august 15 & 16, 2012 ffy2013 eap annual training ffy2013 eap annual training part 6: assurance...

TRANSCRIPT

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training

FFY2013 FFY2013 EAP EAP Annual Annual TrainingTrainingPart 6: Assurance 16; Program Fiscal Management; Local Plan; Incidents & Appeals

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 2

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 3

IntentionsIntentionsPromote A16 as an activity that contributes to

maintaining affordable, continuous, and safe home energy for low-income Minnesota households

Clarify EAP A16 policy and expectationsEmphasize the importance of A16 for household

emergenciesReiterate and clarify the need for documentation

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 4

EAP Improves HH Outcomes in 3 Ways:EAP Improves HH Outcomes in 3 Ways:

Primary Heat payments

Crisis payments

A16 case management

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 5

What It IsWhat It IsAssurance 16 allows states to spend up to five percent (5%) of their LIHEAP Block Grant funds on “services encouraging and enabling households to reduce their home energy needs and thereby the need for energy assistance, including needs assessment counseling, and assistance with energy vendors.” Assurance 16 (A16) funds may also be used for A16 reporting.

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 6

Minnesota FocusMinnesota Focus The statewide focus of A16 continues to be case

management in support of the Coordinated Responsibility Model

Required A16 ActivitiesOutreachAdvocacy Referral

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 7

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 8

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

a

A16A16

A16A16A16A16

A16A16

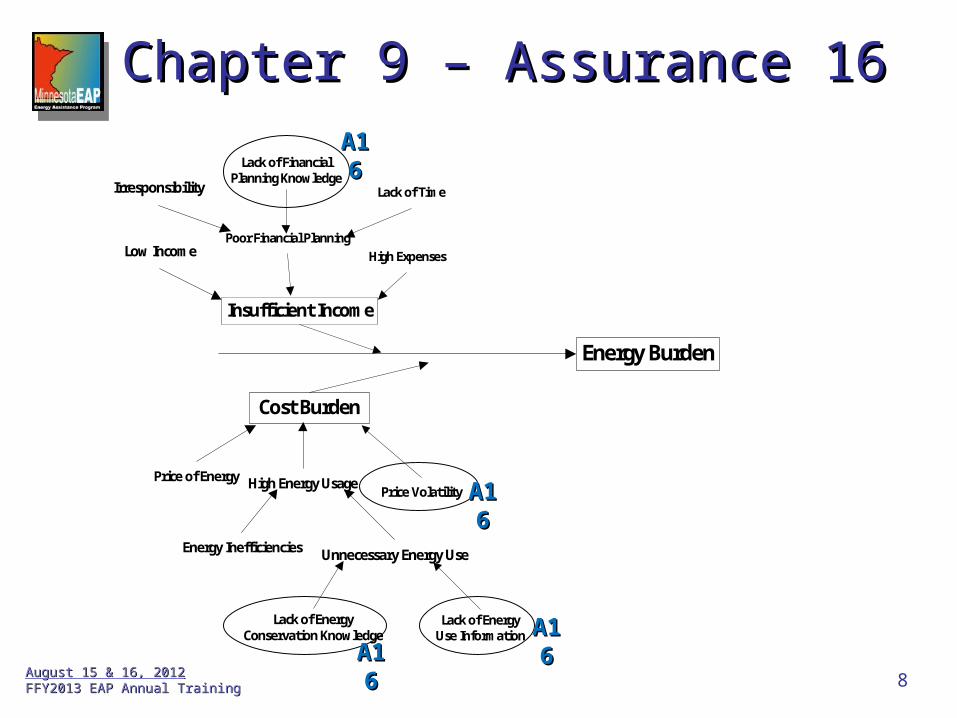

Energy Burden

Insufficient Income

Cost Burden

Price of Energy High Energy UsagePrice Volatility

Energy Inefficiencies Unnecessary Energy Use

Lack of Energy Conservation Knowledge

Lack of Energy Use Information

Low IncomePoor Financial Planning

High Expenses

Irresponsibility

Lack of Financial Planning Knowledge

Lack of Time

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 9

Why it matters: OutreachWhy it matters: Outreach

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 10

Why It Matters: Advocacy & ReferralWhy It Matters: Advocacy & Referral

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

Source: 2005 RECS

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 11

Why It Matters: Referral & OutreachWhy It Matters: Referral & Outreach

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

Source: 2006-10 American Community Survey Public Use Microdata Sample & 2005 RECS

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 12

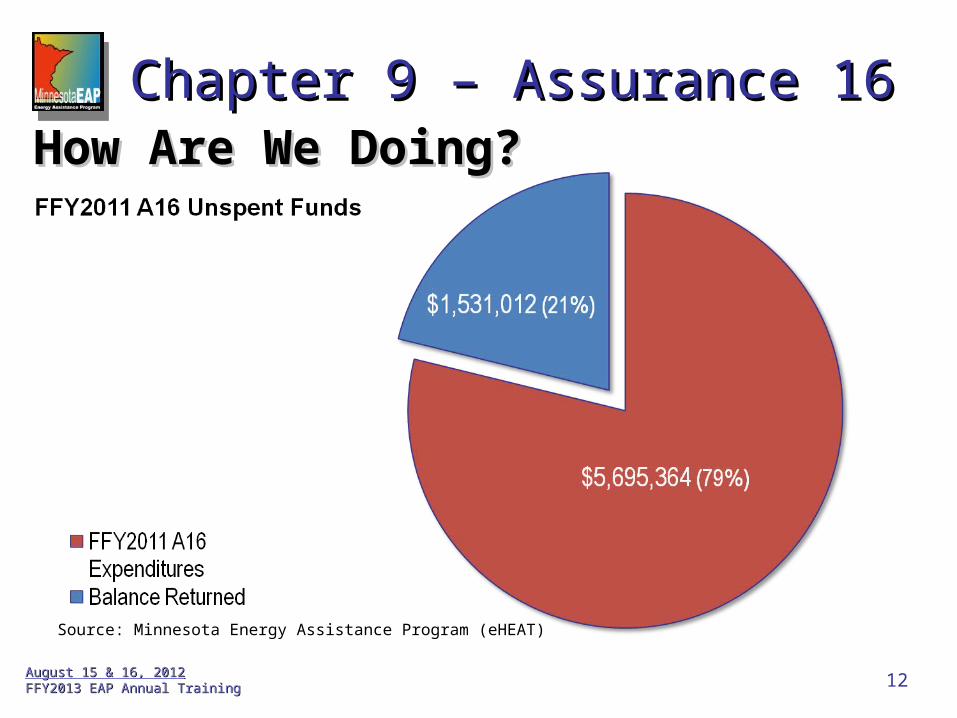

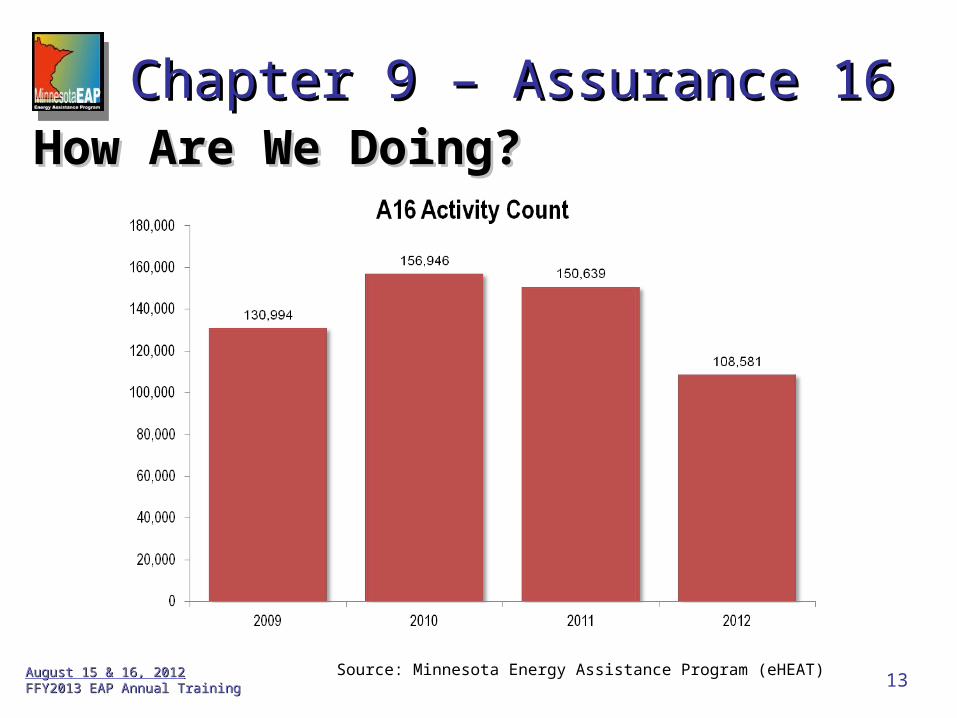

How Are We Doing?How Are We Doing?Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

Source: Minnesota Energy Assistance Program (eHEAT)

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 13

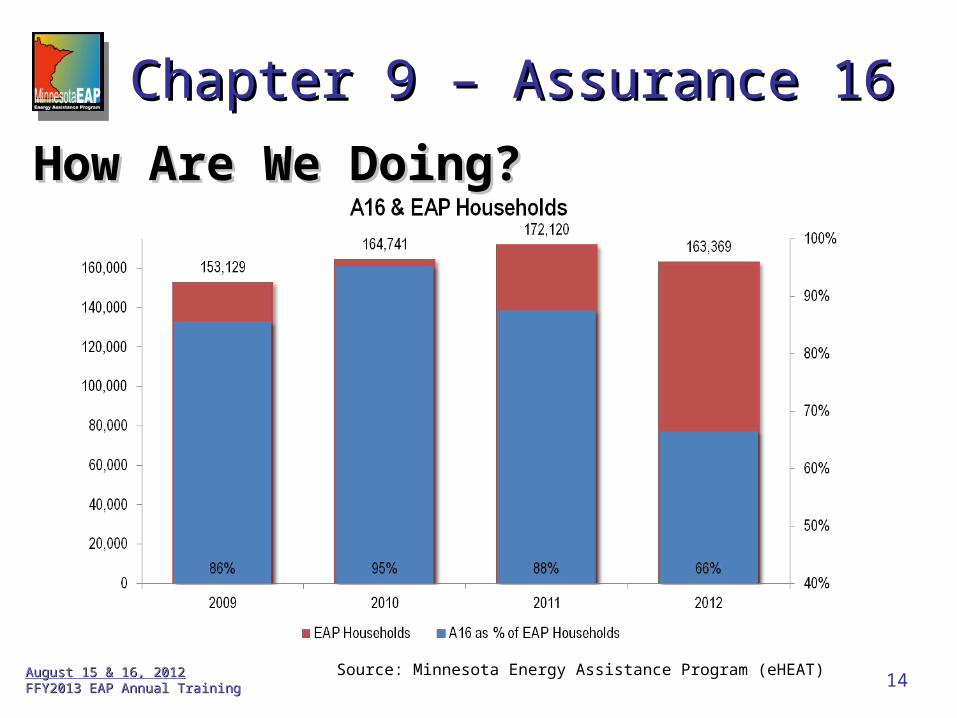

How Are We Doing?How Are We Doing?Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

Source: Minnesota Energy Assistance Program (eHEAT)

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 14

How Are We Doing?How Are We Doing?

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

Source: Minnesota Energy Assistance Program (eHEAT)

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 15

Allowable ActivitiesAllowable Activities EAP-related outreach, referral and advocacy A16 does not fund all of an SP’s outreach, referral and advocacy

activities A16 is EAP money for EAP activities

Allowable Expenditures The direct preparation, performance and recording of EAP outreach,

EAP referral and EAP advocacy activities can be charged to A16, including the related portion of fringe benefits earned

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 16

Examples of Activities & Information Chargeable to A16 Examples of Activities & Information Chargeable to A16 Staff time for an EAP staff person making a referral to Head Start Needs assessment counseling for EAP households Working with energy vendors on behalf of a household EAP outreach materials and activities Other EAP public relations measures and activities Postage to mail A16 materials and information Non-EAP outreach workers’ travel time, mileage and time assisting

with EAP application during home visits

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 17

A16 Case Management ActivitiesA16 Case Management Activities Encouraging households to sign up for CWR protection, where

applicable Helping households identify a reasonable payment amount for

their budgets Helping households negotiate a reasonable payment

agreement with energy vendors

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 18

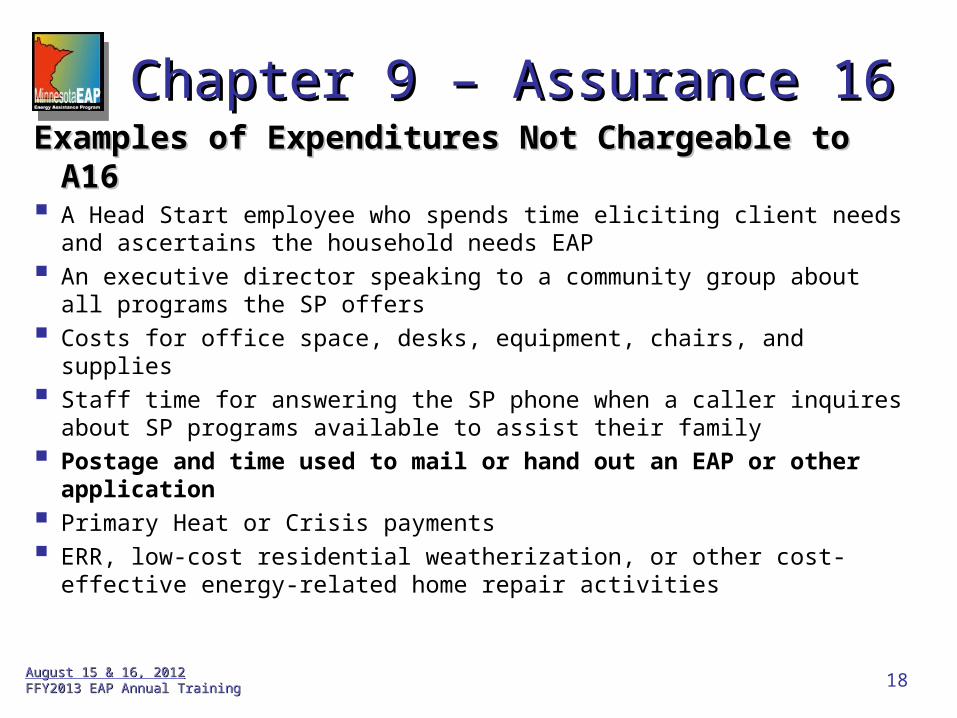

Examples of Expenditures Not Chargeable to A16Examples of Expenditures Not Chargeable to A16 A Head Start employee who spends time eliciting client needs and

ascertains the household needs EAP An executive director speaking to a community group about all programs

the SP offers Costs for office space, desks, equipment, chairs, and supplies Staff time for answering the SP phone when a caller inquires about SP

programs available to assist their family Postage and time used to mail or hand out an EAP or other application Primary Heat or Crisis payments ERR, low-cost residential weatherization, or other cost-effective energy-

related home repair activities

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 19

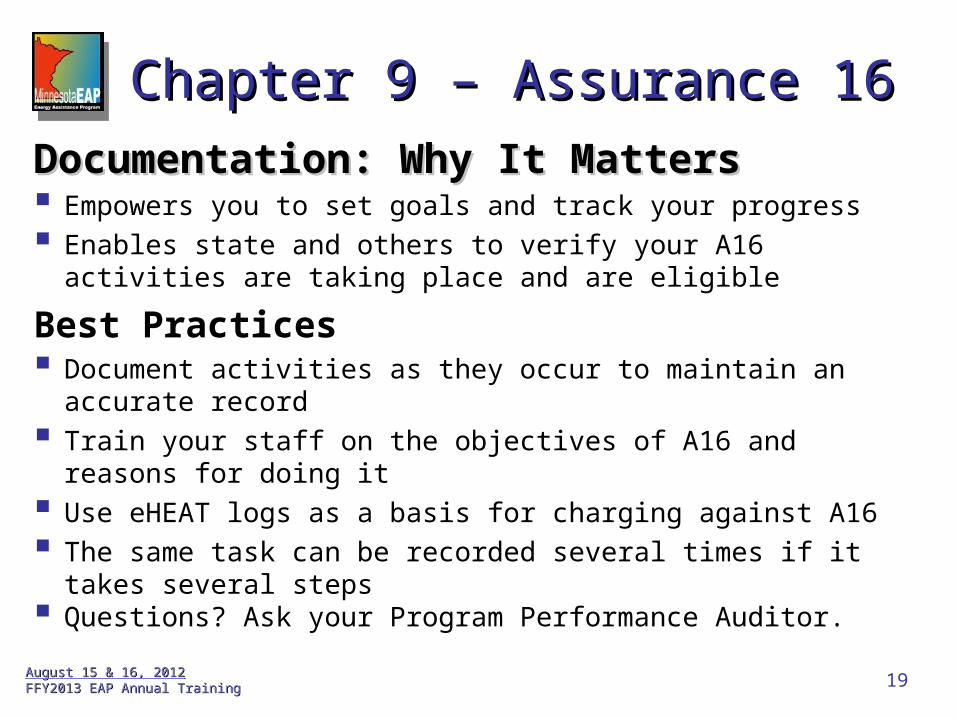

Documentation: Why It MattersDocumentation: Why It Matters Empowers you to set goals and track your progress Enables state and others to verify your A16 activities are taking place

and are eligible

Best Practices Document activities as they occur to maintain an accurate record Train your staff on the objectives of A16 and reasons for doing it Use eHEAT logs as a basis for charging against A16 The same task can be recorded several times if it takes several steps Questions? Ask your Program Performance Auditor.

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 20

Documentation:Documentation: Best Practices Best Practices (Continued) Enter enough detail in the eHEAT notes field to differentiate A16 from

Admin activities Notes Examples: Who, What, Where, When, How

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

Do Don’t10/21/12 -Mailed 300 applications to Seniors Inc. MS

Mailed applications.

12/23/12 - Advocated with Xcel to help household obtain CWR protection - MS

Advocated with energy vendor.

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 21

Q&AQ&A

Chapter 9 – Assurance 16 Chapter 9 – Assurance 16

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 22

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 23

Manual ChangesManual ChangesProperty Management RequirementsRecord Retention Requirements

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 24

Property Management RequirementsProperty Management RequirementsChanges in Property Management are based on

current federal and state requirements Impetus is concern safeguarding sensitive data and

increasingly scarce resources Let the appropriate people in your agency know

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 25

Property Management RequirementsProperty Management RequirementsEquipmentService Providers must follow the standards found in OMB Circulars A-110 Attachment N. Property Management Standards and Attachment O. Procurement Standards; A-102 Common Rule Section .31 Real Property, .32 Equipment and .36 Procurement as applicable.

In addition, the following policies regarding sensitive equipment apply.

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 26

Sensitive EquipmentSensitive EquipmentSensitive Equipment means tangible, nonexpendable, personal

property having a useful life of more than one year that is generally for individual use; could easily be sold or subject to pilferage or misuse; or could be used to store sensitive personal information

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 27

Sensitive EquipmentSensitive Equipment Examples include:

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

Personal computers (PCs - both desktop and portable models)

Televisions and other video equipment

Network servers Projectors

Cellular phones Cameras

Personal digital assistants (PDAs) Tape recorders

Printers Facsimile machines

Other PC accessories that are detachable from the PC (flash drives, modems, external disk drives, tape backup systems, scanners)

Pager

Wireless technology

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 28

Property Management RequirementsProperty Management RequirementsProcedures for managing equipment will meet the following requirements: Property records must be maintained A physical inventory of the property must be taken and the results

reconciled with the property records at least once every year Procedures must be in place to:

Prevent loss, damage, or theft of the property Keep the property in good condition Ensure the highest possible return if the property must be sold

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 29

Inventory RequirementsInventory Requirements Individual pieces of EAP-funded sensitive equipment must remain recorded in the Service

Provider’s inventory records while retained in the Service Provider’s possession for the reasonable estimated life of the respective item

See the table below for the estimated useful life of possible EAP-related sensitive equipment

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

Description Estimated Useful Life (Years)Audio/Visual Equipment 5Computer 5Computer Peripheral 8Copy Machine 5Electronic Equipment 10Office Machine 5Photography Equipment 8Printing/Laminating Equipment 10Telecommunications Equipment 10

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 30

Equipment Disposal or TransferEquipment Disposal or Transfer In addition to equipment with a value of $5,000 or greater,

DOC must approve disposal of sensitive equipment SPs must ensure and certify that any information retained in

the equipment that is subject to data practices requirements is completely removed prior to disposition Removal must be done by overwriting the data Equipment capable of holding sensitive data must be

overwritten at least 6 times before their disposal or transfer will be approved

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 31

Record RetentionRecord Retention Service Providers are required to maintain copies of all books, records,

documents, and accounting procedures and practices relevant to EAP for a minimum of six years

Previously, the contract erroneously indicated three years Contract language:

“Under Minn. Stat. § 16C.05, subd. 5, the Grantee’s books, records, documents, and accounting procedures and practices of the Grantee or other party relevant to this grant agreement or transaction are subject to examination by the State and/or the State Auditor or Legislative Auditor, as appropriate, for a minimum of six years from the end of this grant agreement, receipt and approval of all final reports, or the required period of time to satisfy all state and program retention requirements, whichever is later.”

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 32

Q&AQ&A

Ch. 16–Fiscal Management Ch. 16–Fiscal Management

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 33

FFY2013 EAP Local PlanFFY2013 EAP Local Plan

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 34

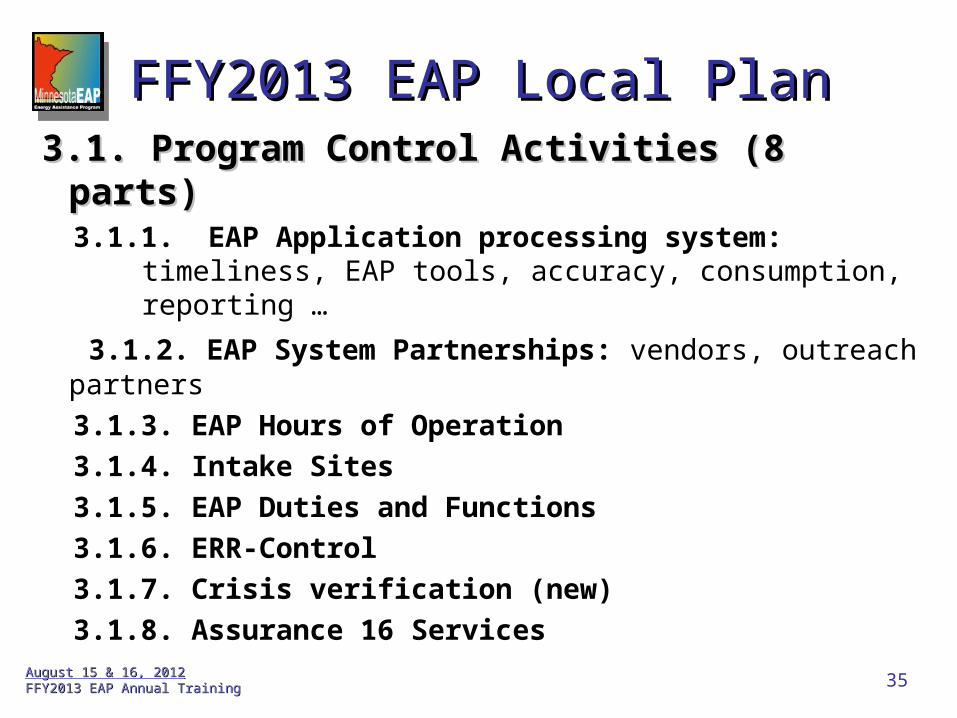

3. Control Activities 3. Control Activities 3.1. Program Control Activities

3.2. Control Activities – Fiscal

2013 Updates3.1.6. ERR-Control questions are improved

3.1.7. Crisis verification is added

FFY2013 EAP Local PlanFFY2013 EAP Local Plan

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 35

3.1. Program Control Activities (8 parts)3.1. Program Control Activities (8 parts)3.1.1. EAP Application processing system: timeliness, EAP

tools, accuracy, consumption, reporting …

3.1.2. EAP System Partnerships: vendors, outreach partners 3.1.3. EAP Hours of Operation

3.1.4. Intake Sites

3.1.5. EAP Duties and Functions

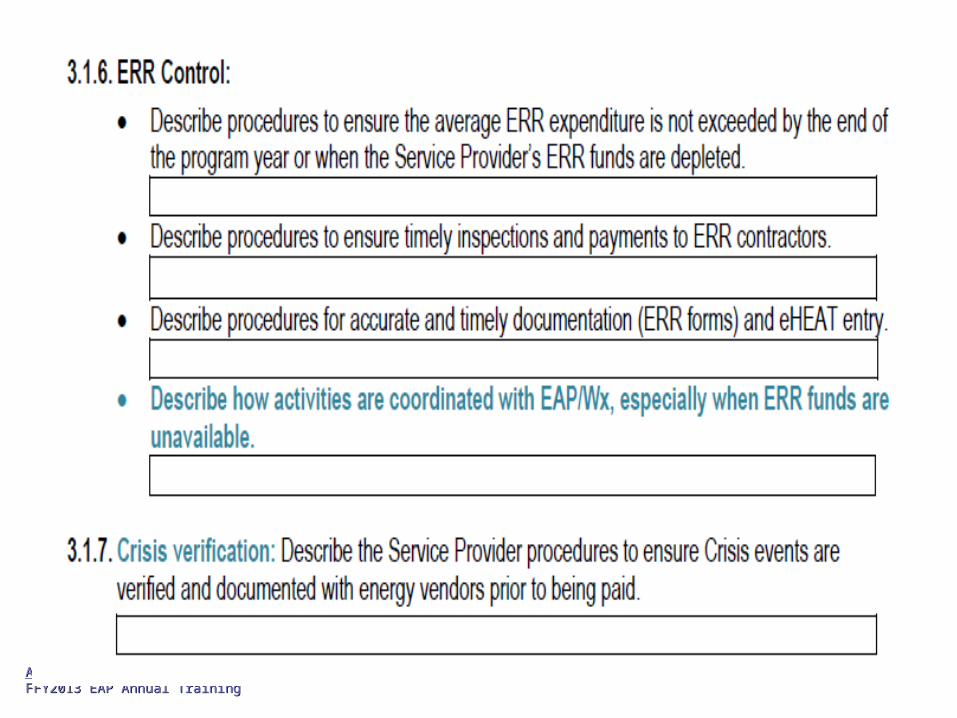

3.1.6. ERR-Control

3.1.7. Crisis verification (new)

3.1.8. Assurance 16 Services

FFY2013 EAP Local PlanFFY2013 EAP Local Plan

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 36

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 37

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 387

1

2

2

2

5

5

2 1

2

2

2 4

1

1

1

1

2

2

1 1

1

1

2

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 39

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 40

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 41

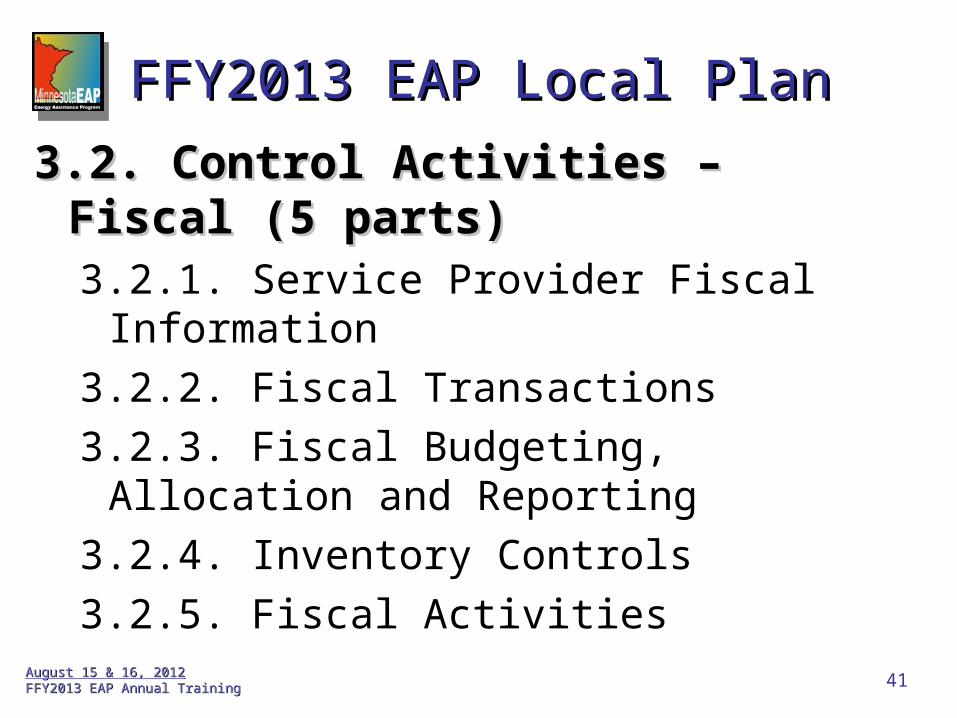

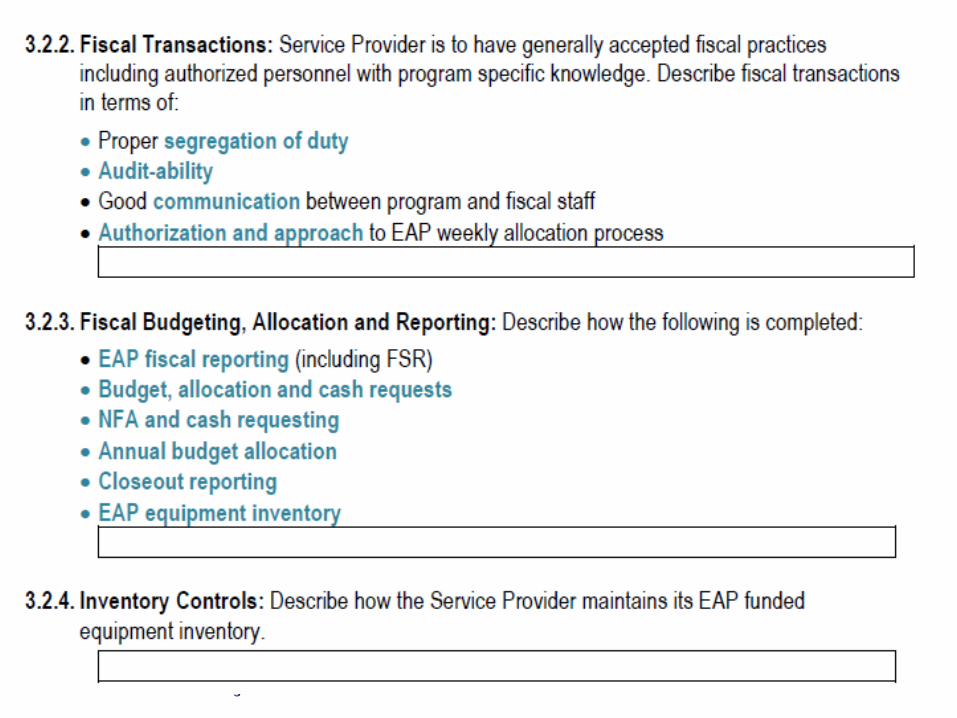

3.2. Control Activities – Fiscal (5 parts)3.2. Control Activities – Fiscal (5 parts)3.2.1. Service Provider Fiscal Information3.2.2. Fiscal Transactions3.2.3. Fiscal Budgeting, Allocation and Reporting 3.2.4. Inventory Controls3.2.5. Fiscal Activities

FFY2013 EAP Local PlanFFY2013 EAP Local Plan

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 42

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 43

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 44

Q&AQ&A

FFY2013 EAP Local PlanFFY2013 EAP Local Plan

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 45

Chapter 12 Incidents & Appeals Chapter 12 Incidents & Appeals

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 46

HighlightsHighlightsContextPolicies and procedures

Expanded types of incidents New overpayment policies and recovery processes Revised appendices

Reminders and areas for improvement

Chapter 12 Chapter 12 IncidentsIncidents && Appeals Appeals

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 47

FFY12 chapter was improved and reorganizedNumerous corrections required this yearOffice of the Legislative Auditor Limited funds increases pressure for:

Accuracy of benefits Full recovery of overpayments

Chapter 12 Chapter 12 ContextContext

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 48

Types of IncidentsTypes of IncidentsEvent NotificationsData Security and BreachesErrorsWaste (new)Abuse (new)Suspected FraudDisasters and Emergencies

Chapter 12 Chapter 12 IncidentsIncidents

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 49

DefinitionsDefinitionsError (redefined)Unintentional misuse of program funds Unintentional mistakes in the handling and processing

of application information Isolated and affects one or just a few households If an unintentional mistake affects more households

follow waste procedures

Chapter 12 Chapter 12 DefinitionsDefinitions

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 50

Definitions Definitions (continued)Waste Waste occurs as the result of resources being consumed by

inefficient or non-essential activities, including systemic errors or misapplication of policy

Abuse Abuse occurs as the result of purposeful departure of policies

and procedures where resources are improperly usedImpacts HHs, integrity of funds, reputation and scarce resources

Chapter 12 Chapter 12 DefinitionsDefinitions

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 51

Overpayment PoliciesOverpayment Policies Section dedicated to overpayments Benefit fix required when a benefit changes by $10 or greater SPs must track HHs with overpayments Mail HH payments to DOC within 1 business day of receipt Until an overpayment process is complete, the HH is not

eligible to receive Crisis benefits A need for different recovery processes for each type

Chapter 12 Chapter 12 OverpaymentsOverpayments

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 52

Error - Overpayment RecoveryError - Overpayment Recovery1. If identified immediately, work with the energy vendor to

determine if incorrect payment can be easily refunded2. Recover credit on energy vendor account, if possible3. Write to HH:

a) Notify them of the situationb) Request repayment of overpaid EAP funds not recoveredc) Clarify the HH’s rights and responsibilities, hardship option, and

appeal processd) Offer to meet with theme) Set up a repayment schedule as needed ensuring that full repayment

is made by September 30 of the current program year

Chapter 12 Chapter 12 RecoveryRecovery

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 53

Error - Overpayment RecoveryError - Overpayment Recovery4. If repayment poses a hardship for the household:

a) Obtain a written, signed and dated declaration from the household describing the hardship

b) Retain the declaration in the household’s filec) Terminate recovery of EAP funds

5. The DOC reserves the right to take additional steps

Chapter 12 Chapter 12 RecoveryRecovery

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 54

Waste and Abuse - Overpayment RecoveryWaste and Abuse - Overpayment RecoveryService Providers must report waste or abuse of

program funds to the DOCDOC reviews and determines actions

Service Providers could be subject to repayment with non-federal funds

Energy vendors or contractors could be subject to repayment and determined uncooperative

The DOC reserves the right to take additional steps

Chapter 12 Chapter 12 RecoveryRecovery

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 55

Suspected Fraud - Overpayment RecoverySuspected Fraud - Overpayment Recovery Follow investigation procedures All cases must be reported to the DOC and proper

local authorities eHEAT notes fieldDifferent recovery process depending on the party

suspected of fraud

Chapter 12 Chapter 12 RecoveryRecovery

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 56

HouseholdHousehold Suspected Fraud - Overpayment Recovery Suspected Fraud - Overpayment Recovery

1. If identified immediately, work with the energy vendor to determine if incorrect payment can be easily refunded

2. Recover credit on energy vendor account, if possible3. Write to HH:

a) Notify them of the situationb) Request repayment of overpaid EAP funds not recoveredc) Clarify the HH’s rights and responsibilities and appeal processd) Offer to meet with theme) Set up a repayment schedule as needed ensuring that full repayment

is made by September 30 of the current program year

Chapter 12 Chapter 12 RecoveryRecovery

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 57

HouseholdHousehold Suspected Fraud - Overpayment Recovery Suspected Fraud - Overpayment Recovery

4. The DOC reserves the right to deny a household suspected of fraud for the current program year and require all EAPbenefits be repaid

Chapter 12 Chapter 12 RecoveryRecovery

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 58

SPSP Suspected Fraud - Overpayment Recovery Suspected Fraud - Overpayment Recovery

SPs suspected of fraud are reviewed by the DOC The DOC determines actions including repayment with

non-federal funds The DOC reserves the right to take additional steps

Chapter 12 Chapter 12 RecoveryRecovery

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 59

EVEV Suspected Fraud - Overpayment Recovery Suspected Fraud - Overpayment Recovery

Energy vendors or contractors suspected of fraud are reviewed by the DOC The DOC determines actions that could include repayment

and be determined uncooperative The DOC reserves the right to take additional steps

Chapter 12 Chapter 12 RecoveryRecovery

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 60

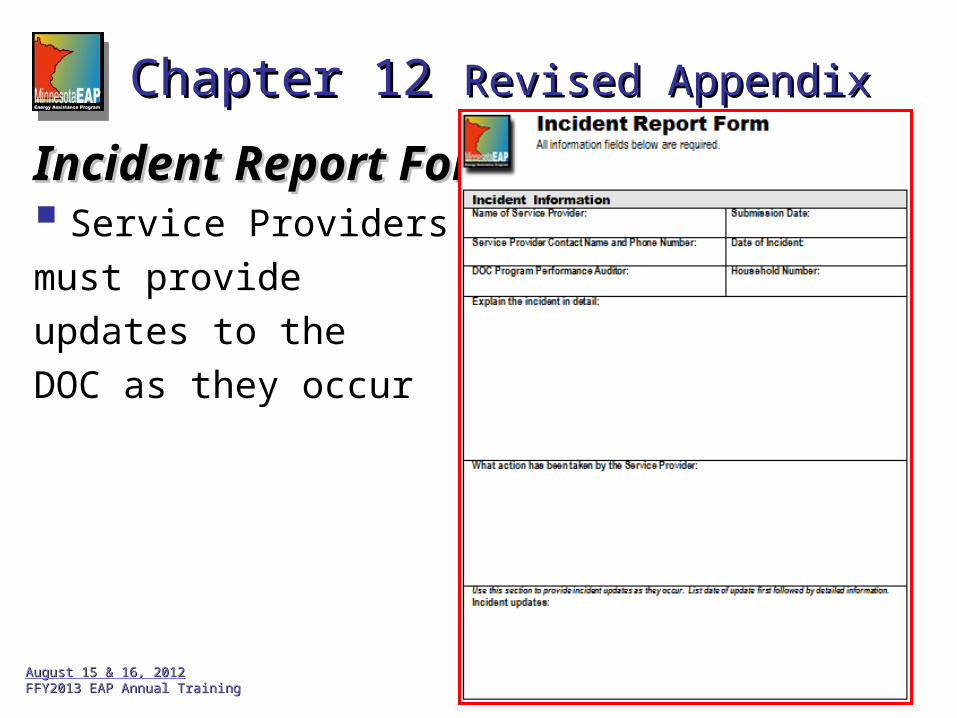

Incident Report FormIncident Report Form Service Providers must provide updates to the DOC as they occur

Chapter 12 Chapter 12 Revised AppendixRevised Appendix

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 61

Chapter 12 Chapter 12 Revised AppendixRevised Appendix

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 62

Reminders and Areas for ImprovementReminders and Areas for Improvement Appeal letter

Crucial timelines in manual Thorough review of household file Respond to each concern the HH indicated in their letter Reference EAP policies Explain their right to appeal to the next level Second reviewer for accuracy Certified mail

Chapter 12 Chapter 12 RemindersReminders

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 63

Reminders and Areas for ImprovementReminders and Areas for Improvement Documentation

eHEAT notes field Household file Appeals tracking sheet

Track overpayments Overpayment process must be complete before HH Crisis

Update DOC Follow policy and recovery processes Ask DOC

Chapter 12 Chapter 12 RemindersReminders

August 15 & 16, 2012August 15 & 16, 2012FFY2013 EAP Annual TrainingFFY2013 EAP Annual Training 64

Q&AQ&A

Chapter 12 Incidents & Appeals Chapter 12 Incidents & Appeals