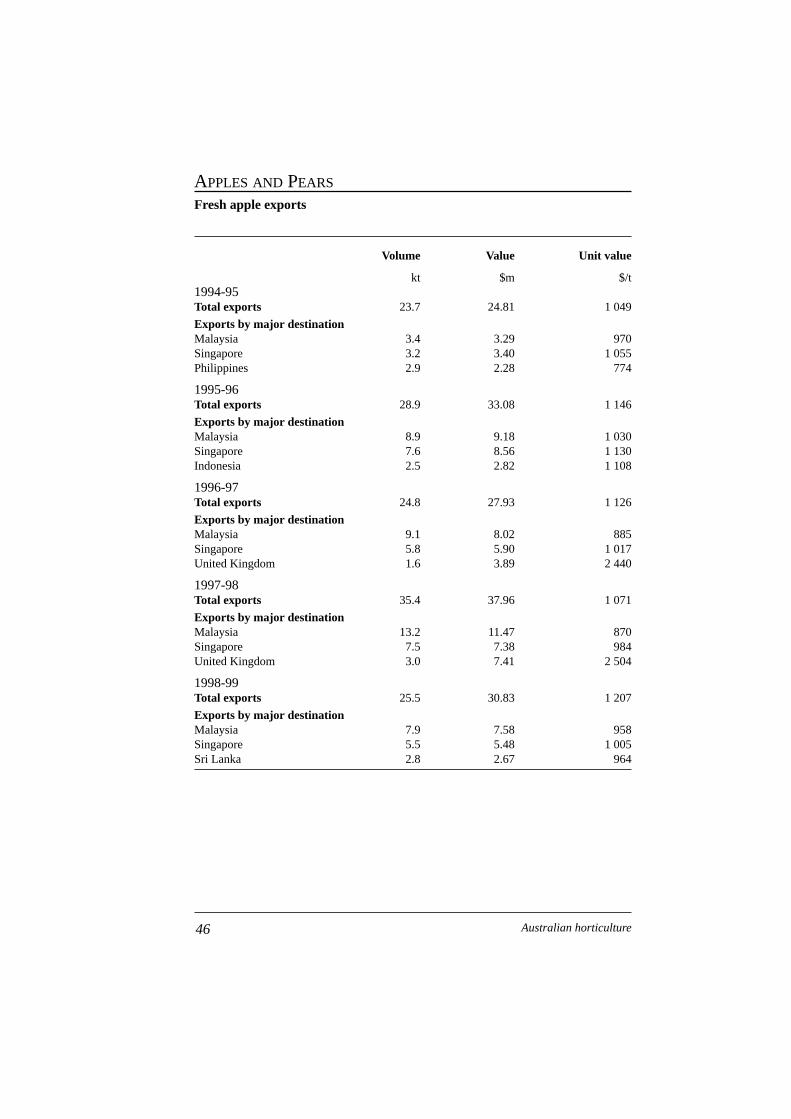

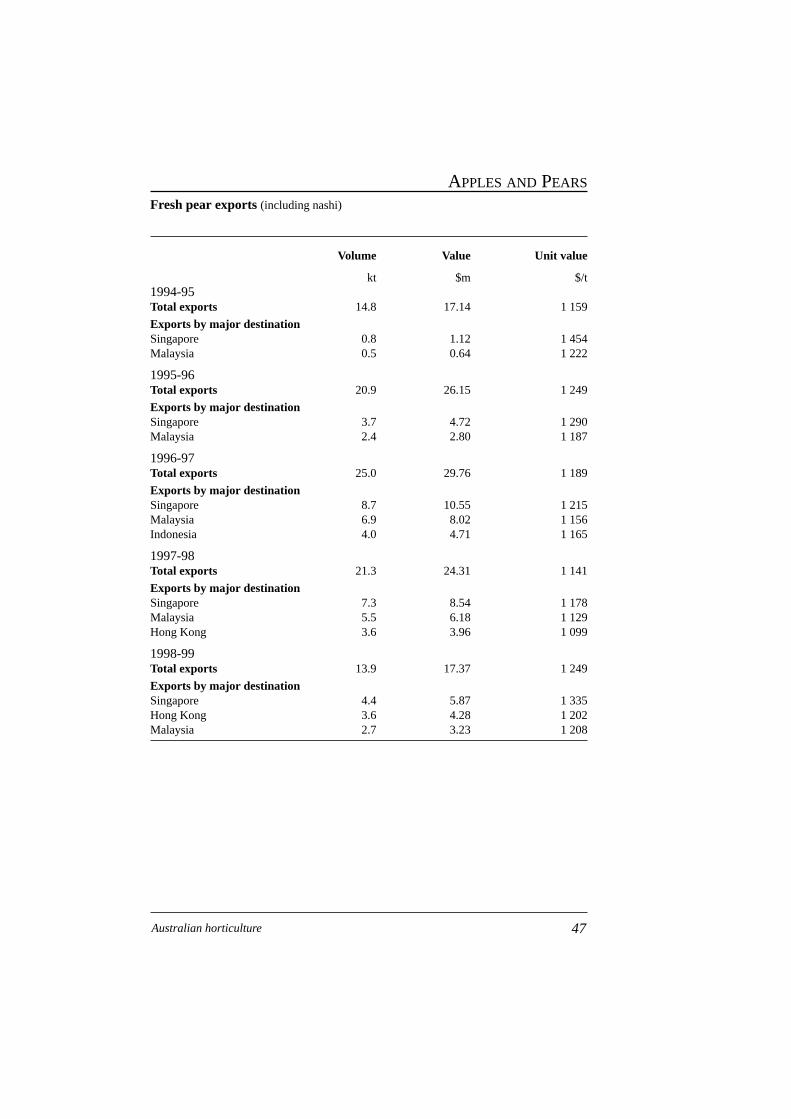

Major producing areas and production trends• Australia accounts for around 0.7

per cent of world apple produc-tion and 3 per cent of world pearproduction.

• Although apples are grown in allstates, the main apple export pro-ducing regions are Tasmania andthe Donnybrook/Manjimup areain Western Australia.

• The Australian pear industry isbased in the Goulburn Valley inVictoria, which accounts forabout 92 per cent of total pearproduction (AHC 1998).

• While apple production has fluc-tuated over the past five years,pear production has generallyincreased. With both industriesrecently planting newer varieties,this should result in increases inproduction as they come to bearover the next few years.

• Over the next five years, researchand development efforts directed toward disinfestation and chemicalresidue management combined with varietal improvements will be crucialto gaining and maintaining market access.

Domestic consumption• Apparent annual consumption of apples in Australia has fallen from 16.6

kilograms per person in 1989-90 to 13.5 kilograms in 1996-97. The declinehas been attributed to a relatively low advertising budget and an increasedavailability of competitively priced substitutes.

40 Australian horticulture

APPLES AND PEARS