auditing of a marketing department- capstone

TRANSCRIPT

http://www.voki.com/presenter/playPresentation.php?id=8466a2b43729c29dcd7cc0fdfa1a9e7a

Definition of AuditingThe Institute of Internal Auditors (IIA) defines “an independent, objective

assurance and consulting activity designed to add value and improve an

organizations operation. It helps an organization accomplish its objectives by

bringing a systematic, disciplined approach to evaluate and improve the effectiveness

of risk management, control, and governance processes” (Hirth, 2010, 2).

Benefits

Auditing has been perceived and has been that “life saver” for a myriad of organizations by “discovering deviations from accepted standards and instances of illegality, inefficiency, irregularly, ineffectiveness, and “discontents that draw our attention to things that simulation leaves out” (Turkle 2009, 5).

“Internal auditing can more effectively assess the business, identify areas for improvement, and contribute to managing business risk” (Azam, 2011, 44).

Why Marketing Examining a company’s functional department helps determine the risk and threats a little

faster than examining the whole organization.

The marketing department of any organization holds the key to a lot of the business outcomes, such as sales, profit, customer satisfaction, and customer awareness. Bradley (1995) agrees that “the marketing function permeates the entire organization and includes all the activities which affect current and future buyer behavior of customers” (16).

The Internal audit of the marketing department is considered a high risk due to the demanding functions that this department has on the overall result of the company.

Garrison, Noreen, & Brewer (2011) said “if the risks are not managed effectively, they can infringe on a company’s ability to meet its goals” (20).

According to the American Marketing Association (2011) marketing is defined as “the process of planning and executing the conception, pricing, promotion and distribution of ideas, goods and services to create exchange and satisfy individual and organizational objectives”.

Effects of the 5 PP’s Price.

“Pricing is one of the most difficult areas in marketing, since both strategic and tactical aspects must be considered. Customers may relate price and quality: the higher the price, the higher the perceived quality. In such circumstances, if the product design is better than the average available, raising the price may increase sales” (Garrison, 2010, 91).

Profit.

Prices affects profit, Chonko (1995) agrees that “one of the major problems associated with pricing is the pressure for profits” (208). Profits affects not only the organization but the shareholders as well, “the seller is in business to make a profit because profits are what keep organizations producing products into the future” (Chonko, 1995, 206).

Product.

“Product planning means selecting what to provide and sell, and how to match products and services with the needs of the market. By concentrating on the product alone, it is not easy to gain a sustainable competitive advantage in the market, since most products can be imitated relatively easily” (Garrison, 2010, 90).

Effects of the 5 PP’s Promotion.

“Promotion is a collection of methods by which the organization may inform its customers of what is offered” (Bradley, 1995, 91). Promotion is important, its main job is to persuade the customers to buy the organization’s products, the hardest part of this marketing mix is “matching the medium with the audience” (Bradley, 1995).

Place.

Place was not audited in this particular research study reason being it was located unknown and simulated business.

Audit Results

Markup Percentage of Baker

Study was based on Study was based on TraditionalTraditional andand Low End Low End SegmentsSegments

Low EndLow End

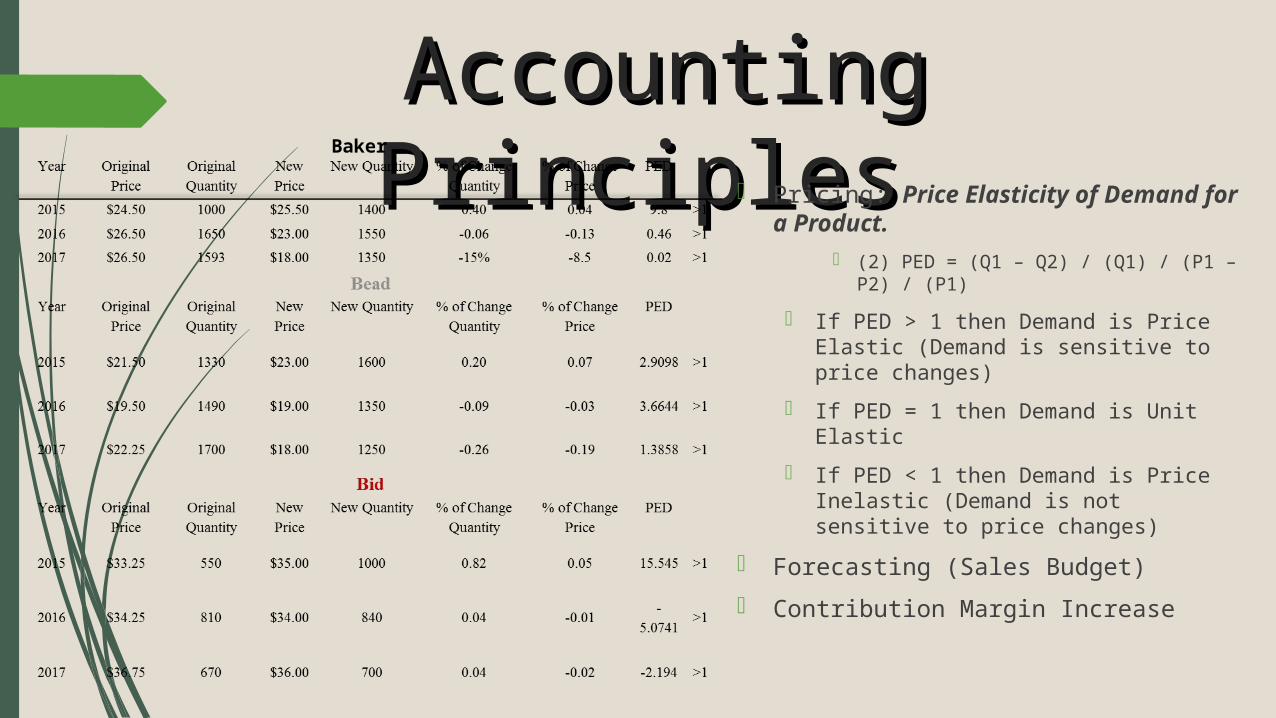

Accounting Principles Accounting Principles Pricing: Price Elasticity of Demand for a

Product. (2) PED = (Q1 – Q2) / (Q1) / (P1 – P2) / (P1)

If PED > 1 then Demand is Price Elastic (Demand is sensitive to price changes)

If PED = 1 then Demand is Unit Elastic

If PED < 1 then Demand is Price Inelastic (Demand is not sensitive to price changes)

Forecasting (Sales Budget)

Contribution Margin Increase

Baker

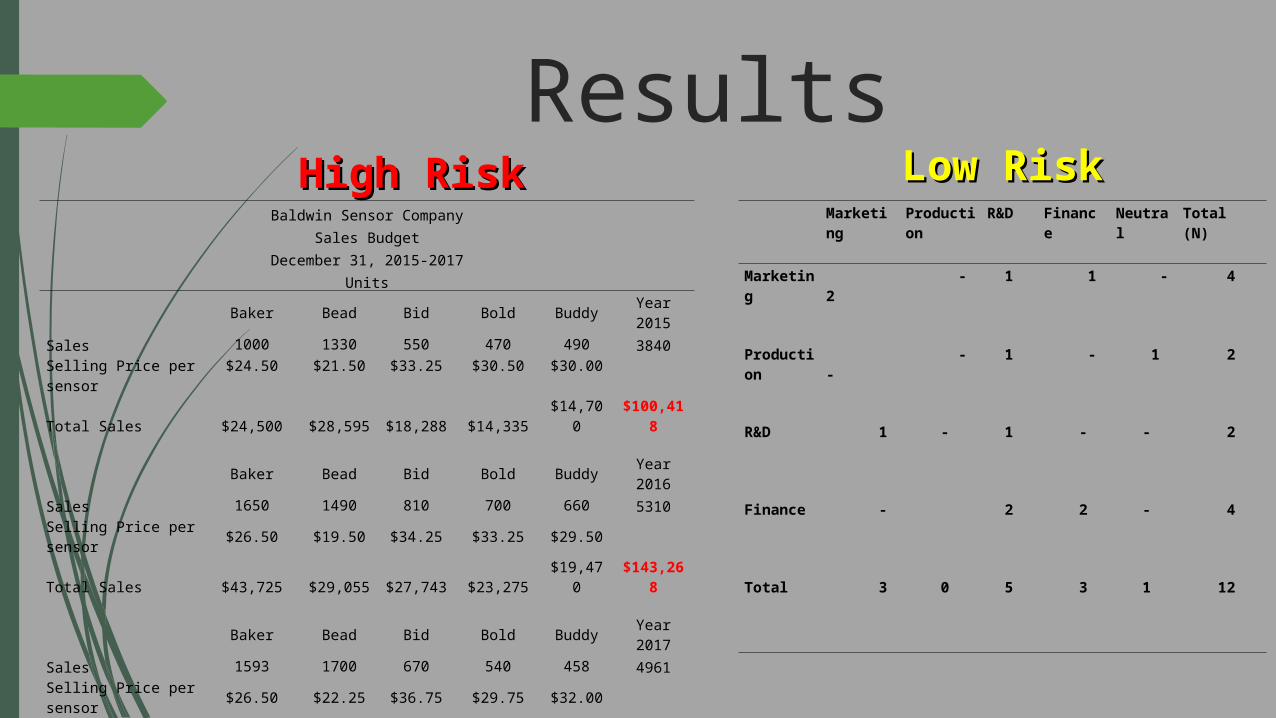

ResultsHigh RiskHigh Risk

Baldwin Sensor Company

Sales Budget

December 31, 2015-2017

Units

Baker Bead Bid Bold Buddy Year 2015

Sales 1000 1330 550 470 490 3840

Selling Price per sensor $24.50 $21.50 $33.25 $30.50 $30.00

Total Sales $24,500 $28,595 $18,288 $14,335 $14,700 $100,418

Baker Bead Bid Bold Buddy Year 2016

Sales 1650 1490 810 700 660 5310

Selling Price per sensor $26.50 $19.50 $34.25 $33.25 $29.50

Total Sales $43,725 $29,055 $27,743 $23,275 $19,470 $143,268

Baker Bead Bid Bold Buddy Year 2017

Sales 1593 1700 670 540 458 4961

Selling Price per sensor $26.50 $22.25 $36.75 $29.75 $32.00

Total Sales $42,215 $37,825 $24,623 $16,065 $14,656 $135,383

Actual Budget Variance Variance%

Sales Year 2015 $100,187.00 $100,418 -$231 -0.23%

Sales Year 2016 $125,410.00 $143,268 -$17,858 -12.46%

Sales Year 2017 $92,184.00 $135,383 -$43,199 -31.91%

Low RiskLow Risk Marketing Production R&D Finance Neutral Total (N)

Marketing 2 - 1 1 - 4

Production - - 1 - 1 2

R&D 1 - 1 - - 2

Finance - 2 2 - 4

Total 3 0 5 3 1 12

Sales Budget Model

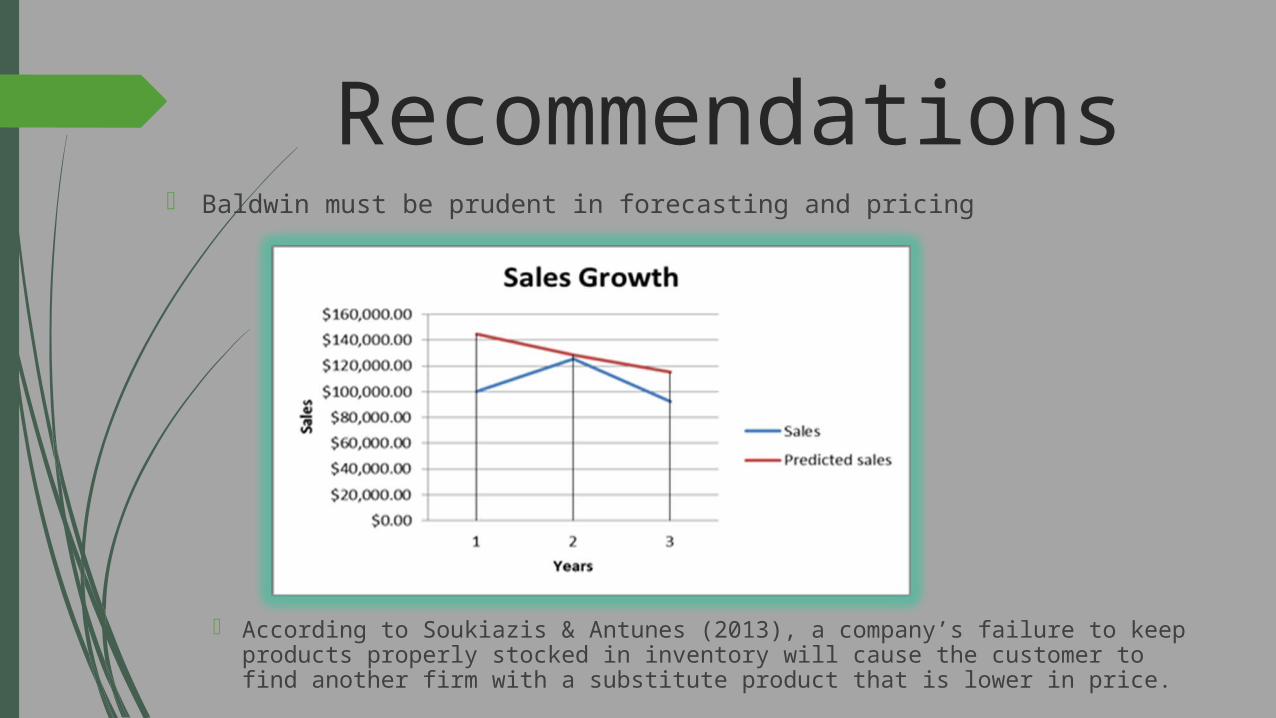

Recommendations Baldwin must be prudent in forecasting and pricing

According to Soukiazis & Antunes (2013), a company’s failure to keep products properly stocked in inventory will cause the customer to find another firm with a substitute product that is lower in price.

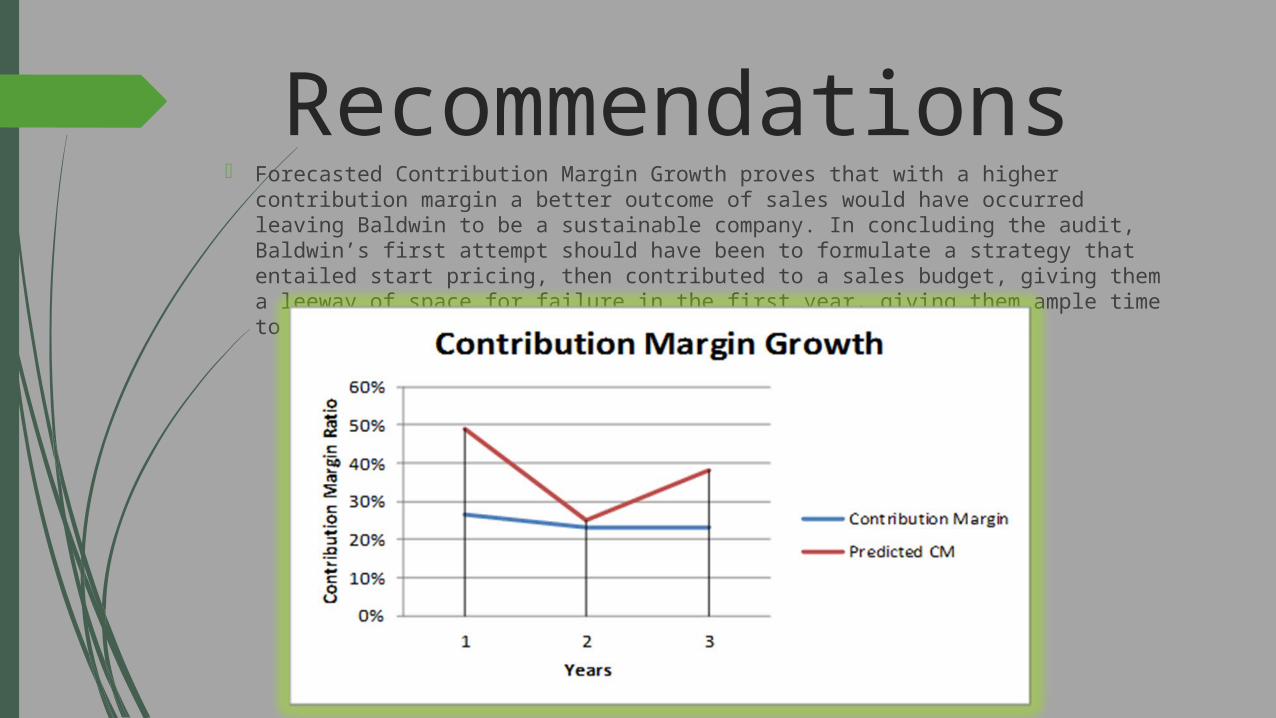

Recommendations Forecasted Contribution Margin Growth proves that with a higher contribution margin a better outcome of

sales would have occurred leaving Baldwin to be a sustainable company. In concluding the audit, Baldwin’s first attempt should have been to formulate a strategy that entailed start pricing, then contributed to a sales budget, giving them a leeway of space for failure in the first year, giving them ample time to secure a close knit with their customer’s wants and needs.

Referen

cesR

eferences

American Marketing Association. (2011). AMA Board approves new marketing

definition. Marketing News. P.5.

Azam, A. (2011). A sharper FOCUS. Internal Auditor, 68(1), 41-45.

Bradley, F. (1995). Marketing management: providing, communicating and delivering

value. Prentice Hall. (16-308).

CAPSIM Simulation. (2014). Team Member Guide. Retrieved on November 5, 2013 from

http://www.capsim.com/guides/capstone2013/the-guide/4-managing-your-company/43-productionf0e5.html

Chonko, L. (1995). Ethical decision making in marketing. Sage Publication. (11-206).

Garrison, R. H., Noreen, E. W., & Brewer, P. C. (2012). Managerial Accounting. 14th Edition.

McGraw-Hill/Irwin. New York, NY

Hirth, B. R. (2010). Internal auditing is an asset for small companies as well as large ones.

Protiviti: Risk & Business Consulting Internal Auditing. pp. 1-5.

Turkle, S. (2009). Simulation and its discontents. The MIT Press Cambridge, Ma pp. 5-6.

Soukiazis, E., & Antunes, M. (2013).The Effects of Internal and External Imbalances on Italy´s Economic Growth. A Balance of Payments Approach with Relative Prices No Neutral

QUESTIONSQUESTIONS